tools spotlight

-

Gold During the Pandemic Winter

February 12, 2021, 8:17 AMThe pandemic winter will take longer than we thought. The longer we struggle with the coronavirus, the brighter gold could shine.

A long, long time ago, there was a bad virus, called the coronavirus, that killed many people all around the world and severely hit the global economy. Luckily, smart scientists developed vaccines that defeated the coronavirus and ended the pandemic. Since then, humankind lived happily – and healthy – ever after.

Sounds beautiful, doesn’t it? This is the story we were all supposed to believe. The narrative was that the development of vaccines would end the pandemic and we would quickly return to normalcy. However, it turns out that this was all a fairy tale – the real struggle with the coronavirus is more challenging than we thought.

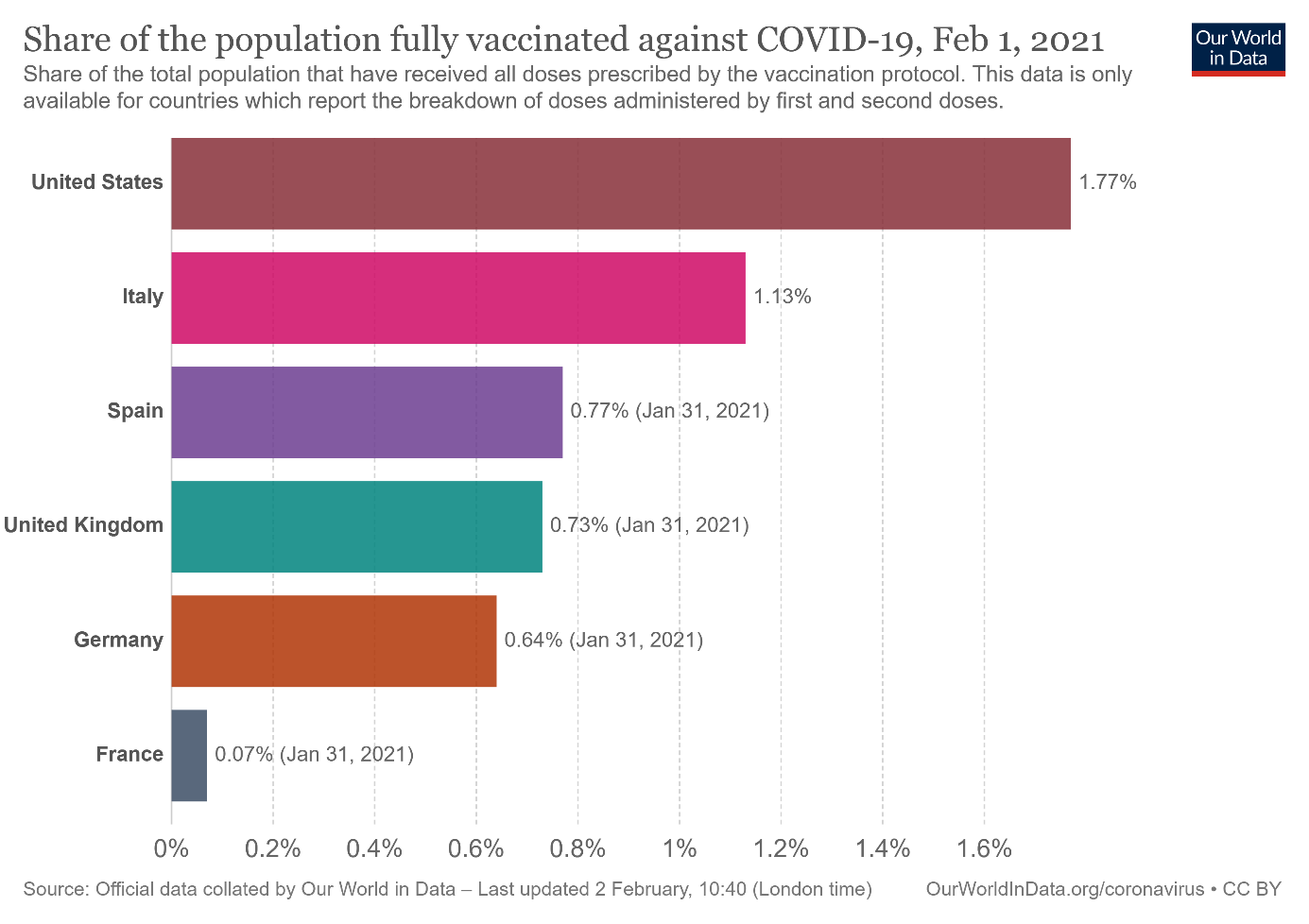

First, the rollout of vaccinations has been very, very slow. As the chart below shows, on February 1, 2021, only about 1.77 percent of Americans became fully vaccinated against COVID-19.

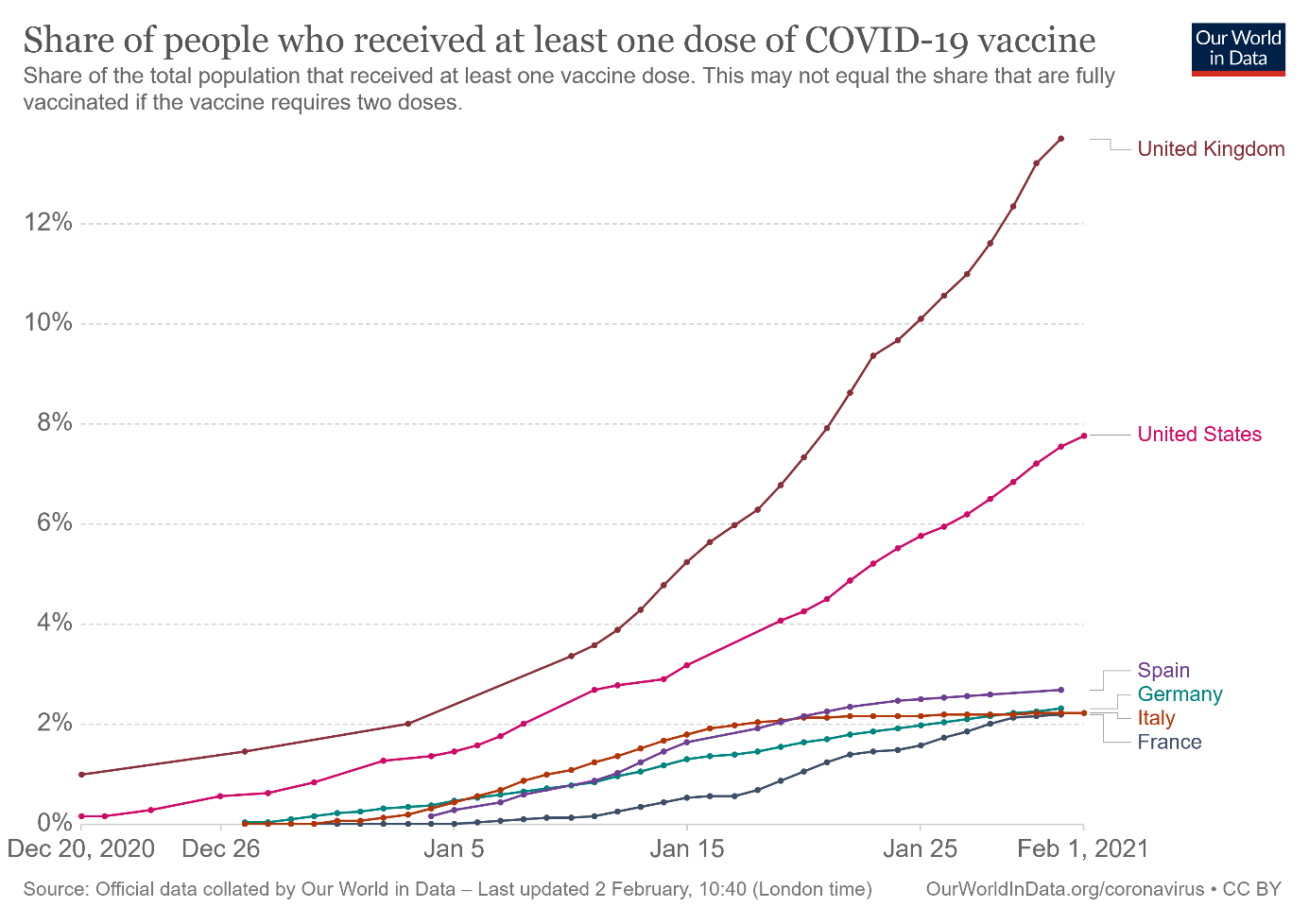

Of course, full protection requires two doses, so it takes some time. But in many countries, the share of the population which received at least one dose of the vaccine is also disappointingly low, as the chart below shows.

It means that our progress towards herd immunity is really sluggish. At such a pace, we are losing the race between injections and infections. And we will not reach herd immunity until the second half of the year or even the next winter…

Second, there is the problem of mutations. The new strains are rapidly popping up which poses a great risk in our fight with the coronavirus. One of these new variants was identified in the United Kingdom and quickly spread through the country. Although it’s not more lethal, it’s more infectious, which makes it more dangerous overall. And the more variants emerge, it’s more likely that we could see a mutation resistant to our current treatments and vaccines. Indeed, some of the mutations change the surface protein, spike, and have been shown to reduce the effectiveness of combating the coronavirus by monoclonal antibodies.

The really bad part is that these two problems are strongly connected. The longer the vaccinations take, the more active cases we have. The more active cases we have, the more mutations happen, as each new infection implies more copies of the coronavirus, which gives it more chances to mutate. The more mutations occur, the higher the odds of a really nasty strain. Therefore, the longer the vaccination process takes, the more probable it is that it will not work and that vaccine-resistant variants might emerge.

Given that in many countries vaccinations are practically the only rational strategy to fight the virus, the vaccine-resistant strain would be a serious blow. Surely, some vaccines could be relatively easily updated, but their rollout would still require time – time we don’t have.

What does it all imply for the gold market? Well, the more sluggish the vaccinations, the higher the risk that something goes wrong and that our battle with COVID-19 will take more time. The longer the fight, the slower the economic recovery. The longer and bumpier road toward herd immunity, the slower lifting sanitary restrictions and social distancing measures, and the later we come back to normalcy. The longer we live in Zombieland, the easier fiscal and monetary policies will be, and the brighter gold will shine.

Another issue is that we shouldn’t forget about the possibility of the pandemic’s long economic shadow. A recent paper has examined the effects of 19 major previous pandemics, finding a long shadow of the economic carnage. Although financial markets are still (wrongly, I believe) betting on a V-shaped recovery, the history suggests that a double dip is likely, as eight of the last 11 recessions experienced it. Recessions sound golden, don’t they?

However, there is one caveat here. The sensitivity of economic activity to COVID-19 infections and restrictions has significantly diminished since the Great Lockdown in the spring of 2020. There are three reasons for that. First, people fear the coronavirus less. Second, epidemic restrictions are better targeted and implemented. Third, entrepreneurs adopted better to cope with the epidemic.

The greater resilience of the economy means a smaller downturn and fewer long-term scars, which will limit any upward COVID-19 related impact on gold prices. But a softer economic impact also implies a quicker recovery, which – together with the upcoming big government stimulus – could increase consumer prices, thus supporting gold prices through the inflation channel. Indeed, commodity prices have been surging in 2021, so gold may follow suit.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the February Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Effective Investment through Diligence & Care.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

New POTUS, New Gold Bull Market?

February 5, 2021, 10:12 AMJoe Biden’s election as president and his first economic proposal proved negative for gold prices, but the presidency might yet turn positive.

The 46th presidency of the United States has officially begun. What does that mean for the U.S. economy, politics and the precious metals market?

Let’s start by noting that this will not be an easy presidency. The epidemic in the U.S. is raging, the economy is in recession, and public debt is ballooning. Foreign relations are strained while the nation is strongly polarized, as the recent riots clearly showed. So, Biden will have to face many problems, with few assets.

First, as he turned 78 in November, Biden has been the oldest person ever sworn in as U.S. president. Second, his political capital is rather weak, as the 2020 election is more about Trump’s loss than Biden’s victory. In other words, many of his voters supported Biden not because of his merits but only because they opposed Trump. Third, he will have the smallest congressional majorities in several years. Democrats have only ten more seats than Republicans in the House and the same number of seats in the Senate. And even with Kamala Harris as a tie-breaker, Biden could not lose a single Democrat senator’s vote to pass any legislation in Senate.

On the one hand, Biden’s tough political position seems to be negative for gold prices, as it lowers the odds of implementing the most radical, leftist political agenda. On the other hand, Biden’s difficulties also lower the chances of sound economic reforms, which is good news for the yellow metal. A divided Congress and Democratic Party with an old president at the helm, who has a weak personal base could result in political conflicts and stalemates which would prove positive for gold.

When it comes to economics, Biden has already presented his pandemic aid bill, worth of $1.9 trillion. The proposal includes direct payments of $1,400 to households, $400 per week in supplementary unemployment benefits through September, billions of dollars for struggling businesses, schools, and local governments, as well as funding that would accelerate vaccination and support other coronavirus containment efforts. Biden also wants to raise the minimum wage to $15 per hour, which will not appeal to Republicans. The big size of the package will also be disliked by the GOP.

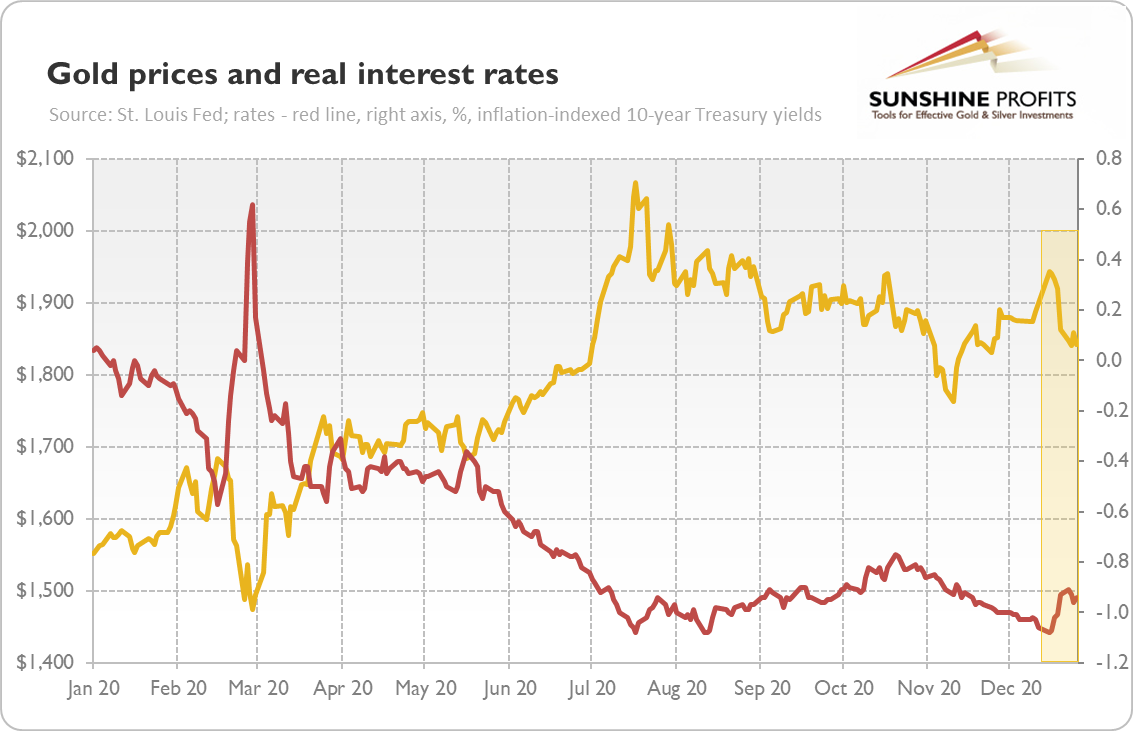

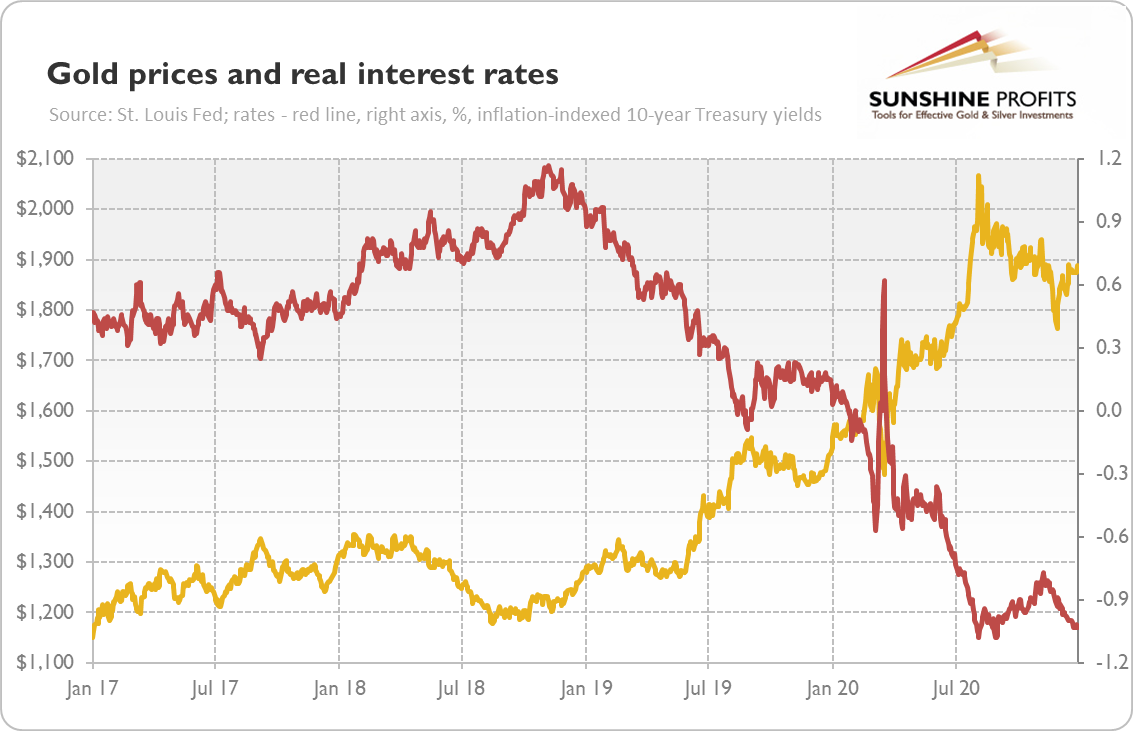

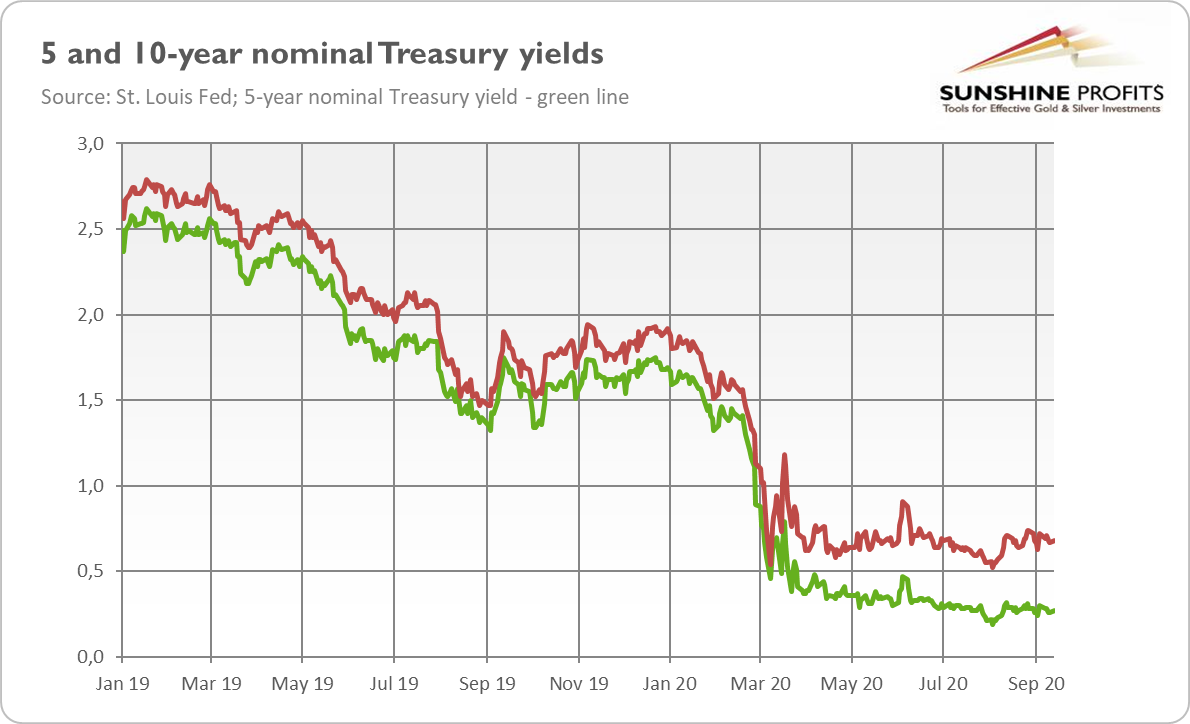

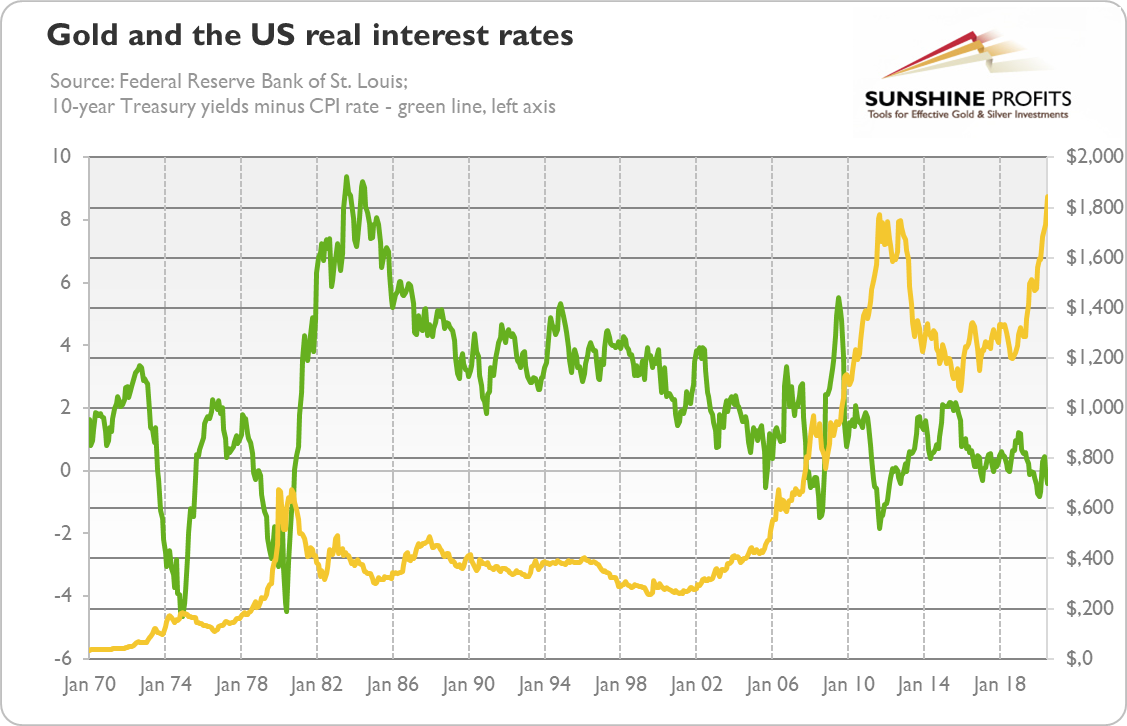

The fact that Democrats have won the Georgia Senate runoffs, taking control over the Senate, increases the chances that Biden will implement his economic stimulus. The equity markets welcomed the idea of another large aid package, in contrast to bond investors who sell Treasuries, causing the yields to go up. The increase in real interest rates pushed gold prices down, as the chart below shows.

It seems that investors liked the idea of big stimulus, hoping for acceleration in economic growth. However, printing more money (I know, the Treasury technically doesn’t print money – but it issues bonds which are to a large extent bought by the Fed) and sending checks to people doesn’t increase economic output. Another problem is that the U.S. can’t run massive fiscal deficits forever and ever, hoping that interest rates will always stay low.

So, although Biden’s economic stimulus may add something to the GDP growth in the short-term, it will not fundamentally strengthen the economy. Quite the contrary, the massive increase in government spending and public debt (as well as in taxation) will probably hamper the long-term productivity growth and make the already fragile debt-based economic model even more fragile. What is really worrisome is that Biden doesn’t seem to care about U.S. indebtedness – he has already spoken strongly against deficit worries and hasn’t proposed any actions to reduce the debt – and plans to unveil the additional economic stimulus.

Hence, although gold declined initially in a response to Biden’s economic stimulus proposal, the new president could ultimately turn out to be positive for the yellow metal. After all, gold declined in the aftermath of the Lehman Brothers’ collapse, but it shined under Barack Obama’s first presidency. And Biden is likely to be even more fiscally irresponsible than Obama (or Trump), while the Fed under Powell is likely to even more monetarily irresponsible than under Bernanke (or Yellen). Indeed, according to The Economist, Biden’s proposal is worth about nine percent of pre-crisis GDP, nearly twice the size of Obama’s aid package in the aftermath of the Great Recession. And, in contrast to previous crises, the Fed has announced the desire to overshoot its inflation target. All these factors should support gold prices in the long run.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the February Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Effective Investment through Diligence & Care.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Interest Rate Increase Cause Gold to Plunge in 2021?

February 4, 2021, 11:15 AMThe decline in the real interest rates is the most important downside risk for gold. Will it materialize, plunging the price of the yellow metal?

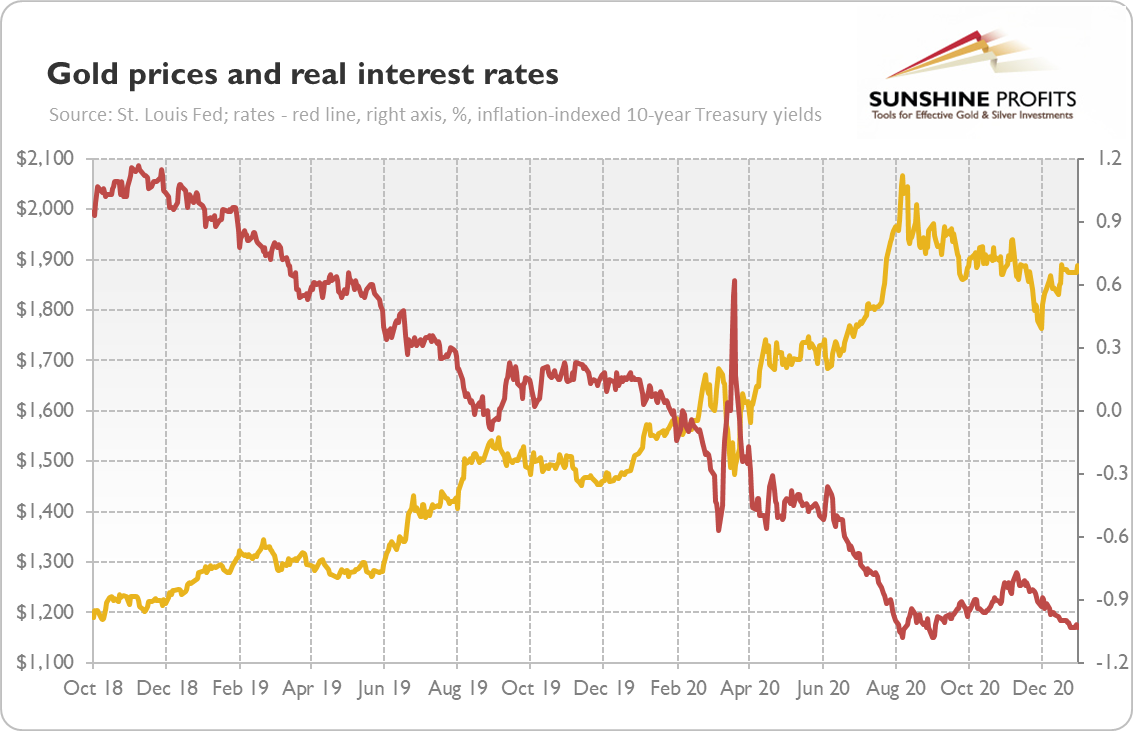

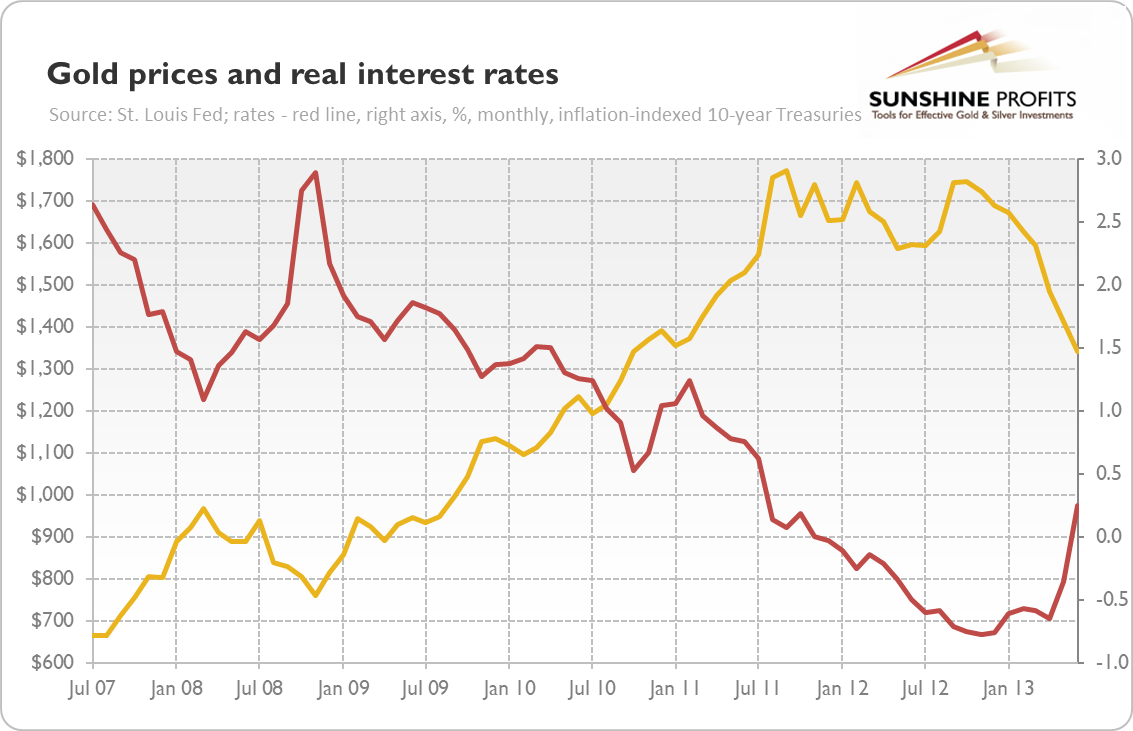

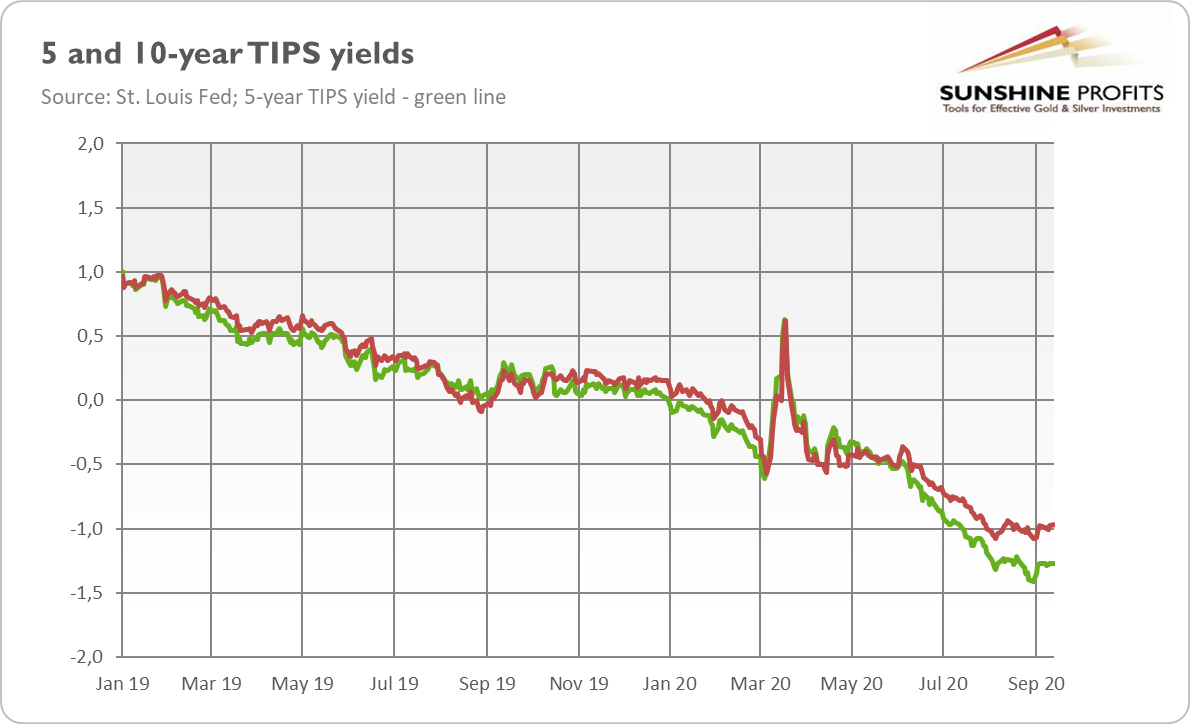

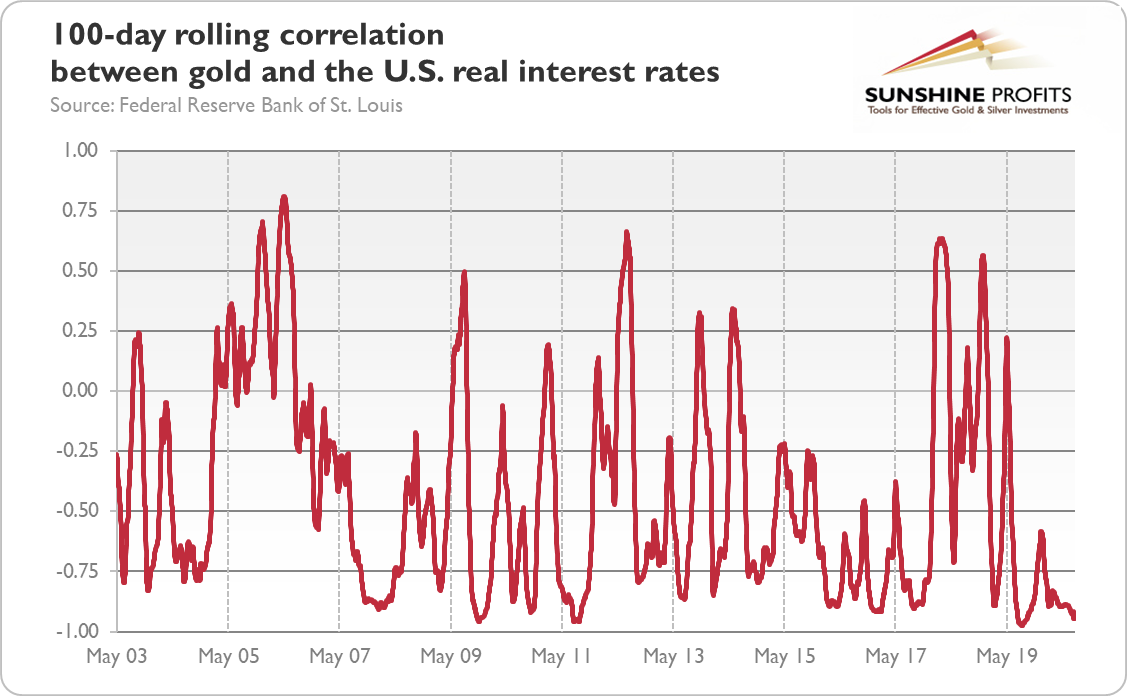

The rise in inflation is the most significant upside risk for gold this year, but there are also a few important downside risks. The most disturbing for us is the possibility that the real interest rates will increase. Why? Please take a look at the chart below.

As you can see, there is a strong negative correlation between the real yields and gold prices. When the interest rates go up, the yellow metal falls, and when the rates go down, gold rallies. Indeed, the real interest rates peaked in November 2018 at 1.17 percent, just one month before the last hike in the Fed’s last tightening cycle. Since then, they were falling, reaching their historical bottom below -1.0 percent in the summer of 2020. Not coincidentally, gold was experiencing a bull market during this period, reaching its record high of almost $2010, just when the rates bottomed. And, as the rates normalized somewhat, the price of gold corrected to the level below $1,900.

Now, the obvious question is whether there is further room for real interest rates to go down. In 2019, they were falling amid the economic slowdown and the dovish Fed cutting the interest rates. Last year, they plunged even further (with a short spike because of the surge in the risk premium), as a result of the COVID-19 related economic crisis and the U.S. central bank slashing the federal funds rate to practically zero.

However, the Great Lockdown and resulting deep downturn are behind us. When we face the second wave of the pandemic and people become vaccinated, there will be an economic recovery. As well, the Fed has already brought the interest rates to zero – meaning that without the U.S. central bank implementing NIRP, the nominal policy rates reached their lower bound. So, assuming that the Fed will not cut interest rates further and that investors will not expect a further slowing down of the economy, the room for further declines in the real interest rate is limited.

The only hope lies in the increase in inflation expectations, which is actually quite probable, as I explained in the previous part of this edition of the Gold Market Overview. Given the surge in the broad money supply, the pent-up demand, and some structural shifts, reflation in 2021 is more likely than it was in the aftermath of the great financial crisis.

However, gold investors should also be prepared for a negative scenario of low inflation. After all, the Fed has repeatedly undershot its annual inflation target. In this case, the real interest rates may stay roughly the same or they could even rise.

Let’s take a look at the chart below, which shows the gold prices and real interest rates after the Great Recession. In the very aftermath of the Lehman Brothers’ bankruptcy, they surged, but after the panic phases ended, they were falling until the end of 2012, just when, more less, the bear market in gold started.

Now, somebody could say that the real interest rates were falling for four years until reaching bottom at the end of 2012, so we shouldn’t worry about the normalization of interest rates. However, the COVID-19 related economic crisis was very deep, but also very short. Everything is happening now at an accelerated speed, so we could already be reaching the local bottom in the interest rates (or be close to it).

Of course, there are important differences between that period and today. First, as I’ve already emphasized, there is now a higher risk of an increase in inflation. Second, in 2013, there was a taper tantrum, while today, the Fed maintains an ultra-dovish stance and does not signal any interest rate hikes in the foreseeable future. Although the U.S. central bank didn’t expand its quantitative easing in December, showing that it feels comfortable with some increases in the bond yields, it’s not going to accept substantial rises in the interest rates. The dovish Fed’s bias is one of the main factors behind the downward trend in the real interest rates (even if they normalize somewhat, they reach further lower peaks and bottoms over time).

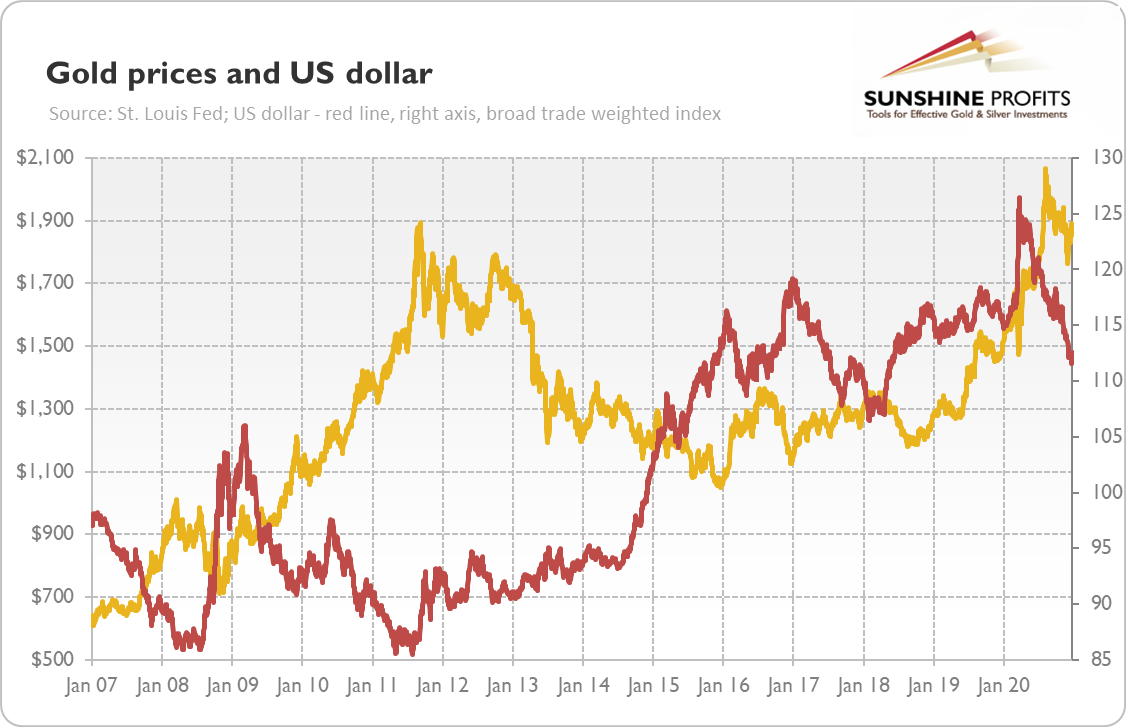

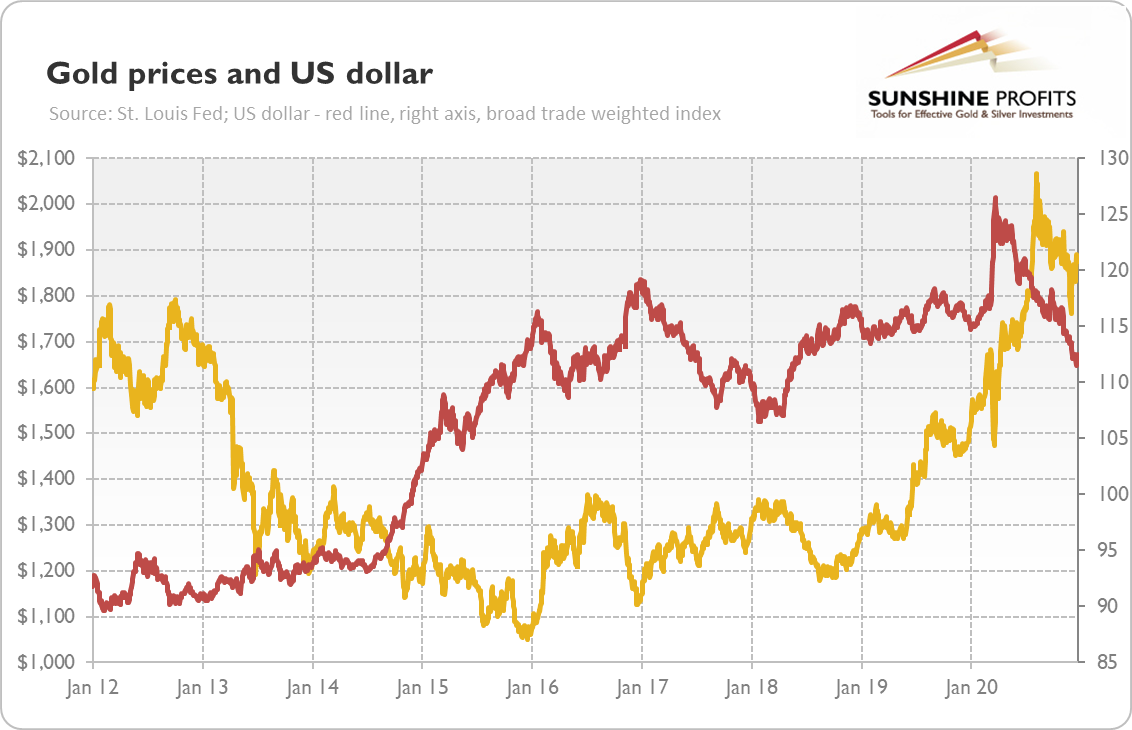

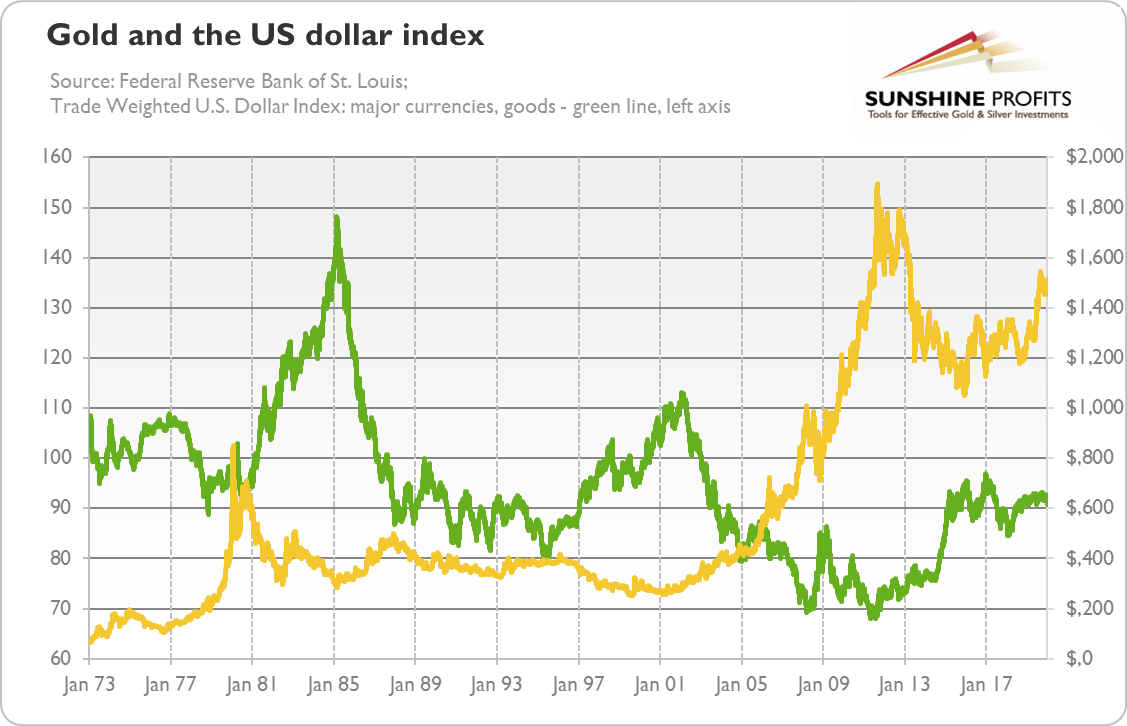

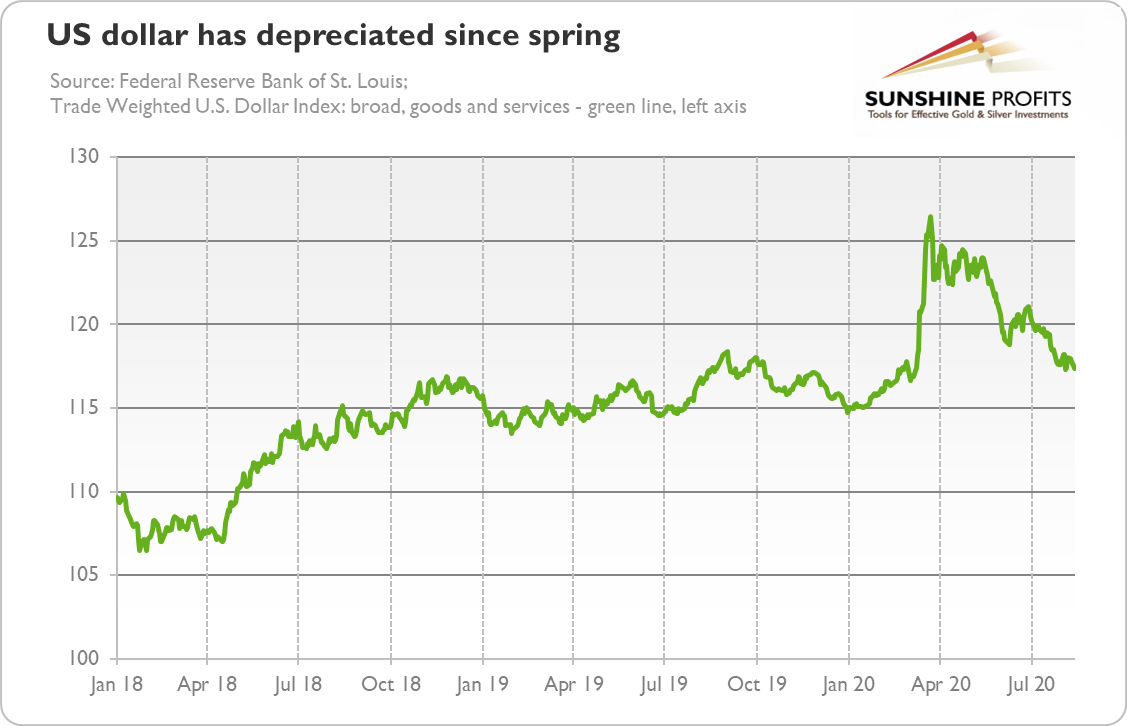

Third, the U.S. dollar looks different. As the chart below shows, the greenback started to appreciate in 2011, pushing gold prices down. But today it is more likely that the U.S. dollar will weaken further due to a changing administration in the White House, the economic stabilization and cash outflows into developing countries, soaring public debts, a zero-interest rate policy, and the risk of an increase in inflation.

If so, the normalization of the real interest rates (if it happens, which is far from being certain) doesn’t have to plunge the yellow metal. In other words, there are important downside risks to the bullish case for gold this year, but 2021 does not have to look like 2013 in the gold market.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the January Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Inflation Make Gold Shine in 2021?

January 22, 2021, 9:51 AMInflation will be one of the greatest upside risks for gold this year. Will it materialize and make gold shine?

The report about gold in 2021 would be incomplete without the outlook for inflation. We have already written about it recently, but this topic is worth further examination. After all, higher inflation is believed to be one of the biggest tail risks in the coming months or years, and one of the greatest upside risks for gold this year.

Most economists and investors still believe that inflation is dead. After all, the only way to justify the central banks’ unprecedentedly dovish actions is the premise of low inflation. And the only way to justify the buoyant stock market amid the new highs in the number of Americans in hospital with COVID-19 is the expectation of an inflationless economic recovery this year. In other words, many people forecast the return to the Goldilocks economy after the end of the pandemic.

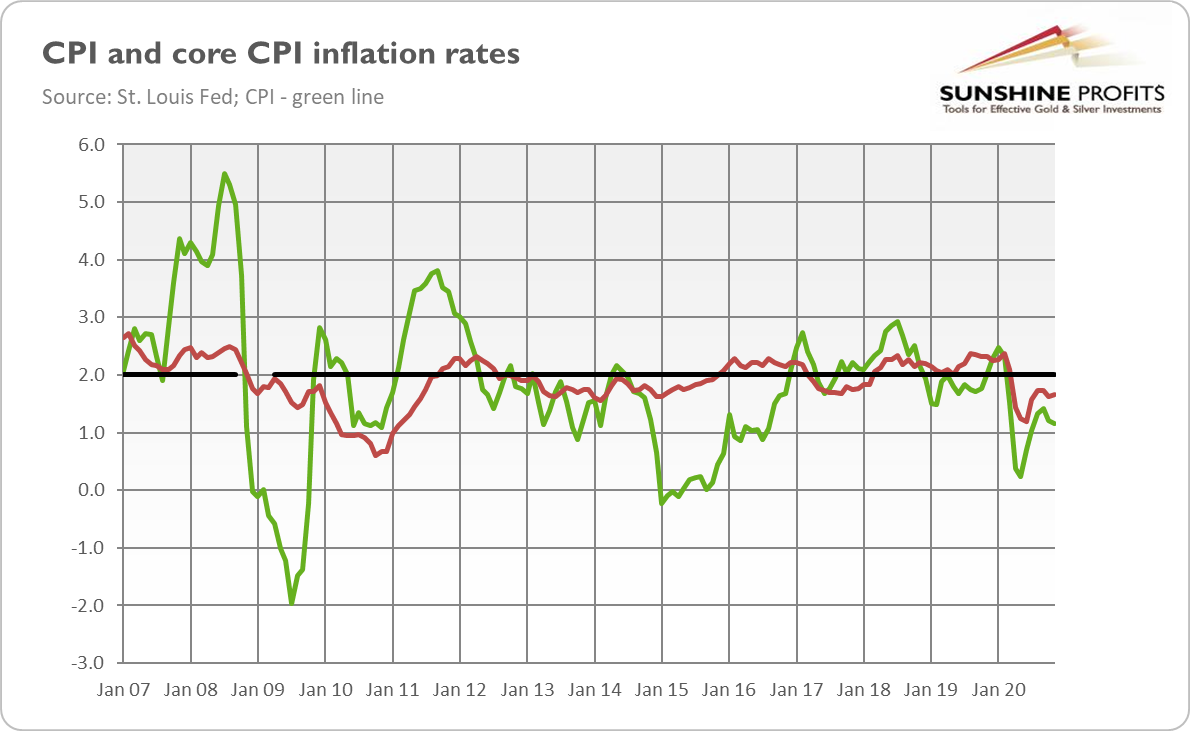

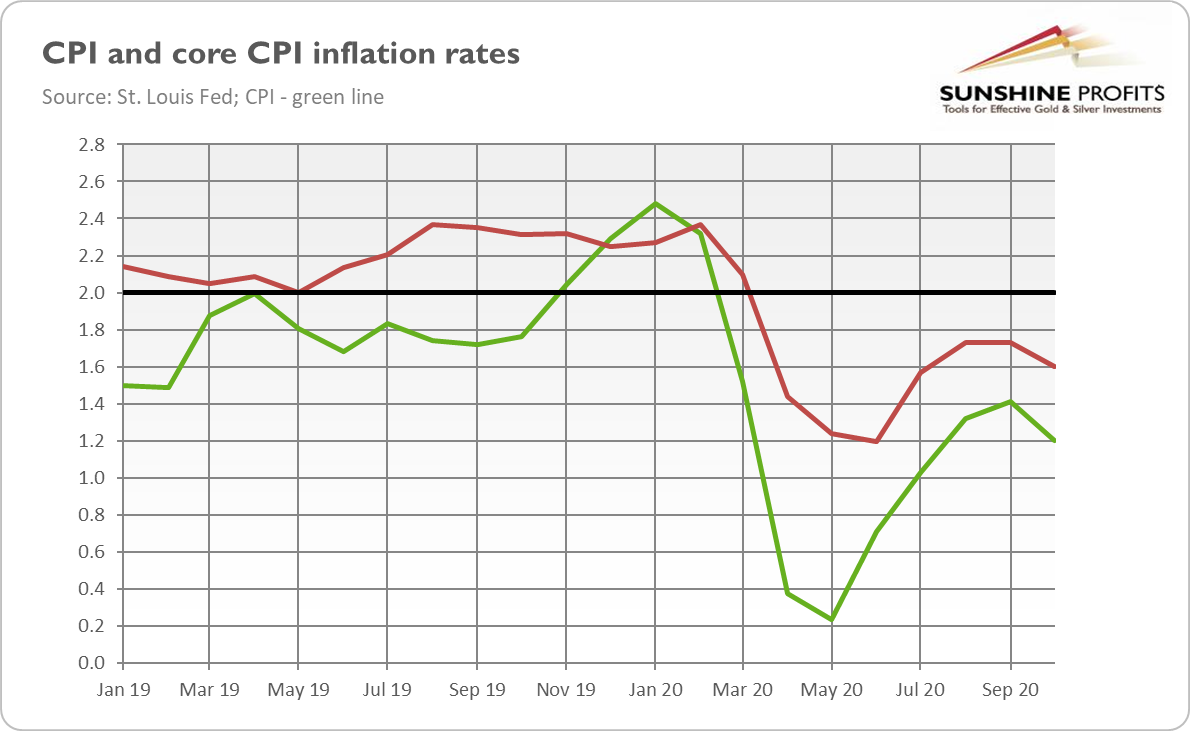

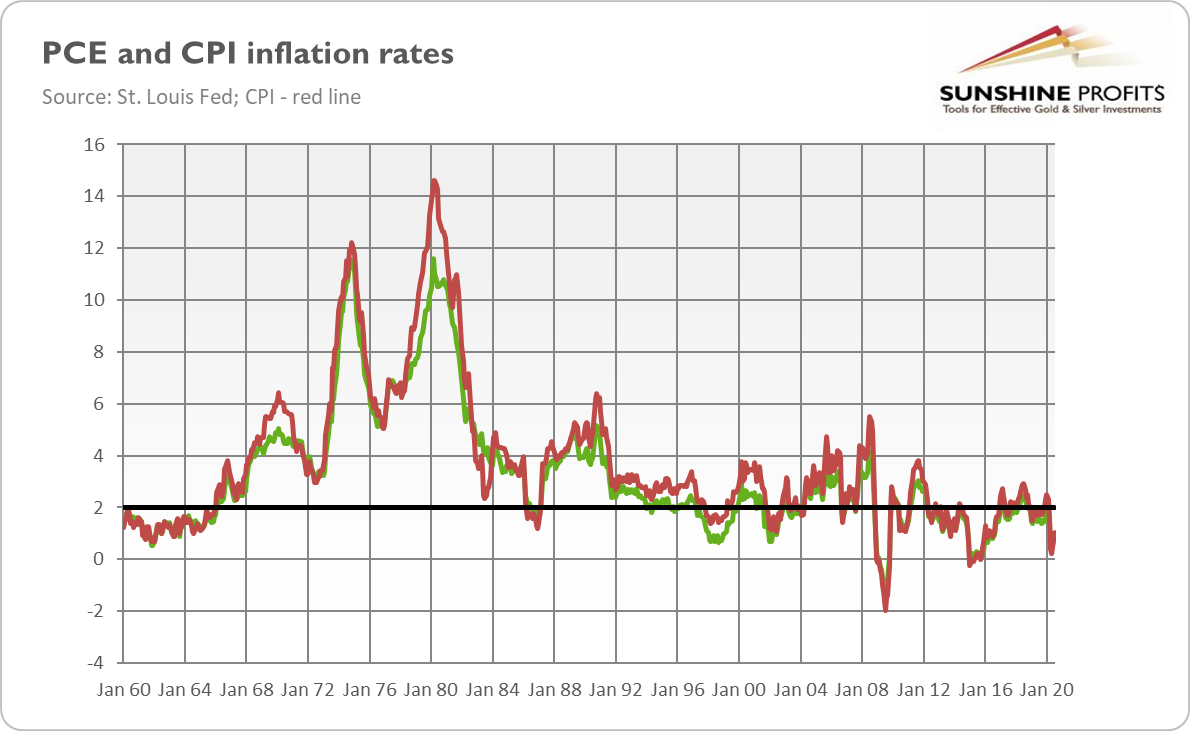

On the surface, it seems that they might be right. We haven’t seen double-digit inflation since the end of 1981. And last time the CPI annual rate was above 3 percent was in January 2012. Actually, in the last ten years, inflation was below the Fed’s 2-percent target most of the time, as the chart below shows.

Moreover, the inflation rates dropped significantly during the U.S. epidemic and the Great Lockdown when people distanced socially and limited their spending. So, given the strength of the negative demand shock and the following plunge in inflation, why should we worry about the risk of higher inflation?

Well, shouldn’t it be obvious after experiencing a pandemic, i.e., an improbable but impactful event? Even a small probability of a surge in inflation should be worrying, especially given the pile of debt and, thus, limited room for central banks to hike interest rates to prevent inflation.

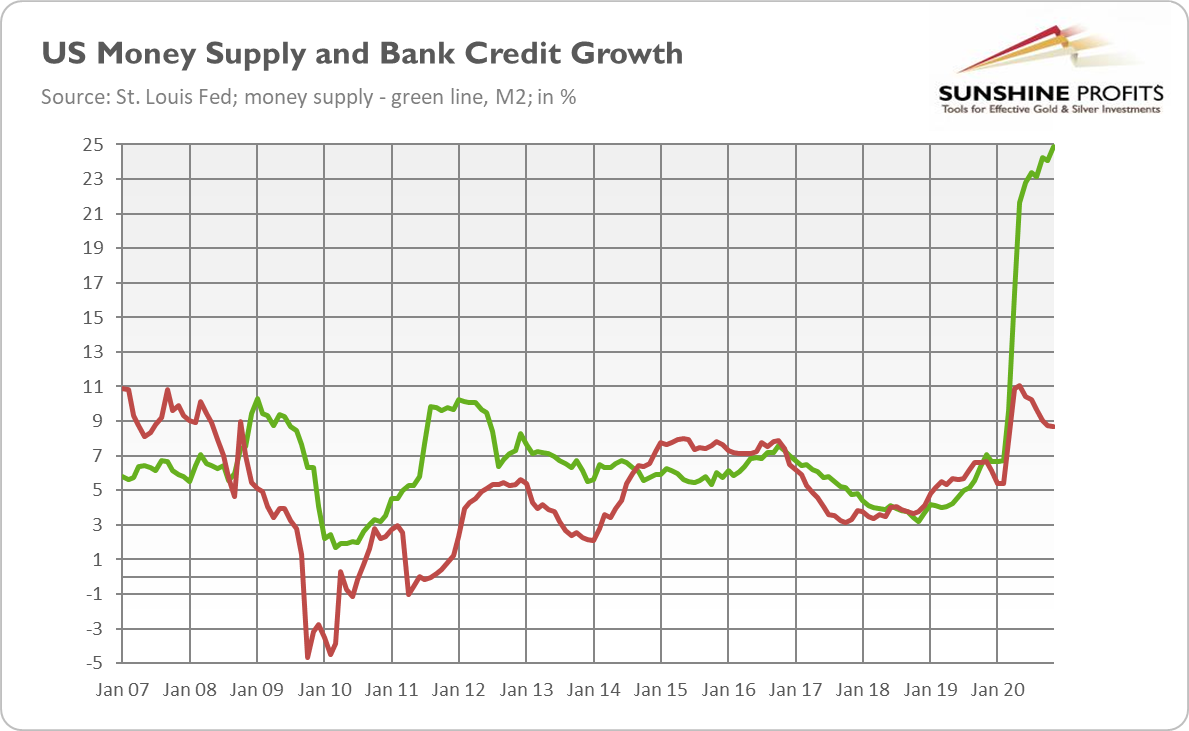

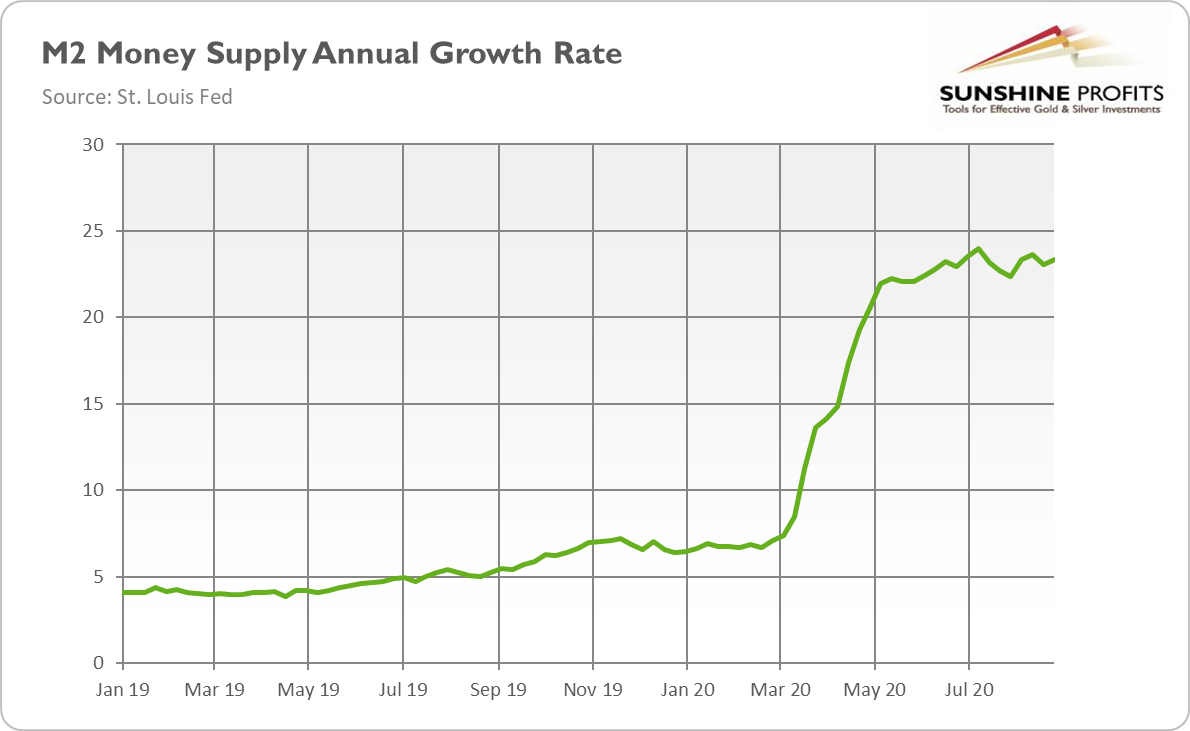

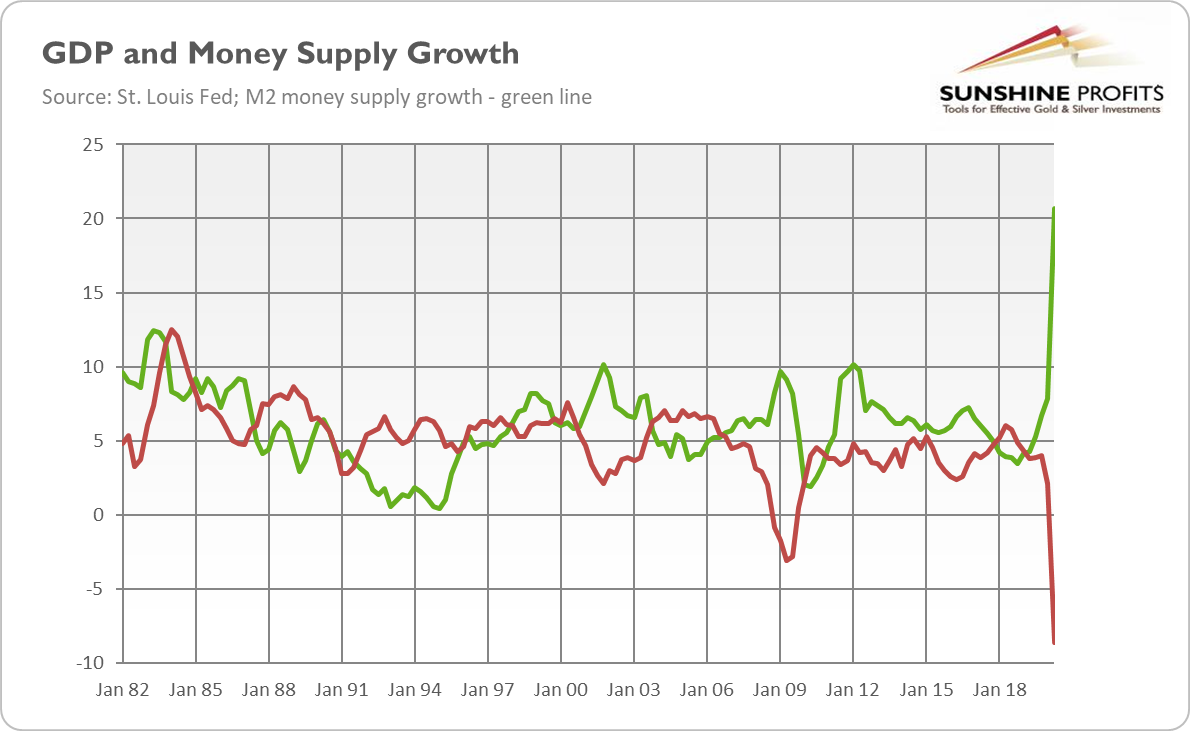

Moreover, the likelihood of an increase in inflation is not so small. As I’ve explained several times, the case for higher inflation is stronger today than in the aftermath of the Great Recession. The first reason is that the broad money supply has surged. This is because the banks haven’t been hit so far (in contrast to the financial crisis where banks suffered greatly), so they have been lending freely, as the chart below shows.

Second, in contrast to the previous economic crisis where people did not spend money because they had no income or they decided to repay their debts, this time, people didn’t spend money because they were stuck at home. But when the health crisis is over and people get vaccinated, some consumers may go on a spending spree. The realization of pent-up demand may overwhelm the firms’ capacity, leading to an increase in prices. There are already some signs of bottlenecks, or supply falling behind demand, such as the increase in prices of some commodities like iron ore.

In other words, when the world returns to normality, the private sector will find itself flush with cash. And I bet that some households will try to make up for all the time not spent in movie theatres, restaurants and hotels during the last year.

Third, there might also be some structural shifts in the global economy, which will reverse the current disinflationary forces. As Charles Goodhart and Manoj Pradhan argue in their book The Great Demographic Reversal, the era of low inflation, caused by globalization, is now ending. You see, in the 1980s and 1990s, China, India and post-communist countries from Europe and Central Asia, entered the global economy. As a consequence, the global labor supply for production of tradeable goods rose enormously, leading to weak inflationary pressure. But all this is going into reverse. Globalization is now weakening and there are no big countries in the queue to enter the global economy. Actually, ageing in China and other countries reduces the global labor supply, thus strengthening inflationary pressure.

Last but not least, the politicians and central bankers have become more complacent. The thoughtless and irresponsible stance of politicians is unsurprising, especially given the temptation to inflate away the public debt. However, the central banks also stopped worrying and embraced the inflation bomb. For example, the Fed has changed its monetary regime in 2020, announcing that it would tolerate overshooting of inflation above its target for a undetermined period of time.

The bottom line is that inflation should return in the coming months (more precisely, in the second half of the year, when the distribution of vaccines will be widespread). We shouldn’t experience double-digit rates, but the markets don’t expect a deflationary crisis either. As the chart below shows, inflationary expectations have already returned to pre-pandemic levels.

All this is good news for price of gold. The case for reflation in the global economy is definitely stronger than after the global financial crisis of 2007-2009. The present risk of higher inflation should support the demand for gold as a hedge against inflation. And the increase in inflation expectations lowers the real interest rates, thereby positively affecting the yellow metal. Although gold will face some important headwinds this year, inflation expectations are likely to outpace the increase in nominal bond yields, which would put downward pressure on the real interest rates and support gold prices.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the January Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Pandemic 2020 Is Gone! Will 2021 Be Better for Gold?

January 15, 2021, 5:04 AMHurray! The disastrous year of 2020, which brought about the COVID-19 pandemic, the Great Lockdown, and the economic crisis, is over! Now, the question is what will 2021 be like – both for the U.S. economy and the gold market.

To provide an answer, below I analyze the most important economic trends for the next year and their implications for the yellow metal.

- Society gains herd immunity by vaccination and the health crisis is overcome.

- With herd immunity approaching, the social fabric returns to normality, and the economy recovers.

- The vaccine rollout increases the risk appetite, reducing the safe-haven demand for both gold and the greenback .

- The return to normality and realization of the pent-up demand (comeback of spending that was put on hold during the U.S. epidemic ) accelerates the CPI inflation rate .

- The Fed stays accommodative, but the recovery in the GDP growth and the labor market makes the U.S. monetary policy less aggressively dovish than in 2020.

- However, the Fed continues to use all of its tools to support the economy in 2021 and, in particular, it does not hike the federal funds rate , even if inflation rises.

- As a result, the real interest rates stay at ultra-low levels. However, the potential for further declines, similar in scale to 2020, is limited, unless inflation jumps.

- The American fiscal policy also remains easy, although relative to 2020, government spending declines, while the budget deficit narrows as a share of the GDP.

- However, the public debt burdens continue to rise. Although the ratio of debt to GDP decreased in Q3 2020 amid the rebound in the GDP, it’s likely to increase further in the future, especially if Congress approves the new fiscal stimulus.

- Given the dovish Fed conducting a zero-interest rate policy , increasing debt burden, and strengthened risk appetite amid the vaccine rollout, the U.S. dollar weakens further. The American currency has already lost more than 11 percent against a broad basket of other currencies since its March peak.

What does this macroeconomic outlook imply for the gold prices? This is a great question, as some of the trends will be supportive for the yellow metal, while others might constitute headwinds, and some factors could theoretically be both positive and negative for the price of gold. For instance, the end of the recession seems to be bad for the yellow metal, but gold often shines during the very early phase of an economic recovery, especially if it is accompanied by reflation, i.e., a return of inflation.

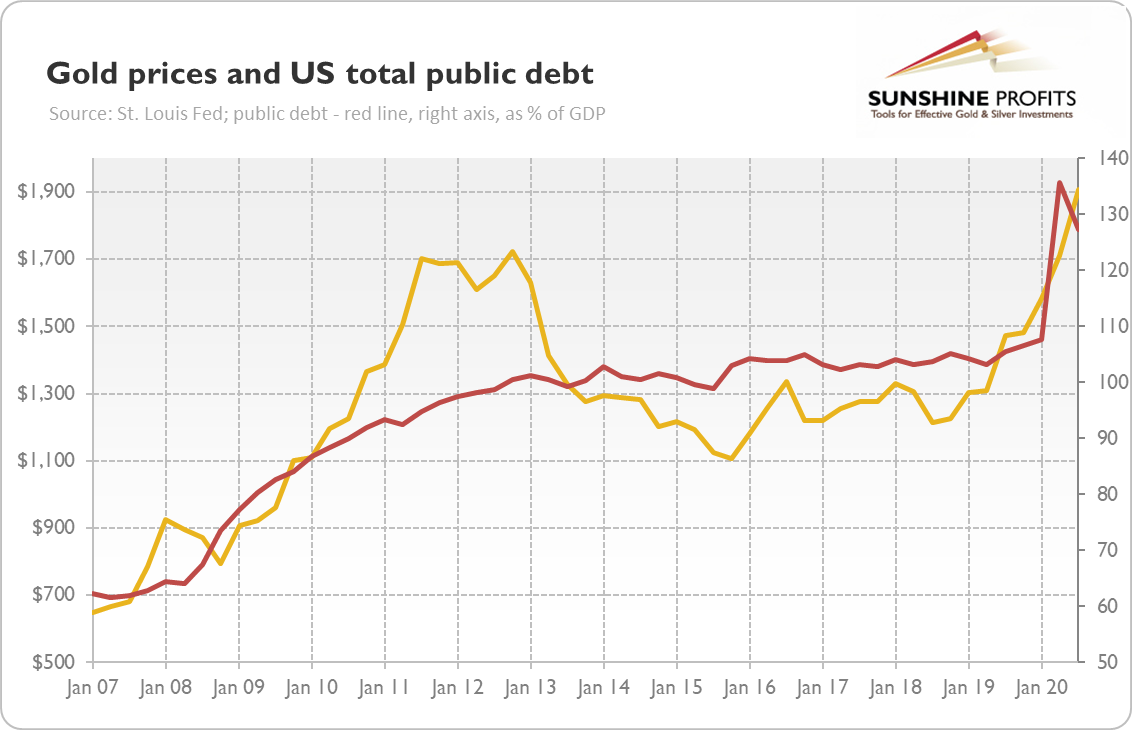

The tailwinds include the continuation of easy monetary and fiscal policies. The federal debt will remain high, while the interest rates will stay low, supporting the gold prices, as was the case in the past (see the chart below).

There is also an upward risk of higher inflation. In such a macroeconomic environment, the U.S. dollar should weaken against other currencies, thus supporting gold prices. As a reminder, the relative strength of the greenback in recent years (see the chart below) limited the gains in the precious metals market.

However, there are also headwinds. You see, levels are significantly different concepts than changes. The latter often matter more for the markets. What do I mean? Well, although both monetary and fiscal policies will remain accommodative, they will be less accommodative than in 2020. Although the real interest rates should stay very low, they will not decline as much as last year (if at all).

In other words, the economy will normalize this year after suffering a deep downturn in 2020, so the economic policy will be less aggressive. Hence, the level of bond yields and the ratio of federal debt to GDP should stabilize somewhat – actually, thanks to the rebound in the GDP in the third quarter of 2020, the share of public indebtedness in the U.S. economy has decreased, as the chart below shows.

Hence, although the price of gold could be supported by the continuation of easy monetary and fiscal policies, low real interest rates, and weak dollar, it’s potential to rally could be limited. The accommodative stance of central banks and unwillingness to normalize the monetary policy for the coming years should prevent a significant bear market in gold, but without any fresh triggers of further declines in the bond yields or without the spark of inflation, the great bull market is also not very likely. So, unless we either see a serious solvency crisis or sovereign debt crisis, or an substantial acceleration in inflation, gold may enter a sideways trend. Or it can actually go south, if it smells the normalization of monetary policy or increases in the interest rates.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the January Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

The Gold Market in 2020 and Beyond

January 8, 2021, 11:12 AMWas the past year good for the yellow metal? What happened in 2020 and what will 2021 be like for the gold market?

Nobody expected the Spanish Inquisition! And nobody expected a pandemic in 2020! Oh boy, what a year… How good that 2020 has already passed! It was an extraordinary year, unlike any other in many decades. Unfortunately, 2020 was a disastrous time for many people all over the world who suffered from COVID-19 or whose relatives and friends died because of the coronavirus or the collapse of the healthcare system… Our thoughts are with them. Many others lost their jobs or income, and all of us suffered from loneliness and limited freedom during the Great Lockdown. Indeed, it’s good that 2020 is over – and we hope that 2021 will be much better!

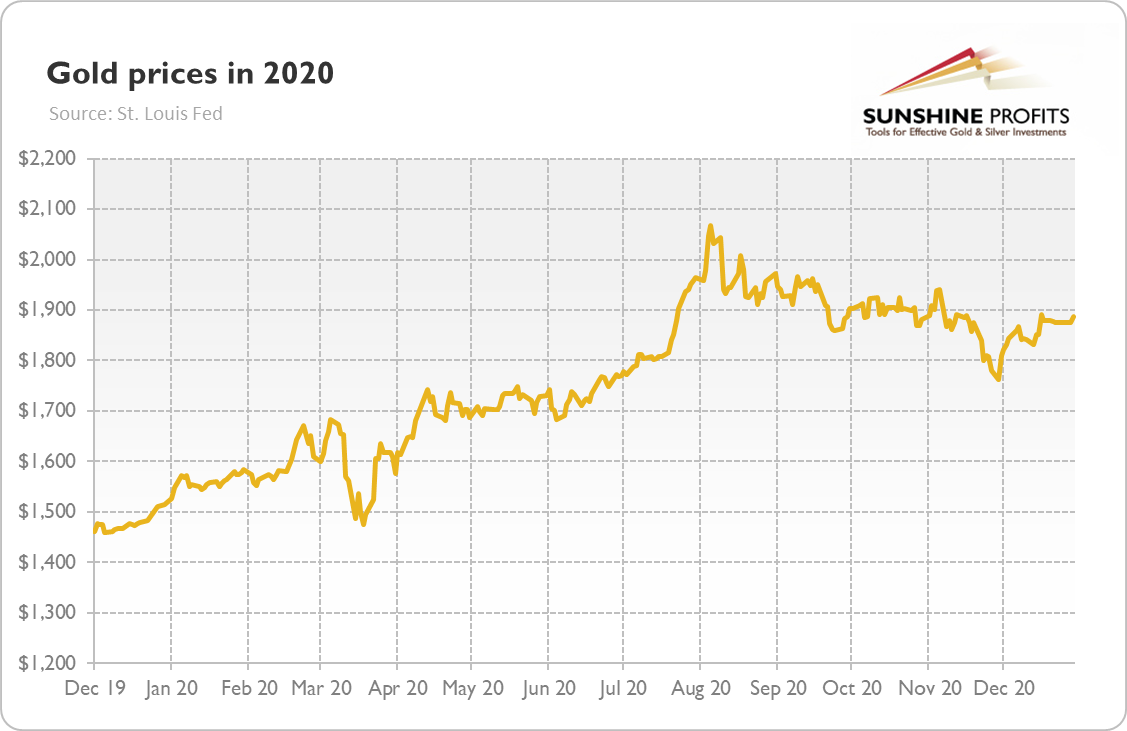

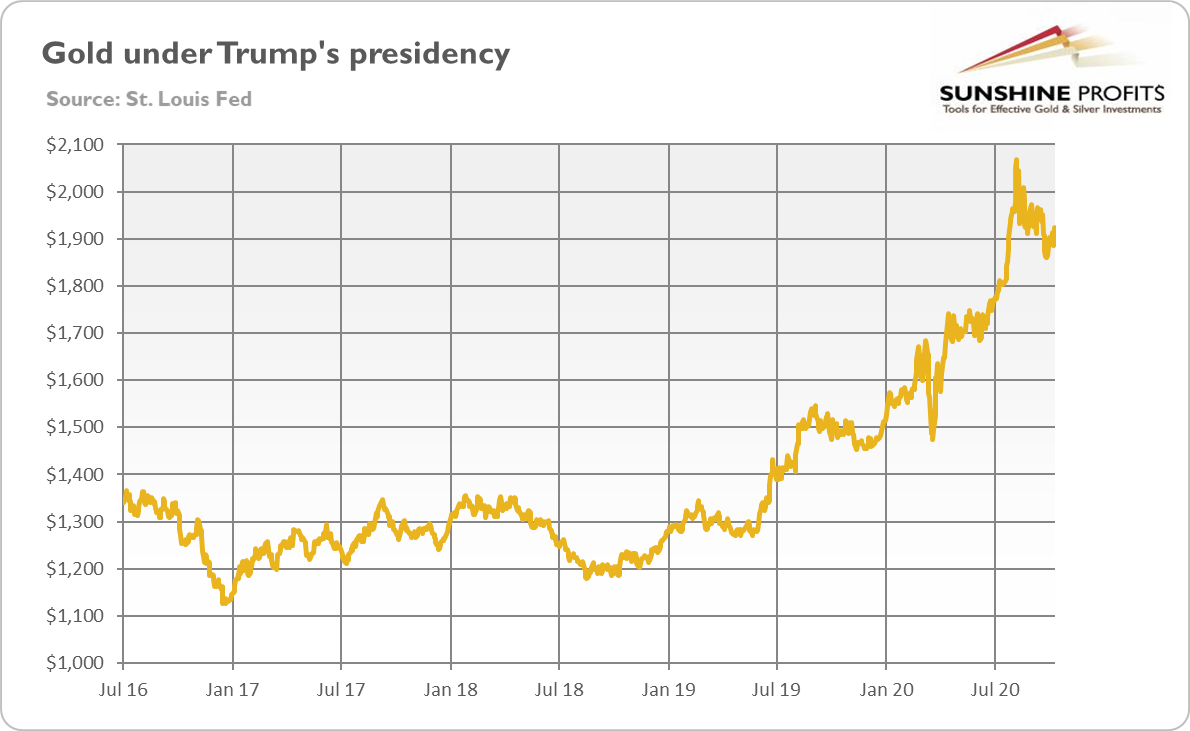

And what did 2020 mean for gold? Well, it turned out that last year was gracious to the yellow metal. As the chart below shows, gold entered 2020 with a price of $1,515 per ounce, and finished the year at $1,888 (London P.M. Fix as of December 30). It means that the shiny metal rose over 24 percent – that’s not bad considering other assets were hit really hard during the economic crisis!

Actually, 2020 was definitely better for gold prices than 2019, when the yellow metal gained “only” over 18 percent. As I didn’t predict the global pandemic (who did?), I didn’t forecast such strong gains in my base scenario. However, given the inversion of the yield curve in 2019, I expected a kind of economic downturn that would positively impact gold prices. One year ago, in a January 2020 edition of the Gold Market Overview, I wrote:

unless anything ugly happens, the macroeconomic environment could be less supportive for gold than in 2019. However, bad things do happen, and, according to Murphy’s law, anything that can go wrong will go wrong. Hence, the gold fundamentals may turn out to be more positive for gold over the year. After all, the yield curve has inverted last year and we are already observing some recessionary trends, especially in the manufacturing sector and among the small-sized companies (…) given the amount of black swans flying just above the market surface, gold might provide us with some bullish surprises as well.

And indeed, the black swan (or perhaps a white or gray swan) landed in 2020, pleasing the gold bulls. However, despite gold’s impressive performance, some people complain that gold didn’t rally more during the coronavirus turmoil. I completely understand this disappointment – after all, the world suffered its deepest economic downturn since the Great Depression, larger even than the Great Recession, and gold gained only 24.6 percent?

However, the crisis was deep but very short, as we quickly learnt how to live with the virus, while our brilliant scientists swiftly developed vaccines. Moreover, this time banks were resilient and there was no financial crisis. Another factor is that gold actually rallied more than 36 percent until its peak in August (or more than 40 percent counting from the bottom), but it later corrected somewhat.

Indeed, we can distinguish a few phases in the gold market in 2020:

- A pre-pandemic bullish phase caused by easy monetary policy and worries about the coronavirus, that lasted until mid-February, with the price of gold increasing from $1,515 to $1,604 (5.9 percent) on February 19, just before the stock market crash.

- The bullish period (with a short bearish correction) more closely related to the unfolding pandemic, the stock market crash and central banks’ panic and bold responses. It started on February 20 and ended on March 6, when the price of gold reached $1,684 (gaining 5 percent).

- The bearish phase caused by investors’ panic selloff of all assets in order to raise cash. It lasted until March 19, when the price of gold reached its 2020 bottom of $1,474 (a decline of 12.5 percent).

- A super bullish phase that lasted until August 6, when the price of gold reached its all-time peak of $2,067, soaring 40.2 percent in just four and half months. This period can be split into: the bullish phase, caused by the coronavirus shock, that lasted until mid-April; the consolidation period, that came when the financial markets calmed down as the initial doomsday scenarios didn’t materialize, and lasted from mid-April to mid-June; and another bullish phase, caused by disastrous economic data for the first half of 2020, and massive stimulus programs delivered by the central banks and governments.

- The bearish period, during which the yellow metal declined to $1,763 on the last day of November, or 14.7 percent, due to positive vaccine-related news and reduced geopolitical uncertainty after the U.S. presidential elections.

- The bullish remainder of the year, during which gold rose to $1,888, or 7 percent, caused by the dark COVID-19 winter, poor economic data, strengthened prospects of another government financial stimulus, and related worries about the rising U.S. debt.

So, it’s pretty obvious that the course of the pandemic was one of the most important tailwinds for the gold prices in 2020. Thus, the correction caused by the vaccine breakthroughs is not surprising, given the scale of the previous rally. However, please note that gold reacted not to the pandemic itself, but rather to the investors, governments, and central banks’ reaction to it. The yellow metal gained the most when investors were fearful, and when the Fed and Treasury injected liquidity into the markets.

This all bodes well for gold in 2021. After all, the U.S. central bank won’t cease conducting its very easy monetary policy, while a Biden-Yellen duo will continue the dovish fiscal policy inherited from the Trump administration. Such a policy mix should support gold prices. Of course, the scale of accommodation would be lower than in 2020, so gold’s performance in 2021 could be worse than last year. But unless we see a normalization in the monetary policy and an increase in the real interest rates, the bull market in gold shouldn’t end.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the January Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Biden Trigger Inflation for Gold?

December 18, 2020, 9:50 AMPresident-elect Joe Biden is expected to increase further government spending. For this and also other reasons, there is a risk that inflation under Biden’s presidency could be higher than under Trump’s. That would be great news for gold.

Let’s face it, Biden won’t have an easy presidency. And I’m not referring to the fact that he will be sworn in as the oldest president in U.S. history or that he will have to deal with the coronavirus pandemic and the process of vaccine distribution across the country. I’m referring to Biden inheriting an economy with slow growth and too much public debt. Given the debt burden, it should be clear that under Biden’s presidency, real interest rates will remain at ultra-low levels. This is how a debt trap works – the more the debt grows, the less the economy (Treasury) can afford higher interest rates.

Moreover, Biden will have to face the risk of inflation. Actually, some analysts say that the new POTUS could contribute to the rise of prices. Is it true? Will we finally see an acceleration in the inflation rate?

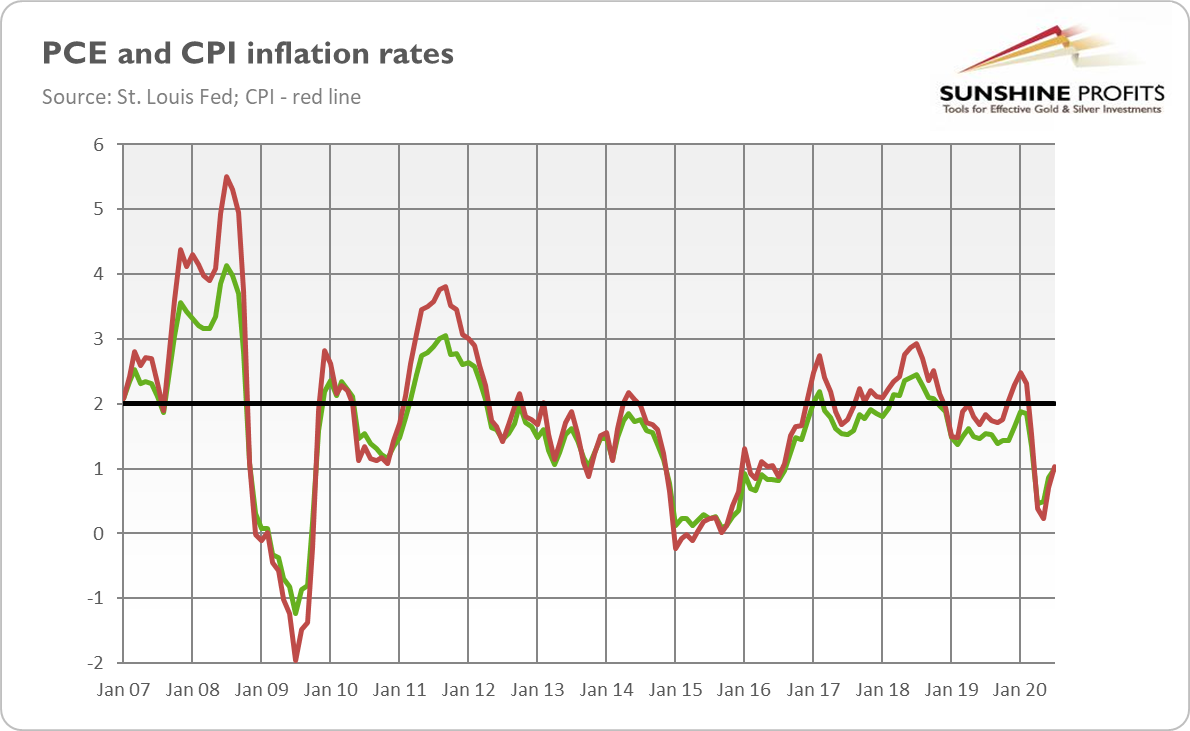

So far, consumer inflation has been subdued. As the chart below shows, the CPI overall annual rate has declined from 2.3 percent before the epidemic to 1.2 percent in October.

For some people, this is all really surprising given all the money pumped by the Fed into the economy. However, the disinflation is perfectly in line with our predictions from the May edition of the Gold Market Overview: “In the short run, we expect disinflation, but we think that the risk of inflation later in the future is higher than a decade ago.”

Indeed, in the short-run, the negative demand shock outweighed other factors, and people simply increased their demand for money because of the enormous uncertainty and limited opportunities to spend money in the offline economy.

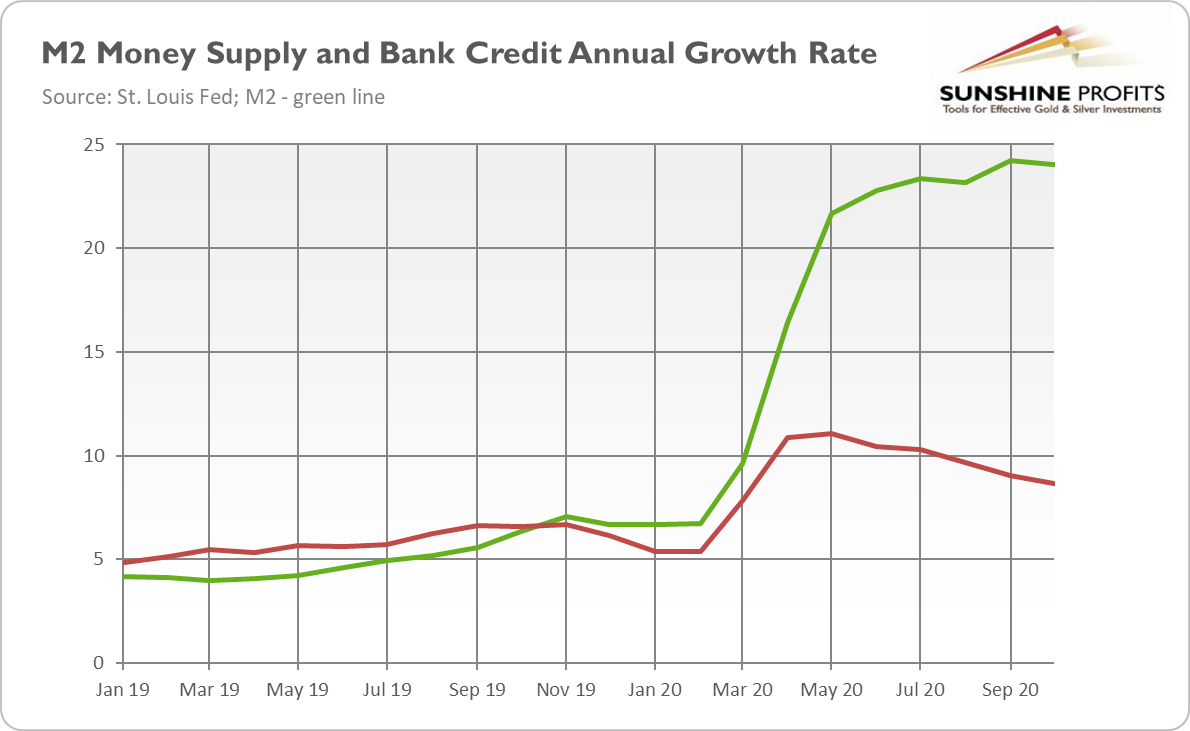

But didn’t the Fed significantly increase the money supply? It did, but the central banks create only a monetary base, while the majority (more than 90 percent) of the broad money supply is created by the commercial banks. So, for inflationary trends, what really matters is not the Fed’s balance sheet, but rather the commercial banks’ credit expansion, since whenever the banks grant loans, they also create deposits, i.e., money supply.

Hey, wait a moment, but didn’t the pace of expansion of the banks’ credit and broad money supply also rise? They did! Just look at the chart below. And this is the reason why I believe that the risk of inflation in the aftermath of the coronavirus crisis is higher than after the Great Recession, when banks were strongly hit and didn’t want to expand credit.

Now the situation is different. However, banks expanded loans not to the consumers but to the entrepreneurs, probably because they needed credit to stay afloat during the Great Lockdown. So, the acceleration in the bank credit could be temporary – indeed, the pace of its expansion has been slowing down recently. But when the pandemic is over, consumers may again tap credit cards and real estate loans.

Indeed, this is an important upward risk for inflation. Some economists point out here the pent-up demand, i.e., the strong increase in demand for a service or product, usually following a period of subdued spending. The idea is that consumers tend to hold off their demand during a recession, only to unleash it during recovery. It makes sense; during a crisis, the uncertainty rises, so people try to cut expenses and accumulate cash. When confidence returns to the marketplace, people spend money more freely.

The same could happen during the current pandemic – not only did uncertainty rise, but people also had to practice social distancing and obey sanitary restrictions, which forced them to reduce their expenditures. Hence, when the pandemic is over, the demand for cash may fall, while spending could increase, thereby accelerating inflation. Of course, some demand will simply stay unrealized forever (it would be impossible to make up for all these missed opportunities to drink beers with friends), but when the storm is over and vaccines boost people’s confidence, they will spend a substantial part of their extra savings accumulated during the pandemic.

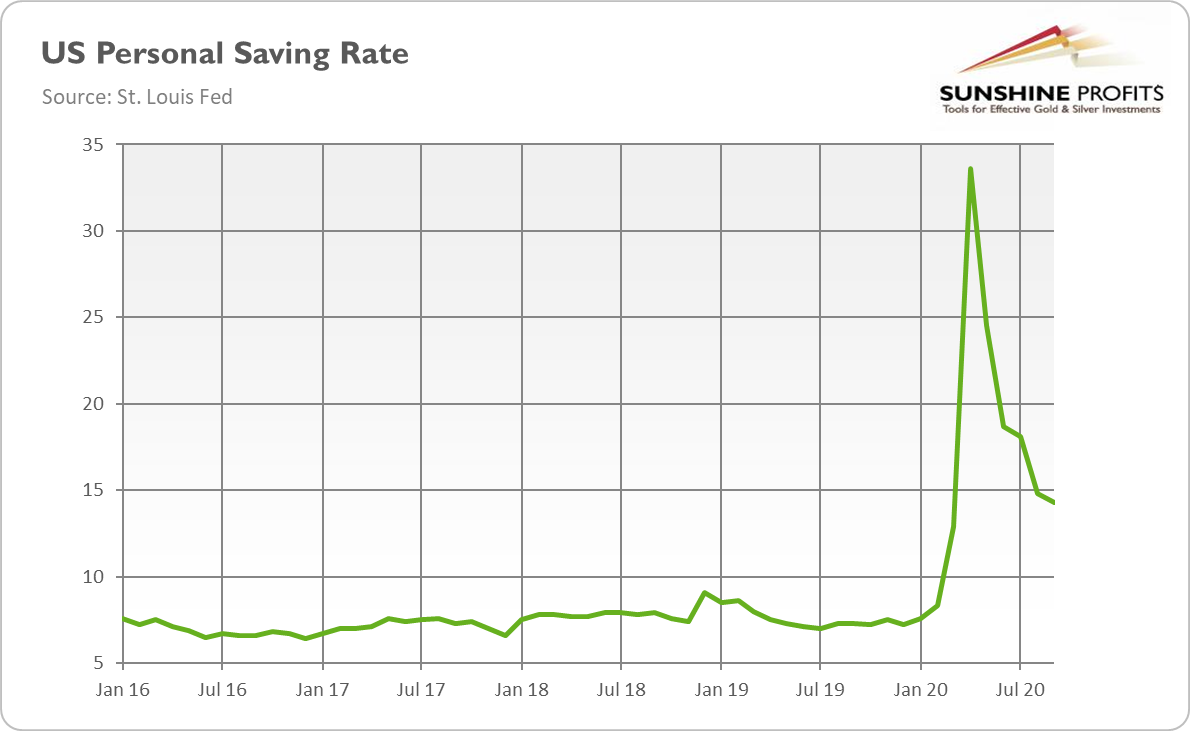

Just take a look the chart below – as you can see, the U.S. personal savings rate has increased from about 8 percent before the epidemic to almost 34 percent in April. Now it is staying above 14 percent, so there is still potential to increase consumer spending in the future.

In other words, people and businesses have not yet used all the stimulus they got from the Fed or the government. Because of this uncertainty, they spent as little as they could, and saved as much they could. Why this is so important? Because when people decide to spend their mountain of money, inflation could accelerate, boosting the demand for gold as an inflation hedge.

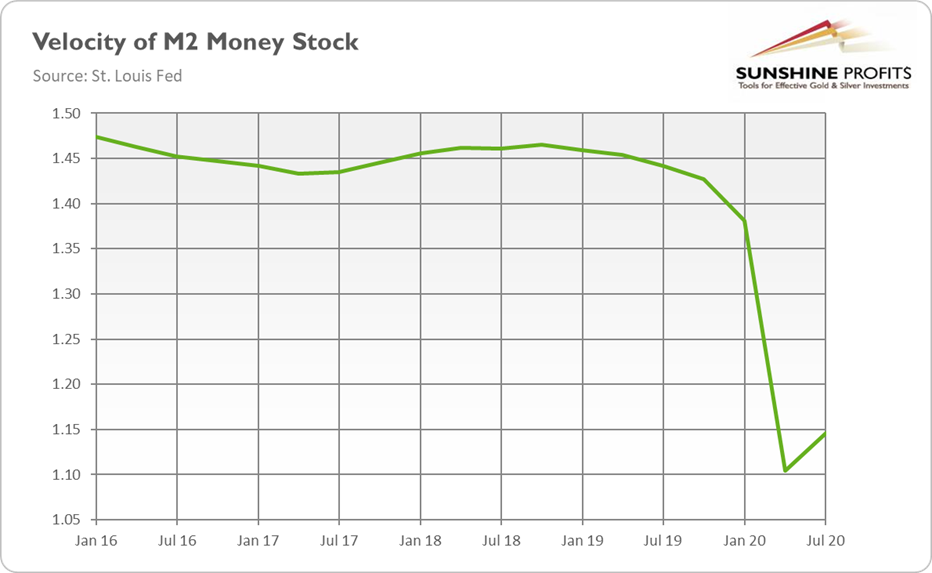

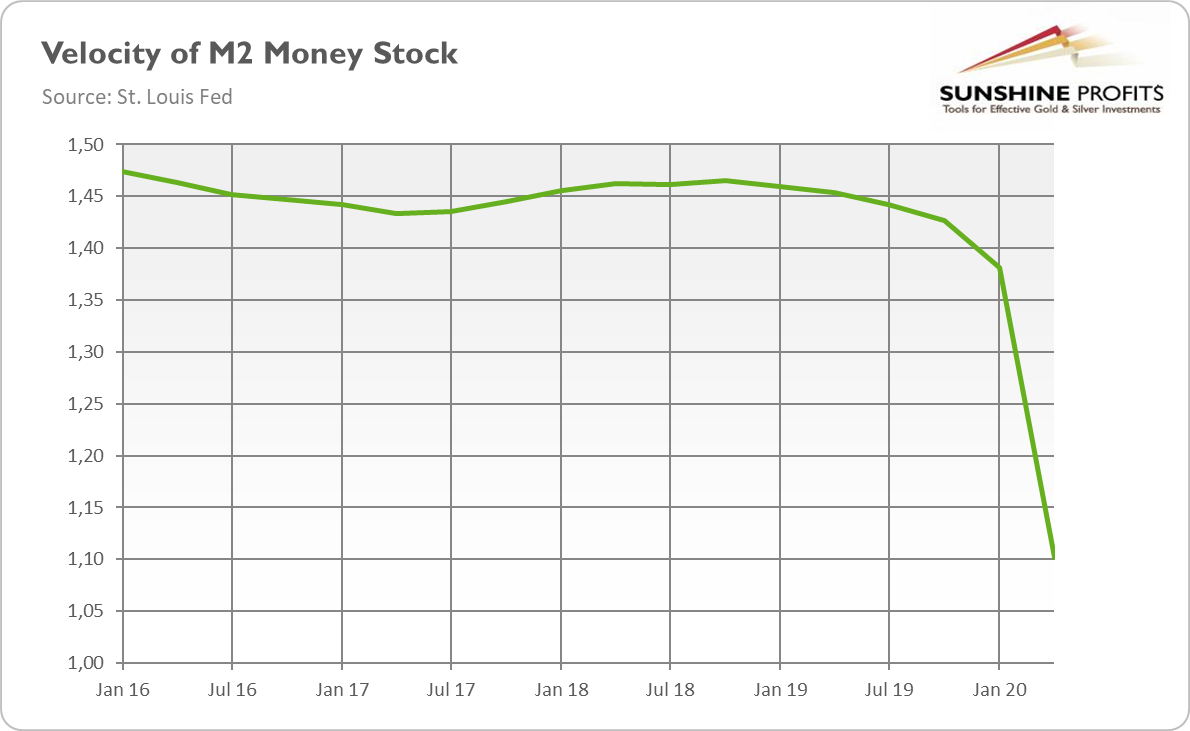

Hence, when the pandemic storm is over, the demand for money should decrease, or the velocity of money should increase. Actually, this is what we have observed in the third quarter of this year – the velocity of M2 money supply has rebounded somewhat, as the chart below shows. So, although the second wave of COVID-19 infections would hamper this process, it’s possible that in 2021 we will see a rise in inflation. Higher inflation also means lower real interest rates, which is another piece of good news for the yellow metal.

Last but not least, Biden is a supporter of major economic relief, including a second round of stimulus checks, so consumers’ spending power should increase further next year, thus contributing to higher consumer prices. So, although it’s not determined, there is a risk that inflation under Biden’s presidency could be higher than under Trump’s presidency. It would be great news for gold, especially that the Fed’s new regime means that it will not strongly react to rising inflation.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the December Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Is the Vaccine a Game-Changer for Gold?

December 11, 2020, 9:04 AMThe vaccines are coming – we’re saved! Although the arriving vaccines are great for humanity, they are bad for the price of gold.

In November, Pfizer and BioNTech announced that their mRNA-based vaccine candidate, BNT162b2, had demonstrated evidence of an efficacy rate above 90% against COVID-19, in the first interim efficacy analysis. As Dr. Albert Bourla, Pfizer Chairman and CEO, said:

Today is a great day for science and humanity. The first set of results from our Phase 3 COVID-19 vaccine trial provides the initial evidence of our vaccine’s ability to prevent COVID-19.

Indeed, the announcement is great news! After all, the vaccine is the ultimate weapon against the virus. There’s no doubt that we will get the vaccine one day. Thank God for scientists – they are really clever people who work hard to develop a safe vaccine! Why can’t we have more of them instead of so many economists? As well, the pandemic triggered unprecedented global cooperation to develop a vaccine as quickly as possible. The funds are enormous, while the bureaucrats eventually decided to behave like decent human beings for once and eased their stance in order to speed up the whole process. Great!

But… there is always a “but”. You see, there are some problems related to Pfizer’s vaccine. First, all we know comes from the press release, but the company didn’t provide any data for a review. Second, the efficacy rate announced by the company pertains only to the seven days after the second dose is taken – we still don’t know how effective the vaccine is in the longer term, and how long immunity lasts. Third, we still don’t know the efficacy of the vaccine among the elderly and people with underlying conditions – or, the most affected people by COVID-19. Fourth, the vaccine is based on mRNA technology, and such a vaccine was never approved for human use. There is always a first time, but new technologies always give birth to some concerns, which could ultimately reduce the public’s preference to get vaccinated.

Another problem is that this vaccine requires two doses that are taken 21 days apart. It delays the moment of immunization and again reduces the motivation to take the vaccine – yes, some people are so lazy, and/or they don’t like injections so much (for whatever reason; we’re not debating whether it’s justified or not) that they can refuse to be vaccinated.

Moreover, Pfizer’s vaccine must be stored at a temperature of about -70°C (-94°F), which is quite low indeed, and can be quite chilly in shorts (unless you are Wim Hof). The problem is transportation and distribution – you see, many hospitals - to say nothing of rural physicians and pharmacies, and healthcare systems in developing countries - do not have adequate freezers to store the vaccine. Last but not least, even if scientists develop the best possible vaccine, it remains useless unless people accept to take it – and this is far from being certain, given the pandemic denial movement and fear of vaccines.

Sure, one could say that all these points are not very problematic. After all, Pfizer is not the only company working on the vaccine. There are actually more than 150 coronavirus vaccines in development across the world. For example, Moderna’s vaccine can be stored at a much higher temperature – a more comfortable -20°C (-4°F), So even if Pfizer’s vaccine turns out to not be the best, other, even better vaccines will arrive on the market – and a lack of any vaccine can transform into a crisis of abundance.

That’s true, but the sad truth is that it’s unlikely that any vaccine will be widely available until mid-2021. Pfizer, for example, announced that it hoped to produce 50 million doses by the end of 2020. As the vaccine needs two doses, only 25 million people could be vaccinated this year. So don’t count on being among this group – countries will prioritize healthcare workers, social workers and uniformed services first, and the elderly next. It means that we will not return to a state of normalcy very soon, and most of us will still need to wear masks, practice social distancing and… wash hands!

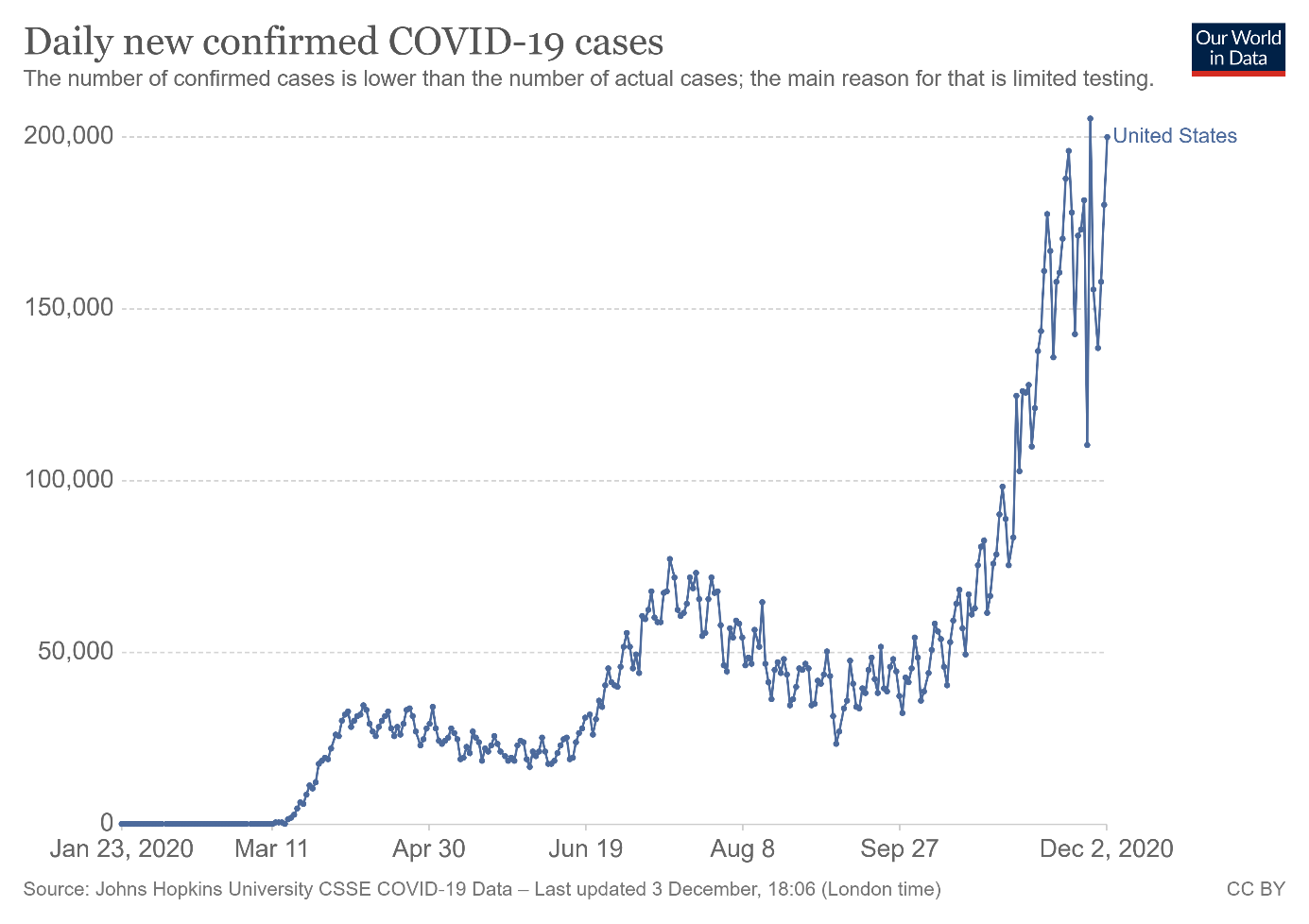

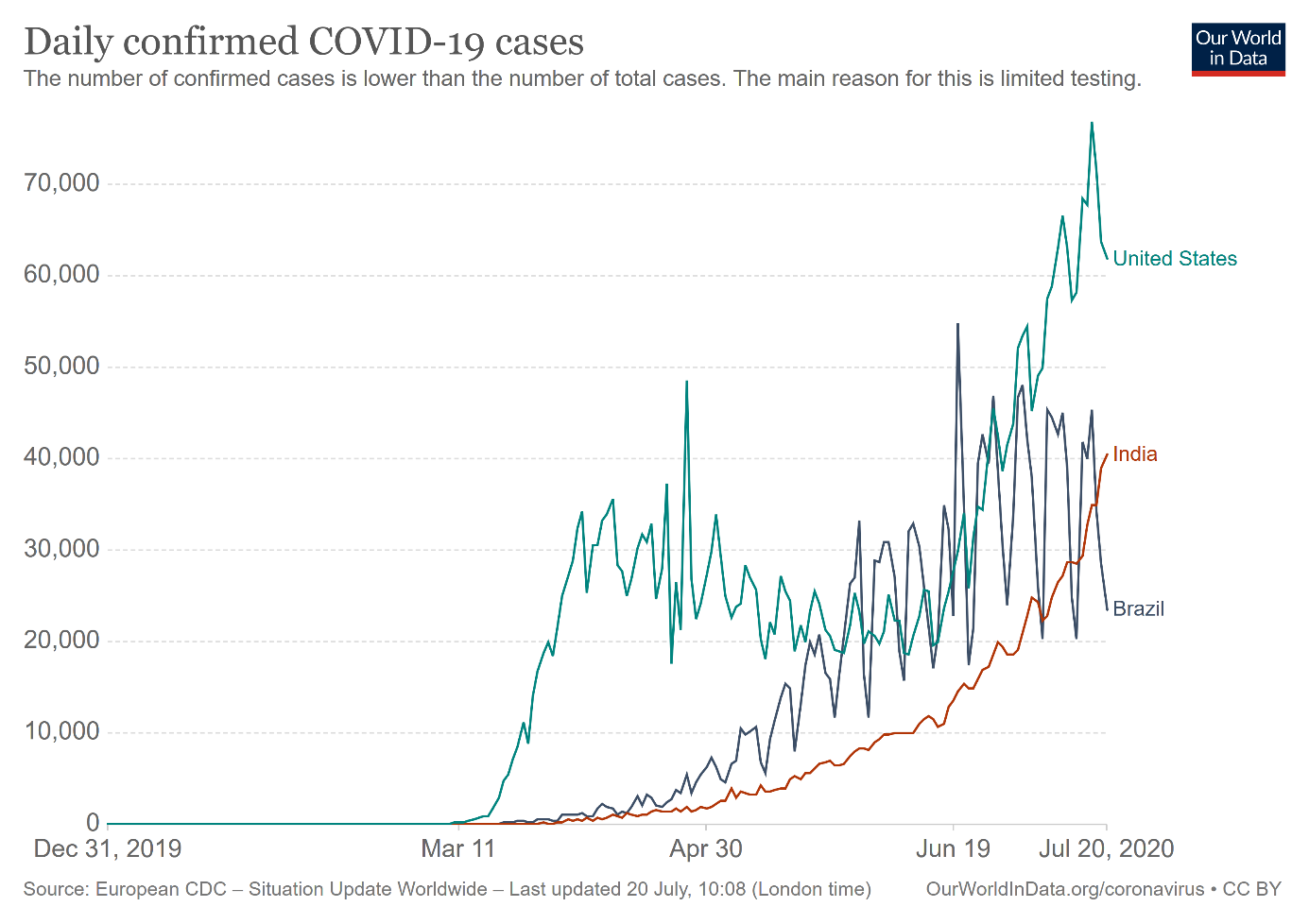

In the meantime, the U.S. is about to enter Covid hell, as Michael Osterholm, one of Biden’s advisers on the epidemic, said. Indeed, the country is nearing 11 million reported COVID-19 cases, and the coronavirus has already killed more than 240,000 Americans. But the worst can still lie ahead for the U.S. As one can see in the chart below, the epidemiological curve is clearly exponential and the daily number of new cases has touched 200,000! Yup, you read it correctly, about two hundred thousand people are infected each day. You don’t have to be a mathematician to figure out that at such a rate of infections, the healthcare system will collapse soon.

What does it all imply for the gold market? Well, although the arriving vaccines are great for humanity, they are bad for the price of the yellow metal. The pandemic greatly supported gold prices. So, the expected end of the epidemic in the U.S. should be negative for the shiny metal.

However, there are two important caveats to this statement. First, there is still a long way to go before widespread vaccination and a true end to the pandemic. In the interim, we still need to face the COVID-19 challenge, so gold shouldn’t suddenly fall out of favor.

Second, gold reacted not only to the pandemic itself, but also – or even more – to the world response of governments and central banks to the health and economic crisis. The easy monetary policy and accommodative fiscal policy will not disappear only because of the vaccine’s arrival. Actually, the harsh winter or “Covid hell” that awaits America will force the Fed and Treasury to continue or even to expand their stimuli, which is good news for gold prices from the fundamental perspective.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the December Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

What Does Biden Imply for Gold?

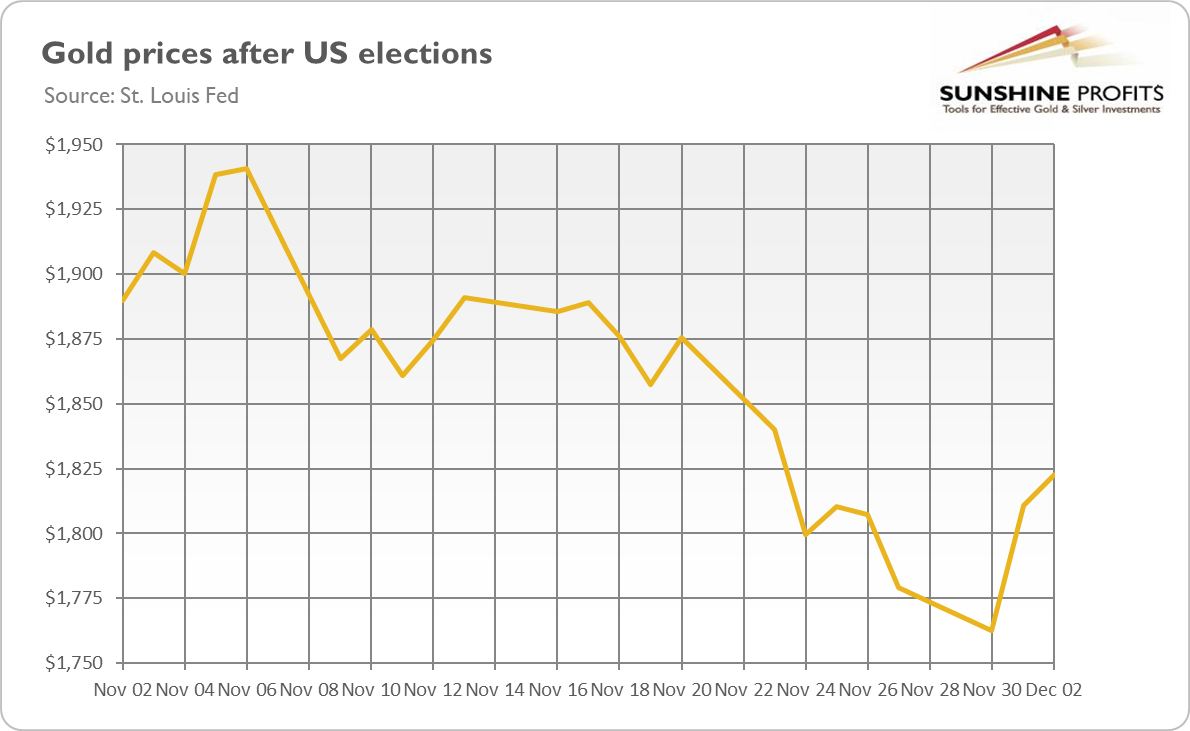

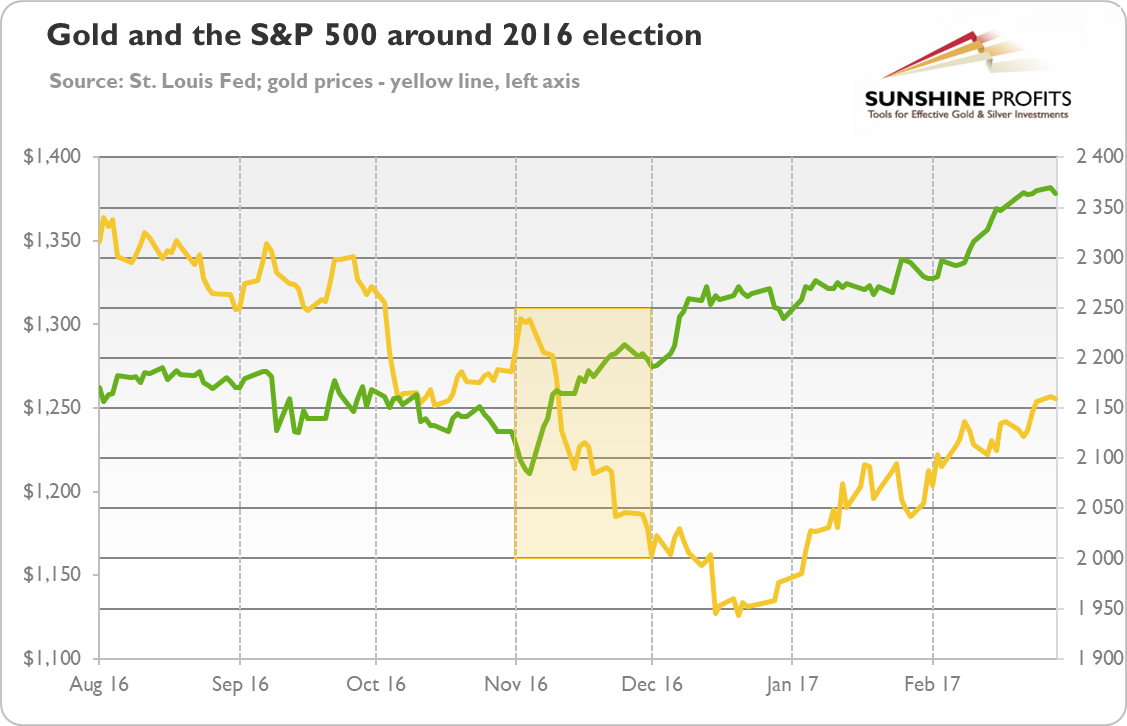

December 4, 2020, 6:30 AMAmerica has elected a new President. It was a close race, but Joe Biden eventually won and he will be inaugurated and take office in the White House on January 20. The price of gold rose initially in the aftermath of the elections, only to plunge on the news regarding Pfizer’s vaccine breakthrough, as the chart below shows. This is what we know.

But what’s next for the price of gold? What does a Biden presidency mean for the yellow metal? To answer these vital questions, we will analyze the agenda of the President-elect. On the official Biden-Harris Presidential Transition website, we found that the new administration has four priorities: COVID-19, economic recovery, racial equity, and climate change.

The first issue obviously concerns the pandemic. While Trump remained relatively indecisive as to whether to fight aggressively with the coronavirus or to downplay the threat – which I believe cost him the votes of the elderly and ultimately a second term – Biden seems to be determined to beat the epidemic. He has acknowledged the challenge and promised to listen to science and health professionals, although it remains to be seen whether he will actually do so. Regardless, Biden has a seven-point plan to combat the virus, of which the two most important points are: 1) to ensure all Americans have access to regular, reliable, and free testing; 2) to implement mask mandates nationwide by working with governors and mayors and by asking the American people to do what they do best: step up in a time of crisis.

Boosting testing rates is a great idea. Quick and widespread testing, combined with contact tracing, is believed by many epidemiologists to be the best idea in combatting the virus. The mask mandates, although controversial from the libertarian point of view, could also importantly reduce transmission of COVID-19. Also important is what the plan does not mention. By this I mean the lack of any references to a lockdown. Therefore, Biden’s determination to beat the virus without resorting to a lockdown, is rather negative for gold prices.

The second priority is economic recovery. The most important points of Biden’s agenda concern building more modern infrastructure, which implies higher government spending. Importantly, Biden plans to partially fund these expenditures by reversing some of Trump’s tax cuts for corporations. Moreover, Biden plans to reform the labor market. He proposes more than doubling the minimum wage, raising it from $7.25 to $15 an hour. He also wants to make it easier for workers to organize unions, and to implement universal paid sick days and 12 weeks of paid family and medical leave. Widening access to affordable health care is also a stated goal.

From the economic point of view, such bold reforms in the labor market that would increase labor costs are not the best idea during an economic recovery, when many small and medium entrepreneurs are still struggling to survive in the market. Reversal of tax cuts would also not be welcomed by Wall Street and corporate America. So, Biden’s economic agenda could benefit gold somewhat, especially if higher infrastructure spending is financed by large fiscal deficits and if it further increases public debt.

However, a lot depends on the narrative adopted by market participants. If investors focus not on the rising public debt, but on the revival of infrastructure and economic recovery, then gold may struggle. However, I believe that in the current macroeconomic environment of low real interest rates, rising public debt and risk of higher inflation in the future, gold should perform satisfactorily.

The third priority of racial equity is described in a somewhat vague manner, which takes the form of postulates rather than specific points. The agenda definitely includes police reform legislation to reduce racial disparities within the criminal justice system. The push for greater racial equity shouldn’t impact gold prices significantly.

And finally, Biden also wants to deal with climate change by investing in green infrastructure, and hoping to achieve a carbon pollution-free power sector by 2035 and net-zero emissions, economy-wide, by no later than 2050. This plan is bold and if the new administration focuses too much on the environment, it could easily burden the private sector with regulations and hamper economic growth. So, this can be positive for gold prices, especially when combined with fresh fiscal stimulus, higher government spending, and ballooning federal debt.

To sum up, Biden’s presidency could be somewhat positive for gold prices due to higher government spending and anti-corporate points like the reversal of Trump’s tax cuts and increasing labor costs (raising the minimum wage, etc.). However, Biden’s impact on the gold market is likely to be smaller than previously thought by many analysts. This is because Republicans may remain in control of the Senate (if they win at least one of two seats in Georgia’s runoff in January), with power to block the most radical ideas of the new administration.

Moreover, the Republicans performed above expectations in the elections, gaining seats in the House and almost retaining the White House. It clearly shows that voters do not support the most progressive elements of the Democrats’ agenda. Biden is, therefore, likely to govern more as a centrist rather than a radical leftist, which is positive for the economy, but bad news for gold prices. Nevertheless, investors shouldn’t overestimate the power of the President over the economy. It means that gold’s bull market can continue under Biden’s presidency, unless the macroeconomic outlook changes abruptly and the real interest rates start to rise.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the December Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Soaring Public Debt and Gold

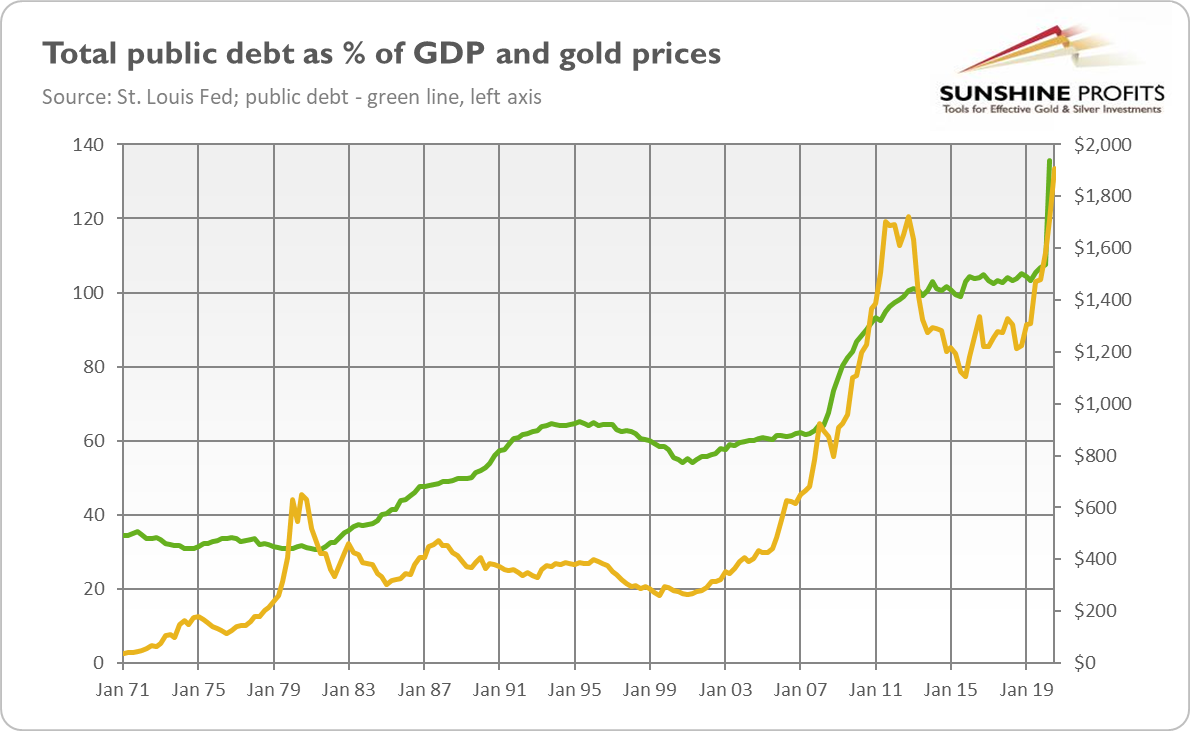

November 20, 2020, 8:02 AMThe global debt is rising at an alarming pace. According to the IMF, the median debt in 2021 is projected to jump by about 17 percent of GDP in advanced economies, 12 percent in emerging economies, and 8 percent in low-income countries.

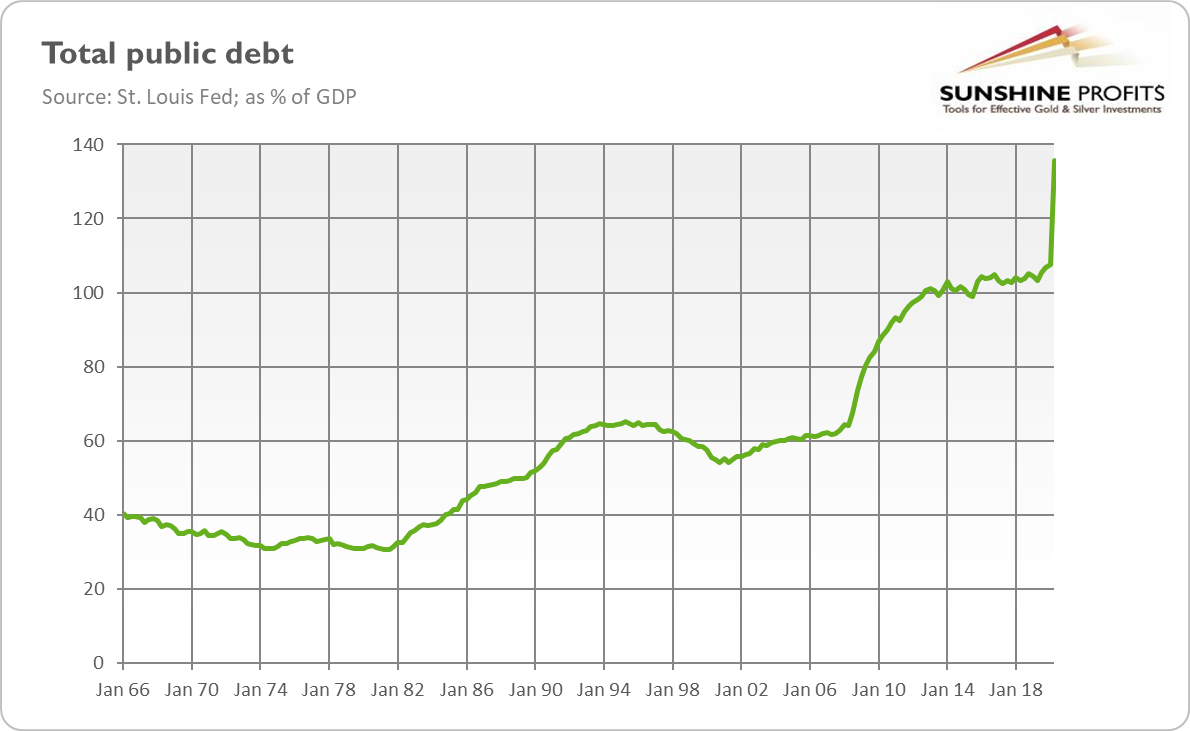

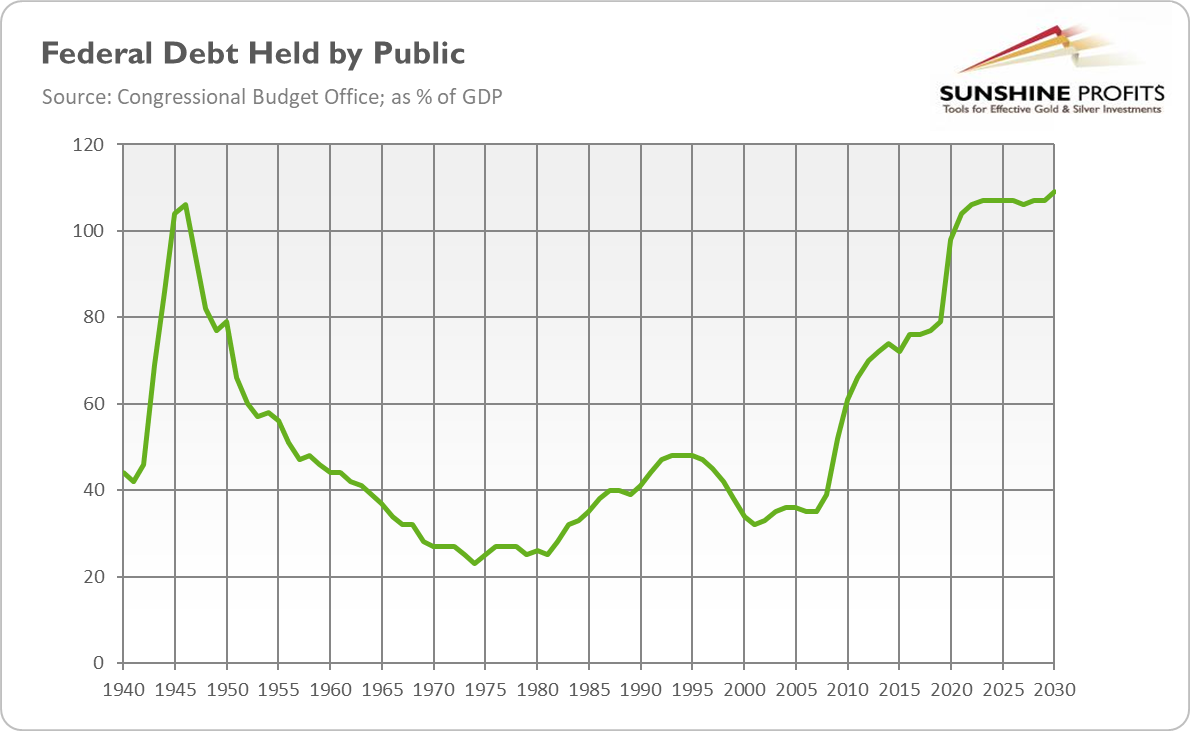

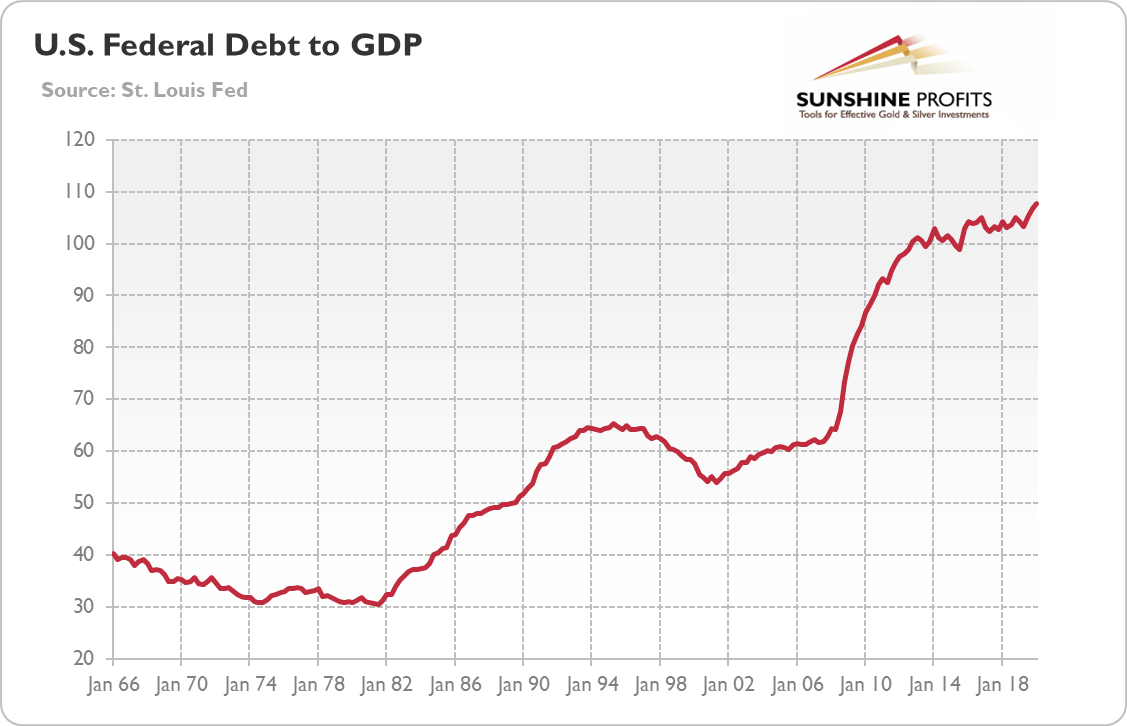

In particular, during the second quarter of 2020, the total US public debt has soared from 108 to 136 percent of the GDP, amid the massive spending in response to the pandemic. As the chart below shows, this is a record level in peacetime. It’s also among the highest debt-to-GDP ratios in the developed world: the US is behind only Japan, Greece, Italy, and Portugal. So, it seems that it’s modern monetary theory and not the coronavirus that has infected Washington, as nobody seems to worry about who will pay for all this spending and debt.

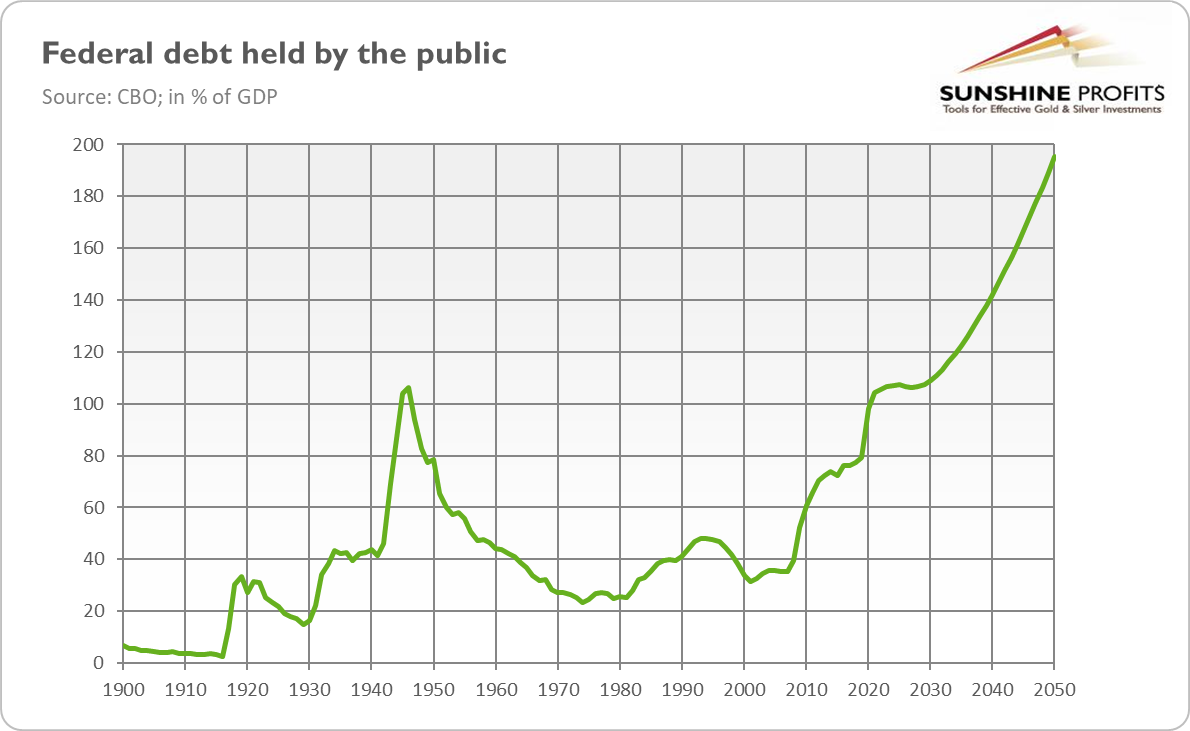

Most importantly, the federal debt held by the public is also skyrocketing. As the chart below shows, it is projected by the Congressional Budget Office to jump from 79 percent last year to 98 percent of GDP in 2020, to 107 percent by 2023 (the highest level in the history of the United States) and to soar even further, to 195 percent of GDP by 2050. So, the ballooning debt is not just a temporary problem caused by the epidemic – it’s an important structural problem of the American economy.

However, this is not the end of the government spending spree and ballooning federal debt. In the Q3, the budget deficit increased by $237 billion and in the upcoming months it is projected to soar even further. After all, both Republicans and Democrats want to increase the fiscal stimulus. The last White House offer stands at $1.8 trillion. If accepted, the total public debt would spike from the current $26.5 trillion in the second quarter of 2020 (see the chart below) to at least $28.5 trillion, or about 143 percent of the GDP, in the very near future.

How will this mammoth spike in the public debt affect the gold prices? That’s a good question! Let’s analyze the past relationship between these two variables to examine this. The chart below does not provide us with a clear answer. We can see that gold reacted positively to the rise in public debt in the 2000s and in 2020, but it failed to shine in the 1980s and early 1990s, when the federal indebtedness also increased.

However, the correlation between the price of the yellow metal and the total public debt as a percentage of the GDP in Q1 1971 to Q2 2020 is significantly positive, as the correlation coefficient amounts to 0.89. This positive link comes mainly from the ballooning public debt in the aftermath of the Great Recession. The bailouts and fiscal stimulus provided by Bush and Obama boosted the public debt from 62 percent before the financial crisis to above 100 percent in 2012. In the same period, the price of gold skyrocketed from $680 to $1,722. And when the trajectory of the public debt has stabilized somewhat around 100-102 percent of GDP, the yellow metal entered a bear market.

But was it just a coincidence, a correlation, or a causal relationship? Well, it’s a difficult question. You see, the soaring American public debt raises worries about the sovereign debt crisis, the future value of the greenback and rising inflation. Thus, the concerns about the ballooning public debt make investors buy gold, which is considered to be both an inflation hedge and a safe-haven asset.

On the other hand, investors shouldn’t forget about the broader macroeconomic context, as soaring public debt never occurs on its own. Actually, the biggest spikes happened as a response to economic recessions (in 2007-2009 and in 2020). The public spending spree after the Great Recession coincided with the easy monetary policy, the decline in the real interest rates, and the U.S. dollar depreciation. As well, gold did not start its bearish trend only because the level of public debt stabilized somewhat, but rather because confidence returned to the marketplace, investors started to expect normalization of the monetary policy, the real interest rates begun to rise, and the greenback entered its bull market.

It means that gold should benefit from the current macroeconomic environment. The ballooning public debt should add to the concerns about the American economy and support the safe-haven demand for gold. Mainstream economists believe that given that the interest rates and debt-servicing costs are low and the US dollar remains a world reserve currency, the sovereign debt crisis is not likely. Well, last year pundits thought similarly that the pandemic was unlikely. And here we are…

Hence, rising indebtedness alone would probably be too little to make gold rally without other fundamental drivers being supportive for the yellow metal. The other side of this coin is that even when the U.S. public debt stabilizes somewhat (which is not very likely in the near future), gold does not have to plunge if other factors remain fundamentally positive.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the November Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will the Disconnect of the Stock Market Support Gold?

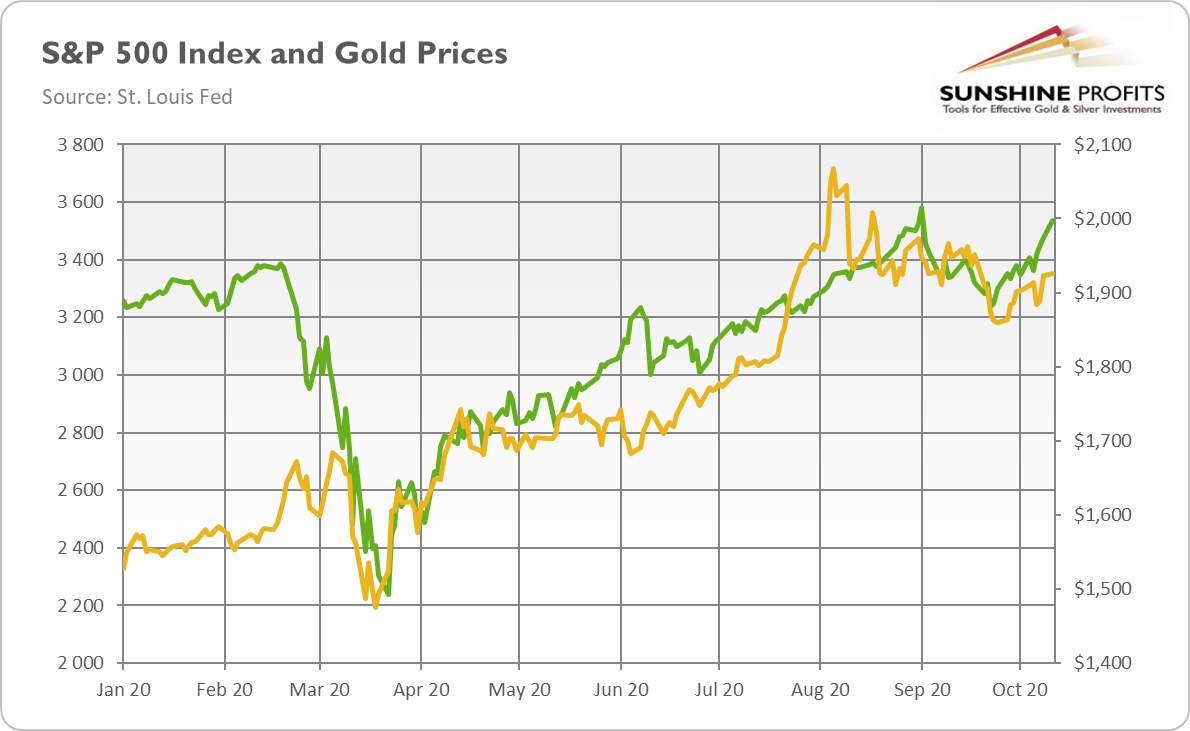

November 13, 2020, 10:27 AMThe disconnect between the US stock market and the real economy continues. The equity valuations are surging, while the economic recovery remains fragile. As the chart below shows, the S&P 500 Index has surpassed February’s peak and it did that in August, even jumping above 3,500 points. In September, there was a correction in the stock market, but again, the equity valuations are going up despite the second wave of coronavirus infections.

So, why do we see lofty equity valuations while the real economy is struggling? Well, there are several explanations for this disconnect. The first is that the stock market is forward-looking, so the current elevated stock prices may reflect optimism about the vaccine against Covid-19, a quick end to the pandemic and clear economic recovery. Of course, this outlook may be justified, but it might also be the case that markets are excessively optimistic about the initial vaccines’ efficacy. And just as the markets downplayed the likelihood and impact of the first wave of the coronavirus, they can underestimate the consequences of the second wave in the fall and winter as well. Keep in mind that the markets also expected a quick, V-shaped economic recovery, which never materialized in the U.S.

The second explanation refers to the S&P 500 composition. You see, the simple truth is that the economic pain inflicted by the epidemic and the Great Lockdown is being borne mainly by small businesses and individual service proprietors (think restaurants, tour guides, etc.), and not by publicly traded companies. The small players simply have too little capital to survive a deep recession, while the big dogs were sitting on cash (and they were often less indebted).

Although some of the listed companies were also hit by the economic crisis, others actually benefited from the pandemic. When small and medium companies went bankrupt or struggled to survive, the big players achieved an even stronger market position than before the economic downturn.

Moreover, Big Tech has a large share in the S&P 500. The five biggest constituents of the Index – Microsoft, Apple, Amazon, Alphabet (Google’s parent) and Facebook – account for about 20 percent (or even more) of the entire market capitalization, a modern-day record of market concentration. And by the way, the coronavirus crisis was tech friendly. With millions of people locked down, companies like Amazon, Microsoft or Netflix were the clear winners. But the S&P500 Index, excluding the big tech stocks (often described by acronyms: FANG/FAANG/FAANGAM) performed much worse than the general index which was clearly driven by a few giants.

Last, but definitely not least, the Fed slashed the federal funds rate to zero and backed the private bond markets. This is why the spread between the corporate and government bond narrowed, despite the recession and increasing corporate debt. Furthermore, it is precisely why the price of gold has moved recently in tandem with equity valuations (see the chart below) – both markets were supported by negative real interest rates.

In other words, investors downplay any risks and instead focus on the current generous liquidity conditions, supported by the central banks. After all, why worry if the Fed is ready to inject liquidity at the first sign of serious problems? But this perverted dynamic may not last forever.

Now, how will the above impact the gold market? Well, the lofty equity valuations may be justified. The coronavirus crisis was tech-friendly, and markets may be right by being optimistic about the vaccine and the eventual triumph over the pandemic.

However, what goes up can also come down, especially if we don’t witness a broad-based, sustainable recovery. The current elevated valuations may result, at least to some extent – from government support and the Fed’s dovish monetary policy, which may end someday. Therefore, the stock market crash (or correction) does not have to be supportive for gold prices at all. If the equity valuations go down because Biden becomes the POTUS and he hikes the corporate tax rates, then yes, gold can act as a safe-haven asset and shine. But, if the stock market bleeds because Powell hikes the interest rates, then gold would suffer too (unless the Fed turns hawkish because of the accelerating inflation).

Therefore, yes, there might be a disconnect between the stock market and the real economy. Of course, the stock market may correct to become better aligned with the economic fundamentals, but precious metals investors should be careful what they wish for, because they just might get it. The correction does not have to support the gold prices, if it’s triggered by the normalization of the monetary policy.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the November Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will the Second Wave of Corona Boost Gold?

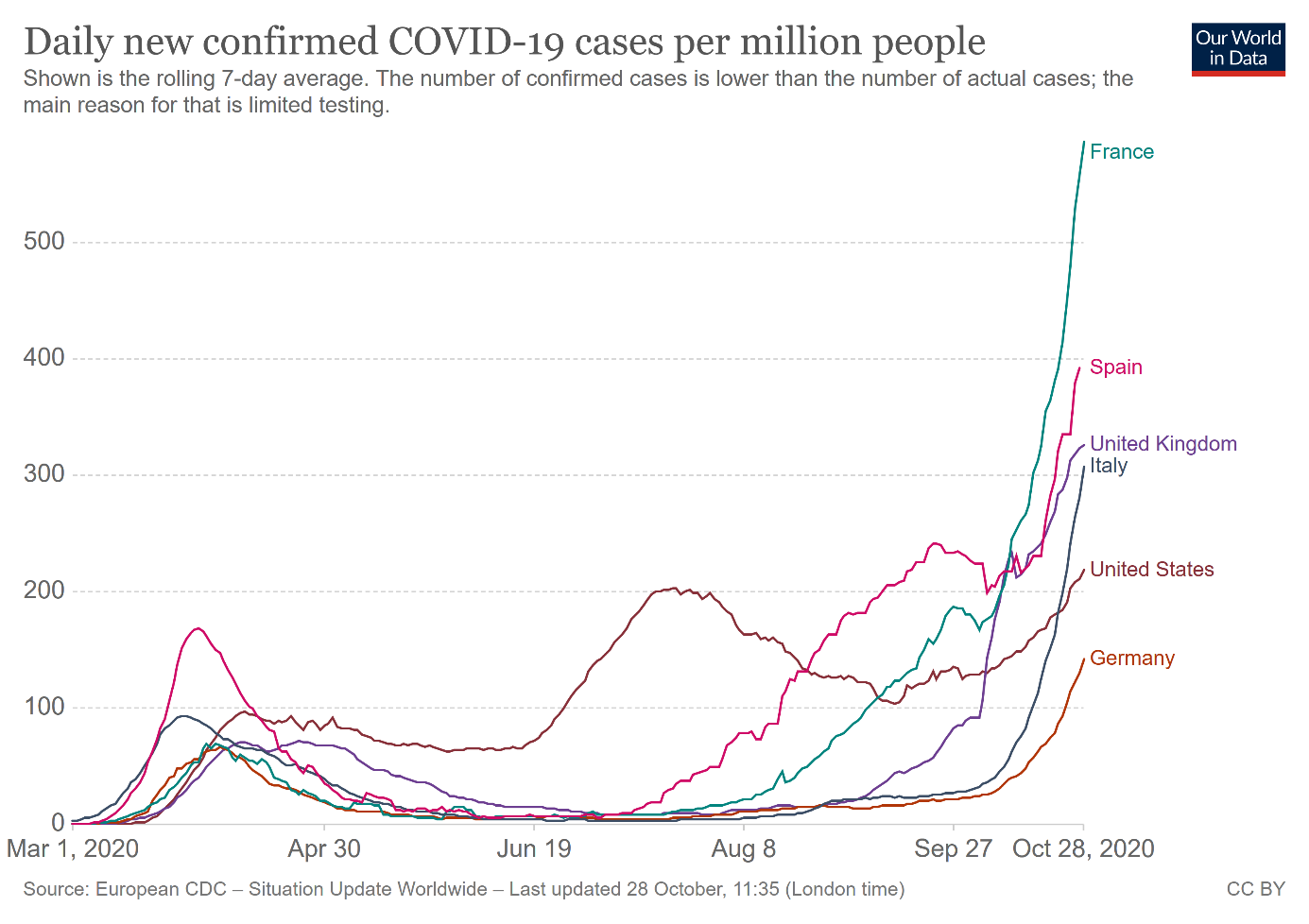

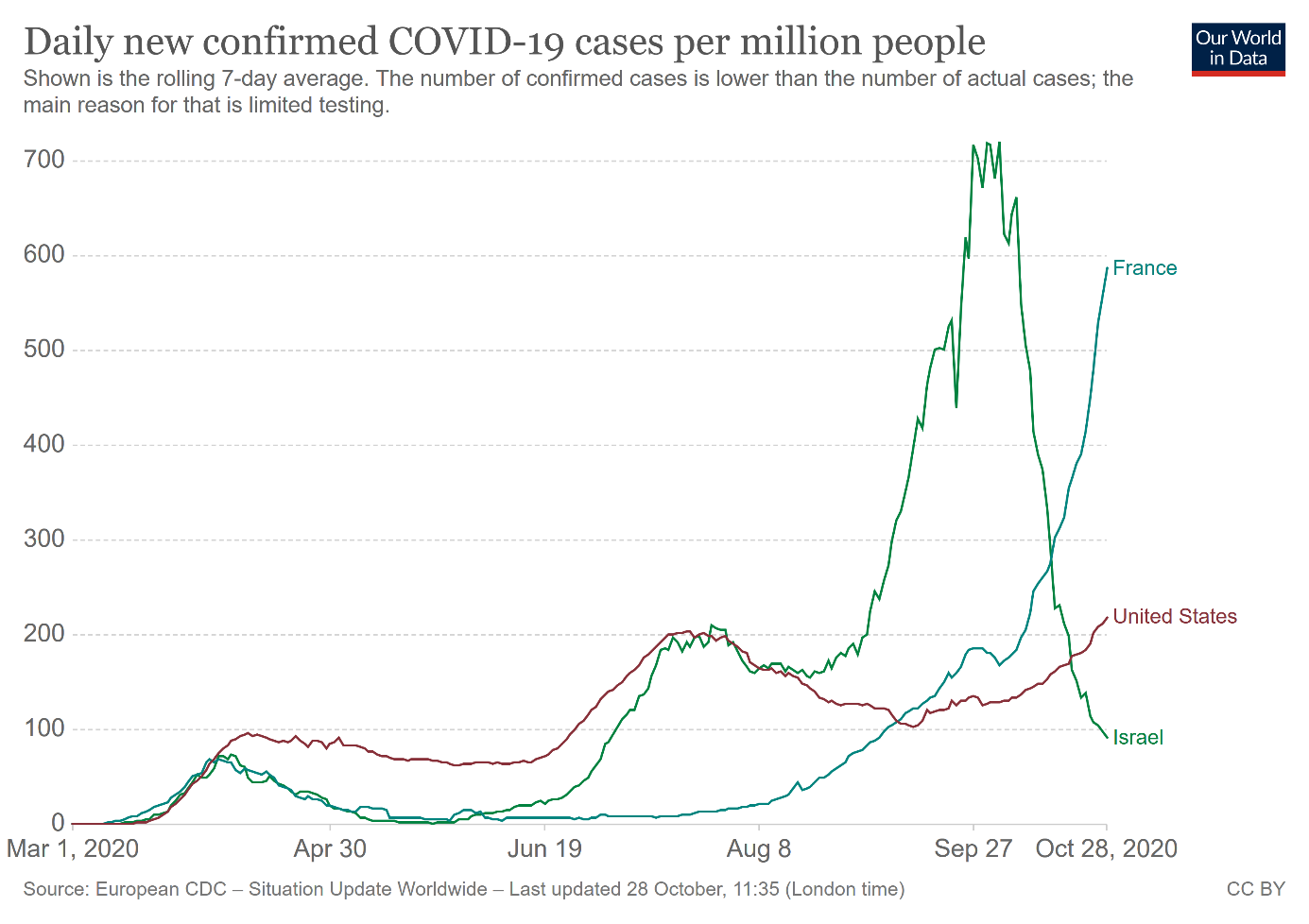

November 6, 2020, 11:03 AMBrace yourselves, winter is coming! This is what Ned Stark in the Game of Thrones told his people to prepare them for the leaner times he saw coming. While one of the biggest threats in GOT were the White Walkers, in our reality, the pandemic is again the greatest danger. As the chart below shows, the second wave of the coronavirus infections is no longer a mere possibility – it’s happening all over the Europe and in the United States (although in the latter country, we could also say about one big wave or three waves). In particular, in France, Italy, Spain, the UK, and in the US, the number of daily new confirmed Covid-19 case per million people has soared much higher than the levels recorded in the spring. And we’ve just entered autumn, with winter yet to arrive…

Naturally, the question arises - Will governments lock the economies down again? Not likely. And why is that, you might wonder. Well, the cynical answer would be that governments are simply broke and they have no funds for supporting the economy during the next lockdown. The pundits call for fresh stimulus in a response to the spring’s Great Lockdown, so just think how much the government spending and the public debt would have to rise to sustain the economy during the Second Lockdown. It would simply be too much of a cost. After all, when you stop the economy, then the economy is, well, stopped. Without a functionable economy, the social fabric gets destroyed and, after some time, the civilization collapses.

However, there are also less cynical reasons why the lockdown is less likely now, despite the fact that the number of daily infections is higher than in the spring. Half a year ago, the governments and healthcare systems were awfully unprepared to handle the epidemic. From the very beginning, the lockdown was stupid and sub-optimal response – but it could be the only viable solution for the Western governments which neither had implemented procedures for social tracing (like in Asian countries), nor managed to conduct efficient and quick testing, nor secured the sufficient number of masks, respirators, disinfectants, hospital beds, etc.

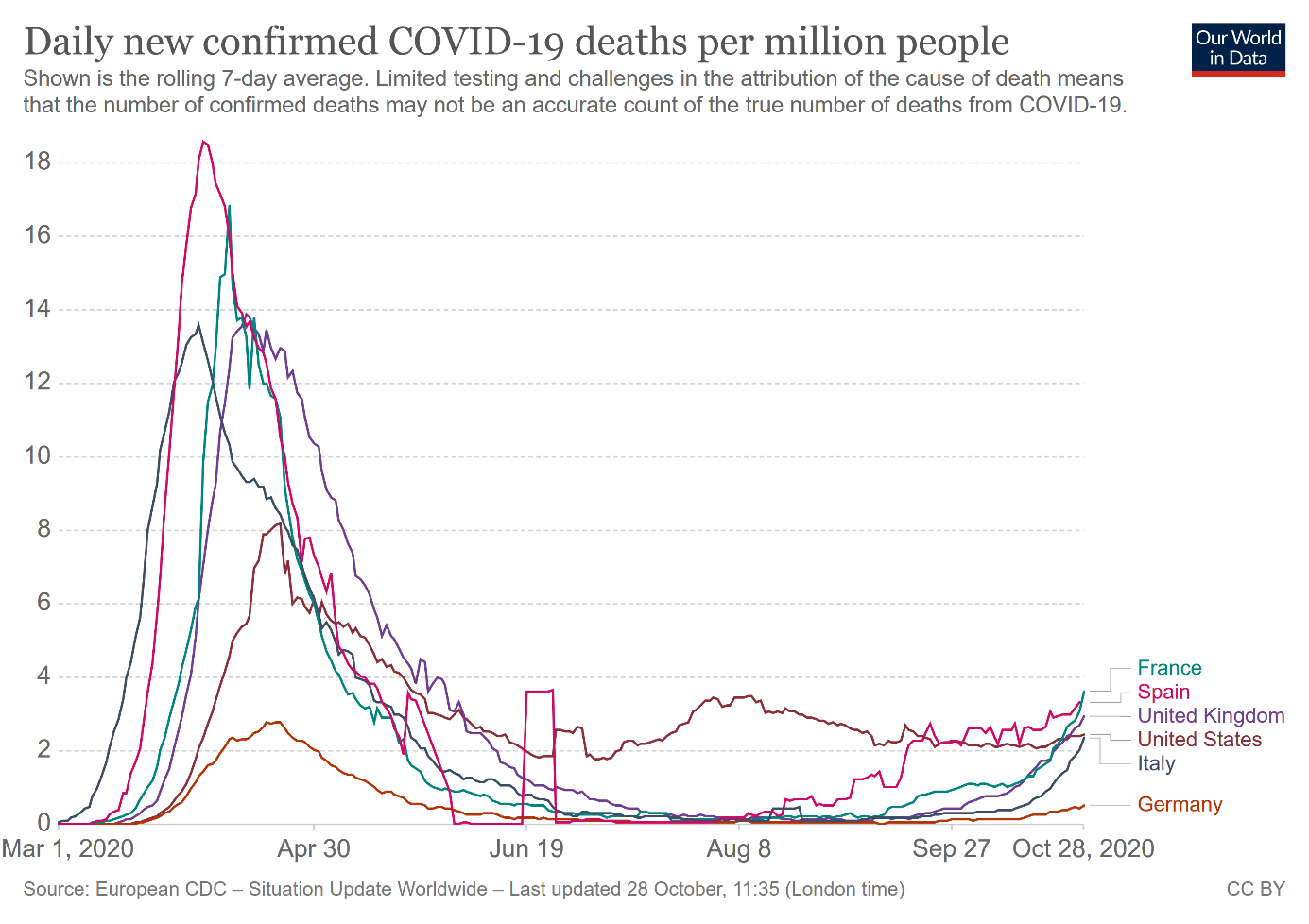

Currently, the situation is better and the sanitary and healthcare systems are better prepared to handle the epidemic. Indeed, as you can see, despite soaring number of cases, the case fatality rates and the number of deaths due to Covid-19 are significantly lower than in the spring.

However, if the risk of a healthcare system collapse increases significantly, under the public’s pressure, the governments could be forced to reintroduce a lockdown (although it may not be as strict as the first one).

This is what the Israeli’s government did in September when the pandemic spiralled out of control. As you can see in the chart below, the daily number of Covid-19 cases (rolling 7-day average) reached 700 per million people, more than three times the number in the US. But France is unfortunately approaching this level…

However, Israel’s case shows that the second lockdown wouldn’t be as bad as the first one. So far, we don’t have any hard data about the Israeli economy, but the data from Apple’s devices indicates that people’s mobility fell by around 30 percent after the lockdown was introduced, compared to the 80-percent decline in the spring. Similarly, the major Israeli stock market index (TA-125) plunged about one third half year ago and only (or “only”) ten percent in September. The currency also weakened against the euro, but not above 10 percent as in the spring, but by about 5 percent.

The softer reaction makes sense. In spring, the coronavirus was completely new, and we didn’t know how dangerous it was. As a matter of fact, we still don’t know many things about the new virus, however, we are now more certain about its fatality rate and how to effectively cure the patients and handle the epidemic.

As I wrote in the June edition of the Gold Market Overview:

The second wave does not have to bring similar effects as the first wave. As people have become accustomed to the epidemic, its impact may be weaker (…) generally people react the most to new, unknown threats, so they should react less vividly in the future to coronavirus-related risks, especially that the authorities should be better prepared.