Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Today’s analysis is, once again, going to be relatively brief, as practically everything that I wrote in Monday’s (Mar. 15) flagship analysis remains up-to-date and the points that I added yesterday remain relevant as well. I will, however, add a more detailed analytical piece about silver.

Let’s start with a quote from yesterday:

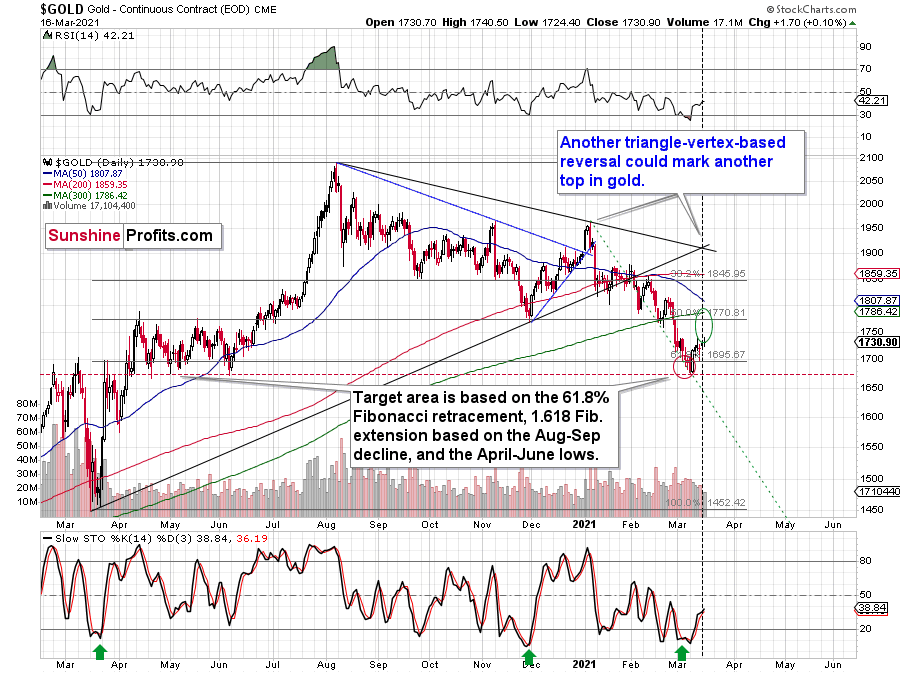

Based on the above chart, the triangle-vertex-based reversal point was due yesterday. However, based on the chart below, it’s due today.

There might be slight differences between chart providers, which – if applied to relatively long-term lines – can distort the implications by a few pixels on the chart. These few pixels might mean a day (or so) of a difference in the case of the triangle-vertex-based formation.

Instead of going over charts of multiple providers on each day, it’s more useful to notice that the triangle-vertex-reversal points work on a near-to basis and thus expect a given reversal to take place close to the point suggested by the above technique, rather than going all-in based on the assumption that it will work perfectly. Every now and then it does work perfectly, but the “broad” approach is overall more useful.

At the moment of writing these words, I see that gold futures formed a small top just about $2 below the previous March high ($1,738). Consequently, both following scenarios would make sense in light of the current triangle-vertex-based reversal:

- Gold could decline right away as it doesn’t have to form a new high at the reversal point – just “a high”

- We could see another small, several-dollar rally, which would take gold to new monthly highs and make the triangle-vertex-based reversal work in a classic way, where it detects the final top for a given rally. The FOMC weeks tend to have higher intraday volatility, especially right before the interest rate decision is announced and during the press conference. This means that gold could move up and down in a quite volatile manner shortly.

Both scenarios seem quite possible and it’s hard to tell which of them is more likely. In both cases, it seems quite likely that another – big – decline will begin soon. Of course, I can’t promise that the rally is going to be completely over today, but this seems quite likely. And if not, it seems that it’s going to be over shortly, anyway.

What happened during the session? Gold moved to $1,740.50 (slightly above the previous March high) and then it reversed, ending it at $1,730.90. The intraday breakout above the March highs was invalidated, which suggests that the second of the above-mentioned scenarios was realized – gold topped exactly (or very close to) its triangle-vertex-based reversal.

Now, today’s the FOMC statement day (+press conference), so we can expect more intraday volatility in the following hours. This could mean a move above yesterday’s highs, but such a move would not be likely to hold.

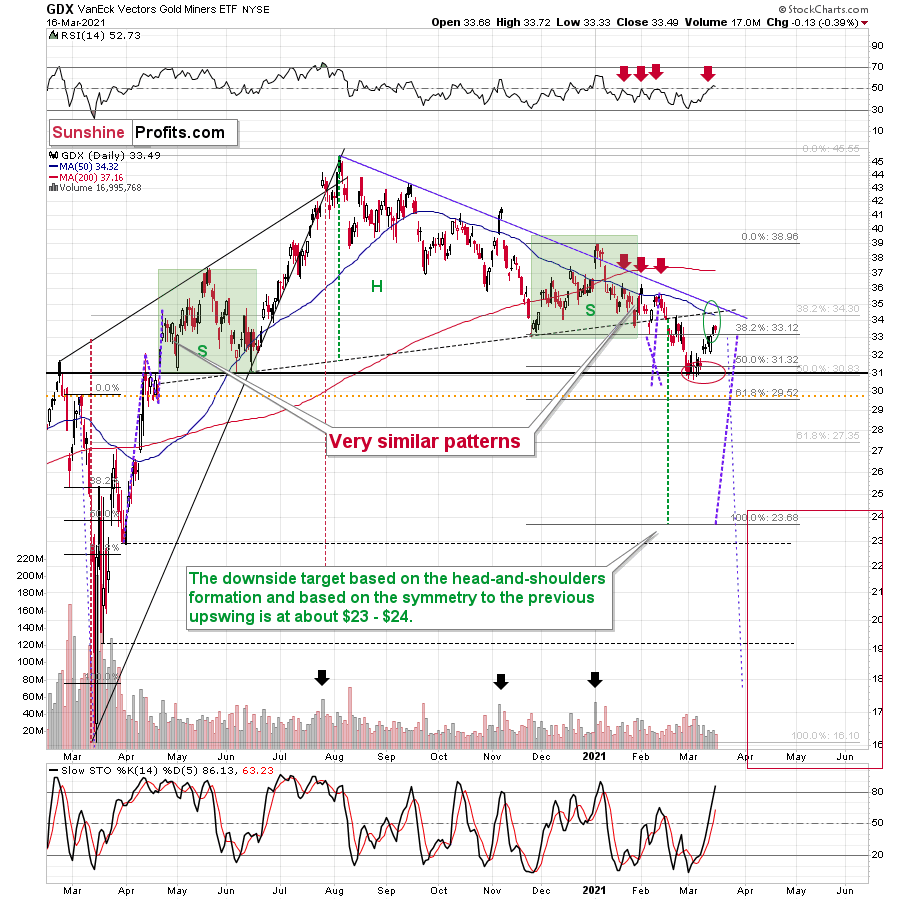

Mining stocks declined a bit yesterday, which means that everything that I wrote about them remains up-to-date:

The mining stocks remain in my upside target area, which means that they could have already topped, or that they could top a bit higher. Regardless, based on all the reasons that I discussed yesterday, and also based on the above comments on gold’s reversal, it seems that the days of this rally are numbered (and it’s not a big number, either).

The neck level of the previously broken head and shoulders pattern, the declining blue resistance line, the 50-day moving average, the late-February high – they all create a very strong short-term resistance not far above yesterday’s closing price. But does it mean that the mining stocks have to move higher from here, or that such a rally would be likely?

Not necessarily. While miners managed to close yesterday’s session above the November low, they didn’t manage to close the day above the January and early-February lows in terms of the closing prices. About a month ago, the GDX tried to invalidate the breakdown below these levels, and this move failed – it was followed by a decline to new yearly lows. Will we see the same thing once again? It seems very likely in my view – the history tends to rhyme.

But how low could the GDX ETF go? My previous comments on that matter remain up-to-date, but I would like to stress that just because the downside target area is relatively far, it doesn’t mean that we will necessarily hold our positions until it’s reached. If we see signs of strength that seem reliable (like miners refusing to decline even though gold moves lower combined with gold reaching an important support level while the USDX encounters resistance), I might write about temporarily closing this position – and perhaps even going long one more time – and we might be able to reap additional profits on the corrective upswing, just as I did earlier this month.

Our final downside target area ($15 – $24.5) is quite broad, because a lot depends on what the general stock market will do. I’ll be looking at gold for the key signs along with a few other factors (including the Gold Miners Bullish Percent Index) and determined the buying opportunity based on them – not necessarily based on the price of the GDX or GDXJ by itself.

Yes, this target is quite low, and thus might appear unrealistic, but let’s consider the following:

- Miners are slightly above their early-2020 high – just like gold.

- Gold is likely to decline to its 2020 lows or so

- General stock market might have just topped.

Considering all three above factors it’s clear that a move to even the 2020 lows is not out of the question.

And this means that junior miners might decline more than senior miners. A move from the current levels to the 2020 would imply a decline by about 50% in case of the GDX, and by about 60% in case of the GDXJ.

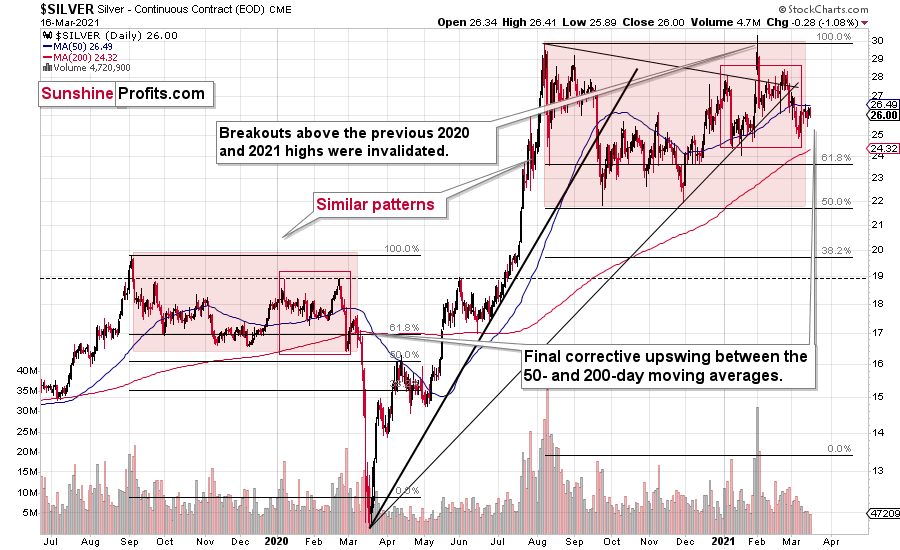

Let’s turn to silver.

Silver is moving similarly to what we saw in the second half of 2019 and early 2020, before the huge slide. I marked the very broad tops that followed a quick rally in the red-shaded rectangles, and I also created solid-line red rectangles based on the last two – normal – tops and the initial decline that followed them.

Based on the sudden increase in silver’s popularity, it spiked 1.5 months ago, but this move to new highs was quickly invalidated. The nature of this move was more or less random – it didn’t stem from a change in fundamentals or from a specific technical pattern, but rather from a sudden growth of interest in silver based on forum posts. Because of that, and because this upswing was quickly invalidated, this quick upswing didn’t really break the self-similarity pattern.

Right now, we see a corrective upswing between – approximately - the 50- and 200-day moving averages (marked with blue and red). This upswing corresponds to the corrective upswing in gold and mining stocks (which allowed us to profitably go long in case of the latter). We saw – approximately – the same thing about 12 months ago, right before the huge slide.

And speaking of time, please note that the final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

If this self-similar pattern is indeed materializing, then the implications are very bearish, and we can expect a major downturn any day or week now.

Let’s be realistic - so far, the analogy might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

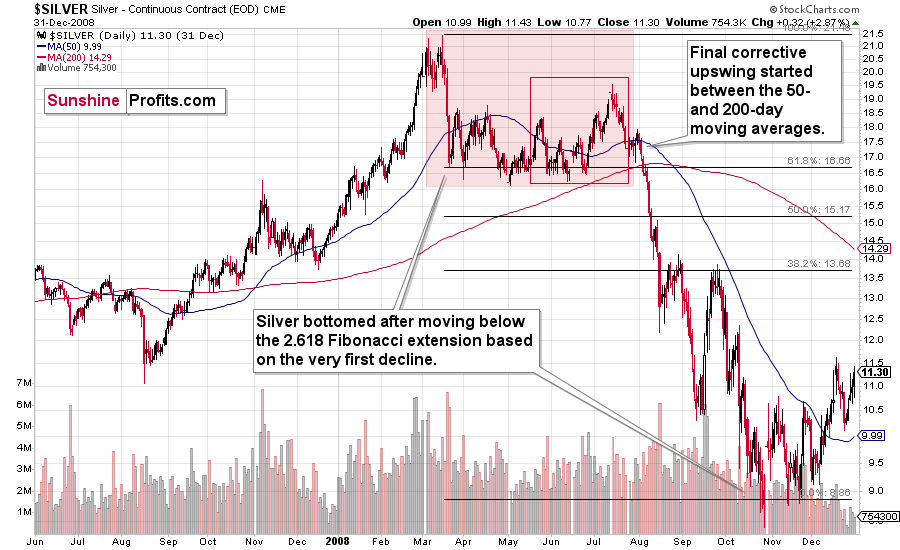

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

Before summarizing, please note silver’s tendency to decline sharply in March – that’s what happened in 2008 and 2020. Even if the entire self-similar pattern doesn’t continue, based on this seasonality, silver is likely to decline soon, anyway.

Summing up, if the similarity to what happened in 2020 and 2008 is upheld, then it seems that we’re about to see a big decline in the price of the white metal. Naturally, that’s not the only reason to expect silver’s weakness in the following weeks and months (not necessarily days) – you will find other reasons in my previous analyses.

Having said that, let’s take a look at the market from a more fundamental angle.

Get Your Popcorn Ready

With the U.S. Federal Open Market Committee (FOMC) taking center stage today, Jerome Powell, Chairman of the U.S. Federal Reserve, could ignite a late-afternoon explosion. With the bond market already skittish and the PMs in wait-and-see mode, Powell is trying to thread an ever-narrowing needle.

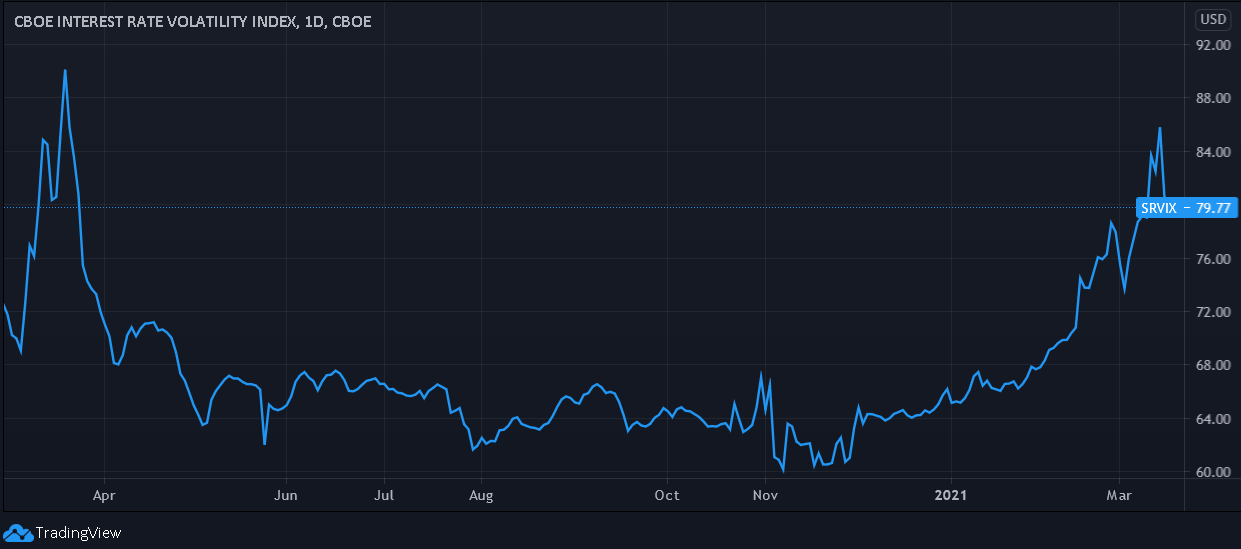

On Mar. 16, the Cboe Volatility index (VIX) – which gauges the S&P 500’s expected volatility over the next 30 days – closed at its lowest level in nearly a year. To explain the significance, the current reading is nearly 77% below the March 2020 high.

Please see below:

However, in stark contrast, the Cboe Interest Rate Swap Volatility Index (SRVIX) still suffers from extreme anxiety. For context, the SRVIX quantifies volatility in the expected forward swap rate (a future interest rate that investors can lock in today). With the current reading only ~12% below the March 2020 high, Powell’s performance (or lack thereof) could send shockwaves across the bond market.

Please see below:

On Mar. 16, I warned that failing to extend the Treasury exemption from U.S. banks’ Supplementary Leverage Ratios (SLR) could lead to $650 billion in U.S. Treasury outflows. But well ahead of the curve, since 2020, hedge funds have been dumping U.S. Treasuries at an alarming pace.

Please see below:

To explain, the blue bars above represent purchases and sales of U.S. Treasuries. If you analyze the right side of the chart (the descending blue bars), you can see that since 2020, hedge funds have been rapidly reducing their U.S. Treasury exposure.

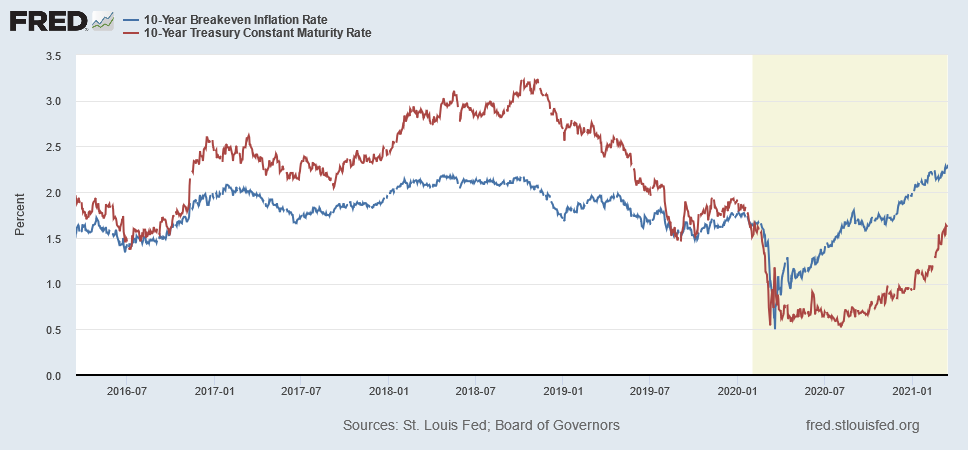

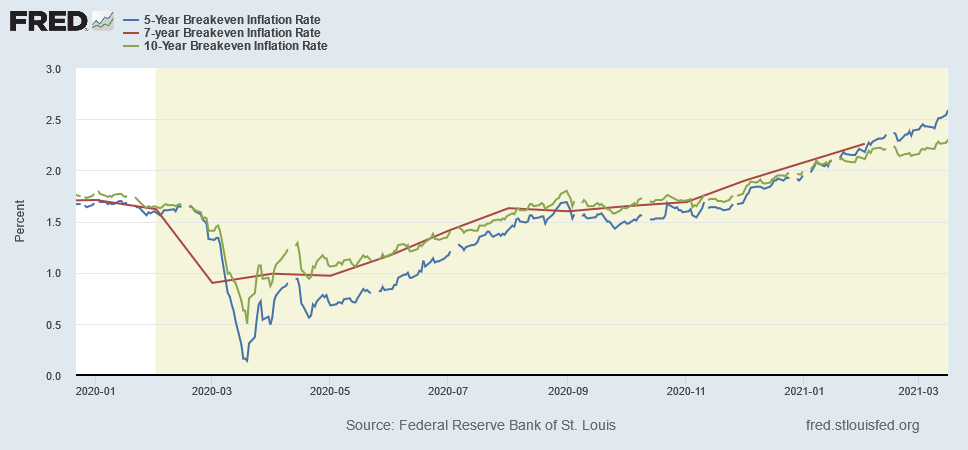

What’s more, Powell’s ‘aw-shucks’ approach to “unwelcome inflation” is beginning to wear thin. If you analyze the chart below, you can see that 5-year inflation expectations have surged to the point where the 5-year-10-year breakeven spread has hit an all-time low.

For context, the spread is calculated by subtracting the 5-year breakeven inflation rate from the 10-year breakeven inflation rate. Thus, the extreme negative reading on the right side of the chart highlights investors’ anxiety over rising inflation.

As further evidence, Bank of America’s Global Fund Managers’ survey revealed that the highest-ever net-percentage (93%) of institutional portfolio managers believe that rising inflation is inevitable.

Please see below:

Continuing the theme, Bill Gross – who was labelled the ‘Bond King’ before Jeffrey Gundlach – told Bloomberg on Mar. 16 that “I see a 3% to 4% [inflation] number ahead of us.” To that point, with Powell’s deny-and-suppress lifeboat beginning to take on water, Gross predicted that “three to six to 12 months at 3% to 4%-plus inflation will give [Powell] pause.”

Translation? The FED Chair will likely be forced to raise short-term interest rates much sooner than he wants.

And how could all of this affect the PMs?

Well, for one, notice the strong relationship between inflation expectations and nominal interest rates?

To explain, the blue line above tracks the U.S. 10-Year breakeven inflation rate, while the red line above tracks the U.S. 10-Year Treasury yield. And with the former often leading the latter, it’s further evidence that Powell has lost control of the bond market.

In addition, a rising USD Index is like kryptonite to the PMs. And while the greenback didn’t participate in the U.S. 10-Year Treasury yield’s summer surge (defying historical precedent), since the New Year, the USD Index has begun to change its tone.

Please see below:

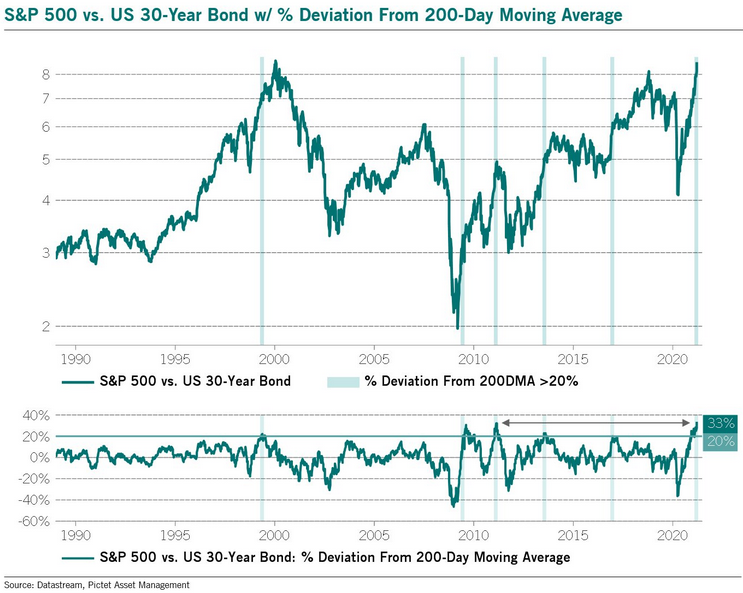

As a third source of concern, the S&P 500 has the potential to sink the PMs. Currently, the S&P 500/U.S. 30-Year Treasury Bond ratio is 33% above its 200-day moving average. To explain the significance, it’s the highest reading since 2011 and only five other times in history has the ratio exceeded 20%.

Please see below:

What’s more, if you analyze the vertical gray bars (marking the five other periods where the ratio was more than 20% above its 200-day MA), you can see that 80% of the time (except for the one bar between 2015 and 2020), material drawdowns of the S&P 500, either immediately, or eventually followed.

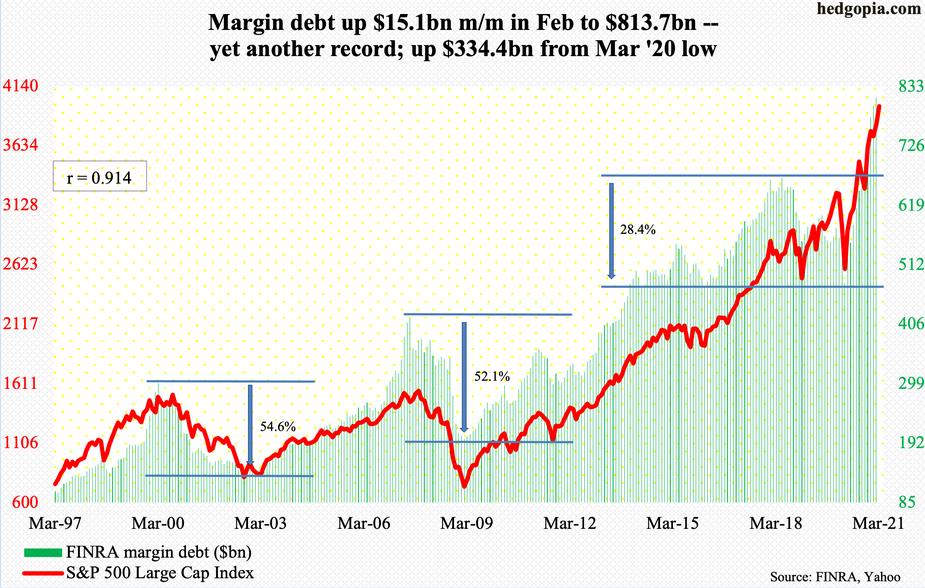

More importantly though, a potential correction could be extreme. Hitting another all-time high in February, monthly margin debt now sits at $813.680 billion – a near 70% increase year-over-year. And if you analyze the chart below, you can see that excessive margin levels often precede significant S&P 500 drawdowns.

But while preconditions are visible to those that care to look, will Powell continue to save the day?

Well, I wrote previously:

Dubbed Operation Twist 3.0, the strategy (a version of yield curve control) requires the FED to buy long-term Treasuries and sell short-term Treasures in order to flatten the yield curve (reduce the spread between short-term and long-term interest rates). Despite its implementation poised to suppress bond yields, buoy equities and breathe new life into the PMs, the sugar high will inevitably wear off.

Why so?

Because you can only stretch a rubber band so far before it snaps.

To stop yields from rising, the U.S. Federal Reserve (FED) has to increase its asset purchases (and buy more bonds in the open market). However, the added liquidity should have the same net-effect because it increases inflation expectations, which a precursor to higher interest rates.

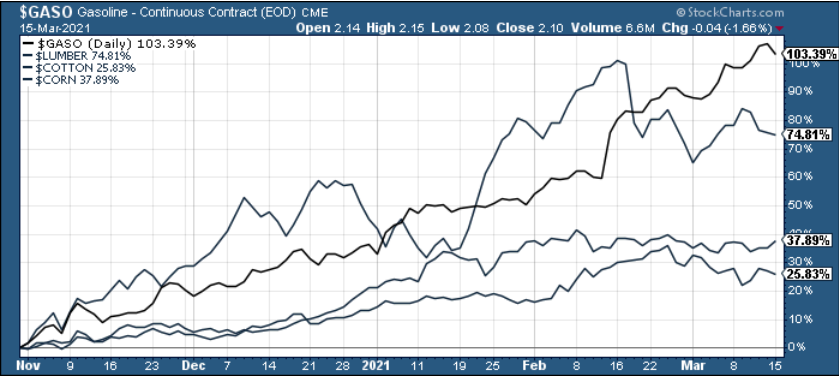

The option is akin to putting out a fire by pouring on more gasoline. If you analyze the chart below, you can see that gasoline (no pun intended) prices have more than doubled since November. As a result, implementing YCC will only exacerbate inflation expectations.

Thus, while Powell could pacify markets today and announce some iteration of YCC, his medium-term fate is likely already sealed: if he does nothing, U.S. Treasury yields will likely soar.

If he does something (YCC), inflation expectations will likely soar.

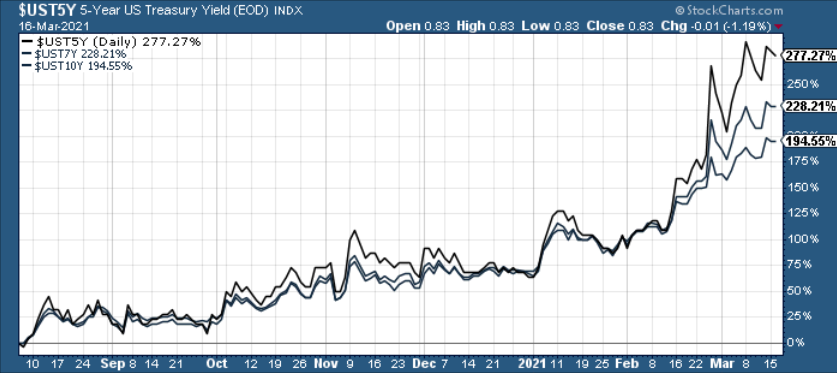

As a result, Powell is running out of bullets and financial markets are forcing his hand. And while YCC likely serves his short-term needs – by suppressing interest rates and pushing up asset prices – it only makes the medium-term repercussions that much worse. But given that he’s gone this far, stretching the rubber band even further isn’t out of the question. Thus, the PMs could receive a major boost if he strikes the right tone. However, the medium-term implications remain profoundly bearish. Case in point: the U.S. 5-Year Treasury yield has risen by nearly 131% YTD, while gold has declined by nearly 9%. And with the USD Index just starting to wake up, a Powell-induced pause, followed by a continuation of the theme, will likely haunt the PMs over the medium-term.

Overview of the Upcoming Part of the Decline

- It seems to me that we are already after the initial bottom and the initial correction. If not, then it seems likely to me that the corrective upswing will be completed within a week. It’s more likely that the next big move lower is already underway, though.

- After miners slide once again in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver (this could take another 1-2 weeks to materialize). I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,450 - $1,500 and the entire decline (from above $1,700 to about $1,475) would be likely to take place within 1-12 weeks and I would expect silver to fall hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments in my view. This might happen with gold close to $1,475, but it’s too early to say with certainty at this time. In other words, the entire decline could take between 1 and 12 weeks, while silver declines particularly fast in the final 1-2 weeks.

- If gold declines even below $1,500 (say, to ~$1350 or so), then it could take another 10 weeks or so for it to bottom, but this is not what I view as a very likely outcome.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops . If the mid-February 2020 top was the final medium-term top, then it seems that we might expect the precious metals sector to bottom in mid-May or close to May’s end.

- The above is based on the information available today and it might change in the following days/weeks.

Letters to the Editor

Q: What is the best level (time) to short gold and silver?

A: In my opinion, right now.

Q: Did you close shorts on March 12th at gold support, and now going short again with this report?

A: No, I wrote about closing short positions in the GDX on February 26, and on March 4 I wrote about closing the remaining short positions (GDXJ) and about going long GDX. I wrote about taking profits off the table from these long positions a week later – on March 11, and it was then, when I opened new short positions in GDXJ.

Q1: Thank you for previous assistance. I still have 1000 units of DUST, as I was away when it hit $24.88. What would be your exit price if you owned 1000 units?

Q2: What's your current target for DUST?

A: The target is the same regardless of the number of units that one holds and in case of DUST it would be $49.88.

However, to provide a complete reply, and in my opinion, if I owned DUST right now, I would sell it, and at the same time I’d buy JDST (assuming the preference regarding leverage stays intact), as I think junior miners are likely to fall more than senior miners.

Summary

To summarize, the PMs’ medium-term decline is well underway, and based on the recent performance of the USD Index, gold and mining stocks, it seems that the corrective upswing is already over (or about to be over). The next big move lower seems to be already underway or about to start.

In addition, because we’re likely entering the “winter” part of the Kondratiev cycle (just like in 1929 and then the 1930s), the outlook for the precious metals’ sector remains particularly bearish during the very first part of the cycle, when cash is king.

The confirmed breakout in the USD Index is yet another confirmation of the bearish outlook for the precious metals market.

After the sell-off (that takes gold to about $1,450 - $1,500), we expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and it seems that we’re about to make much more on this March decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently proving you with a possibility to extend your subscription for a year, two years or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now, while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us..

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $24.12; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $39.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $94.87; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,512.

Gold futures upside profit-take exit price: $1,512.

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief