-

Surging Home Prices and Gold – What’s the Link?

September 2, 2021, 7:46 AMUS home prices are surging, increasingly raising worries about inflation. Could gold follow houses? If so, why?

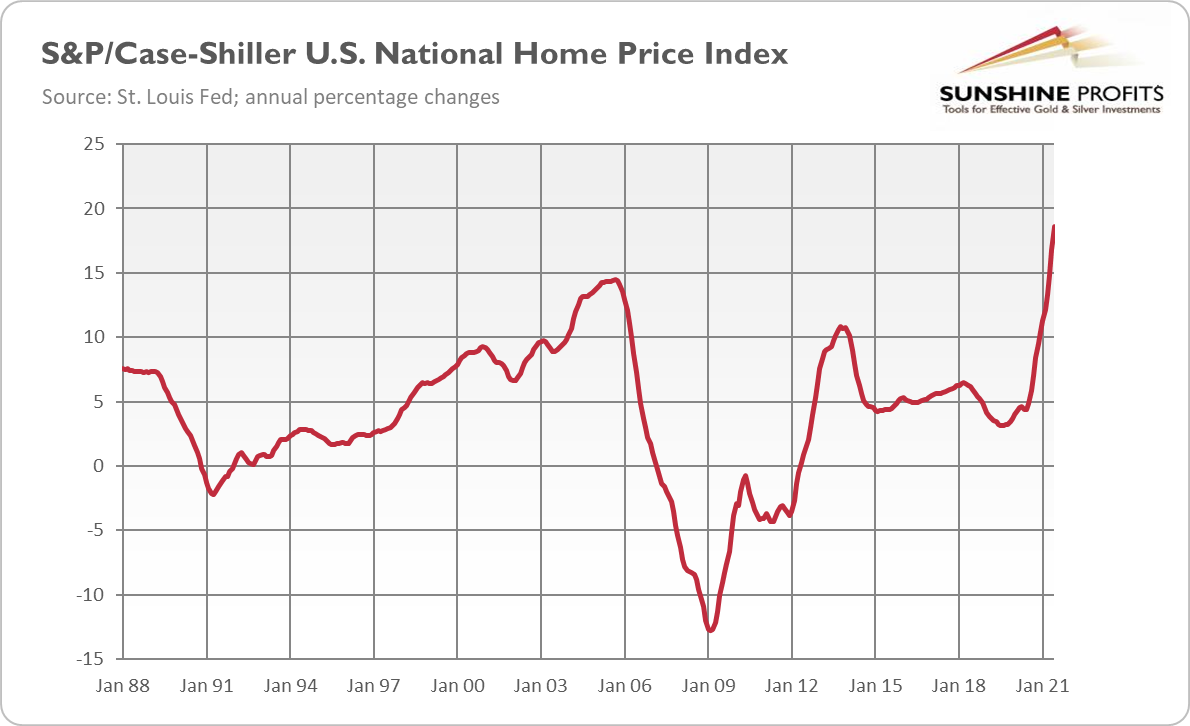

Home price growth in the US has accelerated even further, reaching a new record. The S&P/Case-Shiller U.S. National Home Price Index rose from 255.3 in May to 260.9 in June, boosting the annual percentage gain from 16.8% to 18.1%, as the chart below shows. That’s the largest jump since 1988 when the series began.

Why is it so important? Well, for two reasons. First, such quick growth in home prices increases the risk of a housing bubble and all related economic problems. Please note that home prices are surging now even faster than in the 2000s, which ended in a financial crisis and the Great Recession.

Second, rallying home prices add to the inflationary pressure. What’s important, this year’s impressive home inflation hasn’t shown up in the CPI yet. It will though, as increases in house prices translate into housing inflation, which lifts consumer price measures. This effect may be substantial, given that shelter represents one-third of the overall CPI and about 40% of the core CPI.

Indeed, the recent research from the Dallas Fed, entitled “Surging House Price Expected to Propel Rent Increases, Push Up Inflation”, finds that rising housing prices are usually a leading indicator for rents that are included in the CPI. According to the authors, the correlation between house price growth and rent inflation is the strongest with about an 18-month lag. It means that rent inflation is likely to increase substantially over the next two years, contributing materially to consumer price indexes:

Our forecasting model shows that rent inflation and OER inflation are expected to increase materially in 2022 and 2023. Given their weights in the core PCE price index (which excludes food and energy), rent and OER together are expected to contribute about 0.6 percentage points to 12-month core PCE inflation for 2022 and about 1.2 percentage points for 2023. These forecasts also suggest that rising inflation for rent and OER could push the overall and core PCE inflation rates above 2 percent in 2023, when current supply bottlenecks and labor shortages may have subsided.

So, this research suggests that inflation could stay significantly above the Fed’s target in the coming years and that it might be more persistent than it’s widely believed by the central bankers and Wall Street. In other words, the Fed’s own research suggests that the US central bank might be wrong in claiming that inflation will prove to be temporary – after all, the core inflation is expected to stay above 2%, even when supply-side disruptions resolve.

Importantly, soaring home prices are not the only factor adding to inflation worries. Another one is the fall in consumer confidence in August, partly because of stronger expectations of inflation. According to the Conference Board, consumers’ inflation expectations over the next year increased from 6.6% in July to 6.8% in August.

Last but not least, inflation in the Eurozone has also surged recently. It soared from 2.2% in July to 3% in August, far above expectations and the ECB’s target. The global character of inflation (although it’s stronger in the US) suggests that it’s not caused merely by idiosyncratic factors (as Powell claims), but rather by the combination of supply-side disturbances and demand factors, such as an increase in the money supply entering the economy through consumer spending.

Implications for Gold

What does it all mean for the gold market? Well, rising home prices imply that inflation will be higher in the future than widely expected. Higher inflation could increase the demand for gold as an inflation hedge. It’s also the best guarantee that real interest rates will stay low, which should support gold. More persistent inflation increases the odds of stagflation, gold’s favorite macroeconomic environment.

However, higher inflation could force the Fed to adopt a more hawkish stance and, for example, accelerate its tapering of quantitative easing, which could exert some downward pressure on gold. Actually, this is what is happening right now. Given high inflation, low bond yields and the US dollar in a sideways trend, gold seems undervalued to many analysts. On the other hand, the narrative about transitory inflation combined with the prospects of the Fed’s tightening cycle could make gold struggle.

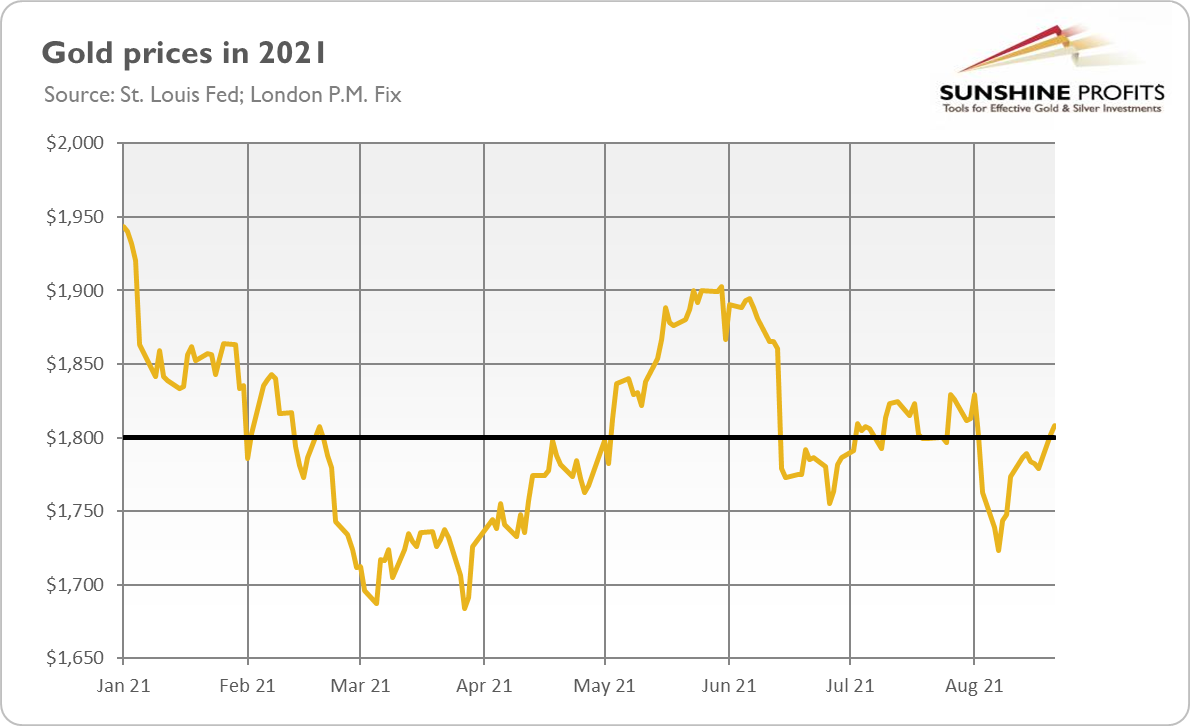

Having said that, gold has recently managed to return above $1,800 again, while September is historically a good month for gold. So, we will see – this month’s FOMC meeting could be crucial in determining the yellow metal’s path.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Moves Above $1,800 After Jackson Hole

August 31, 2021, 6:27 AMThe Jackson Hole is over — we left it in the rearview mirror. Gold moved higher in an immediate reaction, but bullish joy may be premature.

The 2021 Jackson Hole Economic Symposium “Macroeconomic Policy in an Uneven Economy” is already a thing of the past. It was a stimulating conference with a few interesting presentations. But the key appearance for the financial markets was Powell’s speech. Let’s dig into it!

So, the Fed Chair started his remarks with the observation that even though the pandemic recession was the briefest yet deepest on record, the pace of the recovery has exceeded expectations. That being said, the economic expansion has been uneven, and its continuation is threatened by the Delta variant of the coronavirus, high inflation and the remaining slack in the labor market. However, Powell was generally optimistic about the future, saying that the prospects were good for continued progress toward maximum employment, while the elevated inflation would likely be temporary:

The baseline outlook is for continued progress toward maximum employment, with inflation returning to levels consistent with our goal of inflation averaging 2 percent over time.

Actually, Powell was so optimistic about the US economy that he stated that the criteria for tapering of the quantitative easing had been met. The key passage from his speech is as follows:

We have said that we would continue our asset purchases at the current pace until we see substantial further progress toward our maximum employment and price stability goals, measured since last December, when we first articulated this guidance. My view is that the "substantial further progress" test has been met for inflation. There has also been clear progress toward maximum employment. At the FOMC's recent July meeting, I was of the view, as were most participants, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year. The intervening month has brought more progress in the form of a strong employment report for July, but also the further spread of the Delta variant. We will be carefully assessing incoming data and the evolving risks. Even after our asset purchases end, our elevated holdings of longer-term securities will continue to support accommodative financial conditions.

This passage is clearly hawkish, as it implies that the Fed will probably end its asset purchases this year if nothing bad happens.

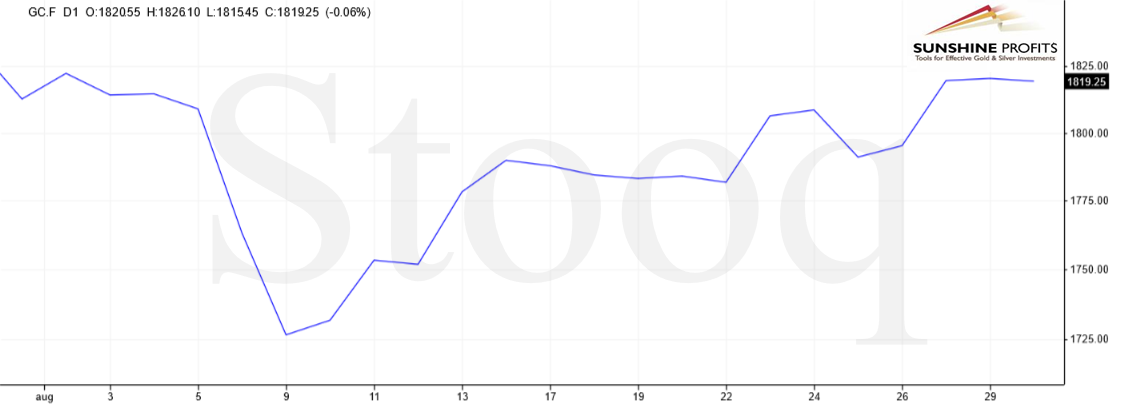

However, the price of gold futures increased on Friday (after Powell’s remarks) from around $1,790 to almost $1,820, as the chart below shows. Why? Well, it seems that the markets read between the lines and interpreted the Fed Chair’s speech as actually quite dovish, or less hawkish than expected.

After all, Powell didn’t present any clear timeline of the Fed’s tightening cycle. Although the Fed Chair mentioned that it could be appropriate to start reducing the pace of asset purchases this year, he also noted some uncertainty about the spread of Delta and its economic aspect.

What’s more, Powell reminded the public that the tapering doesn’t automatically imply hiking the federal funds rate, as raising interest rates would require much more progress towards the Fed’s goals:

The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test. We have said that we will continue to hold the target range for the federal funds rate at its current level until the economy reaches conditions consistent with maximum employment, and inflation has reached 2 percent and is on track to moderately exceed 2 percent for some time. We have much ground to cover to reach maximum employment, and time will tell whether we have reached 2 percent inflation on a sustainable basis.

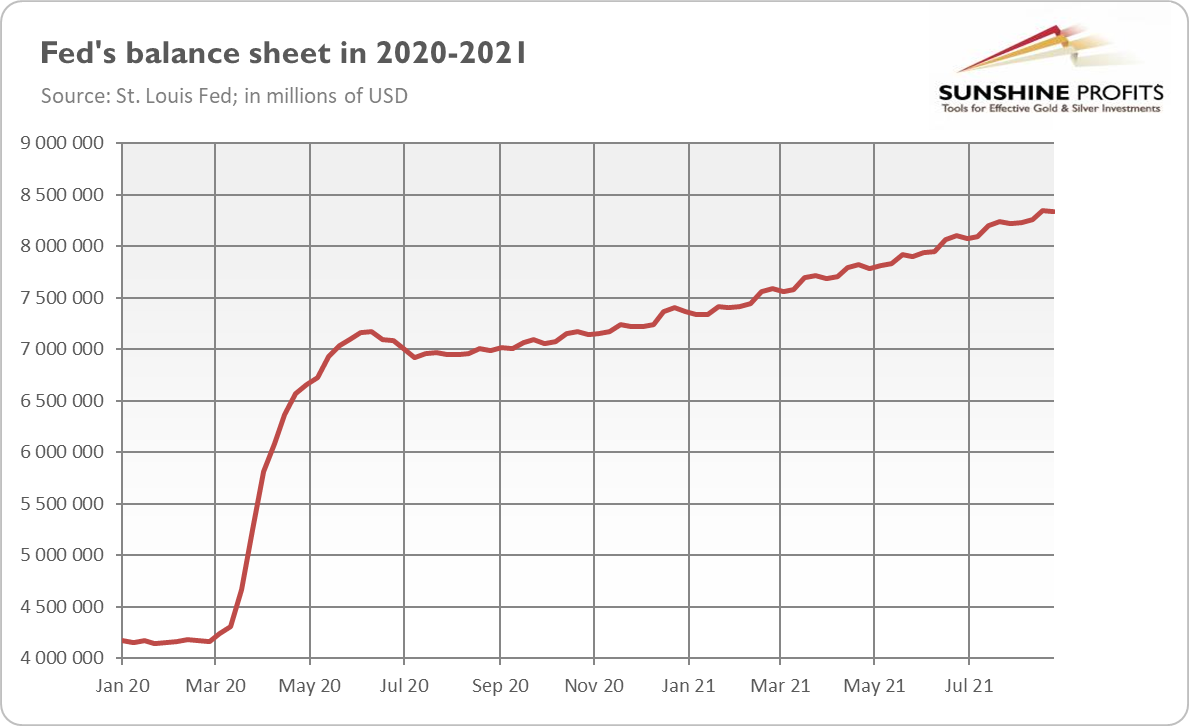

So, we will not see higher interest rates anytime soon, despite higher inflation. This is clearly a dovish signal, and it supports gold prices. After all, the Fed’s monetary policy will remain accommodative, even after the start of tapering. The Fed will still be purchasing assets — the only difference is that it will do so at a slower pace, which means that its balance sheet will remain enormous (see the chart below), implying still large reinvestments of principal repayments.

Implications for Gold

What does it all mean for the gold market? Well, although Powell stated that the Fed’s test of “substantial further progress” had been met for inflation and suggested that it would soon be met for employment as well, his speech didn’t include any revolutionary insights. And, more importantly, it didn’t include any tapering statement. As a result, gold caught its breath.

However, the bullish joy may be premature. The Fed is likely to taper this year, especially if August nonfarm payrolls prove to be strong. Also, the FOMC may issue a tapering statement after its September meeting, announcing the start of reducing the pace of asset purchases in the last quarter of the year. So, the downward pressure on gold prices could stay with us in 2021. On the other hand, the Fed clearly pointed out that the timeline for tapering is not the timeline for interest rates, which could stay at ultra-low levels for months, if not years, working in favor of gold.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Jackson Hole Ahead! What Should We Expect?

August 26, 2021, 10:13 AMGold prices fluctuate around $1,800, waiting for signals from the Fed at Jackson Hole. Which way will we go after the conference?

Finally! The price of gold returned above $1,800 this week, as the chart below shows. It’s a nice change after the slide in early August. Although gold has rebounded somewhat, bulls shouldn’t open the champagne yet. A small beer would be enough for now, as the yellow metal already retreated from $1,800 on Wednesday (the fact that gold was unable to stay above this level is rather disappointing).

So, what is happening on the gold market and what are its prospects? Well, it seems that two narratives are competing with each other ahead of the Jackson Hole conference. The first one is that Powell could provide some clues about the Fed’s tightening cycle, signaling when the tapering would start and how this process would look like. In other words, after July’s FOMC minutes, which came in more hawkish than expected, some analysts expect another hawkish signal from the Fed this week. Gold may suffer due to this, although tapering of the quantitative easing is already priced in to a large extent.

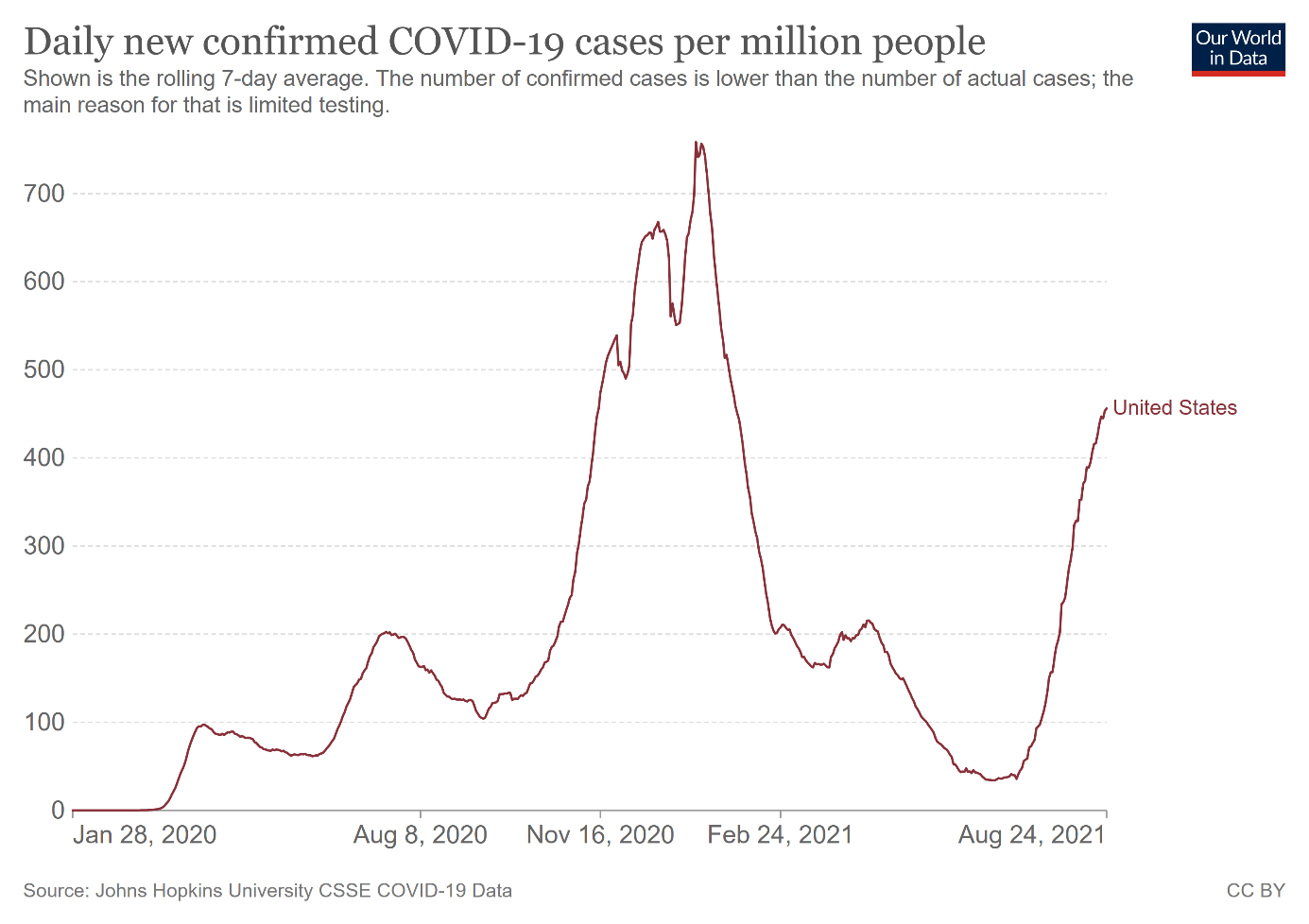

On the other hand, the recent rebound in gold prices might have been caused by investors positioning for a more dovish Fed than before. This is because of the Delta variant of the coronavirus, which is spreading quickly through the US, as the chart below shows.

The rising number of new cases could soften the Fed’s stance or temper its tapering plans. Indeed, Minneapolis Fed President Neel Kashkari said that “COVID-19 delta variant matters a lot”, while Dallas Fed President Robert Kaplan admitted that he might “rethink his call for the Fed [to] start to taper its 120 billion per month and bond purchases if it looks like the spread of coronavirus Delta variant is slowing economic growth.” Of course, both presidents are not voting members of the FOMC this year, but their comments may still be indicative of the thinking within the Fed.

After all, the US central bank says that it’s data-dependent, and some data seems to confirm recent worries about Delta’s impact on the GDP growth. For instance, the HIS Markit Flash U.S. Composite PMI Output Index declined from 59.9 in July to 55.4 in August. This means that U.S. business activity growth slowed for the third month in a row, partially due to Delta and softer consumer demand. The Fed’s more dovish tone and postponement should be positive for gold prices.

Having said that, investors have to remember that Delta’s impact on the economy would be rather limited, as economic agents have already accommodated to the pandemic and nobody wants further lockdowns.

Implications for Gold

What does all this mean for the gold market? Well, the Jackson Hole conference might determine gold’s future direction, as many investors are waiting on the sidelines just to hear what Powell and other central bankers have to say. However, it’s also possible that this year’s symposium will be less impactful than expected. I mean, Powell could refrain from announcing any timeline of the Fed’s tightening cycle, preferring to wait until the FOMC September meeting when August non-farm payrolls are available and it is easier to assess the economic impact of Delta.

However, the lack of hawkish action is dovish action. So, it’s possible that gold investors will find delight in Jackson Hole. However, this “a bit dovish scenario” might already be priced in, so a lot depends on the details of Powell’s speech. My bet is that he will point out both the economy’s strength and the threats of the Delta variant. Nonetheless, I don’t expect that Delta will radically change the Fed’s stance on tapering, so medium-term downward pressure on gold should remain intact.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Inflation Is Prone To Delta. The Same With Gold?

August 24, 2021, 10:20 AMDelta variant caused fresh supply-chain disruptions. Effects? Slower growth and higher inflation. Sounds like a perfect mix for gold!

The Delta variant of the coronavirus is spreading all around the world. Although it won’t affect the world economy as much as the first wave of the pandemic, it will add to the already existing problems. Namely, the rising number of new cases will prolong the supply disruptions, hampering the GDP growth and strengthening the already high inflation (see the chart below).

In particular, last week, the Ningbo-Zhousan port in eastern China was partially closed until further notice after its worker was infected with the Delta strain. The problem is that it’s the world’s third-busiest cargo port, so its closure will cause fresh pressure to the already disrupted shipping industry.

The spread of the Delta variant and related disturbances in global trade have already caused Goldman Sachs to cut its forecasts for the US economy from 6.4% to 6% this year. “The impact of the delta variant on growth and inflation is proving to be somewhat larger than we expected”, the bank’s analysts explained in a note to the clients. The supply chain’s hurdles are expected to curb production and further raise prices, which would lower the purchasing power of consumers and limit their spending.

It implies that high inflation will likely stay with us for longer than the Fed thinks, just as I’ve been saying for a long time. The current situation shows a disturbing resemblance to the 1970s. As you know, inflation was surging then, but the US central bank was downplaying it, blaming the temporary effects of the first oil shock. The result of such a careless stance was the Great Stagflation and the need to aggressively hike federal funds rate by Paul Volcker. Inflation was defeated, but a double-dip recession emerged.

We also have a negative supply shock now (or, I should say, a series of shocks). It’s not an oil shock, but it’s also significant, as the issue broad-based — namely, the semiconductor shock and container shock, which hit all kinds of products. Semiconductors are key for the modern economy. They are used in various industries from consumer electronics to vehicles, and you practically cannot transport goods without containers. And as in the 1970s, the Fed believes that inflation is transitory and will go away on its own.

Yeah. Maybe it would happen if we had to deal with the supply shocks only. But the economy has also been hit by demand shocks – i.e., by the surge in the broad money supply and fiscal deficits used to finance cash transfers to the citizens and generous unemployment benefits. All this adds to inflationary pressures.

Implications for Gold

What does all this mean for the gold market? Well, slower economic growth and higher inflation due to the spread of the Delta variant are good news for gold. It brings us closer to a stagflationary environment, which should be welcomed by the yellow metal. Although gold doesn’t always protect against inflation, it served as a good inflation hedge during the 1970s, so we could reasonably expect similar performance during the potential 2020s stagflation.

Unfortunately, there is one big scratch in this picture: the Fed’s tapering of quantitative easing. More persistent inflation could mobilize inflation hawks to tighten monetary policy in a more rushed manner. As a result, the bond yields could increase, especially given that they are at very low levels, creating downward pressure on gold prices.

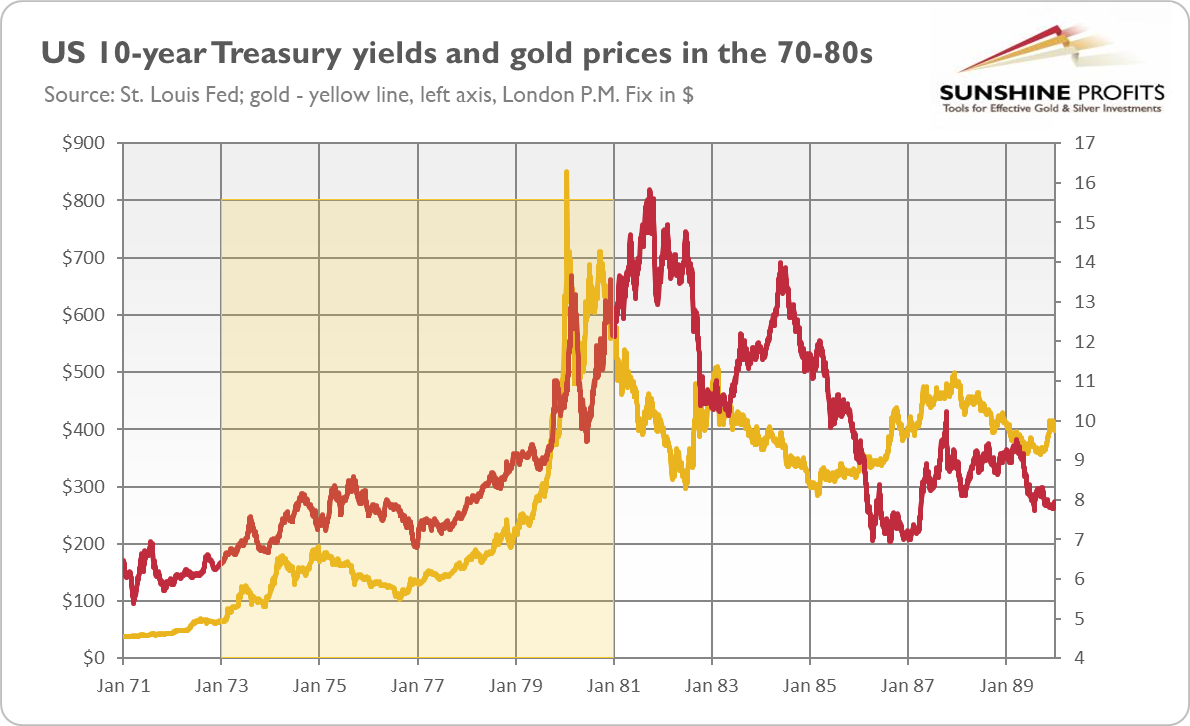

Luckily, history teaches us that bond yields can increase in tandem with gold prices. As the chart below shows, this is what happened in the 1970s. After all, what really counts for the gold market is real interest rates, and they could stay at an ultra-low level or even decline further if inflation surges.

Last but not least, the Delta variant is also likely to hamper economic growth. So, the Fed could actually become more dovish and postpone the end of its asset purchases, especially given that it has already expressed some concerns about the Delta spread. So, although the price of gold could decline further amid potential normalization in interest rates, inflation risk should provide some support or even materialize, pushing inflation itself higher.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Fed to Taper This Year – What Are the Odds?

August 19, 2021, 7:23 AMThe latest FOMC minutes show that the Fed will likely taper quantitative easing this year. It’s largely priced in, but downside risks to gold remain.

Yesterday, the FOMC published minutes from its last meeting in July. The publication is rather hawkish, as it shows growing appetite among the Fed officials for tapering the quantitative easing as early as this year:

Looking ahead, most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year because they saw the Committee’s “substantial further progress” criterion as satisfied with respect to the price-stability goal and as close to being satisfied with respect to the maximum-employment goal.

The discussion about the tapering of the Fed’s asset purchases must have been the key point of July’s FOMC meeting, as it was reiterated later in the minutes with a similar conclusion:

Most participants anticipated that the economy would continue to make progress toward those goals and, provided that the economy evolved broadly as they anticipated, they judged that the standard set out in the Committee’s guidance regarding asset purchases could be reached this year.

Additionally, starting tapering sooner rather than later has several advantages, as it would help to manage the upward risk of the inflation outlook, giving the Fed the opportunity to hike the federal funds rate sooner, if needed. It would also allow the US central bank of a more gradual pace of tapering, reducing the risk of the taper tantrum:

Several participants noted that an earlier start to tapering could be accompanied by more gradual reductions in the purchase pace and that such a combination could mitigate the risk of an excessive tightening in financial conditions in response to a tapering announcement (…)

Some participants suggested that it would be prudent for the Committee to prepare for starting to reduce its pace of asset purchases relatively soon, in light of the risk that the recent high inflation readings could prove to be more persistent than they had anticipated and because an earlier start to reducing asset purchases would most likely enable additions to securities holdings to be concluded before the Committee judged it appropriate to raise the federal funds rate.

What’s more, although FOMC participants decided that the economy had not yet achieved the Committee’s broad-based and inclusive maximum-employment goal, a majority of them stated that most of the negative factors which weighed on the employment growth would ease in the coming months, warranting the start of the tapering.

Last but not least, the Fed seemed to become more hawkish on inflation. The staff considered the risks of the inflation projection to be tilted to the upside, while FOMC members started to see it as potentially more persistent than previously believed:

Looking ahead, while participants generally expected inflation pressures to ease as the effect of these transitory factors dissipated, several participants remarked that larger-than-anticipated supply chain disruptions and increases in input costs could sustain upward pressure on prices into 2022.

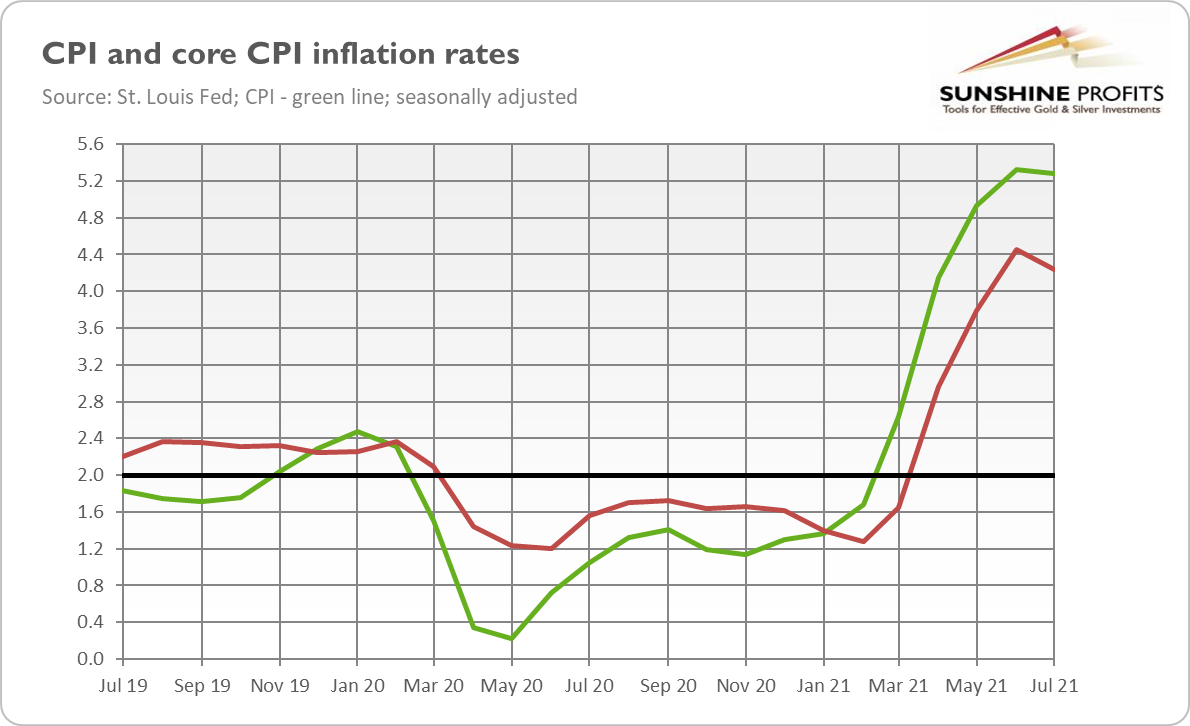

It seems that someone at the Fed has finally noted that inflation had jumped above 5%, as the chart below shows!

Of course, there were also dovish parts, in particular related to the possibility that the spread of the Delta variant of the coronavirus would hamper the economic growth, or that the slack in the labor market could be greater than commonly believed. Thus, several participants emphasized that the Fed should be patient with tapering and that it would be better to start it early next year:

Several others indicated, however, that a reduction in the pace of asset purchases was more likely to become appropriate early next year because they saw prevailing conditions in the labor market as not being close to meeting the Committee’s “substantial further progress” standard or because of uncertainty about the degree of progress toward the price-stability goal (…) Those participants stressed that the Committee should be patient in assessing progress toward its goals and in announcing changes to its plans on asset purchases

Implications for Gold

What do the recent FOMC minutes imply for the gold market? Well, they came in, on balance, hawkish, so they should be negative for the yellow metal. However, the initial reaction was bullish. Perhaps investors were afraid that the minutes would be even more hawkish. The decline in equities could also fuel some safe-haven demand for gold. It’s worth noting that the reaction was rather muted, as the publication didn’t offer any groundbreaking revelations. It seems that next week’s annual Jackson Hole conference could provide more clues about the future US monetary policy.

Having said that, the minutes clearly show that tapering is coming. The Fed could announce it as early as in September, as Dallas Fed President Robert Kaplan prefers, and start it later this year. So, precious metals investors should brace for the inevitable. Luckily, the Fed’s tightening cycle is largely priced in, but any unexpected acceleration in the pace of the monetary policy normalization could rattle the gold market.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM