Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update. Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

Let’s start with a quick review of the key fundamental news that hit the market last week.

Why Should I Still Care About Inflation?

Inflation softened slightly in July and gold prices rose, but the bullish joy may be premature.

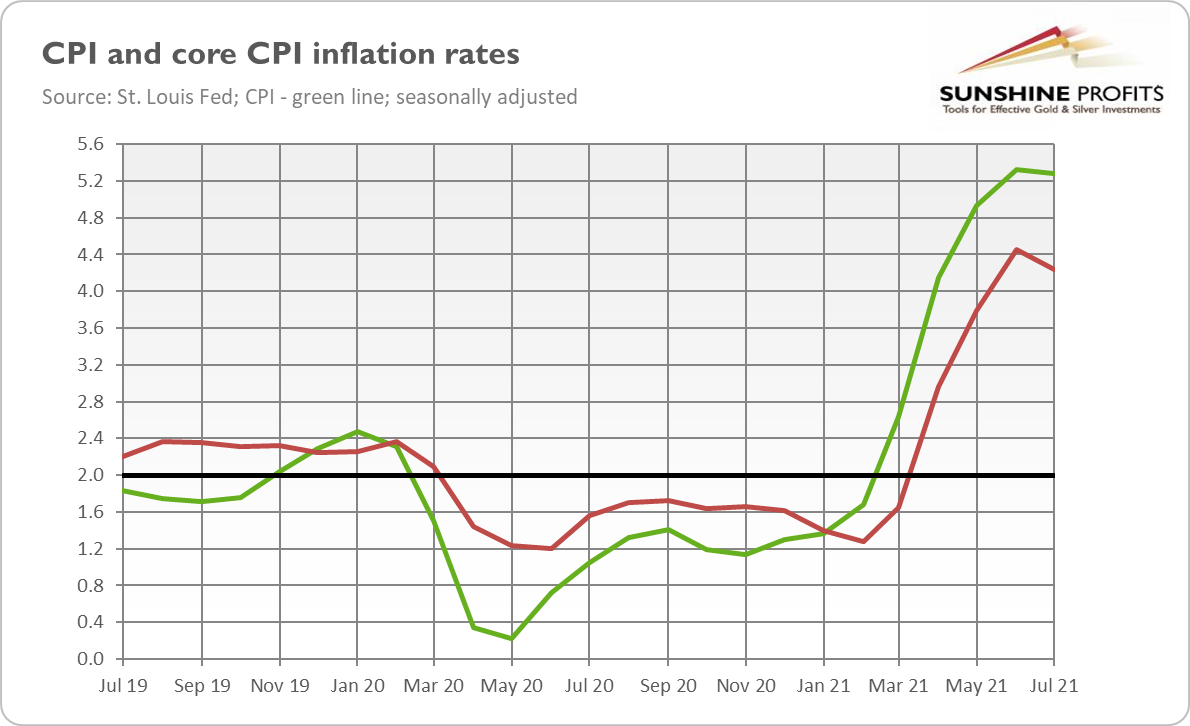

Inflation eased a bit in July, but it remained disturbingly high. According to the latest BLS report on inflation, the CPI increased 0.5% in July after rising 0.9% in June. The core CPI, which excludes food and energy, also softened, as it rose 0.3% in July after increasing 0.9% in June. The deceleration was mainly caused by a much smaller advance in the index for used cars, which increased only 0.2% (it was 10.5% in June).

However, on an annual basis, inflation practically stayed unchanged since June, as the chart below shows. The overall index surged 5.4% for the second month in a row (on a seasonally unadjusted basis), while the core CPI soared 4.3%, following a 4.5% jump in the previous month.

So, at first glance, it seems that inflation has peaked. This might be true, but please notice that it remained disturbingly high despite the deceleration in several subindexes, including the index for used cars. I dread to think what would be if these categories didn’t moderate!

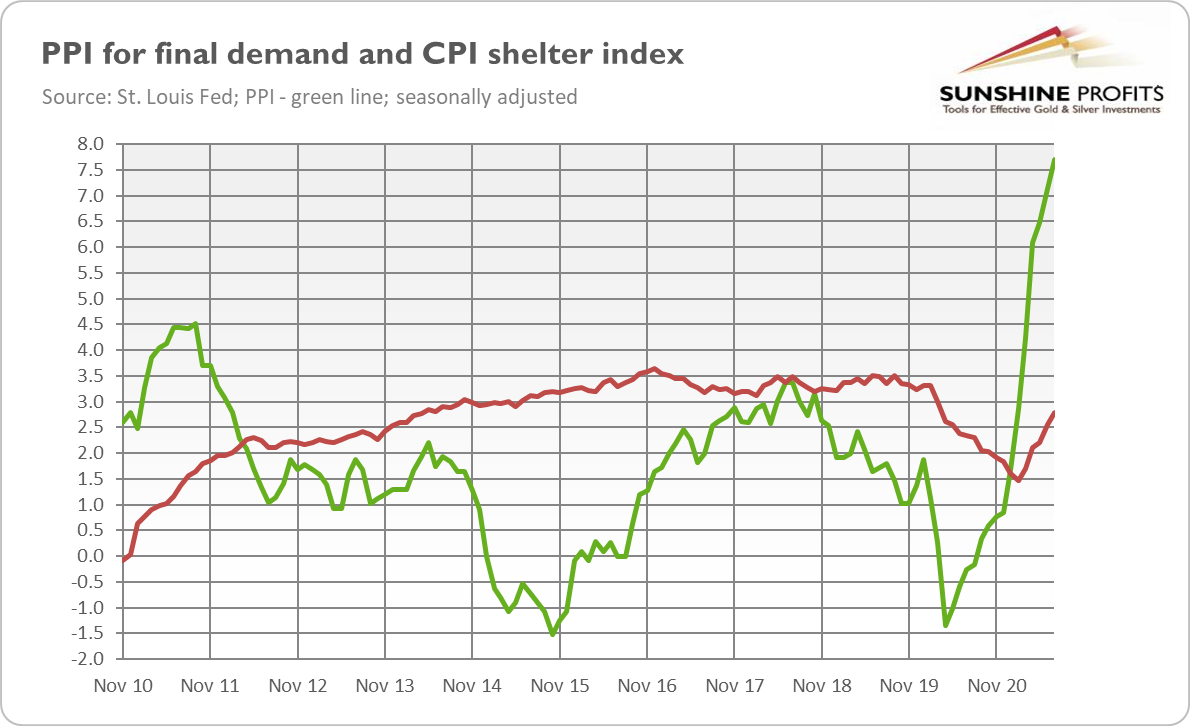

What’s more, the producer price index for final demand rose 1% in July (MoM) and 7.8% over the past 12 months, as one can see in the chart below. It was the largest advance since the 12-month data was first calculated in November 2010. Part of this increase could be passed on to consumers later, as companies have recently gained more ability to lift prices seeing weak resistance to price increases.

Additionally, the index for shelter – the biggest component of the CPI, not hit by the pandemic as strongly as restaurants and hotels industries – has been rising gradually since February 2021, and it has accelerated to 2.8% in July. Last but not least, the US Senate passed Biden’s infrastructure plan, which could also add something to the inflationary pressure by an increase in the money supply. All these developments suggest that inflation isn’t going away just yet.

What does the recent inflation report imply for the gold market? Well, theoretically, softer inflation should be negative for gold, which is seen as an inflation hedge and which historically shined during periods of high and accelerating inflation.

However, as the chart below shows, the price of gold has rebounded somewhat from last week’s low, gaining about $50 from Tuesday to Friday. It seems that steady (and partially below expectations) inflation gives the Fed room to maintain its ultra-dovish monetary policy. Indeed, according to the CME FedWatch Tool, the expectations for the Fed’s tightening cycle have diminished slightly from the previous week, which supported gold prices.

However, a bullish hurray might be premature. Inflation is still high and significantly above the Fed’s target. Inflation expectations remain elevated, and some measures even increased slightly in July. Unfortunately, markets seem not to worry significantly about inflation any longer, and the stock market continues its rally.

Even if inflation really softens later this year, which is likely given that some supply disruptions will probably resolve, it shouldn’t suddenly dive below 2%. So, the July report shouldn’t materially change the Fed’s stance, especially that the US central bank focuses more on the labor market now. Hence, gold investors should brace themselves for the upcoming tapering of quantitative easing.

However, just as day comes after night, upward waves come after bearish trends. The most likely macroeconomic scenario is that inflation will remain high, while the economic growth will slow down, which means stagflation. Indeed, the downward trend in the bond yields – despite high inflation – could signal weak growth, requiring dovish monetary policies. If history is any guide, gold will shine during stagflation.

Medium-Term Implications for Gold

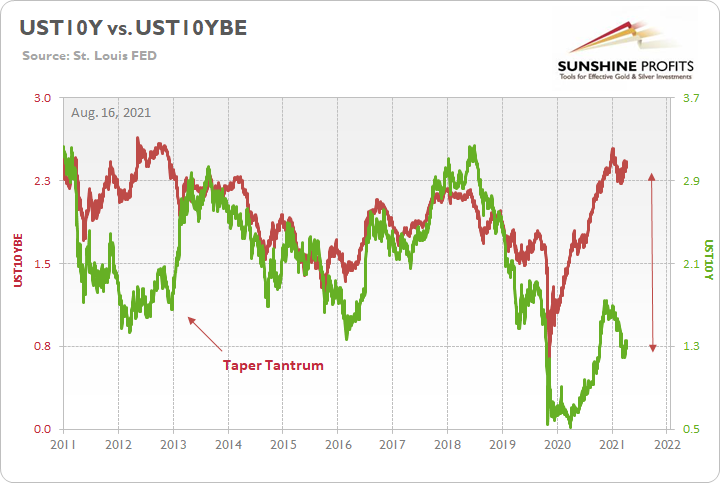

While the U.S. nonfarm payrolls report helped bring the pair closer together, the Delta variant has once again pushed them apart. As a result, the U.S. 10-Year Treasury yield still demonstrates its largest-ever divergence from the U.S. 10-Year breakeven inflation rate.

Please see below:

And if (once) the two lines reconnect, the development will likely send shockwaves across the precious metals market.

To explain, I wrote on May 11:

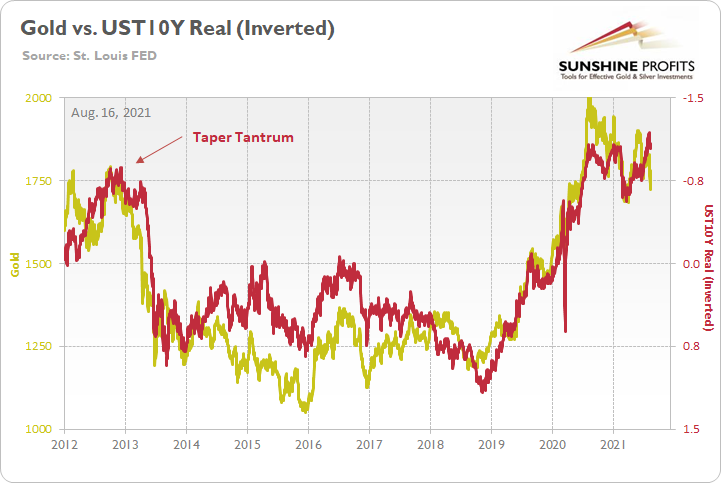

The gold line above tracks the London Bullion Market Association (LBMA) Gold Price, while the red line above tracks the inverted U.S. 10-Year real yield. For context, inverted means that the latter’s scale is flipped upside down and that a rising red line represents a falling U.S. 10-Year real yield, while a falling red line represents a rising U.S. 10-Year real yield.

If you analyze the left side of the chart, you can see that when the U.S. 10-Year Treasury yield began its move to reconnect with the U.S. 10-Year breakeven inflation rate in 2013 (taper tantrum), the U.S. 10-Year real yield surged (depicted by the red line moving sharply lower). More importantly, though, amidst the chaos, gold plunged by more than $500 in less than six months.

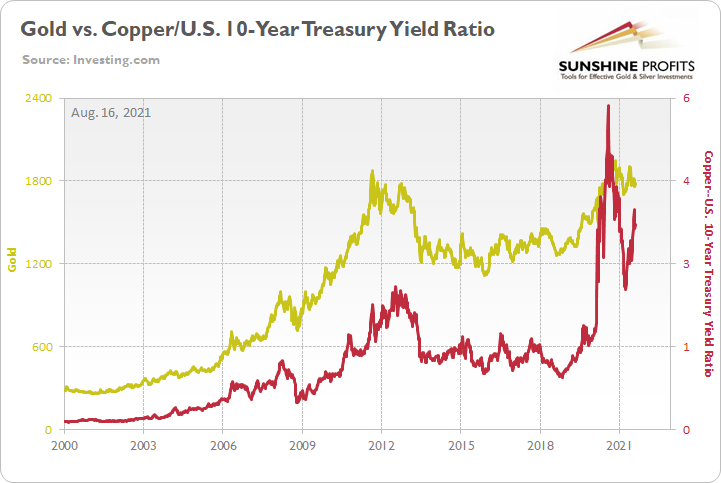

Over the medium-to-long term, the copper/U.S. 10-Year Treasury yield ratio is yet another leading indicator of gold’s future behavior.

I wrote previously:

When the copper/U.S. 10-Year Treasury yield ratio is rising (meaning that copper prices are rising at a faster pace than the U.S. 10-Year Treasury yield), it usually results in higher gold prices. Conversely, when the copper/U.S. 10-Year Treasury yield ratio is falling (meaning that the U.S. 10-Year Treasury yield is rising at a faster pace than copper prices), it usually results in lower gold prices.

If you analyze the chart below, you can see the close connection:

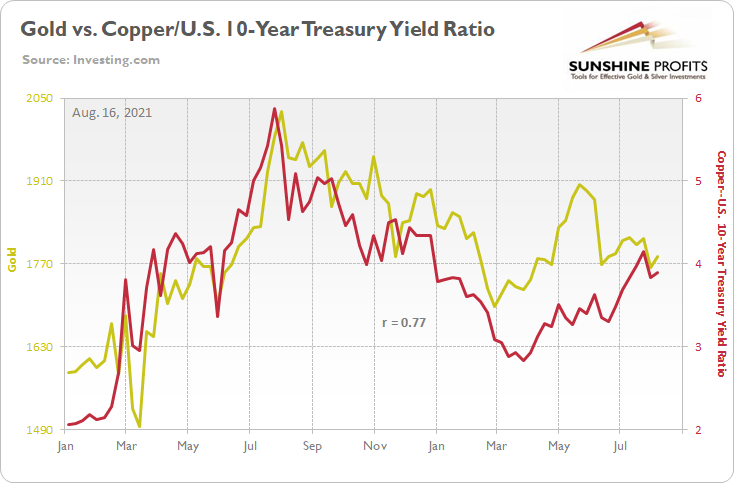

Moreover, while both variables have reconnected once again, the copper/U.S. 10-Year Treasury yield ratio still implies a gold price of roughly $1,750. However, there are plenty of other indicators which imply even lower prices for the yellow metal over the medium term.

Please see below:

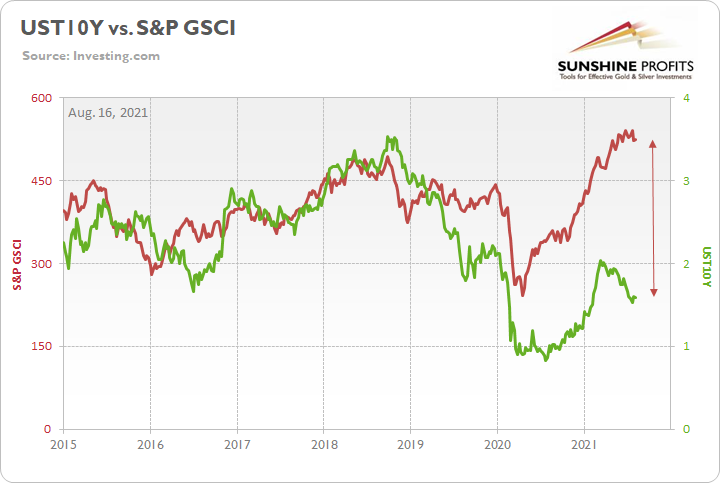

Finally, the S&P GSCI (the commodity index) has decoupled from the U.S. 10-Year Treasury yield. And with the former moving in near lockstep with the latter since 2015, a reversal of the imbalance could increase the PMs’ troubles over the medium term.

On the flip side, if we extend our time horizon, there are plenty of fundamental reasons why gold is likely to soar in the coming years. However, even the most profound bull markets don’t move up in a straight line, and corrections are inevitable.

As it relates to the precious metals, a significant correction (medium-term downtrend) is already underway. However, the pain is not over, and a severe climax likely awaits.

For context, potential triggers are not always noticeable, and the PMs may collapse on their own or as a result of some random trigger that normally wouldn’t cause any major action. However, a trigger will speed things up, and that’s where the S&P 500 comes in:

Stock Market Signals

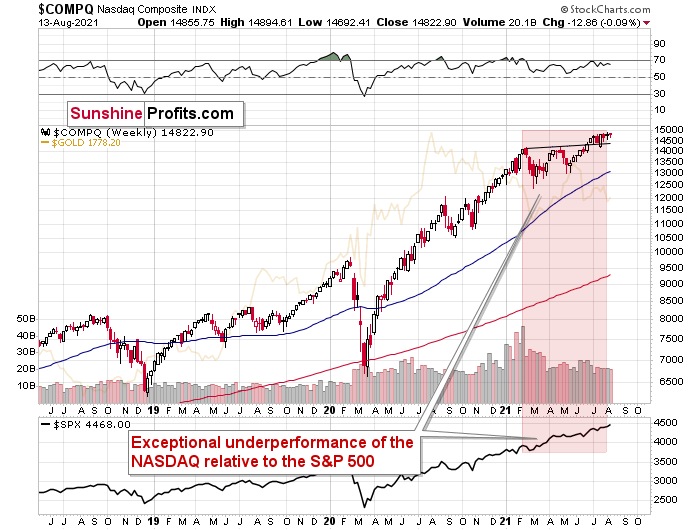

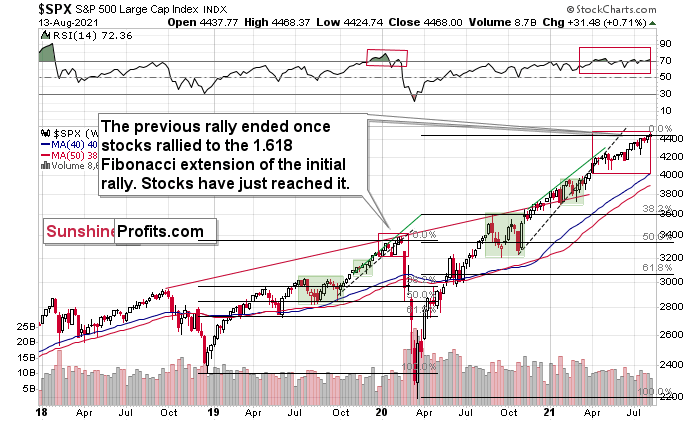

While the S&P 500 moved slightly higher last week, the NASDAQ Composite moved slightly lower and continued its bearish underperformance. Moreover, with both indices’ RSIs (Relative Strength Index) signaling overbought conditions (near 70), a reversion to the mean could result in a profound correction in the coming months.

Please see below:

As for the S&P 500, it’s a similar story. With its RSI mirroring the bearish behavior that we witnessed in 2019/2020 – though five moves are present this time, while two moves were present back then – the S&P 500 remains on a collision course lower. For context, similar behavior led to explosive drawdowns in early 2020 and in the second half of 2018. Moreover, with the Fed turning a bit more hawkish in recent weeks, volatility will likely erupt once the central bank’s taper timeline is finally revealed.

On top of that, the shape, the movement, and the drawdowns that occurred along the way during the S&P 500’s 2018-2020 rally all mirror today’s price action. To explain, the self-similar pattern from 2018-2020 saw the S&P 500 peak once the index rose slightly above the 1.618 Fibonacci extension level based on the size of the initial rally. On the above chart, you can see this as a move to the highest retracement in April 2019 – the full size of the rally compared to the 61.8% retracement is actually 1.618 of the initial rally, because 1 / 0.618 = ~1.618 (the Phi number).

And with the S&P 500 slightly exceeding this extension-based target on Aug. 13, we may have already witnessed the top. Back in 2020, the S&P 500 closed slightly above this level prior to the crash, and with an identical development playing out today, another drawdown could be right around the corner.

Keep in mind though: the PMs’ forthcoming slide is independent (and has been) of the performance of the general stock market – at least with regard to the existence of the PMs’ slide. However, due to the cross-asset implications and the interconnectedness of the financial markets, a severe correction of U.S. equities will likely supercharge the pace of the PMs’ implied decline (especially silver and mining stocks). If stocks continue to rally, PMs will likely still decline, but at a regular pace. As an example, we witnessed that behavior on Aug. 6. Even though the S&P 500 ended the day in the green, the PMs declined significantly.

For context, the precious metals used to bottom about 3 – 3.5 months after the top in the general stock market in some of the similar cases – for instance, in 1929. And with both major indices remaining resilient, the timeframe of the PMs’ final trough is still up in the air.

To explain, I wrote previously:

The U.S. equity benchmark’s RSI (Relative Strength Index) is still showing similarity to late 2019 – early 2020 and the double-top that was present in 2018. Moreover, with the S&P 500’s RSI making its third leap above 70, the indicator is likely in the process of forming a triple-top. To that point, while the RSI’s acceleration back above 70 changes the calculus relative to 2019/2020 – making the current interpretation relatively less bearish – there were two moves above 70 in the case of the RSI in early 2020 and only now we have the third one suggesting that something is different.

At the same time, however, the analogy is more bearish in terms of price moves. Stocks moved to a new high after back-and-forth movement with RSI close to 70. That’s what marked the end of the rally in early 2020.

More importantly, though, once the S&P 500 succumbs to this bearish reality, the development will likely compound the PMs’ selling pressure.

For more context:

Why should we – precious metals investors and traders – be concerned with the performance of stocks? Because when stocks finally top and start to decline, it will likely make the decline in the precious metals market much more severe. For one, identical developments occurred in 2008, 2020 and 1929. Second, the precious metals often bottom about 3 – 3.5 months after the top in the general stock market. Third, the S&P 500’s 2020 analogue is becoming even more valid by the day.

(…)

The markets are self-similar (which is another way of saying that they have a fractal nature), which generally means that while the history tends to rhyme, it also tends to rhyme in similar shapes of alike or various sizes.

For example, the rally from 2018–2020 seems very similar to the rally from 2020 to the present. Both rallies started after a sharp decline, and the first notable correction took the form of back-and-forth trading around the previous high. I marked those situations with big rectangles.

Then the rally continued with relatively small week-to-week volatility. I created rising support lines based on the final low of the broad short-term consolidation and the first notable short-term bottom.

This line was broken, and some back-and-forth trading followed, but it was only about half of the previous correction in terms of price and time.

Then, we saw a sharp rally that then leveled off. And that was the top. The thing that confirmed the top was the visible breakdown below the rising support line right after stocks invalidated a tiny breakout to new highs. That’s what happened in February 2020, and that’s what seems to be taking place right now.

Back in 2020, the rally ended when the weekly RSI moved above 70 once again and when the S&P moved slightly to its new highs. While the history doesn’t have to repeat itself to the letter, if we see another small move higher – to new highs – that also takes the RSI above 70, please keep in mind that it’s not really a bullish development, but actually history forming its final rhyme. And the implications appear bearish for the precious metals sector, as it’s likely to be hit by the first wave of stock market declines – just like it was the case in 2008, 2020, and… 1929.

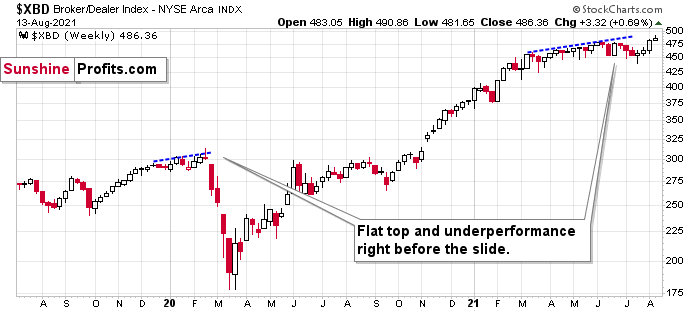

Furthermore, while the broker-dealer index (XBD) moved slightly higher last week, it recorded a mid-week reversal (which is bearish), the index is still underperforming the S&P 500, and a similar burst of very short-term strength occurred last year (mid-Feb.) right before the 2020 crash. Moreover, if financials decline next week, the dynamic will be just as bearish; a weekly rally followed by a weekly decline (of similar magnitude) will be similar to the intraweek reversal that we saw in mid-Feb. 2020. Overall, the monthly underperformance should take precedence over one week of bullish optimism.

Besides, please note that right before the 2020 slide, the financials formed a weekly reversal, and they did the same thing last week.

Please see below:

For context, I wrote previously:

One of the canaries in the coal mine is the financial sector. It indicated the 2020 slide by forming a relatively flat top and underperforming other stocks. That preceded the 2008 slide as well. Well, we’re seeing the financials underperforming once again. While the S&P 500 moved to new highs last week, the financial sector is more or less where it was in early March, below its June highs.

The bottom line?

It seems that history is indeed forming its final rhyme. However, can we start the 3-3.5-month countdown now? Well, while timing remains uncertain, the main drivers of the stock market’s success are beginning to sputter. With inflation running hot and employment likely to surge in the coming months (once enhanced unemployment benefits expire), all of the boxes should be checked for the FED to taper its asset purchases. And with investors largely averse to a reduction in liquidity, the outcome could have a profound impact on both the general stock market and the PMs.

Keep in mind though: a decline in stocks is not required for the PMs to decline. But a break in the former could easily trigger a sell-off in the latter, and if history decides to rhyme again, silver and the miners will be the hardest hit.

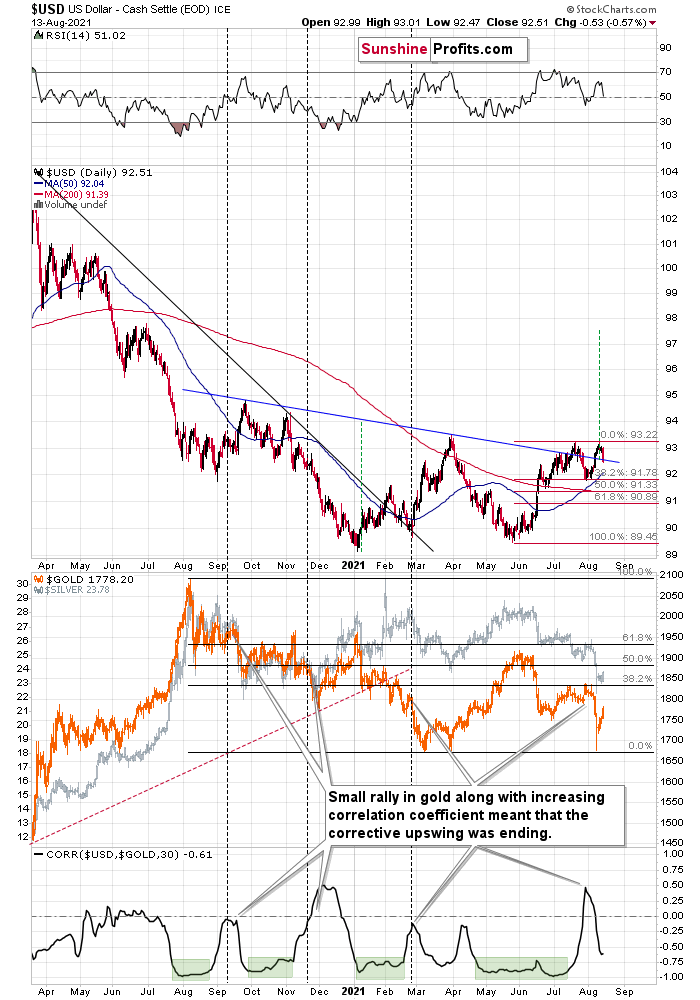

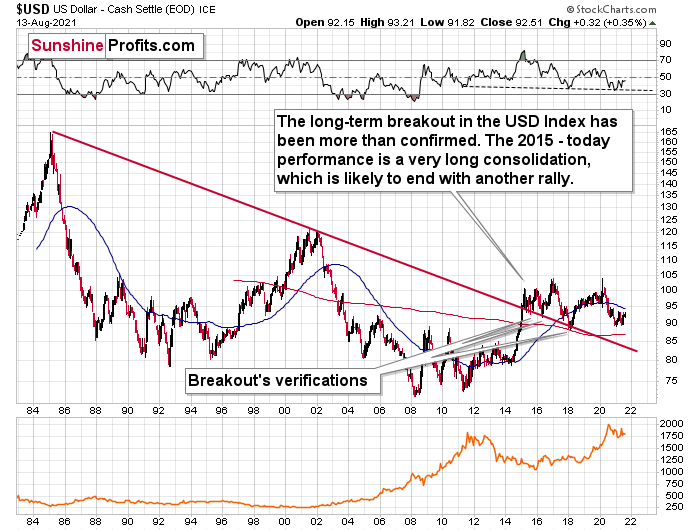

The USD Index (USDX)

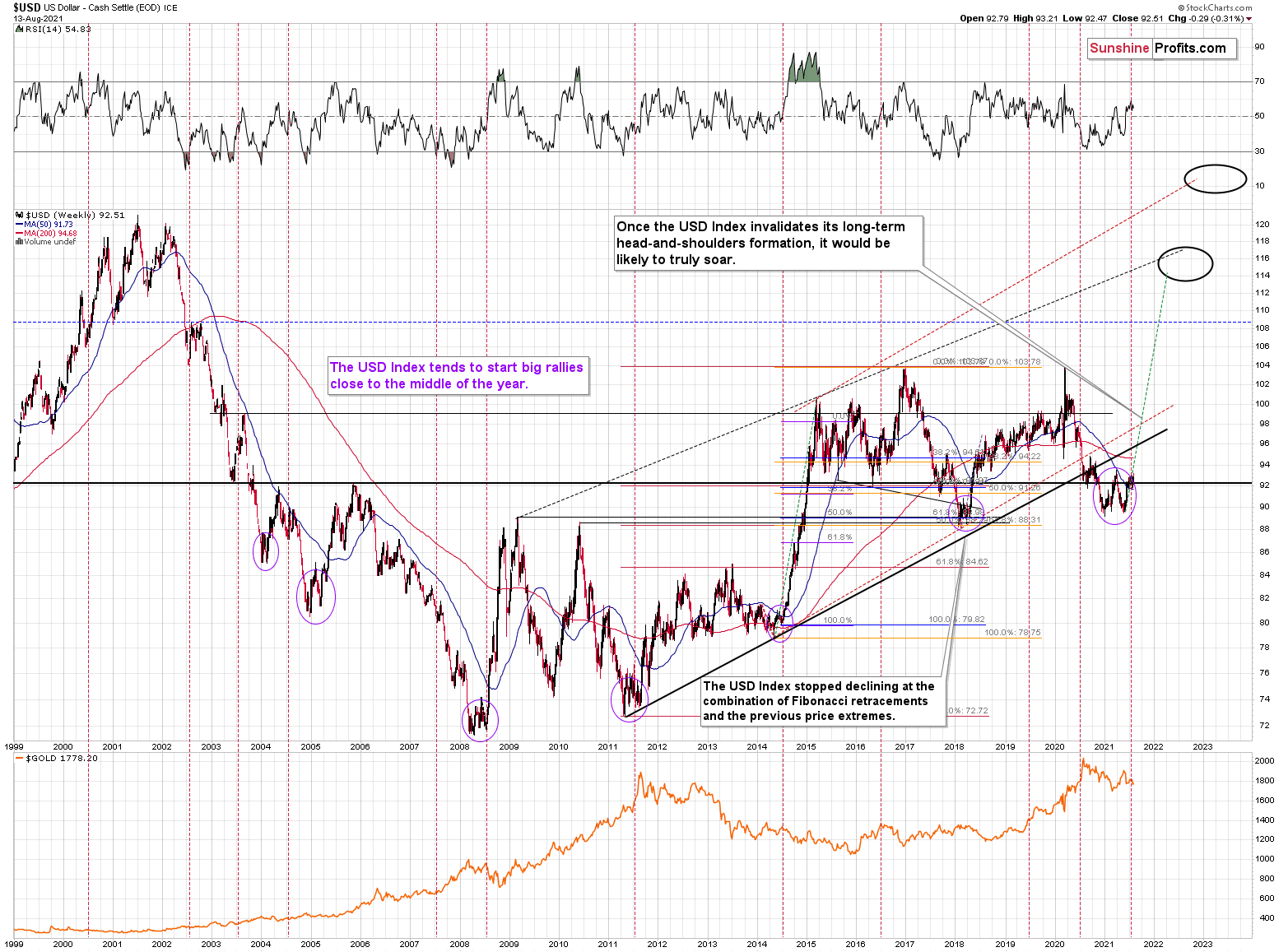

After surging above the neckline of its inverse (bullish) head & shoulders pattern, the USD Index backtested the breakout last week. And while holding the line is an extremely bullish sign, even if short-term weakness materializes, the USDX should still soar over the medium term.

Please see below:

To explain, the USD Index often sizzles in the summer sun and major USDX rallies often start during the middle of the year. For example, summertime spikes have been mainstays on the USD Index’s historical record and in 2004, 2005, 2008, 2011, 2014 and 2018, a retest of the lows (or close to them) occurred before the USD Index began its upward flights.

What’s more, profound rallies (marked by the red vertical dashed lines below) followed in 2008, 2011 and 2014. And with the current situation mirroring the latter, a small consolidation on the long-term chart is exactly what occurred before the USD Index surged in 2014. Likewise, the USD Index recently bottomed near its 50-week moving average; an identical development occurred in 2014. More importantly, though, with bottoms in the precious metals market often occurring when gold trades in unison with the USD Index (after ceasing to respond to the USD’s rallies with declines), we’re still far away from that milestone in terms of both price and duration.

Please see below (quick reminder: you can click on the chart to enlarge it):

Just as the USD Index took a breather before its massive rally in 2014, it seems that we saw the same recently. This means that predicting higher gold prices here is likely not a good idea.

As further evidence, the eye in the sky doesn’t lie. And with the USDX’s long-term breakout clearly visible, the smart money is already backing the greenback.

Please see below:

The bottom line?

Once the momentum unfolds, ~94.5 is likely the USD Index’s first stop, ~98 is likely the next stop, and the USDX will likely exceed 100 at some point over the medium or long term. Keep in mind though: we’re not bullish on the greenback because of the U.S.’ absolute outperformance. It’s because the region is fundamentally outperforming the Eurozone, the EUR/USD accounts for nearly 58% of the movement of the USD Index, and the relative performance is what really matters.

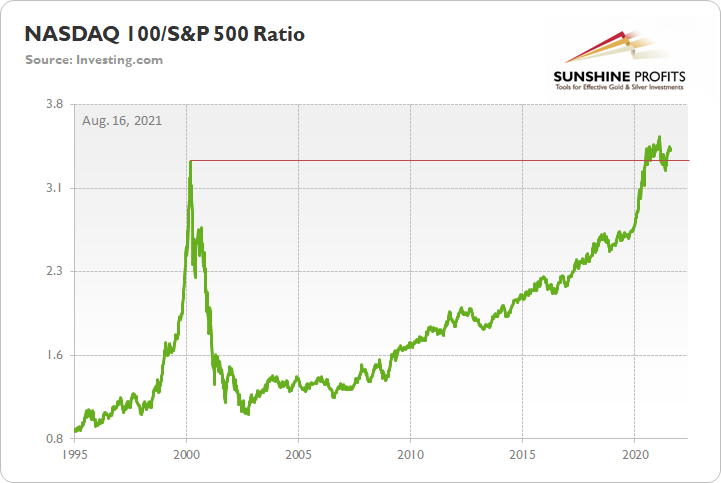

The NASDAQ 100

As a secondary catalyst, a material drawdown of the NASDAQ 100 could eventually rattle U.S. equities.

Please see below:

To that point, given the USDX’s strong negative correlation with the NASDAQ 100, a material reset could propel the greenback back to its March highs. Moreover, following a short-term consolidation, the USDX could even exceed those previous highs.

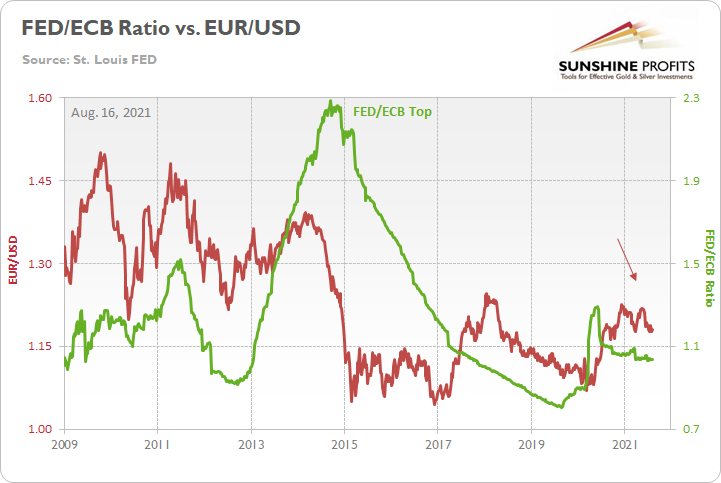

Furthermore, relative outprinting by the European Central Bank (ECB) remains of critical importance. Last week, the FED/ECB ratio was flat, while the EUR/USD increased by 0.30%. And given that the ratio has declined by more than 19% since May 2020, the EUR/USD still has some catching up to do.

Please see below:

The key takeaway?

With the ECB injecting more liquidity to support an underperforming Eurozone economy, the FED/ECB ratio, as well as EUR/USD, should move lower over the medium term. More importantly, though, because the EUR/USD accounts for nearly 58% of the movement of the USD Index, EUR/USD pain will be the USDX’s gain.

In addition, the top in the FED/ECB total assets ratio preceded the slide in the EUR/USD less than a decade ago, and it seems to be preceding the next slide as well. If the USD Index was to repeat its 2014-2015 rally from the recent lows, it would rally to 114. This level is much more realistic than most market participants would agree on.

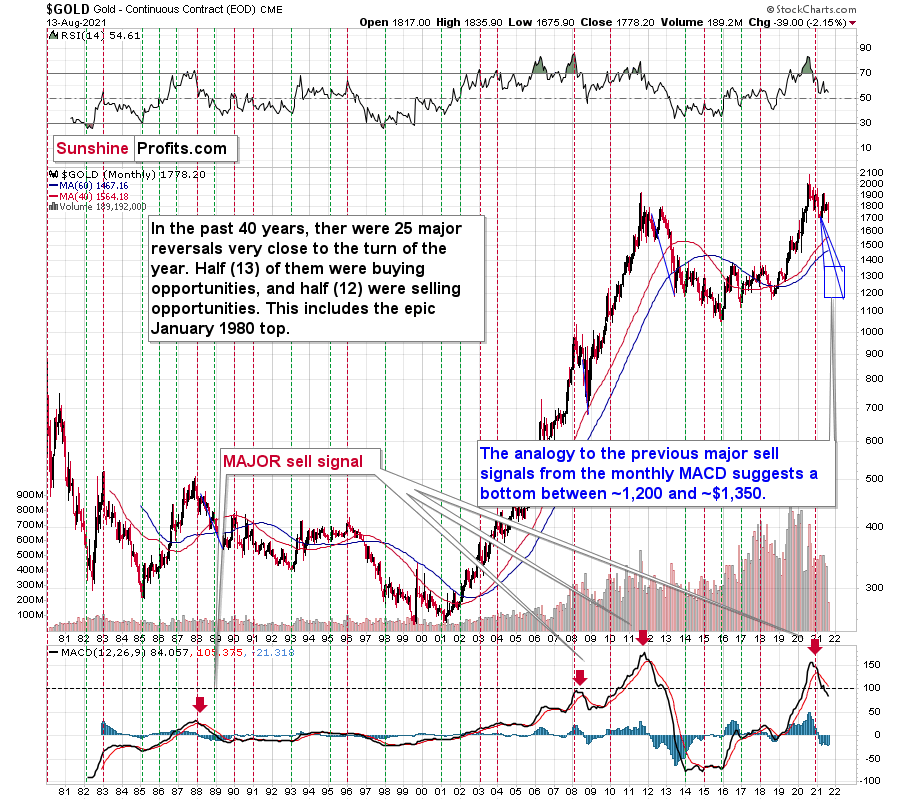

Very Long-Term Indications for Gold

With another month on the books and gold’s back-and-forth behavior whipsawing investors’ emotions, it’s important to remember that the long-term thesis remains intact: the MACD indicator still elicits a strong sell signal and gold’s monthly close has not changed the calculus. As a result, the PMs’ outlook still remains very bearish over the next few months.

To explain, I wrote previously:

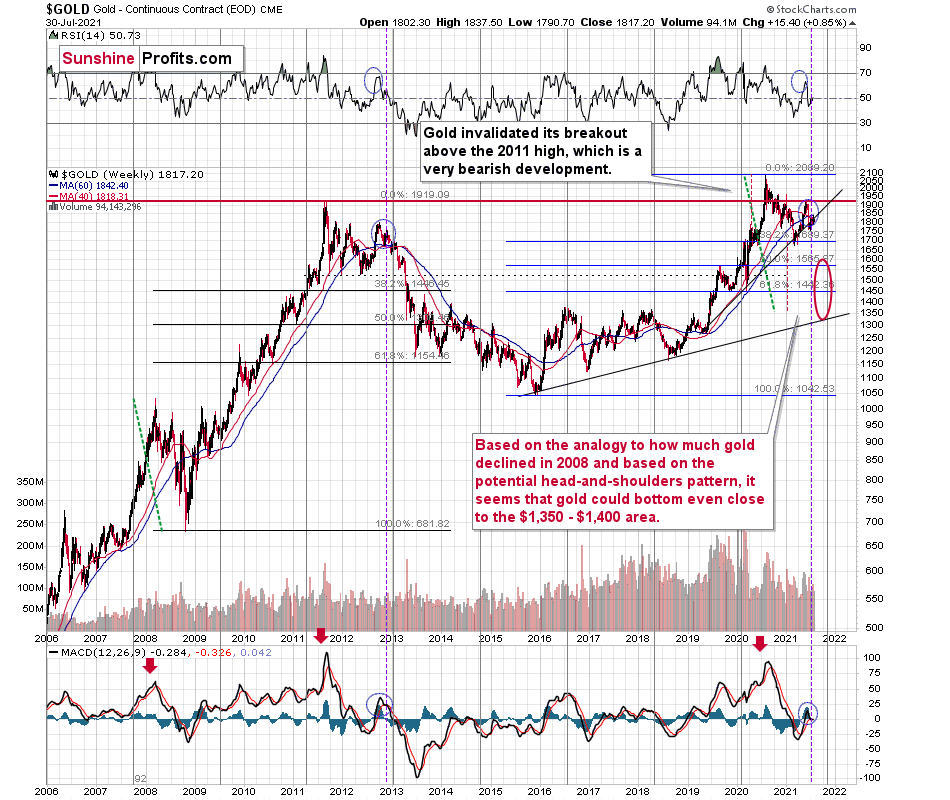

With the month of June now on the books, the MACD indicator is still flashing red. And despite gold’s recent strength and all of the attention that has come with it, the MACD indicator has barely flinched. Furthermore, while a slight pause in the MACD indicator’s downtrend is clearly visible, an identical development also occurred in mid-2012. And what happened then? Well, if you analyze the chart below, you can see that gold’s joy quickly turned into sadness, and the yellow metal suffered a profound decline.

Even eerier, the MACD indicator’s recent pause has occurred at a level that also mirrors the analogue from 2012. And what happened back then? The yellow metal plunged by more than $600 before the bottom was finally reached. Likewise, the current position of the MACD indicator is also symmetrical to the 2008 top. And back then – during the Global Financial Crisis (GFC) – the yellow metal plunged by more than $334 from peak to trough (over 30%).

While short-term price movements often garner the most attention, it’s important to remember that gold’s long-term downtrend is also reminiscent of the second half of 2012. If you analyze the middle-right area of the chart below, you can see that the MACD indicator sounded the alarm in 2012. And while investors ignored the warning and gold moved higher, a profound plunge followed in 2013. Moreover, while the MACD indicator’s sell-signal was visible throughout gold’s entire journey – despite several ebbs and flows in the price action – the narrowing distance between the black and red lines actually preceded gold’s plunge. Thus, with gold’s swan song beginning to play at nearly the same level in 2013, the yellow metal’s recent strength is likely only the intermission.

The above-mentioned narrowing distance between the MACD lines can be seen clearly seen through the blue bars hovering around the 0 level on the indicator part of the chart. We now see the current blue bar move toward 0. We saw the same thing in the second half of 2012, which is when gold rallied for the last time before the huge slide.

Remember the huge gap between the U.S. 10-Year Treasury yield and the U.S. 10-Year breakeven inflation rate? The situation in the very long-term MACD indicator is yet another confirmation that what we saw recently is similar to what we saw before the huge 2012 – 2013 slide. We get the same confirmation from the gold to bonds ratio, and I’ll move to that a bit later.

Based on gold’s previous performance after the major sell signals from the MACD indicator, one could now expect gold to bottom in the ~$1,200 to ~1,350 range. Given the price moves that we witnessed in 1988, 2008 and 2011, historical precedent implies gold forming a bottom in this range. However, due to the competing impact of several different variables, it’s possible that the yellow metal could receive the key support at a higher level.

Considering the reliability of the MACD indicator as a sell signal for major declines, the reading also implies that gold’s downtrend could last longer and be more severe than originally thought. As a result, $1,500 remains the most likely outcome, with $1,350 still in the cards.

Circling back to the Global Financial Crisis (GFC), if you focus your attention on the monthly price action in 2008, epic volatility coincided with the yellow metal’s fall from grace. Conversely, in 2012, gold’s initial decline was relatively muted before the climax unfolded. As a result, whether the yellow metal runs or walks toward its medium-term demise, the recent price action is perfectly normal given the historical similarities. Namely, the volatility was significant but not as extreme as in 2008.

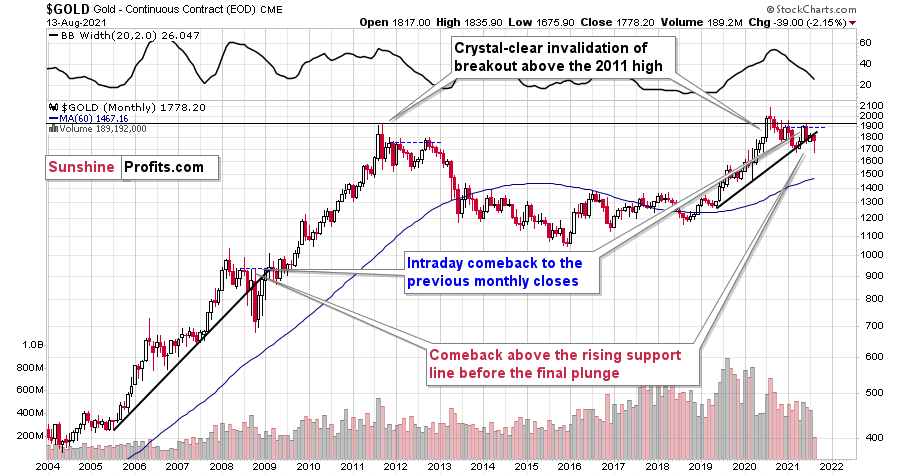

Moreover, while gold staged a comeback last week, the yellow metal is still down by $39 for the month, and the recent rally did not invalidate the breakdown below its rising support line (the black line on the right side of the chart below). As a result, the bearish medium-term implications remain intact.

Please see below:

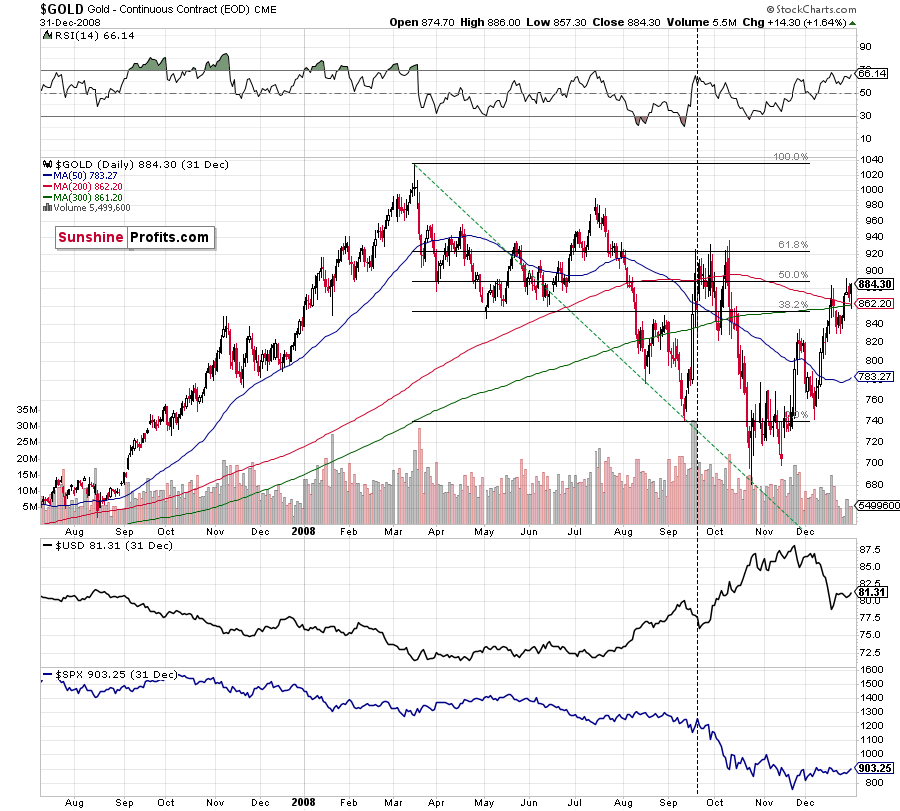

To explain, after making a new all-time high in 2008 (that was a breakout above the 1980 tops), gold declined back to its rising support line before recording a short-term corrective upswing. This upswing ended approximately at gold’s previous monthly closing price. I marked it with a horizontal, blue, dashed line.

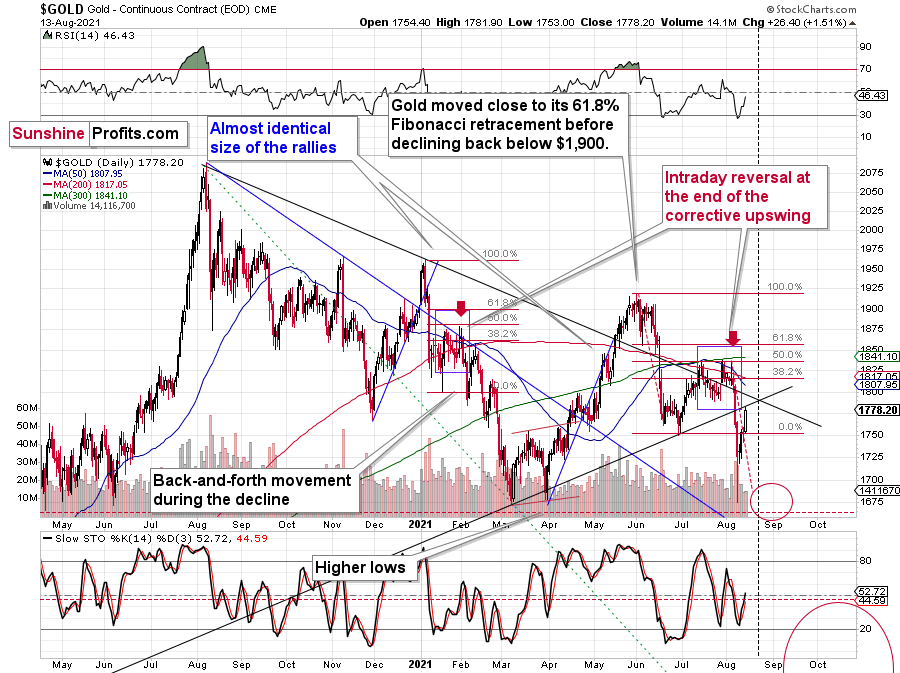

Similarly, if you analyze the right side of the chart, you can see that an identical pattern has emerged. With gold’s corrective upswing following a reconnection with its rising support line, history implies that a sharp decline should occur in the coming months and that the reversal is at hand or already behind us. After all, the thing that triggered the decline almost a year ago was the fact that gold made a new all-time high. Moreover, the recent high was very close to the previous high in terms of the monthly closing prices (Dec. 2020 - $1,895.10 vs. the recent intraday high of $1,915.60).

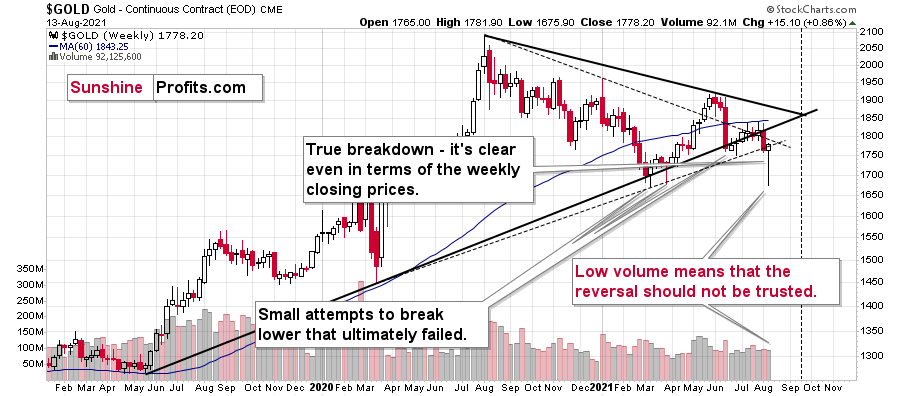

As further evidence, the breakdown is even clearer when we zoom in on the weekly chart. If you analyze the weakness below, you can see that the yellow metal remains firmly below the thick black line. Moreover, while gold rose slightly above the dashed rising support line (which connects the intraday lows), the latter is not as important as the former. More importantly, though, major reversals are validated when they occur on high volume. And given the minimal euphoria that we witnessed last week, the bullish fervor simply wasn’t there. Thus, while the yellow metal recorded a bullish hammer (reversal) candlestick last week – which often predicts trend reversals – the relatively weak volume should make one not accept the bullish candlestick at its face value. Especially that other markets didn’t confirm gold’s reversal.

What’s more, despite the ‘flash crash’ and all of the volatility that surrounded the precious metals last week, gold only rose by ~$15. And with gold mining stocks drastically underperforming the yellow metal – which is one of the most important indicators of medium-term declines – the relative weakness signals that lower lows will likely materialize over the next few weeks/months.

Please see below:

Likewise, gold’s weekly chart depicts the validity of the 2012 analogue. Whether it’s the RSI indicator (as visible on the chart below), the MACD indicator or the overall price action, the readings are profoundly similar, and the bearish implications remain intact.

To explain further, gold’s behavior is mirroring what we witnessed near the end of 2012. For example, following gold’s short-term corrective upswing nearly a decade ago, the yellow metal proceeded to fall off a cliff. And with the shape, the RSI, and the MACD indicators sending the same bearish signals that we witnessed back then (marked with the purple vertical lines and blue ellipses below), if it looks like a duck, swims like a duck and quacks like a duck, then it’s probably a duck.

Furthermore, the recent breakdown also aligns with gold’s self-similar pattern from 2011 to 2013. For example, since we’re right after the point marked with the vertical purple line below, gold should now decline to its previous lows, correct, and then continue its medium-term slide. Likewise, with the duration of the analogue aligning as well, it took 56 weeks for gold to make an initial high and then form a final high from 2011-2013. And since we’re in the midst of a 43-week (76.8% of the 2011-2013 duration) top-to-top pattern, an interim bottom should (assuming that the 76.8% proportion in terms of time remains in place) form in mid-September (which also aligns with gold’s triangle-vertex-based reversal point that was mentioned above) and the final bottom should present itself in mid or late December.

Please see below:

If you analyze the long-term chart above, you can see that gold has invalidated the breakout above its 2011 high. More importantly, though, with its rising support line (on the right side of the chart) also coinciding with the 61.8% Fibonacci retracement level and the 2019 and 2020 lows, ~$1,450 to $1,500 is the most prudent medium-term price target.

Conversely, if the 2008 analogue repeats – and a crisis of confidence erupts across U.S. equities – the PMs could move substantially lower. When combining an equity shock with an USD Index’s resurgence, the yellow metal could bottom at roughly $1,400 (or even ~$1,350). Similarly, while the MACD indicator (on gold’s 40-year chart near the top of today’s edition) signals a bottom in the ~$1,200 to ~1,350 range, to be perfectly clear, ~$1,450 to $1,500 is the most likely outcome.

If you analyze the red arrow in the lower part of the above chart (the weekly MACD sell signal), today’s pattern is similar not only to what we saw in 2011, but also to what we witnessed in 2008. Thus, if similar events unfold – with the S&P 500 falling and the USD Index rising (both seem likely for the following months, even if these moves don’t start right away) – the yellow metal could plunge to below $1,350 or so. The green dashed line shows what would have happened to the gold price if it had not declined as much as it did in 2008.

In addition, relative to 2011-2013, today’s price action is also a splitting image. For starters, gold invalidated the breakout above its 2011 highs. Invalidations of breakouts are sell signals, and it’s tough to imagine a more profound breakout that could have failed.

Furthermore, if you analyze the right side of the chart above (the bottom section), you can see that the MACD indicator has sprouted a tiny weekly buy signal. However, it’s important to remember that the same signal emerged in mid-2008 – which confirmed the previous rally but had no bullish implications for the future. Case in point: following the reading in 2008, gold’s volatility increased, and the yellow metal suffered several declines before finding a lasting bottom in 2009. Thus, the recent reading is nothing to write home about. I marked both cases with red, dashed lines.

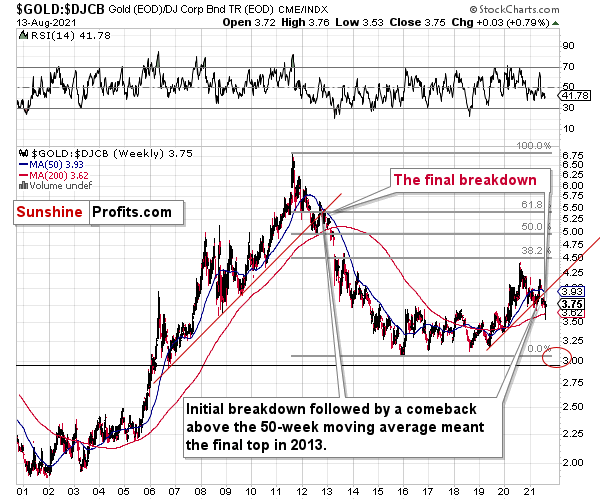

If that wasn’t enough, the gold/ Dow Jones Corporate Bond Index (Total Return) ratio has fallen below its rising support line. And when this occurred in 2012, the most violent part of gold’s decline was already underway.

Please see below:

To explain, if you analyze the middle of the chart above, you can see that the ratio recorded a countered rally, jumped back above its rising support line and 50-week moving average and then… collapsed. And with a similar pattern forming on the right side of the chart, the ratio is looking more and more like a widow-maker. Furthermore, when factoring in mining stocks’ bearish H&S patterns, the fundamental headwinds confronting gold and the strong likelihood of a medium-term swoon in the stock market, you can already hear the yellow metal’s death knell tolling in the distance.

Gold’s Short-and-Medium-Term Outlook

On the surface, gold’s late-week surge may seem quite sanguine. In fact, the yellow metal actually invalidated the breakdown below its June lows. However, with the relief rally occurring on relatively weak volume and gold’s RSI also oversold at the time, the yellow metal’s spike was likely a corrective upswing and not a regime change. Case in point: gold mining stocks declined last week, and silver couldn’t recover from the Aug. 8 ‘flash crash’ (ending the week down by more than 2%; below its previous yearly lows). Likewise, several countertrend rallies that occurred in early 2021 (particularly, in February) also culminated with lower lows over the medium term.

The bottom line? Late August and mid-September remain the most likely timeframes for reversals. And the latter seems more likely to correspond to the important bottom that would be followed by another counter-trend upswing. The important point is that the yellow metal remains poised to fall below its 2021 lows over the medium term.

Please see below:

To explain, I previously wrote multiple times that the gold market seems to really want to decline. As always, context is important. And this time, the context is provided by two similar situations: one from February and one from June. Back in February (marked with a red ellipse), when gold was right after a breakdown below the previous lows, it moved back up quickly after the initial slide. This didn’t mean that the decline ended. Consequently, seeing something similar this time shouldn’t make one think that the decline is over.

The most recent case when gold plunged was the fall in June. That’s when the yellow metal declined below $1,800. Right after the most volatile part of the decline, it moved back up, but that was not the true bottom. Gold continued to move lower after a quick breather, and it bottomed less than two weeks later.

All in all, based on both the above-mentioned analogies and on the triangle-vertex-based reversal, it seems quite likely that we’ll see a short-term bottom in the PMs and miners in the second half of August.

Also, let’s keep in mind that while gold corrected in June, junior gold miners really didn’t – they declined in a much steadier manner.

Moreover, let’s keep in mind that the yellow metal is also following the ominous roadmap from 2012. For example, if we break out the measuring tape and analyze the shape and the length of gold’s price action back then and compare it with today, it’s a tailored fit. Furthermore, the timeframe of the initial decline in 2012 approximately mirrored the length of the consolidation that followed. We see the same thing today – gold has been consolidating for more or less as long as it had been declining.

To explain, I wrote previously:

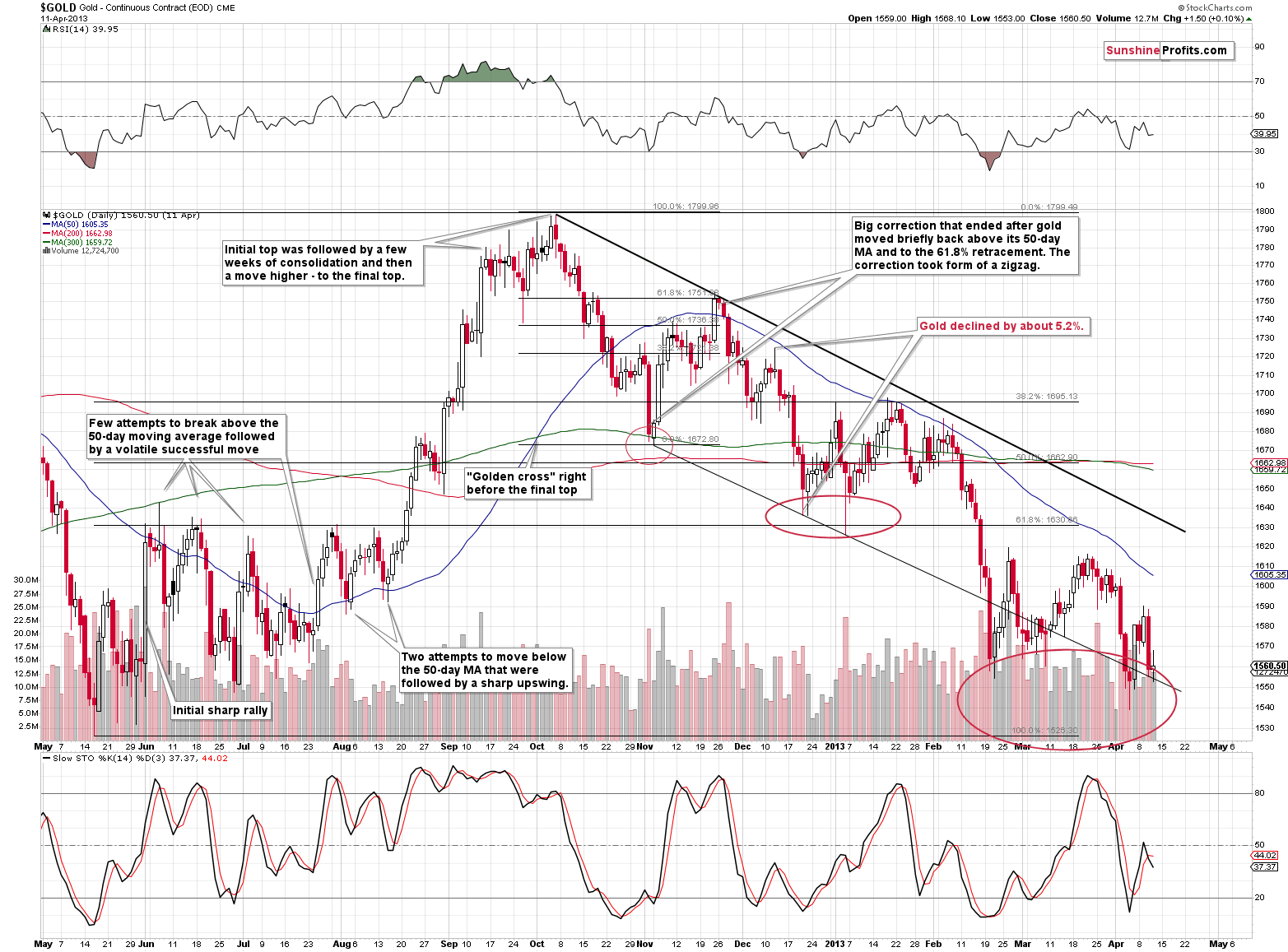

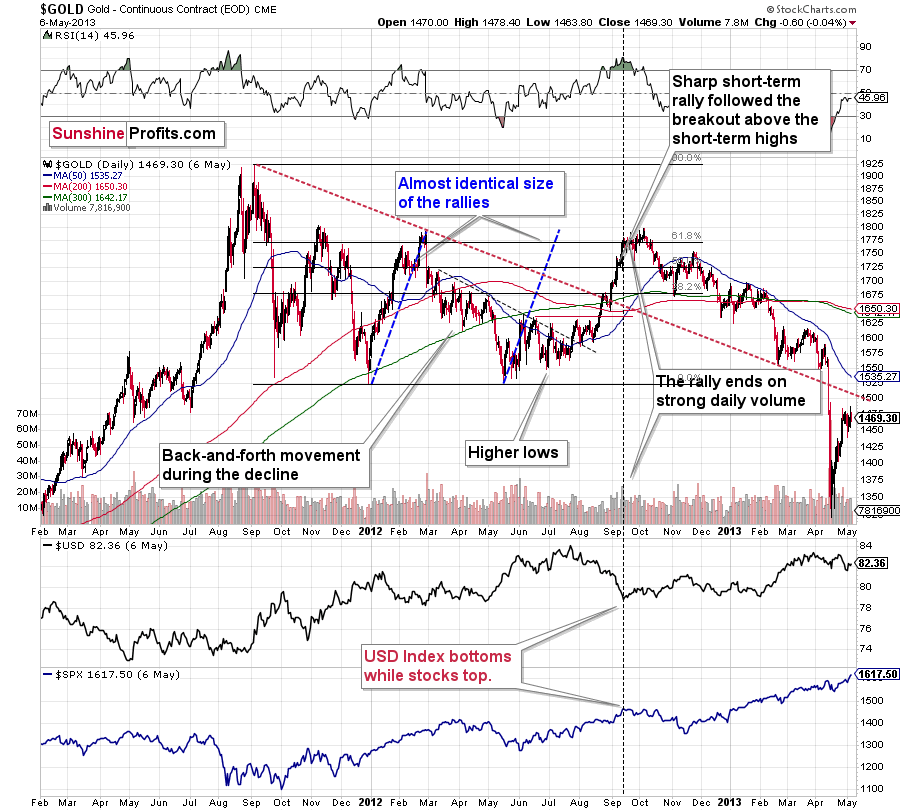

Gold’s recent relief rallies are barely visible on the daily chart. And while the yellow metal garnered strong support following the initial collapse in 2012 (rallying first to its 50% Fibonacci retracement, and then to the 61.8% Fibonacci retracement), today supporters are nowhere to be found (as evidenced by the tepid consolidation on the right side of the chart below). This tells us that the gold market is much weaker right now than it was in 2012 and 2013. As a result, the medium-term outlook remains profoundly bearish.

On top of that, following a bounce in 2012, gold suffered one of its most meaningful historical drawdowns. For context, I’m excluding the 2008 analogy here because the level of volatility during the 2008 financial crisis has yet to materialize across the financial markets. Also, please note that the chart ends where a really huge decline starts, so the real follow-up is much more bearish than it seems based on the chart alone.

Furthermore, if you analyze the bottom-right side of the chart below (marked with a large ellipse), you can see that in February 2013, gold recorded a corrected upswing following its initial plunge. Thereafter, gold fell back near its previous lows before recording another short-term upswing. However, after the dust settled, the yellow metal plunged once again and made lower lows. As a result, the back-and-forth movement that we’re witnessing today is perfectly normal and quite similar to 2013. And again, while gold recovers more of its decline, gold mining stocks haven’t been as lucky. And because our short position is in the GDXJ ETF, the underperformance of the gold miners is what matters the most.

Please see below:

To explain, back in 2012, gold wasn’t confronted with a failed breakout of its previous highs. However, with the yellow metal unable to hold its August 2020 highs and maintain the breakout above its 2011 peak, even a fire hose of liquidity from the Fed couldn’t sustain the optimism. Thus, after gold corrected roughly half of its initial decline and then proceeded to rally back to the 61.8% Fibonacci retracement level in 2012, the recovery was much stronger. This time is different – the yellow metal hasn’t risen visibly above its intraday lows to date. As a result, the outlook is even more bearish now than it was then.

For more on the 2008 and 2012 analogies (key factors for the medium-term outlook), I wrote on Jun. 4:

The analogies to how the situation in gold developed in 2008 and 2012, provides us with an extremely bearish price prediction for gold. Many other factors are pointing to these similarities, and two of them are the size of the correction relative to the preceding decline and to the previous rally. In 2012 and 2008, gold corrected to approximately the 61.8% Fibonacci retracement level. Gold was very close to this level this year, and since the history tends to rhyme more than it tends to repeat itself to the letter, it seems that the top might already be in.

In both years, 2008 and 2012, there were three tops. Furthermore, the rallies that took gold to the second and third top were similar. In 2008, the rally preceding the third top was bigger than the rally preceding the second top. In 2012, they were more or less equal. I marked those rallies with blue lines in the above chart – the current situation is very much in between the above-mentioned situations. Also, the current rally is bigger than the one that ended in early January 2021 but not significantly so.

Remember what happened when gold previously attempted to break above major long-term highs? It was in 2008 and gold was breaking above its 1980 high. Gold wasn’t ready to truly continue its bull market without plunging first. This downswing was truly epic, especially in the case of silver and mining stocks; and now even gold’s price patterns are like what we saw in 2008.

My previous comments on the analogies to 2008 and 2012 remain up-to-date:

Back in 2008, gold corrected to 61.8% Fibonacci retracement, but it stopped rallying approximately when the USD Index started to rally, and the general stock market accelerated its decline.

Taking into consideration that the general stock market has probably just topped, and the USD Index is about to rally, then gold is likely to slide for the final time in the following weeks/months. Both above-mentioned markets support this bearish scenario and so do the self-similar patterns in terms of gold price itself.

Moreover, while the pace of gold’s decline in 2012 started off slow, the momentum picked up later on as the drawdown became even more vicious.

Please see below:

The relatively broad bottom with higher lows is what preceded both final short-term rallies – the current one, and the 2012 one. Their shape as well as the shape of the decline that preceded these broad bottoms is very similar. In both cases, the preceding decline had some back-and-forth trading in its middle, and the final rally picked up pace after breaking above the initial short-term high.

Interestingly, the 2012 rally ended on huge volume, which is exactly what we saw also on May 19 this year. Consequently, forecasting much higher silver or gold prices here doesn’t seem to be justified based on the historical analogies.

The thing I would like to emphasize here is that gold didn’t form the final top at the huge-volume reversal on Sep. 13, 2012. It moved back and forth for a while and moved a bit above that high-volume top, and only then the final top took place (in early October 2012).

The same happened in September and in October 2008. Gold reversed on huge volume in mid-September, and it was approximately the end of the rally. The final top, however, formed after some back-and-forth trading and a move slightly above the previous high.

Consequently, the fact that gold moved a bit above its own high-volume reversal (May 19, 2021) is not an invalidation of the analogy, but rather its continuation.

On top of that, with the Fed’s confidence game won or lost by whether or not inflation proves “transitory,” wouldn’t the central bank appreciate lower gold prices? If you think about it, it would be awfully convenient for the price of gold to decline in order to prove the point of the transitory nature of inflation.

Now, as you know, I’m not a fan of all the conspiracy theories that are out there, and I’m not the first to shout gold manipulation or silver manipulation every time the yellow or while metal goes down, but I also know that being realistic is one of my strengths. With the situation being what it is, and since the communities of top investment bankers and the community of officials interlace, I think that we have yet another reason to expect that the gold price is going to slide in the following weeks/months.

Finally, there are more layers to the analogue from 2008 that are extremely important.

Please see below:

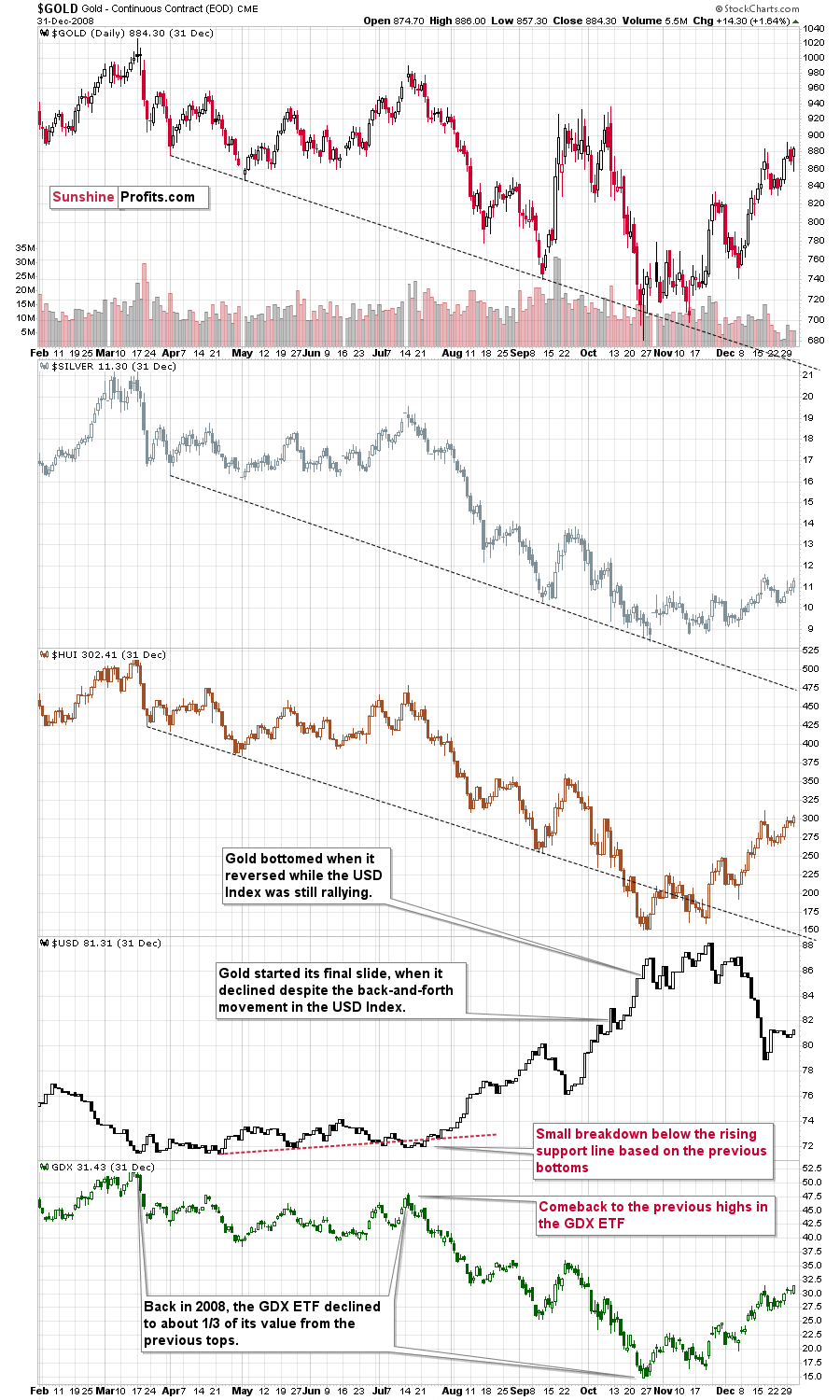

Please note (in the lower part of the above chart) that back then, the final huge slide in the mining stocks started when the GDX ETF moved back to its previous highs, while the USD Index moved a bit below its rising support line based on the previous tops. That’s exactly what happened recently as well. The final bottom in the GDX ETF formed about 3 months later at about 1/3 of its starting price.

The recent high was $40.13 and 1/3 thereof would be $13.38. While I don’t want to say that we will definitely see the GDX ETF as low as that, it’s not something that would be out of the ordinary, given the analogy to 2008. Now you see why the large bottoming target on the GDX ETF chart with the lower border in the $15s might actually be conservative… As always, I’ll keep you – my subscribers – updated.

“Ok, but what price level would be likely to trigger a bigger rebound during the next big slide?”

Well, the 76.4% Fibonacci retracement level (it’s visible as the 23.6% Fibonacci retracement level on the above chart as inverting the scale is used as a workaround) also coincides with gold’s April 2020 low. Taken together, an interim bottom could form in the ~$1,575 to $1,600 range.

For context, back in early March, the yellow metal continued to decline after reaching the 61.8% Fibonacci retracement (visible as 38.2% Fibonacci retracement) level, while, in contrast, the miners began to consolidate. Gold finally bottomed slightly below the retracement – at its previous lows. This time around, we might witness a similar event. And while the story plays out, the miners’ relative strength should signal the end of the slide (perhaps with gold close to 1,600), while gold will likely garner support sometime thereafter (at $1,575 – $1,580 or so).

Remember though: this is only an interim target. Over the medium term, the yellow metal will likely form a lasting bottom in the ~$1,350 to $1,500 range.

The Gold Miners

While gold shrugged off the Aug. 8 ‘flash crash’ and bounced back above its June lows, the yellow metal’s renewed sense of swagger hasn’t been mimicked by its precious metals peers. For example, while gold ended the week up by 0.86%, the GDXJ ETF (our short position) ended the week down by 1.72%.

Please see below:

Furthermore, while gold jumped by roughly $15 last week, the HUI Index declined by five index points. And with the bearish underperformance often a precursor to profound medium-term drawdowns, the precious metals are behaving like its 2012-2013. Last week is yet another confirmation of the analogy.

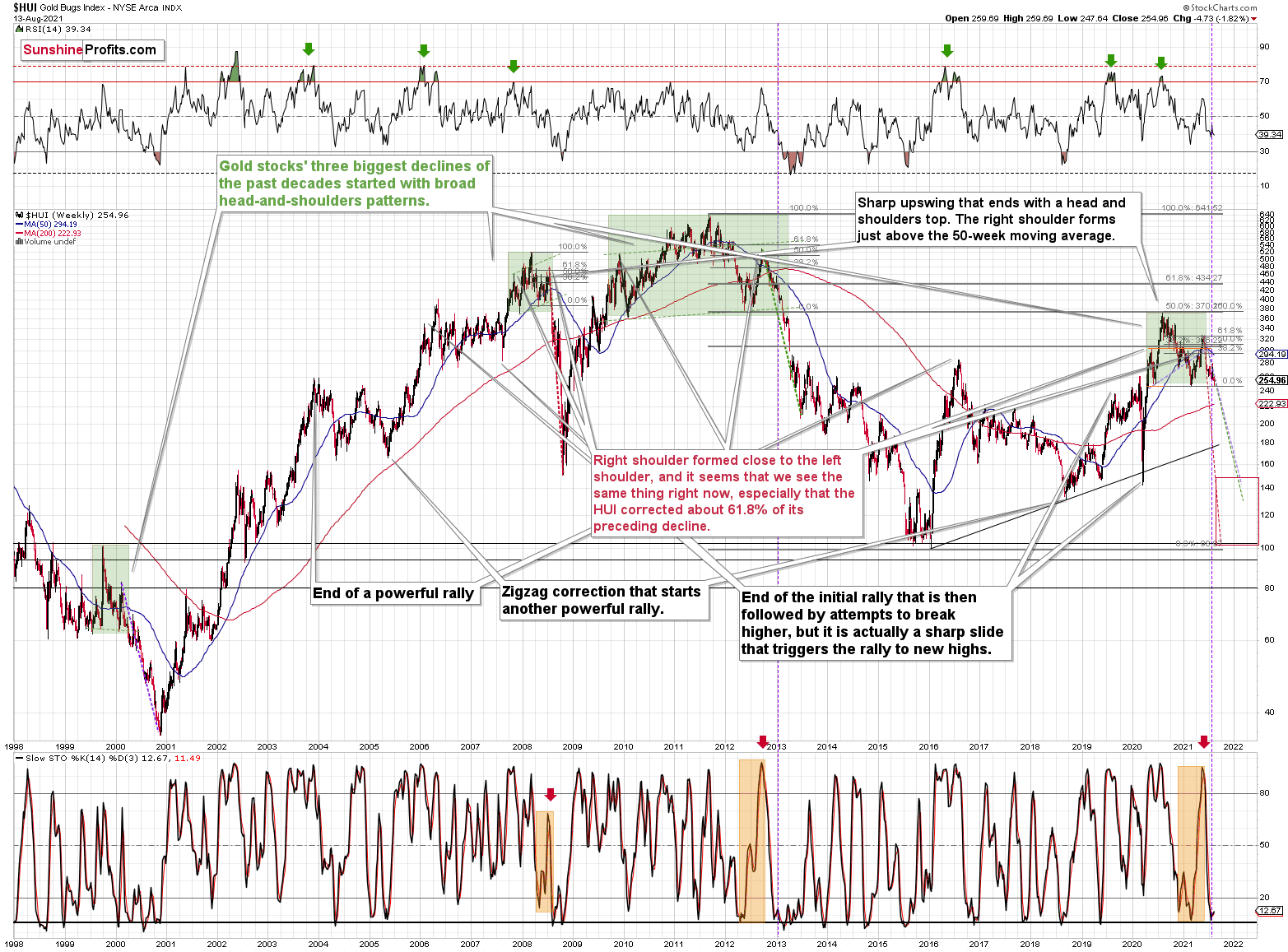

Case in point: after the HUI Index recorded a short-term buy signal in late 2012 – when the index’s stochastic indicator was already below the 20 level (around 10) and the index was in the process of forming the right shoulder of a huge, medium-term head-and-shoulders pattern – the index moved slightly higher, consolidated, and then fell off a cliff.

Please see below:

To explain, can you see the HUI’s rally at the end of 2012 that followed a small buy signal from the stochastic indicator? I marked it with a purple, dashed line. No? That’s because it’s been practically nonexistent. The HUI Index moved higher by so little that it’s impossible to see it from the long-term point of view. On top of that, with the shape of gold’s recent price action, its RSI, and its MACD indicators all mirroring the bearish signals that we witnessed back in December 2012, the current setup signals that we’re likely headed for a similar swoon.

For context, I warned previously that the miners’ drastic underperformance of gold was an extremely bearish sign. I wrote the following about the week beginning on May 24:

(…) gold rallied by almost $30 ($28.60) and at the same time, the HUI – a flagship proxy for the gold stocks… Declined by 1.37. In other words, gold stocks completely ignored gold’s gains. That shows exceptional weakness on the weekly basis and is a very bearish sign for the following weeks.

And why is this quote so important? Well, because the bearish phenomenon still remains intact. As mentioned, with gold rising by roughly $15 and the HUI Index declining by about five index points, the bearish underperformance is accelerating. Precisely, something similar happened during the week beginning on July 6. The gold price rallied by $27.40, and the HUI Index declined by 1.39. As a result, with the HUI Index’s ominous signals still present, if history rhymes (as it tends to), medium-term support will likely materialize in the 100-to-150 range. For context, high-end 2020 support implies a move back to 150, while low-end 2015 support implies a move back to 100. And yes, it could really happen, even though such predictions seem unthinkable.

In addition, the drastic underperformance of the HUI Index also preceded the bloodbath in 2008. To explain, right before the huge slide in late September and early October, gold was still moving to new intraday highs; the HUI Index was ignoring that, and then it declined despite gold’s rally. However, it was also the case that the general stock market suffered materially. If stocks didn’t decline back then so profoundly, gold stocks’ underperformance relative to gold would have likely been present but more moderate.

Nonetheless, bearish head & shoulders patterns have often been precursors to monumental collapses. For example, when the HUI Index retraced a bit more than 61.8% of its downswing in 2008 and in between 50% and 61.8% of its downswing in 2012 before eventually rolling over, in both (2008 and 2012) cases, the final top – the right shoulder – formed close to the price where the left shoulder topped. And in early 2020, the left shoulder topped at 303.02. Thus, three of the biggest declines in the gold mining stocks (I’m using the HUI Index as a proxy here) all started with broad, multi-month head-and-shoulders patterns. And in all three cases, the size of the declines exceeded the size of the head of the pattern.

Furthermore, when the HUI Index peaked on Sep. 21, 2012, that was just the initial high in gold. At that time, the S&P 500 was moving back and forth with lower highs. And what was the eventual climax? Well, gold made a new high before peaking on Oct. 5. In conjunction, the S&P 500 almost (!) moved to new highs, and despite bullish tailwinds from both parties, the HUI Index didn’t reach new heights. The bottom line? The similarity to how the final counter-trend rally ended in 2012 (and to a smaller extent in 2008) remains uncanny.

As a result, we’re confronted with two bearish scenarios:

- If things develop as they did in 2000 and 2012-2013, gold stocks are likely to bottom close to their early-2020 low.

- If things develop like in 2008 (which might be the case, given the extremely high participation of the investment public in the stock market and other markets), gold stocks could re-test (or break slightly below) their 2016 low.

In both cases, the forecast for silver, gold, and mining stocks is extremely bearish for the next several months.

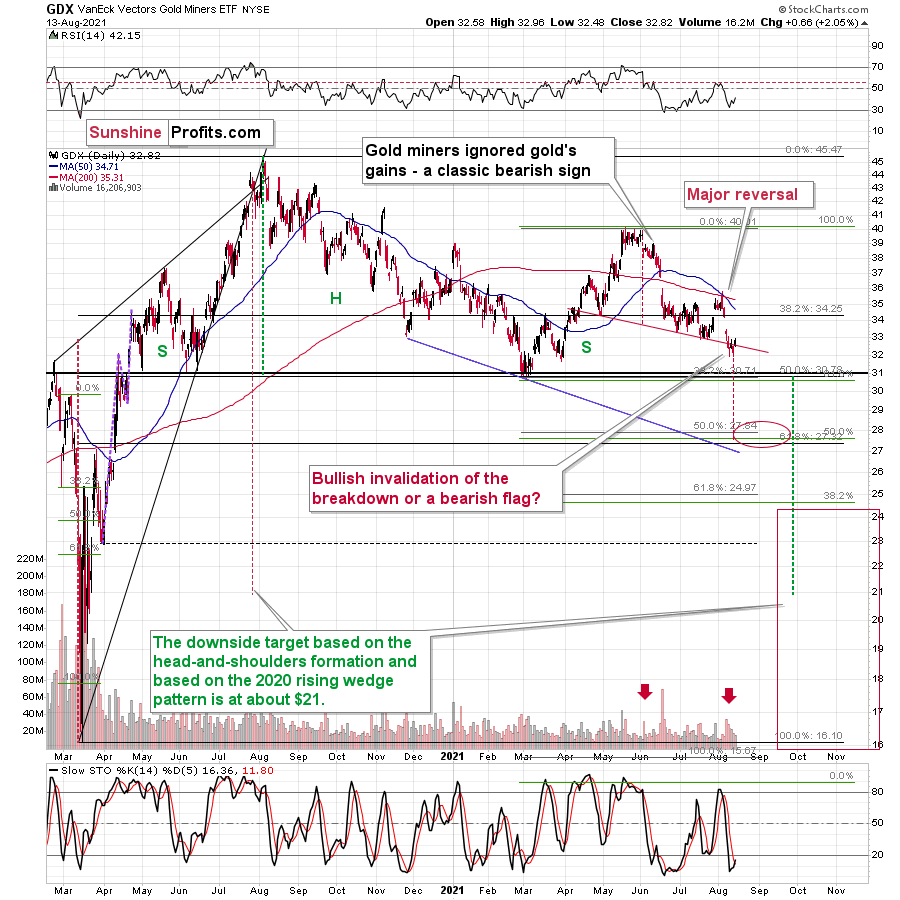

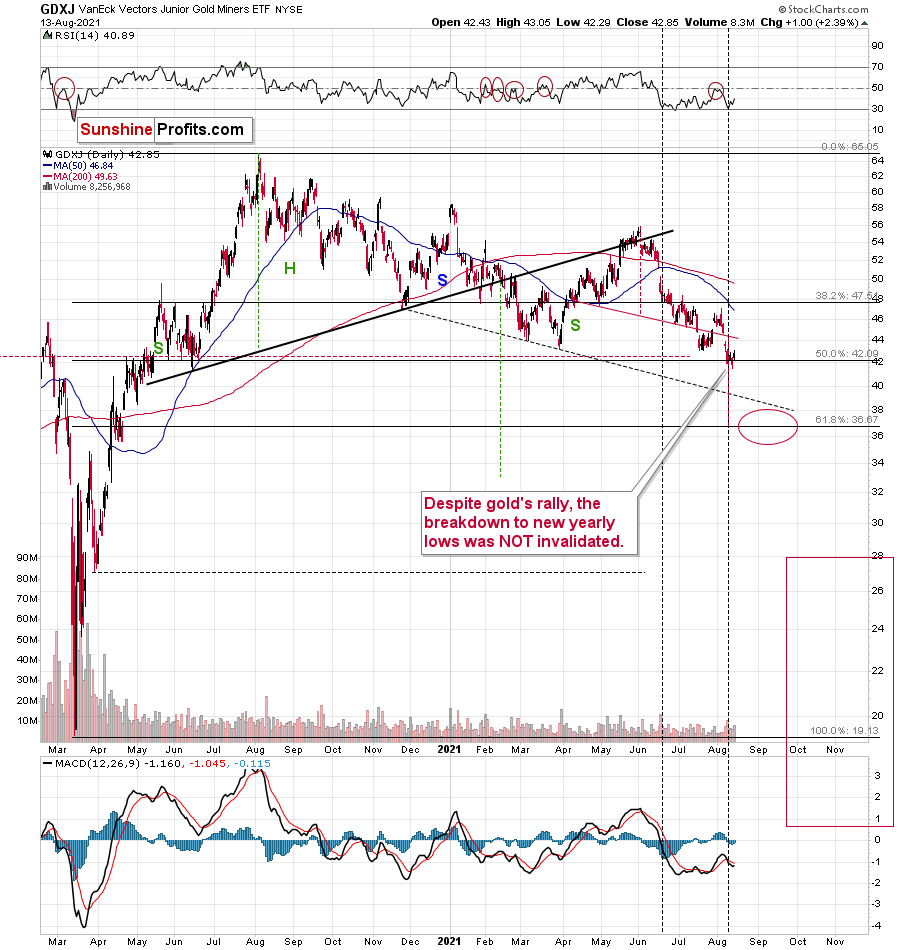

As further evidence, let’s compare the behavior of the GDX ETF and the GDXJ ETF. Regarding the former, the senior miners (GDX) are in the midst of forming an ominous bear flag and the volume that accompanied Friday’s (Aug. 13) corrective upswing was relatively weak and it declined while the flag pattern was formed – just as it should if the formation was valid.

Conversely, the GDX ETF did invalidate the breakdown below the neckline of its bearish H&S pattern (which is a bullish sign). However, the GDXJ ETF did not. And with the junior miners’ initial plunge (the pole) implying a continuation of the downtrend (following a consolidation that forms the flag), there are more indicators weighing down the gold miners than lifting them up.

Please see below:

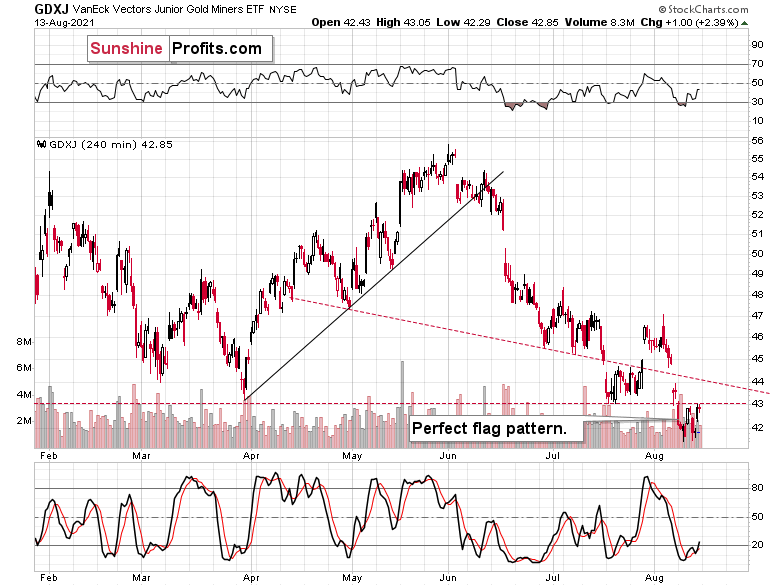

Speaking of the GDXJ ETF, not only are the junior miners lagging behind their senior counterparts, but the four-hour chart provides a clear visual of the initial breakdown and the formation of the current bear flag.

Please see below:

The flag is perfect, and it took place on relatively declining volume, suggesting that another move will also be to the downside. After all, the moves that follow flags tend to be similar to the ones that preceded them.

The price levels at which the flag was formed are also very important, and it’s clearer on the daily chart.

Junior miners broke below the previous 2021 lows, and they held this breakdown, even though gold rallied quite visibly last week. This serves as a great confirmation that the move lower is about to take place.

And how should we expect the climax to unfold? Last week, I wrote the following:

Well, the GDXJ ETF may consolidate in the short term, but lower lows are still likely, and initial support should materialize at roughly $37 (the 61.8% Fibonacci retracement level). Thereafter, a short-term corrective upswing should follow before the GDXJ ETF reverses course once again and records its final bottom near the end of the year – at much, much lower price levels. All in all, it seems that our profits on the GDXJ (short position in it) are going to become MUCH bigger before this decline is over.

The above remains up-to-date. In fact, we already saw the short-term consolidation last week, so the decline could resume any day now.

In conclusion, the gold miners’ continued underperformance of the yellow metal is akin to a fire alarm signaling an impending blaze. And while many investors have forged through the smoke in 2021 and suffered a loss of breath in the process, our medium-term forecast does not change our outlook for gold, silver and mining stocks over the long term. With the trio underpinned by robust long-term fundamentals and their medium-term drawdowns likely to elicit secular buying opportunities, we’re confident that the precious metals will remain atop investors’ wish lists for years to come.

What Links Stocks and Miners?

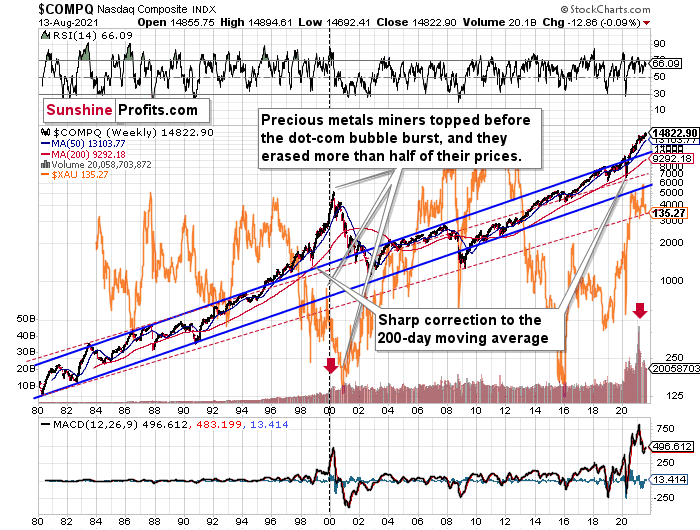

With the MACD indicator recording an epic sell signal, the extreme reading can only be rivaled by the peak of the dot-com bubble.

To explain, I wrote previously:

While history might not repeat itself, though it does rhyme, those who insist on ignoring it are doomed to repeat it. And there’s practically only one situation from more than the past four decades that is similar to what we see right now.

It’s the early 2000s when the tech stock bubble burst. It’s practically the only time when the tech stocks were after a similarly huge rally. It’s also the only time when the weekly MACD soared to so high levels (we already saw the critical sell signal from it). It’s also the only comparable case with regard to the breakout above the rising blue trend channel. The previous move above it was immediately followed by a pullback to the 200-week moving average, and then the final – most volatile – part of the rally started. It ended on significant volume when the MACD flashed the sell signal. Again, we’re already after this point.

The recent attempt to break to new highs that failed seems to have been the final cherry on the bearish cake.

Why should I – the precious metals investor – care?

Because of what happened in the XAU Index (a proxy for gold stocks and silver stocks) shortly after the tech stock bubble burst last time.

What happened was that the mining stocks declined for about three months after the NASDAQ topped, and then they formed their final bottom that started the truly epic rally. And just like it was the case over 20 years ago, mining stocks topped several months before the tech stocks.

Mistaking the current situation for the true bottom is something that is likely to make a huge difference in one’s bottom line. After all, the ability to buy something about twice as cheap is practically equal to selling the same thing at twice the price. Or it’s like making money on the same epic upswing twice instead of “just” once.

And why am I writing about “half” and “twice”? Because… I’m being slightly conservative, and I assume that the history is about to rhyme once again as it very often does (despite seemingly different circumstances in the world). The XAU Index declined from its 1999 high of 92.72 to 41.61 – it erased 55.12% of its price.

The most recent medium-term high in the GDX ETF (another proxy for mining stocks) was at about $45. Half of that is $22.5, so a move to this level would be quite in tune with what we saw recently.

And the thing is that based on this week’s slide in the NASDAQ that followed the weekly reversal and the invalidation, it seems that this slide lower has already begun.

“Wait, you said something about three months?”

Yes, that’s approximately how long we had to wait for the final buying opportunity in the mining stocks to present itself based on the stock market top.

The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. Consequently, we might see the next major bottom – and the epic buying opportunity in the mining stocks – about three months after the general stock market tops. The NASDAQ might have already topped, so we’re waiting for the S&P 500 to confirm the change in the trend.

The bottom line?

New lows are likely to complete the GDX ETF’s bearish H&S pattern and set the stage for an even larger medium-term decline. And if the projection proves prescient, medium-term support (or perhaps even the long-term one) will likely emerge at roughly $21.

But why ~$21?

- The target aligns perfectly with the signals from the GDX ETF’s 2020 rising wedge pattern. You can see it in the left part of the above chart. The size of the move that follows a breakout or breakdown from the pattern (breakdown in this case) is likely to be equal (or greater than) the height of the wedge. That’s what the red dashed line marks.

- The broad head-and-shoulders pattern with the horizontal neckline at about $31 points to the $21 level as the likely target.

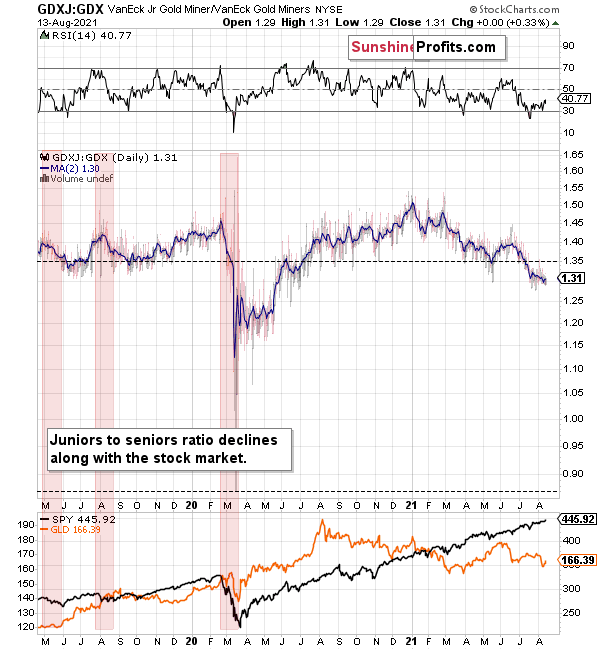

Even more ominous, the GDXJ ETF remains a significant underperformer of the GDX ETF. Despite sanguine sentiment and a strong stock market creating the perfect backdrop for the junior miners, the GDXJ ETF hasn’t lived up to the hype. To that point, it’s important to remember that small fakeouts in the juniors to seniors ratio often occur right before medium-term tops. Why? Because juniors tend to catch up with seniors, somewhat similarly to silver.

In addition, once one realizes that GDXJ is more correlated with the general stock market than GDX is, GDXJ should be showing strength here, and it isn’t. If stocks don’t decline, GDXJ is likely to underperform by just a bit, but when (not if) stocks slide, GDXJ is likely to plunge visibly more than GDX.

Expanding on that point, the GDXJ/GDX ratio has been declining since the beginning of the year, which is remarkable because the general stock market hasn’t plunged yet. However, if the S&P 500 proceeds to decline, the junior miners will likely underperform the senior miners. As a result, the GDXJ ETF has a lot more room to fall than the GDX ETF.

Please see below:

Why haven’t the juniors been soaring relative to senior mining stocks? What makes them so special (and weak) right now? In my opinion, it’s the fact that we now – unlike at any other time in the past – have an asset class that seems similarly appealing to the investment public. Not to everyone, but to some. And this “some” is enough for juniors to underperform.

Instead of speculating on an individual junior miner making a killing after striking gold or silver in some extremely rich deposit, it’s now easier than ever to get the same kind of thrill by buying… an altcoin (like Dogecoin or something else). In fact, people themselves can engage in “mining” these coins. And just like bitcoin seems similar to gold to many (especially the younger generation) investors, altcoins might serve as the “junior mining stocks” of the electronic future. At least they might be perceived as such by some.

Consequently, a part of the demand for juniors was not based on the “sympathy” toward the precious metals market, but rather on the emotional thrill (striking gold) combined with the anti-establishment tendencies (gold and silver are the anti- metals, but cryptocurrencies are anti-establishment in their own way). And since everyone and their brother seem to be talking about how much this or that altcoin has gained recently, it’s easy to see why some people jumped on that bandwagon instead of investing in junior miners.

This tendency is not likely to go away in the near term, so it seems that we have yet another reason to think that the GDXJ ETF is going to move much lower in the following months – declining more than the GDX ETF. The above + gold’s decline + stocks’ decline is truly an extremely bearish combination, in my view.

So, how low could the GDXJ ETF go?

Well, absent an equity rout, the juniors could form an interim bottom in the $34 to $36 range. Conversely, if stocks show strength, juniors could form the interim bottom higher, close to the $42.5 level. For context, the above-mentioned ranges coincide with the 50% and 61.8% Fibonacci retracement levels and the GDXJ ETF’s previous highs (including the late-March/early-April high in case of the lower target area). Thus, the S&P 500 will likely need to roll over for the weakness to persist beyond these levels.

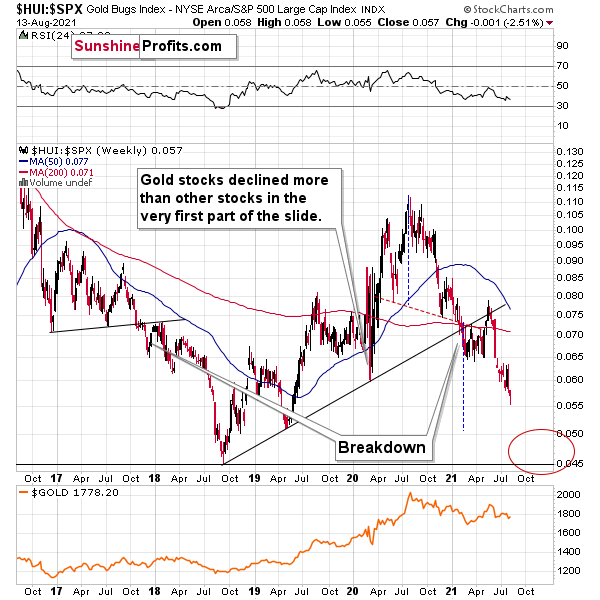

In addition, I warned on Jun. 1 that the HUI Index/S&P 500 ratio invalidation of the breakdown below its rising support line (which became resistance) would be short-lived.

I wrote:

[The invalidation] doesn’t outweigh the myriad of other indicators – both technical and fundamental – that signal further weakness. In other words, the ratio should move back below its rising support/resistance line shortly.

And going from “maybe” to “likely” to “happened” once again, the HUI Index/S&P 500 ratio is now back in the bearish zone. Moreover, after the ratio made another new low last week (and is also firmly below its 2020 low), the weakness has removed any doubt about the gold miners’ profound underperformance. Thus, the medium-term implications remain extremely bearish.

Please see below:

On top of that, the countertrend upswing actually mirrored the behavior that we witnessed in 2018. If you analyze the left side of the chart, you can see that the ratio flirted with its rising support line before eventually rolling over. And with the current price action looking eerily similar, the ratio’s final act could be just as painful.

For more context:

When the ratio presented on the above chart above is rising, it means that the HUI Index is outperforming the S&P 500. When the line above is falling, it means that the S&P 500 is outperforming the HUI Index.

The target for the ratio based on this formation is at about 0.05 (slightly above it). Consequently, if the S&P 500 doesn’t decline, the ratio at 0.05 would imply the HUI Index at about 196. However, if the S&P 500 declined to about 3,200 or so (its late-2020 lows) and the ratio moved to about 0.05, it would imply the HUI Index at about 160 – very close to its 2020 lows.

All in all, the implications of mining stocks’ relative performance to gold and the general stock market are currently bearish.

But if we’re headed for a GDX ETF cliff, how far could we fall?

Well, there are three reasons why the GDX ETF might form an interim bottom at roughly ~$27.50 (assuming no big decline in the general stock market):

- The GDX ETF previously bottomed at the 38.2% and 50.0% Fibonacci retracement levels. And with the 61.8% level next in line, the GDX ETF is likely to garner similar support.

- The GDX ETFs late-March 2020 high should also elicit buying pressure.

- If we copy the magnitude of the late-February/early-March decline and add it to the early-March bottom, it corresponds with the GDX ETF bottoming at roughly $27.50.

Keep in mind though: if the stock market plunges, all bets are off. Why so? Well, because when the S&P 500 plunged in March 2020, the GDX ETF moved from $29.67 to below $17 in less than two weeks. As a result, U.S. equities have the potential to make the miners’ forthcoming swoon all the more painful.

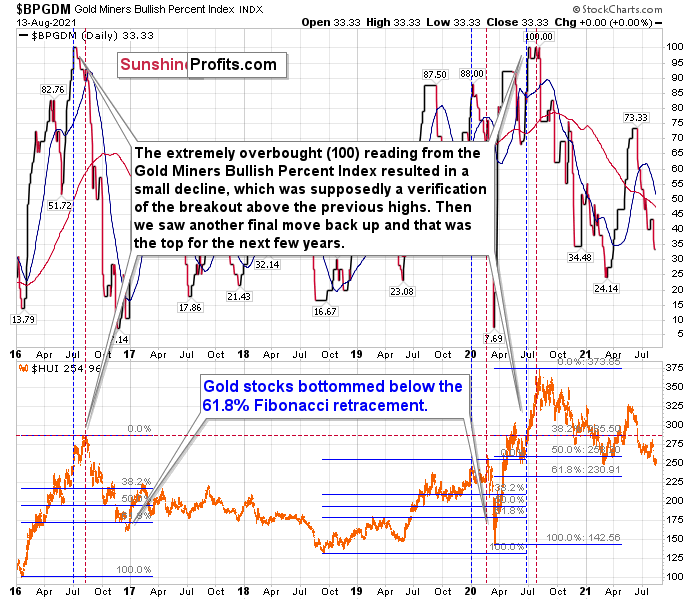

As another reliable indicator (in addition to the myriads of signals coming not only from mining stocks, but from gold, silver, USD Index, stocks, their ratios, and many fundamental observations) the Gold Miners Bullish Percent Index ($BPGDM) isn’t at levels that trigger a major reversal. The Index is now at 33. However, far from a medium-term bottom, the latest reading is still more than 23 points above the 2016 and 2020 lows.

Back in 2016 (after the top), and in March 2020, the buying opportunity didn’t present itself until the $BPGDM was below 10.

Thus, with the sentiment still relatively elevated, it will take more negativity for the index to find the true bottom.

The excessive bullishness was present at the 2016 top as well, and it didn’t cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

Please note that back in 2016, there was an additional quick upswing before the slide, and this additional upswing had caused the $BPGDM to move up once again for a few days. It then declined once again. We saw something similar also in the middle of 2020. In this case, the move up took the index once again to the 100 level, while in 2016 this wasn’t the case. But still, the similarity remains present.

Back in 2016, when we saw this phenomenon, it was already after the top and right before the big decline. Based on the decline from above 350 to below 280, we know that a significant decline is definitely taking place.

But has it already run its course?

Well, in 2016 and early 2020, the HUI Index continued to move lower until it declined below the 61.8% Fibonacci retracement level. The emphasis goes on “below” as this retracement might not trigger the final bottom. Case in point: back in 2020, the HUI Index undershot the 61.8% Fibonacci retracement level and gave back nearly all of its prior rally. And using the 2016 and 2020 analogues as anchors, this time around, the HUI Index is likely to decline below 231. In addition, if the current decline is more similar to the 2020 one, the HUI Index could move to 150 or so, especially if it coincides with a significant drawdown of U.S. equities.

With all of that said: how will we know when a medium-term buying opportunity presents itself?

I view price target levels as guidelines and the same goes for the Gold Miners Bullish Percent Index (below 10), but the final confirmation will likely be gold’s strength against the ongoing USDX rally. At many vital bottoms in gold, that’s exactly what happened, including the March bottom.

Silver

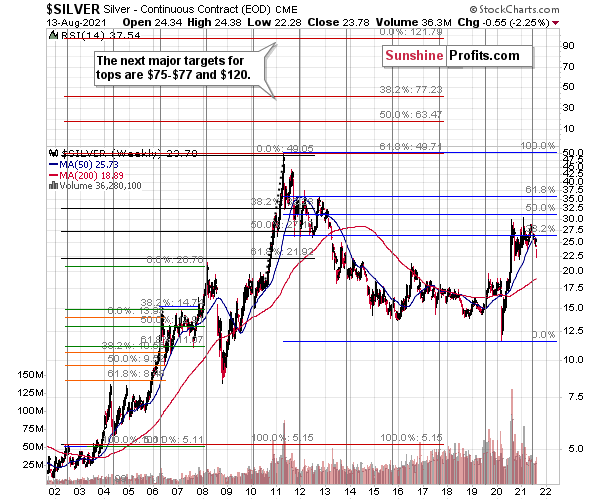

With silver’s long-term cycle implying a surge above $75 (and even $100) over the next several years, the white metal’s secular uptrend remains intact. However, with an epic collapse likely to precede the forthcoming Renaissance, volatility presents us with ample opportunities.

Case in point: silver cycles last roughly two years and the turning points culminate with extreme volatility in both directions. Sometimes ferocious rallies follow, and other times the white metal falls off a cliff. In the here and now, with silver approaching the end of its current cycle, a supreme climax could be around the corner. Moreover, when we combine the myriad of technical and fundamental indicators signaling the same outcome, the white metal could get cut in half over the next few months.

Please see below:

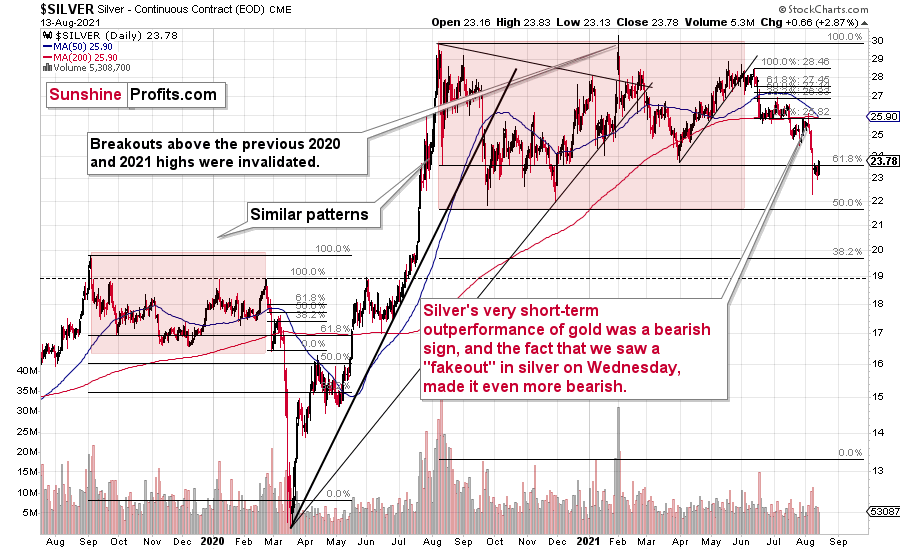

As for the short term, analyzing silver’s historical fakeouts has proven quite valuable. For example, while many investors chase the white metal’s upward momentum only to find little light at the end of the tunnel, I’ve warned on several occasions that falling for the seduction is an extremely costly mistake.

And last week, while gold’s performance was a major outlier, silver did not invalidate the breakdown below its 2021 lows, and similar to the gold miners, the white metal did not elicit any material optimism. As a result, further drawdowns are likely to materialize over the medium term.

To clarify: in my view, silver is very likely to soar in the following years, but timing matters, and ignoring cycles, trends, and technical patterns is what could make people lose a lot of capital.

To explain, I wrote on Aug. 2:

As far as silver is concerned, the situation is also developing just as I described previously:

(…)

Silver moved to its recent short-term high while gold is not even close to being halfway back up. This means that on a very short-term basis, silver is clearly outperforming gold.

This is also what tends to happen shortly before significant declines across the precious metals sector.

Now, the sizes of both moves were not that significant, so this performance could also be more or less random, and, if that was the case, the outperformance would be just accidental. Consequently, it’s not a game-changing signal in terms of its importance. It is something that’s on top of multiple other indications that we have, and the most important ones are not of a short-term nature at all. The long-term self-similarities in gold and the HUI Index (gold stocks) are the true key to understanding where the precious metals sector is likely to head next, and you already know about those, as I described them thoroughly on Monday.

(…) Not only did the early indications prove to be correct, but we actually saw a fresh sell signal in the form of silver’s “fakeout”.

The white metal appeared to be moving back above its June lows, but it was quickly hammered back down, and it ended the session a bit lower. Invalidations of breakouts are very bearish, and silver is known for breaking above certain resistance levels very briefly (without analogous action in gold and gold stocks) only to invalidate them shortly – and it usually happens right before significant moves to the downside.

The implications are clearly bearish, and, more importantly, it’s not the only confirmation that gold received.

Please note that silver didn’t invalidate its breakdown to new 2021 lows despite gold’s strength last week. Neither silver nor mining stocks confirmed gold’s rally, so it seems that it was gold’s reaction that was fake.

Silver’s confirmed breakdown to new lows is likely to lead it to new lows sooner rather than later, especially given how similar the current situation is to the previous patterns that preceded big declines.

For more context on silver’s self-similarity patterns, I wrote previously:

If you analyze the left side of the chart above, you can see that silver moved back and forth before breaking toward its September highs. However, after failing to complete the milestone, the white metal eventually collapsed. As a result, with the pattern on the right side of the chart eerily similar, investors’ optimism has occurred at what’s likely the worst possible time.

To that point, with its current behavior also mirroring 2008 – where silver fell below and then rallied back above its 50-day MA before plunging – the white metal remains on a journey of self-destruction.

If we zoom in on the white metal’s price action in 2008, you can see that an immaterial bounce also occurred right before silver fell off a cliff.

The final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

Let’s be realistic - so far, the analogy (to what happened in 2019 and 2020) might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

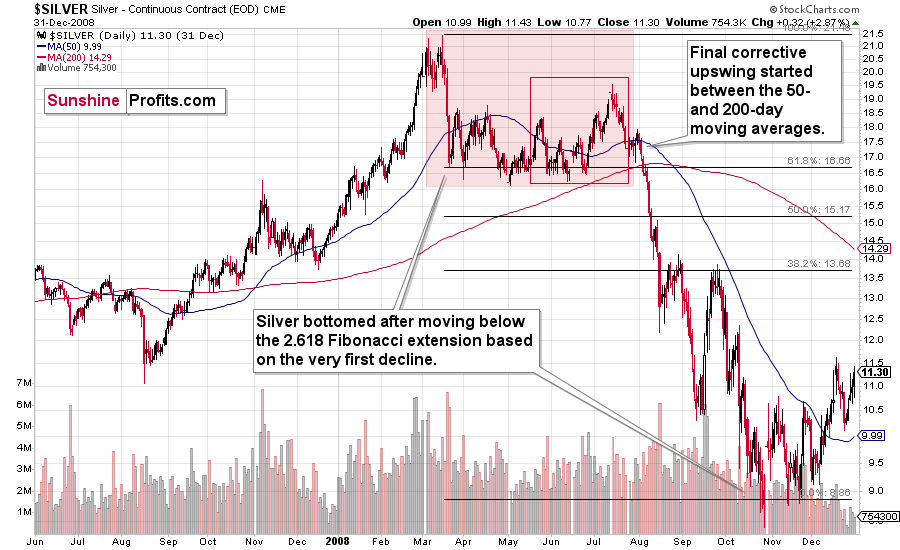

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

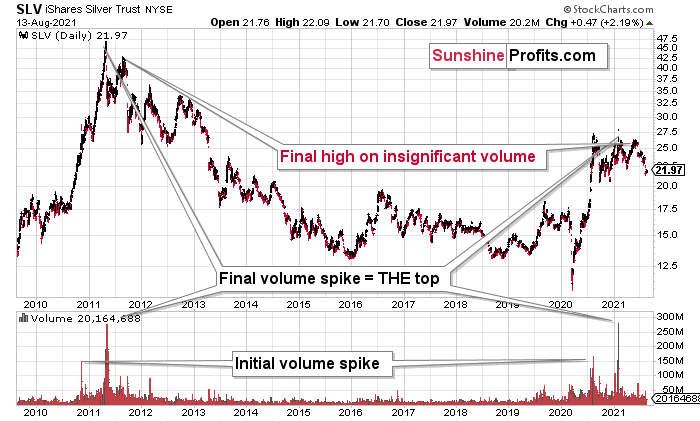

Highlighting the effect of WallStreetBets’ #SilverSqueeze, the SLV ETF’s volume spikes in 2020/2021 were nearly identical to the surges that we witnessed ~10 years ago. If you analyze the chart below, you can see that the massive inflows at the end of 2012 were not the beginning of a medium-term upswing. In fact, they coincided with silver’s final bounce before the white metal suffered a major decline.

Please see below:

If you analyze the volume spikes at the bottom of the chart, 2021 and 2011 are a splitting image. To explain, in 2011, an initial abnormal spike in volume was followed by a second parabolic surge. However, not long after, silver’s bear market began.

SLV-volume-wise, there's only one similar situation from the past - the 2011 top. This is a very bearish analogy as higher prices of the white metal were not seen since that time, but the analogy gets even more bearish. The reason is the "initial warning" volume spike in this ETF. It took place a few months before SLV formed its final top, and we saw the same thing also a few months ago, when silver formed its initial 2020 top.

In addition, the SLV ETF is also following the 2011 playbook. Back then, the SLV ETF recorded an initial spike in price and volume and followed that up with a parabolic spike in both that marked THE top. This was then followed by one last spike in price on relatively average volume. To that point, if you focus your attention on the right side of the chart above, you can see that an identical formation is present. After an initial spike in price and volume, the big one occurred in early 2021. And with silver’s latest rally occurring on relatively average volume, the price action looks a lot like the calm before the 2011 storm.

That third average-volume top in 2011 was the final chance to sell silver above $40 and perhaps to short it. It could be the same right now, but with regard to the $25 price level. Of course, silver is likely to soar well above $50 and $100 in the following years, but currently, the analogy points to lower prices in the medium term.

The history may not repeat itself to the letter, but it tends to be quite similar. And the more two situations are alike, the more likely it is for the follow-up action to be similar as well. And in this case, the implications for the silver price forecast are clearly bearish.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

Similarly, silver’s inverse price action also has bearish implications. Nearly identical to the inverted formation that emerged from 2006 to 2009, today’s chart looks eerily similar to its predecessor.

While it’s more of a wild card, the above pattern shows that silver’s 2020 top plots are nearly identical to the inverse of the 2006-2009 performance. I copied the 2006 – 2009 performance right below the regular price movement and inverted it. I also copied this inverted pattern to the last few years.

The similarity is quite significant. And whenever a given pattern has been repeated, the odds are that it could also repeat in the not-too-distant future. Of course, there is no guarantee for that, but once the same market has reacted in a certain way to a specific greed/fear combination, it can just as well do it again. And these similarity-based techniques work quite often. So, while it’s not strong enough to be viewed as a price-path-discovery technique on its own, it should make one consider some scenarios more closely. In particular, this means that the declines in the prices of silver, gold, and mining stocks could be bigger and take longer than it seems based on other charts and techniques.

The above is also in tune with the implications of the sell signal from the MACD indicator on the monthly gold chart.

The only thing that comes to my mind which could – realistically – trigger such a prolonged decline would be a major drop in the general stock market. Given what I wrote above, the latter is quite possible, so I’ll be on the lookout for confirmations and invalidations of this scenario.

If history rhymes, silver could be in for a profound decline over the next few months (beyond my initial target). Moreover, the development would increase the duration of the precious metals’ bear market (also beyond my initial forecast).

After all, gold did invalidate its long-term breakout above the 2011 highs, and the way gold reacted to a small upswing in the USD Index was truly profound…

Turning to cross-asset correlations, gold, silver and the HUI Index’s 10, 30 and 90-day correlations are performing as expected. The PMs still exhibit strong negative relationships with the U.S. dollar, and that’s what we should expect over the medium term. And with the U.S. dollar in season once again, an uprising could send the PMs running in the opposite direction.

For more context, I wrote previously:

Since gold, silver, and mining stocks have been strongly negatively correlated with the USD Index in the medium term, it seems likely that they will be negatively affected by the upcoming sizable USDX upswing.

…Until we see the day where gold reverses or soars despite the U.S. currency’s rally.

If that happens with gold at about $1,350 - $1,500, we’ll have a very good chance that this was the final bottom. If it doesn’t happen at that time, or gold continues to slide despite USD’s pause or decline, we’ll know that gold has further to fall.

Naturally, we’ll keep you – our subscribers – informed.

Overview of the Upcoming Part of the Decline

- The corrective upswing in gold is over, and the big decline seems to be already underway.

- After miners slide in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this would take place – perhaps with gold close to $1,600. I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,350 - $1,500 and the entire decline (from above $1,900 to about $1,475) would be likely to take place within 6-20 weeks, and I would expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments, in my view. This might also happen with gold close to $1,475, but it’s too early to say with certainty at this time.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

To summarize, the corrective upswing in gold is over, and it seems that the big downswing in gold, silver, and mining stocks is already underway. I previously warned you that “the next few days may (!) bring some back-and-forth action instead of the decline’s continuation,” and I also wrote that it was unlikely that this would take place for long. It seems that it is exactly what happened – we saw some back and forth action, and while gold’s last week’s performance might seem bullish at first glance, neither gold’s volume, nor action in silver nor mining stocks confirm it. In fact, silver’s and junior miners’ breakdowns to new yearly lows were confirmed.