-

Weak November Payrolls Won’t Help Gold

December 7, 2021, 10:49 AMNovember employment report was mixed. Unfortunately for gold, however, it won’t stop the Fed’s hawkish agenda.

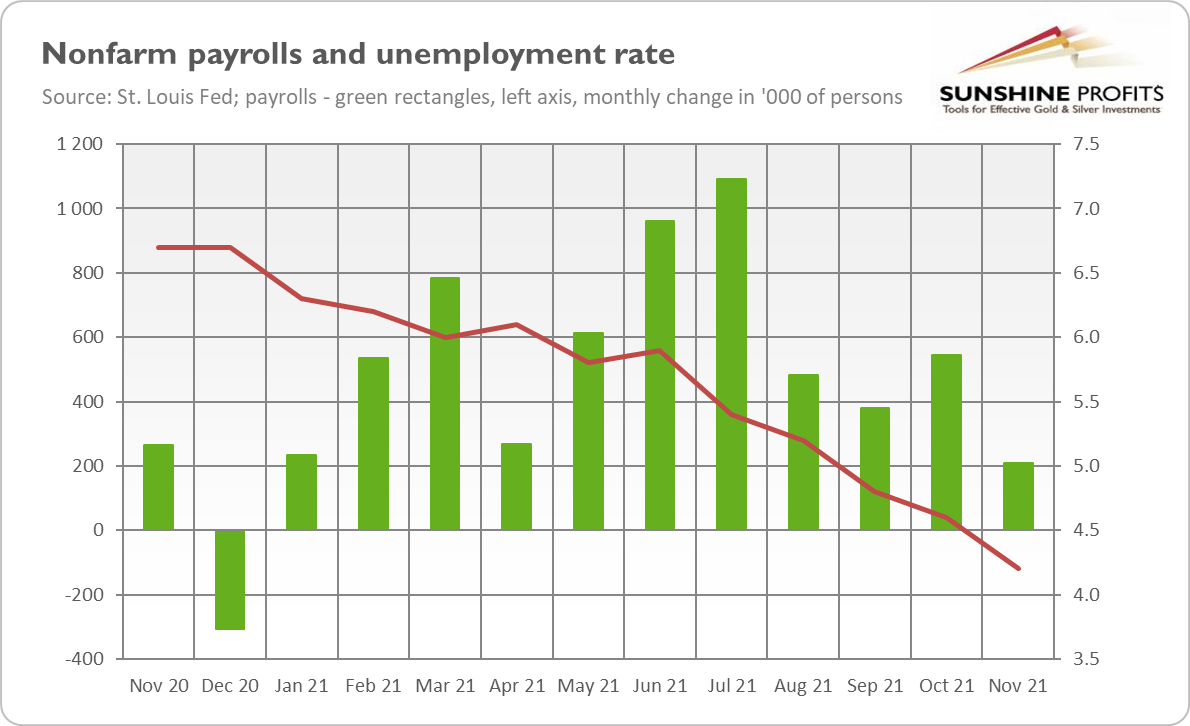

Nonfarm payrolls disappointed in November. As the chart below shows, the US labor market added only 210,000 jobs last month. This number is much lower than both October’s figure (546,000 gains) and the market expectations (MarketWatch’s analysts forecasted 573,000 added jobs). So, it’s a huge blow to those optimistic about the US economy.

However, this is a huge blow that nobody will care about because the disappointing payrolls were accompanied by a big decline in unemployment. As the chart above shows, the unemployment rate decreased by 0.4 percentage points, from 4.6% in October to 4.2% in November.

What’s more, the unemployment rate declined simultaneously with the increases in both the labor-force participation rate (from 61.6% to 61.8%) and the employment-to-population ratio (from 58.8% to 59.2%). This means that the reduction in unemployment was genuine and rather not a result of dropping out from the labor market.

Additionally, wage inflation has slowed down from 4.84% in October to 4.8% in November, remaining below expectations, which could slightly ease inflationary concerns. Last but not least, after revisions, employment in September and October combined was reported to be 82,000 higher than previously indicated, and the monthly job growth has averaged 555,000 so far this year. Therefore, even a weak November doesn’t change the fact that 2021 marked a great improvement in the US labor market.

Implications for Gold

What does the November employment report imply for the gold market? The nonfarm payrolls disappointed, but it’s not enough to stop the Fed from accelerating the pace of tapering its quantitative easing, especially given the significant reduction in the unemployment rate. So, the hawkish revolution won’t be stopped. It may even be strengthened, as a big decline in unemployment brings us closer to “full employment” and meeting the criteria for hiking interest rates.

This is, of course, not good news for the gold bulls. After hearing worries about inflation a few weeks ago, the Fed managed to calm investors. They’ve believed that Powell and his colleagues would take the inflationary threat seriously. Markets now expect a speed-up in the pace of tapering in December and as much as three interest rates hikes in 2022 (there are even investors who bet on seven hikes by the end of the next year!).

However, there is a silver lining here. With the unemployment rate at 4.2%, the potential for further improvement is rather limited. And when a new upward trend begins, we will have rising unemployment rate and high inflation at the same time. Such conditions create stagflation, which would take gold higher.

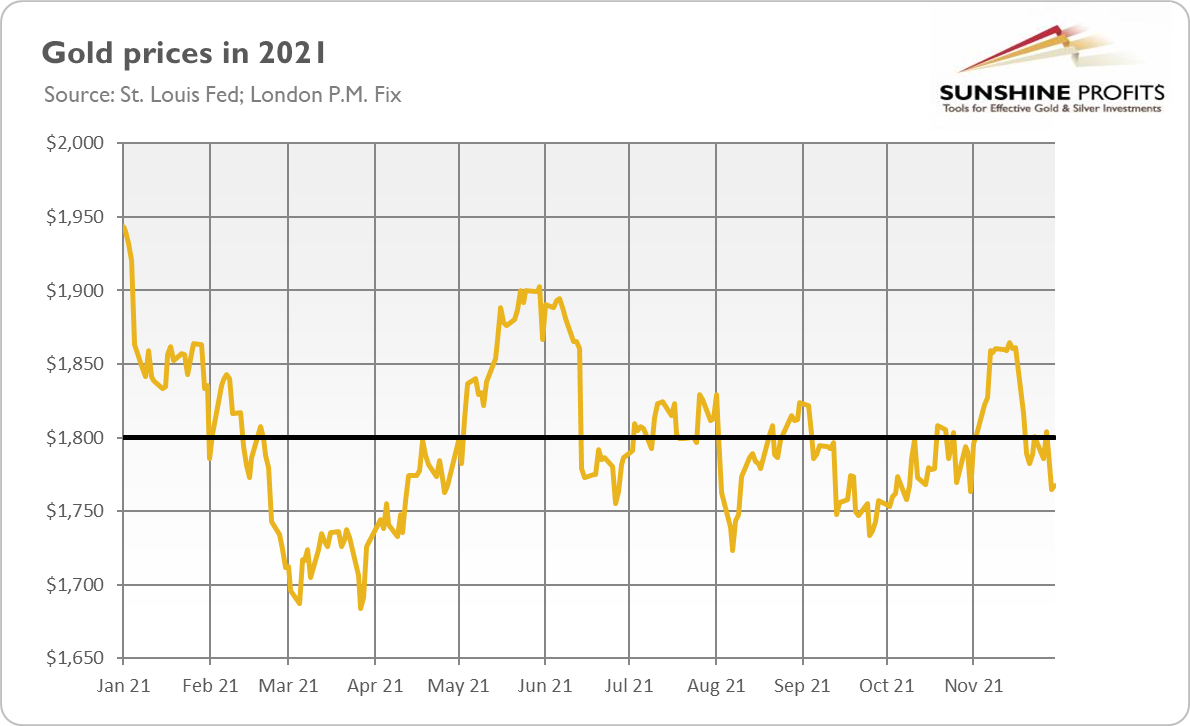

This is still a song of the future, though. Let’s focus on the recent past: gold prices increased slightly on Friday (December 3, 2021). Although the London P.M. Fix hardly changed (see the chart below), the New York price rebounded to about $1,783 on Friday from $1,769 the day before. However, it doesn’t change the fact that gold remains stuck in a sideways trend below $1,800, as concerns about inflation exist along with expectations of a more aggressive Fed tightening cycle.

Luckily for gold, despite its hawkish rhetoric, the US central bank will remain behind the inflation curve. The cautious, dovish policy is simply too tempting, as hitting the brakes too hard could trigger a financial crisis and a recession. With the CPI annual rate above 6%, the Fed should have already hiked the federal funds rate instead of waiting until Q2 2022. And even with three 25-basis point hikes, real interest rates will remain deeply in negative territory, which should be supportive of gold prices.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Hawks Triumph, Doves Lose, Gold Bulls Cry!

December 2, 2021, 10:55 AMThe hawkish revolution continues. Powell, among the screams of monetary doves, suggested this week that tapering could be accelerated in December!

People live unaware that an epic battle between good and evil, the light and dark side of the Force, hard-working entrepreneurs and tax officials is waged every day. What’s more, hawks and doves constantly fight as well, and this week brought a victory for the hawks among the FOMC.

The triumph came on Tuesday when Fed Chair Jerome Powell testified before Congress. He admitted that inflation wasn’t “transitory”, as it is only expected to ease in the second half of 2022. Inflation is therefore more persistent and broad-based than the Fed stubbornly maintained earlier this year, contrary to evidence and common sense:

Generally, the higher prices we’re seeing are related to the supply and demand imbalances that can be traced directly back to the pandemic and the reopening of the economy. But it’s also the case that price increases have spread much more broadly and I think the risk of higher inflation has increased.

Importantly, Powell also agreed that “it’s probably a good time to retire that word.” You don’t say! Hence, the Fed was wrong, and I was right. Hurray! However, it’s a Pyrrhic victory for gold bulls. This is because the recognition of the persistence of inflation pushes the Fed toward a more hawkish position. Indeed, Powell suggested that the FOMC participants could discuss speeding up the taper of quantitative easing in December:

At this point the economy is very strong and inflationary pressures are high and it is therefore appropriate, in my view, to consider wrapping up the taper of our asset purchases, which we actually announced at the November meeting, perhaps a few months sooner, and I expect that we will discuss that at our upcoming meeting in a couple of weeks.

What’s more, Powell seemed to be unaffected by the Omicron coronavirus strain news. He was a bit concerned, but not about its disturbing impact on the demand side of the economy; he found supply-chain disruptions that could intensify inflation way more important. That’s yet another manifestation of Powell’s hawkish stance.

Implications for Gold

What does the Fed’s hawkish tilt imply for the gold market? Well, gold bulls get along with doves, not hawks. A more aggressive tightening cycle, including faster tapering of asset purchases, could boost expectations of more decisive interest rates hikes. In turn, the prospects of a more hawkish Fed could increase the bond yields and strengthen the US dollar. All this sounds bearish for gold.

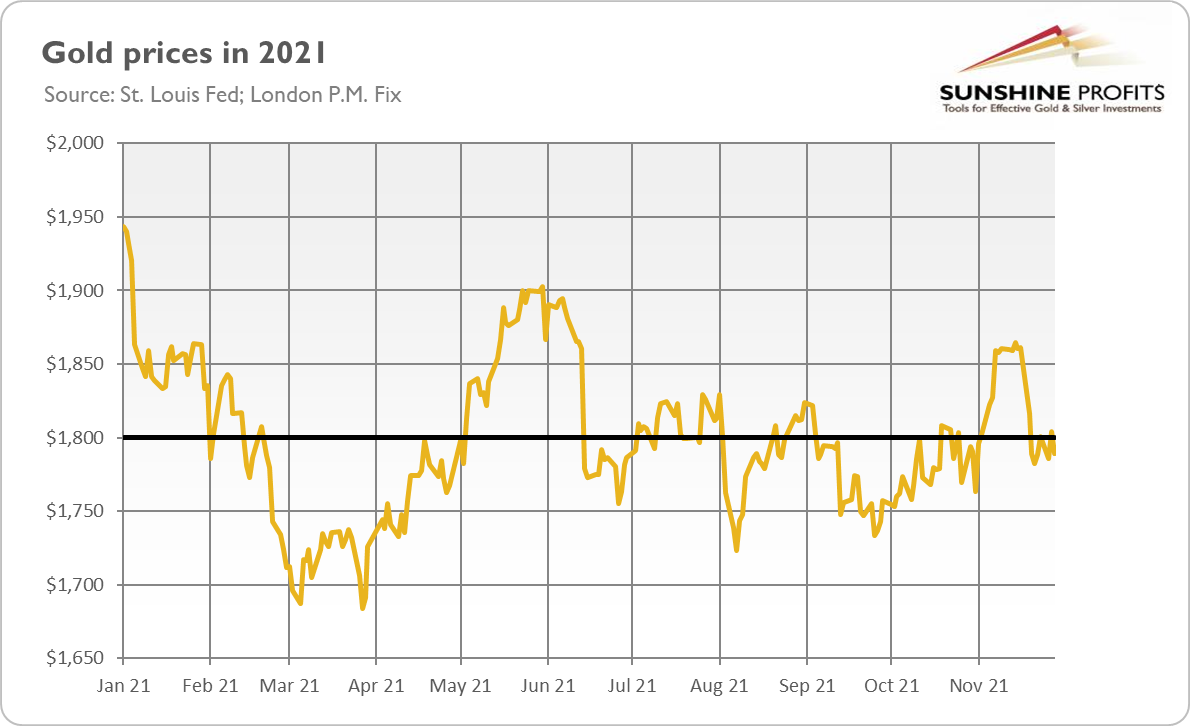

Indeed, the London price of gold dropped on Wednesday below $1,800… again, as the chart above shows. Hence, gold’s inability to stay above $1,800 is disappointing, especially in the face of high inflation and market uncertainty. Investors seem to have once again believed that the Fed will be curbing inflation. Well, that’s possible, but my claim is that despite a likely acceleration in the pace of the taper, inflation will remain high for a while.

I bet that despite the recent hawkish tilt, the Fed will stay behind the curve. This means that the real interest rates should stay negative, providing support for gold prices. The previous tightening cycle brought the federal funds rate to 2.25-2.5%, and we know that after an economic crisis, interest rates never return to the pre-crisis level. This is also what the euro-dollar futures suggests: that the upcoming rate hike cycle will end below 2%. The level of indebtedness and financial markets’ addiction to easy money simply do not allow the Fed to undertake more aggressive actions. Will gold struggle in the upcoming months then? Yes. Gold bulls could cry. But remember: tears cleanse and create more room for joy in the future.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

The Fed Worries About Inflation. Should We Worry About Gold?

November 30, 2021, 10:19 AMOops!... Gold did it again and declined below $1,800 last week. What’s happening in the gold market?

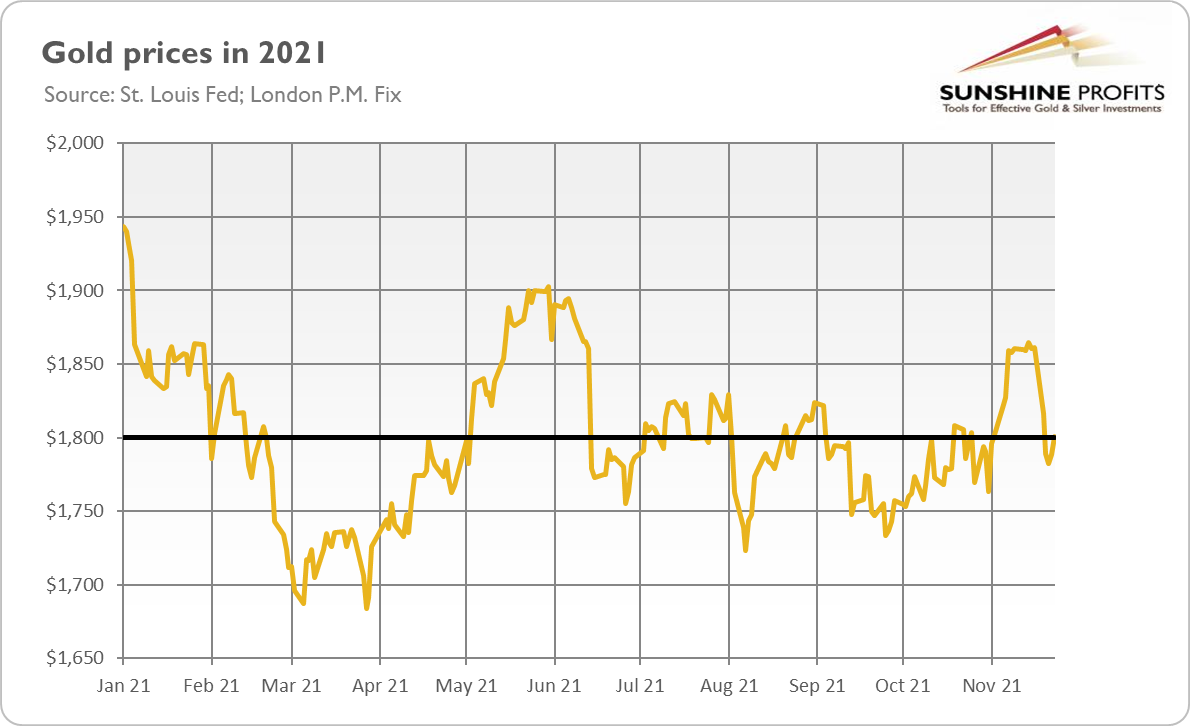

Did you enjoy your roast turkey? I hope so, and I hope that its taste – and Thanksgiving in general – sweetened the recent declines in gold prices. As the chart below shows, the price of the yellow metal (London P.M. Fix) plunged from above $1,860 two weeks ago to above $1,780 last week. It has slightly rebounded since then, but, well, only slightly.

What exactly happened? Funny thing, but actually nothing revolutionary. After all, the reappointment of the same man as the Fed Chair and the publication of the FOMC minutes from the meeting that had already took place earlier in November, were the highlights before Thanksgiving.

Well, sometimes lack of changes is a change itself and information about the past can shed some light on the future. Let’s start from Powell’s renomination for the second term as the Federal Reserve chair. In response, the market bets that the Fed will hike interest rates more aggressively in 2022 have increased. At first glance, the strong investors’ reaction seems strange, given that the monetary policy shouldn’t radically change with Powell still at the helm.

However, the continuation of Powell’s leadership implies that Lael Brainard, regarded as more dovish than Powell, won’t become the new Fed Chair – what was expected by some market participants. Hence, the dovish scenario won’t materialize, which is hawkish for gold.

Just two days later, the FOMC revealed the minutes from its November meeting. The main message – the Fed decided to taper its quantitative easing – was, of course, included in the post-meeting statement. The minutes revealed, however, that the Fed officials had become more worried about inflation and had expressed a more hawkish stance than the statement suggested.

First of all, we learned from the minutes that some central bankers opted for more aggressive tapering and a more flexible approach that would allow for adjustments in the face of high and persistent inflation:

Some participants preferred a somewhat faster pace of reductions that would result in an earlier conclusion to net purchases (…). Some participants suggested that reducing the pace of net asset purchases by more than $15 billion each month could be warranted so that the Committee would be in a better position to make adjustments to the target range for the federal funds rate, particularly in light of inflation pressures. Various participants noted that the Committee should be prepared to adjust the pace of asset purchases and raise the target range for the federal funds rate sooner than participants currently anticipated if inflation continued to run higher than levels consistent with the Committee's objectives (…) participants noted that the Committee would not hesitate to take appropriate actions to address inflation pressures that posed risks to its longer-run price stability and employment objectives.

This is because the FOMC members’ concerns about inflation strengthened. As we can read in the minutes,

They indicated that their uncertainty regarding this assessment had increased. Many participants pointed to considerations that might suggest that elevated inflation could prove more persistent. These participants noted that average inflation already exceeded 2 percent when measured on a multiyear basis and cited a number of factors—such as businesses' enhanced scope to pass on higher costs to their customers, the possibility that nominal wage growth had become more sensitive to labor market pressures, or accommodative financial conditions—that might result in inflation continuing at elevated levels.

Last but not least, the Fed officials also made other hawkish comments. Some participants argued that labor force participation would be lower than before the pandemic because of structural reasons. It implies that we are closer to reaching the “full employment”, so monetary policy could be less accommodative. What’s more, “some participants highlighted the fact that price increases had become more widespread”, while a couple of them noted possible signs that inflation expectations had become less anchored. So, the Fed officials’ worries about inflation strengthened.

Implications for Gold

What does it all imply for the gold market? Well, both the reappointment of Powell as the Fed Chair and the latest FOMC minutes were interpreted as hawkish, which pushed gold prices down. The more upbeat prospects for monetary tightening are clearly negative for the yellow metal, as they boosted the bond yields (see the chart below).

This is something I warned investors against earlier this month. I wrote in the Fundamental Gold Report on November 16 that “when something reaches the bottom, it should rebound later. And if real interest rates start to rally, then gold could struggle again.” This is exactly what happened. Later, in the article on November 18, I added that “I will feel more confident about the strength of the recent rally when gold rises above $1,900”.

Well, gold failed to do this, so I’m not particularly bullish on gold right now. We could say that gold did it again: it played with the hearts of gold bulls but got lost in the game, as it didn’t resist the pressure.

Yes, the new Omicron variant of coronavirus has been noted, and uncertainty about this strain could provide short-term support for the yellow metal. However, it seems that the prospects of monetary tightening and higher real interest rates will continue to put downward pressure on gold prices. I agree, the rally looked refreshing after months of disappointment. However, it seems that we have to wait longer, possibly for the start of the Fed’s increasing the interest rates, to see gold truly shining.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

More Public Debt Is Coming. Another Gold’s Rally Ahead?

November 23, 2021, 8:46 AMDemocrats are not slowing down - the social spending bill follows the infrastructure package. Will gold benefit, or will it get into deep water?

Will the American spending spree ever end? On Monday last week (November 15, 2021), President Biden signed a $1 trillion infrastructure package, and just a few days later, Biden’s social spending bill worth another $1.75 trillion passed the US House of Representatives. Apparently, $1 trillion was not enough! Apparently, we don’t already have too much money chasing too few goods. No, the economy needs even more money!

Yes, I can almost hear the lament of American families: “we need more money, we already bought everything possible, we already own three cars and a lot of other useless crap, but we need more! Please, the almighty government, give us some bucks, let your funds revive our land”. Luckily, the gracious Uncle Sam listened to the prayers of its poor citizens.

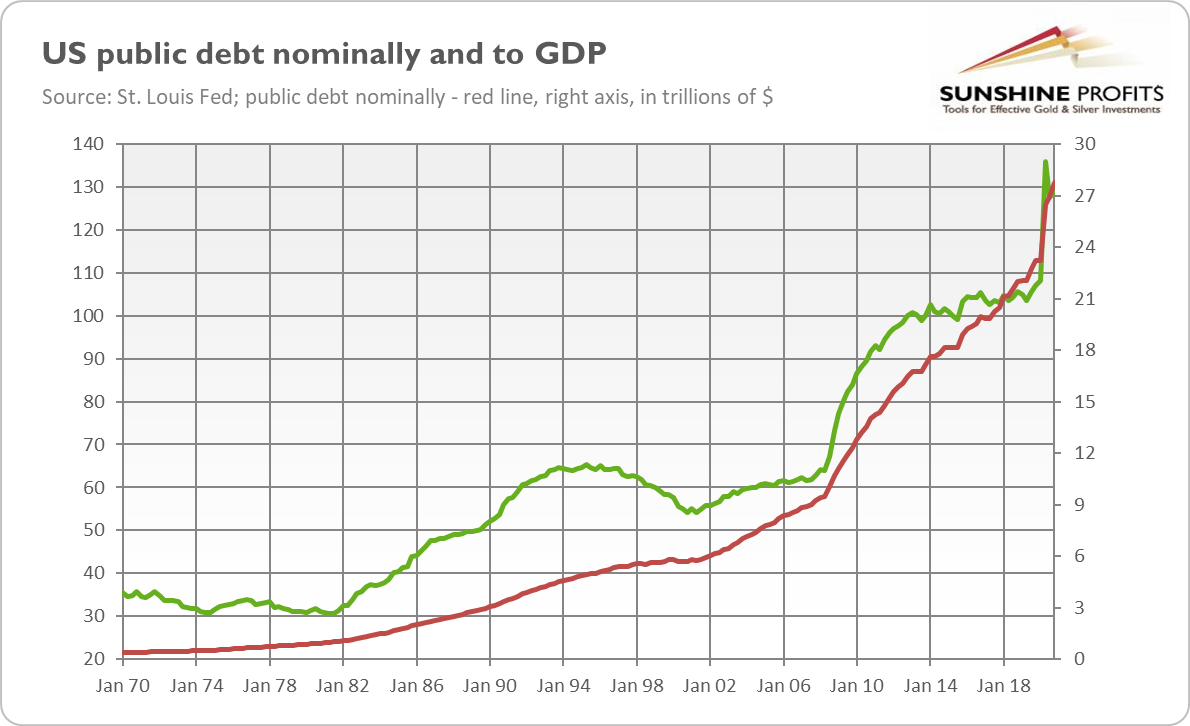

Given the above, one could think that the US economy is not already heavily indebted. Well, it’s the exact opposite. As the chart below shows, the American public debt is more than $27 trillion and 125% of GDP, but who cares except for a few boring economists?

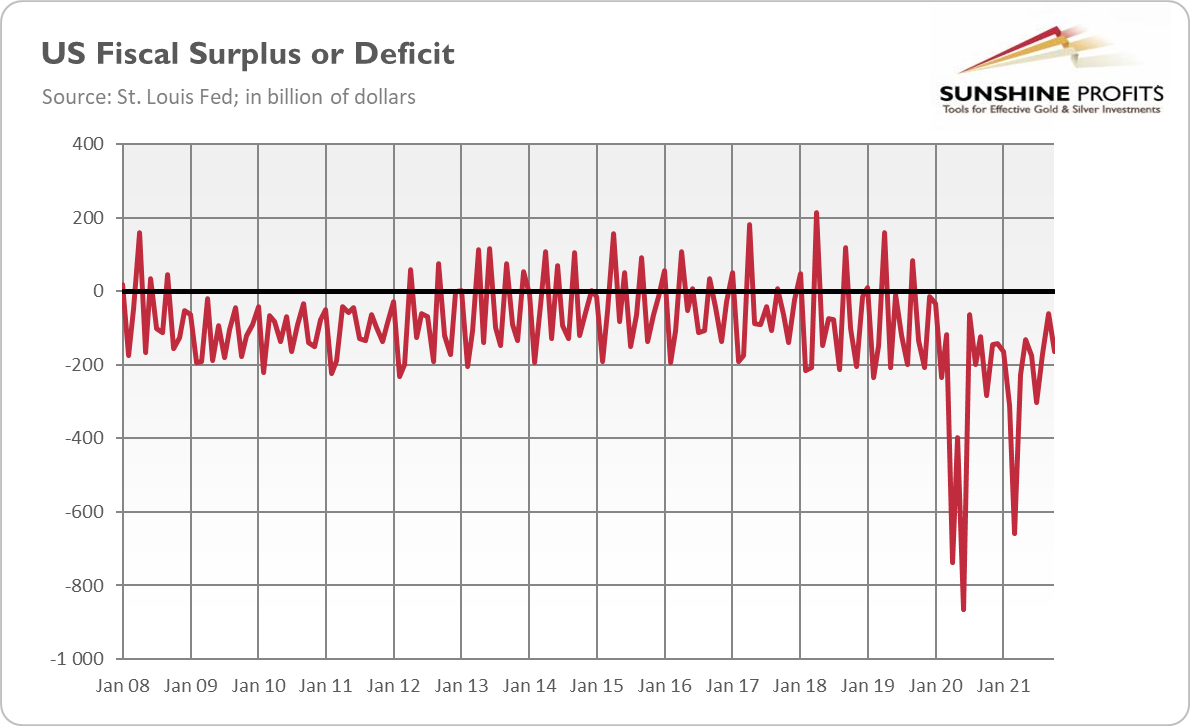

Of course, neither infrastructure nor spending bill will increase the fiscal deficits and overall indebtedness to a similar extent as the pandemic spending packages. These funds will be spread over years. Additionally, the fiscal deficit should narrow in FY 2022 as pandemic relief spending phases out (this is already happening, as the chart below shows), while the economic recovery combined with inflation tax bracket creep increases tax revenues.

However, both of Biden’s bills will increase indebtedness, lowering the financial resilience of the US economy. What’s more, the overall debt is much larger than the public debt I focused on here. Other categories of debt are also rising. For instance, total household debt has jumped 6.2% in the third quarter of 2021 year-over-year, to a new record of $15.2 trillion.

Implications for Gold

What does the fiscal offensive imply for the precious metal market? In the short run, not much. Fiscal hawks like me will complain, but gold is a tough metal that does not cry. Both of Biden’s pieces of legislation have been widely accepted, so their impact has already been incorporated into prices. Actually, the actual bills could be even seen as conservative – compared to Biden’s initial radical proposals.

In the long run, fiscal exuberance should be supportive of gold prices. The ever-rising public debt should zombify the economy and erode the confidence in the US dollar, which could benefit the yellow metal. However, the empire collapses slowly, and there is still a long way before people cease to choose the greenback as their most beloved currency (there is simply no alternative!).

So, it seems that, in the foreseeable future, gold’s path will still be dependent mainly on inflation worries and expectations of the Fed’s action. Most recently, gold prices have stabilized somewhat after the recent rally, as the chart below shows.

Normal profit-taking took place, but gold found itself under pressure also because of the hawkish speech by Fed Governor Christopher Waller. He described inflation as a heavy snowfall that would stay on the ground for a while, rather than a one-inch dusting:

Consider a snowfall, which we know will eventually melt. Snow is a transitory shock. If the snowfall is one inch and is expected to melt away the next day, it may be optimal to do nothing and wait for it to melt. But if the snowfall is 6 to 12 inches and expected to be on the ground for a week, you may want to act sooner and shovel the sidewalks and plow the streets. To me, the inflation data are starting to look a lot more like a big snowfall that will stay on the ground for a while, and that development is affecting my expectations of the level of monetary accommodation that is needed going forward.

So, brace yourselves, a janitor is coming with a big shovel to clean the snow! Just imagine Powell with a long-eared cap, gloves, and galoshes giving a press conference! At least the central bankers would finally do something productive! Or… maybe shoveling is not coming! Although the Fed may turn a bit more hawkish if inflation stays with us for longer than expected previously, it should remain behind the curve, while the real interest rates should stay ultra-low. The December FOMC meeting will provide us with more clues, so stay tuned!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Investors Expect High Inflation. Golden Inquisition Ahead?

November 18, 2021, 9:04 AMInflation expectations reached a record high. Is gold preparing a counterattack to punish gold bears?

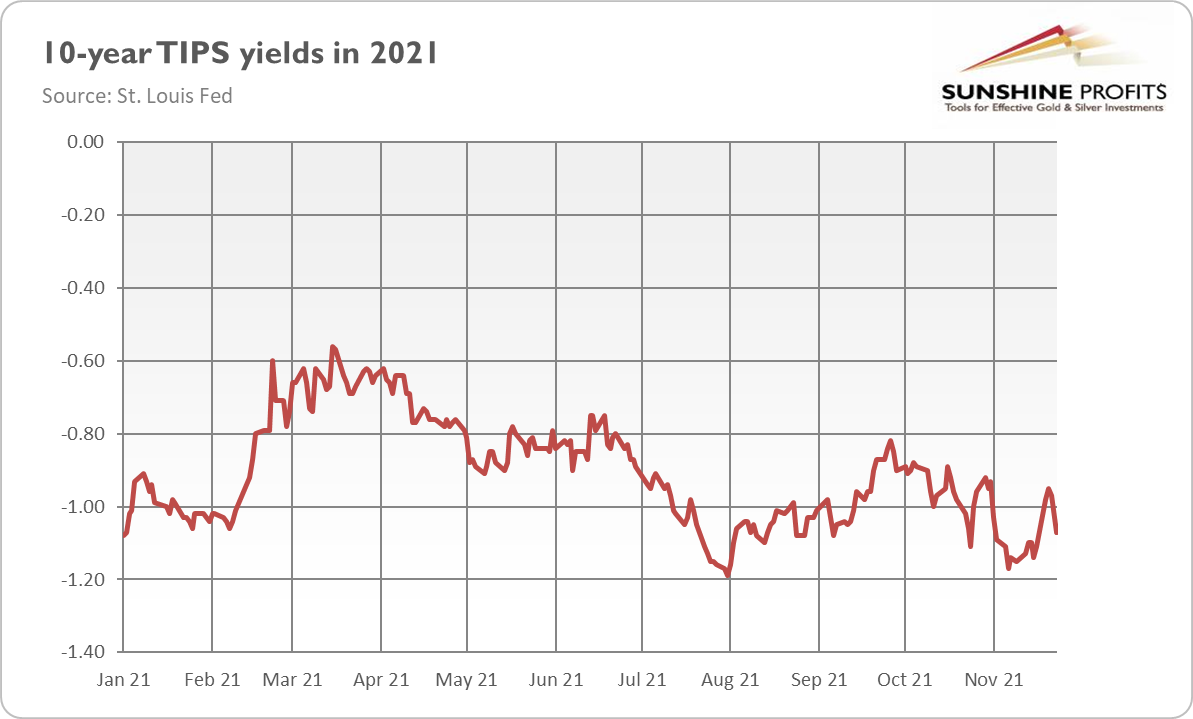

In a classic Monty Python sketch, nobody expects the Spanish inquisition. In the current marketplace, everyone expects high inflation. As the chart below shows, the inflation expectations embedded in US Treasury yields have recently risen to the highest level since the series began in 2003.

Houston, we have a problem, an unidentified object is flying to the moon! The 5-year breakeven inflation rate, which is the difference between the yields on ordinary Treasury bonds and inflation-protected Treasuries with the same maturity, soared to 2.76% on Monday. Meanwhile, the 10-year breakeven inflation rate surged to 3.17%. The numbers show the Treasury market’s measure of average CPI annual inflation rates over five and ten years, respectively.

The chart is devastating for the Fed’s reputation if there’s anything left. You probably remember how the US central bank calmed investors, saying that we shouldn’t worry about inflation because inflation expectations are well-anchored. No, they don’t!

Of course, the current inflation expectations oscillate around 3%, so they indicate that the bond market is anticipating a pullback in the inflation rate from its current level. Nevertheless, the average of 3% over ten or even just five years would be much above the Fed’s target of 2% and would be detrimental for savers in particular, and the US economy in general.

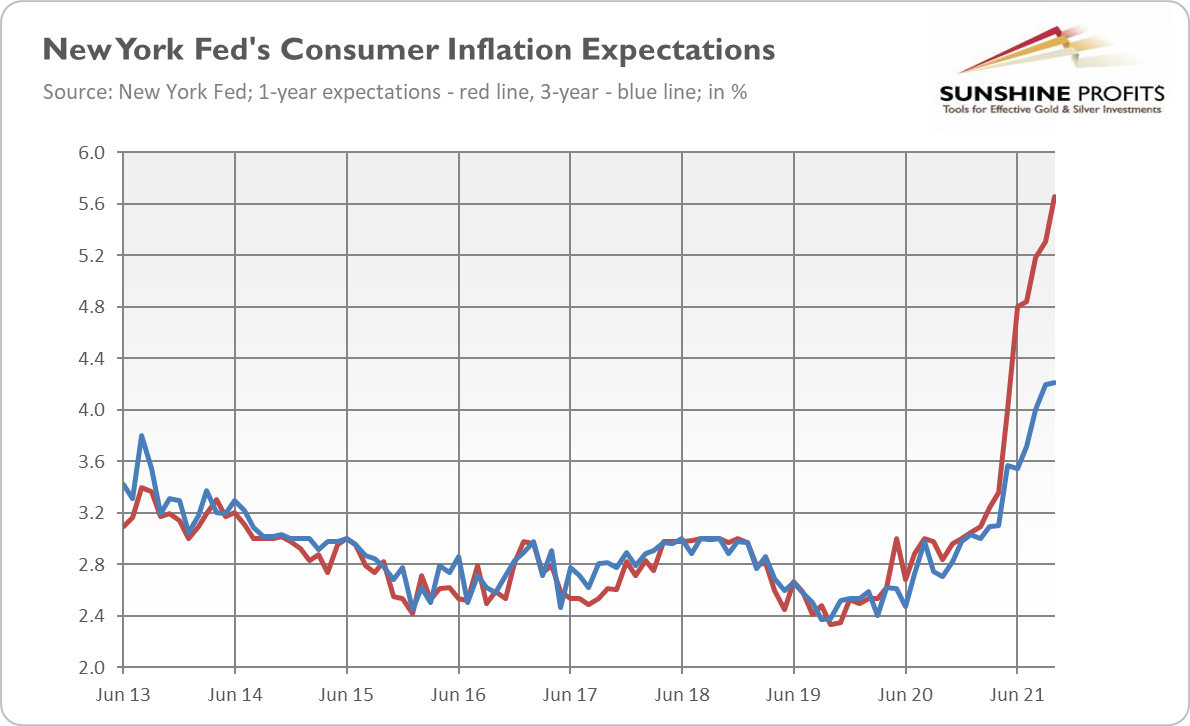

I’ve already shown you market-based inflation expectations, which are relatively relaxed, but please take a look at the chart below, which displays the consumer expectations measured by the New York Fed’s surveys. As one can see, the median inflation expectations at the one-year horizon jumped 0.4 percentage point in October, to 5.7%. So much for the inflation expectations remaining under control!

Implications for Gold

Surging inflation expectations are positive for the gold market. They should lower real interest rates and strengthen inflationary worries. This is because the destabilized inflation expectations may erode the confidence in the US dollar and boost inflation in the future. So, gold could gain as both an inflation hedge and a safe haven.

And, importantly, the enlightened Fed is likely to remain well behind the curve in setting its monetary policy. This is even more probable if President Biden appoints Lael Brainard as the new Fed Chair. She is considered a dove, even more dovish than Powell, so if Brainard replaces him, investors should expect to see interest rates staying lower for longer. So, inflation expectations and actual inflation could go even higher.

Hence, the dovish Fed combined with high inflation (and a slowdown in GDP growth) creates an excellent environment for gold to continue its rally. After all, the yellow metal has broken out after several months of consolidation (as the chart below shows), so the near future seems to be brighter.

There are, of course, some threats for gold, as risks are always present. If the US dollar continues to strengthen and the real interests rebound, gold may struggle. But, after the recent change, the sentiment seems to remain positive.

Anyway, I would like to return to the market-based inflation expectations and the famous Monty Python sketch. With an inflation rate of 3%, which is the number indicated by the bond market, the capital will halve in value in just 24 years! So, maybe it would be a too-far-reaching analogy, but Monty Python inquisitors wanted to use a rack to torture heretics by slowly increasing the strain on their limbs and causing excruciating physical pain (luckily, they were not the most effective inquisitors!). Meanwhile, inflation hits savers by slowly decreasing the purchasing power of money and causing significant financial pain.

With the inflation rate at about 6%, hedging against inflation is a no-brainer. It’s a matter of financial self-defense! You don’t have to use gold for this purpose – but you definitely can. After several disappointing months, and the lack of gold’s reaction to inflation, something changed, and gold has managed to break out above $1,800. We will see how it goes on. I will feel more confident about the strength of the recent rally when gold rises above $1,900.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM