tools spotlight

-

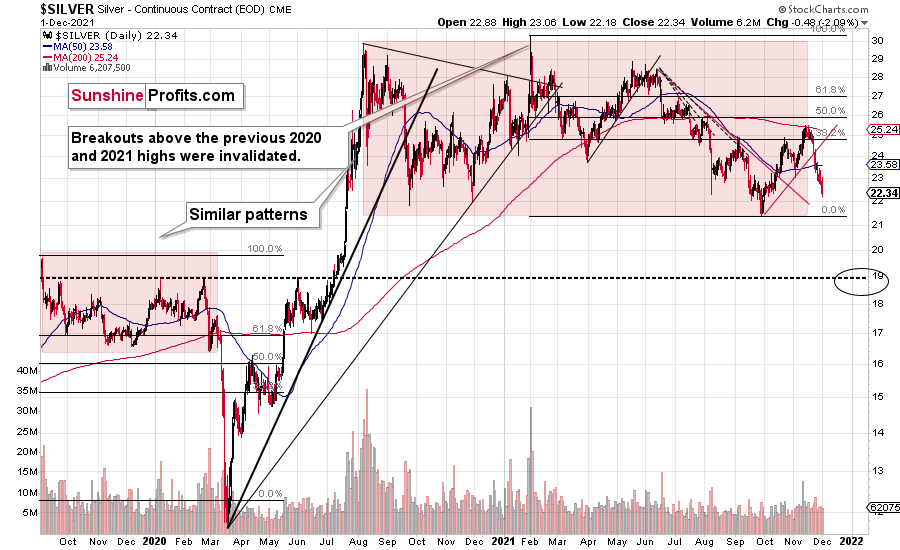

Gold: Ladies and Gentlemen, We Have a Breakdown!

December 2, 2021, 7:21 AMAfter the miners' recent confirmed breakdown, gold is also showing signs of the same. Silver ain’t doing better.

Breakdowns are important. Confirmed breakdowns are even more so.

Mining stocks confirmed their breakdown recently, so they were likely to fall. And they just did. The situation has developed in tune with my previous expectations. In yesterday’s analysis, I wrote the following:

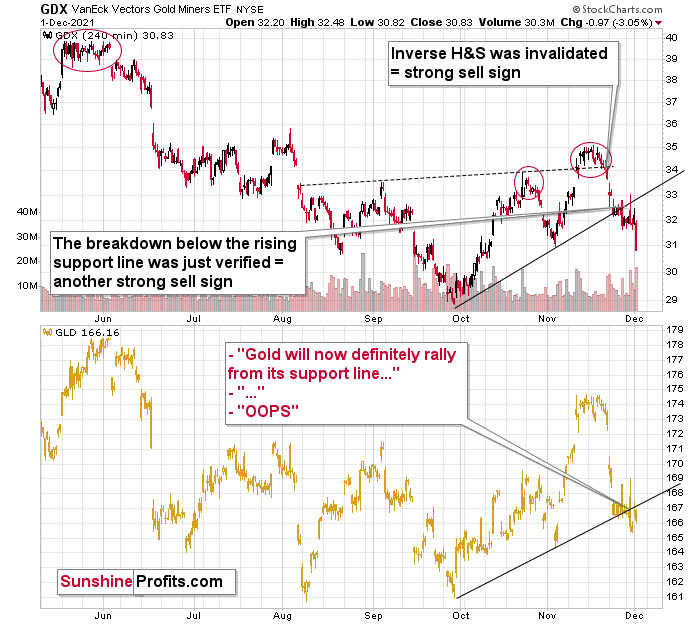

The upper part of the chart features the GDX ETF (proxy for gold mining stocks), and the lower part thereof features the GLD ETF (proxy for gold price itself.)

First of all, gold stocks were first to break below their rising support line – that happened a couple of days ago. Gold moved decisively below its rising support line only yesterday. This emphasizes that gold stocks are leading gold lower. This, in turn, is a bearish confirmation in itself, as that’s what tends to happen at the beginning of a bigger move lower.

The way both markets performed yesterday was also quite interesting.

In case of mining stocks, the intraday rally took GDX just slightly above its rising support line and then miners moved back down in a flash. In other words, if anyone had exited their short positions in order to re-enter them at higher prices, they had very little time to do so, and the most realistic version of this scenario is that they ended the session while missing the 1% decline in the GDX. The silver price was down by just 4 cents, but still, it was a move lower despite an intraday rally.

In the case of GLD, one might have thought that gold was bound to rally since it stopped at its rising support line (based on the Sep. and Nov. lows). And gold even rallied by about $20 intraday… Only to decline more and end yesterday’s session lower.

That was not a reversal. That was a bull trap.

And the most bearish thing about yesterday’s decline – and weakness? It happened while the USD Index moved lower during the day. The USDX ended the day 0.33 lower, which “should have” triggered gold’s rally. Instead, gold declined, proving that it really wants to move lower. And suggesting that profits from one’s short positions in mining stocks are likely to become bigger.

Don’t get me wrong – I do think that we’ll see a counter-trend upswing, but it’s just not that likely that we’ll see it right now. For quite some time, I’ve been repeating that it’s likely that we’ll see some kind of corrective upswing once gold moves back to its yearly lows, and this remains to be the case.

Then, after the rebound, gold is likely to decline once again, perhaps to its final lows (for many years to come).

The GDX ETF declined by 3.05% yesterday.

The GDXJ ETF declined by 3.77% yesterday, and I just received the following message from one of the people who were following my analyses: “MY BEST FINANCIAL DAY IN MY LIFE…AND I trust you enjoyed the same success!!!!!!!!!!!!!”

Indeed, I congratulate everyone who was able to patiently wait out the corrective upswing and is now benefitting from the decline. Of course, my congratulations extend also to those who were able to exit short positions earlier and re-enter them at higher prices – it seemed too risky in my view, but some of you might have been able to do it. Congratulations either way.

So, will we see a corrective upswing now? While that’s possible, it’s not imminent. One of the previous situations that’s similar to the current one is what we saw right before the mid-year top. I marked mid-year declines (from the start to the first more visible correction) in both charts: GDX and GDXJ with orange rectangles. If the history repeats itself, both proxies for mining stocks could move back to their previous 2021 lows before correcting.

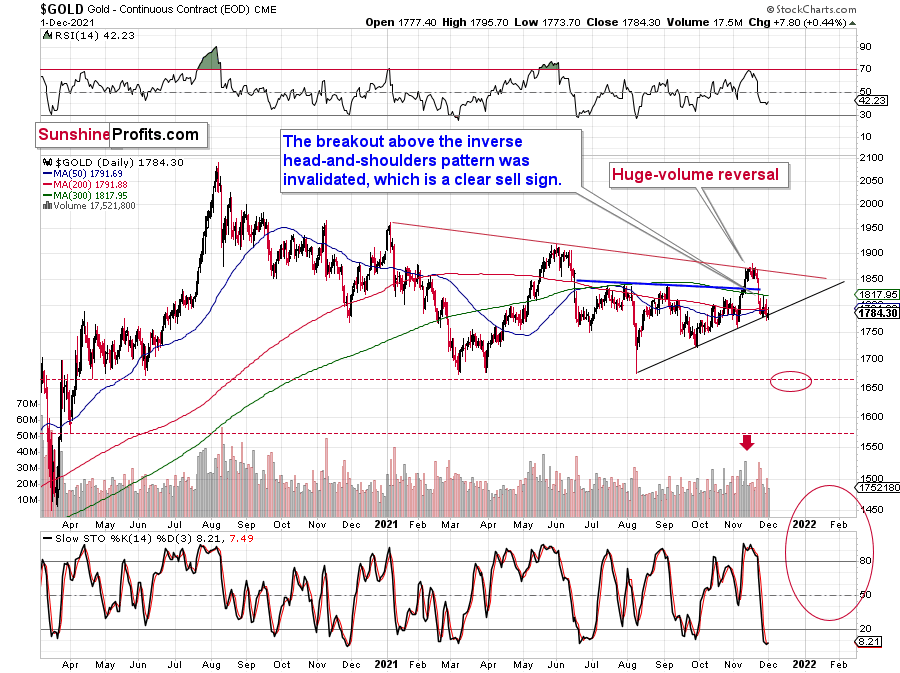

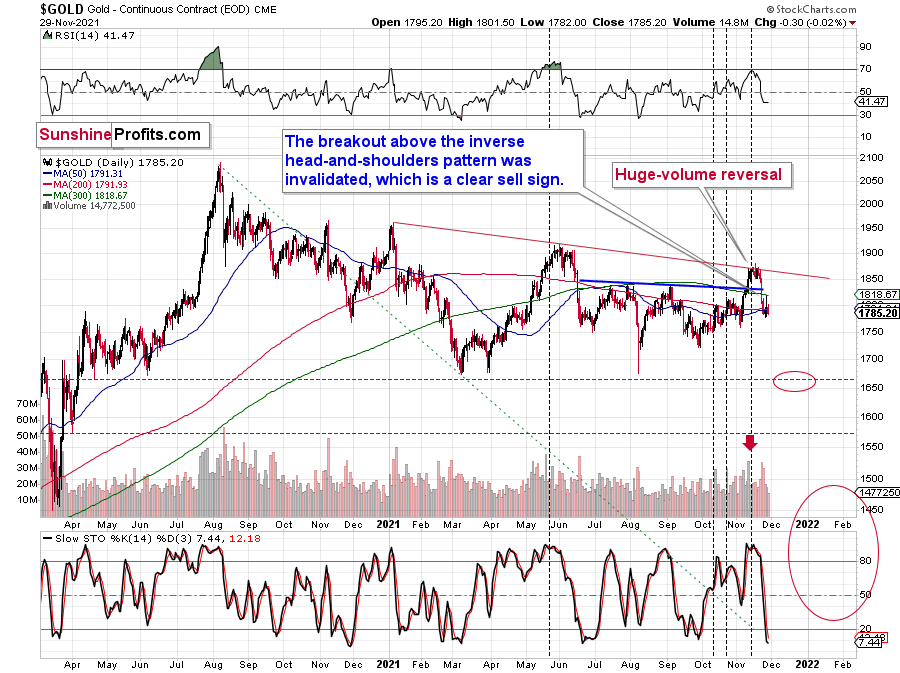

There’s also an additional (and actually, the foremost) reason to expect decline’s continuation. Today’s pre-market breakdown in gold.

On the above chart it’s not clear if the gold price moved below the rising support line (marked with black) or not, but it is clear on the below chart that also features today’s pre-market trading (up to the moment when I saved the chart that is).

Ladies and gentlemen, we have a breakdown.

It’s not confirmed yet, but given how weak gold was recently – refusing to rally despite USD’s declines – it’s likely to be confirmed shortly.

Silver already declined as well, confirming the general direction of the entire sector:

While GDX declined by slightly more than 3%, GDXJ almost 4%, silver was down by about 2%. Compared to the previous decline silver declined more than miners, but not in percentage terms. Counting the percentages from the recent top (November intraday high to yesterday’s intraday low), GDX is down by 12.14%, silver is down by 12.99% and GDXJ is down by 15.17%. The GDXJ still declined the most – in perfect tune with my expectations.

Please note that in 2020, juniors and seniors both declined, but juniors declined more, and they even briefly moved below the price of the seniors (GDXJ moved below GDX for a very short while). If that was to happen once again (and it seems quite likely to me), then it means that junior miners have much greater downside potential – that’s why I’m focusing on shorting this part of the precious metals sector.

Having said that, let’s take a look at the situation from a more fundamental angle.

Time After Time

With the S&P 500 extending its Omicron freak out, battered bulls were left in disarray once again. And with the PMs no longer able to surf the general stock market’s bullish wave, reality has re-emerged once again.

To explain, I wrote on Nov. 11:

While the PMs may have won the recent battle, they’re unlikely to win the war. With inflation surging, markets rattled, The White House rattled and precious metals investors assuming that policymakers will do nothing (even as their anxiety accelerates), the calculus boils down to one fundamental question: do you believe the U.S. dollar or do you believe the PMs?

Please see below:

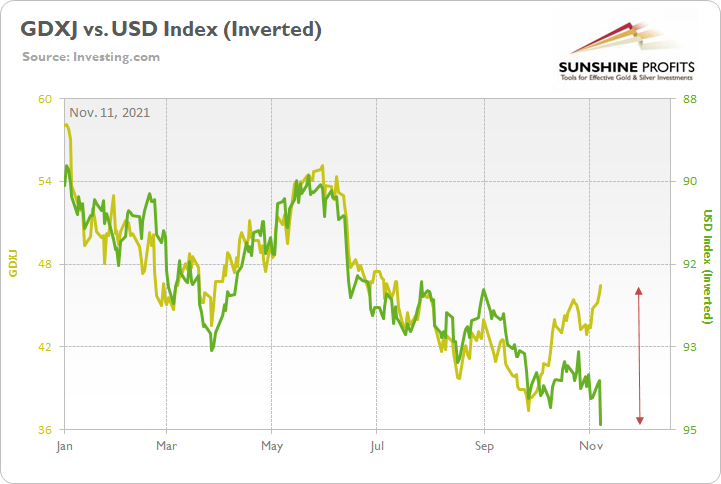

To explain, the gold line above tracks the GDXJ ETF (our short position) in 2021, while the green line above tracks the inverted (scale flipped upside down) USD Index. If you analyze the relationship, you can see that when the USD Index rises (the green line falls), the GDXJ ETF often heads in the opposite direction.

However, with the U.S. dollar betting that the Fed will tighten and the junior miners betting that it won’t, we expect the former to win out over the medium term.

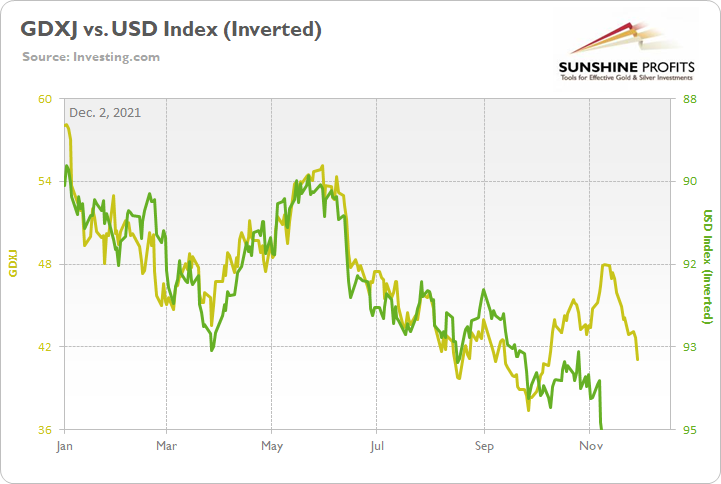

And now, with the USD Index continuing its ascent and the GDXJ ETF reversing sharply, the junior miners faltered in their attempt to run away from the USD Index.

Please see below:

To that point, with investors assuming that 1970s-style hyperinflation would occur with little pushback from policymakers, I warned on numerous occasions that the prospect was far-fetched. And while it may seem counterintuitive, surging inflation is actually bearish for the PMs. And why is that? Well, it’s because willing policymakers can control inflation. And when they perform hawkish shifts, the PMs often suffer mightily.

For context, I wrote on Nov. 12:

With the inflation narrative shifting from ‘no big deal’ to ‘out of control,’ investors had it wrong then, and they likely have it wrong now. Inflation is hot, no doubt about it. But the notion of 1970s-style hyperinflation is much more semblance than substance. The U.S. dollar is rallying (disinflationary), the taper is underway (disinflationary), U.S. Treasury yields are rallying (disinflationary) and the FOMC can raise interest rates without crashing the U.S. economy. As a result, the 2021 theme of ‘USD Index up, PMs down’ should resurface sooner rather than later.

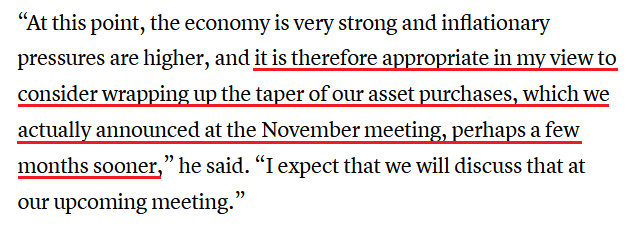

Furthermore, with Fed Chairman Jerome Powell validating the thesis on Nov. 30, the central bank chief essentially admitted that accelerating the pace of the taper is likely a done deal at the FOMC’s next policy meeting (Dec. 14/15). He said:

Source: CNBC

Source: CNBCOn top of that, Powell sounded pretty hawkish during his testimony on Dec. 1. He said:

“Policy has adapted to that and will continue to adapt. We’ve seen inflation be more persistent. We’ve seen the factors that are causing higher inflation to be more persistent….

“We have to balance those two goals [the labor market and inflation] when they are in tension, as they are right now," Powell said. “But I assure you we will use our tools to make sure that this high inflation we are experiencing does not become entrenched.”

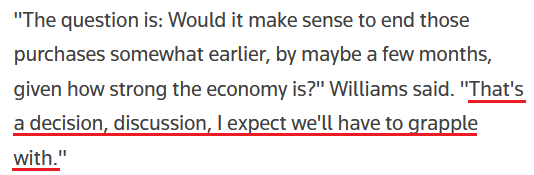

For context, it’s clear that Powell, Clarida, Waller and Bostic are all advocating for a faster taper. And now, even New York Fed President John Williams (a major dove) isn’t so sure of his surroundings. Moreover, while he remained evasive on further policy action, he said on Dec. 1:

Source: Reuters

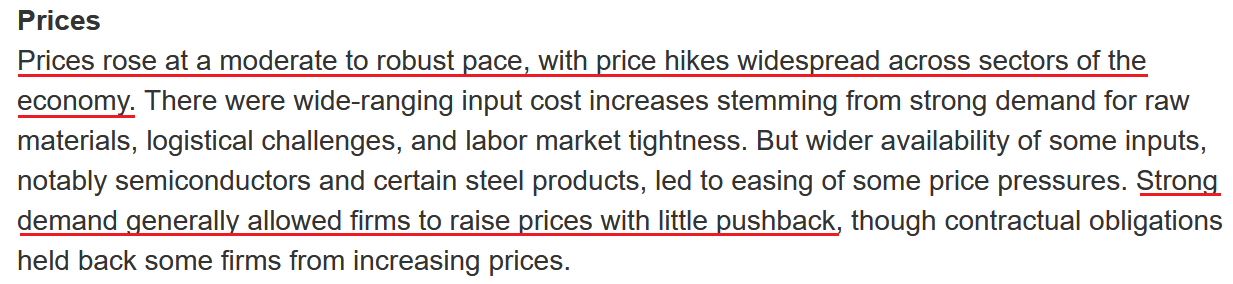

Source: ReutersAnd as all of the drama was unfolding, the Fed also released its latest Beige Book on Dec. 1. As it relates to wage inflation, the report revealed:

“Nearly all Districts reported robust wage growth. Hiring struggles and elevated turnover rates led businesses to raise wages and offer other incentives, such as bonuses and more flexible working arrangements.”

For context, Powell also expressed concerns about wage inflation on Dec. 1. He said:

"We have seen wages moving up significantly. We don’t see them moving up at a troubling rate that would tend to spark higher inflation, but that’s something we’re watching very carefully."

And as it relates to input and output inflation, the Beige Book revealed:

Source: U.S. Fed

Source: U.S. FedAlso highlighting Powell’s inflationary conundrum, the Institute for Supply Management (ISM) released its Manufacturing PMI on Dec. 1. And while its prices index decreased from 85.7 in October to 82.4 in November, the report revealed that “raw materials prices increased for the 18th consecutive month, at a slower rate in November” and that “all 18 industries reported paying increased prices.”

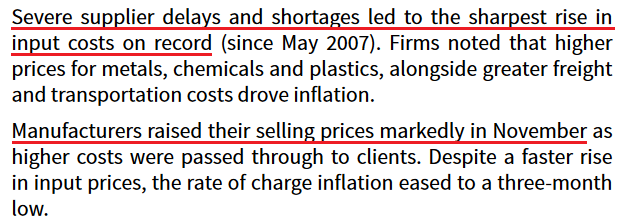

Likewise, IHS Markit’s Manufacturing PMI (also released on Dec. 1) had a similar message:

Source: IHS Markit

Source: IHS MarkitAlso noteworthy, the report was an ominous sign for stock market bulls. For example, demand destruction is already unfolding. If you’re unfamiliar with the term, it means that surging inflation cannot persist forever. Eventually, prices eclipse demand, and consumers stop purchasing the products.

Chris Williamson, Chief Business Economist at IHS Markit, said:

“While demand remains firm, November brought signs of new orders growth cooling to the lowest so far this year, linked to shortages limiting scope to boost sales and signs of push-back from customers as prices continued to rise sharply during the month.

While average selling price inflation eased as firms sought to win customers, the rate of input cost inflation hit a new high, hinting at a squeeze on margins.”

Finally, with inflation running hot and the Fed’s hawkish rhetoric poised to morph into hawkish policy in the comings months, the timing of Powell’s ‘come-to-Jesus’ moment is far from a surprise. To explain, when inflation becomes political, the performance of the PMs, the stock market, or any other asset class becomes a secondary concern. At the forefront, the most important thing for U.S. President Joe Biden is to ensure his political survival.

And with headlines like the one below becoming more common (written by USA Today on Nov. 29), failure to calm the pricing pressures could derail his re-election odds. As a result, inflation is now a net-negative for Biden and Powell, and the USD Index should benefit materially from the upcoming battle.

The bottom line? Surging inflation is doing more harm than good to the U.S. economy, and Biden and Powell recognize this. And with higher precious metals prices mutually exclusive to their goals, the PMs are unlikely to celebrate what unfolds over the next few months.

To that point, I spent a lot of time analyzing the performance of the S&P Goldman Sachs Commodity Index (S&P GSCI). For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products and two precious metals.

More importantly, though, it’s inflation’s canary in the coal mine. And with the index declining by 11% in November, there was plenty of wreckage across the commodities complex. Moreover, with the drawdown coinciding with Powell’s recent hawkish rhetoric, more of the same will likely materialize over the medium term.

In conclusion, the PMs were mixed on Dec. 1, though, silver and mining stocks suffered painful contusions. And with Omicron and Powell helping to upend investor sentiment, the PMs face an ominous future. Moreover, while the USD Index takes a breather after its recent sprint higher, the greenback’s fundamentals remain robust. And with Biden and Powell indirectly boarding the U.S. dollar’s bullish train, the next stop is likely ~98.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Don’t Get Yourself Into a Bull Trap With Gold

December 1, 2021, 9:03 AMYou see a commodity going down, then it reverses and starts teasing you with an upward move… only to end up declining further. Is this the case now?

I started yesterday’s analysis with a question that I then replied to, explaining why I thought that it wasn’t necessarily a good idea take profits from one’s short positions at this time, as the corrective upswings could be nothing to write home about, and that it might not be that easy to get back in the short positions at better (higher) prices.

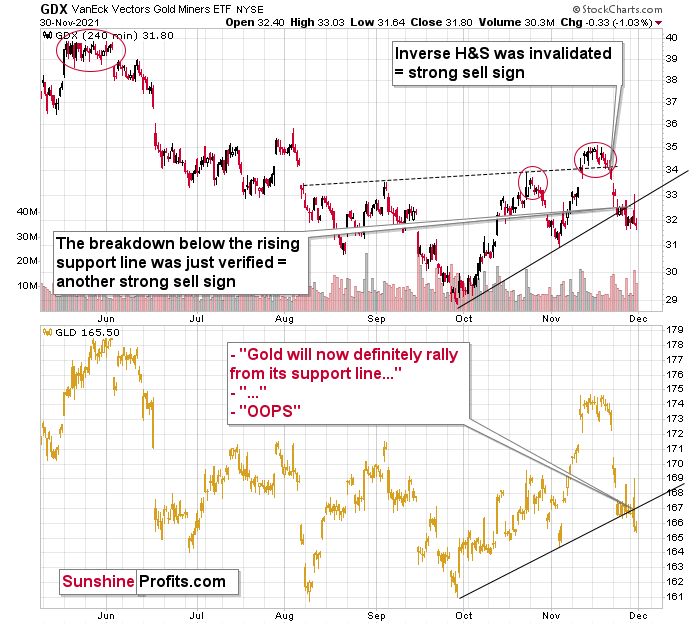

Well, yesterday’s session showed exactly what I meant, and the 4-hour chart found below provides the details.

The upper part of the chart features the GDX ETF (proxy for gold mining stocks), and the lower part thereof features the GLD ETF (proxy for gold price itself.)

First of all, gold stocks were first to break below their rising support line – that happened a couple of days ago. Gold moved decisively below its rising support line only yesterday. This emphasizes that gold stocks are leading gold lower. This, in turn, is a bearish confirmation in itself, as that’s what tends to happen at the beginning of a bigger move lower.

The way both markets performed yesterday was also quite interesting.

In case of mining stocks, the intraday rally took GDX just slightly above its rising support line and then miners moved back down in a flash. In other words, if anyone had exited their short positions in order to re-enter them at higher prices, they had very little time to do so, and the most realistic version of this scenario is that they ended the session while missing the 1% decline in the GDX. The silver price was down by just 4 cents, but still, it was a move lower despite an intraday rally.

In the case of GLD, one might have thought that gold was bound to rally since it stopped at its rising support line (based on the Sep. and Nov. lows). And gold even rallied by about $20 intraday… Only to decline more and end yesterday’s session lower.

That was not a reversal. That was a bull trap.

And the most bearish thing about yesterday’s decline – and weakness? It happened while the USD Index moved lower during the day. The USDX ended the day 0.33 lower, which “should have” triggered gold’s rally. Instead, gold declined, proving that it really wants to move lower. And suggesting that profits from one’s short positions in mining stocks are likely to become bigger.

Don’t get me wrong – I do think that we’ll see a counter-trend upswing, but it’s just not that likely that we’ll see it right now. For quite some time, I’ve been repeating that it’s likely that we’ll see some kind of corrective upswing once gold moves back to its yearly lows, and this remains to be the case.

Then, after the rebound, gold is likely to decline once again, perhaps to its final lows (for many years to come).

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

The Mother of All Stock Market Invalidations

November 30, 2021, 7:46 AMLet’s start today’s analysis with a question that I just received:

Now that gold, silver and the miners are oversold, what kind of a bounce do you expect? Why not take profits and re-short at a higher level?

Well, I’m fine with everyone using my opinions on the market in any way they see fit (as long as they are not viewed as “investment advice”, that is). This means that one is free to take profits now and re-open the short positions at higher levels after a rebound… that is, if a rebound does indeed take place and one is realistically able to get back in their short positions at higher prices.

The question starts with an assumption that gold, silver, and miners are oversold, and that I expect a bounce.

But are they indeed oversold?

The Stochastic Indicator based on gold (lower part of the above chart) moved below 20, so it is in the oversold territory, but the RSI (upper part of the chart) is slightly above 40, and only levels below 30 are viewed as oversold.

Is the Stochastic Indicator reliable enough to trigger a rebound on its own? Well, it might or might not be the case. In January 2021, the move below 20 in Stochastic triggered a small rally, and the same happened in late February, but the corrections were not very significant. In early March, when the indicator moved below 20, the decline still continued.

Gold’s price is slightly above the previous highs, and it’s trading close to its 50- and 200-day moving averages. That’s quite a normal performance.

Given that gold-based RSI recently touched the 70 level and then gold declined sharply, the current situation is similar to what we saw in January 2021. Gold was also trading close to its 50- and 200-day moving averages at that time. The pullbacks were relatively small in the case of gold, and… they were even smaller in the case of mining stocks.

The very short-term back and forth movement that we saw in January wasn’t really worth trading – the risk of not being able to get back in at higher prices was too big. It seems to be quite high also at this time, especially when we consider what’s going on in the stock markets. And yes, I mean stock markets, not just one. Let’s take a look at “world stocks”.

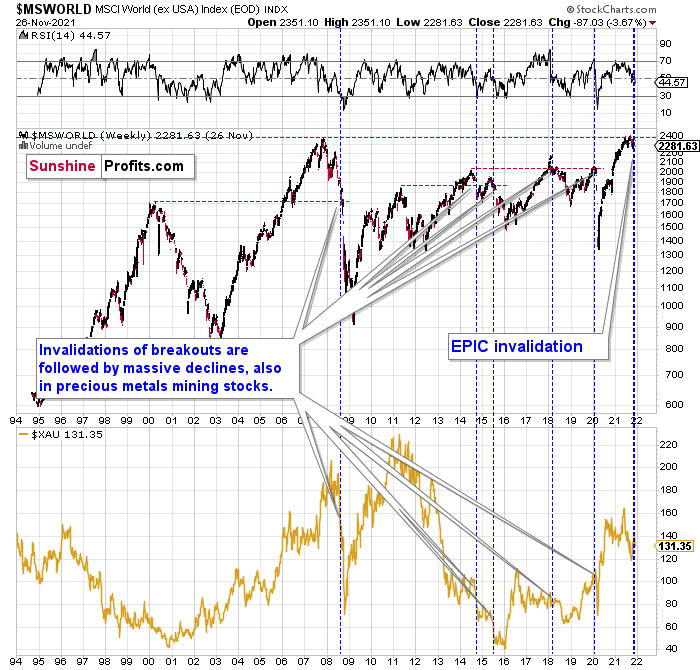

In the chart below, you’ll find the Morgan Stanley Investment International (MSCI) index on world markets, excluding the USA.

Something truly epic is happening in this chart. Namely, world stocks tried to soar above their 2007 high, they managed to do so and… they failed to hold the ground. Despite a few attempts, the breakout was invalidated. Given that there were a few attempts and that the previous high was the all-time high (so it doesn’t get more important than that), the invalidation is a truly critical development.

It's a strong sell signal for the medium- and quite possibly for the long term.

From our – precious metals investors’ and traders’ – point of view, this is also of critical importance. All previous important invalidations of breakouts in world stocks were followed by massive declines in the mining stocks (represented by the XAU Index).

Two of the four similar cases are the 2008 and 2020 declines. In all cases, the declines were huge, and the only reason why they appear “moderate” in the lower part of the above chart is that it has a “linear” and not “logarithmic” scale. You probably still remember how significant and painful (if you were long that is) the decline at the beginning of 2020 was.

Now, all those invalidations triggered big declines in the mining stocks, and we have “the mother of all stock market invalidations” at the moment, so the implications are not only bearish, but extremely bearish.

What does it mean? It means that it is time when being out of the short position in mining stocks to get a few extra dollars from immediate-term trades might be risky. The possibility that the omicron variant of Covid makes vaccination ineffective is too big to be ignored as well. If that happens, we might see 2020 all over again – to some extent. In this environment, it looks like the situation is “pennies to the upside and dollars to the downside” for mining stocks. Perhaps tens of dollars to the downside… You have been warned.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Can You Hear It? That’s the Crowd Booing Gold’s Downturn

November 29, 2021, 9:17 AMEven though the technicals have been predicting this for several months, people were still taken aback by gold’s fall — that’s why they're booing.

While the precious metals received a round of applause for their performances in October, I warned on several occasions that the celebration was premature. And with gold, silver, and mining stocks resuming their 2021 downtrends, investors’ cheers have turned into jeers in short order.

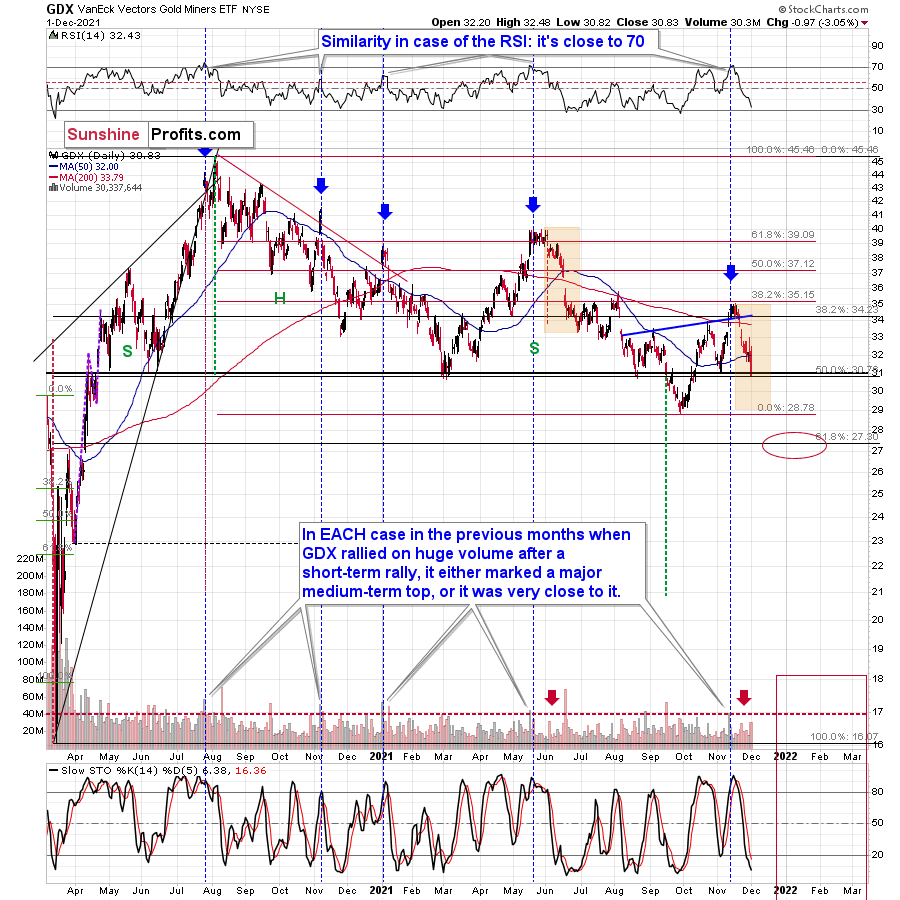

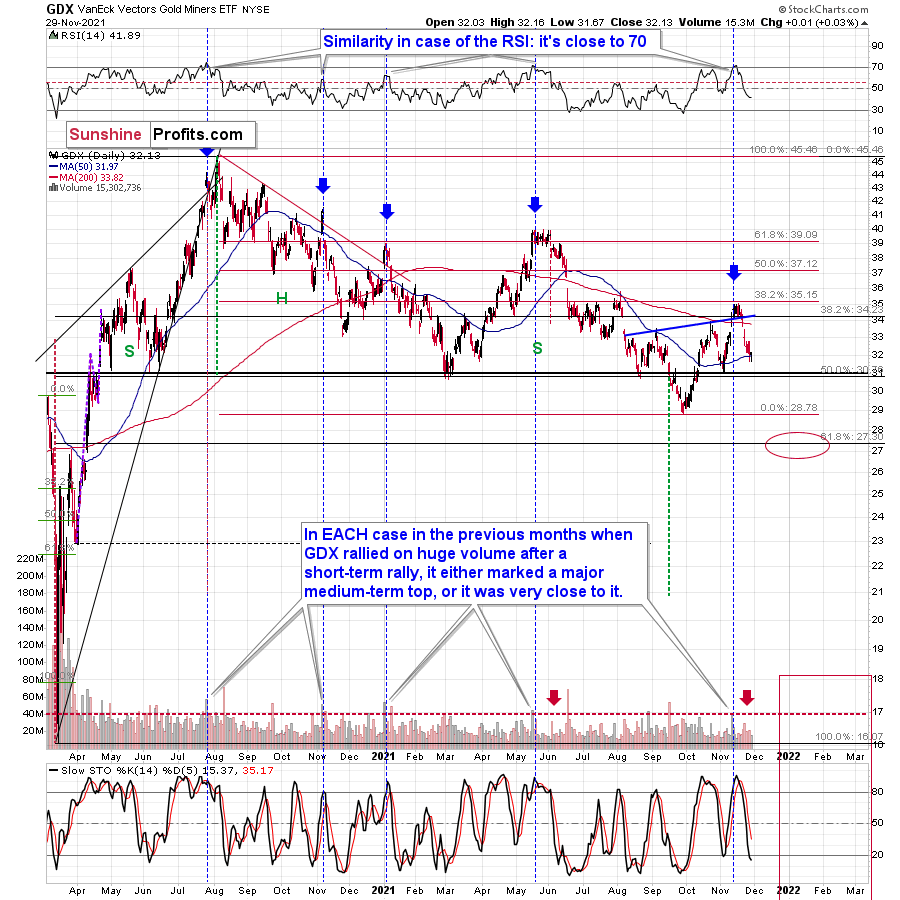

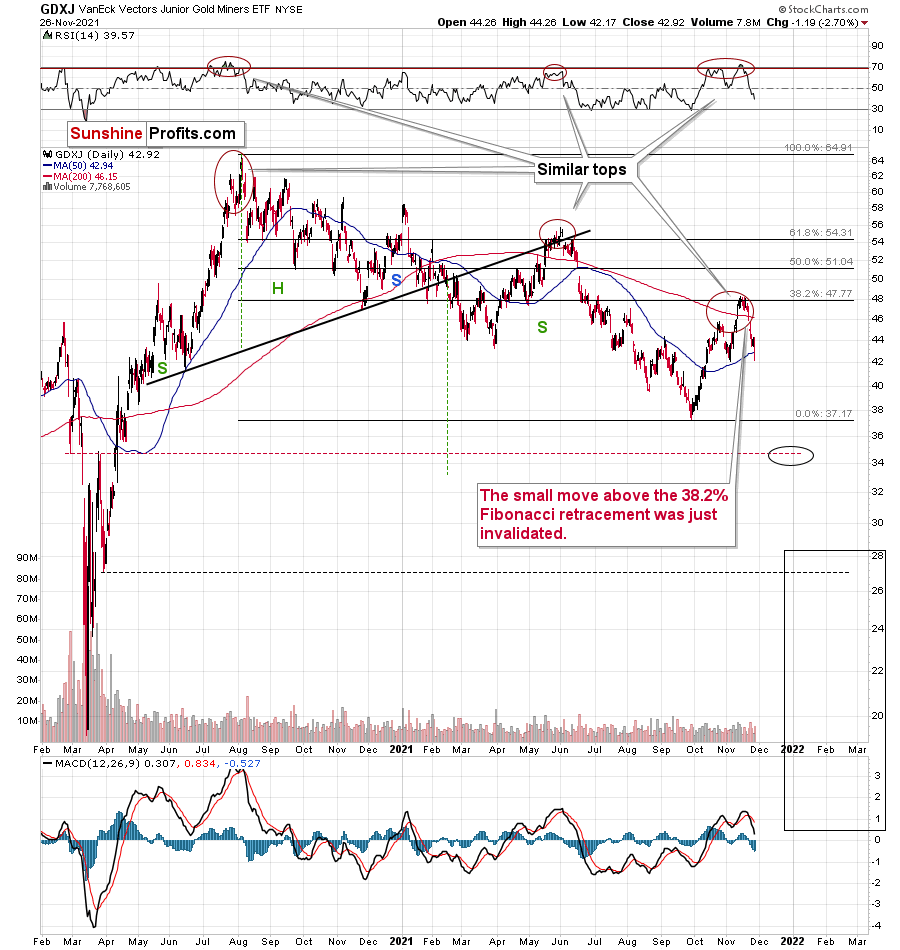

To explain, I warned previously that the GDX ETF could rally to or slightly above $35 (the senior miners reached this level intraday on Nov. 12, moving one cent above it). However, with the GDX ETF’s RSI (Relative Strength Index) signaling overbought conditions, I highlighted just how quickly the air often comes out of the balloon. For context, the blue vertical dashed lines below depict the sharp reversals that followed after the GDX ETF’s RSI approached or superseded 70.

Why am I telling you this? To emphasize that what happened recently was neither random nor accidental. What you see is a true, short-term top that formed in tune with previous patterns. You also see a fake inverse head-and-shoulders formation that was invalidated. This means that the implications of what happened really are bearish.

Let’s check why and how, in tune with the past patterns, the previous broad top really was. Please see below:

The GDX ETF rallied on huge volume on Nov. 11 and there were only 4 cases in the recent past when we saw something like that after a visible short-term rally.

In EACH of those 4 cases, GDX was after a sharp daily rally.

In EACH of those 4 cases, GDX-based RSI indicator (upper part of the chart above) was trading close to 70.

The rallies that immediately preceded these 4 cases:

- The July 27, 2020 session was immediately preceded by a 29-trading-day rally that took the GDX about 42% higher. It was 7 trading days before the final top (about 24% of time).

- The November 5, 2020 session was immediately preceded by a 5-trading-day rally that took the GDX about 14%-15% higher (the high-volume day / the top). It was 1 trading day before the final top (20% of time).

- The January 4, 2021 session was immediately preceded by a 26-trading-day rally that took the GDX about 17%-18% higher (the high-volume day / the top). It was 1 trading day before the final top (about 4% of time).

- The May 17, 2021 session was immediately preceded by a 52-trading-day rally that took the GDX about 30% higher. It was 7 trading days before the final top (about 13% of time).

So, as you can see these sessions have even more in common than it seemed at the first sight. The sessions formed soon before the final tops (4% - 24% of time of the preceding rally before the final top), but the prices didn’t move much higher compared to how much they had already rallied before the high-volume sessions.

Consequently, since history tends to rhyme, it would have been only natural for one to expect the GDX ETF to move a bit higher here (but not significantly so) and for one to assume that this move higher would take between additional 0 to 7 trading days (based on the Nov. 12 session). That’s what is wrote to my subscribers – to expect this kind of performance.

The final top formed on Nov. 16 - 4 trading days after the huge-volume session, practically right in the middle of the expected 0-7 trading day range.

Moreover, since the GDX topped very close to its 38.2% Fibonacci retracement, it seems that miners corrected “enough” for another huge downswing to materialize.

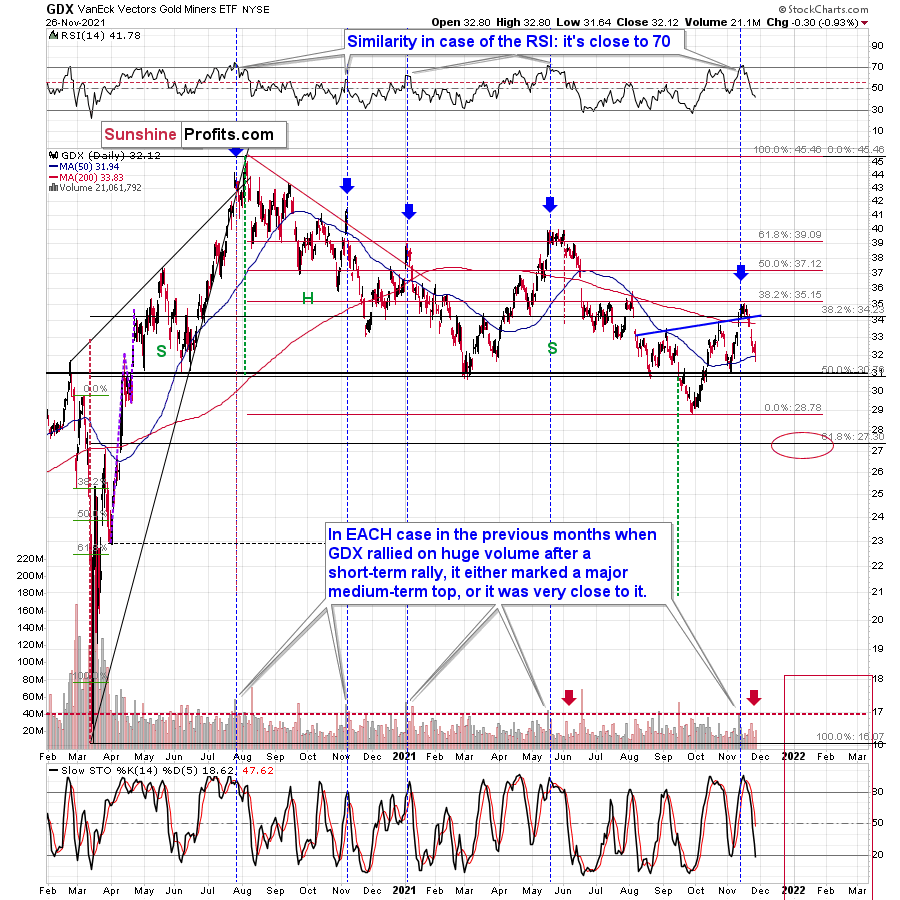

Having said that, let’s move on to more recent developments.

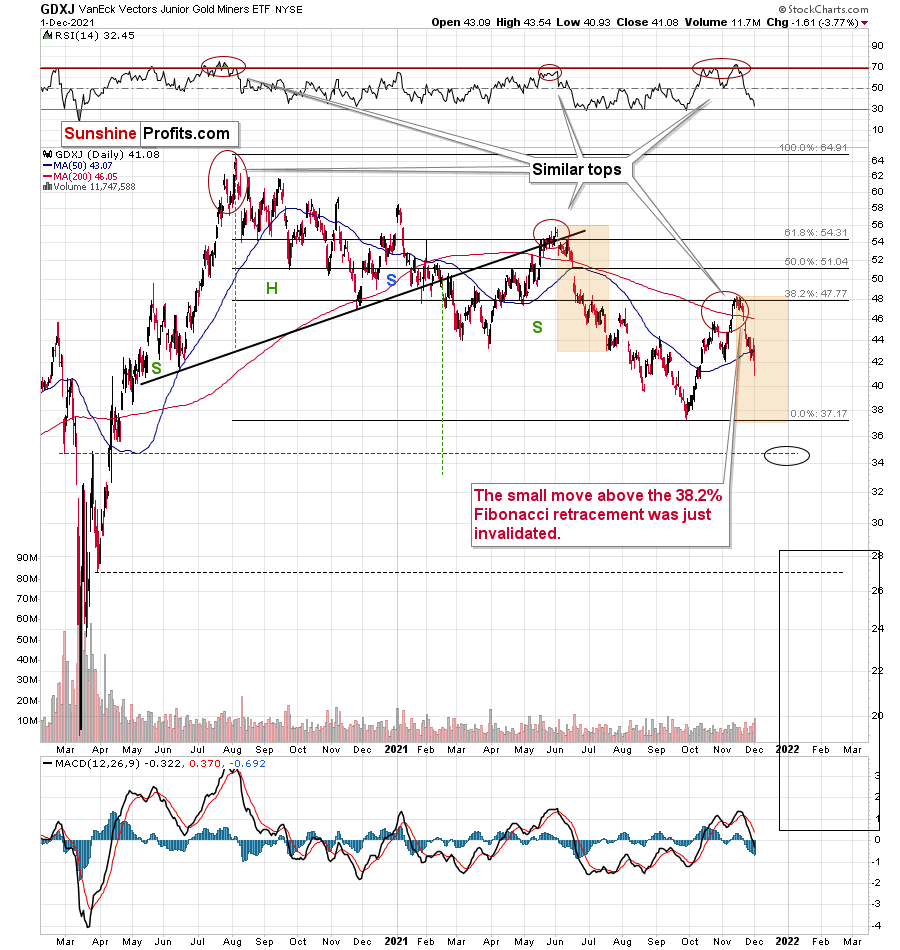

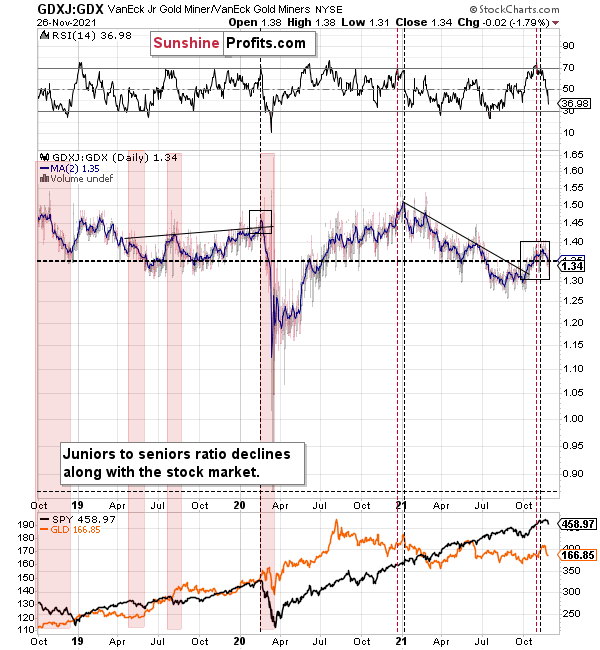

Gold price declined heavily recently and the same goes for the silver price. What’s more, the proxy for junior mining stocks - the GDXJ ETF (our short position) materially underperformed on Nov. 26 – after it declined by nearly 3x the percentage of the GDX ETF – and, in my opinion, more downside is likely to materialize over the medium term.

The GDXJ ETF ended the Nov. 26 session slightly below its 50-day moving average, and the milestone is often a precursor to sharp drawdowns. That’s what happened in late February 2020 and also in mid-June 2021. Big declines followed in both cases.

Moreover, with the S&P 500’s weakness on Nov. 26 mirroring the onslaught that unfolded in early 2020, the GDXJ ETF’s underperformance follows a familiar script. As a result, another ‘flash crash’ for the pair may unfold once again.

Keep in mind, though: while asset prices often don’t move in a straight line, a bullish pause may ensue if/once gold reaches its previous lows. All in all, though, lower lows should confront the GDXJ ETF over the short term and my $35 price target remains up to date. As a reminder, that’s only an interim target, analogous to the late-Feb. 2020 low. Interestingly, it is the February 2020 low along with its late-March 2020 high that created this target.

Also, the GDXJ/GDX ratio is falling once again. And with the price action implying that the GDXJ ETF is underperforming the GDX ETF, a drop below 1 isn’t beyond the realms of possibility. In fact, it’s quite likely. As such, this is why I’m shorting the junior mining stocks.

For context, I think that gold, silver and the GDX ETF are all ripe for sharp re-ratings over the medium term. However, I think that the GDXJ ETF offers the best risk-reward proposition due to its propensity to materially underperform during bear markets in the general stock market.

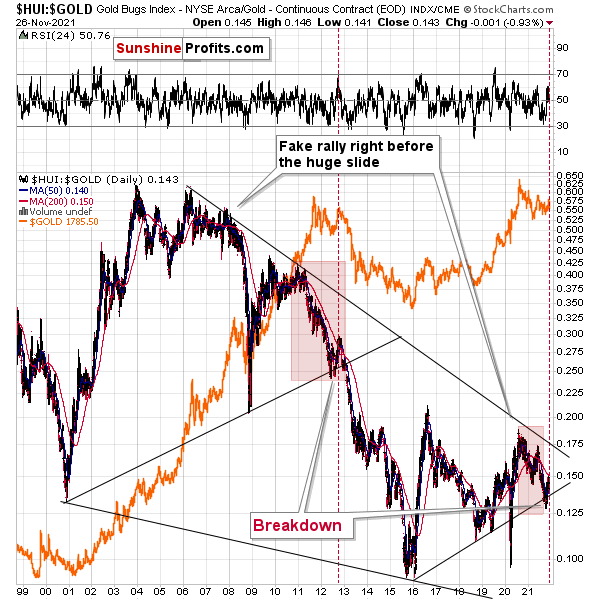

Finally, the HUI Index/gold ratio is also eliciting bearish signals. For example, I marked (with the shaded red boxes below) just how similar the current price action is to 2013. And back then, after a sharp decline was followed by a small corrective upswing before the plunge, the ratio’s current behavior mirrors its historical counterpart.

What’s more, the end of the corrective upswing in 2013 occurred right before gold sunk to its previous lows (marked with red vertical dashed lines in the middle of the chart below). Thus, the ratio is already sending ominous warnings about the PMs’ future path.

In addition, with the S&P 500 acting as the bearish canary in the coal mine, the ratio plunged in 2008 and 2020 when the general stock market tanked. Thus, if a similar event unfolds this time around, the gold miners’ sell-off could occur at a rapid pace.

For more context, I wrote previously:

A major breakdown occurred after the HUI Index/gold ratio sunk below its rising support line (the upward sloping black line on the right side of the chart above). Moreover, with the bearish milestone only achieved prior to gold’s crash in 2012-2013, the ratio’s breakdown in 2013 was the last chance to short the yellow metal at favorable prices. And while I’ve been warning about the ratio’s potential breakdown for weeks, the majority of precious metals investors are unaware of the metric and its implications. As a result, investors’ propensity to ‘buy the dip’ in gold will likely backfire over the medium term.

In conclusion, the crowd has turned on the precious metals, and the narrative has shifted once again. However, despite all of the drama and the volatility that came with it, the technicals have been predicting this outcome for several months. And with the GDXJ ETF down by more than 20% YTD (as of the Nov. 26 close), the junior miners’ 2021 performance is far from critically-acclaimed. As a result, the chorus of boos will likely continue over the short- and/or medium term.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Early (Gold Video) Heads-up before the Next Week

November 28, 2021, 11:06 AMIn today’s early heads-up video, I’m talking about Friday’s intraday reversal in gold price along with a likely reason that caused it (the initial reaction to the omicron variant of the Covid-19). The way gold price reacted tells us quite a lot about the outlook for the following weeks…

You can access the video using the following link:

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM