-

Bulls or Bears: Who Is Pulling Santa’s Gold Sleigh?

December 23, 2021, 6:00 AMSanta Claus is coming to town! What will he give gold: a gift or a rod?

During the holiday week, not much happens in the marketplace. Investors focus on two things right now: whether Democrats will be able to pass Biden’s spending bill in the face of Senator Joe Manchin’s opposition, and whether the coronavirus Omicron variant will trigger new restrictions and hamper economic growth. After all, this strain has already become the dominant one in the US, but its effects are not yet known.

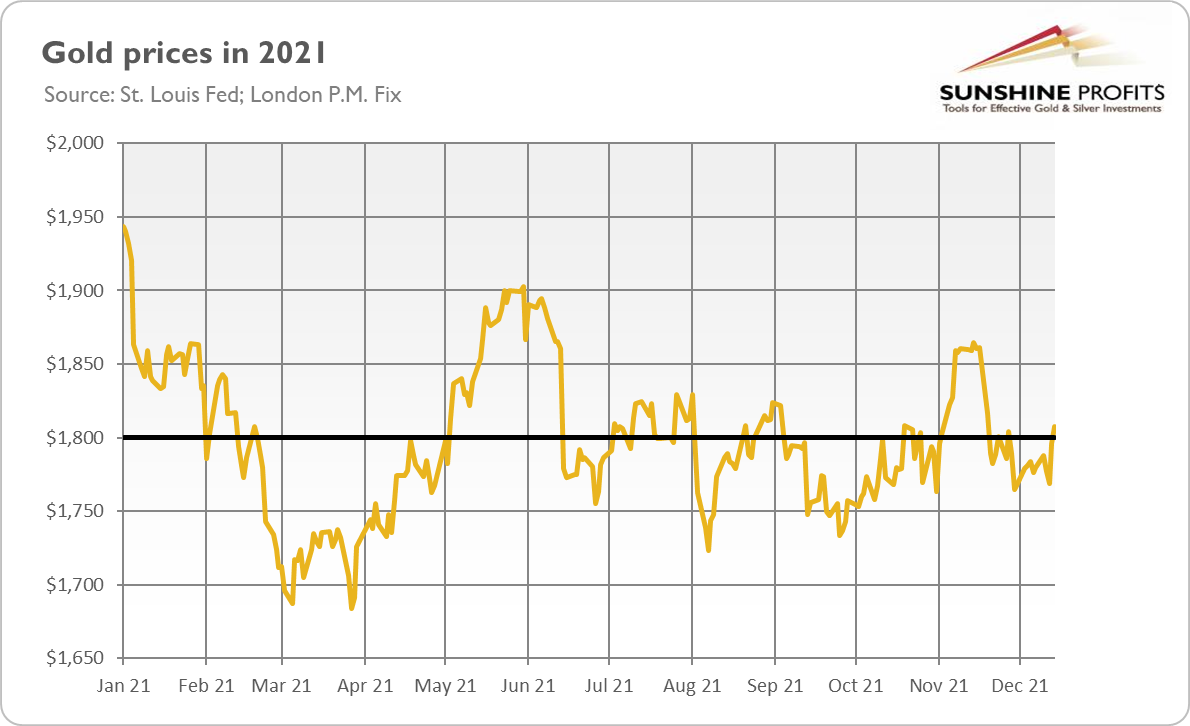

Like most of 2021, gold has been rubbing against $1,800 this week but did not have the strength to permanently rise above this level. Despite a surge in inflation and very low real interest rates, the yellow metal didn’t rally. Thus, we could say that gold was rather naughty this year and doesn’t deserve gifts from Santa.

However, maybe it’s not gold’s fault, but our too high expectations? After all, gold had to compete with cryptocurrencies and industrial metals (or commodities in general), both of which performed exceptionally well during periods of high inflation. Despite all the Fed’s hawkish rhetoric and tapering of quantitative easing, gold didn’t break down.

Hence, it all depends on the perspective. The same applies to historical analyses and forecasts for 2022. The bears compare the current situation with the 2011-2013 period. The 2020 peak looked like the 2011 peak. Thus, after a period of consolidation, we could see a big decline, just as it happened in 2013.

On the other hand, gold bulls prefer to compare today with 2015, as we are only a few months away from the Fed’s interest rate hikes. As a reminder, gold bottomed in December 2015, so the hope is that we will see another bottom soon, followed by an upward move. In other words, the bears believe that the replay of the “taper tantrum” is still ahead of us, while the bulls claim that the worst is already behind us.

Implications for Gold

Who is right? Of course, me! But seriously: both sides make valid points. Contrary to 2013, the current tapering was well telegraphed and well received by the markets. Thus, the worst can indeed be already behind us. Especially that the 2020 economic crisis was very deep, but also very short, so everything was very condensed. I mean: the Great Recession lasted one and a half years, while the Great Lockdown lasted only two months. The first taper tantrum occurred in 2013, while the first hike in the federal funds rate – at the end of 2015. We won’t wait that long now, so the period of downward pressure on gold prices stemming from expectations of the Fed’s tightening cycle will be limited.

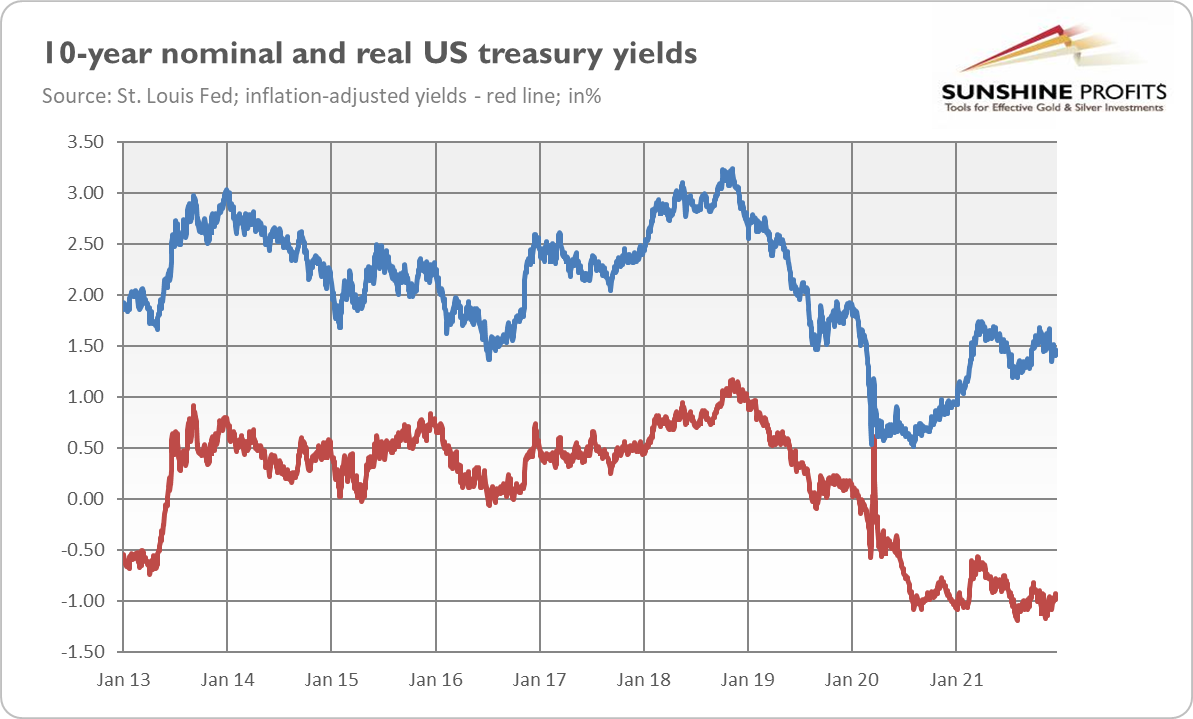

Having said that, gold bears highlight an important point: real interest rates haven’t normalized yet. As the chart below shows, although nominal bond yields have rebounded somewhat from the August 2020 bottom, real rates haven’t followed. The reason was, of course, the surge in inflation. However, if inflation eases, inflation-adjusted rates will go up. Additional risk here is that the Fed will surprise the markets on a hawkish side.

The bottom line is that Santa Claus may bring gold a rod this time. Although gold’s reaction to the recent FOMC meeting was solid, the overall performance of the yellow metal this month is worse compared to the historically strong action in December. I don’t expect a similarly strong downward move as in 2013, but real interest rates could normalize somewhat in 2022, given the upcoming Fed’s tightening cycle and possible peak in inflation. The level of indebtedness will limit the scope of the move, but it won’t change the direction.

Anyway, whether you are a gold bull or a gold bear, I wish you a truly merry and golden Christmas (or just winter holidays)! Let the profits shine, even if gold won’t!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Powell Sent Gold Above $1,800 – But Only for a Short While

December 21, 2021, 7:03 AMFinally, Powell admitted higher inflation risks and gold jumped above $1,800. Before anyone noticed, however, it plummeted below the key level again.

Who are you, Mr. Powell: a reptilian or a human? A dove or a hawk? Since we all know the answer to the first question, let’s focus on the second one. Markets decided that Powell’s last press conference was rather dovish, but a careful reading doesn’t support this view. The main dovish signal was Powell’s emphasis that quantitative easing tapering and interest rate hikes are separate issues, as the tightening cycle criteria are stricter. So, the first rate hike may not come immediately after the end of tapering, which is scheduled for mid-March.

Even if they are separate, we shouldn’t expect a long break between the end of quantitative easing and the first rate hike. This gap will definitely be shorter than in 2014-2015. In the last tightening cycle, the Fed ended asset purchases in October 2014, while the first increase in the federal funds rate occurred in December 2015. Powell himself, however, pointed out that the economy is much stronger, while inflation is much higher, so a long separation before interest rate hikes is not likely:

I don't foresee that there would be that kind of very extended wait at this time. The economy is so much stronger. I was here at the Fed when we lifted it off last time and the economy is so much stronger now, so much closer to full employment. Inflation is running well above target and growth as well above potential. There wouldn't be the need for that kind of long delay (…) The last cycle that was quite a long separation before interest rates, I don't think that's at all likely in this cycle. We're in a very, very different place with high inflation, strong growth, a really strong economy (…) So this is a strong economy, one in which it's appropriate for interest rate hikes.

In fact, this delay may be very short. On Friday, Fed Governor Chris Waller said that the interest rate increase will likely be warranted “shortly after” the end of asset purchases, possibly even at the FOMC meeting in March 2022.

Another hawkish message sent by Powell was his acknowledgment of stronger inflation risks, i.e., that inflation may turn out to be more lasting than expected now:

There’s a real risk now, we believe, I believe, that inflation may be more persistent and that may be putting inflation expectations under pressure. And that the risk of higher inflation becoming entrenched has increased, it’s certainly increased. I don’t think it’s high at this moment, but I think it’s increased. And I think that’s part of the reason behind our move today, is to put ourselves in a position to be able to deal with that risk.

Thus, the Fed has become more concerned about high inflation and has timidly started reacting to it. The acceleration in the pace of tapering was, except for the more hawkish rhetoric, the first step – but not the last one.

Implications for Gold

The yellow metal responded surprisingly well to the last FOMC meeting, at which the Fed announced a more aggressive pace of tapering and rate hikes next year. As the chart below shows, gold rose almost $40, or more than 2%, from Wednesday to Friday last week, jumping again above the key level of $1,800.

Perhaps investors expected even more forceful actions. After all, despite all the hawkish reaction, the Fed remains behind the curve and shows no hurry to become really proactive. Such a passive attitude is really risky, as history teaches us that high inflation doesn’t just go away on its own, but its stabilization requires a decisive tightening of monetary policy. The longer the Fed waits, the more severe reaction would be needed, which increases the odds of putting the economy into recession.

All this seems bullish for gold prices. However, gold was unable to retain its position above $1,800 and declined on Monday (December 20, 2021), so gold bulls can only hope that the yellow metal will the find strength to rally next year. It’s possible if inflation wreaks more havoc in 2022, but a hawkish Fed’s rhetoric remains an important headwind for the gold market.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Fed Accelerates Tapering, but Gold Shows Resilience

December 16, 2021, 9:03 AMThe Fed begins to get up steam and has finally turned its hawkish mode on. Was it something the gold bulls wanted to hear?

The Fed’s full capitulation and unconditional surrender of the doves! Yesterday (December 15, 2021), the FOMC issued) the newest statement on monetary policy in which it erased any description of inflation as “transitory.” It took them only half a year to figure it out, but better late than never. Additionally, the Fed practically rejected its new monetary framework called “Flexible Average Inflation Targeting”, which allowed inflation to run hot for some time. In November, we could read:

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation having run persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

In the last statement, however, this mammoth paragraph was substantially altered.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent. With inflation having exceeded 2 percent for some time, the Committee expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment.

What is missing is the reference to the Fed’s tolerance of inflation above its target. This means that the US central bank has turned the hawkish mode on. Indeed, in line with expectations, the Fed has accelerated the pace of tapering of its quantitative easing. The Committee announced a doubling of the monthly reduction in the purchased assets from $10 billion for Treasuries and $5 billion for MBS to, respectively, $20 and $10 billion. It means that the Fed will end its asset purchase program by March rather than by mid-year.

In light of inflation developments and the further improvement in the labor market, the Committee decided to reduce the monthly pace of its net asset purchases by $20 billion for Treasury securities and $10 billion for agency mortgage-backed securities.

Dot-Plot and Gold

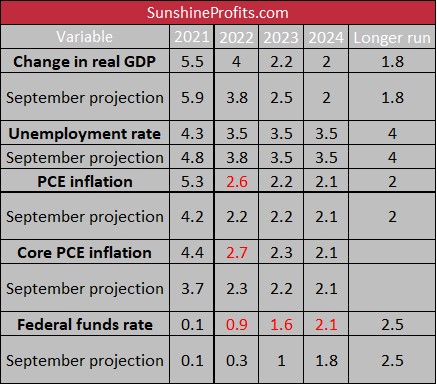

These are not all December monetary fireworks we got, though. The statement was accompanied by fresh economic projections conducted by FOMC members. How do they look at the economy right now? As the table below shows, central bankers expect faster economic growth and a lower unemployment rate next year compared to the September projections. This is not something the gold bulls would like to hear.

More importantly, however, FOMC participants see inflation as more persistent at the moment because they expect 2.6% PCE inflation at the end of 2022 instead of 2.2%. In other words: inflation is currently believed to reach this level only a year from now! Interestingly (at least for economic nerds like me), Committee members expect that core PCE inflation will be higher than the overall index in 2022, and will amount to 2.7%. It is an indication that the Fed considers inflation more broad-based now than just driven by rising energy prices.

Last but definitely not least, more interest rate hikes are coming. According to the latest dot plot, FOMC members see three increases in the federal funds rate next year as appropriate. That’s a huge hawkish turn compared to September, when they perceived only one interest rate hike as desired. Central bankers expect another three hikes in 2023 (the same as in September) and additional two in 2024 (one less than in September). Hence, the whole forecasted path of the interest rates becomes steeper and the Fed is now anticipating eight 25-basis point rate hikes from 2022 to 2024, one more than they saw in September.

Implications for Gold

Given the hawkish FOMC statement and economic projections, gold is doomed, right? Well, in theory, a more aggressive Fed’s tightening cycle should boost bond yields and strengthen the greenback, pushing gold prices down. However, what does gold say to the God of Bears? Not today!

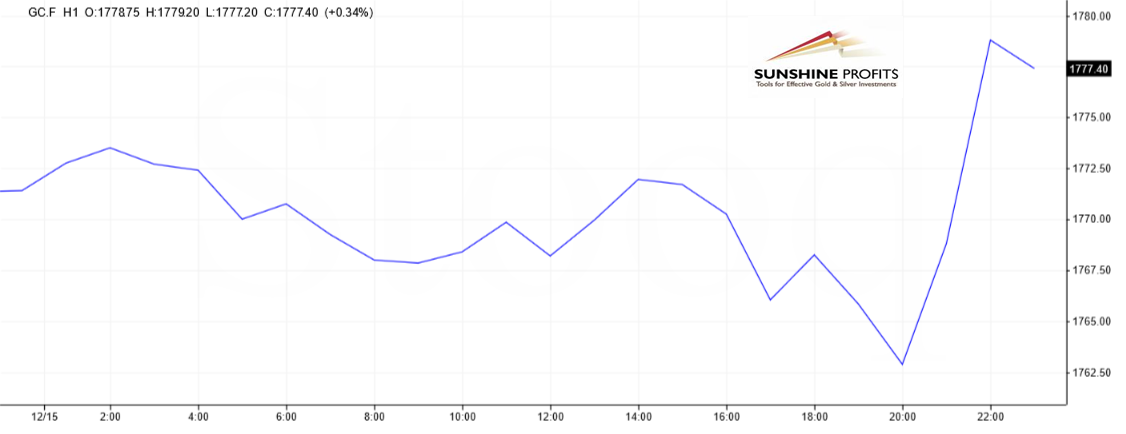

Indeed, the chart below shows that theory and practice are not the same. Initially, the price of gold declined from around $1,765 to around $1,755, but it quickly rebounded and even increased to $1,780.

So, what happened and what does it imply for gold’s future? Well, gold didn’t panic, as hawkish statements and dot-plot were widely anticipated. They were probably a little more hawkish than expected, but, on the other hand, Powell’s press conference was deemed as more dovish than predicted. Since Powell’s earlier transparency and dovish heart rescued gold from falling down, gold bulls may breathe a sigh of relief.

However, we believe that this wasn’t the Fed’s last word. Inflation is likely to increase further next year; so, the US central bank, which is terribly behind the curve, could be forced to tighten its monetary policy even more. Thus, although my worries about this FOMC meeting turned out to be unnecessary, they could materialize later.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Inflation Beast Roars - Gold Only Modestly Up

December 14, 2021, 10:39 AMThe inflation beast is growing stronger. Unfortunately for gold bulls, we cannot say the same about the yellow metal. Is sacrifice going on tomorrow?

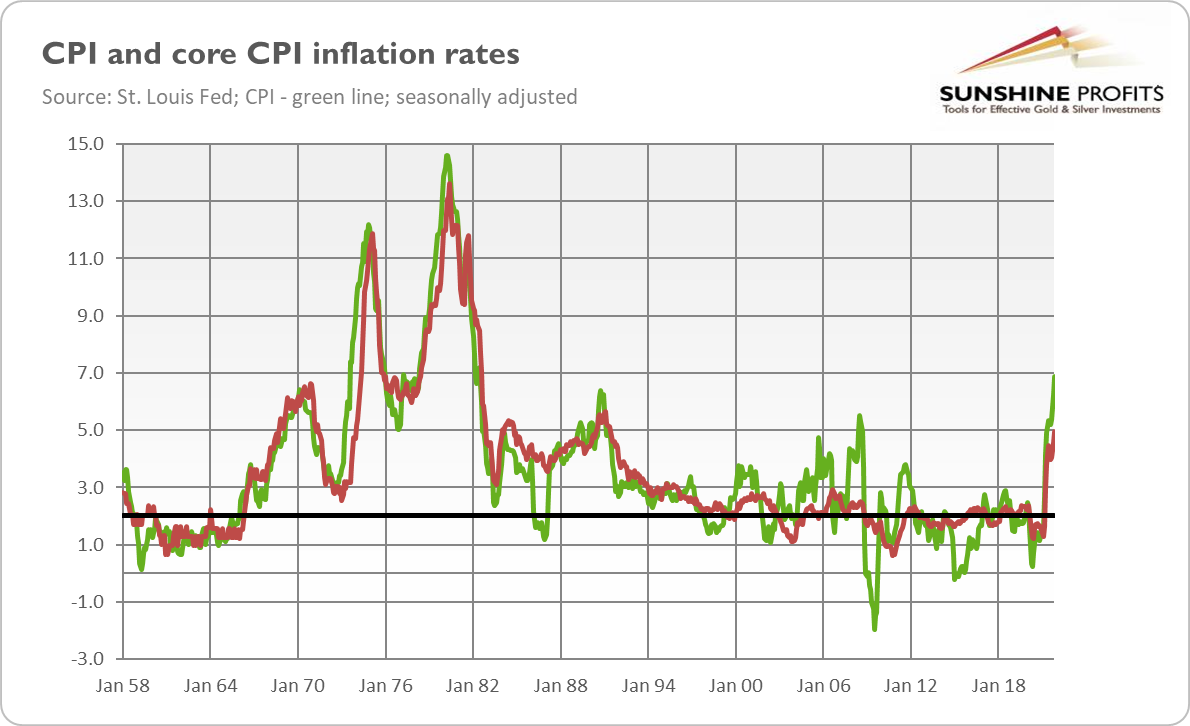

“Woe to you, oh earth and sea, for the Devil sends the beast with wrath, because he knows the time is short (...). Let him that hath understanding count the number of the beast,” says the Bible. The current number of the beast is not 6.66%, but 6.8% - this is how high the CPI annual inflation rate was in November.

The number came above expectations and implies further acceleration in inflation from 6.2% in October. It was also the largest 12-month increase since the period ending June 1982, as the chart below indicates.

The latest BLS report on inflation also shows that consumer inflation rose 0.8% on a monthly basis after rising 0.9% in October. The core CPI rate increased 0.5% in November, following a 0.6-percent increase in the previous month. On an annual basis, it jumped 5% after a 4.6% increase in October (see the chart above). So, as Iron Maiden sings, “hell and fire was spawned to be released”.

Indeed, November readings clearly falsify central banks’ narrative about transitory inflation (which was already partially abandoned) and confirm my claim that inflation will stay with us for longer. As a reminder, my bet is that we will see the peak of inflation no earlier than somewhere in Q1 2022. Actually, it might be even a bit later, as the Omicron coronavirus variant could contribute to supply disruptions and add to inflationary pressure.

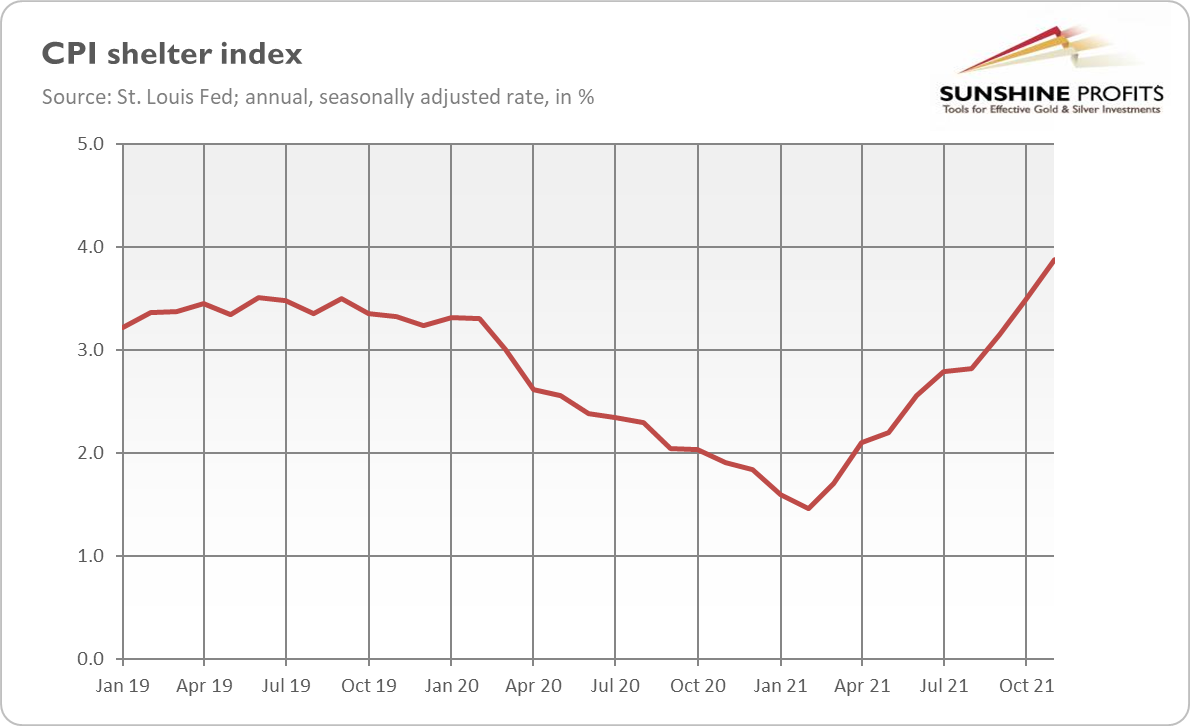

What’s important here is to remember that current inflation is not merely a supply problem. It’s true that the energy index is surging, but the shelter index is also rising, and it has even surpassed the pre-pandemic level, as the chart below shows. So, inflation has a really broad nature, which makes perfect sense, as it was caused by a boost in the money supply and strong demand. The BLS report confirms this view: “The monthly all items seasonally adjusted increase was the result of broad increases in most component indexes, similar to last month.”

Implications for GoldThe inflationary beast not only reared its ugly head, but it started roaring and growing stronger. The CPI inflation rate jumped to 6.8% in November, and it’s probably not the final number! Actually, it could have been even higher if the Omicron variant of coronavirus had not emerged, slowing down some expenditures.

What does this acceleration imply for the gold market? Well, one week ago I wrote: “My bet is that inflation will stay elevated or that it could actually intensify further. In any case, the persistence of high inflation could trigger some worries and boost the safe-haven demand for gold.” Indeed, inflationary pressure intensified further, which pushed gold prices higher, as the chart below shows.

However, I also expressed concerns about the Fed’s reaction to high inflation and its implications for gold:

I’m afraid that gold bulls’ joy would be – to use a trendy word – transitory. The December FOMC meeting will be probably hawkish and will send gold prices down. Given the persistence of inflation, the Fed is likely to turn more hawkish and accelerate the pace of tapering.

The higher than expected inflation rate in November, and a very modest gold’s reaction to it, only strengthen my fears that tomorrow could be a great day for monetary hawks and a sad day for gold. Given such high inflation, the Fed has simply no choice and must accelerate the pace of the tapering and hiking cycle. So, to paraphrase Iron Maiden, sacrifice is going on tomorrow.

On the other hand, gold often bottomed out in December historically (in recent years, it did so in 2015, 2016, 2017, and 2019). We’ll find out soon whether my fears were justified!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Stuck Between High Inflation and Strong Dollar

December 9, 2021, 10:21 AMInflation supports gold, the expected Fed’s reaction to price pressure – not. Since gold ended November with a small gain, what will December bring?

I have good and bad news. The good is that the price of gold rose 2% in November. The bad –is that the price of gold rose 2% in November. It depends on the perspective we adopt. Given all the hawkish signals sent by the Fed and all the talk about tapering of quantitative easing and the upcoming tightening cycle, even a small increase is an admirable achievement.

However, if we focus on the fact that US consumer inflation rose in October to its highest level in 30 years, and that real interest rates have stayed deeply in negative territory, gold’s inability to move and stay above $1,800 looks discouraging.

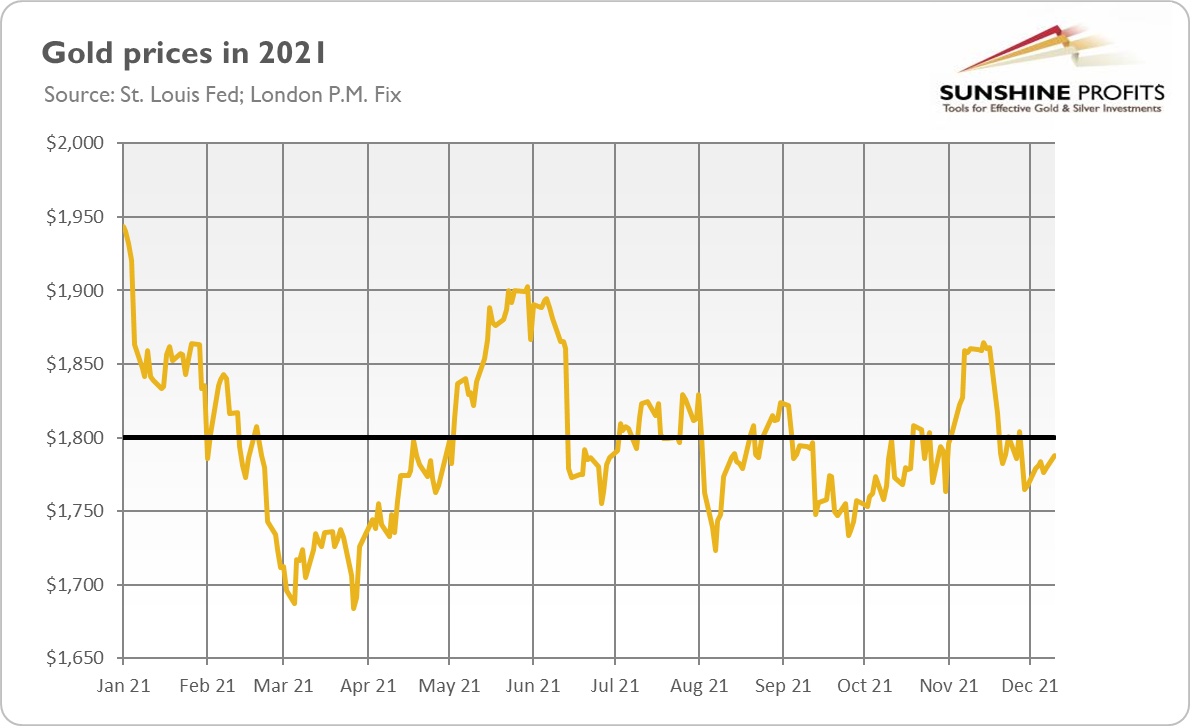

We can also look at it differently. The good news would be that gold jumped to $1,865 in mid-November. The bad news, on the other hand, would be that this rally was short-lived with gold prices returning to their trading range of $1,750-$1,800 in the second half of the month, as the chart below shows.

Now, according to the newest WGC’s Gold Market Commentary, gold’s performance in November resulted from the fact that higher inflation expectations were offset by a stronger dollar and rising bond yields that followed Powell’s nomination for the Fed Chair for the second term.

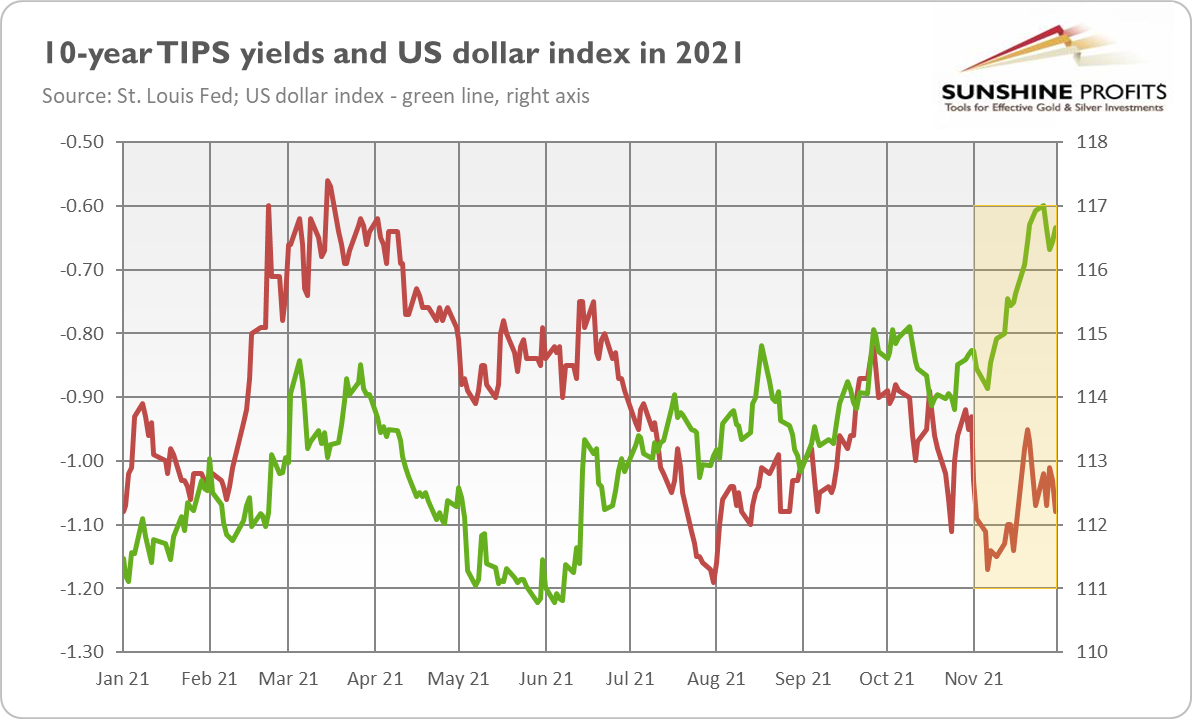

Indeed, as you can see in the chart below, the greenback strengthened significantly in November, and real interest rates rallied for a while. Given the scale of the upward move in the dollar, and that it was combined with a surge in yields, gold’s performance last month indicates strength rather than weakness. As the WGC notes, “dollar strength was a headwind in November, acting as a drag on gold’s performance, but not enough to outweigh inflation concerns.”

Implications for Gold

Great, but what’s next for the gold market in December and 2022? Well, that’s a good question. The WGC points out that “gold remains heavily influenced by investors’ continued focus on the path of inflation (…) and the Fed’s and other central banks’ potential reaction to it.” I agree. Inflation worries increase demand for gold as an inflation hedge, supporting gold, but they also create expectations for a more hawkish Fed, hitting the yellow metal.

It seems that the upcoming days will be crucial for gold. Tomorrow (December 10, 2021), we will get to know CPI data for November. And on Wednesday (December 15, 2021), the FOMC will release its statement on monetary policy and updated dot plot. My bet is that inflation will stay elevated or that it could actually intensify further. In any case, the persistence of high inflation could trigger some worries and boost the safe-haven demand for gold.

However, I’m afraid that gold bulls’ joy would be – to use a trendy word – transitory. The December FOMC meeting will probably be hawkish and will send gold prices down. Given the persistence of inflation, the Fed is likely to turn more hawkish and accelerate the pace of tapering.

Of course, if the Fed surprises us on a dovish side, gold should shine. What’s more, the hawkish tone is widely expected, so it might be the case that all the nasty implications are already priced in. We might see a “sell the rumor, buy the fact” scenario, but I’m not so sure about it. The few last dot-plots surprised the markets on a hawkish side, pushing gold prices down. I’m afraid that this is what will happen again. Next week, the Fed could open the door to earlier rate hikes than previously projected. Hence, bond yields could surge again, making gold move in the opposite direction. You’ve been warned!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM