Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal that confirms that the bottom is in.

Welcome to this week's Gold Investment Update. Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

Let’s start with a quick discussion of the fundamental drivers that could affect the precious metals in the coming weeks.

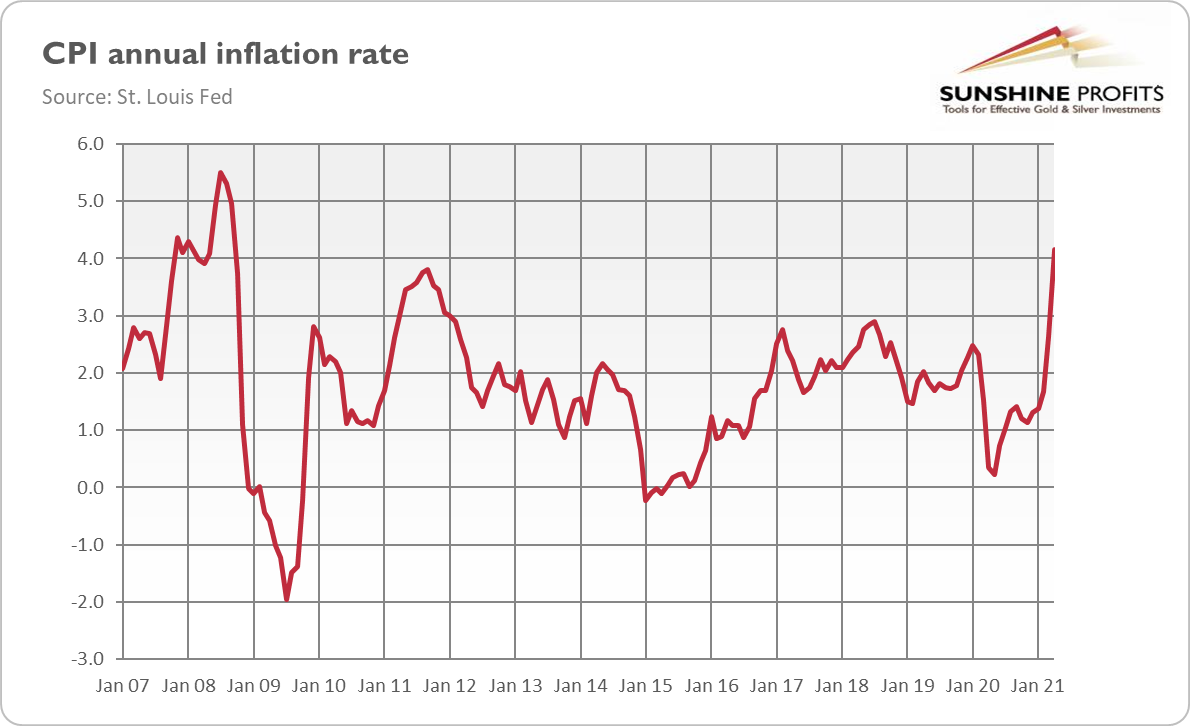

With the Consumer Price Index (CPI) coming in hot on May 12 – surging by 4.2% year-over-year – the strongest print since the Great Recession more than doubled the U.S. Federal Reserve’s (FED) 2.0% target.

Please see below:

Moreover, while the shock resulted in a surge in the U.S. 10-Year Treasury yield and a pullback in gold, a reversal of fortunes occurred later in the week. After a bevy of FED speakers reassured investors that interest rates will remain low for a long time – including FED Vice Chairman Richard Clarida calling April’s print “one data point” and adding that “the economy remains a long way from our goals” – the FED’s confidence game is extremely supportive of the yellow metal.

Moreover, because gold is a proven long-term hedge against inflation, lower real interest rates and a weaker U.S. dollar are extremely bullish. Therefore, the FED had the yellow metal shine once again.

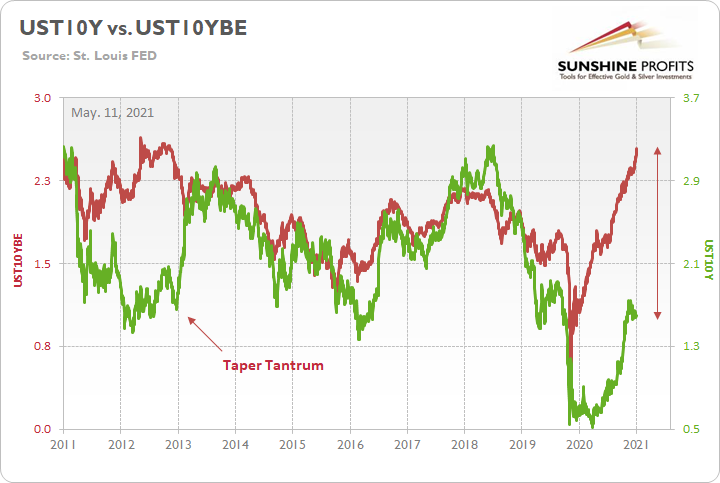

However, it’s important to remember that we’ve been down this road before. With the U.S. 10-Year Treasury yield demonstrating its largest-ever divergence from the U.S. 10-Year breakeven inflation rate, a spike in the former could cause gold’s house of cards to come crashing down.

To explain, I wrote on May 11:

The green line above tracks the U.S. 10-Year Treasury yield, while the red line above tracks the U.S. 10-Year breakeven inflation rate. If you analyze the left side of the chart, you can see that when the bond market finally snapped in 2013, the U.S. 10-Year Treasury yield’s surge was fast and furious. More importantly, though, if you analyze the right side of the chart, you can see that today’s gap makes 2013 look like an appetizer. As a result, with material divergences often reversing in violent fashion, it’s only a matter of time until the next earthquake erupts.

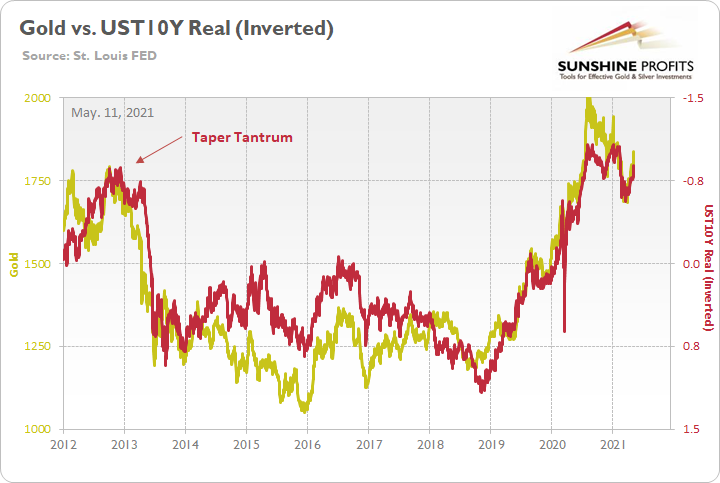

Moreover, once the event unfolds, the impact will severely shake the foundation of the PMs. Case in point: with gold moving inversely of the U.S. 10-Year real yield, major explosions in the bond market often leaves the yellow metal buried under the rubble.

Please see below:

To explain, the gold line above tracks the London Bullion Market Association (LBMA) Gold Price, while the red line above tracks the inverted U.S. 10-Year real yield. For context, inverted means that the latter’s scale is flipped upside down and that a rising red line represents a falling U.S. 10-Year real yield, while a falling red line represents a rising U.S. 10-Year real yield.

If you analyze the left side of the chart, you can see that when the U.S. 10-Year Treasury yield began its move to reconnect with the U.S. 10-Year breakeven inflation rate in 2013 (taper tantrum), the U.S. 10-Year real yield surged (depicted by the red line moving sharply lower). More importantly, though, amidst the chaos, notice how gold plunged by more than $500 in less than six months? Thus, while the yellow metal may seem like it’s on solid footing, once another tremor from the bond market strikes, gold will suffer from severe aftershock.

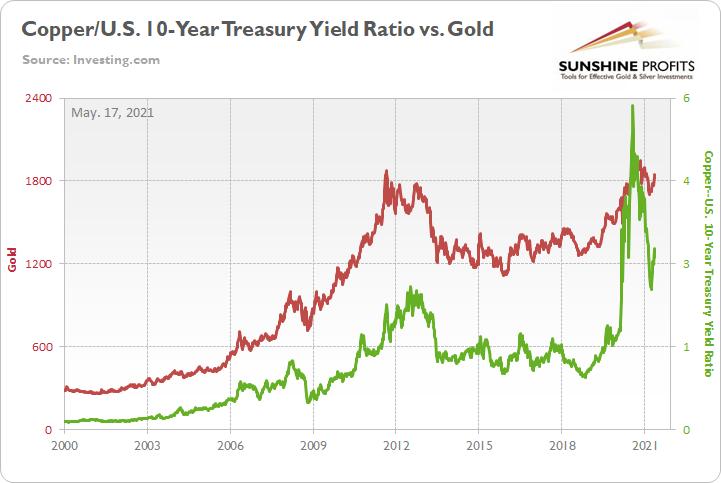

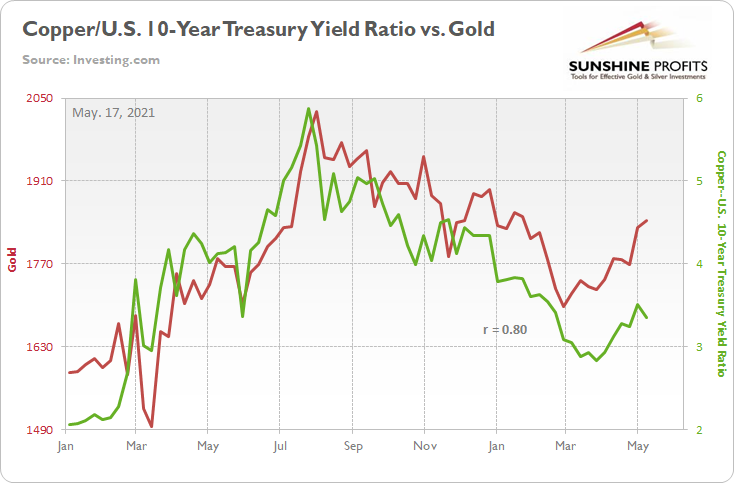

Likewise, over the medium-to-long-term, the copper/U.S. 10-Year Treasury yield ratio is a leading indicator of gold’s future behavior.

I wrote previously:

When the copper/U.S. 10-Year Treasury yield ratio is rising (meaning that copper prices are rising at a faster pace than the U.S. 10-Year Treasury yield), it usually results in higher gold prices. Conversely, when the copper/U.S. 10-Year Treasury yield ratio is falling (meaning that the U.S. 10-Year Treasury yield is rising at a faster pace than copper prices), it usually results in lower gold prices.

If you analyze the chart below, you can see the close connection:

Moreover, with the ratio declining by 5.34% last week and gold rallying by 0.65%, further downward pressure on the former should eventually elicit a similar response from the latter.

Please see below:

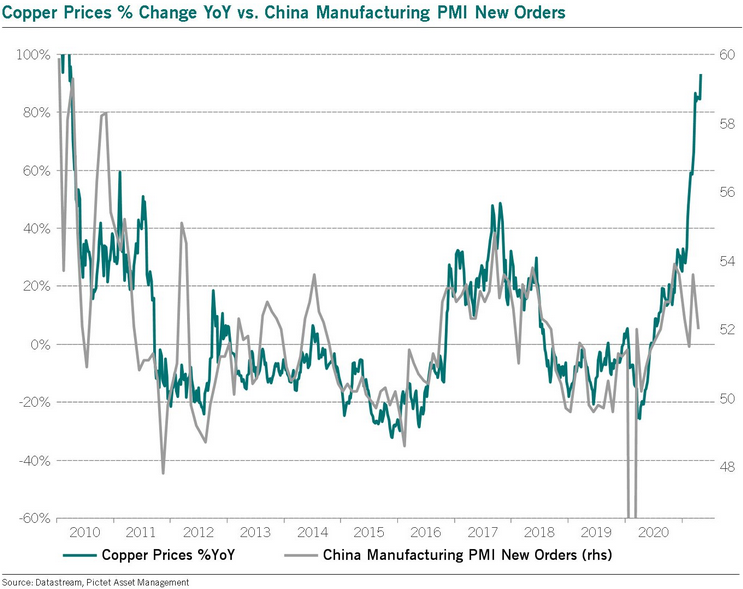

To that point, I mentioned last week that with China’s manufacturing PMI (new orders) beginning to roll over, copper’s recent momentum could be ripe for a reversal. And after a 1.98% decline last week, continued weakness in the bronze metal could usher the copper/U.S. 10-Year Treasury yield ratio even lower.

To explain, the blue line above tracks the year-over-year (YoY) percentage change in copper, while the gray line above tracks China’s manufacturing PMI (new orders). If you analyze the right side of the chart, you can see that investors have priced in the highest Chinese demand in more than 10 years. Conversely, with the gray line signaling extreme overconfidence, a reconnect could weigh heavily on gold in the coming weeks.

The bottom line?

With the copper/U.S. 10-Year Treasury yield ratio highly correlated with the yellow metal, copper’s rocket ship has helped propel gold higher in recent weeks. However, if momentum sputters and the enterprise comes back down to earth, gold will likely suffer a hard landing.

On the flip side, if we extend our time horizon, there are plenty of fundamental reasons why gold is likely to soar in the coming years. However, even the most profound bull markets don’t move up in a straight line, and corrections are inevitable.

As it relates to the precious metals, a significant correction (medium-term downtrend) is already underway. However, the pain is not over, and a severe climax likely awaits.

For context, potential triggers are not always noticeable, and the PMs may collapse on their own or as a result of some random trigger that normally wouldn’t cause any major action. However, a trigger will speed things up, and that’s where the S&P 500 comes in:

S&P 500 (SPX) Signals

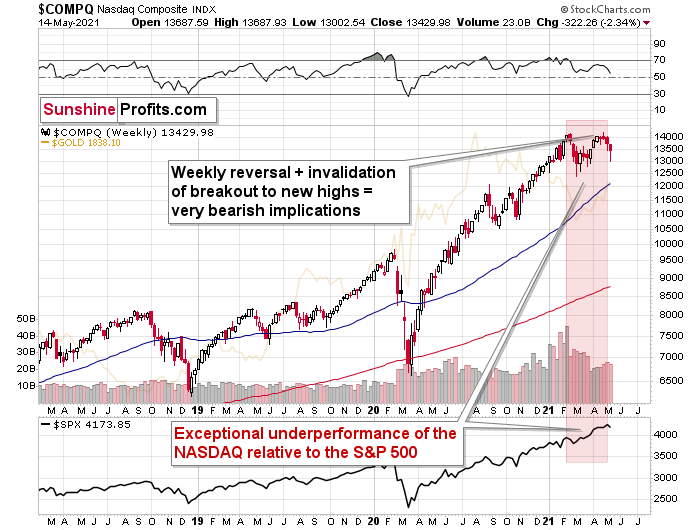

With the NASDAQ Composite suffering from severe underperformance, not only did the tech-heavy index decline by another 2.34% last week, but the implications of its failed attempt at breaking to new highs and its ominous shooting star remain intact. For context, a shooting star candle signals a bearish reversal when formed during an uptrend.

Please see below:

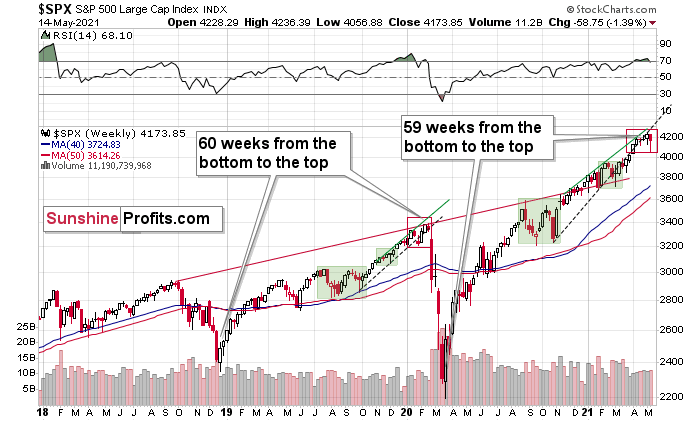

As for the S&P 500, the U.S. equity benchmark’s 2018-2020 analogue has become even more valid. With the timeframe of its trough-to-peak rally from 2018-2020 mirroring the length of its current revival, a significant reversal could be forthcoming.

Please see below:

To explain, I wrote on May 11:

The markets are self-similar (which is another way of saying that they have a fractal nature), which generally means that while the history tends to rhyme, it also tends to rhyme in similar shapes of alike or various sizes.

For example, the rally from 2018–2020 seems very similar to the rally from 2020 to the present. Both rallies started after a sharp decline, and the first notable correction took the form of back-and-forth trading around the previous high. I marked those situations with big rectangles.

Then the rally continued with relatively small week-to-week volatility. I created rising support lines based on the final low of the broad short-term consolidation and the first notable short-term bottom.

This line was broken, and some back-and-forth trading followed, but it was only about half of the previous correction in terms of price and time.

Then, we saw a sharp rally that then leveled off. And that was the top. The thing that confirmed the top was the visible breakdown below the rising support line right after stocks invalidated a tiny breakout to new highs. That’s what happened in February 2020, and that’s what happened this month.

“Time is more important than price; when the time comes, the price will reverse”. Both rallies took an almost identical amount of time: 60 weeks vs. 59 weeks. This is particularly bearish when one takes into account the fact that back in 2020 the rally ended when the weekly RSI moved back below 70 – and we saw the same thing last week.

Likewise, with the NASDAQ Composite looking increasingly fragile and several speculative IPOs and SPACs already being sent to slaughter, the medium-term outlook for the S&P 500 remains profoundly bearish. For context, the six largest companies in the NASDAQ Composite (Apple, Microsoft, Amazon, Tesla, Facebook and Alphabet) are also the six largest companies in the S&P 500. Thus, the latter is unlikely to escape a technology tirade.

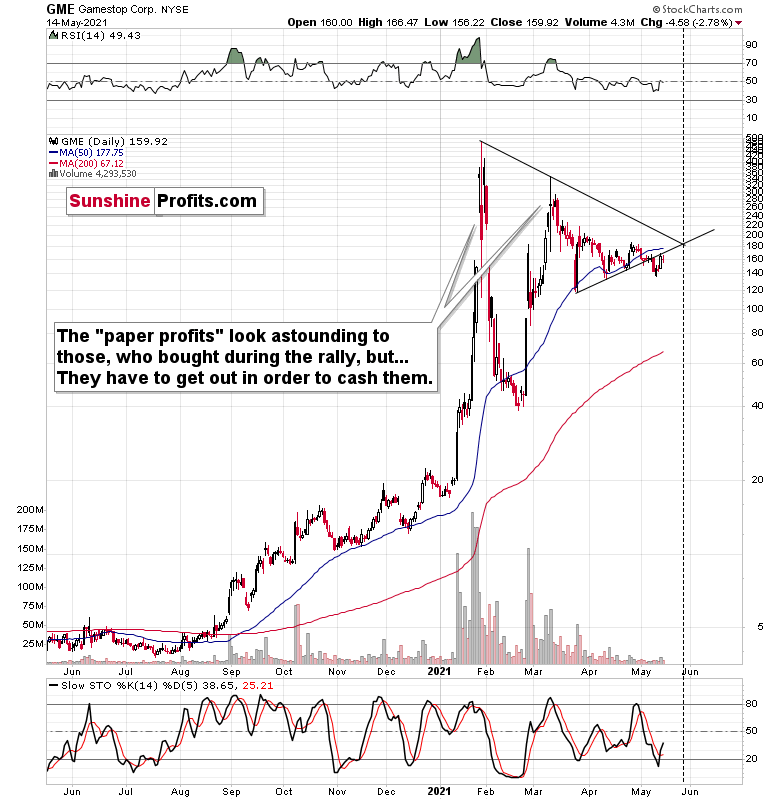

Furthermore, with GameStop – the head of the speculative snake – breaking below two major support lines (the rising one based on the January and February lows and the lower border of the triangle pattern), major pain could be ahead for those invested in the stock.

To explain, GameStop’s volume has completely evaporated, meaning that new buyers remain few and far between. Moreover, with GameStop simply one example of many speculative black swans, an unwinding of the excess could have major implications for the general stock market. The bottom line? With the S&P 500’s May 13/14 relief rallies that didn’t even take the GME back above its rising support line, the next few months could be extremely unkind to overleveraged equity investors.

More importantly, though, the S&P 500’s medium-term outlook puts the precious metals in a precarious position. I’ve mentioned on several occasions that the PMs tend to bottom approximately three months after the general stock market tops. And while the exact date of the S&P 500’s precipice remains unclear, the PMs should suffer three months (or so) of bearish price action once the S&P 500 meets its maker.

Furthermore, the U.S. equity benchmark is now entering a much tougher macroeconomic environment. With the Bank of Canada (BOC) and the Bank of England (BOE) already reducing their asset purchases, the U.S. Federal Reserve (FED) is likely next in line. And with liquidity the main driver of the S&P 500’s strong performance, investors are unlikely to celebrate the dry season.

Keep in mind though: a decline in stocks is not required for the PMs to decline. But a break in the former could easily trigger a sell-off in the latter, and if history decides to rhyme again, silver and the miners will be the hardest hit.

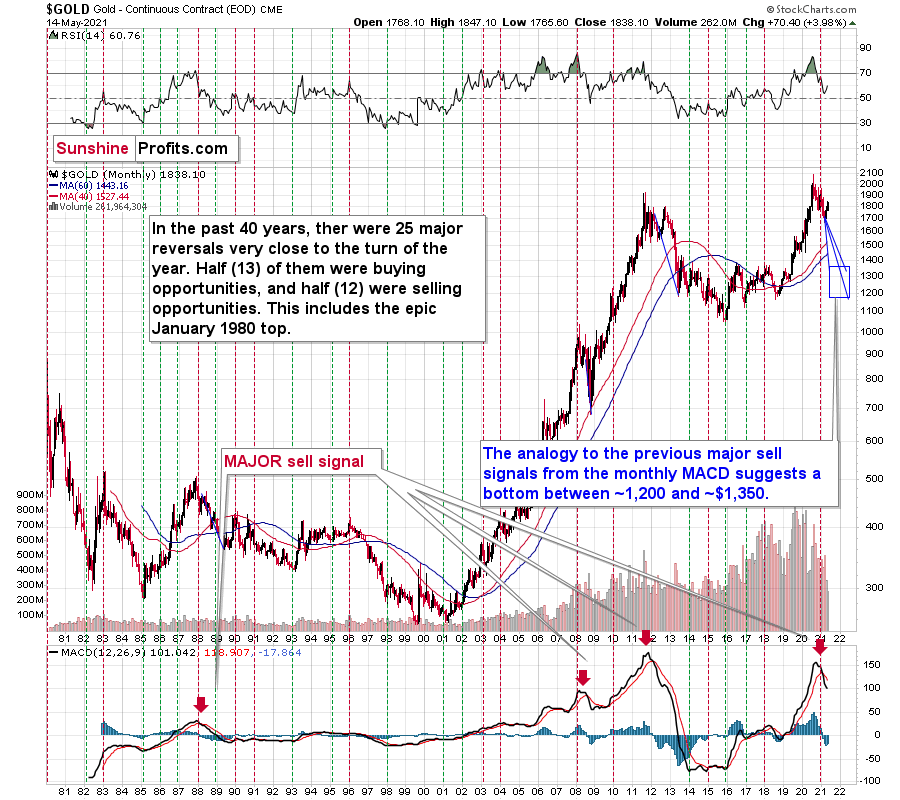

Very Long-term MACD Sell Signal for Gold

While short-term price movements often garner the most attention, it’s important to remember that gold’s long-term downtrend remains intact. Case in point: despite the yellow metal’s recent rally making plenty of noise, the MACD indicator has been completely silent. Still, showing a clear sell-signal on the right side of the chart below (at the bottom), the yellow metal’s superficial strength is reminiscent of the second half of 2012.

If you analyze the middle-right area of the chart below, you can see that the MACD indicator sounded the alarm in 2012. And while investors ignored the warning and gold moved higher, a profound plunge followed in 2013. Moreover, while the MACD indicator’s sell-signal was visible throughout gold’s entire journey – despite several ebbs and flows in the price action – the narrowing distance between the black and red lines actually preceded gold’s plunge. Thus, with gold’s swan song beginning to play at nearly the same level in 2013, the yellow metal’s recent strength is likely only the intermission.

The above-mentioned narrowing distance between the MACD lines can be seen clearly seen through the blue bars hovering around the 0 level on the indicator part of the chart. We now see the current blue bar move toward 0. We saw the same thing in the second half of 2012, which is when gold rallied for the last time before the huge slide.

Remember the huge gap between the U.S. 10-Year Treasury yield and the U.S. 10-Year breakeven inflation rate? The situation in the very long-term MACD indicator is yet another confirmation that what we saw recently is similar to what we saw before the huge 2012 – 2013 slide. We get the same confirmation from the gold to bonds ratio, and I’ll move to that a bit later.

For more context, I wrote previously:

With February’s monthly close the last piece of the puzzle, the MACD indicator’s sell-signal is now perfectly clear. If you analyze the chart below (at the bottom right), you can see that the MACD line has crossed the signal line from above – a development that preceded significant drawdowns in 2008 and 2011.

Based on gold’s previous performance after the major sell signals from the MACD indicator, one could now expect gold to bottom in the ~$1,200 to ~1,350 range. Given the price moves that we witnessed in 1988, 2008 and 2011, historical precedent implies gold forming a bottom in this range. However, due to the competing impact of several different variables, it’s possible that the yellow metal could receive the key support at a higher level.

Only a shade below the 2011 high, today’s MACD reading is still the second-highest reading in the last 40 years. More importantly though, if you analyze the chart below (the red arrows at the bottom), the last four times the black line cut through the red line from above, a significant drawdown occurred.

Also ominous is that the magnitude of the drawdowns in price tend to coincide with the magnitude of the preceding upswings in MACD. And with today’s reading only surpassed by 2011, a climactic move to the $1,250/$1,450 range isn’t out of the question for gold. The above is based on how low gold had previously declined after a similarly important sell signal from the MACD

Now, the month is not over yet, so one might say that it’s too early to consider the sell signal that’s based on monthly closing prices, but it seems that given the level that the MACD had previously reached and the shape of the top in the black line, it makes the situation so similar to 2011/2012 that the sell signal itself is just a cherry on the bearish analytical cake.

Considering the reliability of the MACD indicator a sell signal for major declines, the reading also implies that gold’s downtrend could last longer and be more severe than originally thought. As a result, $1,500 remains the most likely outcome, with $1,350 still in the cards.

The USD Index (USDX)

It’s easy to get carried away by the day-to-day price action, and it’s even easier to feel the emotions that other market participants are feeling while looking at the same short-term price action. Right now, it’s tempting to be bullish on gold. It’s “easy” to be bullish on gold while looking at what happened in the last 1.5 months. But what’s easy is rarely profitable in the long run.

“Easy choices – hard life. Hard choices – easy life” – Jerzy Gregorek

Let’s get beyond the day-to-day price swings. The Fed has been keeping the interest rates at ultra-low levels for many months, and it has just pledged to keep them low for a long time. The world is enduring the pandemic, and the amount of money that entered the system is truly astonishing. The savings available to investors skyrocketed. The USD Index has been beaten down from over 100 to about 90. And yet, gold is not at new highs. In fact, despite the 2020 attempt to rally above its 2011 high, gold’s price collapsed, and it invalidated the breakout above these all-important highs. It’s now trading just a few tens of dollars higher than it had been trading in 2013, right before the biggest slide of the recent years.

Something doesn’t add up with regard to gold’s bullish outlook, does it?

Exactly. Gold is not yet ready to soar, and if it wasn’t for the pandemic-based events and everything connected to them, it most likely wouldn’t have rallied to, let alone above its 2011 highs before declining profoundly. And what happens if a market is practically forced to rally, but it’s not really ready to do so? Well, it rallies… For a while. Or for a bit longer. But eventually, it slides once again. It does what it was supposed to do anyway - the only thing that changes is the time. Everything gets delayed, and the ultimate downside targets could increase, but overall, the big slide is not avoided.

Let’s say that again. Not avoided, but delayed.

And this is where we are right now. In the following part of the analysis, I’m going to show you how the situation in the USD Index is currently impacting the precious metals market, and how it’s likely to impact it in the following weeks and months.

Riding investors’ emotional roller coaster, the love-hate relationship between financial markets and the USD Index is quite absurd. However, with alternating emotions often changing like the seasons, the greenback’s latest stint in investors’ doghouse could be nearing its end. Case in point: with the most speculative names in the stock market enduring a springtime massacre, beneath the surface laughter has already turned into tears. And while gold, silver and mining stocks have been buoyed by the intense emotional high that’s only visible on the surface, it’s only a matter of time before the veneer is lifted.

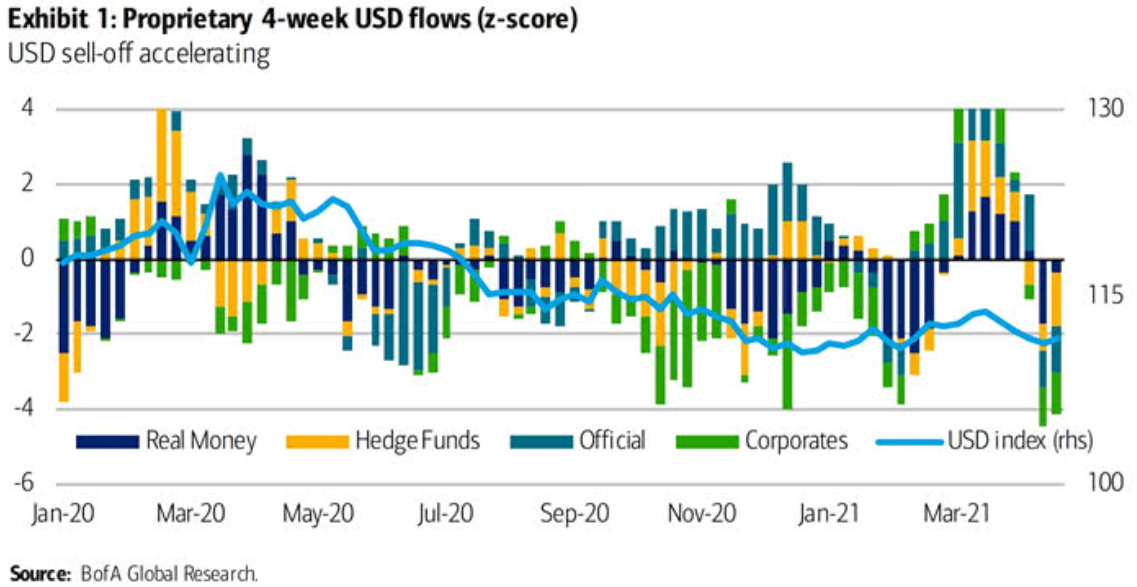

To that point, while I won’t romanticize the USD Index’s recent underperformance, it’s important to remember that extreme pessimism is often the spark that lights the USD Index’s fire.

Please see below:

To explain, the bars above track various market participants’ four-week allocations to the U.S. dollar, while the horizontal light blue line above tracks the USD Index. If you analyze the right side of the chart, you can see that fund flows have fallen off of a cliff in recent weeks. However, if you analyze the behavior of the USD Index near Jan-20, Jan-21 and Mar-21, you can see that extremely pessimistic fund flows are often followed by short-term rallies in the USD Index. As a result, with the latest readings already breaching -4 (using the scale on the left side of the chart), USD-Index bears have likely already offloaded their positions.

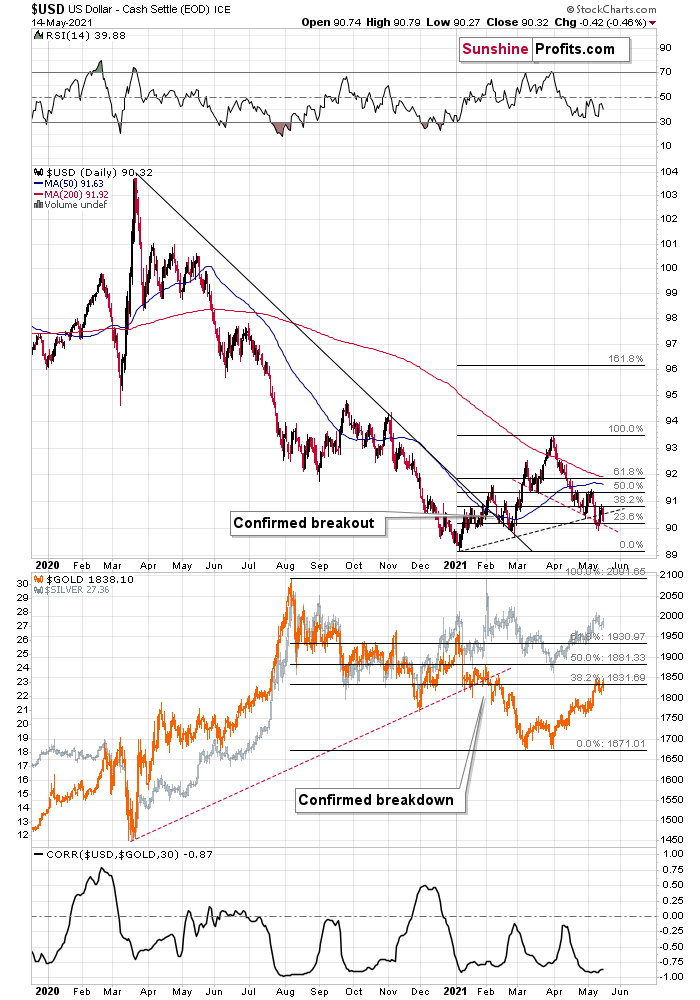

What’s more, not only did the USD Index end last week up by 0.10%, but the greenback invalidated the breakdown below its head & shoulders pattern – which is quite bullish – and also invalidated the breakdown below its rising dashed support line (the black line below). Moreover, while the greenback fell below the latter again on May 14, the short-term weakness is far from a game-changer as the breakdown is not confirmed.

Please see below:

On top of that, with the USD Index hopping in the time machine and setting the dial on 2016, a similar pattern could be emerging. To explain, I wrote on May 11:

While the self-similarity to 2018 in the USD Index is not as clear as it used to be (it did guide the USDX for many weeks, though), there is also another self-similar pattern that seems more applicable now. One of my subscribers noticed that and decided to share it with us (thanks, Maciej!).

Here’s the quote, the chart, and my reply:

Thank you very much for your comprehensive daily Gold Trading Reports that I am gladly admitting I enjoy a lot. While I was analyzing recent USD performance, (DX) I have spotted one pattern that I would like to validate with you if you see any relevance of it. I have noticed the DX Index performing exactly in the same manner in a time frame between Jan. 1, 2021 and now as the one that started in May 2016 and continued towards Aug. 16. The interesting part is not only that the patterns are almost identical, but also their temporary peeks and bottoms are spotting in the same points. Additionally, 50 daily MA line is almost copied in. Also, 200 MA location versus 50 MA is almost identical too. If the patterns continue to copy themselves in the way they did during the last 4 months, we can expect USD to go sideways in May (and dropping to the area of 90,500 within the next 3 days) and then start growing in June… which in general would be in line with your analysis too.

Please note the below indices comparison (the lower represents the period between May-Dec 2016 and higher Jan – May 2021). I am very much interested in your opinion.

Thank you in advance.

And here’s what I wrote in reply:

Thanks, I think that’s an excellent observation! I read it only today (Monday), so I see that the bearish note for the immediate term was already realized more or less in tune with the self-similar pattern. The USDX moved a bit lower, but it doesn’t change that much. The key detail here would be that the USDX is unlikely to decline much lower, and instead, it’s likely to start a massive rally in the next several months - that would be in perfect tune with my other charts/points.

I wouldn’t bet on the patterns being identical in the very near term, though, just like the late June 2016 and early March 2021 weren’t that similar.

As soon as the USD Index rallies back above the rising support line, the analogy to 2016 will be quite clear once again –the implications will be even more bullish for the USDX and bearish for the precious metals market for the next several months.

Please note that back in 2016, there were several re-tests of the rising support line and tiny breakdowns below it before the USD Index rallied. Consequently, the current short-term move lower is not really concerning, and forecasting gold at much higher levels because of it might be misleading. I wouldn’t bet on the silver bullish forecast either. The white metal might outperform at the very end of the rally, but it has already done so recently on a very short-term basis, so we don’t have to see this signal. And given the current situation in the general stock market – which might have already topped – silver and mining stocks might not be able to show strength relative to gold at all.

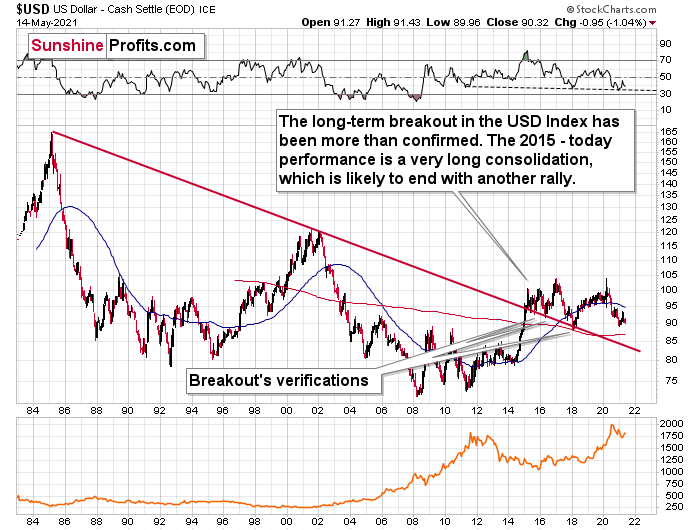

If that wasn’t enough, the USD Index’s long-term breakout remains intact. And when analyzing from a bird’s-eye view, the recent weakness is largely inconsequential.

Please see below:

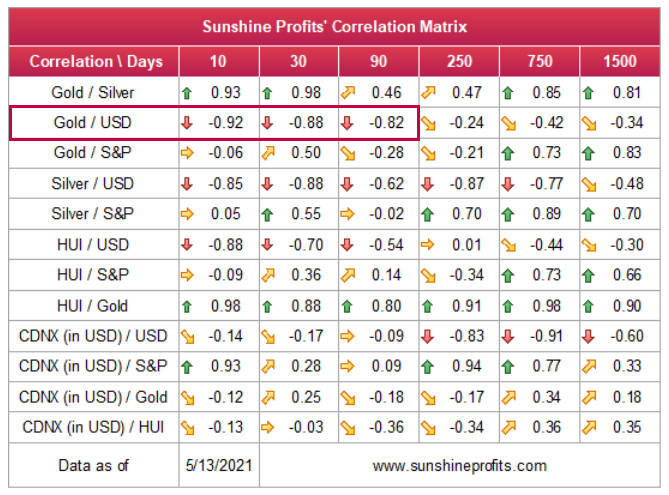

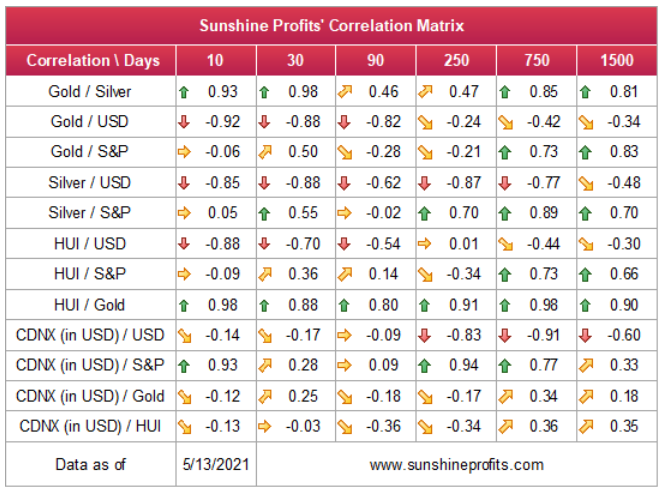

Moreover, please note that the correlation between the USD Index and gold is now strongly negative (-0.92 over the last 10 days) and it’s been the case for several weeks now. The same thing happened in early January 2021 and in late July – August 2020. These were major tops in gold.

The bottom line?

After regaining its composure, ~94.5 is likely the USD Index’s first stop. In the months to follow, the USDX will likely exceed 100 at some point over the medium or long term.

Keep in mind though: we’re not bullish on the greenback because of the U.S.’ absolute outperformance. It’s because the region is doing (and likely to do) better than the Eurozone and Japan, and it’s this relative outperformance that matters, not the strength of just one single country or monetary area. After all, the USD Index is a weighted average of currency exchange rates and the latter move on a relative basis.

In conclusion, with investors and the USD Index likely headed toward reconciliation, the greenback’s medium-term prospects remain robust. With macroeconomic headwinds aligning with technical catalysts, investors’ risk-on inertia is already showing cracks in its foundation. And with the USD Index considered a safe-haven currency, a reversal in sentiment will likely catapult the USD Index back into the spotlight. Moreover, with gold, silver and mining stocks often moving inversely to the U.S. dollar, the mood music will likely turn somber across the precious metals market. The bottom line? With the metals’ mettle likely to crack under the forthcoming pressure, their outlook remains profoundly bearish over the next few months.

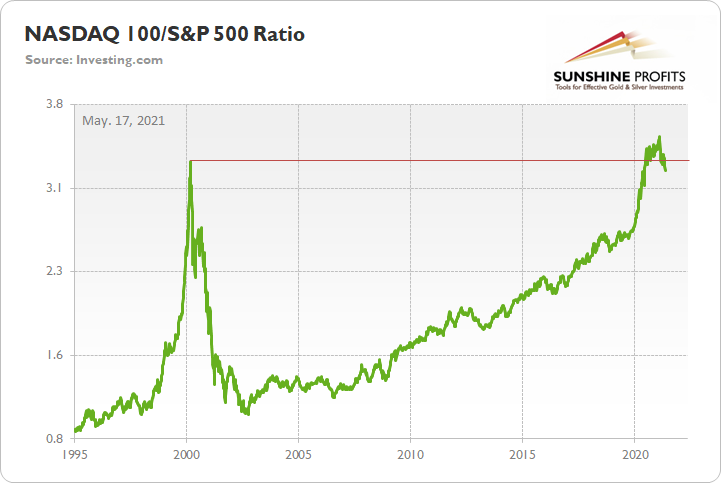

As a secondary catalyst, a material drawdown of the NASDAQ 100 could eventually rattle U.S. equities. And with the NASDAQ 100/S&P 500 ratio already beginning to roll over, a reversion to the mean could light plenty of fireworks across Wall Street.

To that point, given the USDX’s strong negative correlation with the NASDAQ 100, a material reset could propel the greenback back to its March highs. Moreover, following a short-term consolidation, the USDX could even exceed those previous highs.

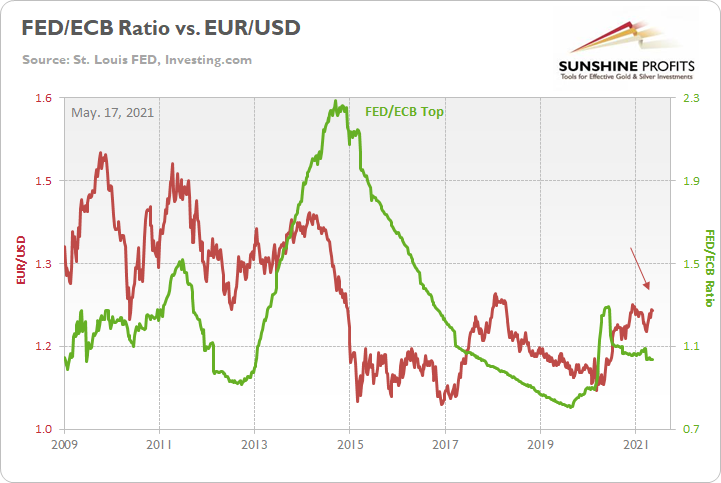

Third, relative outprinting by the European Central Bank (ECB) remains of critical importance. Last week, the FED/ECB ratio was flat, while the EUR/USD declined by 0.19%. However, given that the ratio has declined by more than 19% since May, by nearly 5% over the last seven weeks and is showing a material divergence on the right side of the chart below, the EUR/USD still has some catching up to do.

Please see below:

The key takeaway?

With the ECB injecting more liquidity to support an underperforming Eurozone economy, the FED/ECB ratio, as well as EUR/USD, should move lower over the medium term. More importantly, though, because the EUR/USD accounts for nearly 58% of the movement of the USD Index, EUR/USD pain will be the USDX’s gain.

In addition, the top in the FED/ECB total assets ratio preceded the slide in the EUR/USD less than a decade ago, and it seems to be preceding the next slide as well. If the USD Index was to repeat its 2014-2015 rally from the recent lows, it would rally to 114. This level is much more realistic than most market participants would agree on.

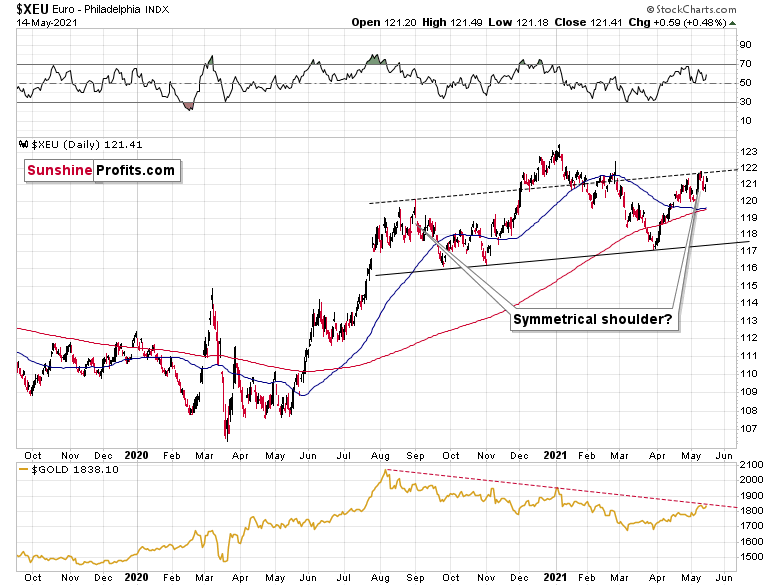

In addition, the Euro Index is in the midst of forming a textbook head & shoulders pattern. If you analyze the right side of the chart below, you can see that the symmetrical pattern has the current rally mirroring the summer of 2020. And while we’re still in the early innings of forming the right shoulder, the completion of the masterpiece could have a profound impact on the PMs.

Please see below:

To explain, gold continues to underperform the euro. If you analyze the bottom half of the chart above, you can see that material upswings in the Euro Index have resulted in diminishing marginal returns for the yellow metal. Thus, a relative weakness is an ominous sign, and if the Euro Index reverses, it could weigh heavily on gold over the medium term.

The Gold Miners

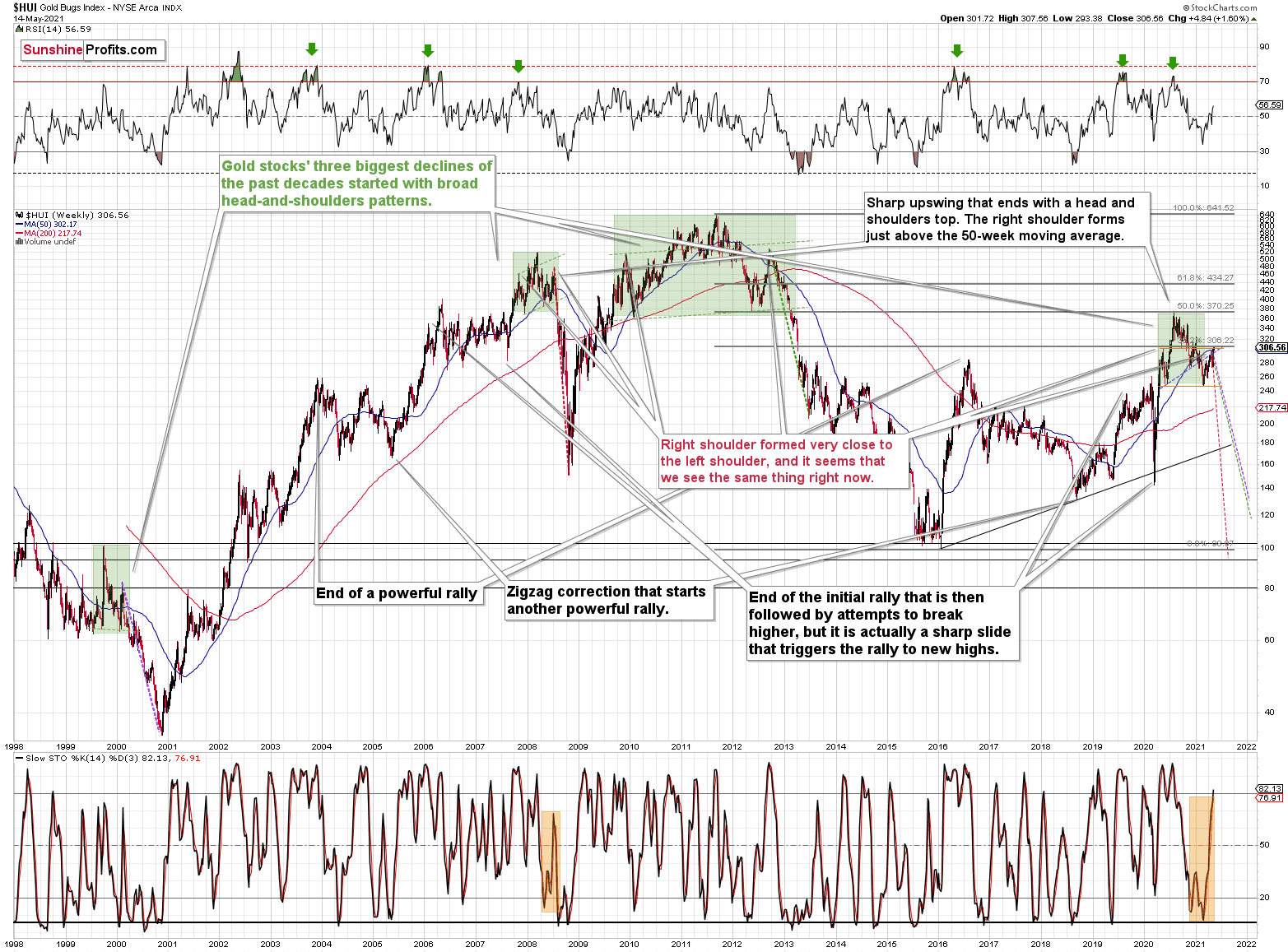

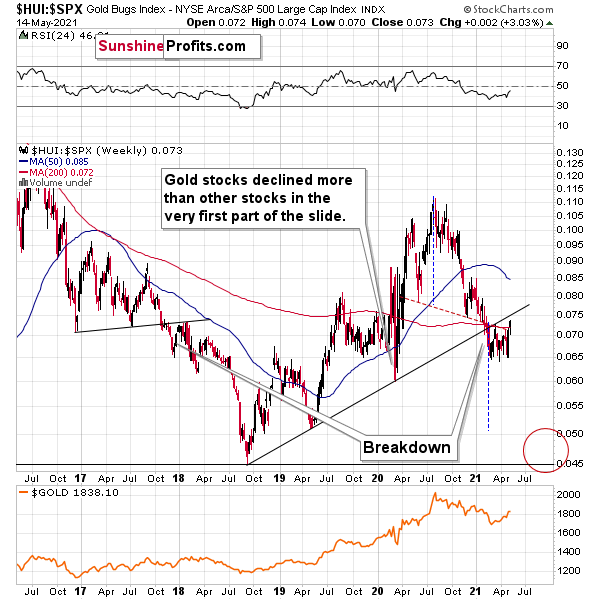

With the HUI Index (a proxy for gold mining stocks) inching higher last week, my initial ~300 target proved to be quite prescient (from the long-term point of view, even 310 is very close to the 300 level). However, with the BUGS’ (after all, HUI is called the Gold Bugs Index) broad head & shoulders pattern still on schedule, the index is sending an inauspicious signal.

Please see below:

To explain, I wrote previously:

Note that the 2007 – 2008 and the 2009 – 2012 head and shoulders patterns didn’t have the right shoulders all the way up to the line that was parallel to the line connecting the bottoms. I marked those lines with green in the above-mentioned formations. In the current case, I marked those lines with orange. Now, in both cases, the final top – the right shoulder – formed close to the price where the left shoulder topped. And in early 2020, the left shoulder topped at 303.02.

That’s why I previously wrote that “it wouldn’t be surprising to see a move to about 300 in the HUI Index”. And that’s exactly what we saw. To clarify, one head-and-shoulders pattern – with a rising neckline – was already completed, and one head-and-shoulders pattern – with a horizontal neckline – is being completed, but we’ll have the confirmation once miners break to new yearly lows.

In addition, the recent rally is not a game-changer, but rather a part of a long-term pattern that’s not visible when one focuses on the short-term only.

The thing is that the vast majority of individual investors and – sadly – quite many analysts focus on the trees while forgetting about the forest. During the walk, this might result in getting lost, and the implications are no different in the investment landscape.

From the day-to-day perspective, a weekly – let alone monthly – rally seems like a huge deal. However, once one zooms out and looks at the situation from a broad perspective, it’s clear that:

“What has been will be again, what has been done will be done again; there is nothing new under the sun.” (-Ecclesiastes 1:9)

The rally is very likely the right shoulder of a broad head and shoulders formation. “Very likely” and not “certainly”, because the HUI Index needs to break to new yearly lows in order to complete the pattern – for now, it’s just potential. However, given the situation in the USD Index (i.a. the positions of futures traders as seen in the CoT report, and the technical situation in it), it seems very likely that this formation will indeed be completed. Especially when (not if) the general stock market tumbles.

In addition, three of the biggest declines in the mining stocks (I’m using the HUI Index as a proxy here), all started with broad, multi-month head-and-shoulders patterns. And in all three cases, the size of the decline exceeded the size of the head of the pattern.

Can we see gold stocks as low as we saw them last year? Yes.

Can we see gold stocks even lower than at their 2020 lows? Again, yes.

Of course, it’s far from being a sure bet, but the above chart shows that it’s not irrational to expect these kind of price levels before the final bottom is reached. This means that a $24 target on the GDX ETF is likely conservative.

In addition, mining stocks are currently flirting with two bearish scenarios:

- If things develop as they did in 2000 and 2012-2013, gold stocks are likely to bottom close to their early 2020 high.

- If things develop like in 2008 (which might be the case, given the extremely high participation of the investment public in the stock market and other markets), gold stocks could re-test (or break slightly below) their 2016 low.

I know, I know, this seems too unreal to be true… But wasn’t the same said about silver moving below its 2015 bottom in 2020? And yet, it happened.

Keep in mind though: scenario #2 most likely requires equities to participate. In 2008 and 2020, the sharp drawdowns in the HUI Index coincided with significant drawdowns of the S&P 500. However, with the words ‘all-time high’ becoming commonplace across U.S. equities, the likelihood of a three-peat remains relatively high.

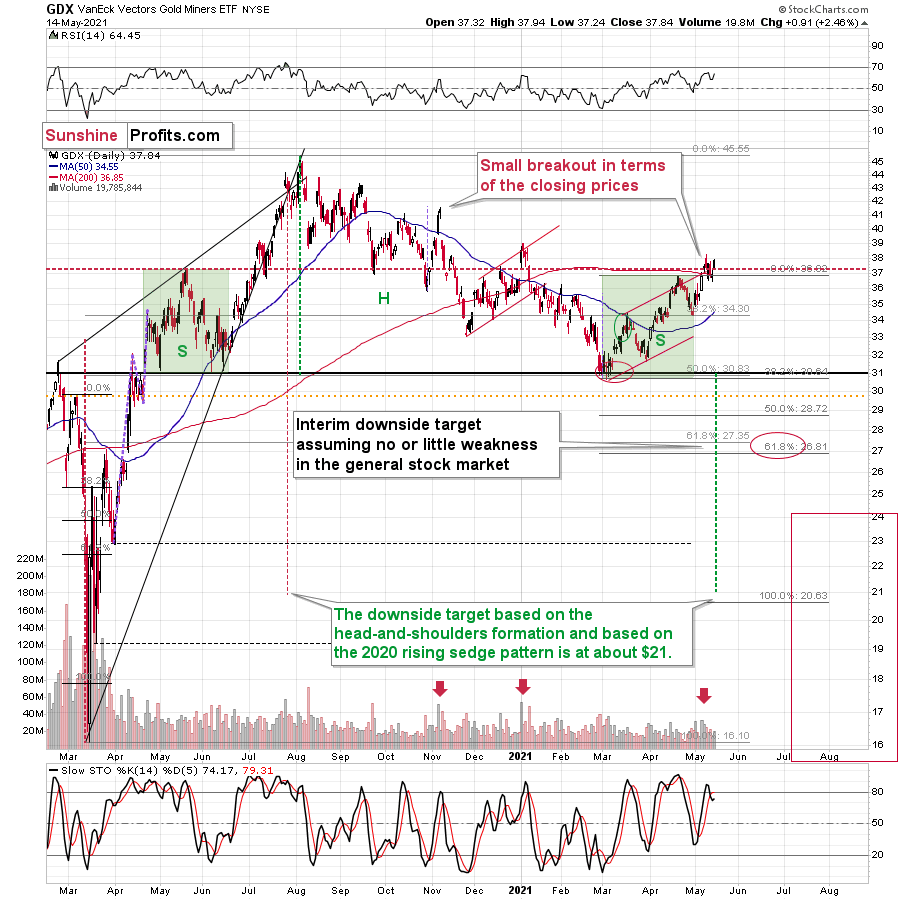

As for the GDX ETF, while the senior miners moved higher last week, the majority of the strength was recorded on May 13/14. And with the late-week optimism occurring on relatively low volume, the relief rally was similar to the bullish trepidation that we witnessed in the general stock market. Moreover, the GDX ETF’s recent rally actually creates symmetry between its left and right shoulders. With May 2020’s peak occurring at nearly the same level, a move lower from here would only enhance the validity of the GDX ETFs head & shoulders pattern.

Likewise, this is the third time that the GDX ETF has poked its head above the upper trendline of its roughly one-and-a-half-month channel. Adding to possible major disappointment, the GDX ETF’s swoon in late 2020/early 2021 occurred precisely after the senior miners delivered their third act. Furthermore, a small breakout without confirmation is akin to a promise from a friend that can’t keep their word. Thus, with the GDX ETF still underperforming gold on a relative basis, it’s important to analyze the recent price action within its proper context.

For more context, I wrote on May 5:

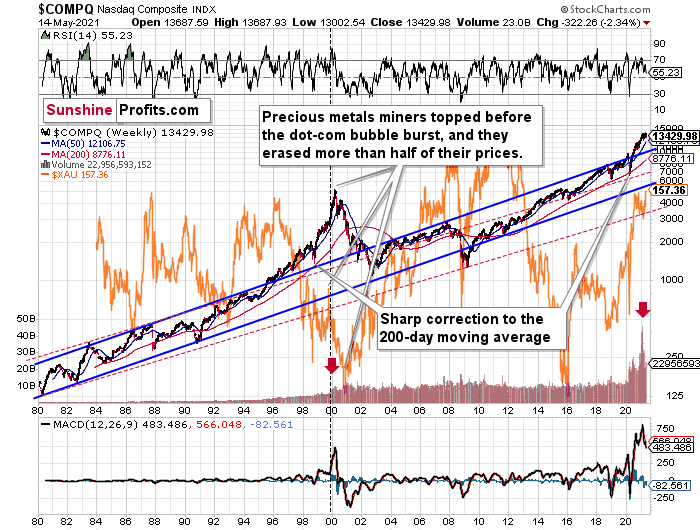

The history might not repeat itself, but it does rhyme, and those who insist on ignoring it are doomed to repeat it. And there’s practically only one situation from more than the past four decades that is similar to what we see right now.

It’s the early 2000s when the tech stock bubble burst. It’s practically the only time when the tech stocks were after a similarly huge rally. It’s also the only time when the weekly MACD soared to so high levels (we already saw the critical sell signal from it). It’s also the only comparable case with regard to the breakout above the rising blue trend channel. The previous move above it was immediately followed by a pullback to the 200-week moving average, and then the final – most volatile – part of the rally started. It ended on significant volume when the MACD flashed the sell signal. Again, we’re already after this point.

The recent attempt to break to new highs that failed seems to have been the final cherry on the bearish cake.

Why should I – the precious metals investor care?

Because of what happened in the XAU Index (a proxy for gold stocks and silver stocks) shortly after the tech stock bubble burst last time.

What happened was that the mining stocks declined for about three months after the NASDAQ topped, and then they formed their final bottom that started the truly epic rally. And just like it was the case over 20 years ago, mining stocks topped several months before the tech stocks.

Mistaking the current situation for the true bottom is something that is likely to make a huge difference in one’s bottom line. After all, the ability to buy something about twice as cheap is practically equal to selling the same thing at twice the price. Or it’s like making money on the same epic upswing twice instead of “just” once.

And why am I writing about “half” and “twice”? Because… I’m being slightly conservative, and I assume that the history is about to rhyme once again as it very often does (despite seemingly different circumstances in the world). The XAU Index declined from its 1999 high of 92.72 to 41.61 – it erased 55.12% of its price.

The most recent medium-term high in the GDX ETF (another proxy for mining stocks) was at about $45. Half of that is $22.5, so a move to this level would be quite in tune with what we saw recently.

And the thing is that based on this week’s slide in the NASDAQ that followed the weekly reversal and the invalidation, it seems that this slide lower has already begun.

“Wait, you said something about three months?”

Yes, that’s approximately how long we had to wait for the final buying opportunity in the mining stocks to present itself based on the stock market top.

The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. Consequently, we might see the next major bottom – and the epic buying opportunity in the mining stocks – about three months after the general stock market tops. The NASDAQ might have already topped, so we’re waiting for the S&P 500 to confirm the change in the trend.

The bottom line?

New lows are likely to complete the GDX ETF’s bearish H&S pattern and set the stage for an even larger medium-term decline. And if the projection proves prescient, medium-term support (or perhaps even the long-term one) will likely emerge at roughly $21.

But why ~$21?

- The target aligns perfectly with the signals from the GDX ETF’s 2020 rising wedge pattern. You can see it in the left part of the above chart. The size of the move that follows a breakout or breakdown from the pattern (breakdown in this case) is likely to be equal (or greater than) the height of the wedge. That’s what the red dashed line marks.

- The target is also confirmed when applying the Fibonacci extension technique. To explain, if we take the magnitude of the GDX ETF’s recent peak-to-trough decline and extrapolate it by multiplying it by the Fibonacci sequence, the output results in a target adjacent to $21. I used the Fibonacci retracement tool to show that in the above chart. Interestingly, the same technique was useful in 2020 in order to time the March bottom.

- The broad head-and-shoulders pattern with the horizontal neckline at about $31 points to the $21 level as the likely target.

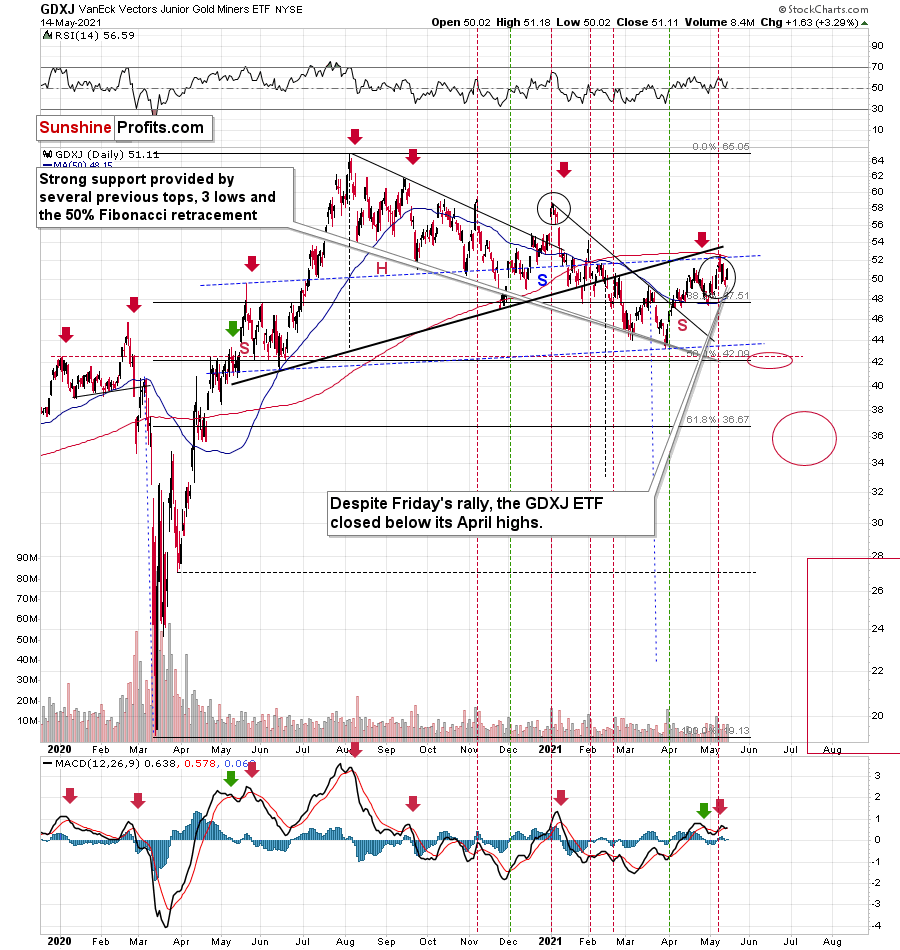

In addition, when observing through the lens of the GDXJ ETF, the junior miners are eliciting the same bearish signals. If you analyze the chart below, you can see that despite the recent strength, the GDXJ ETF is still trading below its medium-term rising support line (the thick black line below). More importantly, though, with the junior miners failing to reclaim this key level, their bearish H&S pattern remains intact.

Please see below:

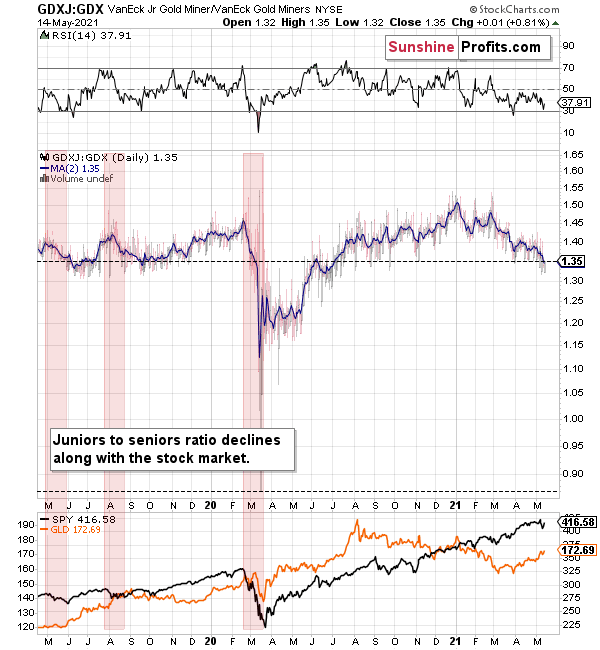

Even more ominous, the GDXJ ETF remains a significant underperformer of the GDX ETF. Despite sanguine sentiment and a strong stock market creating the perfect backdrop for the junior miners, the GDXJ ETF hasn’t lived up to the hype. Moreover, after failing to rally above its April highs on May 14, the outlook is even more bearish than it appears on the surface.

To explain, I wrote previously:

GDXJ is underperforming GDX just as I’ve been expecting it to. Once one realizes that GDXJ is more correlated with the general stock market than GDX is, GDXJ should be showing strength here, and it isn’t. If stocks don’t decline, GDXJ is likely to underperform by just a bit, but when (not if) stocks slide, GDXJ is likely to plunge visibly more than GDX.

Expanding on that point, the GDXJ/GDX ratio has been declining since the beginning of the year, which is remarkable because the general stock market hasn’t plunged yet. And once the general stock market suffers a material decline, the GDXJ ETF’s underperformance will likely be heard loud and clear.

Please see below:

To explain, I wrote on May 11:

What about juniors? Why haven’t they been soaring relative to senior mining stocks? What makes them so special (and weak) right now? In my opinion, it’s the fact that we now – unlike at any other time in the past – have an asset class that seems similarly appealing to the investment public. Not to everyone, but to some. And this “some” is enough for juniors to underperform.

Instead of speculating on an individual junior miner making a killing after striking gold or silver in some extremely rich deposit, it’s now easier than ever to get the same kind of thrill by buying… an altcoin (like Dogecoin or something else). In fact, people themselves can engage in “mining” these coins. And just like bitcoin seems similar to gold to many (especially the younger generation) investors, altcoins might serve as the “junior mining stocks” of the electronic future. At least they might be perceived as such by some.

Consequently, a part of the demand for juniors was not based on the “sympathy” toward the precious metals market, but rather on the emotional thrill (striking gold) combined with the anti-establishment tendencies (gold and silver are the anti- metals, but cryptocurrencies are anti-establishment in their own way). And since everyone and their brother seem to be talking about how much this or that altcoin has gained recently, it’s easy to see why some people jumped on that bandwagon instead of investing in junior miners.

This tendency is not likely to go away in the near term, so it seems that we have yet another reason to think that the GDXJ ETF is going to move much lower in the following months – declining more than the GDX ETF. The above + gold’s decline + stocks’ decline is truly an extremely bearish combination, in my view.

So, how low could the GDXJ ETF go?

Well, absent an equity rout, the juniors could form an interim bottom in the $34 to $36 range. Conversely, if stocks show strength, juniors could form the interim bottom higher, close to the $42.5 level. For context, the above-mentioned ranges coincide with the 50% and 61.8% Fibonacci retracement levels and the GDXJ ETF’s previous highs (including the late-March/early-April high in case of the lower target area). Thus, the S&P 500 will likely need to roll over for the weakness to persist beyond these levels.

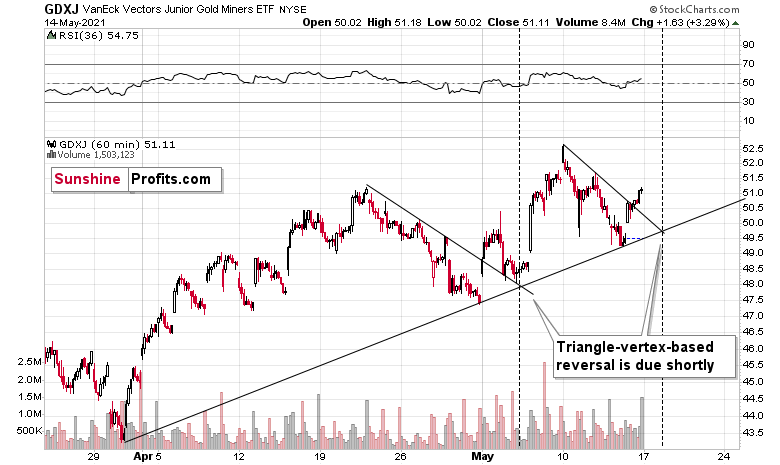

If that wasn’t enough, the GDXJ ETF’s prospects are actually dwindling by the hour. Case in point: if you analyze the chart below, you can see that the junior miners miraculously held above their rising support line. However, with a second triangle-vertex-based reversal point fast approaching, the clock is ticking on the GDXJ ETF’s recent strength. Moreover, an identical setup led to a bearish reversal earlier this month, and the triangle-vertex-based reversal pattern is increasingly reliable over the short, medium and long term.

Please see below:

The next triangle-vertex-based reversal point is due later today or tomorrow, so it seems that the days (hours?) of the rally are numbered. The pre-market upswing in gold seems to fit the above very well.

As further evidence of the miners’ shrinking margin for error, the HUI Index/S&P 500 ratio has recorded a major, confirmed breakdown. And with the ratio nowhere near recapturing its former glory, it’s another sign that a storm is brewing. Moreover, after moving back and forth for the last few months, not only has the HUI Index/S&P 500 ratio broken below its rising support line (the upward sloping black line below), but the ratio has also broken below the neckline of its roughly 12-month H&S pattern (the dotted red line below). As a result, given the distance from the head to the neckline, the HUI Index/S&P 500 ratio is on a collision course back to (at least) 0.050.

Please see below:

When the ratio presented on the above chart above is rising, it means that the HUI Index is outperforming the S&P 500. When the line above is falling, it means that the S&P 500 is outperforming the HUI Index. If you analyze the right side of the chart, you can see that the ratio has broken below its rising support line. For context, the last time a breakdown of this magnitude occurred, the ratio plunged from late-2017 to late-2018. Thus, the development is profoundly bearish.

Playing out as I expected, a sharp move lower was followed by a corrective upswing back to the now confirmed breakdown level (which is now resistance). Mirroring the behavior that we witnessed in early 2018, after breaking below its rising support line, the HUI Index/S&P 500 ratio rallied back to the initial breakdown level (which then became resistance) before suffering a sharp decline. And with two-thirds of the analogue already complete, the current move lower still has plenty of room to run. Likewise, the early-2018 top in the HUI Index/S&P 500 ratio is precisely when the USD Index began its massive upswing. Thus, with history likely to rhyme, the greenback could spoil the miners’ party once again.

In addition, the HUI to S&P 500 ratio broke below the neck level (red, dashed line) of a broad head-and-shoulders pattern, and it verified this breakdown by moving temporarily back to it. The target for the ratio based on this formation is at about 0.05 (slightly above it). Consequently, if the S&P 500 doesn’t decline, the ratio at 0.05 would imply the HUI Index at about 196. However, if the S&P 500 declined to about 3,200 or so (its late-2020 lows) and the ratio moved to about 0.05, it would imply the HUI Index at about 160 – very close to its 2020 lows.

All in all, the implications of mining stocks’ relative performance to gold and the general stock market are currently bearish.

But if we’re headed for a GDX ETF cliff, how far could we fall?

Well, there are three reasons why the GDX ETF might form an interim bottom at roughly ~$27.50 (assuming no big decline in the general stock market):

- The GDX ETF previously bottomed at the 38.2% and 50.0% Fibonacci retracement levels. And with the 61.8% level next in line, the GDX ETF is likely to garner similar support.

- The GDX ETFs late-March 2020 high should also elicit buying pressure.

- If we copy the magnitude of the late-February/early-March decline and add it to the early-March bottom, it corresponds with the GDX ETF bottoming at roughly $27.50.

Keep in mind though: if the stock market plunges, all bets are off. Why so? Well, because when the S&P 500 plunged in March 2020, the GDX ETF moved from $29.67 to below $17 in less than two weeks. As a result, U.S. equities have the potential to make the miners’ forthcoming swoon all the more painful.

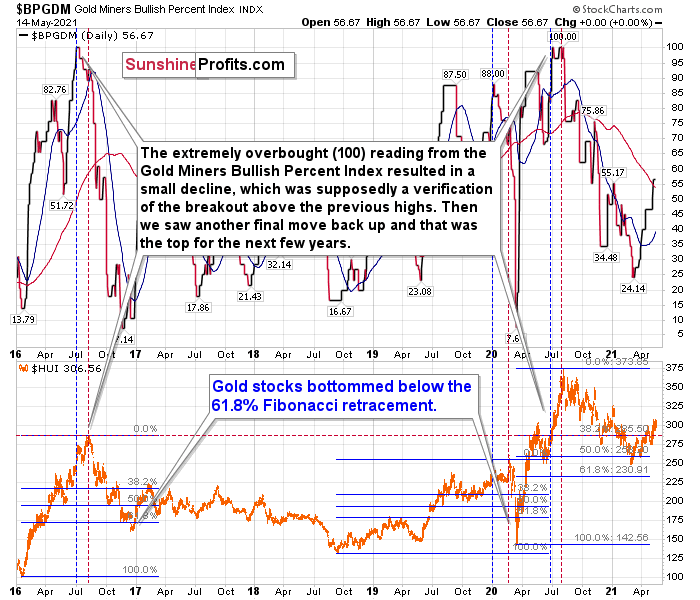

As another reliable indicator (in addition to the myriads of signals coming not only from mining stocks, but from gold, silver, USD Index, stocks, their ratios, and many fundamental observations) the Gold Miners Bullish Percent Index ($BPGDM) isn’t at levels that trigger a major reversal. The Index is now approaching 57. However, far from a medium-term bottom, the latest reading is still more than 47 points above the 2016 and 2020 lows.

Back in 2016 (after the top), and in March 2020, the buying opportunity didn’t present itself until the $BPGDM was below 10.

Thus, with the sentiment still relatively elevated, it will take more negativity for the index to find the true bottom.

The excessive bullishness was present at the 2016 top as well, and it didn’t cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

Please note that back in 2016, there was an additional quick upswing before the slide, and this additional upswing had caused the $BPGDM to move up once again for a few days. It then declined once again. We saw something similar also in the middle of 2020. In this case, the move up took the index once again to the 100 level, while in 2016 this wasn’t the case. But still, the similarity remains present.

Back in 2016, when we saw this phenomenon, it was already after the top and right before the big decline. Based on the decline from above 350 to below 280, we know that a significant decline is definitely taking place.

But has it already run its course?

Well, in 2016 and early 2020, the HUI Index continued to move lower until it declined below the 61.8% Fibonacci retracement level. The emphasis goes on “below” as this retracement might not trigger the final bottom. Case in point: back in 2020, the HUI Index undershot the 61.8% Fibonacci retracement level and gave back nearly all of its prior rally. And using the 2016 and 2020 analogues as anchors, this time around, the HUI Index is likely to decline below 231. In addition, if the current decline is more similar to the 2020 one, the HUI Index could move to 150 or so, especially if it coincides with a significant drawdown of U.S. equities.

With all of that said: how will we know when a medium-term buying opportunity presents itself?

We view price target levels as guidelines and the same goes for the Gold Miners Bullish Percent Index (below 10), but the final confirmation will likely be gold’s strength against the ongoing USDX rally. At many vital bottoms in gold, that’s exactly what happened, including the March bottom.

Gold

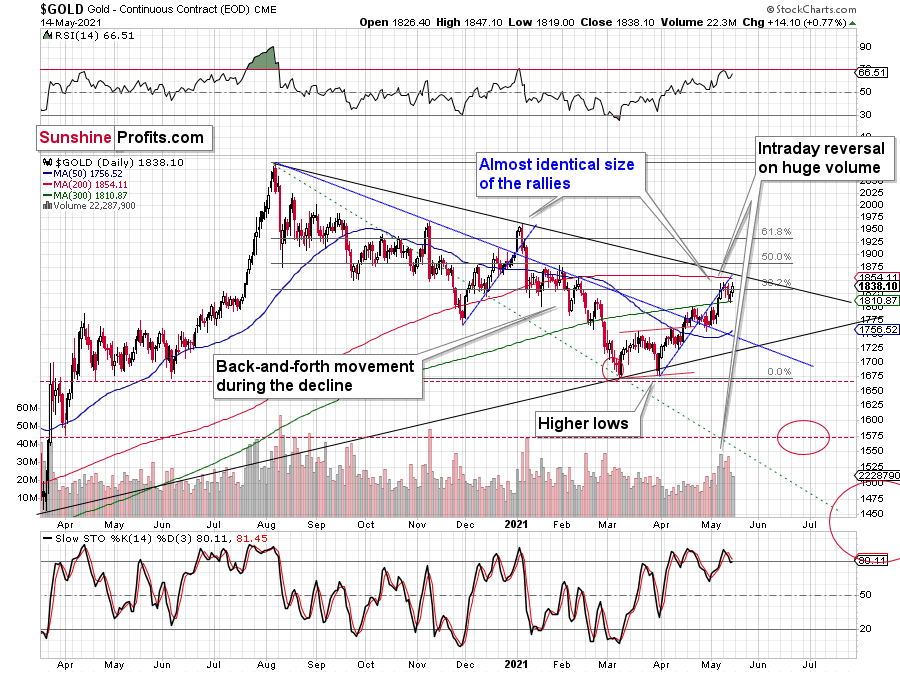

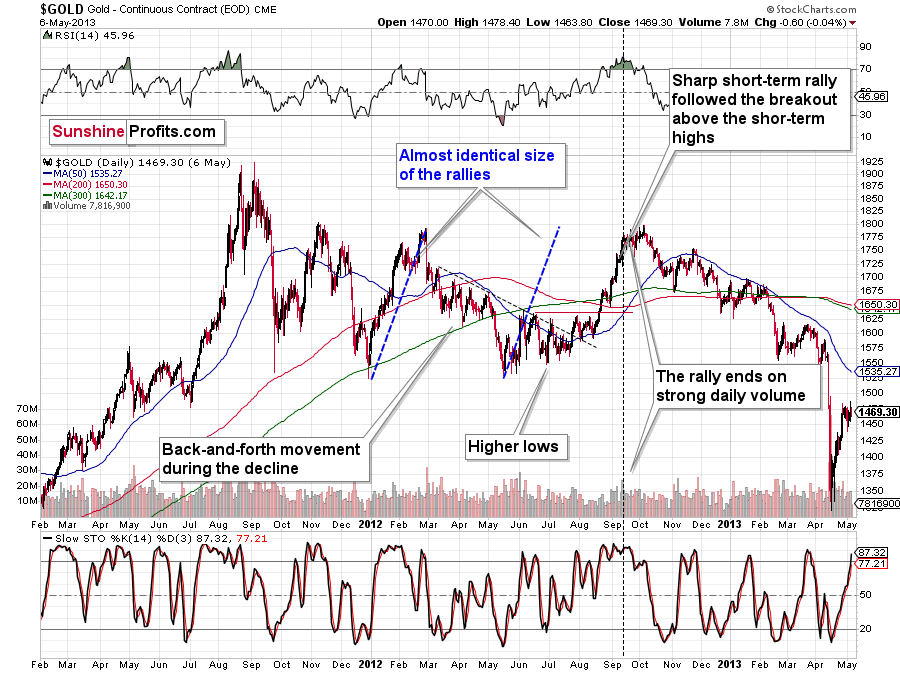

With gold’s back-and-forth price action culminating with relatively low volume on May 14, the yellow metal is mirroring its behavior from 2012. Case in point: back then, gold zigzagged with anxiety before suffering a material drawdown. In fact, in early October 2012, it moved slightly above the initial highs right before sliding. And while it wouldn’t be surprising to see some early-week strength (in fact, we see gold about $9 higher in the pre-market session), the implications from the GDXJ ETF’s triangle-vertex-based reversal pattern (on the hourly chart) signals that time is about to run out.

Please see below:

Based on today’s pre-market upswing, gold might reach its declining medium-term resistance line (~1,860) any hour now, which might seem like a very bullish development until one considers the following:

- Based on the self-similarity to 2012, that’s exactly what gold “should” do right before topping and sliding.

- This move would make the size of the current rally practically identical to the rally from late 2020 to early 2021, which was followed by a sharp slide.

- We have a short-term triangle-vertex-based reversal in the junior miners early this week, so we would likely see some kind of reversal anyway, and since the current move is up, we’re likely to see a top shortly.

Let’s dig deeper into point 2. The rally taking place from March to the present is almost exactly the same as the one from late November 2020 to early January 2021. Why is this notable?

Because of the similarity to the final top before the 2012-2013 slide that I mentioned before.

The March 2021 low formed well below the previous low, but as far as other things are concerned, the current situation is similar to what happened in 2012.

The relatively broad bottom with higher lows is what preceded both final short-term rallies – the current one, and the 2012 one. Their shape as well as the shape of the decline that preceded these broad bottoms is very similar. In both cases, the preceding decline had some back-and-forth trading in its middle, and the final rally picked up pace after breaking above the initial short-term high.

Interestingly, the 2012 rally had ended in huge volume, which is exactly what we saw on Friday. To be 100% precise, the 2012 rally didn’t end then, but it was when over 95% of the rally was over. Gold moved very insignificantly higher since that time. Most importantly, though, it was the “dollars to the upside, hundreds of dollars to the downside” situation. And it seems that we are in this kind of situation right now once again.

Interestingly, back in 2013 gold started its gargantuan (on a side note, the Gargantua and Pantagruel book where this word comes from is one of the most ridiculous, obscene and oddly entertaining books I’ve ever read) slide from about $1,800 and it is not far from this level also today.

Moreover, let’s keep in mind that the RSI indicator just topped very close to 70, which is what tends to happen when gold tops. The upside seems very limited.

“Ok, but what price level would be likely to trigger a bigger rebound during the next big slide?”

Well, the 76.4% Fibonacci retracement level (it’s visible as the 23.6% Fibonacci retracement level on the above chart as inverting the scale is used as a workaround) also coincides with gold’s April 2020 low. Taken together, an interim bottom could form in the ~$1,575 to $1,600 range.

For context, back in early March, the yellow metal continued to decline after reaching the 61.8% Fibonacci retracement (visible as 38.2% Fibonacci retracement) level, while, in contrast, the miners began to consolidate. Gold finally bottomed slightly below the retracement – at its previous lows. This time around, we might witness a similar event. And while the story plays out, the miners’ relative strength should signal the end of the slide (perhaps with gold close to 1,600), while gold will likely garner support sometime thereafter (at $1,575 – $1,580 or so).

Remember though: this is only an interim target. Over the medium term, the yellow metal will likely form a lasting bottom in the ~$1,450 to $1,500 range.

And why is that?

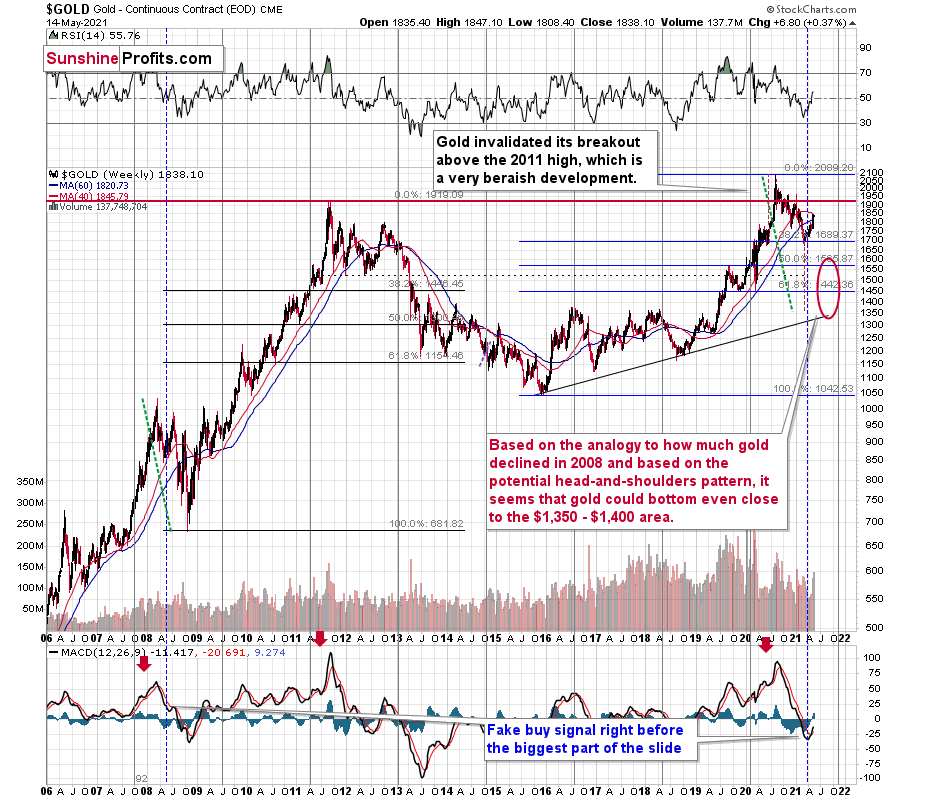

Well, if you analyze the long-term chart below, you can see that the yellow metal has invalidated the breakout above its 2011 high. More importantly, though, with its rising support line (on the right side of the chart) also coinciding with the 61.8% Fibonacci retracement level and the 2019 and 2020 lows, ~$1,450 to $1,500 is the most prudent medium-term price target.

Conversely, if the 2008 analogue repeats – and a crisis of confidence erupts across U.S. equities – the PMs could move substantially lower. When combining an equity shock with an USD Index’s resurgence, the yellow metal could bottom at roughly $1,400 (or even ~$1,350). Similarly, while the MACD indicator (on gold’s 40-year chart near the top of today’s edition) signals a bottom in the ~$1,200 to ~1,350 range, to be perfectly clear, ~$1,450 to $1,500 is the most likely outcome.

If you analyze the red arrow in the lower part of the above chart (the weekly MACD sell signal), today’s pattern is similar not only to what we saw in 2011, but also to what we witnessed in 2008. Thus, if similar events unfold – with the S&P 500 falling and the USD Index rising (both seem likely for the following months, even if these moves don’t start right away) – the yellow metal could plunge to below $1,350 or so. The green dashed line shows what would have happened to the gold price if it had not declined as much as it did in 2008.

In addition, relative to 2011-2013, today’s price action is also a splitting image. For starters, gold invalidated the breakout above its 2011 highs. Invalidations of breakouts are sell signals, and it’s tough to imagine a more profound breakout that could have failed.

Furthermore, if you analyze the right side of the chart above (the bottom section), you can see that the MACD indicator has sprouted a tiny weekly buy signal. However, it’s important to remember that the same signal emerged in mid-2008 – which confirmed the previous rally but had no bullish implications for the future. Case in point: following the reading in 2008, gold’s volatility increased, and the yellow metal suffered several declines before finding a lasting bottom in 2009. Thus, the recent reading is nothing to write home about. I marked both cases with red, dashed lines.

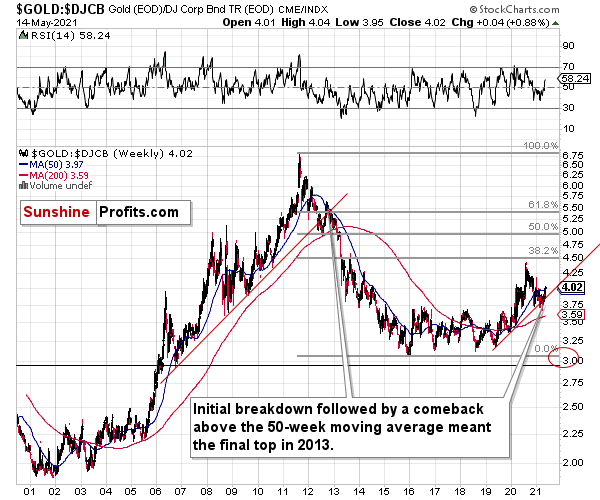

If that wasn’t enough, the gold/ Dow Jones Corporate Bond Index (Total Return) ratio recorded two meaningful developments:

- The ratio invalidated the breakdown below its rising support line (the red line on the right side of the chart below).

- The ratio moved above its 50-week moving average (the blue line below).

However, it’s important to remember that the ratio did the exact same thing in 2012-2013 before moving substantially lower.

Please see below:

To explain, if you analyze the middle of the chart above, you can see that the ratio recorded a countered rally, jumped back above its rising support line and 50-week moving average and then… collapsed. And with a similar pattern forming on the right side of the chart, the ratio is looking more and more like a widow-maker. Furthermore, when factoring in mining stocks’ bearish H&S patterns, the fundamental headwinds confronting gold and the strong likelihood of a medium-term swoon in the stock market, you can already hear the yellow metal’s death knell tolling in the distance.

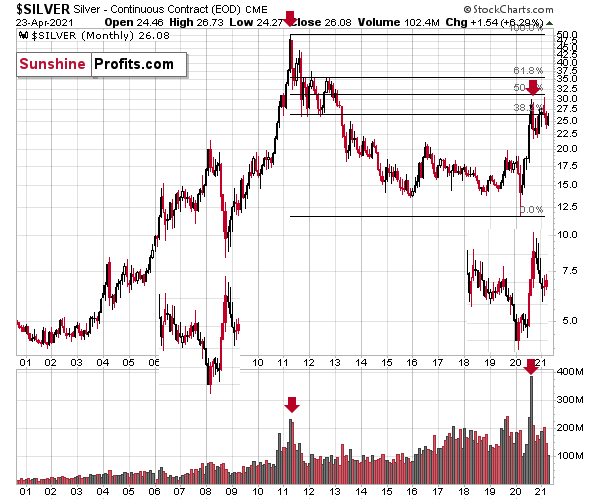

Silver

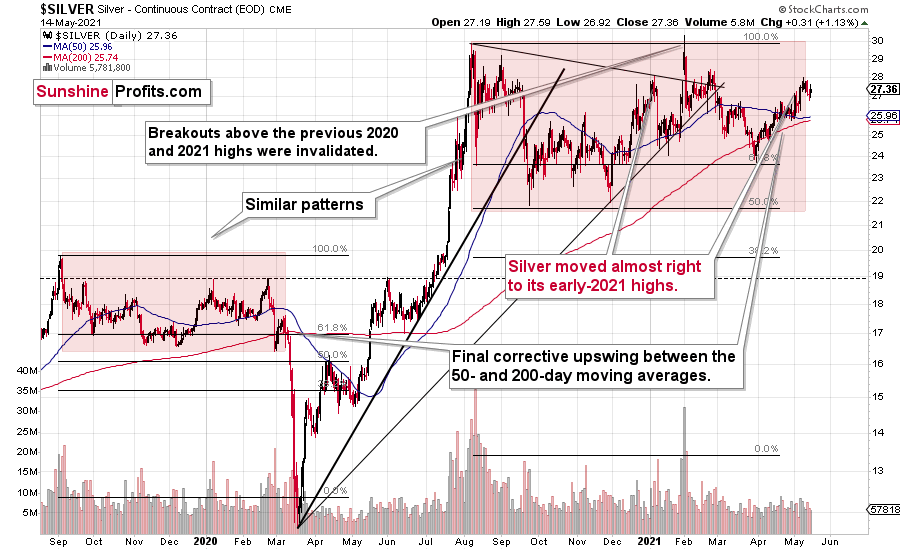

While silver’s recent outperformance may seem appetizing, the white metal is known to overpromise and underdeliver. Case in point: after recording several false breakouts, every prior display of strength ended with extreme disappointment. And while bearish medium-term implications should take precedence over short-term spurts, the white metal is once again seducing investors like it did in late 2019/early 2020.

Please see below:

To explain, if you analyze the left side of the chart above, you can see that silver moved back and forth before breaking toward its September highs. However, after failing to complete the milestone, the white metal eventually collapsed. As a result, with the pattern on the right side of the chart eerily similar, investors’ optimism has occurred at what’s likely the worst possible time.

To that point, with its current behavior also mirroring 2008 – where silver fell below and then rallied back above its 50-day MA before plunging – the white metal remains on a journey of self-destruction.

Also, let’s keep in mind that silver tends to outperform gold on a very short-term basis right before big declines, and that’s what it’s been doing for a few days now.

For context, I wrote previously:

If we zoom in on the white metal’s price action in 2008, you can see that an immaterial bounce also occurred right before silver fell off a cliff.

The final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

Let’s be realistic - so far, the analogy might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

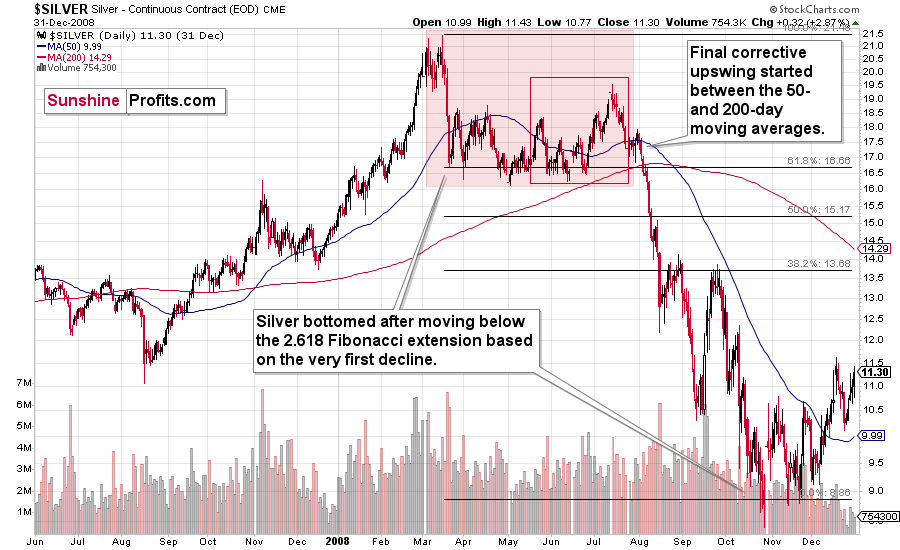

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

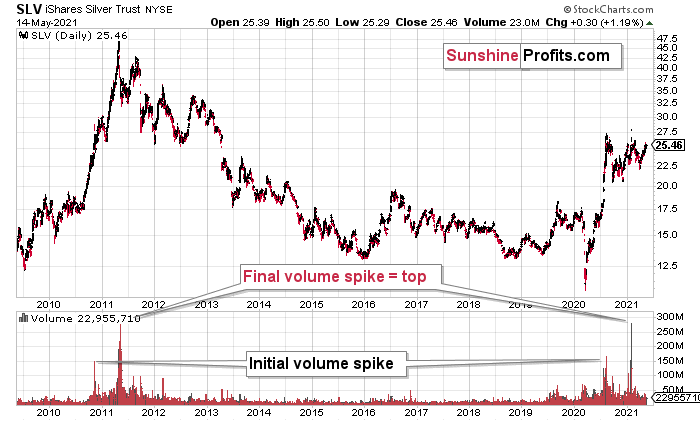

Highlighting the effect of WallStreetBets’ #SilverSqueeze, the SLV ETF’s volume spikes in 2020/2021 were nearly identical to the surges that we witnessed ~10 years ago. If you analyze the chart below, you can see that the massive inflows at the end of 2012 were not the beginning of a medium-term upswing. In fact, they coincided with silver’s final bounce before the white metal suffered a major decline.

Please see below:

If you analyze the volume spikes at the bottom of the chart, 2021 and 2011 are a splitting image. To explain, in 2011, an initial abnormal spike in volume was followed by a second parabolic surge. However, not long after, silver’s bear market began.

SLV-volume-wise, there's only one similar situation from the past - the 2011 top. This is a very bearish analogy as higher prices of the white metal were not seen since that time, but the analogy gets even more bearish. The reason is the "initial warning" volume spike in this ETF. It took place a few months before SLV formed its final top, and we saw the same thing also a few months ago, when silver formed its initial 2020 top.

The history may not repeat itself to the letter, but it tends to be quite similar. And the more two situations are alike, the more likely it is for the follow-up action to be similar as well. And in this case, the implications for the silver price forecast are clearly bearish.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

Similarly, silver’s inverse price action also has bearish implications. Nearly identical to the inverted formation that emerged from 2006 to 2009, today’s chart looks eerily similar to its predecessor.

While it’s more of a wild card, the above pattern shows that silver’s 2020 top plots are nearly identical to the inverse of the 2006-2009 performance. I copied the 2006 – 2009 performance right below the regular price movement and inverted it. I also copied this inverted pattern to the last few years.

The similarity is quite significant. And whenever a given pattern has been repeated, the odds are that it could also repeat in the not-too-distant future. Of course, there is no guarantee for that, but once the same market has reacted in a certain way to a specific greed/fear combination, it can just as well do it again. And these similarity-based techniques work quite often. So, while it’s not strong enough to be viewed as a price-path-discovery technique on its own, it should make one consider some scenarios more closely. In particular, this means that the declines in the prices of silver, gold, and mining stocks could be bigger and take longer than it seems based on other charts and techniques.

The above is also in tune with the implications of the sell signal from the MACD indicator on the monthly gold chart.

The only thing that comes to my mind which could – realistically – trigger such a prolonged decline would be a major drop in the general stock market. Given what I wrote above, the latter is quite possible, so I’ll be on the lookout for confirmations and invalidations of this scenario.

If history rhymes, silver could be in for a profound decline over the next few months (beyond my initial target). Moreover, the development would increase the duration of the precious metals’ bear market (also beyond my initial forecast).

After all, gold did invalidate its long-term breakout above the 2011 highs, and the way gold reacted to a small upswing in the USD Index was truly profound…

Turning to cross-asset correlations, gold, silver and the HUI Index’s 10-day correlations have stabilized. With the PMs exhibiting negative relationships with the U.S. dollar, their short-term behavior is similar to what we should expect over the medium term. More importantly, though, with the USD Index beginning to resemble a caged animal, once the greenback is released back into the wild, the PMs are likely to be its first meal.

For more context, I wrote previously:

Since gold, silver, and mining stocks have been strongly negatively correlated with the USD Index in the medium term, it seems likely that they will be negatively affected by the upcoming sizable USDX upswing.

…Until we see the day where gold reverses or soars despite the U.S. currency’s rally.

If that happens with gold at about $1,700, we’ll have a very good chance that this was the final bottom. If it doesn’t happen at that time, or gold continues to slide despite USD’s pause or decline, we’ll know that gold has further to fall.

Naturally, we’ll keep you – our subscribers – informed.

To move forward, how does the GDX downside target compare to gold’s downside target? If, at the same time, gold moves to about $1,700 and miners are already after a ridiculously big drop (to $31-$32 in the GDX ETF, or lower), the binding profit-take exit price of your GDX ETF will become $32.02 (those with higher risk tolerance might lower it to $31.15 or so, but moving it lower seems just too risky).

At this time, the final GDX target (the one that would correspond to gold at $1,500 or so) is still unclear. The $17 - $23 area seems probable, especially if the general stock market slides once again. It’s too early to say with any significant level of certainty. Gold is providing us with a clearer final target, so that’s what we’ll focus on. And most importantly – we’ll focus on gold’s performance relative to the USD Index.

Overview of the Upcoming Part of the Decline

- It seems likely to me that the current corrective upswing is very close to being over, given gold’s similarity to what happened in 2012, USD’s similarity to 2016 and the situation in the general stock market.

- After miners slide once again in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver (this could take another 1-2 weeks to materialize). I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,450 - $1,500 and the entire decline (from above $1,700 to about $1,475) would be likely to take place within 1-12 weeks, and I would expect silver to fall hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments, in my view. This might happen with gold close to $1,475, but it’s too early to say with certainty at this time. In other words, the entire decline could take between 1 and 12 weeks, with silver declines occurring particularly fast in the final 1-2 weeks.

- If gold declines even below $1,500 (say, to ~$1350 or so), then it could take another 10 weeks or so for it to bottom, but this is not what I view as a very likely outcome.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops. If the general stock market puts the final top in the first half of May (which seems quite likely given NASDAQ’s top in late April), then we might expect the precious metals sector to bottom sometime in August.

- The above is based on the information available today, and it might change in the following days/weeks.

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Letters to the Editor

Q: There is a lot of pressure from both sides on the DXY. The DXY wants to move down, and THIS IS THE ISSUE. If it breaks below 90 and holds, will the risk for a downward movement increase? There is definitely a fight going on right now, as there are large camps on both sides of the DXY. Short position is a risk in PMs. Please define the short and long positions fight in the DXY, the forces of this battle and how this is going to continue until a direction is established. Why is the DXY continuing its trend down while gold is proceeding with a move up in value?

A: The reasons for the USD’s declines, in my view, are mostly based on the perception regarding the monetary stance in the U.S. and in the Eurozone. The market still seems to believe that the Eurozone might really experience hawkish actions and not just hawkish comments. This is enough for a “snowball effect” to start, where people enter positions just because the market moved in a certain direction. And these trends then continue until the positions are too extreme – just like pendulum swings. Based on comparisons to historical patterns (and no, it doesn’t really matter that the analogies are to situations from different times because the underlying emotions: fear and greed are the same) it seems that the position is too excessive already, and that the move in the other direction – a rallying USDX – is already underway.

Just as it was the case in 2016, the rally doesn’t look convincing initially. But the point is that when it finally does start to look convincing, and it’s obvious that the trend is up… It’s already after a large part of the rally, and the best opportunities are already gone. In fact, when everyone gets bullish on the USD Index, it might be time to consider getting bearish on it.

I don’t think that a breakdown below 90 would be a huge downside risk. The strongest support is provided by the early-2021 low, so a confirmed (!) breakdown below this level would indeed be a bearish development that might change the short-term outlook. However, it seems more likely to me that we won’t see this kind of performance, and instead, the 2016 self-similar pattern will continue, taking the USD Index higher and contributing to gold’s decline.

Q: With the escalating conflict in Gaza, do you believe Gold could rally to a new top in the coming days? What's the influence of the conflict, in your opinion?

A: To answer the last question: most likely temporary. The geopolitical events tend to have only temporary effects on the prices of precious metals. This fits the scenario in which gold – currently – moves higher (just a little above the previous highs), just like it did in 2012, and then it slides in a profound manner, and that’s the beginning of the final slide in the precious metals sector that takes us to the ultimate buying opportunity.

Summary

To summarize, even though it doesn’t seem to be the case based on this month’s price change in gold, it seems that the yellow metal’s days are numbered. This is based not only on the excessively oversold USD Index and its 2016 self-similar pattern but also on what’s happening in the stock market, silver’s recent outperformance and price levels reached throughout the precious metals sector. From the long-term point of view, the current situation seems similar to what we saw in the second half of 2012, while from the short-term point of view it seems similar to what we saw at the beginning of 2021. While the very near term remains unclear (Friday’s reversal might have been the final top, but there’s no certainty there), the outlook for the next several months remains very bearish.

After the sell-off (that takes gold to about $1,350 - $1,500), we expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Monday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief