Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Welcome to this week's flagship Gold & Silver Trading Alert. As we’ve promised you previously, in our flagship Alerts, we will be providing you with much more comprehensive and complex analyses (approximately once per week), which will usually take place on Monday.

Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

To begin, let’s discuss the fundamental news that hit the market recently, namely, the blockade of the Suez Canal and the SLR exemption.

In short, neither the blockade of the Suez Canal nor the expiration of the SLR exemption should significantly affect the gold market. The price of the yellow metal is likely to be shaped by other factors in the coming weeks and months.

Do you think you’ve had a bad day? If yes, then imagine the helmsman of the Ever Given who somehow managed to get his giant container ship stuck in the Suez Canal, disrupting global trade and causing economic damage worth millions of dollars each hour. Sure, the blockade won’t sink the global economy (pun intended), but it won’t help it either. After all, the Suez Canal is the gateway between Europe and Asia, through which around 12-13% of world trade flows, as does 30% of the world's daily shipping container freight. So, every day of obstruction disrupts the movement of goods worth about $9 billion, having a significant impact on global trade.

Of course, the world won’t end, and ships can always choose an alternative route round the Cape of Good Hope at the southern tip of Africa, but this route takes several days longer. So, the blockade has significantly delayed the consignments of goods and fuel, and exacerbated the already pandemic-disturbed supply channels. As a reminder, there are shortages of containers, semi-conductors, and other inputs and finished goods, that have significantly lengthened delivery times and pushed prices up. Although the blockade of the Suez Canal is temporary, it adds additional disruption on top of the existing supply problems. Meanwhile, the central banks and governments interpret everything as demand problems that need to be addressed through easy monetary policy and loose fiscal policy.

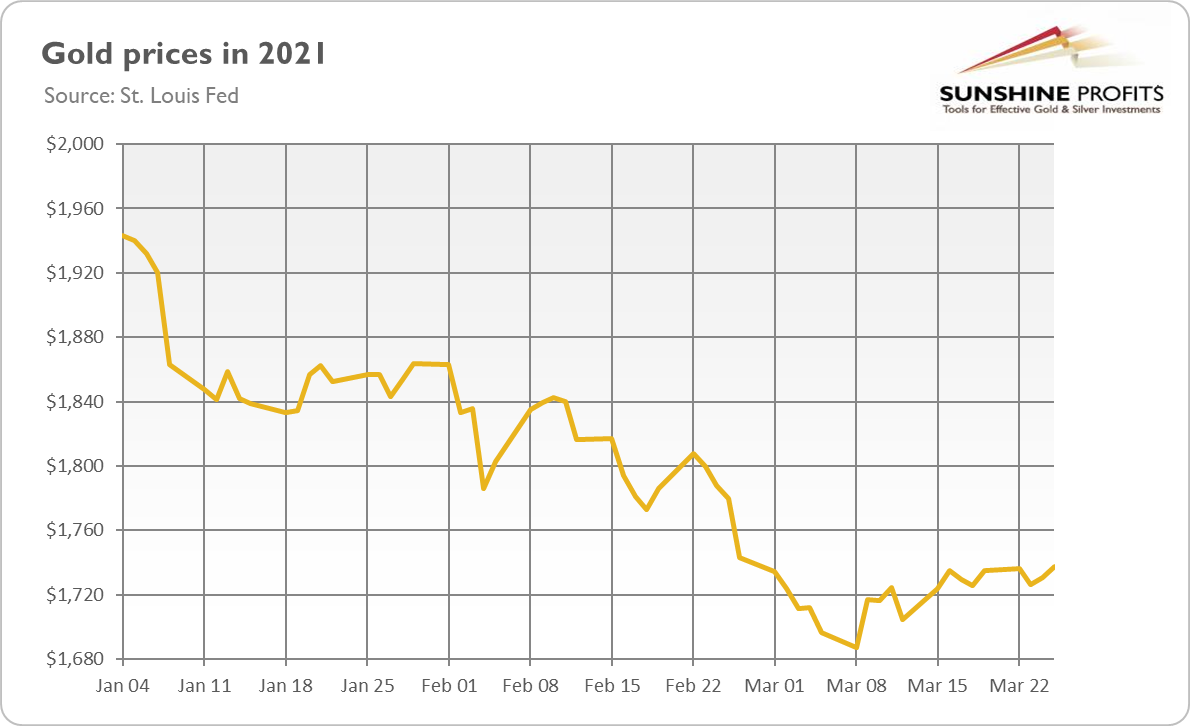

The accident of the Ever Given won’t significantly impact gold prices. And, as the chart below shows, we haven’t seen any substantial effects so far.

However, the blockade could remind investors (if they somehow managed to forget amid the pandemic) that black swans exist and fly low, and it’s reasonable to have a portion of one’s investment portfolio in safe havens such as gold (for instance, the insurance part of the portfolio). Additionally, the upward pressure on prices (although limited) could strengthen the appeal of gold as an inflation hedge, especially considering that officially reported inflation is likely to jump next month because of the low base effect and all the recent supply disruptions.

Fed Allows for Expiration of SLR

And now for something completely different. The Federal Reserve Board announced that the temporary change to its supplementary leverage ratio, or SLR, for bank holding companies will expire as scheduled on March 31. What does this mean for the U.S. economy and the gold market?

The SLR is a regulation that requires the largest U.S. banks to hold a minimum level of capital. The ratio says how much equity capital the banks have to hold relative to their total leverage exposure (3% in the case of large banks and 5% in the case of top-tier banks). To ease strains in the Treasury market during the Covid-19 epidemic, the Fed temporarily excluded the U.S. Treasuries and central bank reserves from the calculation. In other words, banks could increase their holdings of government bonds and central bank reserves without raising equity capital.

But now, with the exemption expired, their equity capital will be calculated again relative to the banks’ total leverage exposure, including Treasuries and central bank reserves. So, it might be the case that the banks will have to either increase the amount of equity (which is rather unlikely) or reduce the amount of government bonds. And if they sell Treasuries, it would add to the upward pressure on the bond yields. This would prove rather negative for gold, which is a non-interest-bearing asset.

However, it doesn’t have to be the case. I mean here that the U.S. eight large and systematically important banks wouldn’t fall below their 5% regulatory minimum. Actually, they are said to have a roughly 25% buffer above minimum thresholds, so the expiry of the SLR exemptions doesn’t have to significantly affect the functioning of the Treasury market, at least not immediately. Hence, the impact of the expiration of the SLR exemption could have limited effect on the gold market, if any.

It seems that the price of the yellow metal will be rather shaped by the real interest rates, the U.S. dollar, inflation, the level of confidence in the U.S. economy, etc. In the short-term, the focus on economic recovery could continue the downward pressure on gold prices, but in the long-term, the stagflation theme could resurface and push the price of the yellow metal up.

Having said that, let’s move to the cross-asset implications that could affect the precious metals in the coming weeks.

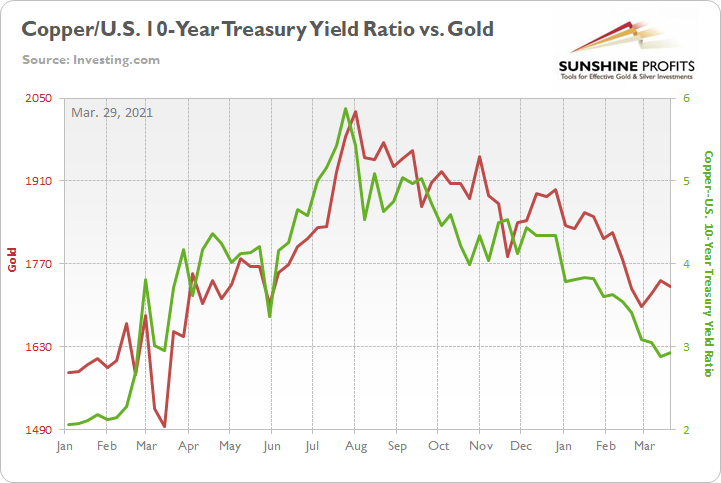

Over the medium-to-long-term, the copper/U.S. 10-Year Treasury yield ratio is a leading indicator of gold’s future behavior.

I wrote previously:

When the copper/U.S. 10-Year Treasury yield ratio is rising (meaning that copper prices are rising at a faster pace than the U.S. 10-Year Treasury yield), it usually results in higher gold prices. Conversely, when the copper/U.S. 10-Year Treasury yield ratio is falling (meaning that the U.S. 10-Year Treasury yield is rising at a faster pace than copper prices), it usually results in lower gold prices.

If you analyze the chart below, you can see the close connection:

Peaking and rolling over within days of one another, gold and the copper/U.S. 10-Year Treasury yield ratio have been in a downward spiral since August. And despite diverging slightly over the last three weeks, the overall downtrend remains in place. Case in point: because gold has the tendency to suffer sharp daily corrections and the fact that historical divergences are often outliers and not trends (see October below), if the copper/U.S. 10-Year Treasury yield ratio continues to elicit weakness, the yellow metal is likely to follow suit.

Please see below:

Highlighting the bearish relationship, with the U.S. 10-Year Treasury yield surging by nearly 80% year-to-date (YTD) and nearly 204% since its August trough, gold topped exactly one day after the U.S. 10-Year Treasury yield bottomed. And with the U.S. 10-Year Treasury yield’s current pause likely to give way to further upward momentum, the potential remains profoundly bearish for the yellow metal.

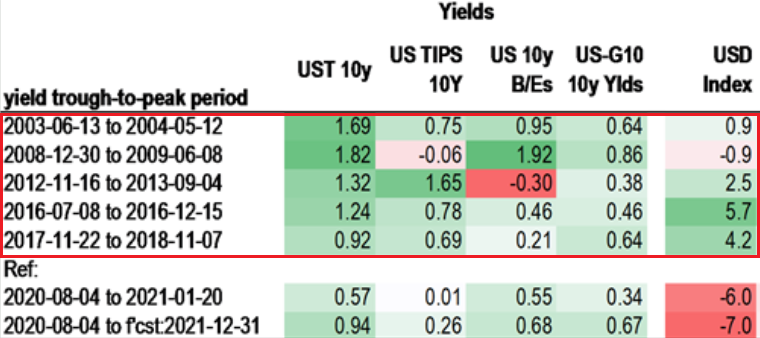

In addition, after defying historical precedent for all of 2020, the USD Index is beginning to follow the U.S. 10-Year Treasury yield higher. If you analyze the table below, you can see that a bottom, and subsequent move higher in the U.S. 10-Year Treasury yield, has coincided with a rise in the USD Index 80% of the time since 2003.

And while the USD Index is still lower now than it was in August, since the New Year, the relationship has begun to take shape.

Please see below:

And piecing together the puzzle, because the yellow metal exhibits a negative correlation with the U.S. dollar, gold’s pain tends to coincide with U.S. dollar gains. As a result, if the USD Index continues its upward momentum, the development will add even more concrete to gold’s wall of worry.

On the flip side, if we extend our time horizon, there are plenty of fundamental reasons why gold is likely to soar in the coming years. However, even the most profound bull markets don’t move up in a straight line, and corrections are inevitable.

As it relates to the precious metals, a significant correction (medium-term downtrend) is already underway. However, the pain is not over, and a severe climax likely awaits.

For context, potential triggers are not always noticeable, and the PMs may collapse on their own or as a result of some random trigger that normally wouldn’t cause any major action. However, a trigger will speed things up and that’s where the S&P 500 comes in:

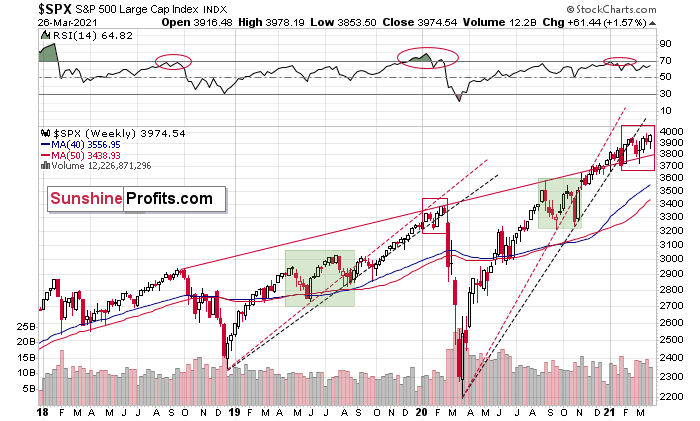

S&P 500 (SPX) Signals

Shades of 2018-2019, the S&P 500’s current price action is following a familiar script. Back then, the U.S. equity benchmark recorded a sharp move higher, consolidated (with heightened volatility, which I marked with a green box below), continued its uptrend, then suffered a material drawdown. Something very similar happened in the past 12 months – at least the upswing part.

After the second bottom of the green-shaded area, the S&P 500 rallied in a stable manner between rising black and red lines that were based on the previous bottoms. The breakdown below them was accompanied by increased volatility and then the stock market plunged. We’ve seen everything from that pattern also this time, only the plunge hasn’t started… Yet.

Please see below:

In similar fashion, today, the S&P 500’s fits and starts are signaling an identical outcome. After breaking below its red and black dashed rising support lines in 2020 and 2021 (on the right side of the chart), the S&P 500 is currently trading below both levels. Furthermore, the heightened volatility that unfolded from August to October is a tell-tale sign that the 2018-2019 analogue could rear its ugly head.

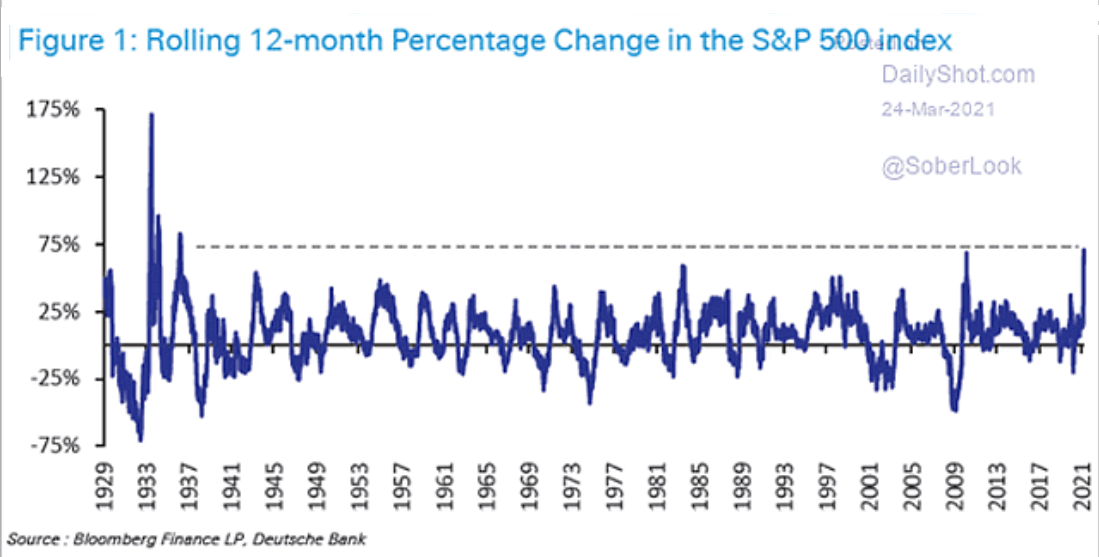

Likewise, the S&P 500 just recorded its highest 12-month percentage change since 1936. And notice below how large aberrations are often followed by large reversions?

Conversely, while the outlook for the S&P 500 remains profoundly bearish over the medium term, timing is increasingly uncertain. With stimulus checks largely priced in and peak options activity signaling a slow burn, bouts of volatility often occur without warning. Thus, because preconditions are already present, it’s likely a matter of when, not if, the climax unfolds.

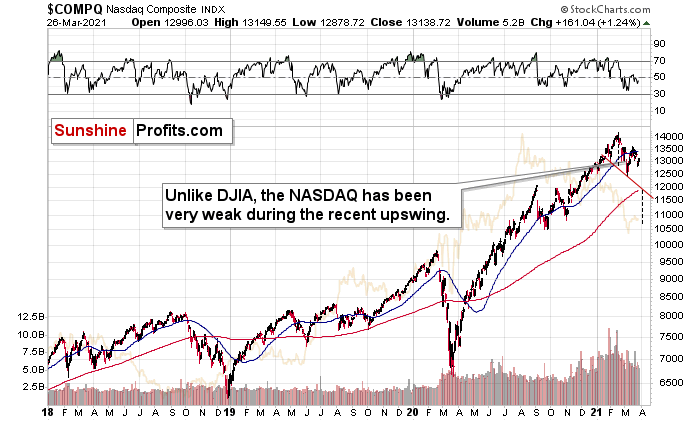

As for the NASDAQ Composite – which led equities’ surge in 2020 – the tech-heavy index could act as equities’ canary in the coal mine. A mile away from new highs, not only has equities’ leadership changed, but the NASDAQ Composite could also be in the early innings of forming a bearish head and shoulders pattern.

Please see below:

For context, the potential H&S pattern is still relatively immature. But if the NASDAQ Composite breaks below ~12,000 (the neck level), a drawdown to ~10,550 or ~10,850 (the mid-2020 lows) could be next in line. Remember, the six largest companies in the NASDAQ Composite – Apple, Microsoft, Amazon, Tesla, Facebook and Alphabet – are also the six largest companies in the S&P 500. Thus, a drawdown of the former will weigh heavily on the latter. Likewise, a potential equity rout is profoundly bearish for the PMs, as silver and the miners will likely be the hardest hit.

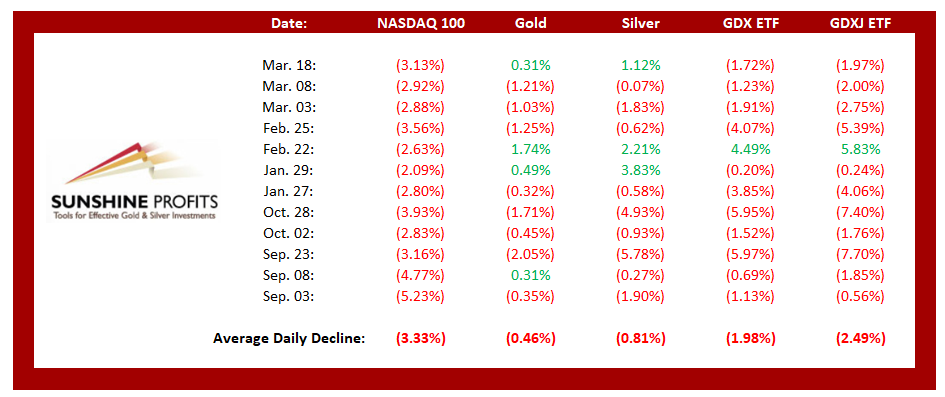

For context, if you analyze the table above, you can see that NASDAQ 100 drawdowns of more than 2.00% tend to unnerve the PMs. Moreover, if you exclude silver’s short squeeze on Jan. 29 and the NASDAQ 100’s relatively ‘quiet’ 2.63% drawdown on Feb. 22, bouts of equity volatility significantly impact the PMs (especially the miners).

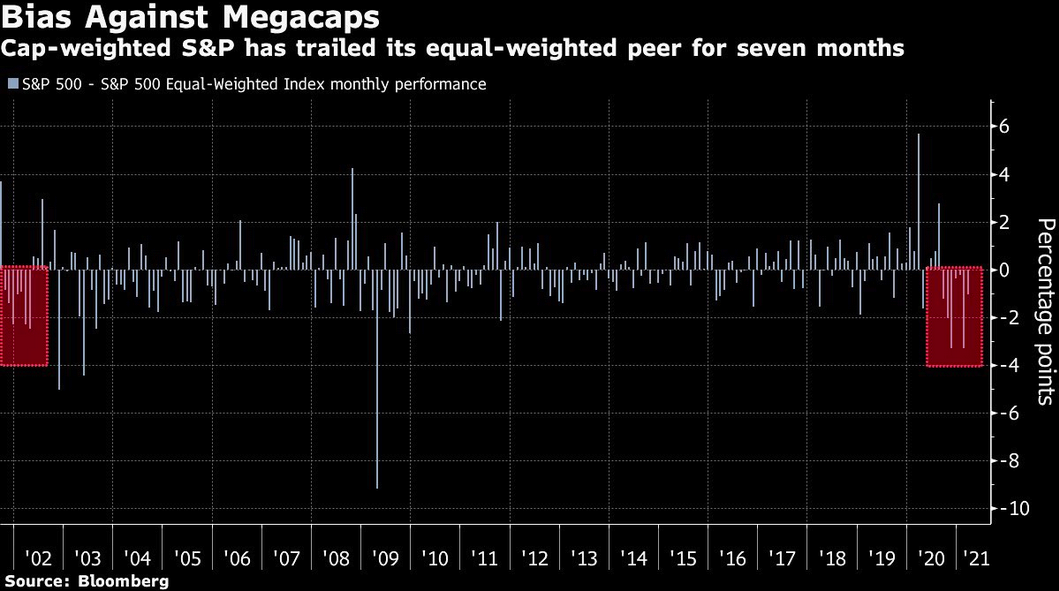

As further evidence of Big Tech’s underperformance, the S&P 500 equal-weight index has outperformed the S&P 500 – a market-cap weighted index where Apple, Microsoft, Amazon, Tesla, Facebook and Alphabet have the most influence – for seven-straight months. To explain the significance, it’s the longest streak since the dot-com bust.

Please see below:

Keep in mind though: a decline in stocks is not required for the PMs to decline. But a break in the former could easily trigger a sell-off in the latter, and if history decides to rhyme again, silver and the miners will be the hardest hit.

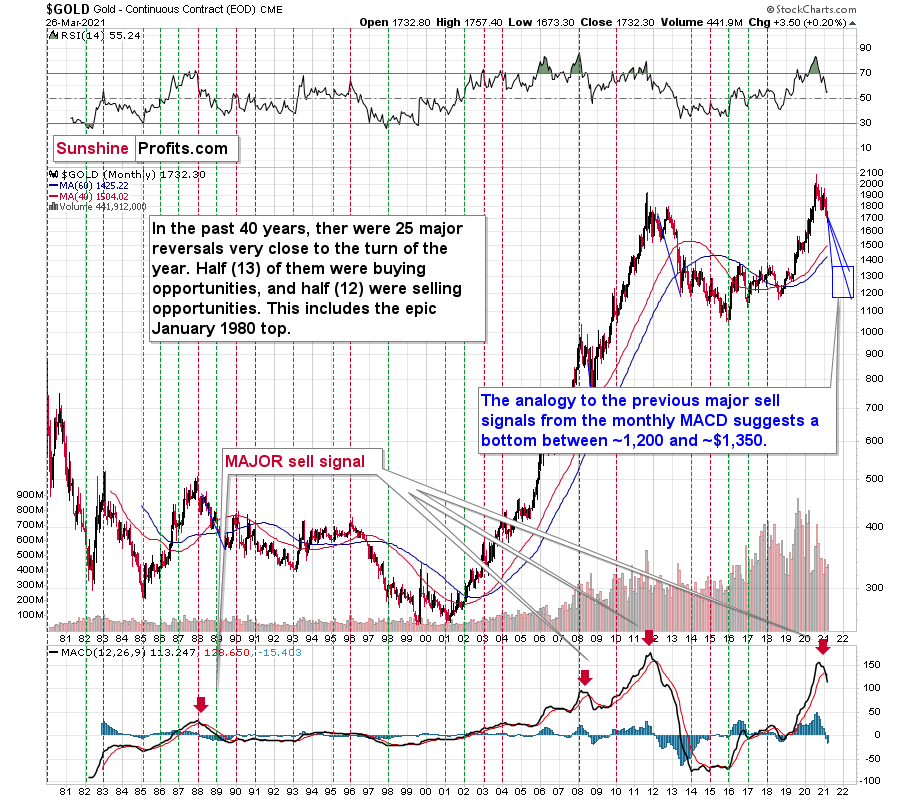

Very Long-term MACD Sell Signal for Gold

With February’s monthly close the last piece of the puzzle, the MACD indicator’s sell-signal is now perfectly clear. If you analyze the chart below (at the bottom right), you can see that the MACD line has crossed the signal line from above – a development that preceded significant drawdowns in 2008 and 2011.

Based on gold’s previous performance after the major sell signals from the MACD indicator, one could now expect gold to bottom in the ~$1,200 to ~1,350 range. Given the price moves that we witnessed in 1988, 2008 and 2011, historical precedent implies gold forming a bottom in this range. However, due to the competing impact of several different variables, it’s possible that the yellow metal could receive the key support at a higher level.

For more context, I wrote previously:

Only a shade below the 2011 high, today’s MACD reading is still the second-highest reading in the last 40 years. More importantly though, if you analyze the chart below (the red arrows at the bottom), the last four times the black line cut through the red line from above, a significant drawdown occurred.

Also ominous is that the magnitude of the drawdowns in price tend to coincide with the magnitude of the preceding upswings in MACD. And with today’s reading only surpassed by 2011, a climactic move to the $1,250/$1,450 range isn’t out of the question for gold. The above is based on how low gold had previously declined after similarly important sell signal from the MACD

Now, the month is not over yet, so one might say that it’s too early to consider the sell signal that’s based on monthly closing prices, but it seems that given the level that the MACD had previously reached and the shape of the top in the black line, it makes the situation so similar to 2011/2012 that the sell signal itself is just a cherry on the bearish analytical cake.

Considering the reliability of the MACD indicator as a sell signal for major declines, the reading also implies that gold’s downtrend could last longer and be more severe than originally thought. As a result, $1,500 remains the most likely outcome, with $1,350 still in the cards.

The USD Index (USDX)

Counted out, counted down and rarely counted on, investors threw in the USD Index’s towel long before the fight even began. However, after shaking the cobwebs and landing a few haymakers, the greenback’s Rocky-like comeback is proof that ‘it ain’t over till it’s over.’

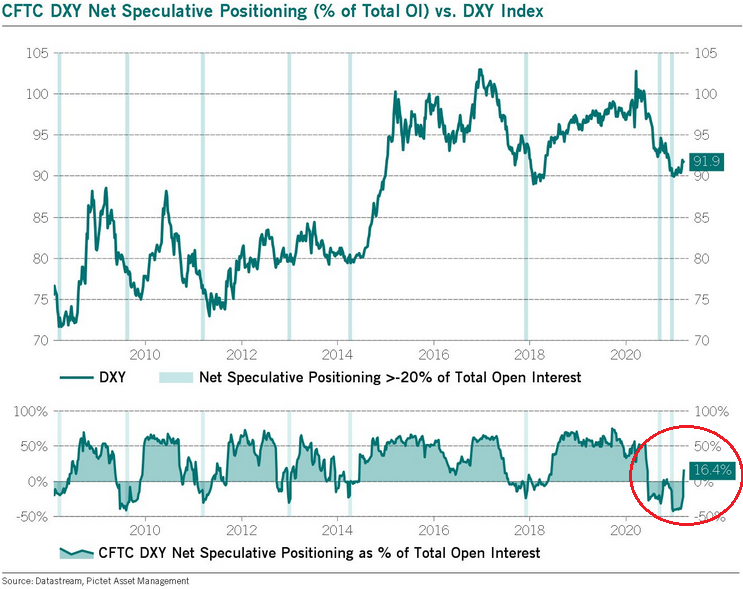

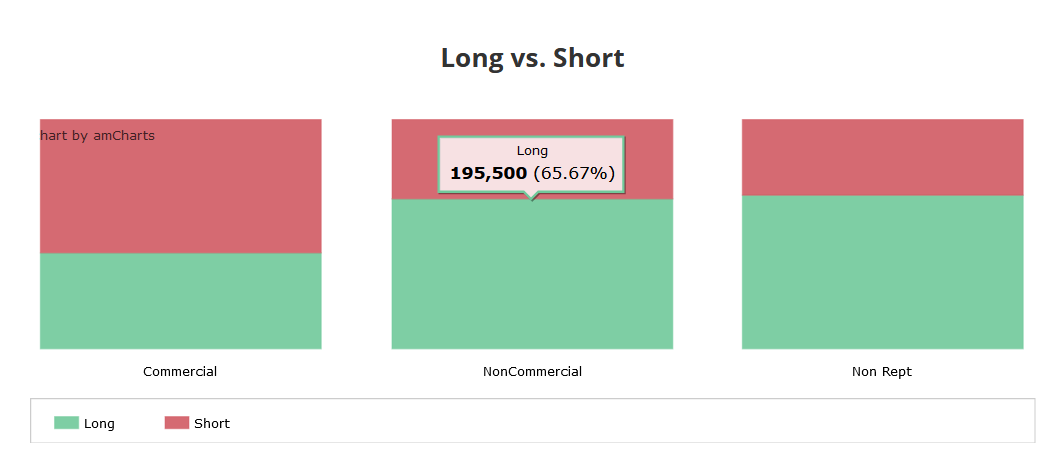

Now, with thousands of screaming fans chanting “USD, USD,” the eye of the tiger could be eying another move higher. As evidence, if you analyze the chart below, you can see that non-commercial (speculative) traders have quietly repositioned from net-short to net-long.

To explain, notice how oversold periods in 2014 and 2018 – where net-speculative short interest as a percentage of total open interest was extremely high – preceded sharp rallies in the USD Index? Thus, with 2021 the most extreme on record, the forthcoming rally should be significant.

How significant? Well, let’s take a look at how things developed in the past – after all, history tends to rhyme.

Let’s focus on what happened when the net speculative positions were significantly (!) negative and then they became significantly (!) positive, so without paying attention to tiny moves (like the one that we saw last summer), let’s focus on the more meaningful ones (like the one that we see right now – the net positions just became visibly positive – over 16%, after being very negative for quite some time.

In short, that’s how the following profound rallies started:

- The big 2008 rally (over 16 index points)

- The big 2009 – 2010 rally (over 14 index points)

- The 2011 – 2012 rally (over 11 index points)

- The 2013 rally (“only” over 5 index points)

- The big 2014 – 2015 rally (over 20 index points)

- The 2018 rally (over 15 index points)

The current rally started at about 89, so if the “normal” (the above shows what is the normal course of action) happens, the USD Index is likely to rally to at least 94, but since the 5-index point rally seems to be the data outlier, it might be better to base the target on the remaining 5 cases. Consequently, one could expect the USD Index to rally by at least 11 – 20 index points, based on the net speculative positions alone. This means the upside target area of about 105 – 114.

Consequently, a comeback to the 2020 highs is not only very likely, but also the conservative scenario.

Adding to the momentum, in 2020, the USD Index sat out the U.S. 10-Year Treasury yield’s ferocious upswing. Defying historical precedent, a bottom and subsequent move higher in the U.S. 10-Year Treasury yield has coincided with a rise in the USD Index 80% of the time since 2003. But now in sync, 2021 has been a much different story. If you analyze the chart below, you can see that the USD Index has been moving in lockstep with the U.S. 10-Year Treasury yield since the New Year.

In addition, not only has the USD Index broke above its previous highs, but the basket just reclaimed its 200-day moving average(which is often indicative of a long-term uptrend). As a result, the greenback continues to float like a butterfly and sting like a bee.

For historical context, after recapturing its 200-day MA in 2018, the USD Index only suffered mild pullbacks before surging above 95. As such, with the mid-2020 highs the USD Index’s next opponent, 94.5 is unlikely to put up much of a fight.

Keep in mind though: in the very-short term, the USD Index could move lower and retest its prior 2021 highs. However, the damage should be minimal, and it wouldn’t invalidate the USD Index’s medium-term breakout. Because of this, the outlook remains profoundly bearish for the gold, silver, and mining stocks over the medium term. If you analyze the table below, you can see that the precious metals tend to move inversely to the U.S. dollar.

But saving the best for last, the 2017-2018 analogue could be the USD Index’s knockout punch. With this version likely to be titled “The Resurgence: Part 2,” while history often rhymes, it’s rare for it to rhyme with this level of specificity.

Please see below:

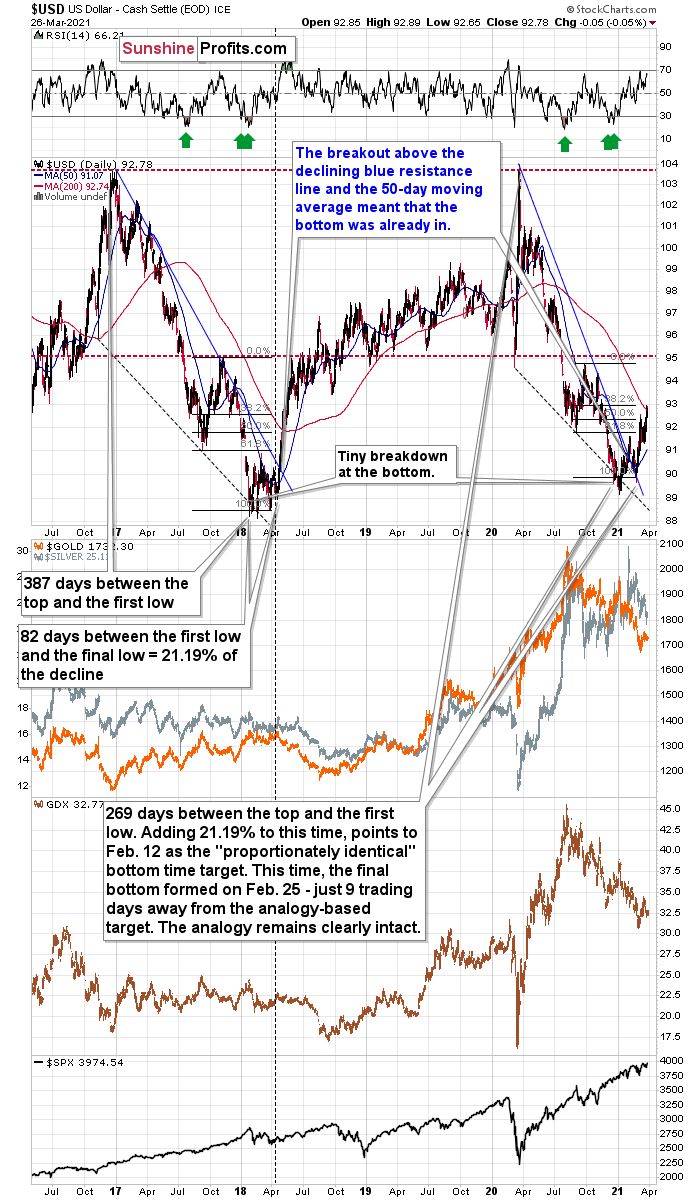

Even more revealing, while it took less than 118 days for the USD Index to move from peak to trough in 2020-2021, the uprising could occur at a much faster pace. In 2018, the USD Index’s breakout above its 50-day moving average is exactly what added gasoline to the USDX’s 2018 fire. And after the 2018 breakout, the USDX surged back to its previous high. Today, that level is 94.5.

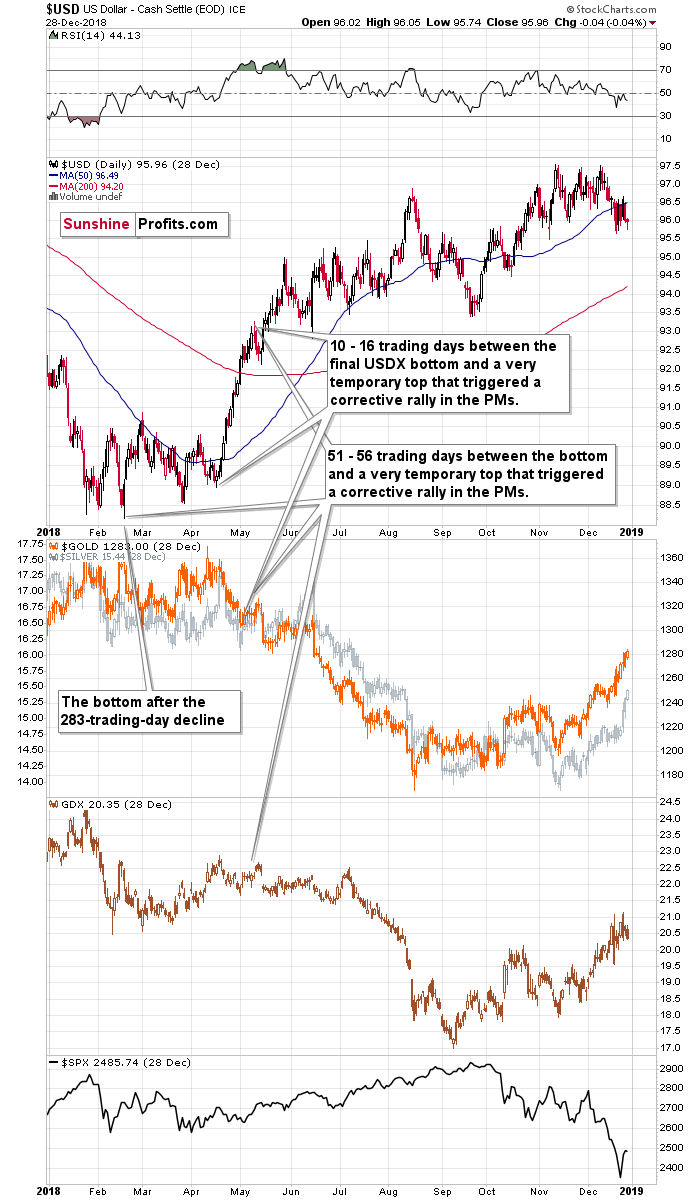

Furthermore, in 2017-2018, it also took 82 days for the USDX to form a final bottom (the number of days between the initial bottom and the final bottom) and the duration amounts to 21.19% of the overall timeframe. If we applied a similar timeframe to today’s move, then the USD Index should have bottomed on Feb. 12. It actually bottomed (finally) on Feb. 25, which was just 8 trading days away from the former date. Taking into account the sizes of the moves that preceded the previous declines (they took approximately one year to complete), this is extremely close and an excellent confirmation that the self-similar pattern remains intact.

Also noteworthy, as the USDX approached its final bottom in 2017-2018, gold traded sideways. Today, however, gold has been in a downward spiral and it doesn’t seem that the decline is over. From a medium-term perspective, the yellow metal’s behavior is actually more bearish than it was in 2017-2018.

And while the self-similar pattern is already playing out as predicted, please read below for further explanation as to why the USD Index’s current and historical price action remains a spitting image:

It’s not true that there were no pullbacks during the 2018 rally. There were, but they were simply too small to be visible from the long-term point of view.

The first notable pullback took place in early May 2018, and it contributed to a corrective upswing in the precious metals market. To be precise, the USD Index declined after rallying for 56 trading days, but gold rallied earlier – 51 trading days after the USD Index’s final bottom. The USDX’s immediate-top formed 16 trading days after its final bottom, and gold’s bottom formed 10 trading days after the USD’s final bottom.

Comparing this to the size of the previous decline in terms of the trading days, it was:

- 51 – 56 trading days / 283 trading days = 18.02% - 19.79%

- 10 – 16 trading days / 283 trading days = 3.53% - 5.65%

Also indicating a messy divorce, when the USD Index turned a short-term decline into consolidation in mid-2018, can you guess what happened next? Well, the USD Index moved significantly higher, while gold moved significantly lower.

Please see below:

Moreover, when comparing the pairs’ behavior in mid-2018 to today, it’s ominously similar.

Please see below:

For additional context, I also wrote on Mar. 10:

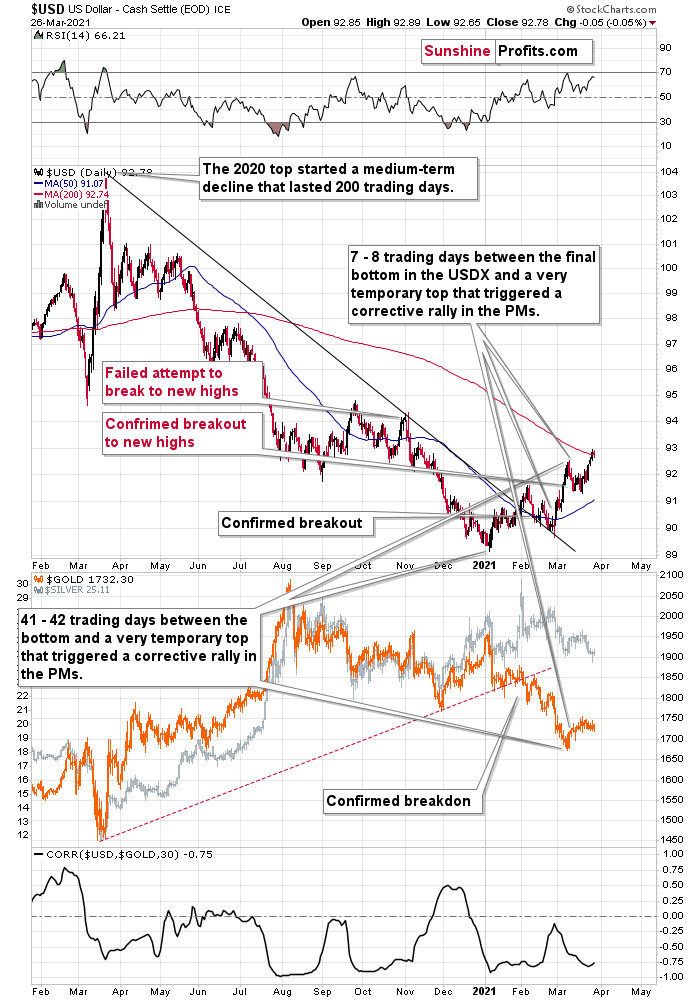

Let’s examine the current situation: the preceding decline lasted for 200 trading days and there were 41 – 42 trading days between the final USDX bottom and the short-term reversals in gold and USDX. Comparing this to the final USDX bottom, we get 7 – 8 trading days.

Applying the previous percentages to the length of the most recent medium-term decline in the USD Index provides us with the following:

- 18.02% - 19.79% x 200 trading days = ~36 - ~40 trading days

- 3.53% - 5.65% x 200 trading days = ~7 - ~11 trading days

The above estimation of about 36 – 40 trading days almost perfectly fits the current 41 – 42-day delay, and the estimation of about 7 – 11 trading days almost perfectly fits the current delay of 7 – 8 trading days.

In other words, the analogy to the 2018 performance does not only remain intact – it actually perfectly confirms the validity of the current corrective upswing. Once again, it’s very likely just a pullback, not a big trend reversal.

Likewise, a potentially bearish pattern that I have been monitoring – where the USD Index’s price action from July to October 2020 mirrored the price action from December 2020 to February/March 2021– has officially been broken. With the USD Index’s medium-term breakout trumping the former, the potentially bearish pattern has been invalidated and the USD Index is likely to continue its ascension.

But to what end?

Well, if we look back at 2020, the USD Index attempted to recapture its previous highs. But lacking the upward momentum, the failure was followed by a sharp move lower. Today, however, the USD Index has broken above its previous highs and the greenback verified the breakout by consolidating, moving back toward the previous lows and rising once again. Now, the USD Index is visibly above its previous highs.

Taken together, and given the magnitude of the 2017-2018 upswing, ~94.5 is likely the USD Index’s first stop. And in the months to follow, the USDX will likely exceed 100 at some point over the medium or long term.

In conclusion, the USD Index went from being on the ropes to winning the crowd. And with the momentum building and the adrenaline rising, it’s only a matter of time before the USD Index lands another haymaker. Moreover, given the precious metals’ negative correlation with the U.S. dollar – combined with the fact that technicals, fundamentals and sentiment are now riding with the greenback – an uprising could leave the gold, silver, and mining stocks battered and bruised. However, after a tough period of soul searching, the precious metals will regain the heavyweight championship once again. Or, if one wants to put it in more technical terms, gold, silver, and miners are likely to start a massive rally, but only after declining visibly first.

Expanding our list of potential upside catalysts, the USD Index still has plenty of other bullets in its chamber. For one, U.S. dollar sentiment is beginning to shift. With short interest hitting an all-time high in late-2020, it was a complete fire sale. However, as mentioned, non-commercial (speculative) traders are now net-long the greenback.

Please see below:

Source: COT

Source: COT

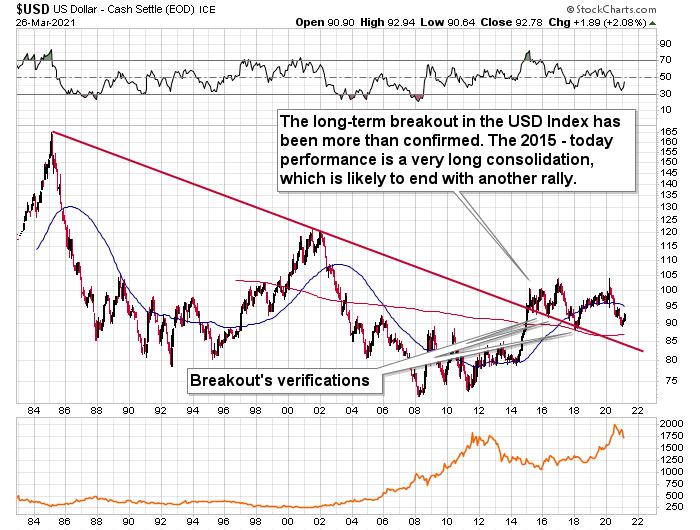

In addition, let’s not forget that the USD Index is after a long-term, more-than-confirmed breakout. This means that the long-term trend for the U.S. dollar is up.

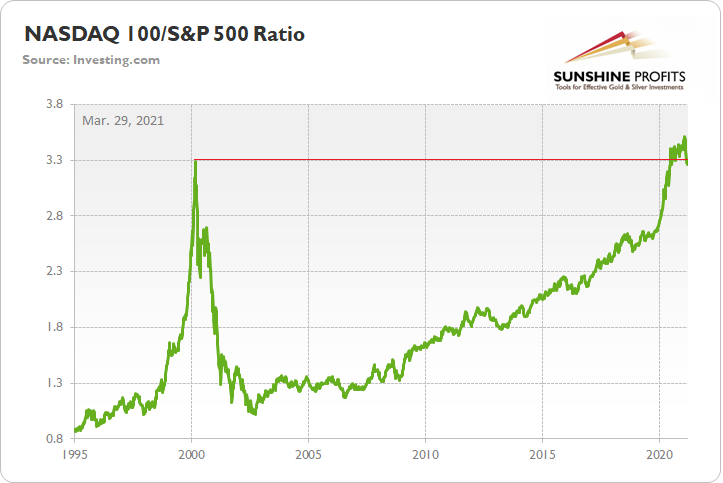

As another potential catalyst, the NASDAQ 100’s underperformance could eventually crack U.S. equities. Unable to make up its mind, the NASDAQ 100/S&P 500 ratio declined by 0.69% last week to fall back below its dot-com bubble peak. More importantly though, if the ratio reverts back to its historical average, it will likely coincide with plenty of fireworks.

To that point, given the USDX’s strong negative correlation with the NASDAQ 100, a reversion to the mean could propel the greenback back to its March highs. Moreover, following a short-term consolidation, the USDX could even exceed those prior highs.

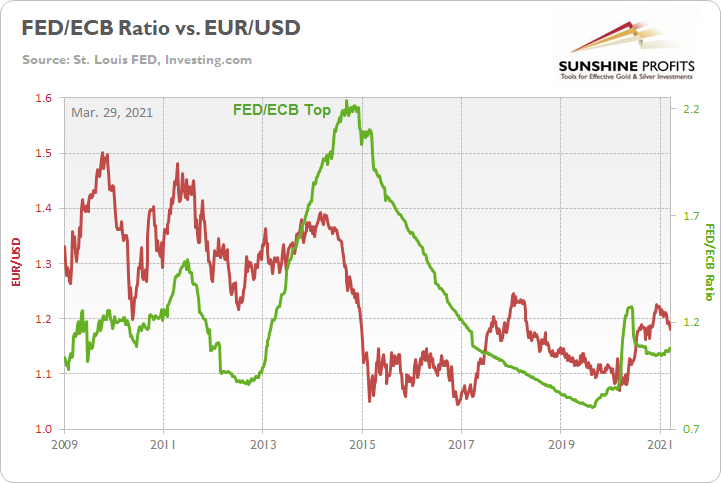

As for the FED/ECB ratio, relative outprinting by the European Central Bank (ECB) remains of critical importance. Last week, the ratio was flat, while the EUR/USD declined by 0.90%. However, given that the ratio has declined by more than 15% since May, the EUR/USD still has some catching up to do.

Please see below:

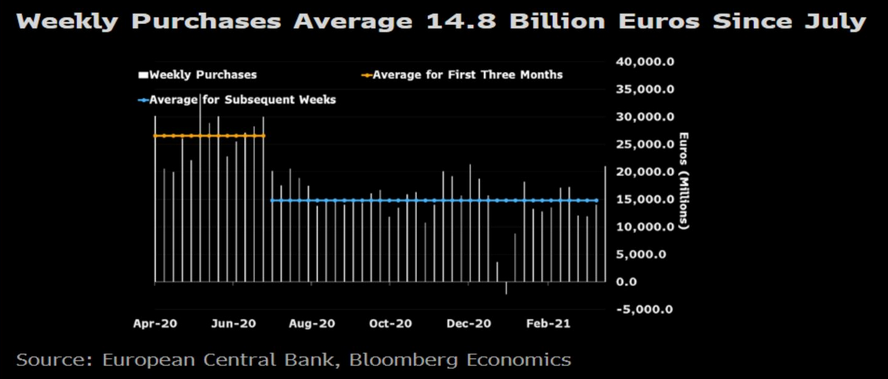

Likewise, after announcing that its weekly PEPP purchases would“be conducted at a significantly higher pace” on Mar. 11, the European Central Bank (ECB) increased its PEPP holdings by €21.1 billion (for the week ended Mar. 19) and the latest splurge was more than 47% above the ~9-month weekly average.

Please see below:

For context, the horizontal blue line above depicts the ECB’s weekly average PEPP purchases since July (€14.8 billion). If you analyze the vertical gray bar on the right side of the chart (€21.1 billion), you can see that the money printer is clearly working overtime.

As a result, with the ECB injecting more liquidity to support an underperforming Eurozone economy, the FED/ECB ratio, and the EUR/USD, should move lower over the medium term. More importantly though, because the EUR/USD accounts for nearly 58% of the movement of the USD Index, EUR/USD pain will be the USDX’s gain.

To explain, I wrote previously:

The top in the FED/ECB total assets ratio preceded the slide in the EUR/USD less than a decade ago and it seems to be preceding the next slide as well. If the USD Index was to repeat its 2014-2015 rally from the recent lows, it would rally to 114. This level is much more realistic than most market participants would agree on.

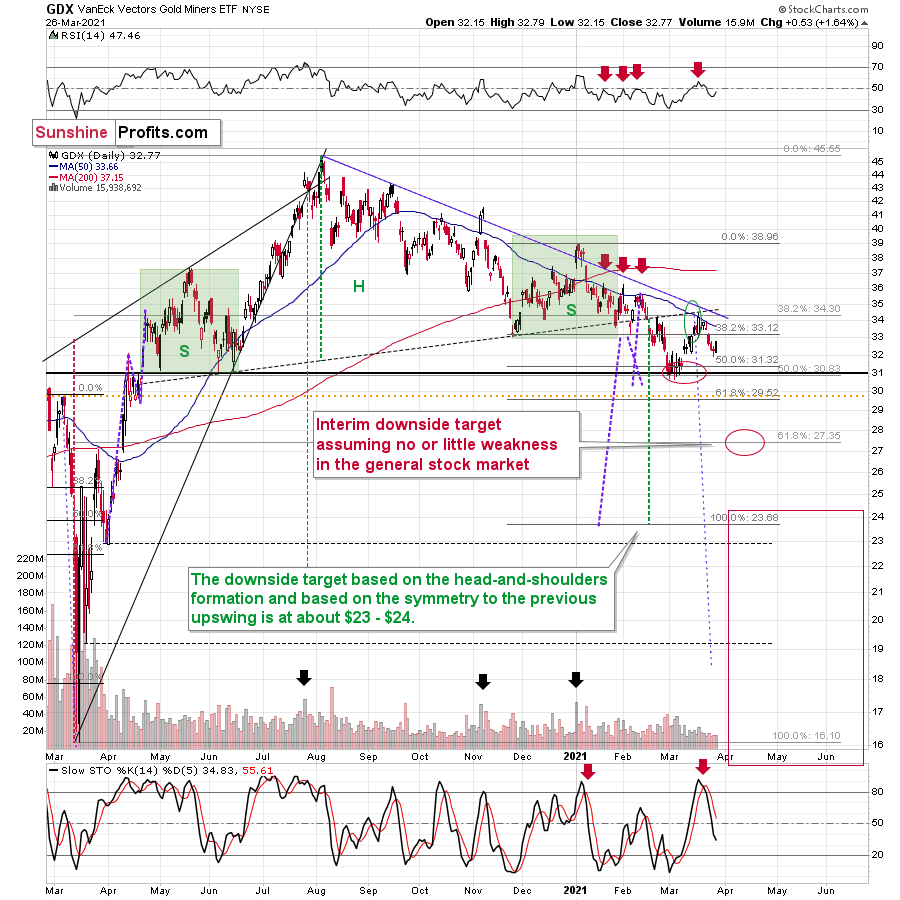

The Gold Miners

On Mar. 19, I warned that the GDX ETF was far from The Lion King.

I wrote:

While the recent rally may resemble Mufasa, beneath the surface, the GDX ETF’s tepid price action looks a lot like Simba. Eliciting a sell signal from the stochastic oscillator, a historical reenactment (repeat of the early-2021 performance) could deliver another sharp move lower.

And with the GDX ETF’s juvenile roar failing to scare off the hyenas, the senior miners once again lost plenty of territory.

Please see below:

In contrast, the GDX ETF was in a fighting mood on Friday (Mar. 26). However, with the corrective upswing cemented on relatively low volume, the daily strength is perfectly normal within the context of a medium-term downtrend. Remember, fits and starts were part of the senior miners’ price action back in January, and yet, the GDX ETF is materially lower now than it was then. In fact, Friday’s rally was even smaller than the late-February corrective upswing.

Please see below:

For context, I wrote on Mar. 26:

After breaking below the rising red support line and declining quite visibly despite gold’s back-and-forth trading, miners finally reached a support level that could trigger something other than more declines.

I marked this support level with black, dashed line. It’s based on the early-March high, the price gap that we saw shortly thereafter, and on the March 12 intraday low. A triple support level might seem like a very big deal, but let’s keep in mind that all these support levels are of very short-term nature. Consequently, if they are going to trigger a rebound, it’s likely to be of very short-term nature as well.

And why am I so confident about the medium-term outlook? Because of the long-term indications for the USD Index, the massive rally in the long-term rates, and because of all the factors that I’ve been describing so far today and that I will describe yesterday.

But one of the short-term reasons (that’s not as important as the other ones, but still) is the shape of the early-January slide - it mirrors today’s price action. Back in January, the GDX ETF recorded a material daily rally, consolidated, then sunk like a stone. Because of that, a few days of back-and-forth trading (consolidation) is nothing to write home about.

To explain, I wrote on Mar. 18:

The GDX ETF encountered the strongest combination of resistance areas, while the Stochastic indicator moved above the 80-level. Technically, the situation is now much more bearish in the GDX ETF chart than it was at the beginning of the year. Back in January, the GDX ETF was only at the declining blue resistance line.

Now, in addition to being very close to the above-mentioned line it’s also at:

- The neck level of the previously broken broad head and shoulders pattern

- The 50-day moving average

- The previous (late-February) highs.

But if we’re headed for a GDX ETF cliff, how far could we fall?

Well, there are three reasons why the GDX ETF might form an interim bottom at roughly ~$27.50 (assuming no big decline in the general stock market):

- The GDX ETF previously bottomed at the 38.2% and 50.0% Fibonacci retracement levels. And with the 61.8% level next in line, the GDX ETF is likely to garner similar support.

- The GDX ETFs late-March 2020 high should also elicit buying pressure.

- If we copy the magnitude of the late-February/early-March decline and add it to the early-March bottom, it corresponds with the GDX ETF bottoming at roughly $27.50.

Keep in mind though: if the stock market plunges, all bets are off. Why so? Well, because when the S&P 500 plunged in March 2020, the GDX ETF moved from $29.67 to below $17 in less than two weeks. As a result, U.S. equities have the potential to make the miners’ forthcoming swoon all the more painful. Conversely, if gold forms an interim bottom close to $1,600, the miners could enjoy a corrective upswing. However, at this point, it’s still too early to tell.

Also supporting the potential move, the GDX ETF’s head and shoulders pattern – marked by the shaded green boxes above – signals further weakness ahead.

I wrote previously:

The most recent move higher only made the similarity of this shoulder portion of the bearish head-and-shoulders patternto the left shoulder) bigger. This means that when the GDX breaks below the neck level of the pattern in a decisive way, the implications are likely to be extremely bearish for the next several weeks or months.

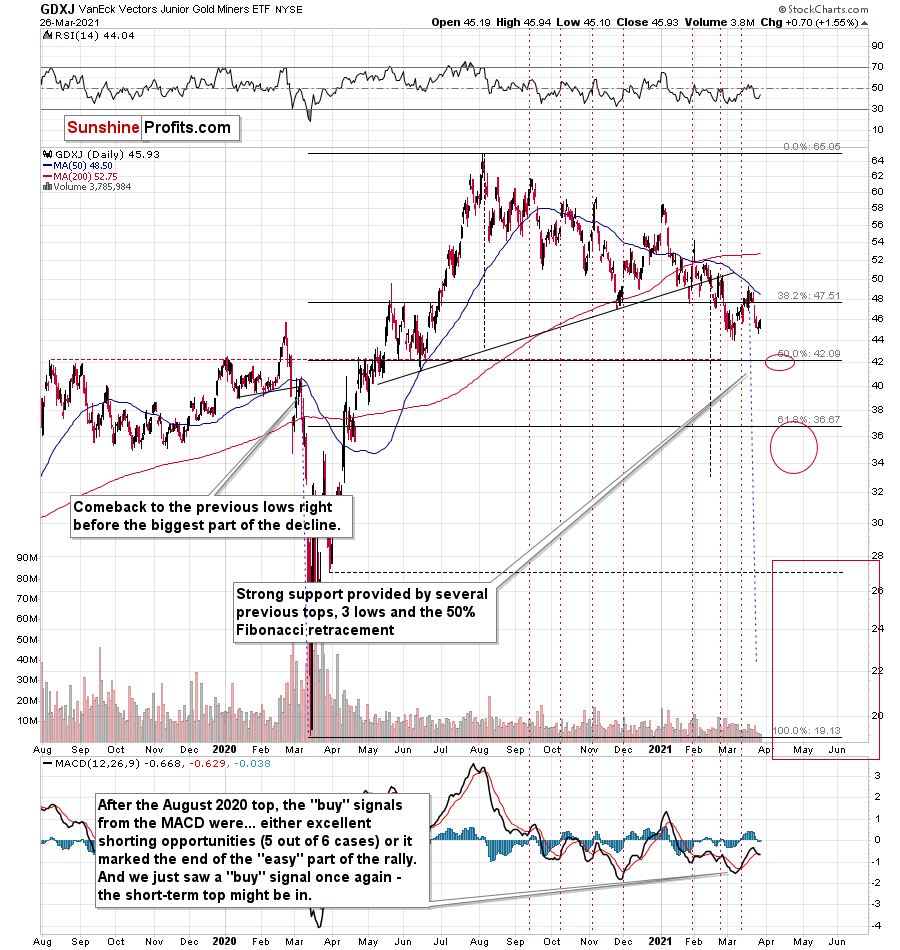

Turning to the junior gold miners, the GDXJ ETF will likely be the worst performer during the upcoming swoon. Why so? Well, due to its strong correlation with the S&P 500, a swift correction of U.S. equities will likely sink the juniors in the process.

What’s more, erratic signals from the MACD indicator epitomizes the GDXJ ETF’s heightened volatility.

Please see below:

To explain, I wrote on Mar. 12:

The above chart is a big red warning flag for beginner investors. The flag reads: “verify the efficiency of a given tool on a given market, before applying it”.

The bottom part of the above chart features theMACD indicator. Normally, when the indicator line (black) crosses its signal line (red), we have a signal. If it’s moves above the signal line, it’s a buy sign, and if it moves below it, it’s a sell sign.

But.

If one actually looks at what happened after the previous “buy signals” in the recent months, they will see that in 5 out of 6 cases, these “buy signals” practically marked the exact tops, thus being very effective sell signals! In the remaining case, it was a good indication that the easy part of the corrective upswing was over.

I’m not only describing the above due to its educational value, but because we actually saw a “buy signal” from the MACD, which was quite likely really a sell signal.

Remember though: the MACD indicator is far from a light switch. While false buy signals often precede material drawdowns, the reversals don’t occur overnight. As a result, it’s perfectly normal for the GDXJ ETF to trade sideways or slightly higher for a few days before moving lower.

But how low could the GDXJ ETF go?

Absent an equity rout, the juniors could form an interim bottom in the $34 to $36 range. Conversely, if stocks show strength, juniors could form the interim bottom higher, close to the $42.5 level. For context, the above-mentioned ranges coincide with the 50% and 61.8% Fibonacci retracement levels and the GDXJ ETF’s previous highs (including the late-March/early-April high in case of the lower target area). Thus, the S&P 500 will likely need to roll over for the weakness to persist beyond these levels.

Some people (especially the permabulls that have been bullish on gold for all of 2021, suffering significant losses – directly and in missed opportunities) will say that the final bottom is already in. And this might very well be the case, but it seems highly unlikely to me. On a side note, please keep in mind that I’m neither a permabull nor a permabear for the precious metals sector, nor have I ever been. Let me emphasize that I’m currently bearish (for the time being), but earlier this month, we went long mining stocks on March 4 and exited this profitable trade on March 11.

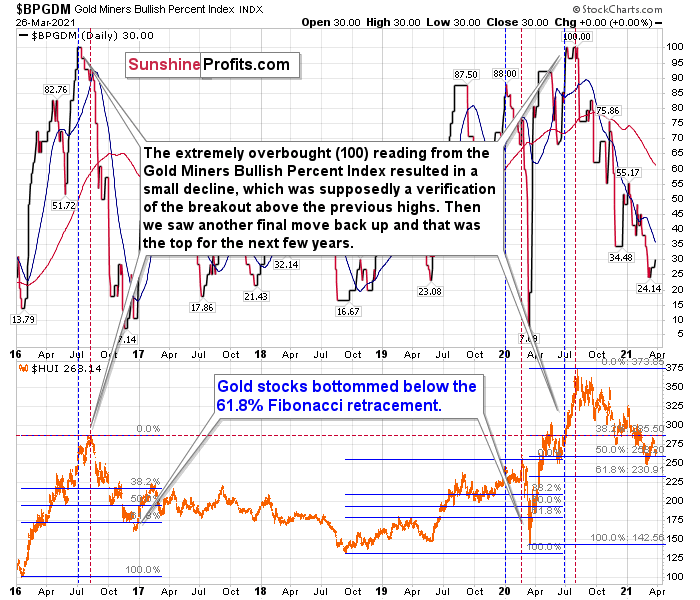

As another reliable indicator (in addition to the myriads of signals coming not only from mining stocks, but from gold, silver, USD Index, stocks, their ratios, and many fundamental observations) the Gold Miners Bullish Percent Index ($BPGDM) isn’t at levels that elicit a major reversal. The Index is now back at 30. However, far from a medium-term bottom, the latest reading is still more than 20 points above the 2016 and 2020 lows.

Back in 2016 (after the top), and in March 2020, the buying opportunity didn’t present itself until the $BPGDM was below 10.

Thus, with sentiment still relatively elevated, it will take more negativity for the index to find the true bottom.

The excessive bullishness was present at the 2016 top as well and it didn’t cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

Please note that back in 2016, there was an additional quick upswing before the slide and this additional upswing had caused the $BPGDM to move up once again for a few days. It then declined once again. We saw something similar also in the middle of 2020. In this case, the move up took the index once again to the 100 level, while in 2016 this wasn’t the case. But still, the similarity remains present.

Back in 2016, when we saw this phenomenon, it was already after the top, and right before the big decline. Based on the decline from above 350 to below 280, we know that a significant decline is definitely taking place.

But has it already run its course?

Well, in 2016 and early 2020, the HUI Index continued to move lower until it declined below the 61.8% Fibonacci retracement level. The emphasis goes on “below” as this retracement might not trigger the final bottom. Case in point: back in 2020, the HUI Index undershot the 61.8% Fibonacci retracement level and gave back nearly all of its prior rally. And using the 2016 and 2020 analogues as anchors, this time around, the HUI Index is likely to decline below 231. In addition, if the current decline is more similar to the 2020 one, the HUI Index could move to 150 or so, especially if it coincides with a significant drawdown of U.S. equities.

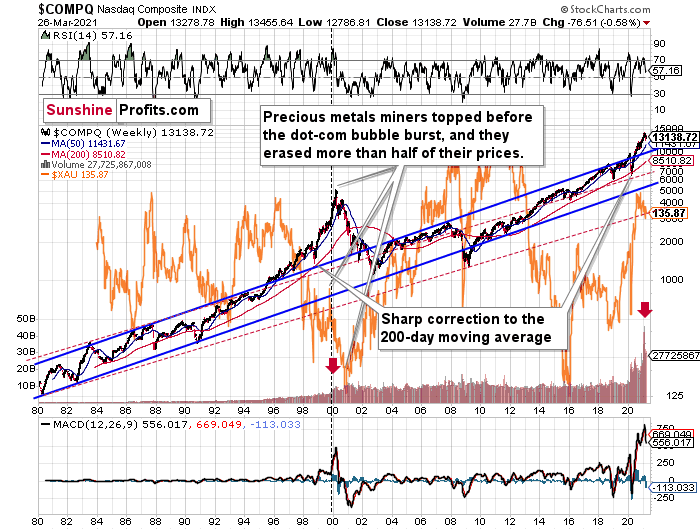

Circling back to the NASDAQ Composite, the unwinding of excessive speculation could deliver a fierce blow to the gold miners. Case in point: when the dot-com bubble burst in 2000, the NASDAQ lost nearly 80% of its value, while the gold miners lost more than 50% of their value.

Please see below:

Right now, the two long-term channels above (the solid blue and red dashed lines) show that the NASDAQ is trading well above both historical trends.

Back in 1998, the NASDAQ’s last hurrah occurred after the index declined to its 200-day moving average (which was also slightly above the upper border of the rising trend channel marked with red dashed lines).

And what happened in the first half of 2020? Well, we saw an identical formation.

The similarity between these two periods is also evident if one looks at the MACD indicator. There has been no other, even remotely similar, situation where this indicator would soar so high.

Furthermore, and because the devil is in the details, the gold miners’ 1999 top actually preceded the 2000 NASDAQ bubble bursting. It’s clear that miners (the XAU Index serves as a proxy) are on the left side of the dashed vertical line, while the tech stock top is on its right side. However, it’s important to note that it was stocks’ slide that exacerbated miners’ decline. Right now, the mining stocks are already declining, and the tech stocks continue to rally. Two decades ago, tech stocks topped about 6 months after miners. This might spoil the party of the tech stock bulls, but miners topped about 6 months ago…

Also supporting the 2000 analogue, today’s volume trends are eerily similar. If you analyze the red arrows on the chart above, you can see that the abnormal spike in the MACD indicator coincided with an abnormal spike in volume. Thus, mounting pressure implies a cataclysmic reversal could be forthcoming.

Interestingly, two decades ago, miners bottomed more or less when the NASDAQ declined to its previous lows, created by the very first slide. We have yet to see the “first slide” this time. But, if the history continues to repeat itself and tech stocks decline sharply and then correct some of the decline, when they finally move lower once again, we might see THE bottom in the mining stocks. Of course, betting on the above scenario based on the XAU-NASDAQ link alone would not be reasonable, but if other factors also confirm this indication, this could really take place.

Either way, the above does a great job at illustrating the kind of link between the general stock market and the precious metals market that I expect to see also this time. PMs and miners declined during the first part of the stocks’ (here: tech stocks) decline, but then they bottomed and rallied despite the continuation of stocks’ freefall.

Even more ominous, the MACD indicator is now flashing a clear sell signal. And because the current reading is analogous to the one that preceded the dot-com bust, the NASDAQ Composite – and indirectly, the PMs – continue to sail toward the perfect storm.

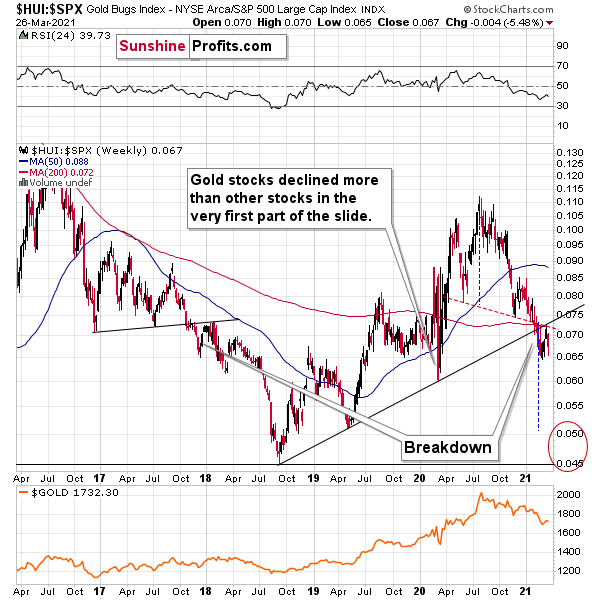

Further validating bearish picture for the mining stocks, the HUI Index/S&P 500 ratio has already broken below critical support, and this breakdown was verified.

Please see below:

When the line above is rising, it means that the HUI Index is outperforming the S&P 500. When the line above is falling, it means that the S&P 500 is outperforming the HUI Index. If you analyze the right side of the chart, you can see that the ratio has broken below its rising support line. For context, the last time a breakdown of this magnitude occurred, the ratio plunged from late-2017 to late-2018. Thus, the development is profoundly bearish.

Playing out as I expected, a sharp move lower was followed by a corrective upswing back to the now confirmed breakdown level (which is now resistance). More importantly though, last week’s rejection, combined with the ratio’s move back toward its previous lows, is profoundly bearish for the miners.

Why so?

Well, mirroring the behavior that we witnessed in early 2018, after breaking below its rising support line, the HUI Index/S&P 500 ratio rallied back to the initial breakdown level (which then became resistance) before suffering a sharp decline. And with two-thirds of the analogue already complete, the current move lower still has plenty of room to run. Likewise, the early-2018 top in theHUI Index/S&P 500 ratio is precisely when the USD Index began its massive upswing. Thus, with history likely to rhyme, the greenback could spoil the miners’ party once again.

As well, please note that the HUI to S&P 500 ratio broke below the neck level (red, dashed line) of a broad head-and-shoulders pattern and it verified this breakdown by moving temporarily back to it. The target for the ratio based on this formation is at about 0.05 (slightly above it). Consequently, if the S&P 500 doesn’t decline at all (it just closed the week at 3913.10), the ratio at 0.05 would imply the HUI Index at about 196. However, if the S&P 500 declined to about 3,200 or so (its late-2020 lows) and the ratio moved to about 0.05, it would imply the HUI Index at about 160 – very close to its 2020 lows.

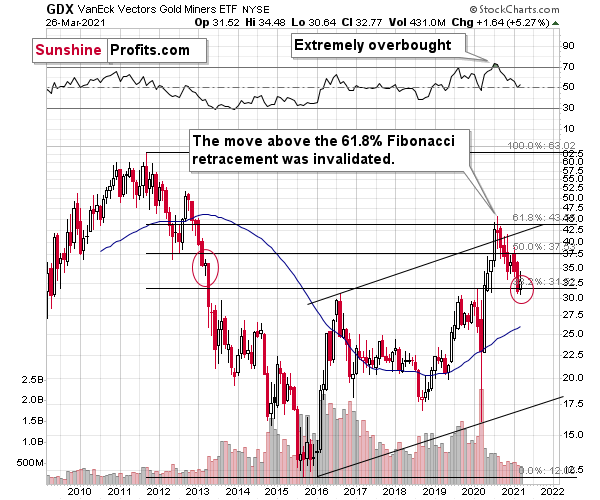

Also medium-term bearish, it’s important to remember that in mid-2020, the GDX ETF invalidated its long-term breakout above the 61.8% Fibonacci retracement level (based on the 2011 to 2016 decline).

Please see below:

To explain, I wrote previously:

When GDX approached its 38.2% Fibonacci retracement, it declined sharply – it was right after the 2016 top. And miners’ inability to move above the 61.8% Fibonacci retracement level and their invalidation of the tiny breakout is a bearish sign. The same goes for miners’ inability to stay above the rising support line – the line that’s parallel to the line based on the 2016 and 2020 lows.

Finally, keep in mind that the similarity between how miners declined in 2013 also remains intact and the red ellipses marked on the above chart show that a short-term pause is a normal part of even the biggest declines. Consequently, a corrective upswing doesn’t have to mean much, if anything, from the medium-term point of view.

Gold

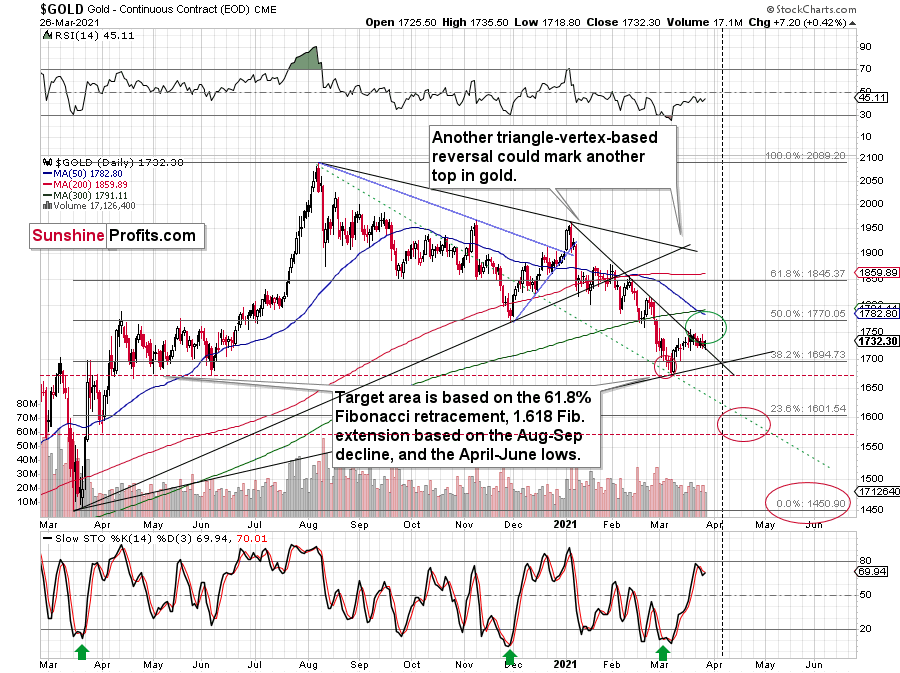

Offering an olive branch to bulls and bears, holding above its declining resistance line (which is now support) is clearly bullish for gold. However, the yellow metal’s overture has yet to be confirmed and the breakout doesn’t invalidate the bearish implications over the medium term.

What breakout, you might ask? Gold closed the week slightly above the declining resistance line, which – while small – it still a breakout. This is a bullish development.

Please see below:

Given the mixed signals, the yellow metal could deliver a short-term bounce to ~$1,770 (the 50% Fibonacci retracement level) However, gold’s triangle-vertex-based reversal point (which I warned about previously and preceded the yellow metal’s prior swoon) originally set the table for a corrective rally in early April. However, let’s keep in mind that it could be actually a near-term top that is then followed by the powerful decline.

To explain, while a corrective upswing could (doesn’t have to) occur, ~$1,770 also coincides with gold’s 50-day MA (which should act as resistance).

Will we see gold rally from here? The jury remains out.

At the moment of writing these words, gold is trading once again very close to the previously broken line, ready to invalidate the breakout. If it does invalidate it (by moving below $1,725), then the bullish potential created by Friday’s rally will be gone.

Does the possibility (!) of seeing a temporary upswing imply that it’s a good idea to close our short positions? I don’t think so. In my view, the risk of missing the decline is too big and the situation in the USD Index is too bullish right now, to justify this action.

So, if a short-term bounce doesn’t take place, where could we be headed shortly?

Well, the 76.4% Fibonacci retracement level (it’s visible as the 23.6% Fibonacci retracement level on the above chart as inverting the scale is used as a workaround) also coincides with gold’s April 2020 low. Taken together, an interim bottom could form in the ~$1,575 to $1,600 range.

For context, back in early March, the yellow metal continued to decline after reaching the 61.8% Fibonacci retracement (visible as 38.2% Fibonacci retracement) level, while in contrast, the miners began to consolidate. Gold finally bottomed slightly below the retracement – at its previous lows. This time around, we might witness a similar event. And while the story plays out, the miners’ relative strength should signal the end of the slide (perhaps with gold close to 1,600), while gold will likely garner support sometime thereafter (at $1,575 – $1,580 or so).

Remember though: this is only an interim target. Over the medium term, the yellow metal will likely form a lasting bottom in the ~$1,450 to $1,500 range.

And why is that?

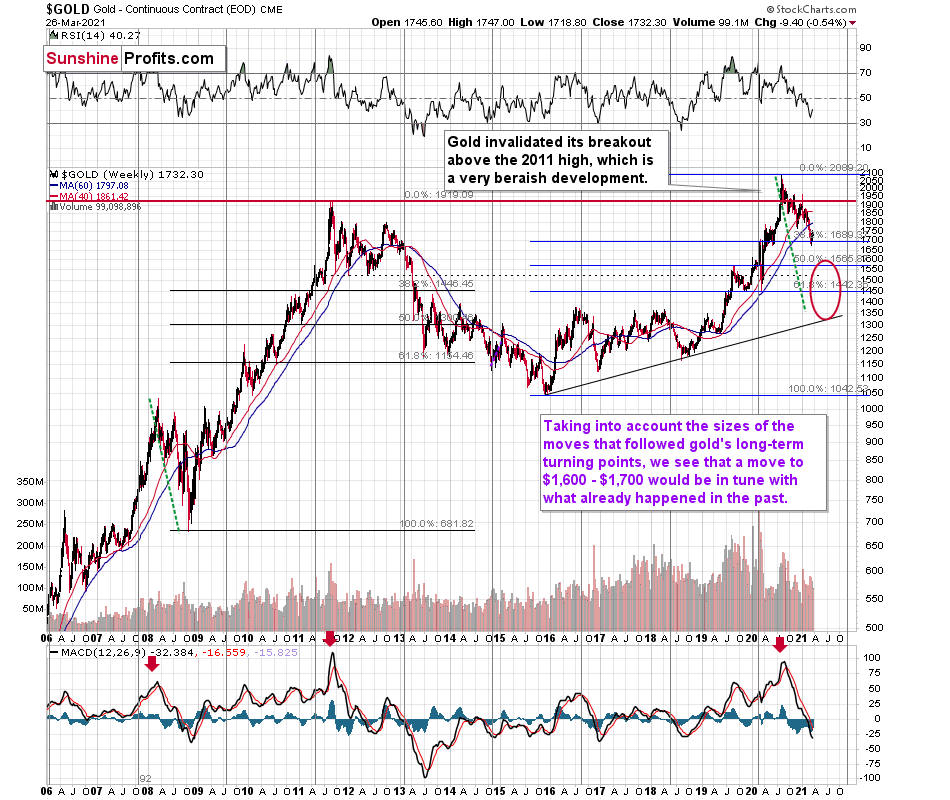

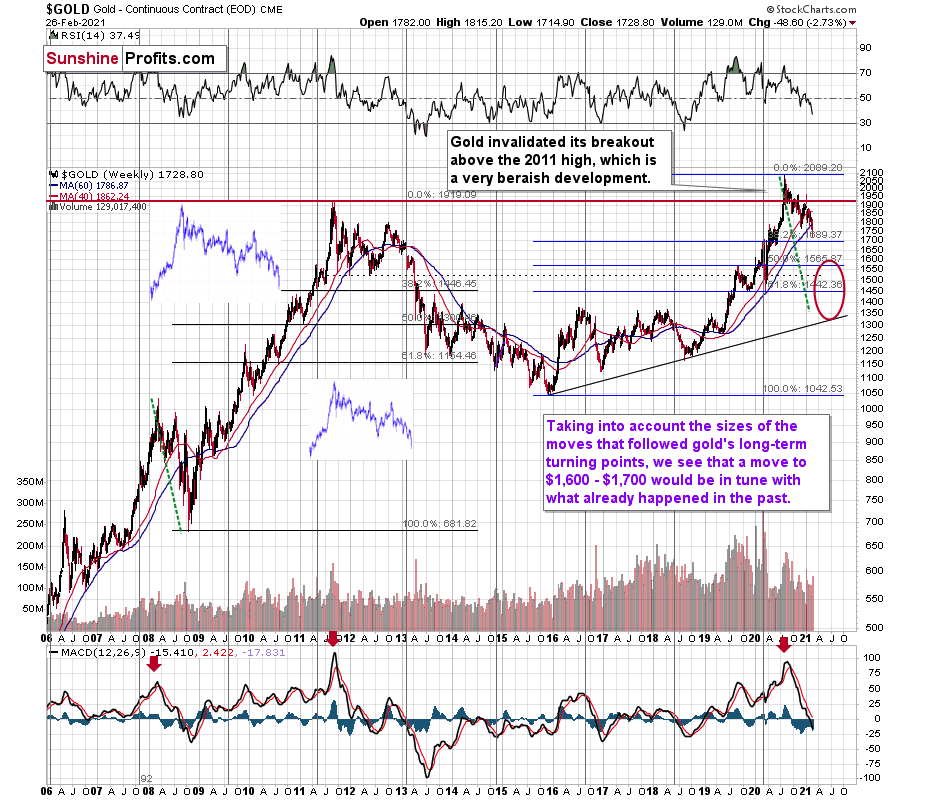

Well, if you analyze the long-term chart below, you can see that the yellow metal has invalidated the breakout above its 2011 high. More importantly though, with its rising support line (on the right side of the chart) also coinciding with the 61.8% Fibonacci retracement level and the 2019 and 2020 lows, ~$1,450 to $1,500 is the most prudent medium-term price target.

Conversely, if the 2008 analogue repeats – and a crisis of confidence erupts across U.S. equities – the PMs could move substantially lower. When combining an equity shock with a USD Index resurgence, the yellow metal could bottom at roughly $1,400 (or even ~$1,350). Similarly, while the MACD indicator (on gold’s 40-year chart near the top of today’s edition) signals a bottom in the ~$1,200 to ~1,350 range, to be perfectly clear, ~$1,450 to $1,500 is the most likely outcome.

For more context, I wrote previously:

If you analyze the red arrow in the lower part of the above chart (the weekly MACD sell signal), today’s pattern is similar not only to what we saw in 2011, but also to what we witnessed in 2008. Thus, if similar events unfold – with the S&P 500 falling and the USD Index rising (both seem likely for the following months, even if these moves don’t start right away) – the yellow metal could plunge to below $1,350 or so. The green dashed line shows what would happen gold price, if it was not decline as much as it did in 2008.

As it relates to the chart below, relative to 2011-2013, today’s price action is a splitting image. For starters, gold invalidated the breakout above its 2011 highs. Invalidations of breakouts are sell signals, and it’s tough to imagine a more profound breakout that could have failed.

Second, if you analyze the two white boxes (on the left side of the chart), the blue lines depict today’s short-term price action relative to 2013. As you can see, the movement is nearly identical. I copied the price performance twice, so that you can more easily see the similarity in terms of both the price and time.

Please note that gold delivered a final corrective rebound from the previous lows (so called dead cat bounce) before suffering its current weakness. And in 2013, the yellow metal did the exact same thing. As a result, the free-fall phase has already begun, and the medium-term trend remains down.

For more context, I wrote previously:

The odd thing about the above chart is that I copied the most recent movement in gold and pasted it above gold’s 2011 – 2013 performance. But – admit it – at first glance, it was clear to you that both price moves were very similar.

And that’s exactly my point. The history tends to rhyme and that’s one of the foundations of the technical analysis in general. Retracements, indicators, cycles, and other techniques are used based on this very foundation – they are just different ways to approach the recurring nature of events.

However, every now and then, the history repeats itself to a much greater degree than is normally the case. In extremely rare cases, we get a direct 1:1 similarity, but in some (still rare, but not as extremely rare) cases we get a similarity where the price is moving proportionately to how it moved previously. That’s called a market’s self-similarity or the fractal nature of the markets. But after taking a brief look at the chart, you probably instinctively knew that since the price moves are so similar this time, then the follow-up action is also likely to be quite similar.

In other words, if something looks like a duck, and quacks like a duck, it’s probably a duck. And it’s likely to do what ducks do.

What did gold do back in 2013 at the end of the self-similar pattern? Saying that it declined is true, but it doesn’t give the full picture - just like saying that the U.S. public debt is not small. Back then, gold truly plunged. And before it plunged, it moved lower in a rather steady manner, with periodic corrections. That’s exactly what we see right now.

Please note that the above chart shows gold’s very long-term turning points (vertical lines) and we see that gold topped a bit after it (not much off given their long-term nature). Based on how gold performed after previous long-term turning points (marked with purple, dashed lines), it seems that a decline to even $1,600 would not be out of ordinary.

Finally, please note the strong sell signal from the MACD indicator in the bottom part of the chart. The only other time when this indicator flashed a sell signal while being so overbought was at the 2011 top. The second most-similar case is the 2008 top.

The above-mentioned self-similarity covers the analogy to the 2011 top, but what about the 2008 performance?

If we take a look at how big the final 2008 decline was, we notice that if gold repeated it (percentage-wise), it would decline to about $1,450. Interestingly, this would mean that gold would move to the 61.8% Fibonacci retracement level based on the entire 2015 – 2020 rally. This is so interesting, because that’s the Fibonacci retracement level that (approximately) ended the 2013 decline.

History tends to rhyme, so perhaps gold is going to decline even more than the simple analogy to the previous turning points indicates. For now, this is relatively unclear, and my target area for gold’s final bottom is quite broad.

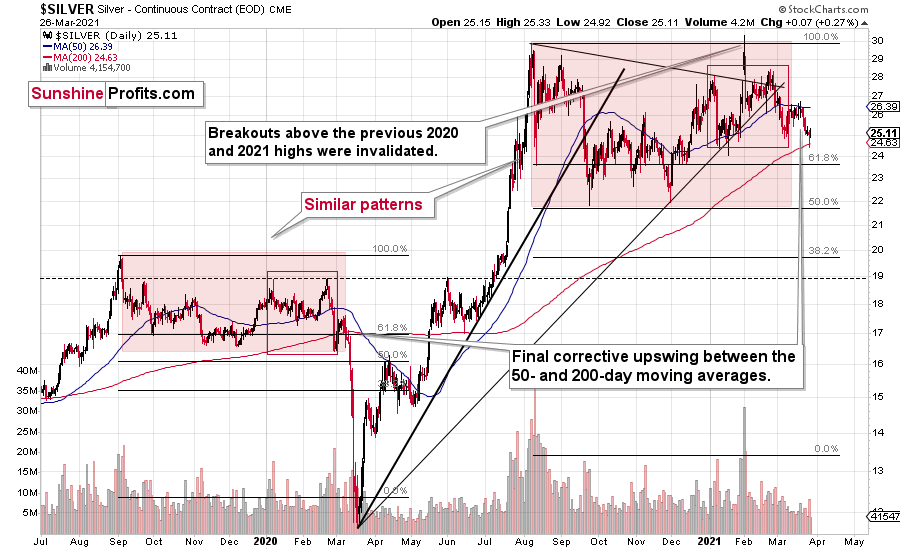

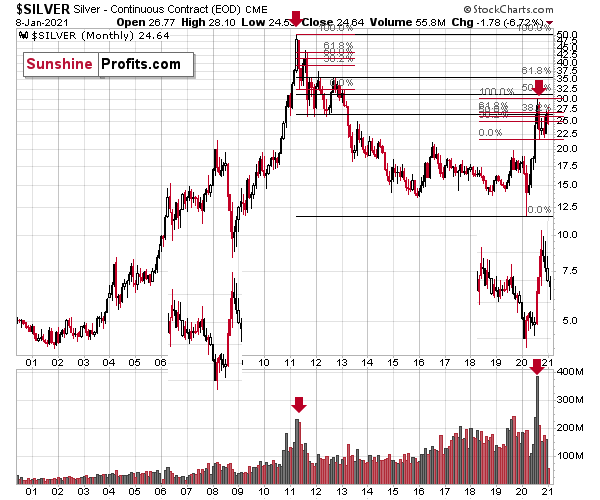

Silver

With silver’s horsepower all noise and no muscle, I warned on Mar. 19 that the white metal’s smooth ride would likely break down in the near future.

I wrote:

Today’s price action mirrors what we witnessed in the second half of 2019 and early 2020 – before silver suffered a sharp decline: silverdeclined substantially, delivered a short-term corrective upswing and then collapsed.

And while the white metal is still in the early inning of delivering on the trifecta, last week’s price action is likely a taste of what’s to come.

Please see below:

Despite the bullish implications of reversing a daily slide on relatively high volume on Mar. 25, the glimmer of hope is far from sunshine. With silver’s self-similarity pattern continuing to play out, the short-term strength will likely be short lived.

Case in point: if you analyze the red box below (on the left within the shaded area), you can see that in 2020, a sharp move higher was followed by a sharp move lower, a slight move higher, then a medium-term collapse. And because waves one and two have already occurred in 2021 (within the second red box on the right), a short-term corrective upswing could be next in line before silver’s medium-term collapse. OR it could be the case that the early-March rally was already the move that was analogous to the early-March-2020 rally and the next big downswing is about to start.

In similar fashion, if you analyze the red box on the 2008 chart below, you can see that an immaterial bounce also occurred right before silver fell off a cliff.

To explain, I wrote on Mar. 17:

The final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

If this self-similar pattern is indeed materializing, then the implications are very bearish, and we can expect a major downturn any day or week now.

Let’s be realistic - so far, the analogy might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

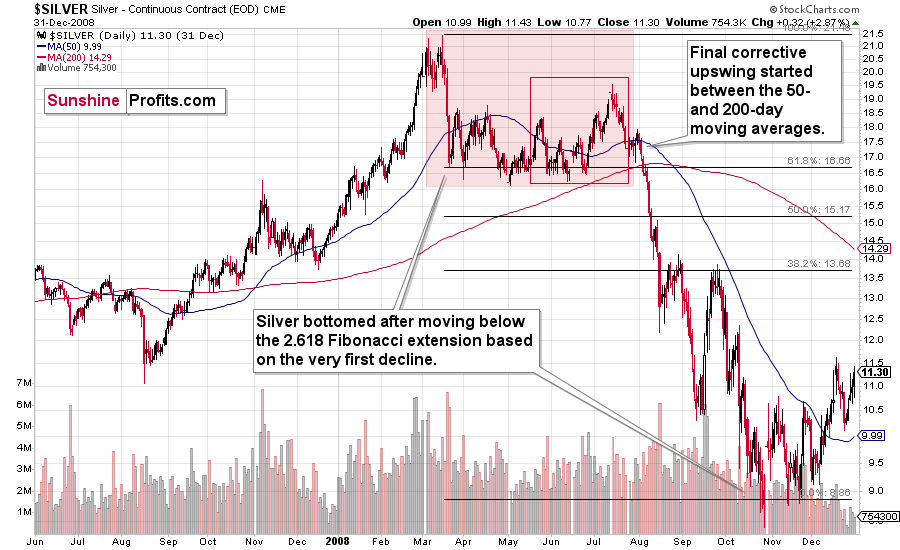

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

Before summarizing, please note silver’s tendency to decline sharply in March – that’s what happened in 2008 and 2020. Even if the entire self-similar pattern doesn’t continue, based on this seasonality, silver is likely to decline soon, anyway.

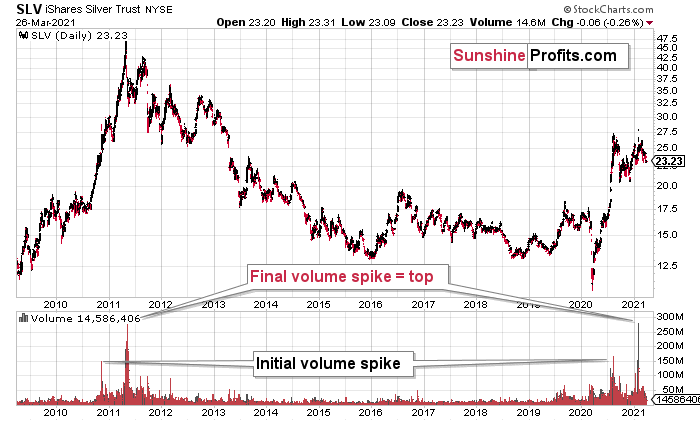

Highlighting the effect of WallStreetBets’ #SilverSqueeze, the SLV ETF’s volume spikes in 2020/2021 were nearly identical to the surges that we witnessed ~10 years ago. If you analyze the chart below, you can see that the massive inflows at the end of 2012 were not the beginning of a medium-term upswing. In fact, they coincided with silver’s final bounce before the white metal suffered a major decline.

Please see below:

To explain, I wrote previously:

If you analyze the volume spikes at the bottom of the chart, 2021 and 2011 are a splitting image. To explain, in 2011, an initial abnormal spike in volume was followed by a second parabolic surge. However, not long after, silver’s bear market began.

SLV-volume-wise, there's only one similar situation from the past - the 2011 top. This is a very bearish analogy as higher prices of the white metal were not seen since that time, but the analogy gets even more bearish. The reason is the "initial warning" volume spike in this ETF. It took place a few months before SLV formed its final top, and we saw the same thing also a few months ago, when silver formed its initial 2020 top.

The history may not repeat itself to the letter, but it tends to be quite similar. And the more two situations are alike, the more likely it is for the follow-up action to be similar as well. And in this case, the implications for the silver price forecast are clearly bearish.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

Similarly, silver’s inverse price action also has bearish implications. Nearly identical to the inverted formation that emerged from 2006 to 2009, today’s chart looks eerily similar to its predecessor.

While it’s more of a wild card, the above pattern shows that silver’s 2020 top plots nearly identical to the inverse of the 2006-2009 performance. I copied the 2006 – 2009 performance right below the regular price movement and I inverted it, and I also copied this inverted pattern to the last few years.

The similarity is quite significant. And whenever a given pattern has been repeated, the odds are that it could also repeat in the not-too-distant future. Of course, there is no guarantee for that, but once the same market has reacted in a certain way to a specific greed/fear combination, it can just as well do it again. And these similarity-based techniques work quite often. So, while it’s not strong enough to be viewed as a price-path-discovery technique on its own, it should make one consider some scenarios more closely. In particular, this means that the declines in the prices of silver, gold, and mining stocks could be bigger and take longer than it seems based on other charts and techniques.

The above is also in tune with the implications of the sell signal from the MACD indicator on the monthly gold chart.

The only thing that comes to my mind, which could – realistically – trigger such a prolonged decline would be a major drop in the general stock market. Given what I wrote above, the latter is quite possible, so I’ll be on the lookout for confirmations and invalidations of this scenario.

If history rhymes, silver could be in for a profound decline over the next few months (beyond my initial target). Moreover, the development would increase the duration of a precious metals’ bear market (also beyond my initial forecast).

After all, gold did invalidate its long-term breakout above the 2011 highs and the way gold reacted to a small upswing in the USD Index was truly profound…

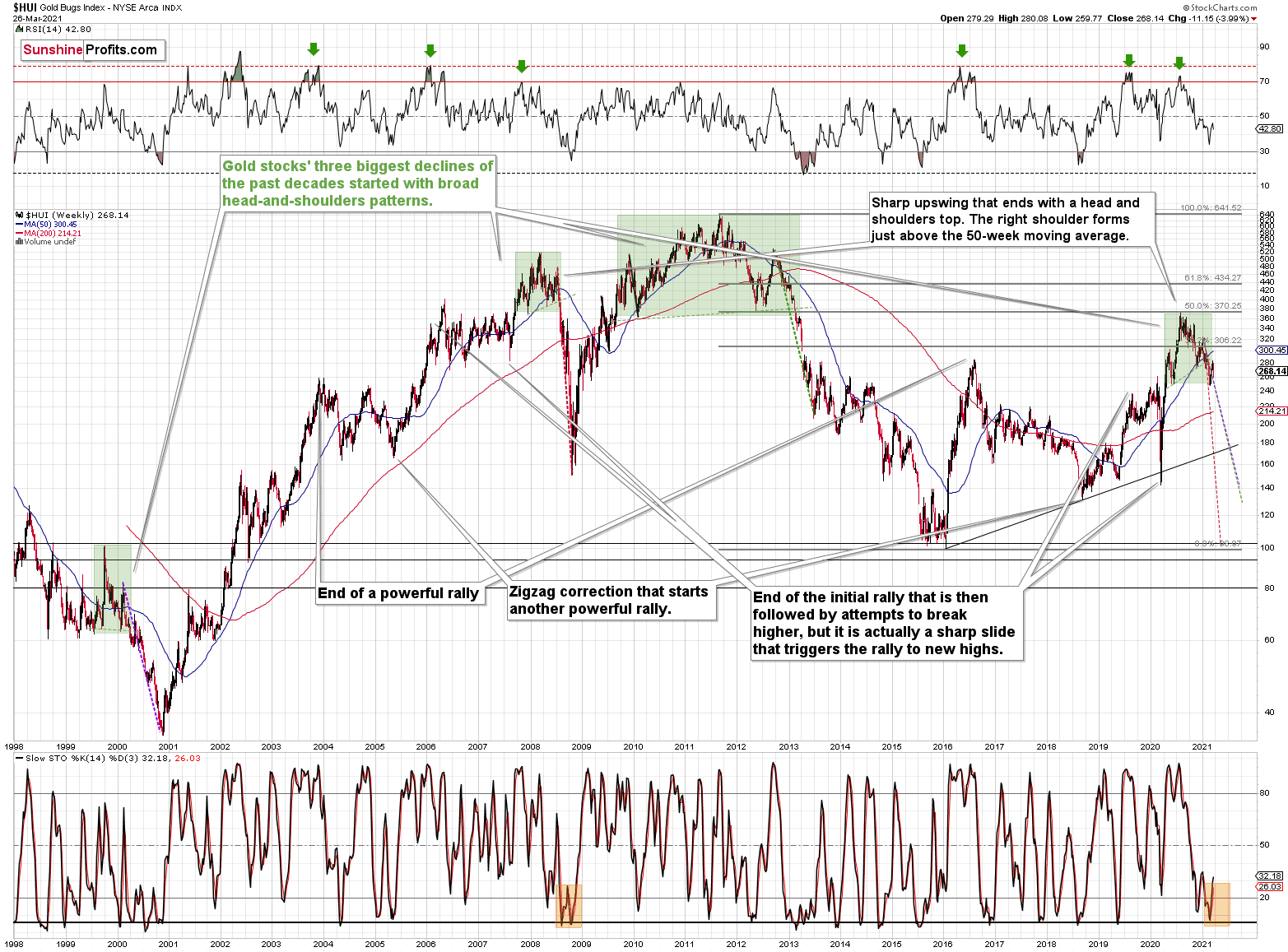

Moving on to the HUI Index (a proxy for gold stocks), it’s also flashing red in a very bright way – especially from a medium-term perspective.

If you analyze the bottom-half of the chart below, you can see that the stochastic oscillator’s current reading mirrors the reading from 2008 (marked by the two areas shaded orange). Back then, an initial spike in the stochastic oscillator was followed by a swift move lower for both the indicator and the HUI Index. And because today’s reading is nearly identical, a similar reversal could reemerge in the coming weeks, days, or hours.

For more context, I wrote previously:

The three of the biggest declines in the mining stocks (I’m using the HUI Index as a proxy here), all started with broad, multi-month head-and-shoulders patterns. And now we’re seeing this pattern all over again.

The above picture should make it clear why I was putting “at least” in bold, when describing the targets based on the head-and-shoulders patterns.

In all three cases, the size of the decline exceeded the size of the head of the pattern. This means that the $24 target on the GDX ETF chart is likely conservative.

Can we see gold stocks as low as we saw them last year? Yes.

Can we see gold stocks even lower than at their 2020 lows? Again, yes.

Of course, it’s far from being a sure bet, but the above chart shows that it’s not irrational to expect these kind of price levels before the final bottom is reached.

The dashed lines starting at the 2020 top are copies of sizes of the declines that started from the right shoulder of the previous patterns. If things develop as they did in 2000 and 2012-2013, gold stocks are likely to bottom close to their 2020 high. However, if they develop like in 2008 (which might be the case, given the extremely high participation of the investment public in the stock market and other markets), gold stocks could re-test (or break slightly below) their 2016 low.

I know, I know, this seems too unreal to be true… But wasn’t the same said about silver moving below its 2015 bottom in 2020? And yet, it happened.

While describing gold’s very long-term chart, I wrote that based on gold’s MACD indicator, the situation is also similar to what happened in 2008. The above chart shows some additional similarities. Let’s consider the sizes of moves between the 2004 bottom (one could argue that this is when the several-year-long rally started) and the 2008 top, between the initial 2006 top and the 2008 top, and between the very beginning of the final rally – at the end of the fake sharp downswing and the 2008 top.

I marked all of them with dashed lines and I copied them to the current situation. By “current” I mean what happened recently and in the previous years – to the situations that seemed analogous to the ones described above. For instance, the near-vertical 2020 downswing that was followed by a big rally that ended with a big head-and-shoulders top seems similar to what happened in mid-2007.

As one might expect, these dashed lines don’t point to the same price top. No wonder – the history doesn’t repeat itself to the letter, as the circumstances are not identical.

But…

What is remarkable is that on average, these dashed lines did a great job at approximately (!) pinpointing the end of the entire rally and the start of the next massive move lower. One of these three dashed lines is several months too early, one is several months too late, and one is almost exactly pointing to the 2020 top.

This makes the current situation even more similar to what happened in 2008, which has profoundly bearish implications for the entire precious metals sector. I provided more details of this analogy in the Feb. 17 Gold & Silver Trading Alert (please be sure to read the part about similarities to 2008 in the HUI Index, if you haven’t done so already).

And continuing to rhyme, the gold miners are still following the 2008 analogue (even more than the 2013 analogue). If you analyze the dotted red line above (on the right side of the chart), it shows just how quickly the miners could decline should the 2008 analogue play out in full. However, to fully align with 2008, there is still plenty of room to move lower. There are likely to be very brief corrections along the way, just like there were corrections during the 2008 slide, but overall, it seems that the mining stocks are headed much lower and the buy signal from the stochastic indicator should be viewed as very short-term phenomena only.

As for the role of equities, I wrote previously:

A move of this magnitude most likely requires equities to participate. In 2008 and 2020, the sharp drawdowns in the HUI Index coincided with significant drawdowns of the S&P 500. However, with the words ‘all-time high’ becoming commonplace across U.S. equities, the likelihood of a three-peat remains relatively high.

With that said: how will we know when a medium-term buying opportunity presents itself?

We view price target levels as guidelines and the same goes for the Gold Miners Bullish Percent Index (below 10), but the final confirmation will likely be gold’s strength against the ongoing USDX rally. At many vital bottoms in gold, that’s exactly what happened, including the March bottom.

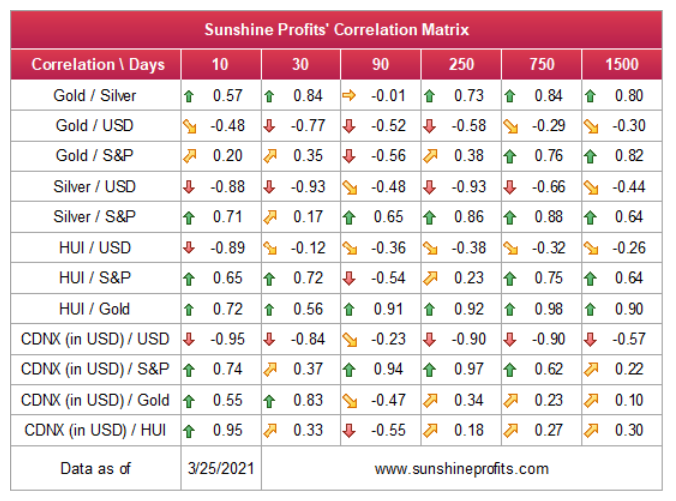

Turning to cross-asset correlations, gold, silver and the HUI Index’s 10-day correlations have stabilized in a logical manner. Exhibiting positive relationships with the S&P 500 and negative relationships with the U.S. dollar, their behavior is akin to what we see over a 250-day period (a reliable length of time). Similarly, the groups’ 30-day correlations are also trending in sensible directions. As a result, and given the PMs’ negative correlation with the U.S. dollar over the last 10, 30 and 250 days, a forthcoming USD Index uprising will likely haunt the PMs over the medium term.

For more context, I wrote previously:

Since gold, silver, and mining stocks have been strongly negatively correlated with the USD Index in the medium term, it seems likely that they will be negatively affected by the upcoming sizable USDX upswing.

…Until we see the day where gold reverses or soars despite the U.S. currency’s rally.

If that happens with gold at about $1,700, we’ll have a very good chance that this was the final bottom. If it doesn’t happen at that time, or gold continues to slide despite USD’s pause or decline, we’ll know that gold has further to fall.

Naturally we’ll keep you – our subscribers – informed.

To move forward, how does the GDX downside target compare to gold’s downside target? If, at the same time, gold moves to about $1,700 and miners are already after a ridiculously big drop (to $31-$32 in the GDX ETF, or lower), the binding profit-take exit price of your GDX ETF will become $32.02 (those with higher risk tolerance might lower it to $31.15 or so, but moving it lower seems just too risky).

At this time, the final GDX target (the one that would correspond to gold at $1,500 or so) is still unclear. The $17 - $23 area seems probable, especially if the general stock market slides once again. It’s too early to say with any significant level of certainty. Gold is providing us with a clearer final target, so that’s what we’ll focus on. And most importantly – we’ll focus on gold’s performance relative to the USD Index.

Overview of the Upcoming Part of the Decline

- It seems quite likely to me that we are already after the initial bottom and the initial correction. If not, then it seems likely to me that the corrective upswing will be completed within the next 2 weeks (with PMs topping in early April). It’s more likely that the next big move lower is already underway, though.

- After miners slide once again in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver (this could take another 1-2 weeks to materialize). I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,450 - $1,500 and the entire decline (from above $1,700 to about $1,475) would be likely to take place within 1-12 weeks and I would expect silver to fall hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments in my view. This might happen with gold close to $1,475, but it’s too early to say with certainty at this time. In other words, the entire decline could take between 1 and 12 weeks, while silver declines occuring particularly fast in the final 1-2 weeks.

- If gold declines even below $1,500 (say, to ~$1350 or so), then it could take another 10 weeks or so for it to bottom, but this is not what I view as a very likely outcome.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops . If the mid-February 2020 top was the final medium-term top (based on NASDAQ’s top, then it seems that we might expect the precious metals sector to bottom in mid-May or close to May’s end. If, however, the mid-March 2021 top was the final medium-term top (based on the S&P 500), then we might expect the precious metals sector to bottom in mid-June or close to June’s end.

- The above is based on the information available today and it might change in the following days/weeks.

Letters to the Editor

Q: Good day, and hope you are doing well. I have a question: AUXAG is apparently consolidating in a similar symmetric triangle as it did in 2016-2017. It seems that we are in a correction zone. Usually, the symmetric triangle is a continuation pattern. If it breaks this triangle, do you think that we might test 56,8 and later 50,3? The measured target of this symmetric triangle seems to be around 42. Do you see any chance for gold to rally again to $2300-2400 and the XAUXAG drops to 42? At the same time silver could eventually rally to $50?

A: (In other words, would I buy the gold to silver ratio given the possibility, and do I think if gold is now going to be stronger than silver). In short, yes, but I think that a directional trade in the mining stocks provides a better risk to reward ratio. As the general stock market is likely to decline, and as the medium-term decline in the precious metals market is likely coming to an end, silver is likely to fall more than gold, thus pushing the gold to silver ratio higher.

Q: I have a question about timing the PMs. On the ride down I closed my short position, twice, and then resumed the short after the GDX had pulled back, saving myself some draw down. This worked out quite well. My question is: do you ever manage a trade this way or do you simply add to the position at certain junctures? As my account grew, I was able to increase the position size at both times without exceeding the percent of my portfolio I allocated for the trade. I was thinking that ~$31, where we closed the short position and went long, would be a natural place for the GDX to pull back before its final move down.

A: If the corrective move is likely to be more significant (and lasting more than a few days), then I might temporarily adjust the position – just as I did earlier this month (going long on March 4), however I will only do so when more factors point to this move. In my approach I’m not trying to time smaller (or intraday) corrections. Of course, one could do so and use my analyses as a supplementary tool to such a trading strategy.

As far as increasing the sizes of trades is concerned, they are increased automatically in case of each trade as sizes of trades are based on a certain percentage of the entire portfolio. So, as the portfolio grows, so do the positions. In addition to that, I’m describing the position size relative to the size of the normal position (not relative to the size of the entire investment account, of course).

Q: I have a question for PR. As we look for a definitive top in the stock market that will help us to time the subsequent length of the decline in the PM sector, can we also look for clues in the ten-year treasury rate? I have read some analysts say that 1.75% on the 10-year would trigger a decline in equities while others say that it would only trigger more buying by the Fed at the long end of the curve, and quickly reverse any decline into another bull wave advance. Also, with all this debt and record margin, when will the margin clerks overpower the Fed? Thanks so much for the daily insightful commentary and analysis. It's the best!

A: Thank you – I’m very happy to read that you enjoy the result of our work so much. The technical analysis doesn’t work that well in case of the interest rates, because the market is not completely (or even to a major degree) free. Theoretically, the long-term rates are allowed to float freely, but then again, we have Operation Twist and other mechanisms (for example, the forward guidance) that are used to manage (or manipulate, which essentially means something similar, the difference being that one word is negatively loaded on the emotional level and the other is not) the rates.

It seems to me that the Fed’s decisions will have much more to do with the performance of the general stock market and the does-it-make-me-look-stupid principle than with actual data. The Fed might talk about the economic indicators, data-driven decisions and so on and so forth, but ultimately, when are they taking the boldest and most decisive actions? After it is already expected of them, based on what the stock market did (usually after it plunged).

The stock market is currently at all-time highs and the inflation is rising just like the Fed wanted it to – how could the Fed potentially explain the massive yield curve control right now?

It would be much easier for them to wait for the stock market to slide and then take action. The stock market declines every now and then – even if it’s not a huge decline – so all the Fed has to do is to wait. And that’s what I expect to happen – that the Fed will take the wait-and-see approach until stocks slide. And then it will likely introduce the yield curve control mechanisms, but that would likely be after both stocks and the precious metals sector have already declined.

As a reminder, I expect the precious metals market to follow stocks lower only during the initial part of the decline (similarly to what happened in 1929 and in 2000, after the tech bubble burst). And since the Fed is unlikely (in my view) to engage in yield curve control on a massive scale (another Operation Twist) until the stock market declines visibly, it doesn’t seem that one should worry too much about the PMs’ decline being prevented by the Fed.

Summary

To summarize, the PMs’ medium-term decline is well underway, and based on the recent performance of the USD Index, gold and mining stocks, it seems that the corrective upswing is already over (or about to be over). The next big move lower seems to be already underway or about to start.

In addition, because we’re likely entering the “winter” part of the Kondratiev cycle (just like in 1929 and then the 1930s), the outlook for the precious metals’ sector remains particularly bearishduring the very first part of the cycle, when cash is king.

The confirmed breakout in the USD Index is yet another confirmation of the bearish outlook for the precious metals market.

After the sell-off (that takes gold to about $1,450 - $1,500), we expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and it seems that we’re about to make much more on this March decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently providing you with a possibility to extend your subscription by a year, two years or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now, while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $24.12; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $39.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $94.87; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,512.

Gold futures upside profit-take exit price: $1,512.

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.