Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

The precious metals market declined yesterday, and while the move is still small, it’s nice to see that our short positions in juniors are already profitable.

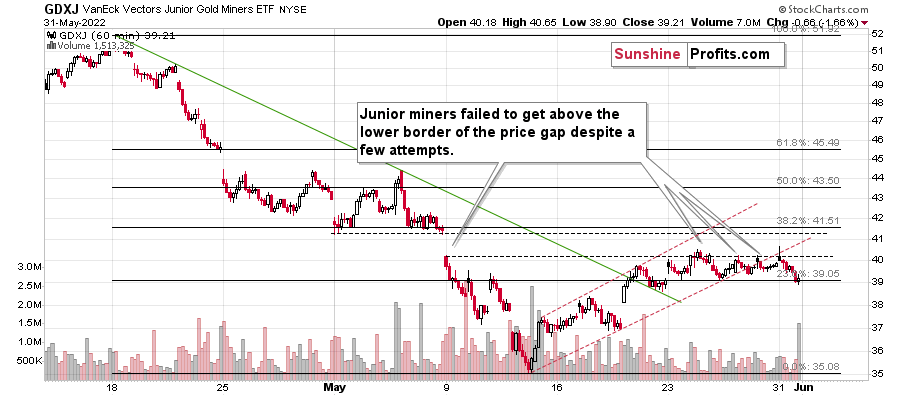

Something quite interesting happened in their price movement at the beginning of yesterday’s session, and that’s what I’d like to start with today.

Juniors tried to rally above their recent highs and resistance levels, but failed. They formed an hourly reversal candlestick and then declined in the following part of the session.

What was “supposed” to be a breakout turned out to be a fakeout, and lower values followed. This is bearish, and it tells us that taking profits from our previous long positions in the junior miners several days ago was likely a great idea.

To clarify, the above is bearish only for the very short term. It doesn’t tell us much about the bigger picture. So let’s zoom out. Significantly.

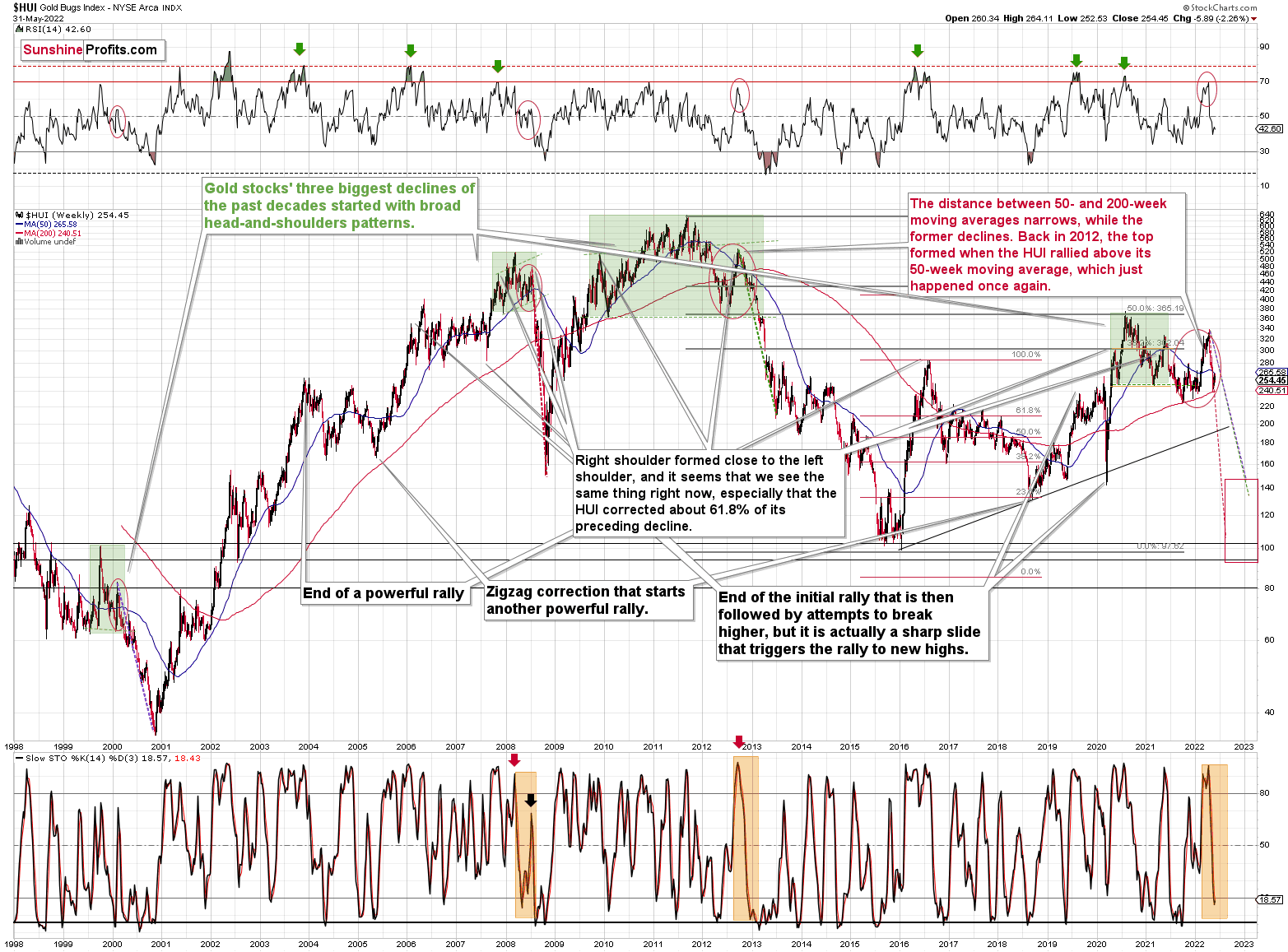

There are quite a few analogies between now and 2012, and I described them in the huge last Friday’s analysis. However, there are also signs that what we’re seeing is actually similar to what happened in 2008. I also described some of them on Friday, but the one that I would like to emphasize today is already visible on the above chart.

Namely, gold stocks declined practically just as rapidly as they did in 2008. Here’s the really interesting part: they corrected after moving close to their 200-week moving average – just like what we saw in 2008. This red line triggered corrections in both cases. They were not huge, but notable from the short-term point of view.

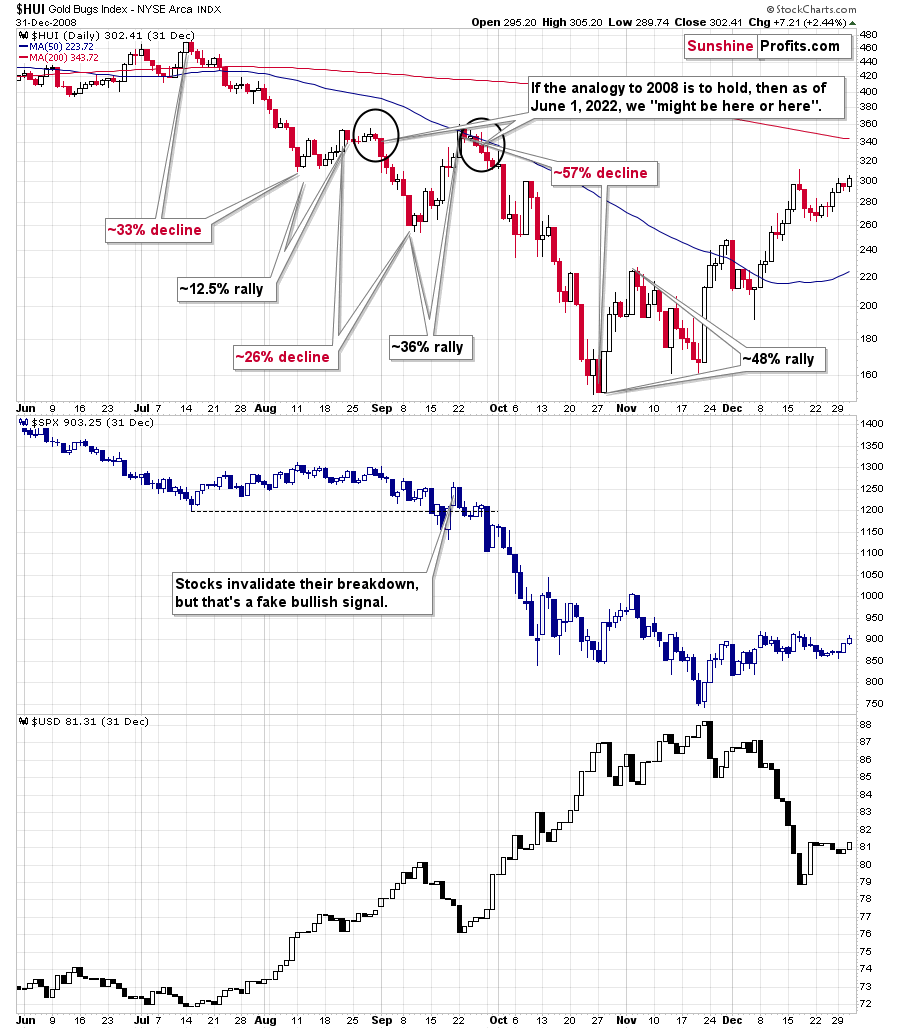

You know how much the HUI Index declined before this correction (between the July 2008 top and the August 2008 bottom)?

About 33%.

The decline in the HUI Index that we saw between April and May took it about 27% lower.

Not identical, but very similar.

And the recent correction? The HUI moved up around 8% higher in terms of closing prices and about 11% higher. Back in 2008, the analogous rally took the HUI about 12.5% higher.

Once again: not identical, but similar. Things are just a little less extreme this year.

If this similarity is to continue, then we can expect another mover lower to materialize shortly. Well, that’s what we already knew based on other indications, but what the above analogy also tells us is that the HUI Index could decline significantly once again. Back in 2008, it declined by about 26%, which was a little less than before the consolidation.

Please keep in mind that history tends to rhyme, not repeat itself to the letter. So, the above doesn’t imply that the HUI now has to decline by exactly 26%. It does tell us, however, that mining stocks can be expected to decline by as much (approximately!) as they did before correcting, and that’s an important clue.

If the GDXJ declines by as much as it did before correcting, it will move slightly below $28. The nearby support is provided by the previous low (dashed line, slightly below $27). While it’s unclear if it moves below $27 or not – before correcting – it’s very likely that we’ll see a huge decline below $30, and that the profits on our short positions are likely to increase significantly.

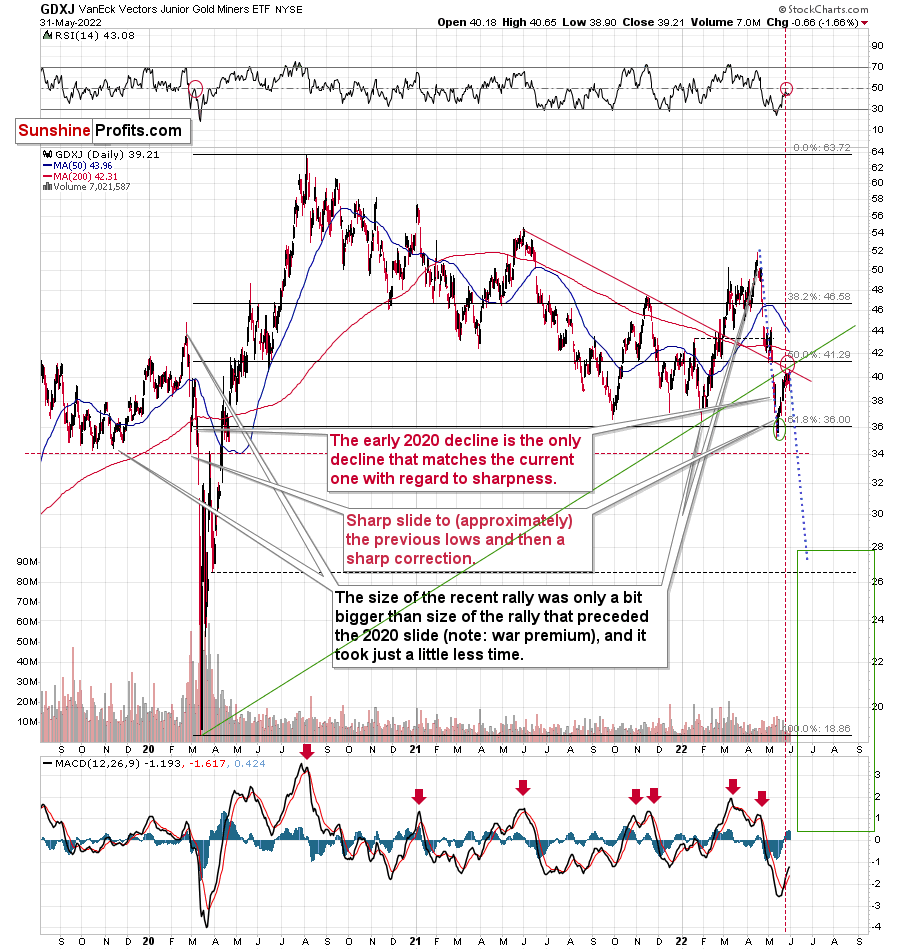

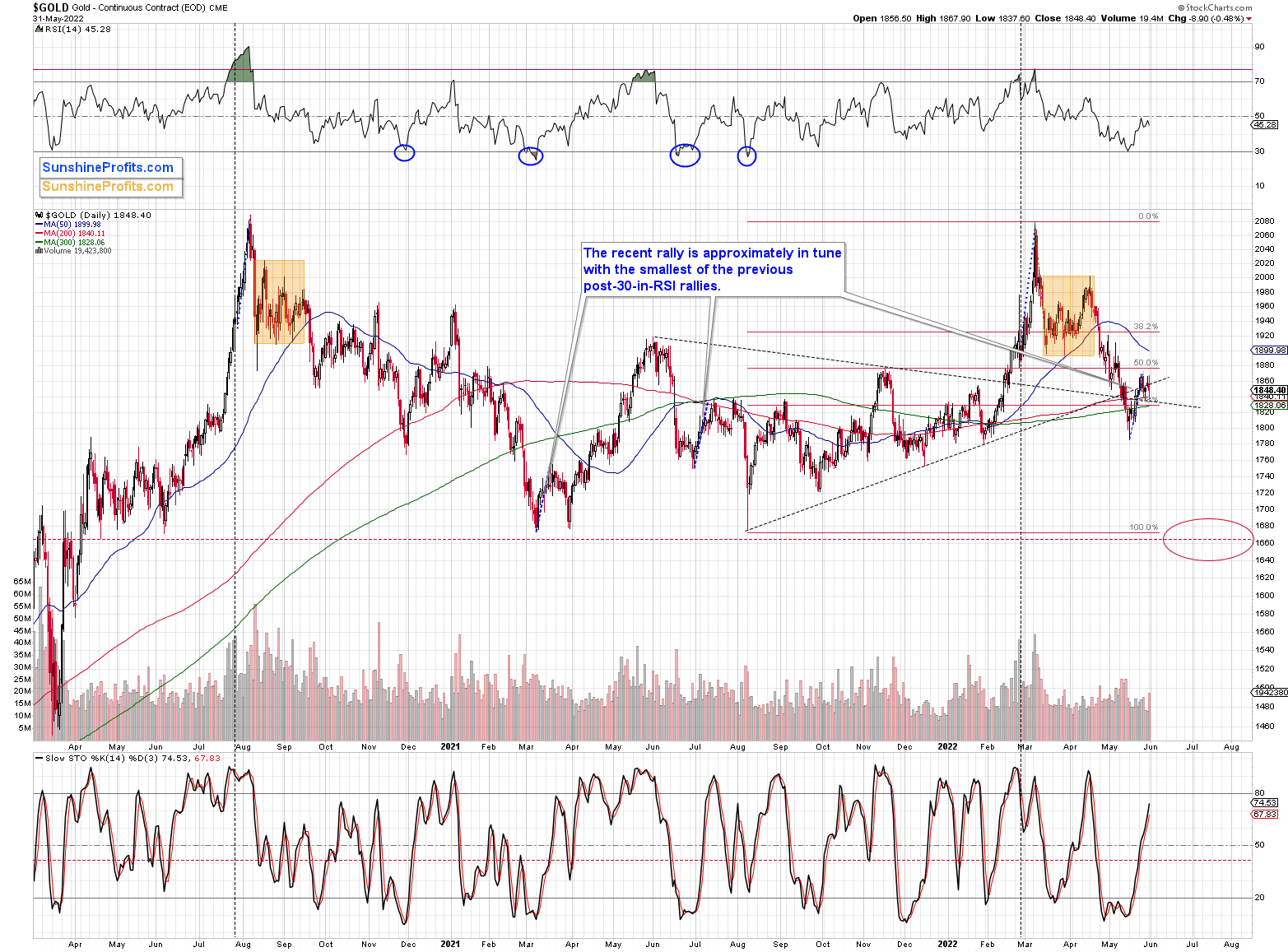

Is the very short-term top in? That appears likely, though it’s not 100% certain. The GDXJ appears to have topped in the lower part of my target area, and the same goes for the RSI (which might have topped close to 50, just like it did in early 2020).

The gold market doesn’t provide any major clues right now, except for the fact that we saw a substantial increase in volume while gold declined. That’s bearish, but not very strongly so. It doesn’t have to be, though, as based on multiple other factors, gold is likely to decline in the medium term and analogies to previous huge declines are only one of them. Rising real interest rates and the USD Index are the two key bearish drivers of gold prices.

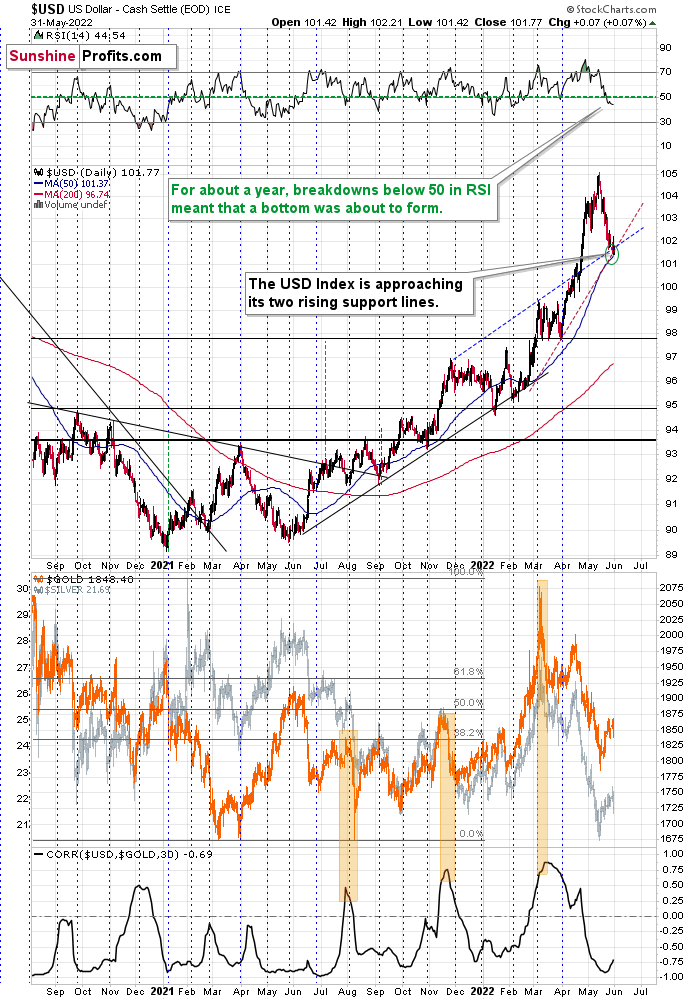

Speaking of the USD Index, it seems that it might have just bottomed right in my target area.

The combination of two rising support lines (and the 50-day moving average) was likely to stop the pullback, and we might have seen exactly that.

Please keep in mind that the RSI below 50 also indicated good buying opportunities for the USD Index during the recent run-up.

Most importantly, though, let’s keep in mind that gold stopped reacting to USDX’s weakness recently as it didn’t move to new highs while the former moved to new short-term lows.

The above is a powerful bearish combination of factors for the precious metals market.

All in all, it seems that we’re about to see another sizable decline in the prices of junior mining stocks, and while I can’t promise any performance, it seems likely to me that profits on our short positions will increase substantially.

Having said that, let’s take a look at the markets from a more fundamental point of view.

Mounting Pressure

While I've been warning since 2021 that inflation would surprise to the upside and force the Fed's hand, the latter's rate hike cycle is already underway. Moreover, with quantitative tightening (QT) – where the Fed sells assets on its balance sheet – scheduled to commence today, the liquidity drain should have drastic consequences for the PMs and the S&P 500 over the next few months.

To explain, while investors assume that inflation will peak and normalize without any material impact on the U.S. economy or the financial markets, a realization contrasts nearly 70 years of history. For context, I wrote on May 26:

While 50 basis point rate hikes are likely done deals in June and July, a realization will only put the U.S. federal funds rate at 1.83%. With annualized inflation at 8%+, calming the price pressures with such little action is completely unrealistic. In fact, it’s never happened.

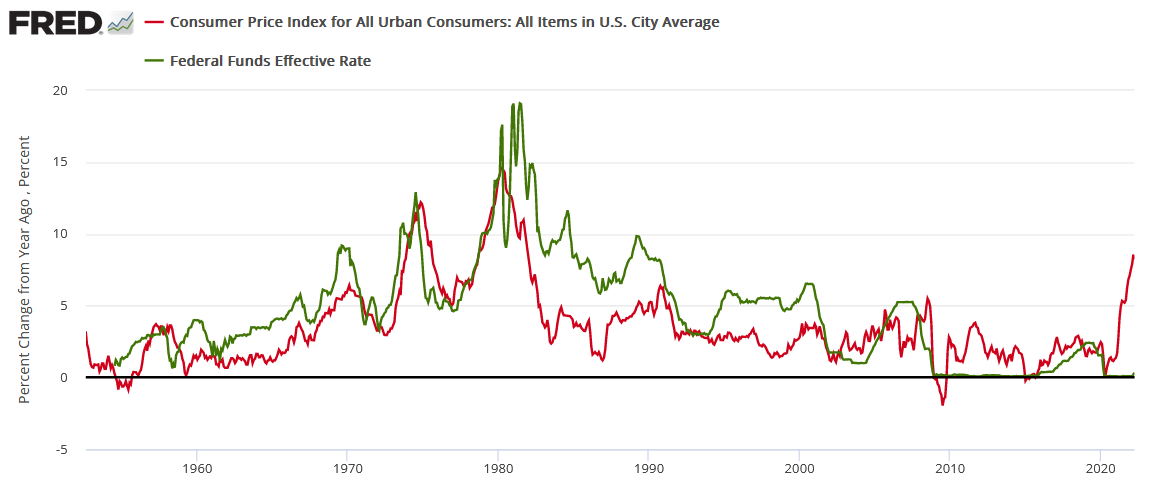

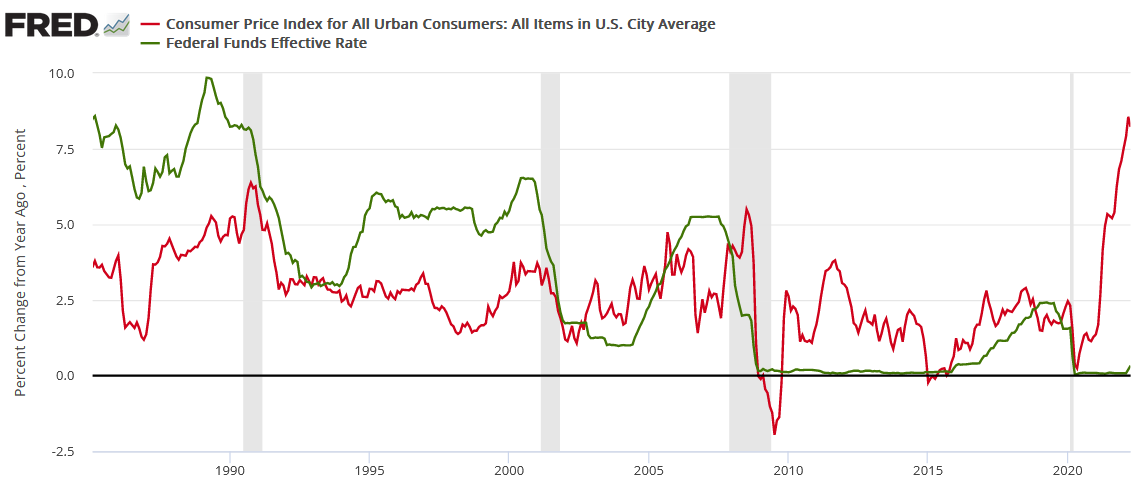

If you analyze the chart below, you can see that the U.S. federal funds rate (the green line) nearly always rises above the year-over-year (YoY) percentage change in the headline Consumer Price Index (the red line) to curb inflation. Therefore, investors are kidding themselves if they think the Fed is about to re-write history.

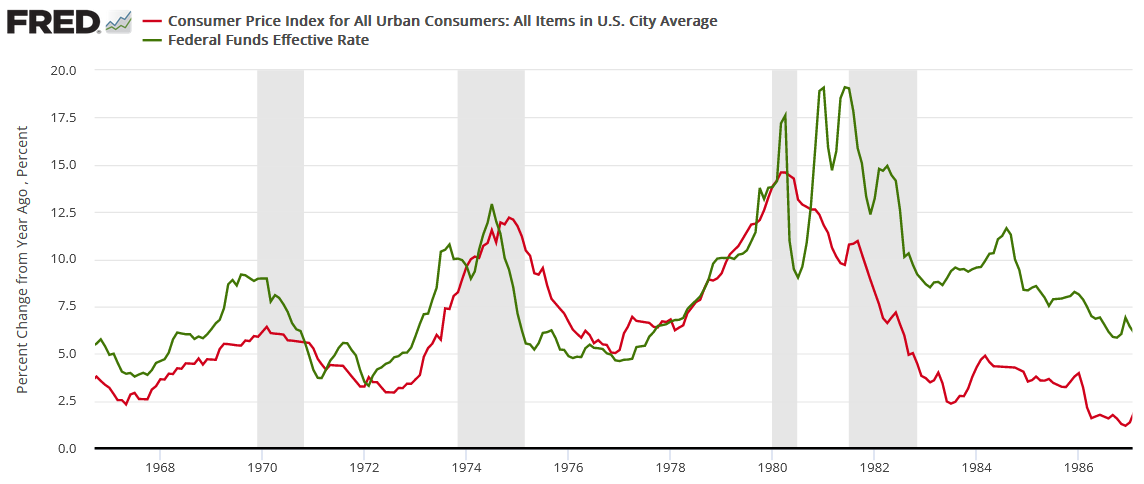

Furthermore, while the consensus either doesn't care or doesn't know history, unanchored inflation in the 1970s/1980s pushed the U.S. into recession four times over ~12 years (the vertical gray bars below). For context, if we exclude the COVID-19 pandemic, the U.S. has only entered a recession once in the last 20 years. Thus, putting a Band-Aid on a gunshot wound won't do much good.

Please see below:

Likewise, modern history sings a similar tune. For example, the Fed has never curbed inflation without the U.S. federal funds rate eclipsing the YoY CPI rate at some point. Therefore, if the Fed pauses at 1.83% and inflation falls to its 2% target, Powell and his crew would accomplish something that’s never been done.

To that point, notice how every inflation spike leads to a higher U.S. federal funds rate and then a recession. As such, do you really think this time is different?

Also, the only immaterial rebuttal is when inflation increased in 2011 and calmed down on its own. However, the headline CPI peaked at 3.81%, and that’s nothing like the current situation. Second, the S&P Goldman Sachs Commodity Index (S&P GSCI) declined by 25% from its 2011 peak.

For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products and two precious metals. However, energy accounts for roughly 54% of the index’s movement.

Please see below:

As a result, like I wrote on May 31, the only bullish outcome is if economically-sensitive commodities collapse on their own. Then, input inflation would subside and eventually cool output inflation, and the Fed could turn dovish.

However, the central bank has been awaiting this outcome for two years. Thus, my comments from Apr. 6 remain critical. If investors continue to bid up stock prices, the follow-through from commodities will only intensify the pricing pressures in the coming months. Therefore, investors are flying blind once again.

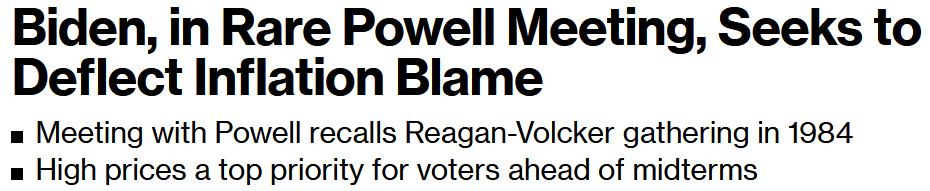

Yet, while the consensus still assumes that the Fed will accomplish the impossible, the political blame game has intensified.

Please see below:

Source: Bloomberg

Source: Bloomberg

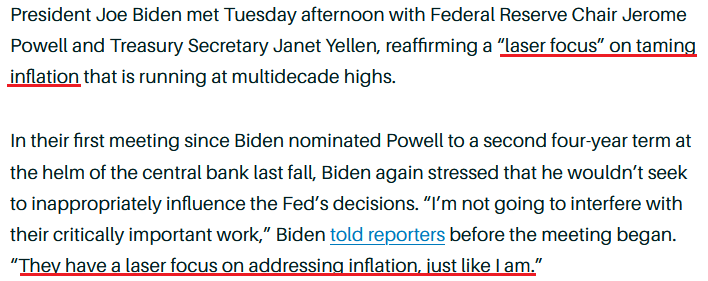

Furthermore, before meeting with Fed Chairman Jerome Powell on May 31, U.S. President Joe Biden emphasized the importance of curbing inflation. He said:

Source: Barron’s

Source: Barron’s

Likewise, Biden wrote the following in the Wall Street Journal on May 30:

“I ran for president because I was tired of the so-called trickle-down economy. We now have a chance to build on a historic recovery with an economy that works for working families. The most important thing we can do now to transition from rapid recovery to stable, steady growth is to bring inflation down. That is why I have made tackling inflation my top economic priority.”

“The Federal Reserve has a primary responsibility to control inflation. My predecessor demeaned the Fed, and past presidents have sought to influence its decisions inappropriately during periods of elevated inflation. I won’t do this. I have appointed highly qualified people from both parties to lead that institution. I agree with their assessment that fighting inflation is our top economic challenge right now.”

In addition, Cecilia Rouse, Biden’s Chair of the Council of Economic Advisers, told Bloomberg on May 31 that Biden “plans to stay out of [the Fed’s] way. The President wants to say, go forth and do what you need to do.”

As a result, while the “transitory” gambit continues to unravel, the political consequences of inflation have come to bear. Moreover, I warned on Nov. 18 that the war was already underway. I wrote:

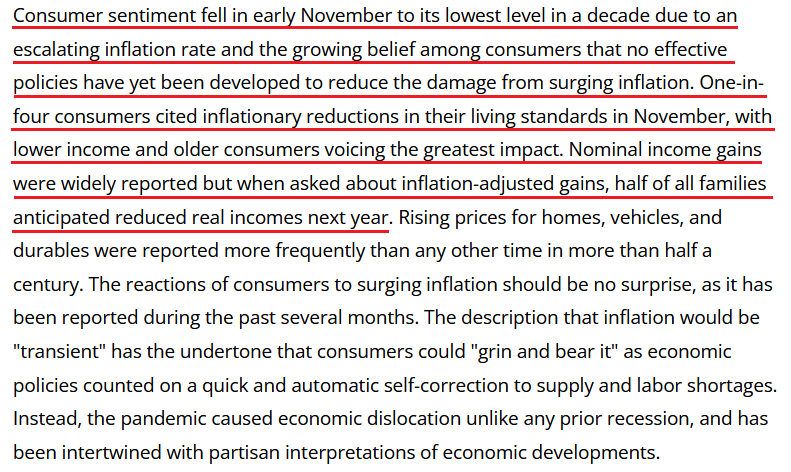

The University of Michigan released its Consumer Sentiment Index on Nov. 12. With the index hitting a 10-year low, it’s no coincidence that the White House (and soon likely the Fed) has made inflation Public Enemy No. 1.

Please see below:

Source: the University of Michigan

Source: the University of Michigan

Second, the political component shouldn’t be ignored. Biden’s approval ratings keep hitting new lows along with consumer confidence. Thus, is it in his best interest to maintain the status quo? Of course not. That’s why he’s been so forceful on inflation over the last few weeks. Essentially, if he (and/or the Fed) does nothing, he’ll likely lose the next presidential election and the Democrats will likely lose control of Congress. However, if he tames inflation, then he’s a hero. Left with those two options, which one do you think he’ll choose?

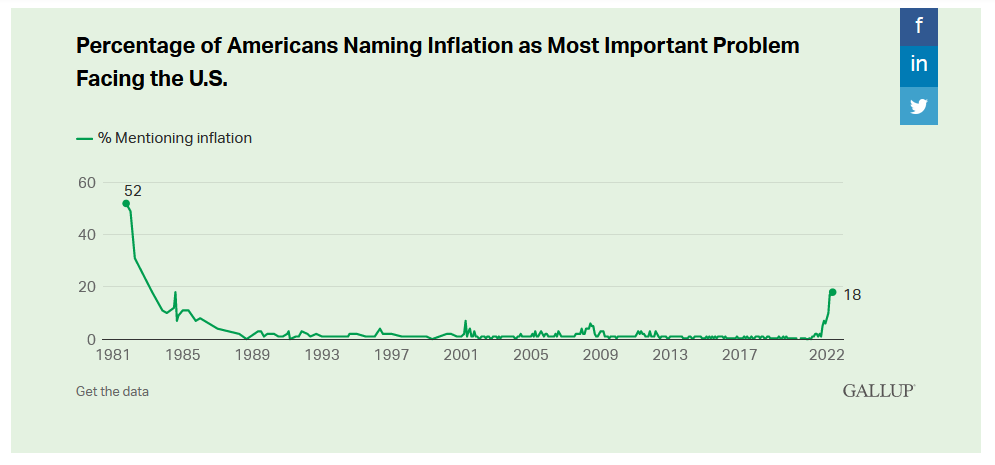

To that point, Gallup released its Economic Confidence Index on May 31. It declined from -39 in April to -45 in May, and the report stated: “It is the lowest reading in Gallup's trend during the coronavirus pandemic, and likely the lowest confidence has been since the tail end of the Great Recession in early 2009.”

In addition:

“Mentions of inflation have leveled off since March, with readings of 17% or 18%, after increasing throughout the fall and winter months. They remain relatively high compared with recent history but have been higher in the past, including 52% in October 1981, 49% in January 1982 and 31% in April 1982, around the time inflation was last at its current rate. Inflation had been named by an average of 1% of Americans between 1990 and 2021.”

Therefore, with inflation now obvious to investors, the Fed and the general public, the trio can’t run from reality anymore.

Please see below:

Also noteworthy, the Institute for Supply Management (ISM) released its Chicago PMI on May 31. The report revealed:

“Prices Paid expanded by 2.5 points to 88.6 with over three-quarters of firms inferring higher prices. Raw material, labor and shipping costs were acute. Some firms did see prices easing in certain commodities.”

Similarly, the Dallas Fed released its Texas Manufacturing Outlook Survey on May 31. The report revealed:

“Labor market measures indicated robust employment growth and longer workweeks. The employment index edged down four points to 20.9 but remained highly elevated. Thirty-one percent of firms noted net hiring, while 11 percent noted net layoffs. The hours worked index also remained elevated but edged down to 7.4.”

“Prices and wages continued to increase strongly in May. The raw materials prices index held steady at 61.8 – more than twice its average of 27.8. The finished goods prices index was also largely unchanged at a highly elevated reading of 41.8. The wages and benefits index came in at 50.5, similar to April and markedly higher than its 20.2 average.”

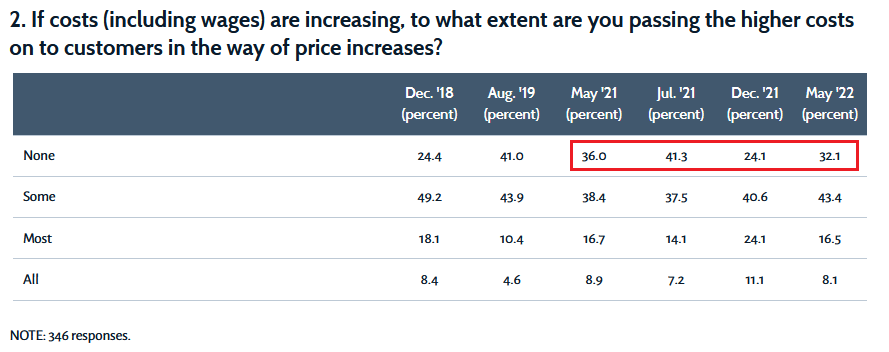

On top of that, survey respondents were asked about passing on higher wages and input costs to consumers. Moreover, while the percentage of respondents not passing on the costs increased from 24.1% in December to 32.1% in May, the latter is lower than the readings from May and July 2021. As a result, ~68% of Texas manufacturing, service, and retail companies are still raising their prices.

Please see below:

Source: Dallas Fed

Source: Dallas Fed

The bottom line? Investors are running towards a cliff, and they don’t even know it. With nearly 70 years of history showing that unanchored inflation ends in a recession, the idea of doing so little and achieving a “soft landing” materially lacks credibility.

Moreover, it’s ironic that the consensus assumes a dovish pivot from the Fed will cure all of the financial market’s ills. In reality, ignoring inflation would have catastrophic long-term consequences. The longer officials wait, the more damage they create.

In conclusion, the PMs declined on May 31, as optimism turned to pessimism on Wall Street. However, while investors and the Fed search for a magical solution to their inflation problem, history has humbled those who want to have their cake and eat it too. As a result, this time should be no different.

Overview of the Upcoming Part of the Decline

- It seems to me that the short-term rally in the precious metals market is either over or very close to being over. It’s so close to being over that I think it’s already a good idea to be shorting junior mining stocks.

- We’re likely to (if not immediately, then soon) see another big slide, perhaps close to the 2021 lows ($1,650-$1,700).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, it seems to me that the short-term rally in the precious metals market is either over or close to being over. In fact, it’s so close to being over that I think it’s already a good idea to be shorting junior mining stocks.

I previously wrote that the profits from the previous long position (congratulations once again) were likely to further enhance the profits on this huge decline, and that’s exactly what happened. The profit potential with regard to the upcoming gargantuan decline remains huge.

As investors are starting to wake up to reality, the precious metals sector (particularly junior mining stocks) is declining sharply. Here are the key aspects of the reality that market participants have ignored:

- rising real interest rates,

- rising USD Index values.

Both of the aforementioned are the two most important fundamental drivers of the gold price. Since neither the USD Index nor real interest rates are likely to stop rising anytime soon (especially now that inflation has become highly political), the gold price is likely to fall sooner or later. Given the analogy to 2012 in gold, silver, and mining stocks, “sooner” is the more likely outcome.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $27.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $19.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $17.22

SLV profit-take exit price: $16.22

ZSL profit-take exit price: $41.87

Gold futures downside profit-take exit price: $1,706

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $11.87

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $31.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief