Briefly: in our opinion, full (100% of the regular position size) speculative long positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Practically everything that I wrote yesterday either happened in tune with that or it remains up-to-date, so today’s technical part will be rather brief.

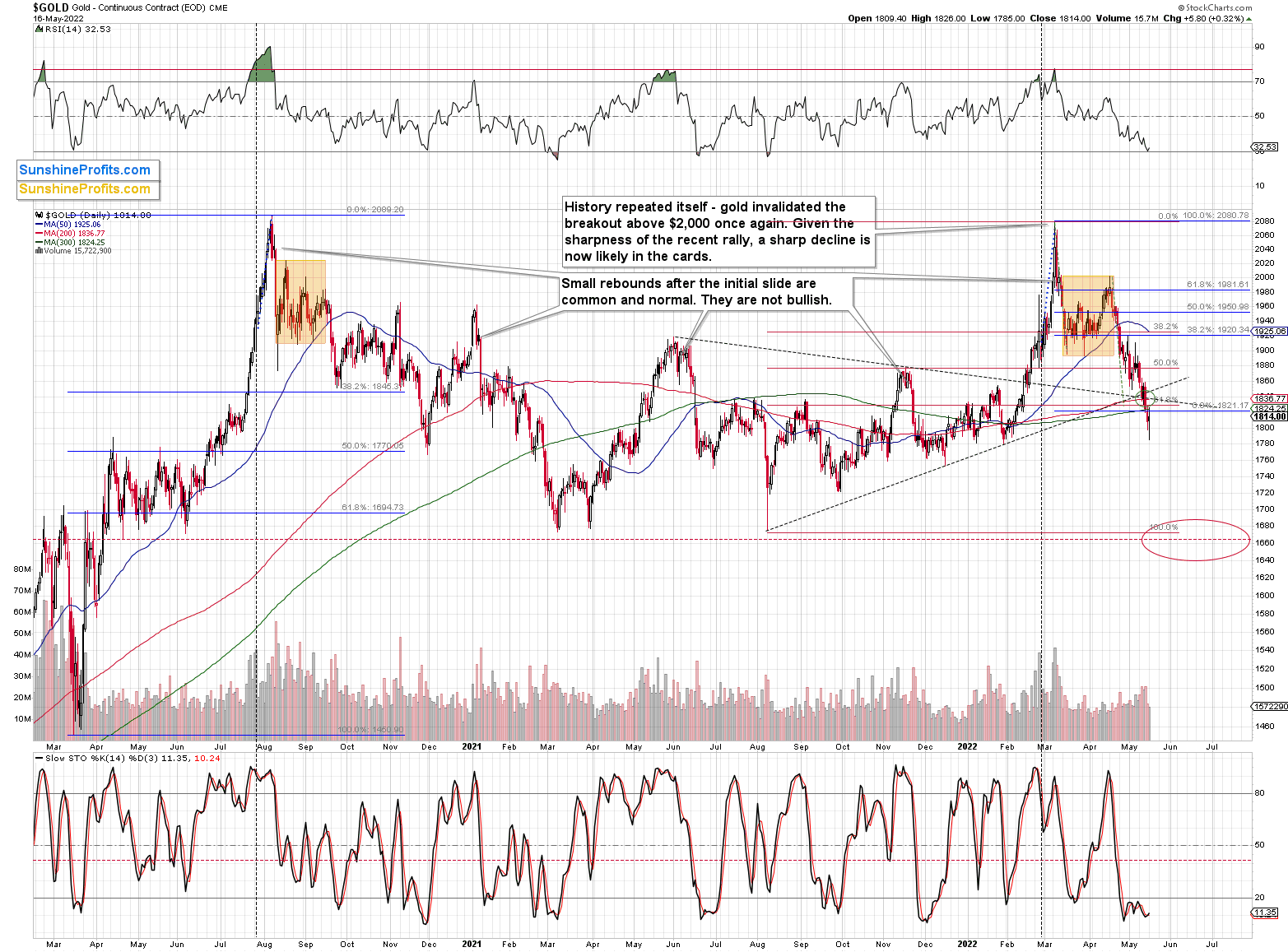

In short, gold reversed yesterday’s decline after almost touching its previous 2022 lows, and at the same time, it practically erased the entire war-tension-based rally – just like it was supposed to.

Gold ended the day only $5.80 higher, but the important thing is that it reversed at all. Gold’s RSI also bounced off the 30 level, which can be viewed as a buy signal on its own.

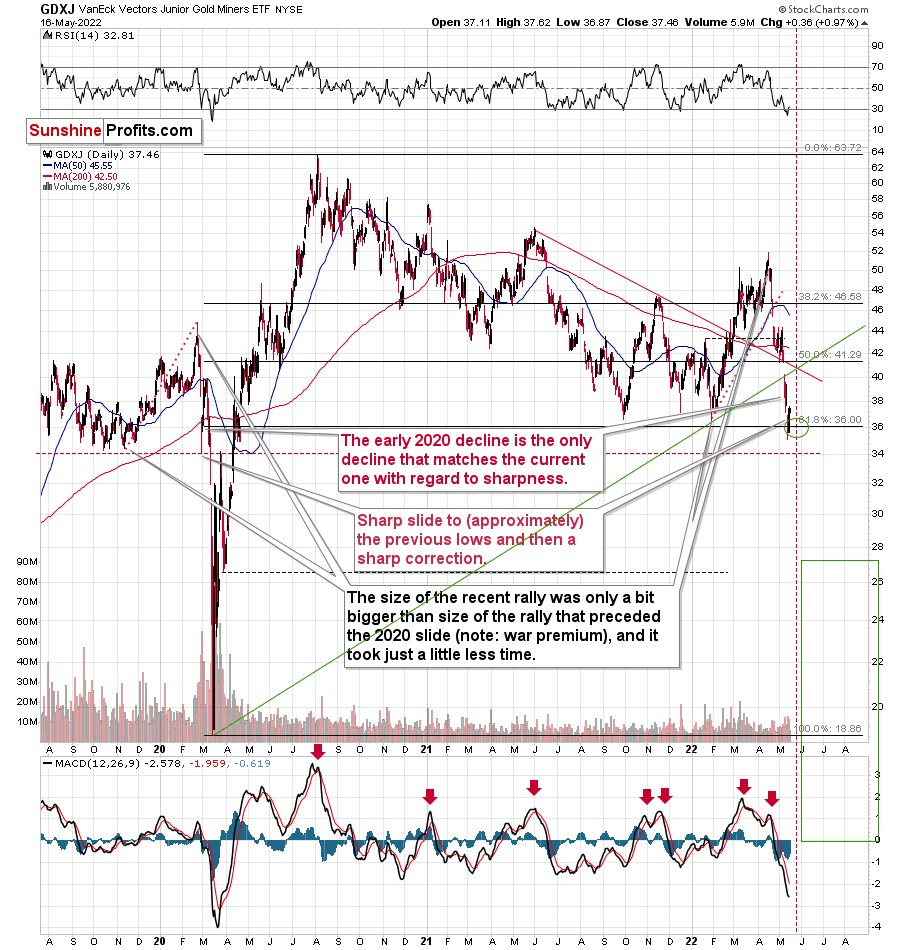

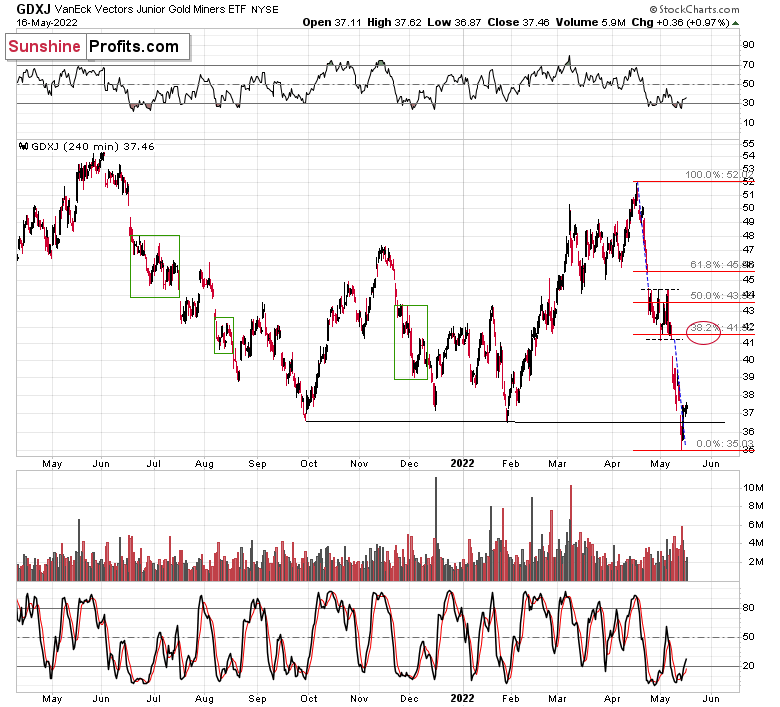

Junior miners were up by almost 1% yesterday, about 3 times more than gold. They continue to show strength, and our long positions (that became profitable almost immediately) are getting more profitable also in today’s early trading as the GDXJ is up in London trading.

In yesterday’s analysis, I wrote that the S&P 500 invalidated its head and shoulders pattern on an intraday basis, and even though it declined very modestly yesterday, it’s up in a clear manner in today’s pre-market trading.

This means that the odds of a short-term rally in the following days have greatly increased. This makes the current long position in junior mining stocks even more justified.

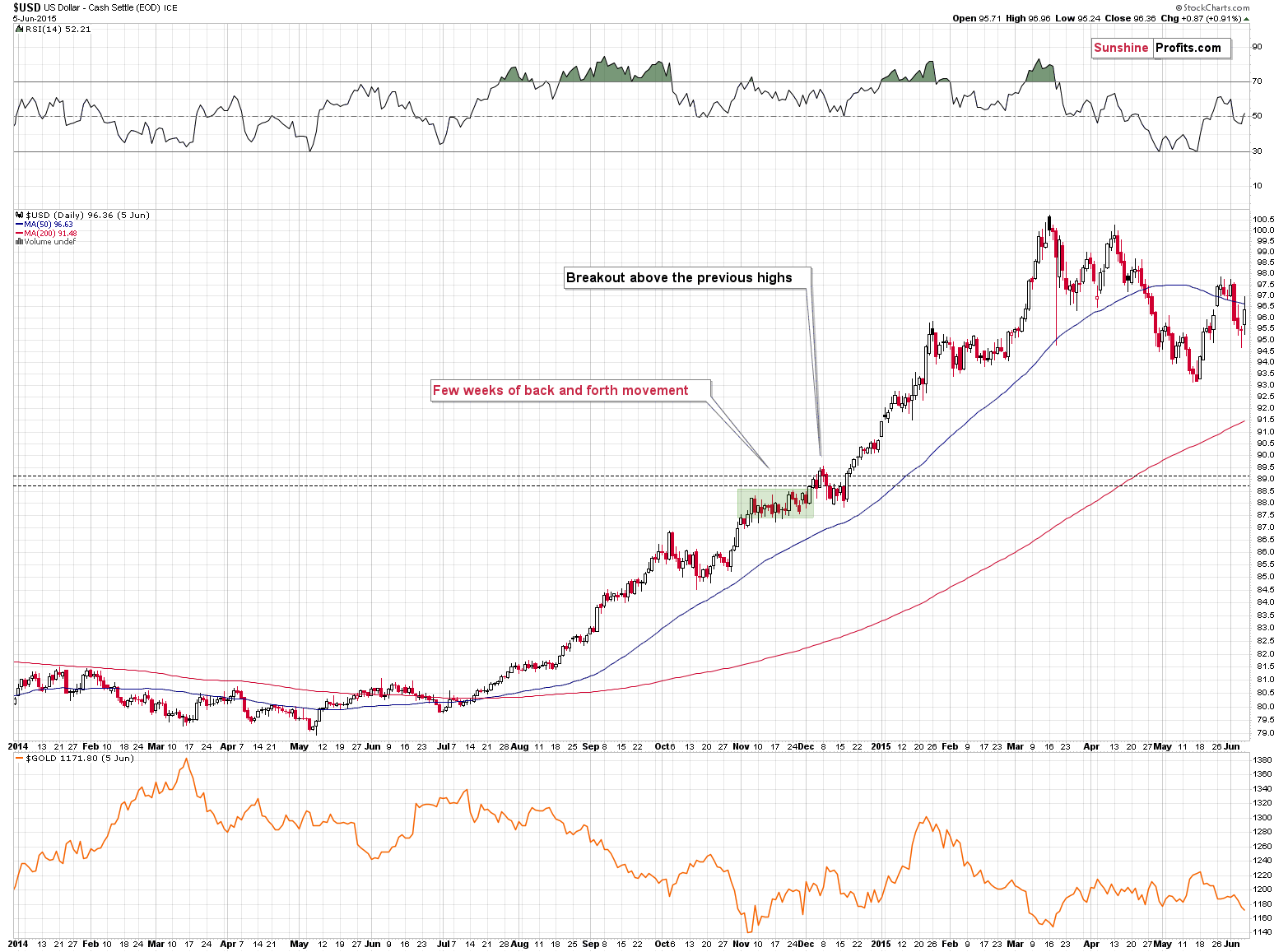

Also, as far as the USD Index is concerned, I previously wrote the following:

The higher of the recent highs is at 103.96 right now, so if the analogy to 2014 is to remain intact, the USD Index could now top at close to 104.5 or even 105.

That’s exactly what happened recently. On Thursday, the USD Index moved to 104.96, and in Friday’s trading it rallied above 105 (to 105.065) and it invalidated the breakout above this level - which is in perfect tune with what I wrote above. Consequently, it seems that we could now see a move to about 103-103.5, after which USD’s rally could continue.

The opposite is likely to take place in the precious metals sector. Gold, silver, and mining stocks are likely to rally in the near term, and then – after topping at higher levels – their decline would continue.

The USD Index futures moved to about 103.7 in today’s pre-market trading (so far), so you might be wondering if the bottom is in or about to be, and therefore, will gold stop rallying.

Please note that it’s possible that the USD Index bottoms shortly in the 103-103.5 range but then continues to trade sideways for a few days, while gold continues to rally. In fact, that’s what happened in late 2014. Consequently, what we saw so far today doesn’t imply that gold’s, silver’s, or miners’ rallies are over.

Having said that, let’s take a look at the markets from a fundamental point of view.

The Fed’s Recession

A sense of relative calm has come over the financial markets, as many of the drivers of the recent volatility are known to investors and, therefore, don't carry the same shock-and-awe value. However, the fundamental implications remain the same. With unanchored inflation poised to push the U.S. economy into recession, Fed officials realize that orchestrating the event themselves may be the lesser of two evils.

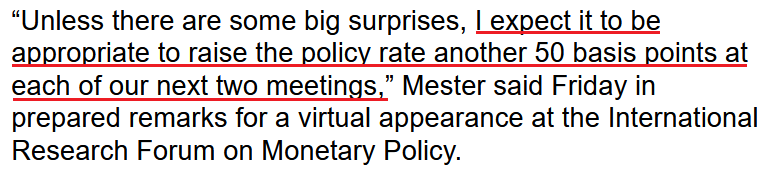

For example, Cleveland Fed President Loretta Mester said on May 13: "risks to inflation remain strongly on the upside, especially in the midst of the continuing war in Ukraine and the potential that the zero-COVID policy in China will further disrupt supply chains. I will need to see several months of sustained downward monthly readings of inflation before I conclude that inflation has peaked."

She added:

"If by the September [FOMC] meeting, the monthly readings on inflation provide compelling evidence that inflation is moving down, then the pace of rate increases could slow; but if inflation has failed to moderate, then a faster pace of rate increases may be necessary."

As a result, she expects 50 basis point rate hikes to remain on autopilot for the next few months.

Please see below:

Source: Bloomberg

Source: Bloomberg

Likewise, New York Fed President John Williams has been one of the most dovish central bank officials. However, he said on May 16: “We do need to move – again, the word is ‘expeditiously’ – to more normal rates this year, and we’re on our way to do that. But we also need to watch, and we need to monitor what’s happening in the economy.”

Thus, while a sharp deceleration in inflation could result in more patience (which has always been the case), he was crystal clear about the Fed’s top priority:

Source: Bloomberg

Source: Bloomberg

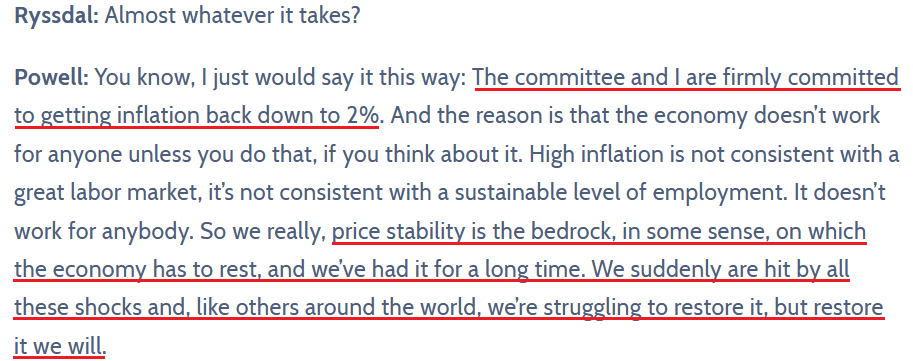

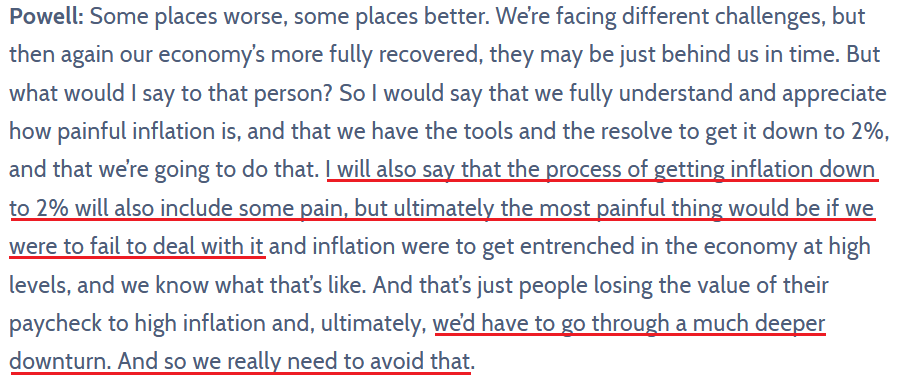

Furthermore, his tone matches the sentiment that Fed Chairman Jerome Powell exuded on May 12. I wrote on May 16:

When asked on May 12 if he will do “whatever it takes” to restore price stability, Powell responded:

Source: Marketplace

Source: Marketplace

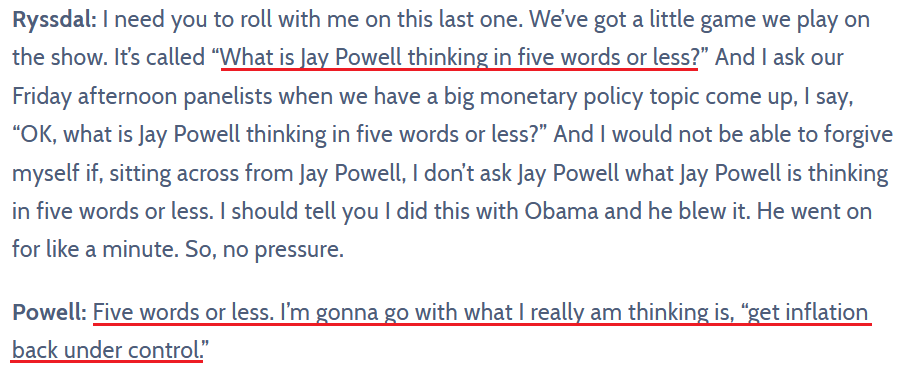

As a result, while I repeatedly warned that Fed officials weren’t bluffing, Powell ended the interview with what may be the most important words uttered in 2022:

Source: Marketplace

Source: Marketplace

Therefore, while investors continue to hold out hope that inflation will subside and a “soft landing” will materialize, the reality is that the Fed needs to orchestrate a minor recession to avoid a larger one down the road. As such, deteriorating macroeconomic data should increase investors’ anxiety as the Fed’s rate hikes have their desired effect.

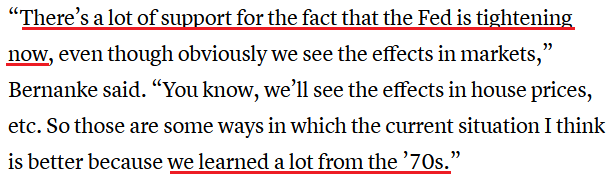

To that point, former Fed Chairman Ben Bernanke said on May 16:

“Why did [the Fed] delay their [inflation] response? I think in retrospect, yes, it was a mistake. And I think they agree it was a mistake.”

Now, for the sake of objectivity, Bernanke is the one that said subprime mortgage defaults were “likely to be contained” in 2007, and we all know what happened next. As a result, he’s in no position to criticize Powell. Yet, while I warned throughout 2021 that inflation would prove problematic, Bernanke highlighted why the Fed was so patient for so long. He said:

“One of the reasons was that they wanted not to shock the market. Jay Powell was on my board during the Taper Tantrum in 2013, which was a very unpleasant experience. He wanted to avoid that kind of thing by giving people as much warning as possible. And so that gradualism was one of several reasons why the Fed didn’t respond more quickly to the inflationary pressure in the middle of 2021.”

However, that was then and this is now; and while the financial markets and the U.S. economy are showing signs of stress, inflation prevents the Fed from running to the rescue.

Please see below:

Source: CNBC

Source: CNBC

To that point, even Powell indirectly stated on May 12 that an orchestrated downturn is more prudent than letting inflation rage and hoping that it eventually subsides:

Source: Marketplace

Source: Marketplace

As a result, while the shock and awe of a hawkish Fed, higher real yields, a stronger USD Index and a potential recession are causing less turbulence than in prior weeks, the fundamental consequences of these developments should frighten investors for much of 2022.

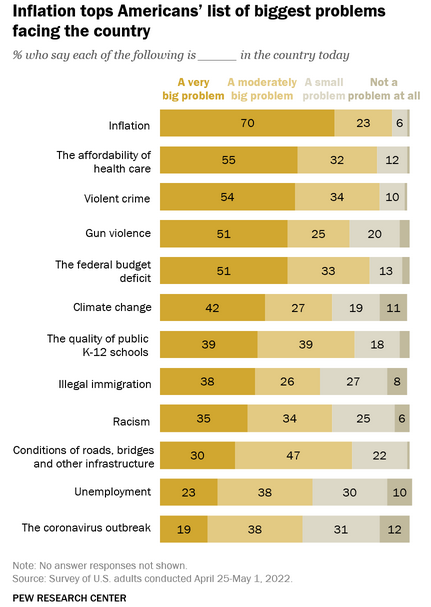

Furthermore, I’ve noted the political ramifications of unanchored inflation on multiple occasions. In a nutshell: the Fed has been given the green light to suffocate inflation because the pricing pressures are bad for U.S. President Joe Biden. As evidence, the Pew Research Center released its latest public opinion poll on May 12. The report revealed:

“The public views inflation as the top problem facing the United States – and no other concern comes close. Seven-in-ten Americans view inflation as a very big problem for the country, followed by the affordability of health care (55%) and violent crime (54%).”

Furthermore, if we combine respondents that called inflation “a very big problem” and “a moderately big problem,” the percentage is 93%.

Please see below:

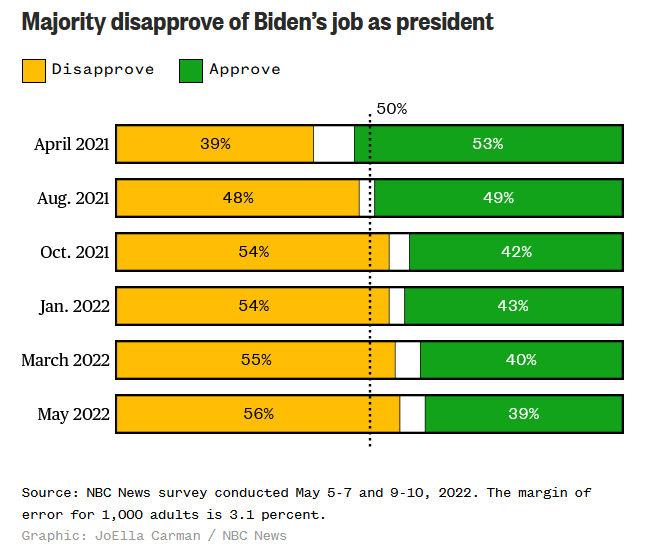

Similarly, and unsurprisingly, NBC released its latest opinion poll on May 15. The report revealed:

“The poll also found that this Supreme Court draft opinion hasn’t substantially altered the overall political environment heading into November’s elections – with inflation and the economy remaining the public’s top issues, President Joe Biden’s job rating falling below 40 percent and a whopping 75 percent of Americans saying the country is headed in the wrong direction.”

“It’s the fourth straight NBC News poll with the wrong-track number higher than 70 percent, and the fifth time in the poll’s 34-year history when the wrong-track number hit 75 percent or higher. The other times were in 2008 (during the Great Recession) and 2013 (during a government shutdown).”

More importantly, though:

“The NBC News poll also finds 39 percent of Americans approving of President Biden’s job as president, versus 56 percent who say they disapprove. While Biden’s approval rating is essentially unchanged from March’s poll – when it was at 40 percent – the new number represents the lowest mark of his presidency.”

Please see below:

As a result, the Democrats are hemorrhaging votes right now, and with the mid-term elections scheduled for Nov. 8, the party is running out of time to right the ship. Therefore, if they don’t show progress on the inflation front, the Republicans will be the primary beneficiaries.

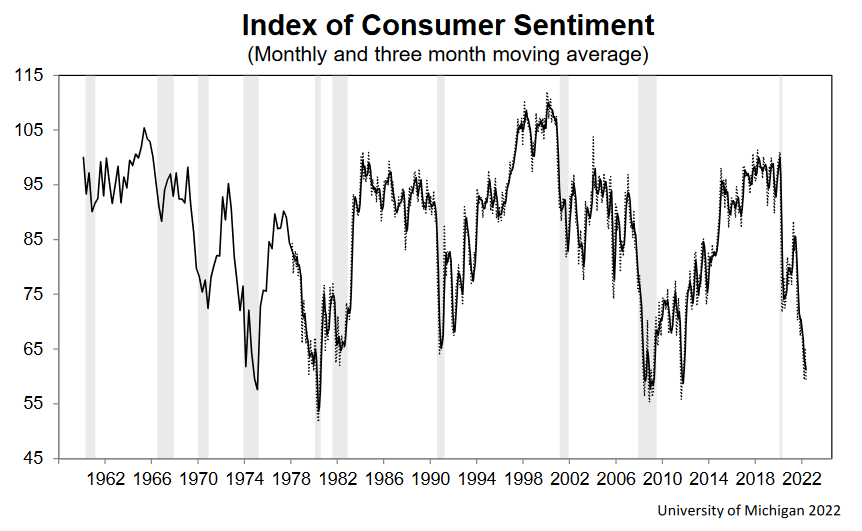

To that point, the University of Michigan released its Consumer Sentiment Index on May 13. Director Joanne Hsu said:

“Consumer sentiment declined by 9.4% from April, reversing gains realized that month( … ). Consumers' assessment of their current financial situation relative to a year ago is at its lowest reading since 2013, with 36% of consumers attributing their negative assessment to inflation. Buying conditions for durables reached its lowest reading since the question began appearing on the monthly surveys in 1978, again primarily due to high prices.”

“The median expected year-ahead inflation rate was 5.4%, little changed over the last three months, and up from 4.6% in May 2021. The mean was considerably higher at 7.4%, reflecting substantial variation in price changes across types of goods and services, and in household spending patterns.”

Thus, consumer sentiment remains in free fall. Moreover, even though consumer spending remains robust RIGHT NOW, the impact of higher interest rates, higher mortgage payments, and higher gasoline prices should wreak havoc on their financial health over the next few months.

Please see below:

Speaking of which, U.S. retail gasoline prices hit a new all-time high on May 15 (the black line below). Moreover, the summer season is when peak demand often materializes. As a result, it’s paramount that Biden and Powell curb the pricing pressures, and orchestrating a short-term recession may be their best hope at this point.

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

The bottom line? While the financial markets have seemingly found their short-term footing, none of the fundamental issues that helped ignite the initial panic have been solved. Moreover, with the Fed on autopilot and Powell’s hawkish rhetoric also at a post-pandemic high, cooling inflation should put heavy pressure on risk assets like the S&P 500 and the PMs. Therefore, while our short-term long position performed well again on May 16, we are ready to switch to the short position soon, as the medium-term trend in the precious metals market remains down.

In conclusion, the PMs rallied on May 16, and the technicals proved prescient in calling the GDXJ ETF’s short-term bottom. Likewise, since more upside should materialize in the coming days, the technicals will also be the best roadmap of when to reposition on the short side. As a result, while the PMs’ medium-term fundamentals remain profoundly bearish, we can still profit from their countertrend rallies.

Overview of the Upcoming Part of the Decline

- It seems to me that the short-term decline in the precious metals market is over and we’re currently seeing a rebound.

- After the above-mentioned correction, we’re likely to see another big slide, perhaps close to the 2021 lows ($1,650 - $1,700).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

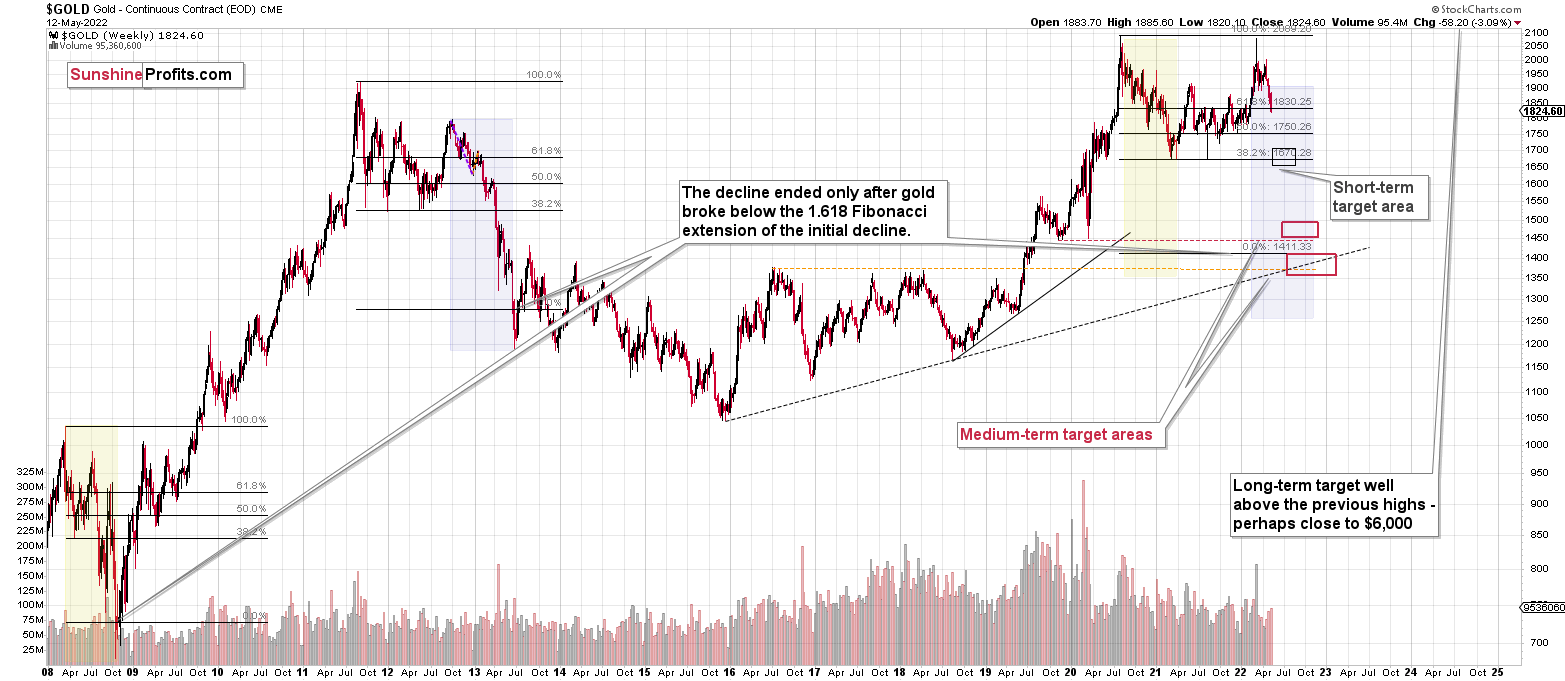

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, it seems that we are about to see a short-term corrective upswing in the precious metals sector (perhaps until the end of this week), even though the medium-term trend remains clearly down.

The medium-term downtrend is likely to continue shortly (perhaps after a weekly or a few-day long correction). As investors are starting to wake up to the reality, the precious metals sector (particularly junior mining stocks) is declining sharply. Here are the key aspects of the reality that market participants have ignored:

- rising real interest rates,

- rising USD Index values.

Both of the aforementioned are the two most important fundamental drivers of the gold price. Since neither the USD Index nor real interest rates are likely to stop rising anytime soon (especially now that inflation has become highly political), the gold price is likely to fall sooner or later. Given the analogy to 2012 in gold, silver, and mining stocks, “sooner” is the more likely outcome.

It seems that our profits from short positions are going to become truly epic in the coming months. And the profits from the current long position are likely to enhance them even further.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative long positions (100% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $40.96; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JNUG (2x leveraged). The binding profit-take level for the JNUG: $56.68; stop-loss for the JNUG: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $22.88

SLV profit-take exit price: $21.28

AGQ profit-take exit price: $32.18

Gold futures downside profit-take exit price: $1,909

HGU.TO – alternative (Canadian) 2x leveraged gold stocks ETF – the upside profit-take exit price: $19.68

HZU.TO – alternative (Canadian) 2x leveraged silver ETF – the upside profit-take exit price: $12.09

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief