-

Fat or Flat: Gold Price in 2022

February 15, 2022, 10:31 AMAnalysts' 2022 forecasts for the gold market are not overwhelmingly enthusiastic – they see it flat. However, maybe the opposite should be expected.

The LBMA has recently published its annual precious metals forecast survey. In general, the report is neutral about gold in 2022. On average, the analysts forecast gold prices to be broadly flat this year compared to the year. The average gold price in 2021 was $1,799, and it is expected to rise merely $3 to $1,802. How boring! However, as the table below shows, the forecasts for other precious metals are much more bearish, especially for palladium.

The headline numbers are the averages of 34 analysts’ forecasts. The greatest bears see the average price of gold as low as $1.630, while the lowest low – at $1,500. Meanwhile, the biggest bulls expect the average price of gold to be $1,965, while the highest high is expected to be $2.280.

The three most important drivers of precious metals prices’ performance this year are the Fed’s monetary policy, inflation, and equity market performance. This is a huge change compared to last year, when analysts considered geopolitical factors, the impact of the COVID-19 pandemic, and the pace of economic recovery to be much more important. I agree this time, of course, as I always believed that macroeconomic factors are more relevant to the long-term trend in the gold market than geopolitical drivers.

Generally, the pick-up in inflation, which will keep real interest rates in negative territory, is seen as a tailwind for gold. Some analysts also expect the greenback to depreciate as the global economic recovery gathers steam, which would also be supportive of gold prices. Meanwhile, normalization of monetary policy is considered the greatest headwind for the yellow metal, as the Fed’s tightening cycle will raise the opportunity cost of holding gold.

However, the markets have probably already priced the interest rate hikes in, so gold doesn’t have to suffer during the tightening cycle. Last time, the price of gold began to rise after the liftoff of the federal funds rate. The analysts surveyed by the LBMA also doubt the central banks’ ability to raise interest rates as high as needed to crush inflation. Instead, they are expected to stay behind the inflation curve. This is because the forecasted tightening cycle could be too difficult for the asset market and indebted economy to stomach, so it will be moderate and short-lived, just like last time.

Implications for Gold

What does the LBMA annual forecast survey predicts for the yellow metal? The report is neutral, probably because gold remains under the influence of opposite forces, which makes forecasting really challenging this year. Gold has been recently in a sideways trend, so it’s somewhat natural to expect simply more of the same, i.e., the flat market. Actually, the pundits always forecast more of the same. For example, the previous edition of the survey was bullish, as 2020 was a great year for gold. Thus, the analysts’ 2021 average forecast for the price of gold was $1,973.8, almost $200 above the actual level. Hence, please take the survey with a pinch of salt.

OK, the analysts don’t predict a literally flat market. The forecasts concerned averages, but some experts see the first half of the year as more bullish than the second, while others, vice versa. I’d rather include myself in the latter group, as my view is that the expectations of Fed tightening will continue to exert downward pressure on gold prices in the coming weeks.

However, the hawkish expectations have probably gone a little too far. At some point this year, they will be adjusted, as it becomes clear that the Fed will be forced to reduce the pace of its tightening or even reverse its stance in order to calm the market and avoid the next economic crisis. Such an adjustment will be positive for gold prices, especially since it might occur amid still high inflation, but gold bulls should remember that there is still a long way to go before that happens.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

The ECB Awakens. Will Gold Feel the Force?

February 10, 2022, 9:54 AMLagarde opened the door to an interest rate hike, which gave the European Central Bank a hawkish demeanor. Does it also imply more bullish gold?

The ECB has awoken from its ultra-dovish lethargy. In December 2021, the central bank of the Eurozone announced that its Pandemic Emergency Purchase Program would end in March 2022. Although this won’t also mean the end of quantitative easing as the ECB continues to buy assets under the APP program, the central bank will be scaling down the pace of purchases this year. Christine Lagarde, the ECB’s President, admitted it during her press conference held last week. She said: “We will stop the Pandemic Emergency Programme net asset purchases in March and then we will look at the net asset purchases under the APP.”

She also left the door open for the interest rates to be raised. Of course, Lagarde did not directly signal the rate hikes. Instead, she pointed out the upside risk of inflation and acknowledged that the macroeconomic conditions have changed:

We are going to use all instruments, all optionalities in order to respond to the situation – but the situation has indeed changed. You will have noticed that in the monetary policy statement that I just read, we do refer to the upside risk to inflation in our projection. So the situation having changed, we need to continue to monitor it very carefully. We need to assess the situation on the basis of the data, and then we will have to take a judgement.

What’s more, Lagarde didn’t repeat her December phrase that raising interest rates in 2022 is “very unlikely”. When asked about that, she replied:

as I said, I don’t make pledges without conditionalities and I did make those statements at our last press conference on the basis of the assessment, on the basis of the data that we had. It was, as all pledges of that nature, conditional. So what I am saying here now is that come March, when we have additional data, when we’ve been able to integrate in our analytical work the numbers that we have received in the last few days, we will be in a position to make a thorough assessment again on the basis of data. I cannot prejudge what that will be, but we are only a few weeks away from the closing time at which we provide the analytical work, prepare the projections for the Governing Council, and then come with some recommendations and make our decisions.

It sounds very innocent, but it’s worth remembering that Lagarde is probably the most dovish central banker in the world (let’s exclude Turkish central bankers who cut interest rates amid high inflation, but they are under political pressure from Erdogan). After all, global monetary policy is tightening. For example, last week, the Bank of England hiked its main policy rate by 25 basis points and started quantitative tightening. Even the Fed will probably end quantitative easing and start raising the federal funds rate in March. In such a company, the ECB seems to be a reckless laggard. Hence, even very shy comments mean something in the case of this central bank. The markets were so impressed that they started to price in 50 basis points of rate hikes this year, probably in an exaggerated reaction.

Implications for Gold

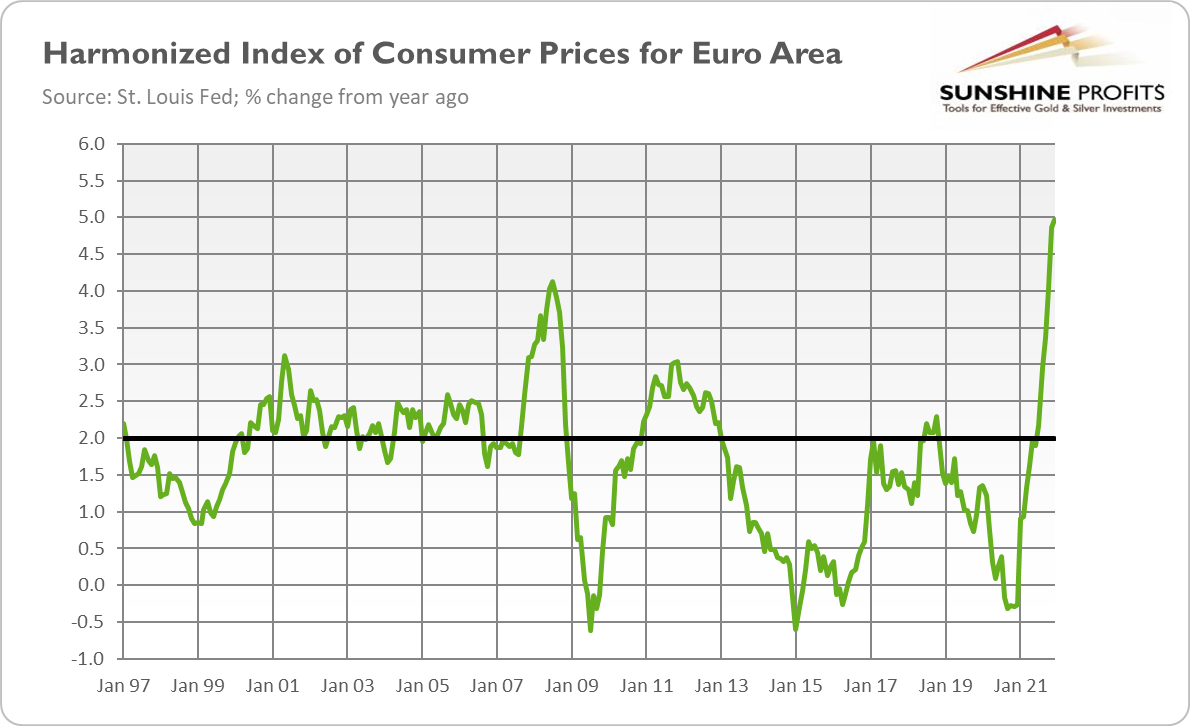

What does the latest ECB monetary policy meeting mean for the gold market? Well, maybe it wasn’t an outright revolution, but the ECB is slowly reducing its massive monetary stimulus. Although the euro area does not face the inflationary pressure of the same kind as the US, with inflation that soared to 5% in December and to 5.1% in January (according to the initial estimate), the ECB simply has no choice. As the chart below shows, inflation in the Eurozone is the highest in the whole history of euro.

Additionally, in the last quarter of 2021, the GDP of the euro area finally reached its pre-pandemic level, two quarters later than in the case of the US. Europe is back in the game. The economic recovery strengthens the hawkish camp within the ECB. All of this is fundamentally bullish for gold prices.

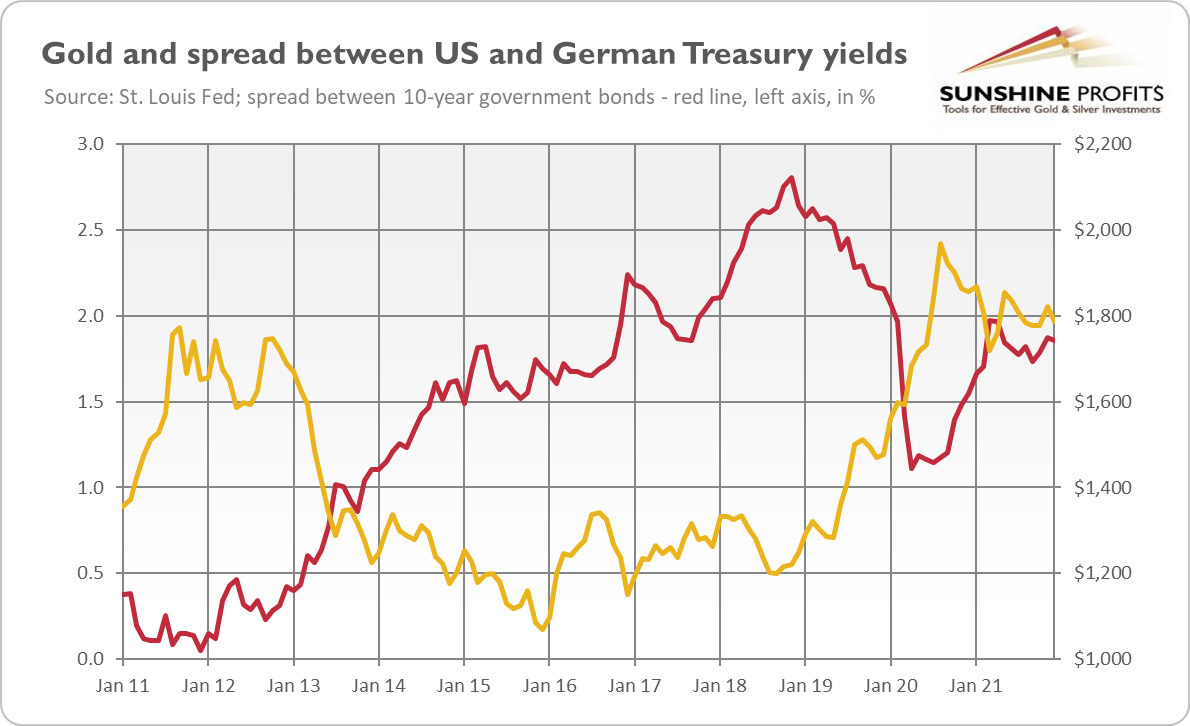

To be clear, don’t expect that Christine Lagarde will turn into Paul Volcker and hike interest rates in a rush. Given the structural problems of the euro area, the ECB will lag behind the Fed and remain relatively more dovish. However, German bond yields have recently risen, and there is still room for further increases. If the market interest rates go up more in Europe than across the pond, which is likely given the financial tightening that has already occurred in the US, the spread between American and German interest rates could narrow further (see the chart below).

The narrowing divergence between monetary policies and interest rates in the US and in the Eurozone should strengthen the euro against the greenback – and it should be supportive of gold. As the chart above shows, when the spread was widening in 2012-2018, gold was in the bear market. The yellow metal started its rally at the end of 2018, just around the peak of the spread.

On the other hand, if the divergence intensifies, gold will suffer. Given that Powell is expected to hike rates as soon as March, while Lagarde may only start thinking about the tightening cycle, we may have to wait a while for the spread to peak. One thing is certain: it can get hot in March!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Even Strong Payrolls Couldn’t Knock Gold off Its $1800 Perch

February 8, 2022, 10:17 AMThe latest employment report strongly supports the Fed’s hawkish narrative. Surprisingly, gold has shown remarkable resilience against it so far.

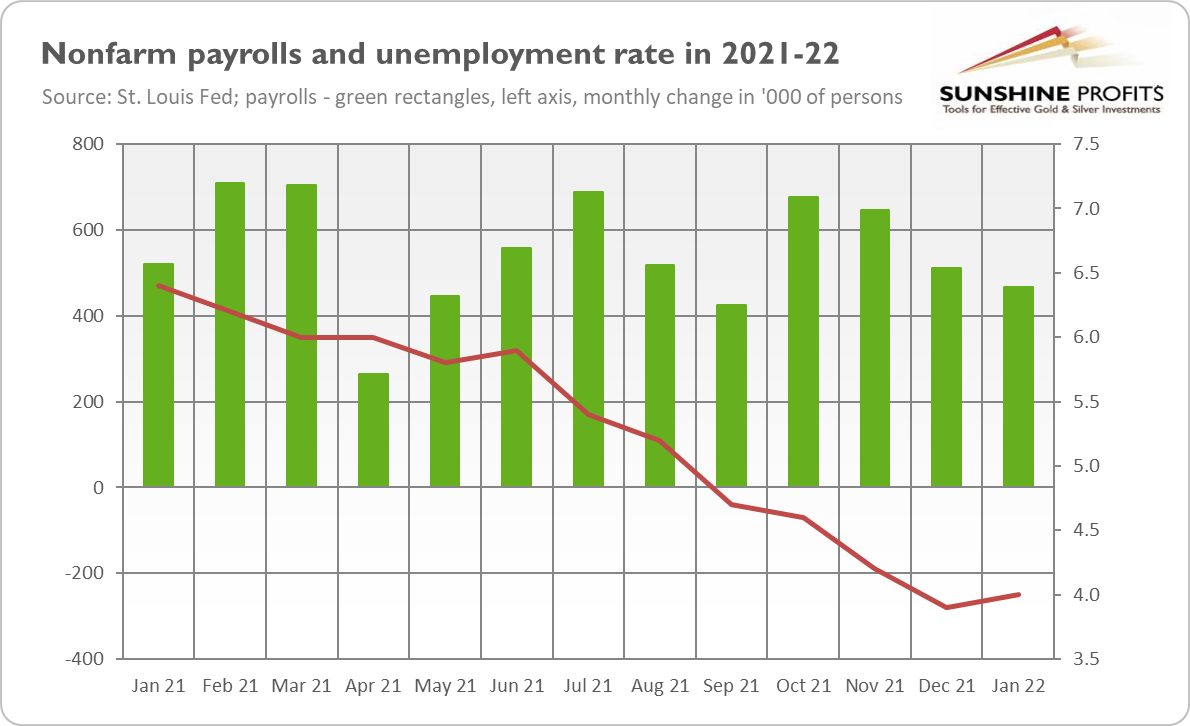

What a surprise! The US labor market added 467,000 jobs last month. As the chart below shows, the number is below December’s figure (+510,000) but much above market expectations – MarketWatch’s analysts forecasted only 150,000 added jobs. Thus, the report reinforces the optimistic view of the US economy’s strength, especially given that the surprisingly good nonfarm payrolls came despite the disruption to consumer-facing businesses from the spread of the Omicron variant of the coronavirus.

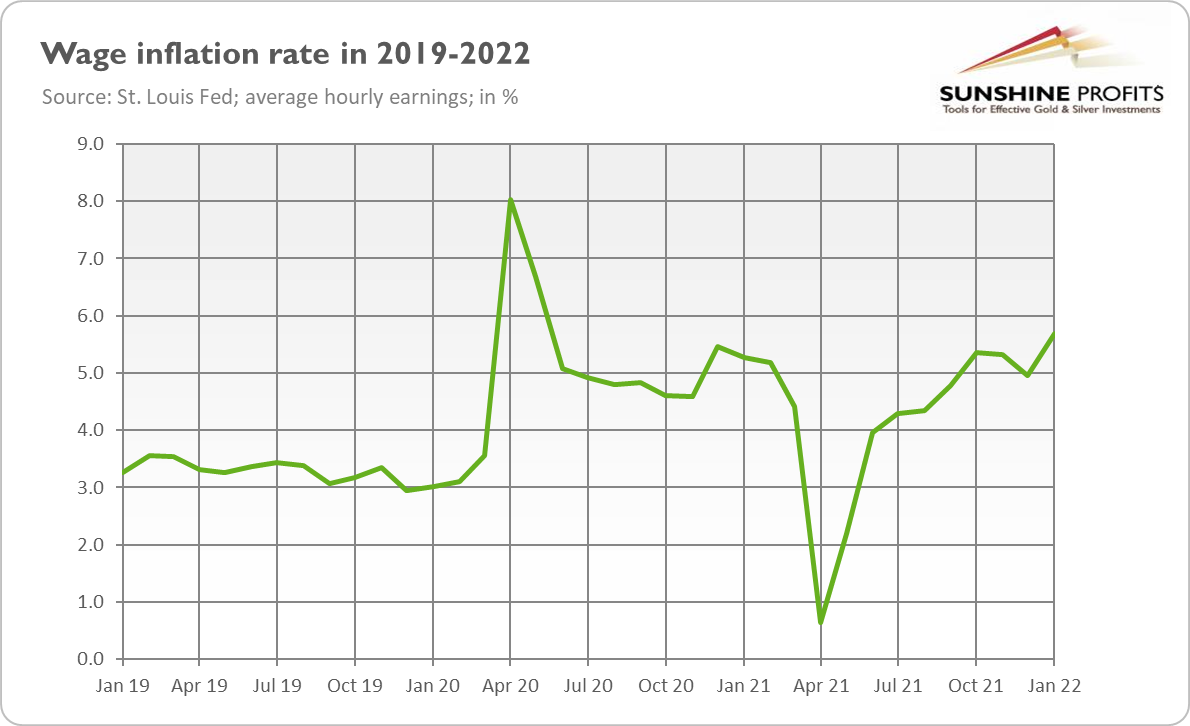

The unemployment rate increased slightly from 3.9% in December to 4% in January, as the chart above shows. However, it was accompanied by a rise in both the labor force participation rate (from 61.9% to 62.2%) and the employment-population ratio (from 59.5% to 59.7%). Last but not least, average hourly earnings have jumped 5.7% over the last 12 months, as you can see in the next chart. It indicates that wage inflation has intensified recently, despite the surge in COVID-19 cases that was expected by some analysts to dent demand for workers.

Hence, the January employment report will cement the hawkish case for the Fed. Rising wages will add to the argument for decisive hiking of interest rates, while the surprisingly strong payrolls will strengthen the Fed’s confidence in the US economy.

Implications for Gold

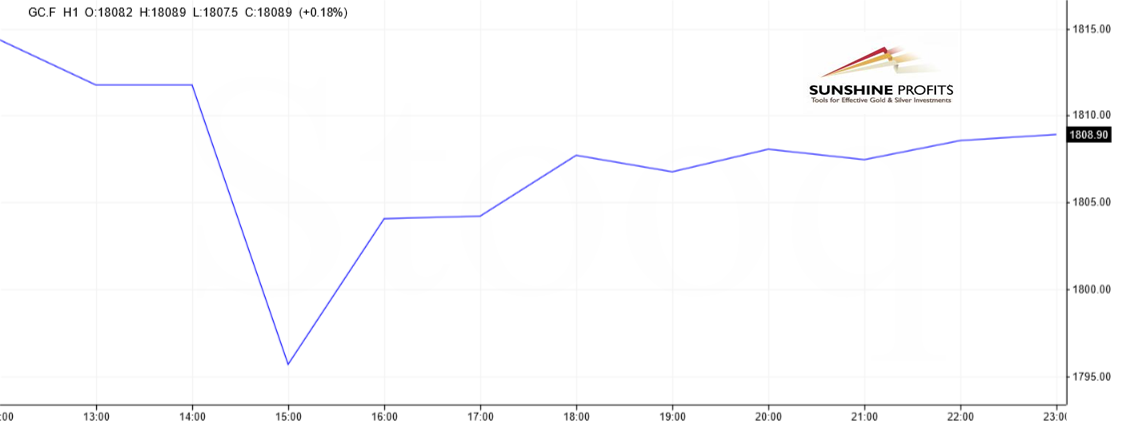

What does the latest employment report imply for the gold market? The unexpectedly high payrolls should be negative for the yellow metal. However, while gold prices initially plunged below $1,800, they rebounded quickly, returning above its key level, as the chart below shows.

Gold’s resilience in the face of a strong jobs report is noteworthy and quite encouraging. After all, the report strengthened the US dollar and boosted market expectations of a 50-basis point hike in the federal funds rate in March (from 2.6% one month ago to more than 14% now). Such a big move is unlikely, but the point is that financial conditions are tightening without waiting for the Fed’s actual actions. In the past, gold disliked strong economic reports and rising bond yields and showed a negative correlation with nonfarm payrolls, but not this time. More generally, although long-term fundamentals have turned more bearish in recent months, gold has remained stuck at $1,800.

However, last week, two factors could have supported gold prices. The first was rising volatility in the equity market. The S&P 500 Index dropped almost 500 points, or 10%, in January, as the chart below shows. Although it has recovered somewhat, it still remains substantially below the top, with the tech sector experiencing weakness. On Thursday, the shares of Meta, Facebook’s parent company, plunged more than 20%.

The second potentially bullish driver was last Thursday’s meeting of the ECB’s Governing Council. The central bank of the Eurozone was more hawkish than expected. Christine Lagarde acknowledged inflationary risks and said that she had become more concerned with the recent surge in inflation. According to initial estimates, the annual inflation rate in the euro area amounted to 5.1% in January 2022, the highest since the common currency was created. Lagarde also backed off her previous guidance that the interest rate hike was “very unlikely” in 2022. The ECB’s pivot – the central bank opening the door for the first rate increase since 2011 – boosted the euro against the greenback.

The bottom line is that gold has made itself comfortable around $1,800 and simply doesn’t want – or is not ready – to go away in either direction, at least not yet. The battle between bulls and bears is still on. I’m afraid that, given the relatively aggressive monetary and financial tightening, the sellers will win this clash and gold will drop before the bulls can regain control over the market. However, recent gold’s resilience indicates that there is an underlying bid in the markets and bulls are not giving up.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Ended January Glued to $1,800. Will It Ever Detach?

February 3, 2022, 10:30 AMGold didn’t shine in January. The struggle could continue, although the more distant future looks more optimistic for the yellow metal.

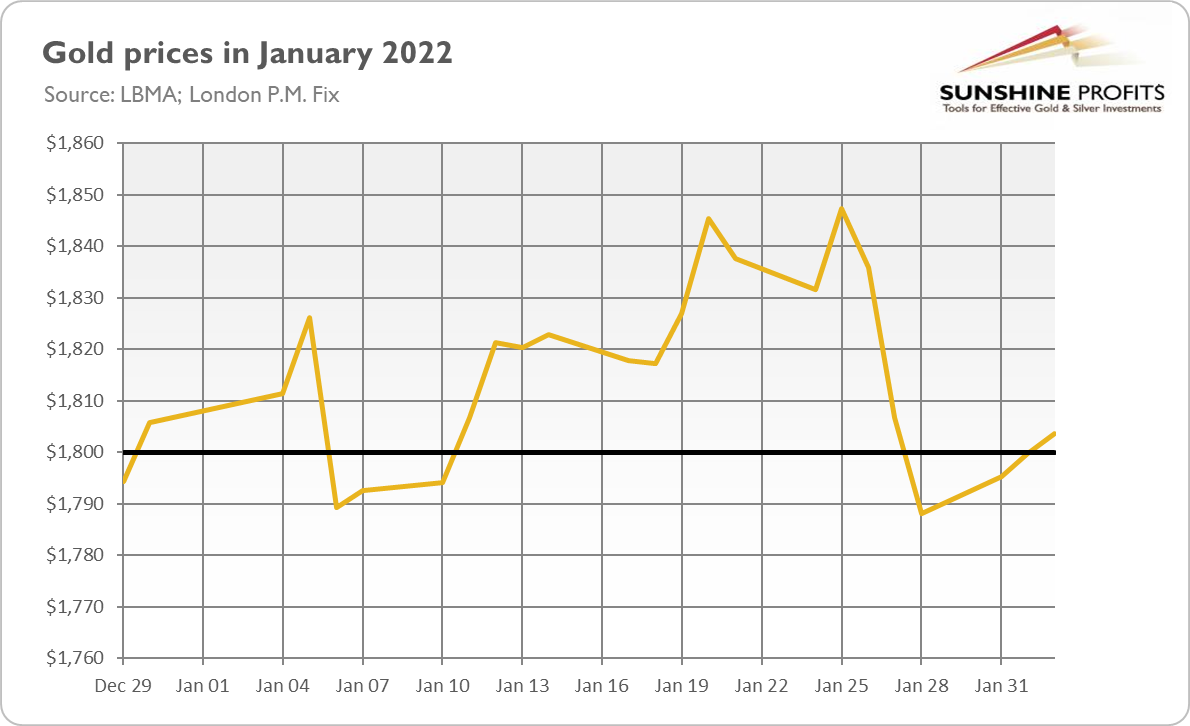

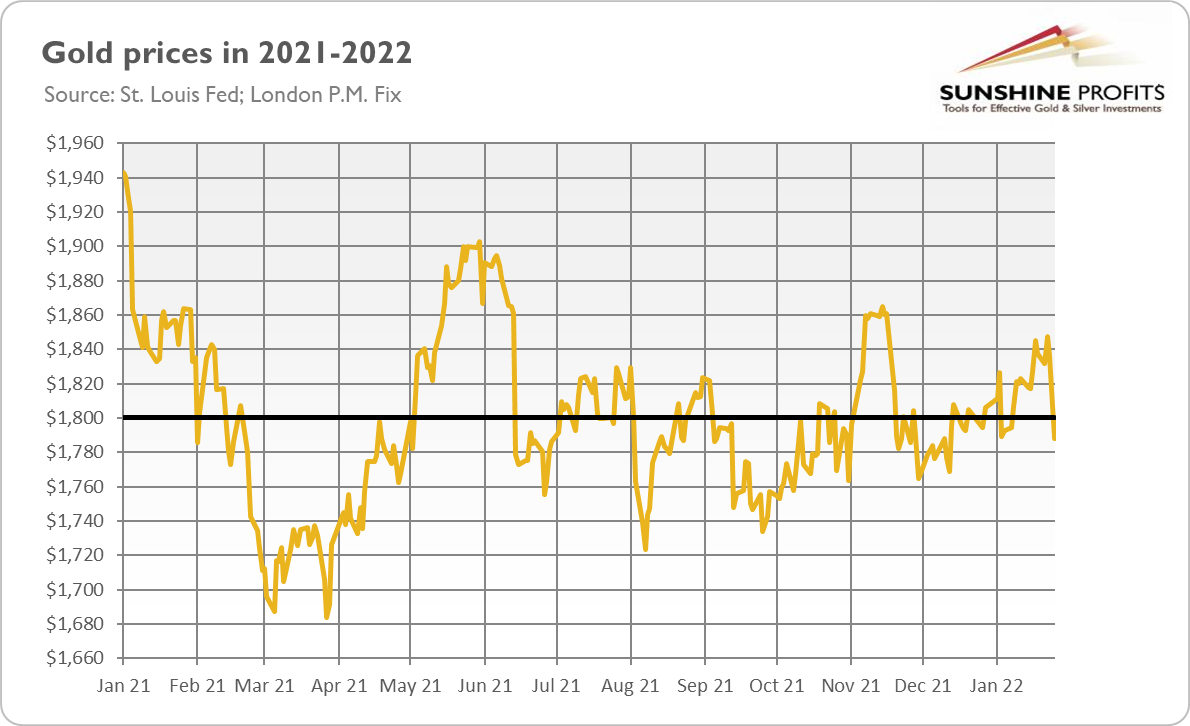

That was quick! January has already ended. Welcome to February! I hope that this year has started well for you. For gold, the first month of 2022 wasn’t particularly good. As the chart below shows, the yellow metal lost about $11 of its value, or less than 1%, during January.

This is the bad side of the story. The ugly side is that gold wasn’t able to maintain its position above $1,800, even though geopolitical risks intensified, while inflation soared to the highest level in 40 years! The yellow metal surpassed the key level in early January and stayed above this level for most of the time, even rallying above $1,840 in the second half of the month. But gold couldn’t hold out and plunged at the end of January, triggered by a hawkish FOMC meeting.

However, there is also a good side. Gold is still hovering around $1,800 despite the upcoming Fed’s tightening cycle and all the hawkish expectations about the US monetary policy in 2022. The Fed signaled the end of tapering of quantitative easing by March, the first hike in the federal funds rate in the same month, and the start of quantitative tightening later this year. Meanwhile, in the last few weeks, the markets went from predicting two interest rate hikes to five.

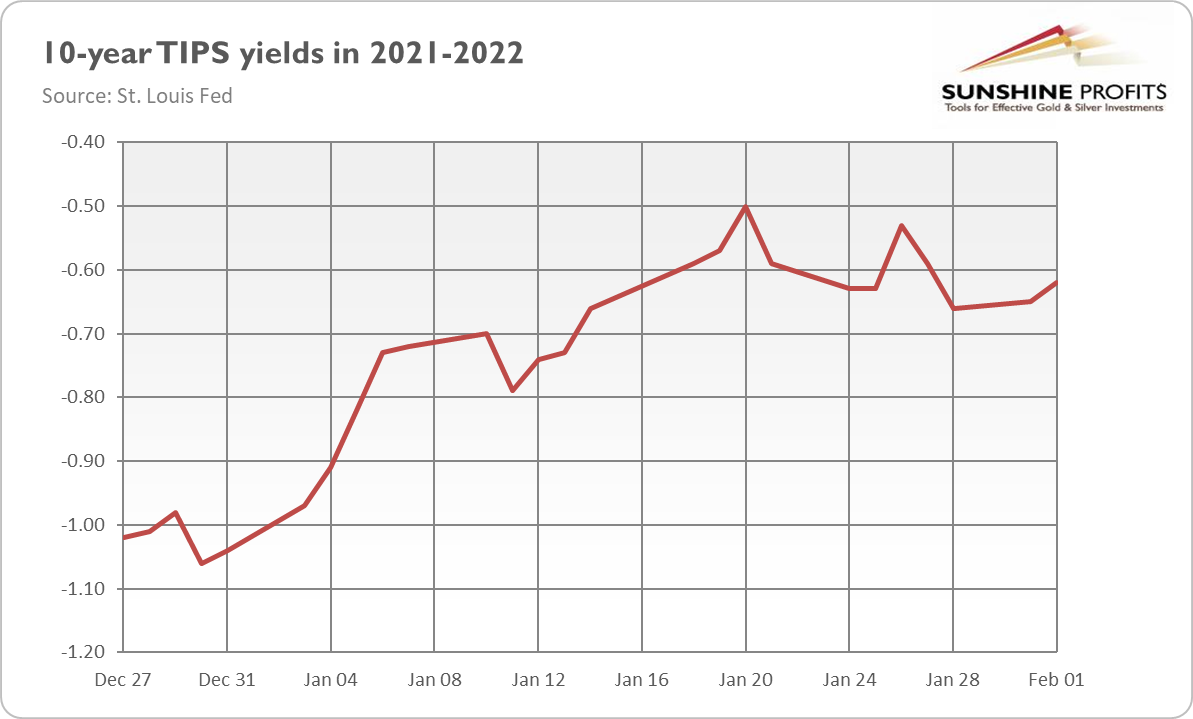

Even more intriguing, and perhaps encouraging as well, is that the real interest rates have increased last month, rising from -1% to -0.6%. Gold is usually negatively correlated with the TIPS yields, but this time it stayed afloat amid rising rates.

Implications for Gold

What does gold’s behavior in January imply for its 2022 outlook? Well, I must admit that I expected gold’s performance to be worse. Last month showed that gold simply don’t want to either go down (or up), but it still prefers to go sideways, glued to the $1,800 level. The fact that strengthening expectations of the Fed’s tightening cycle and rising real interest rates didn’t plunge gold prices makes me somewhat more optimistic about gold’s future.

However, I still see some important threats to gold. First of all, some investors are still underpricing how hawkish the Fed could become to combat inflation. Hence, the day of reckoning could still be ahead of us. You see, just today, the Bank of England hiked its policy rate by 25 basis points, although almost half of the policymakers wanted to raise interest rates by half a percentage point. Second, the market seems to be biased downward, with lower and lower peaks since August 2020.

Having said that, investors should remember that what the Fed says it will do and what it ends up doing are often very different. When the Fed says it will be dovish, it will be dovish. But when the Fed says it will be hawkish, it says so. This is because a monetary tightening could be painful for asset valuations and all the debtors, including Uncle Sam. The US stock market already saw significant losses in January. As the chart below shows, the S&P 500 Index lost a few hundred points last month, marking the worst decline since the beginning of the pandemic.

Thus, the Fed won’t risk recession in its fight with inflation, especially if it peaks this year, and would try to engineer a soft-landing. Hence, the Fed could reverse its stance relatively soon, especially that it’s terribly late with its tightening. However, as long as the focus is on monetary policy tightening, gold is likely to struggle within its tight range.

Some policymakers and economists have argued that the emergence from the COVID-19 pandemic is more like a postwar demobilization and conversion to a civilian industry than a normal business cycle.

White House economists have compared the current picture to the rapid increases in 1947, caused by the end of price controls in conjunction with supply chain problems and pent-up demand after the war (“Historical Parallels to Today’s Inflationary Episode”, Council of Economic Advisers, July 6, 2021).

The problem with this analogy is that it is only one instance from more than 70 years ago. More recent and more frequent inflation episodes have generally been ended by a recession or a mid-cycle slowdown.

Price pressures have an internal momentum of their own and tend to intensify rather than lessen as the business cycle becomes more mature and the margin of spare capacity shrinks in all markets.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Defended $1,800 Bravely, but Gave Up

February 1, 2022, 10:05 AMGold fought valiantly, gold fought nobly, gold fought honorably. Despite all this sacrifice, it lost the battle. How will it handle the next clashes?

Have you ever felt trapped in the tyranny of the status quo? Have you ever felt constrained by some invisible yet powerful forces trying to thwart the fullest realization of your potential? I guess this is what gold would feel like right now – if metals could feel anything, of course.

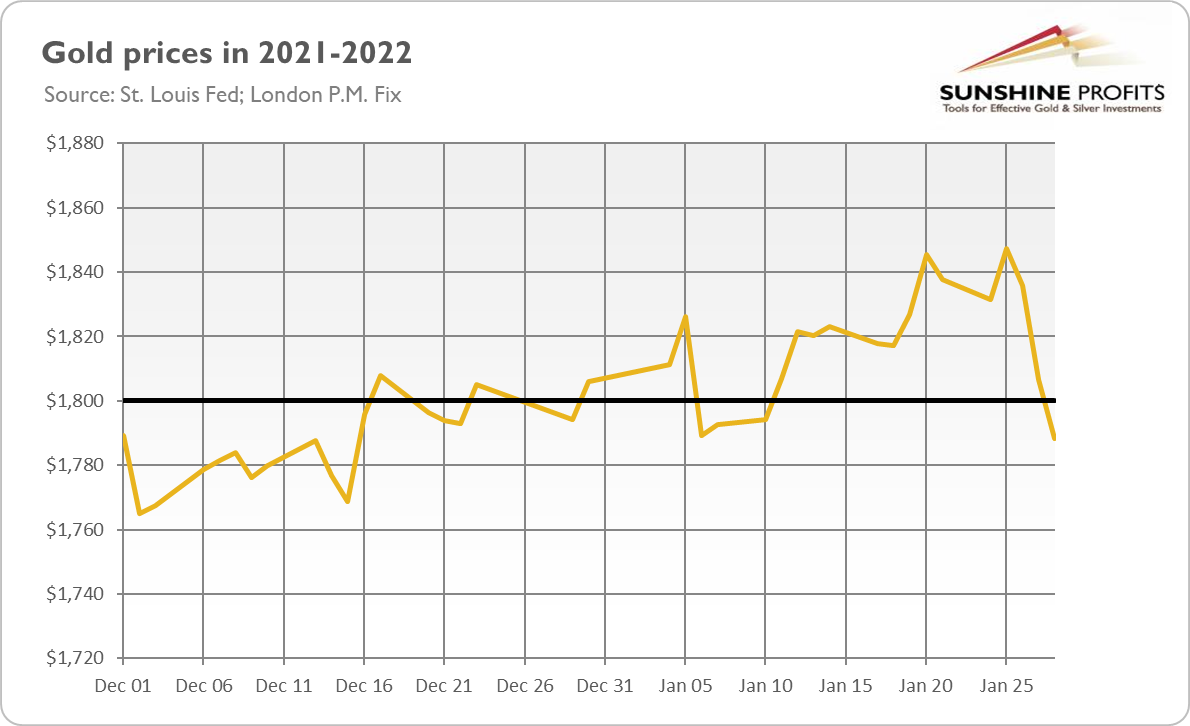

Please take a look at the chart below. As you can see, January looked to be quite good for the yellow metal. Its price surpassed the key level of $1,800 at the end of 2021, rallying from $1,793 to $1,847 on January 25, 2022.

Then the evil FOMC published its hawkish statement on monetary policy. In its initial response, gold slid. That’s true, but it bravely defended its positions above $1,800 during both Wednesday and Thursday. There was still hope. However, on Friday, the metal capitulated and plunged to $1,788.

Here we are again – below the level of $1,800 that gold hasn’t been able to exceed for more than several days since mid-2021, as the chart below shows. Am I disappointed? A bit. Naughty goldie! Am I surprised? Not at all.

Although I cheered the recent rally, I was unconvinced about its sustainability in the current macroeconomic context, i.e., economic recovery with tightening of monetary policy (the surprisingly positive report on GDP in the fourth quarter of 2021 didn’t probably help gold), rising interest rates, and possibly a not-distant peak in inflation. In the previous edition of the Fundamental Gold Report, I described the Fed’s actions as “a big hawkish wave that could sink the gold bulls” and pointed out that “gold started its decline before the statement was published, which may indicate more structural weakness.” I added that it was also disturbing that “gold was hit even though the FOMC statement came largely as expected.” Last but not least, I concluded my report with a warning that “the upcoming weeks may be challenging for gold, which would have to deal with rising bond yields.”

My warning came true very quickly. Of course, we cannot exclude a relatively swift rebound. After all, gold can be quite volatile in the short-term, and this year could be particularly turbulent for the yellow metal. However, I’m afraid that the balance of risks for gold is the downside. Next month (oh boy, it’s February already!), we will see the end of quantitative easing and the first hike in the federal funds rate, followed soon by the beginning of quantitative tightening and further rate hikes.

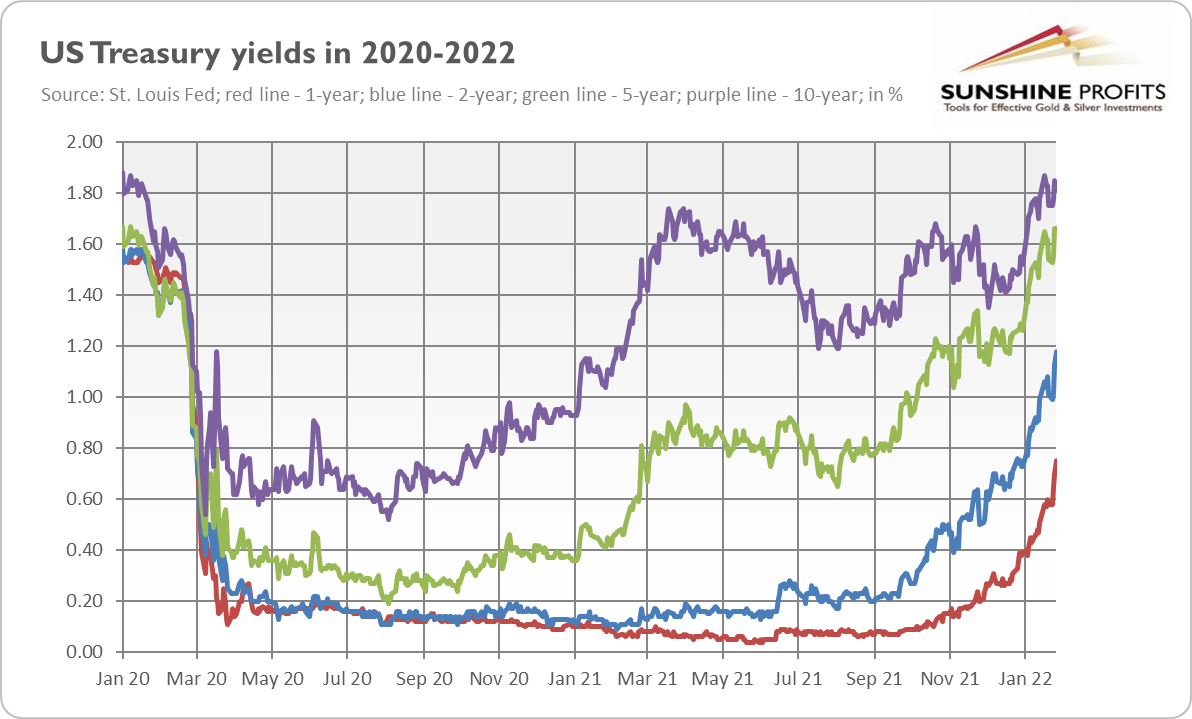

Using its secret magic, the Fed has convinced the markets that it has become a congregation of hawks, or even a cult of the Great Hawk. According to the CME Fed Tool, future traders have started to price in five 25-basis-point raises this year, while some investors believe that the Fed will lift interest rates by 50 basis points in March. All these clearly hawkish expectations led to the rise in bond yields (see the chart below), creating downward pressure on gold.

Implications for Gold

What does the recent plunge in gold prices imply for investors? Well, in a sense, nothing, as short-term price movements shouldn’t affect long-term investments. Trading and investing should be kept separate. However, gold’s return below $1,800 can disappoint even the biggest optimists. The yellow metal failed again.

Not the first and not the last time, though. In my view, gold may struggle by March, as all these hawkish expectations will exert downward pressure on the yellow metal. In 2015, the first hike in the tightening cycle coincided with the bottom of the gold market. It may be similar this time, as the actual hike could ease some of the worst expectations and also push markets to think beyond their tightening horizon.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM