tools spotlight

-

Wake Up, Gold Market! Otherwise Inflation Will Step on You

March 23, 2022, 9:31 AMThe Fed's hawkish alerts seem like a voice in the wilderness to gold investors. However, a carefree attitude can backfire on them – in just a few months.

An epic battle is unfolding across the financial markets as the Fed warns investors about its looming rate hike cycle and the latter ignores the ramifications. However, with perpetually higher asset prices only exacerbating the Fed's inflationary conundrum, a profound shift in sentiment will likely occur over the next few months.

To explain, I highlighted in recent days how the Fed has turned the hawkish dial up to 100. Moreover, I wrote on Mar. 22 that it's remarkable how much the PMs' domestic fundamental outlooks have deteriorated in recent weeks. Yet, prices remain elevated, investors remain sanguine, and the bullish bands continue to play.

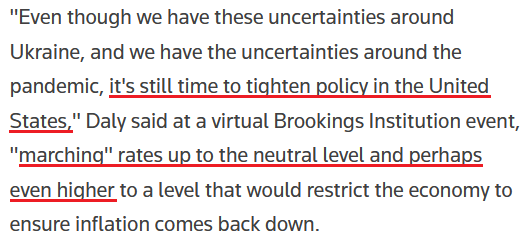

However, with inflation still rising and the Fed done playing games, the next few months should elicit plenty of fireworks. For example, with another deputy sounding the hawkish alarm, San Francisco Fed President Mary Daly said on Mar. 22: "Inflation has persisted for long enough that people are starting to wonder how long it will persist. I'm already focused on letting make sure this doesn't get embedded and we see those longer-term inflation expectations drift up."

As a result, Daly wants to ensure that the "main risk" to the U.S. economy doesn't end up causing a recession.

Please see below:

Source: Reuters

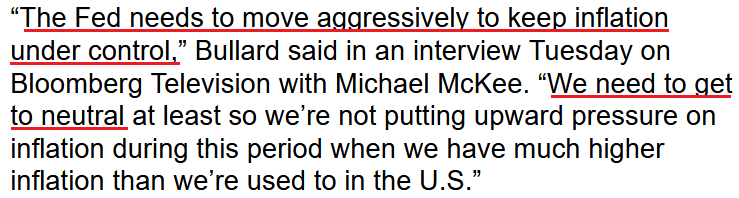

Source: ReutersLikewise, St. Louis Fed President James Bullard reiterated his position on Mar. 22, telling Bloomberg that “faster is better,” and that “the 1994 tightening cycle or removal of accommodation cycle is probably the best analogy here.”

Please see below:

Source: Bloomberg

Source: BloombergFalling on Deaf Ears

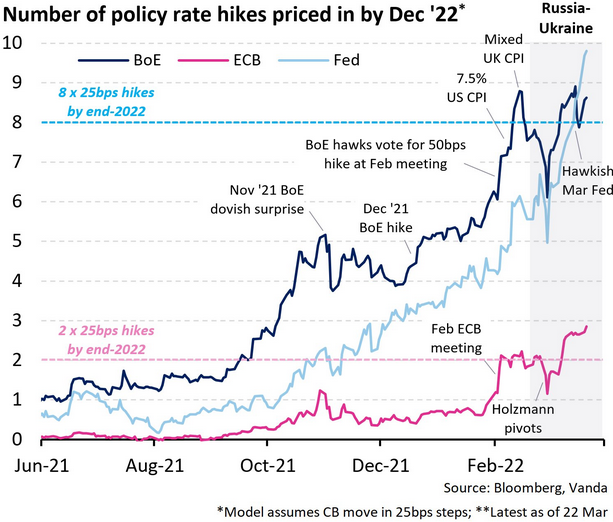

To that point, while investors seem to think that the Fed can vastly restrict monetary policy without disrupting a healthy U.S. economy, a major surprise could be on the horizon. For example, the futures market has now priced in nearly 10 rate hikes by the Fed in 2022. As a result, should we expect the hawkish developments to unfold without a hitch?

Please see below:

To explain, the light blue, dark blue, and pink lines above track the number of rate hikes expected by the Fed, BoE, and ECB. If you analyze the right side of the chart, you can see that the light blue line has risen sharply over the last several days and months. For your reference, if you focus your attention on the material underperformance of the pink line, you can see why I’ve been so bearish on the EUR/USD for so long.

Also noteworthy, please have a look at the U.S. 2-Year Treasury yield minus the German 2-Year Bond yield spread. If you analyze the rapid rise on the right side of the chart below, you can see how much short-term U.S. yields have outperformed their European counterparts in 2021/2022.

Source: Bloomberg/ Lisa Abramowicz

Source: Bloomberg/ Lisa AbramowiczMore importantly, though, with Fed officials’ recent rhetoric encouraging more hawkish re-pricing instead of talking down expectations (like the ECB), they want investors to slow their roll. However, investors are now fighting the Fed, and the epic battle will likely lead to profound disappointment over the medium term.

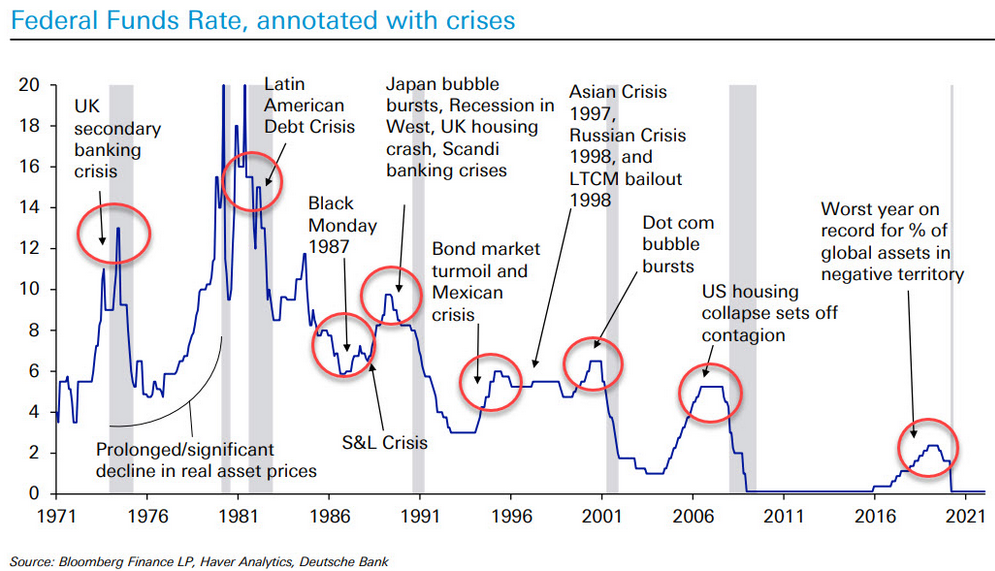

Case in point: when Fed officials dial up the hawkish rhetoric, their “messaging” is supposed to shift investors’ expectations. As such, the threat of raising interest rates is often as impactful as actually doing it. However, when investors don’t listen, the Fed has to turn the hawkish dial up even more. If history is any indication, a calamity will eventually unfold.

Please see below:

To explain, the blue line above tracks the U.S. federal funds rate, while the various circles and notations above track the global crises that erupted during the Fed’s rate hike cycles. As a result, standard tightening periods often result in immense volatility.

However, with investors refusing to let asset prices fall, they’re forcing the Fed to accelerate its rate hikes to achieve its desired outcome (calm inflation). As such, the next several months could be a rate hike cycle on steroids.

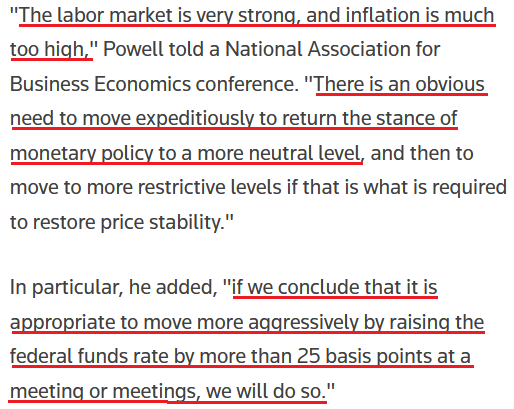

To that point, with Fed Chairman Jerome Powell dropping the hawkish hammer on Mar. 21, I noted his response to a question about inflation calming in the second half of 2022. I wrote on Mar. 22:

"That story has already fallen apart. To the extent it continues to fall apart, my colleagues and I may well reach the conclusion we'll need to move more quickly and, if so, we'll do so."

To that point, Powell said that “there’s excess demand" and that "the economy is very strong and is well-positioned to handle tighter monetary policy." As a result, while investors seem to think that Powell’s bluffing, enlightenment will likely materialize over the next few months.

Please see below:

Source: Reuters

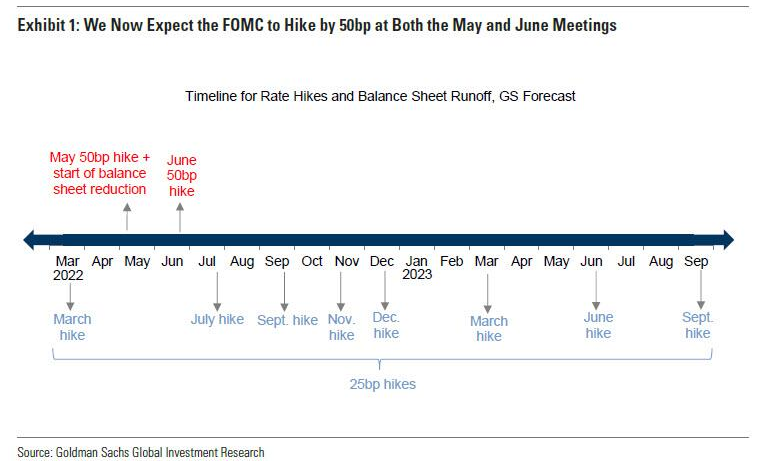

Source: ReutersFurthermore, with Goldman Sachs economists noting the shift in tone from “steadily” in January to “expeditiously” on Mar. 21, they also upped their hawkish expectations. They wrote:

“We are now forecasting 50bp hikes at both the May and June meetings (vs. 25bp at each meeting previously). The level of the funds rate would still be low at 0.75-1% after a 50bp hike in May, and if the FOMC is open to moving in larger steps, then we think it would see a second 50bp hike in June as appropriate under our forecasted inflation path.”

“After the two 50bp moves, we expect the FOMC to move back to 25bp rate hikes at the four remaining meetings in the back half of 2022, and to then further slow the pace next year by delivering three quarterly hikes in 2023Q1-Q3. We have left our forecast of the terminal rate unchanged at 3-3.25%, as shown in Exhibit 1.”

Please see below:

In addition, this doesn’t account for the Fed’s willingness to sell assets on its balance sheet. For context, Powell said on Mar. 16 that quantitative tightening (QT) should occur sometime in the summer and that shrinking the balance sheet “might be the equivalent of another rate increase.” As a result, investors’ lack of preparedness for what should unfold over the next few months has been something to behold. However, the reality check will likely elicit a major shift in sentiment.

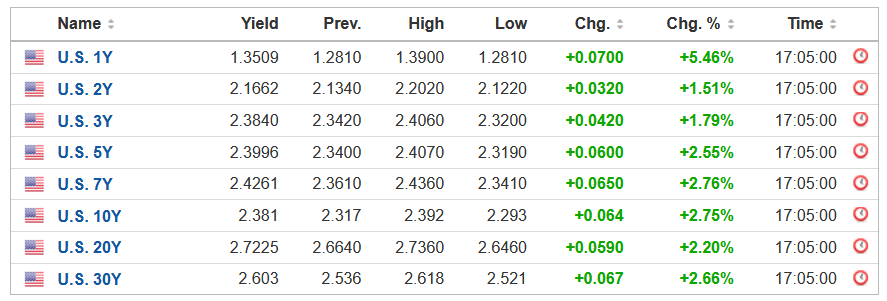

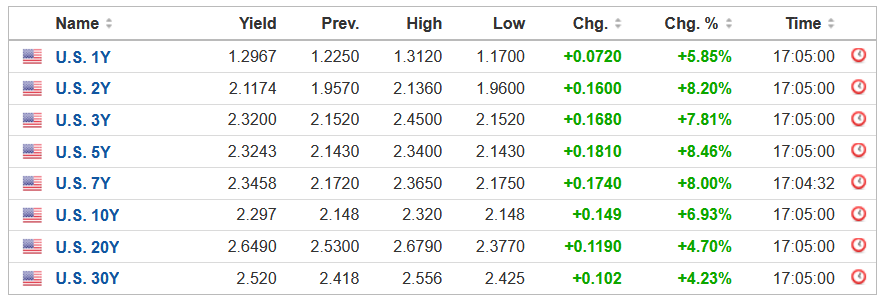

In contrast, the bond market heard Powell’s message loud and clear, and with the U.S. 10-Year Treasury yield hitting another 2022 high of ~2.38% on Mar. 22, the entire U.S. yield curve is paying attention.

Please see below:

Source: Investing.com

Source: Investing.comFinally, the Richmond Fed released its Fifth District Survey of Manufacturing Activity on Mar. 22. With the headline index increasing from 1 in February to 13 in March, the report cited “increases in all three of the component indexes – shipments, volume of new orders, and number of employees.”

Moreover, the prices received index increased month-over-month (MoM) in March (the red box below), while future six-month expectations for prices paid and received also increased (the blue box below). As a result, inflation trends are not moving in the Fed’s desired direction.

Please see below:

Source: Richmond Fed

Source: Richmond FedLikewise, the Richmond Fed also released its Fifth District Survey of Service Sector Activity on Mar. 22, nd while the headline index decreased from 13 in February to -3 in March, current and future six-month inflationary pressures/expectations rose MoM.

Source: Richmond Fed

Source: Richmond FedThe bottom line? While the Fed is screaming at the financial markets to tone it down to help calm inflation, investors aren't listening. With higher prices resulting in more hawkish rhetoric and policy, the Fed should keep amplifying its message until investors finally take note. If not, inflation will continue its ascent until demand destruction unfolds and the U.S. slips into a recession. As such, if investors assume that several rate hikes will commence over the next several months with little or no volatility in between, they're likely in for a major surprise.

In conclusion, the PMs declined on Mar. 22, as the sentiment seesaw continued. However, as I noted, it's remarkable how much the PMs' domestic fundamental outlooks have deteriorated in recent weeks. Thus, while the Russia-Ukraine conflict keeps them uplifted, for now, the Fed's inflation problem is nowhere near an acceptable level. As a result, when investors finally realize that a much tougher macroeconomic environment confronts them over the next few months, the shift in sentiment will likely culminate in sharp drawdowns.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Time for Investors to Accept That Gold Isn’t Soaring Yet?

March 22, 2022, 9:50 AMIt’s déjà vu all over again. With the PMs still ignoring technicals and fundamentals, their strength on Mar. 21 was akin to mining momentum. To explain, I wrote on Mar. 18:

The weak fundamental outlook that caused gold to underperform the S&P GSCI in early 2022 has only intensified since the Fed meeting. Despite that, momentum investors are following the trend and rallies in crude are sparking rallies in the metals.

To that point, with WTI rallying hard on Mar. 21, the PMs remained elevated despite the sharply deteriorating domestic fundamental environment. However, peak sentiment may have already materialized, with the last (likely) piece of the headline risk puzzle commencing on Mar. 21. To explain, I wrote on Mar. 9:

While picture-perfect scenarios have confronted the PMs in recent weeks, the optimistic headlines are likely near their peak. For example, with U.S. economic sanctions already priced in and only Europe left to consider a Russian import ban, we'll need WW3 to create more headline risk.

Moreover, with WW3 unlikely in my opinion, whispers of a European import ban made the rounds on Mar. 21. As a result, the PMs’ news-based momentum may have received its final jolt.

Please see below:

Source: Reuters

Source: ReutersFurthermore, as headline risk decelerates, the main drivers of the PMs’ performance should become more important. Likewise, with the PMs’ domestic fundamental outlooks hitting new 2022 lows on Mar. 21, the next few months should elicit sharp drawdowns.

To explain, inflation remains extremely problematic. In fact, while signs of deceleration were present in January, the Russia-Ukraine conflict has supercharged commodities’ fervor and put the Fed in a precarious situation. However, even as Fed officials pivot from no rate hikes to three rate hikes to seven rate hikes, investors are not listening. As a result, market participants are digging their own graves.

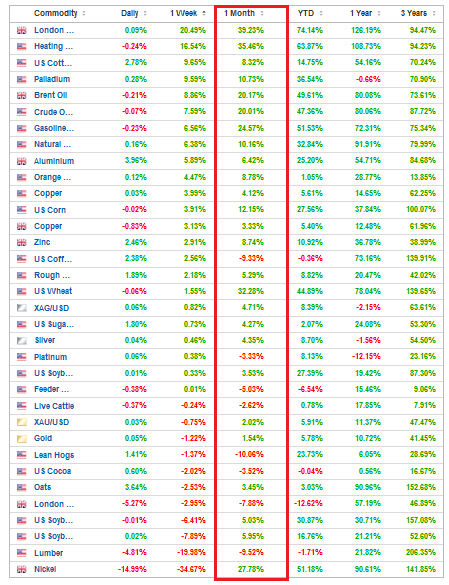

Please see below:

Source: Investing.com

Source: Investing.comTo explain, the table above tracks the performance of various commodities over different periods. If you analyze the vertical red rectangle, you can see that most commodities have rallied over the last month. As a result, investors are ignoring Fed officials’ warnings, as rate hikes help slow economic growth, not accelerate it. Think about it:

- Rate hikes increase borrowing costs and decrease consumers’ disposable income, which reduces demand.

- Less demand results in less consumption and less economic activity.

- Less economic activity results in less demand for commodities.

- Lower commodity demand results in lower commodity prices.

- Lower commodity prices result in lower input prices.

- Lower input prices result in lower output prices (inflation).

Moreover, while officials understand this relationship and hope to achieve this outcome, investors are now fighting the Fed. As such, if (when) the wake-up call materializes, the PMs should suffer profoundly.

As evidence, Fed Chairman Jerome Powell dropped the hawkish hammer on Mar. 21. When asked about inflation peaking this quarter and cooling in the second half of the year, he said:

"That story has already fallen apart. To the extent it continues to fall apart, my colleagues and I may well reach the conclusion we'll need to move more quickly and, if so, we'll do so."

To that point, Powell said that “there’s excess demand" and that "the economy is very strong and is well-positioned to handle tighter monetary policy." As a result, while investors seem to think that Powell’s bluffing, enlightenment will likely materialize over the next few months.

Please see below:

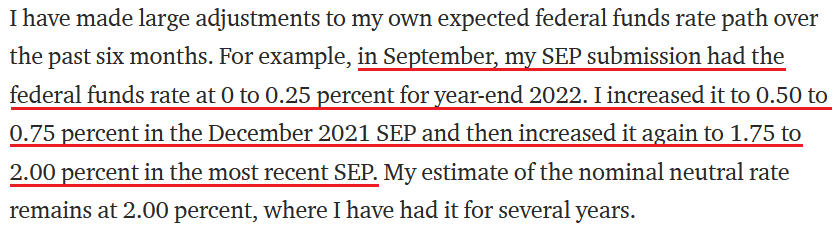

Source: ReutersThus, have you ever seen Powell more hawkish? In addition, notice how he said “at a meeting or meetings” when discussing the potential for “more than” 25 basis point rate hikes. As such, while Minneapolis Fed President Neel Kashkari (a major dove) had expected zero-to-one rate hikes in 2022 when submitting his projections in September, Powell let investors know that the Fed may double up “at a meeting or meetings.” For context, this is what Kashkari wrote on Mar. 18:

Source: Neel Kashkari/Medium

Source: Neel Kashkari/MediumFrom Bad to Worse

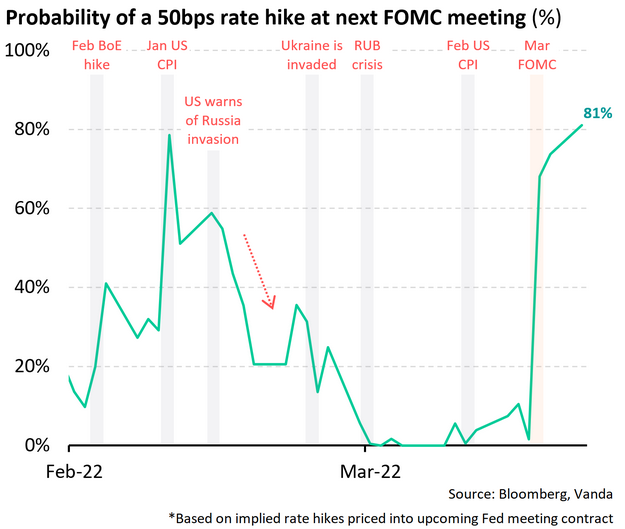

Furthermore, while some investors seem to think that the Fed will sit idly by and watch inflation rage, the futures market has priced in an 81% chance that the Fed will hike rates by 50 basis points on May 4.

Please see below:

To explain, the green line above tracks the market-implied probability of a 50 basis point rate hike on May 4. While the Russia-Ukraine conflict initially reduced the chance to zero, expectations have risen sharply recently. As a result, if commodity investors don’t listen to Powell and they keep bidding up prices, he’ll have no choice but to follow through with his hawkish threats.

To that point, I noted on Mar. 21 how the PMs are ignoring the materially shifting narrative. I wrote:

While the PMs have ridden the momentum of the Russia-Ukraine conflict, their medium-term fundamentals are worse now than they were in 2021. Back then, the Fed parroted the “transitory” narrative, and the PMs could take solace in their dovish pushback. However, the inflation outlook has worsened in the last few months, and commodities’ fervor is only accelerating the problem. Moreover, when doves like Kashkari turn hawkish, the game has changed. As a result, the PMs may learn this lesson the hard way over the medium term.

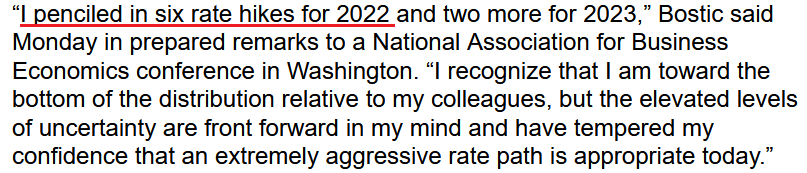

If that wasn’t enough, while Atlanta Fed President Raphael Bostic expects six rate hikes in 2022, his less-than-consensus view is still hawkish relative to where he was three months ago.

Please see below:

Source: Bloomberg

Source: Bloomberg In addition, he added:

“I am comfortable with more aggressive movements if that is what the data and the evidence suggests is what is appropriate. So I’m not wedded to moving only 25 basis points. I’m not wedded to moving every other meeting. I am going to be very, very open in terms of my approach.”

Thus, while the PMs seem to think that the Fed’s inflation fight won’t impact their medium-term prospects, the reality is that higher real interest rates are needed to reduce inflation. With commodity investors failing to comply, the merry-go-round of higher input prices leading to higher output prices will continue. As a result, the downside risk confronting the PMs is enormous at this point.

Finally, while the PMs and the general stock market covered their ears on Mar. 21, the bond market heard Powell’s message loud and clear. For example, the U.S. 10-Year Treasury yield closed at a new 2022 high of ~2.30% on Mar. 21. Moreover, the entire U.S. yield curve rallied sharply. As such, since the PMs’ domestic fundamental outlooks have materially worsened during the Russia-Ukraine conflict, they’re likely to suffer profound declines when prices revert to their intrinsic values.

Source: Investing.com

Source: Investing.comThe bottom line? While Europe's potential import ban helped underwrite another daily rally for crude and other commodities, the higher the prices, the more hawkish the Fed. Since investors don't realize that their short-term bullishness is actually medium-term bearish, epic drawdowns should materialize once sentiment shifts.

Remember, the Fed can only slow inflation by slowing the U.S. economy. That's why Powell keeps referencing a "soft landing" when describing the tradeoff between calming inflation and maintaining growth. However, with continued inflation of 8%+ likely to push the U.S. into recession, Powell knows that doing nothing is as bad as doing too much. As a result, investors should eventually learn that Powell's dovish days are over.

In conclusion, the PMs rallied on Mar. 21, as the Russia-Ukraine conflict still garners all of investors' attention. However, it's remarkable how much the PMs' domestic fundamental outlooks have deteriorated in recent weeks. With Fed officials more hawkish now than at any point in 2021, their fight with inflation is bullish for the USD Index and U.S. Treasury yields, not the PMs. As a result, don't be surprised if (when) a flash crash materializes.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Fed’s Plans Are Now Predatory. Will Gold Fall Prey to Them?

March 21, 2022, 9:23 AMWith rampant inflation forcing the Fed into a hawkish corner, I warned throughout 2021 that the end of looser-for-longer monetary policy would surprise investors. To explain, I wrote on Aug. 31:

With Fed Chairman Jerome Powell threading the dovish needle on Aug. 27, investors rejoiced as he downplayed the consequences of surging inflation. However, while his perpetual patience may elicit comfort in the short term, the medium-term ramifications could end up shocking the financial markets.

Case in point: while Powell allows the economy to run hot, his lack of prudence has left him far behind the inflation curve. With one policy mistake liable to result in an accelerated rate hike cycle once the Fed finally moves, his ability to placate investors could come under immense pressure.

Now, with the most dovish Fed official sounding the hawkish alarm on Mar. 18, the PMs could suffer a hard landing as the liquidity drain unfolds. To explain, Minneapolis Fed President Neel Kashkari preached patience throughout all of 2021. However, in an article written on Mar. 18, he stated:

“In the September 2021 Summary of Economic Projections (SEP), I estimated inflation would be 4.2 percent for 2021 and 1.8 percent for 2022. Actual inflation for 2021 ended up being 5.8 percent, and I just increased my forecast this week to 4.5 percent for 2022. PCE inflation for the 12 months through January was 6.1 percent. What happened, and why were my forecasts about inflation wrong?”

Well, after citing multiple factors including supply chain disruptions, wage inflation and resilient consumer demand, he concluded:

“The FOMC has already made a profound shift in the past six months with its forward guidance on the path of the federal funds rate and the balance sheet, and I believe the SEP we just released is sending a strong signal that further reinforces our commitment to achieving our inflation target. The first hike we announced this week demonstrates that we will follow through on our guidance with action.”

More importantly, though, he said:

Source: Neel Kashkari/MediumThe Doves Are Gone

Thus, the most dovish Fed official of them all expects the U.S. federal funds rate to hit 1.75% to 2% by the end of 2022. For context, this implies seven to eight rate hikes, which is in line or slightly more than the FOMC's median estimate of seven. Moreover, when the doves turn hawkish, the medium-term implications are often profound. While the PMs remain elevated for the time being, their fundamental outlooks continue to worsen.

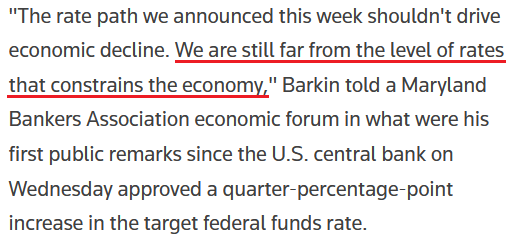

To that point, other Fed officials also made the rounds on Mar. 18. For example, Richmond Fed President Thomas Barkin said that "think of [the SEP] as an indication that the extraordinary support of the pandemic era is unwinding." Moreover, he stated that the U.S. federal funds rate still has plenty of room to run.

Please see below:

Source: Reuters

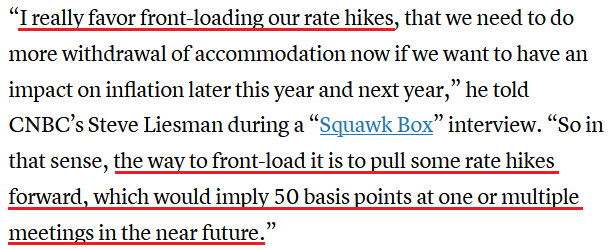

Source: ReutersLikewise, Fed Governor Christopher Waller told CNBC on Mar. 18 that “inflation is raging.” Moreover, he said that the neutral federal funds rate likely lies between 2% and 2.25%, and that the Fed should “try to be above that by the end of the year.” As a result, he’s advocating for more than eight or nine rate hikes by the end of 2022. For context, the neutral rate is the overnight lending rate that neither expands nor restricts the U.S. economy.

Furthermore, with inflation showing no signs of slowing down, Waller said that he expects a 50 basis point rate hike “at one or multiple meetings in the near future.”

Please see below:

Source: CNBC

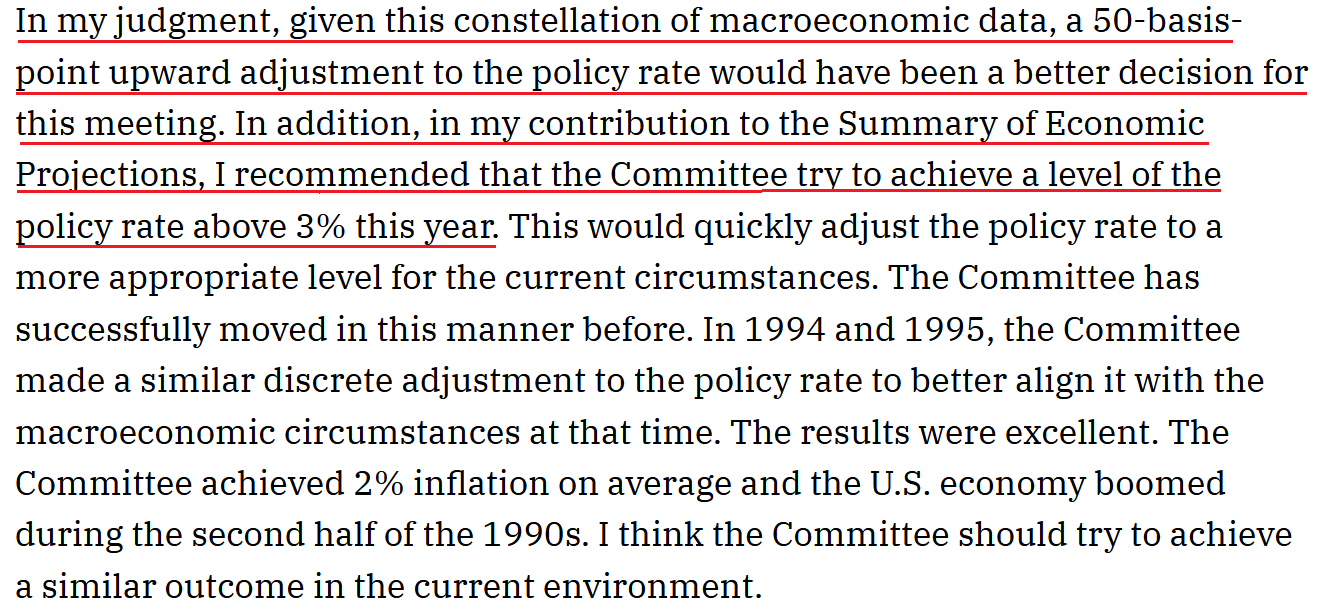

Source: CNBCIf that wasn’t enough, St. Louis Fed President James Bullard went rogue on Mar. 18. Releasing a statement about his dissatisfaction with the FOMC’s 25 basis point rate hike, he stated:

“I dissented with the Federal Open Market Committee (FOMC) decision announced on March 16, 2022, to raise the target range for the federal funds rate by 25 basis points to 0.25% to 0.50%. In my view, raising the target range to 0.50% to 0.75% and implementing a plan for reducing the size of the Fed’s balance sheet would have been more appropriate actions.”

He added:

“The combination of strong real economic performance and unexpectedly high inflation means that the Committee’s policy rate is currently far too low to prudently manage the U.S. macroeconomic situation. Moreover, U.S. monetary policy has been unwittingly easing further because inflation has risen sharply while the policy rate has remained very low, pushing short-term real interest rates lower. The Committee will have to move quickly to address this situation or risk losing credibility on its inflation target.”

As a result:

Source: James Bullard/ St. Louis Fed

Source: James Bullard/ St. Louis FedThus, while Bullard is clearly on the hawkish end of the spectrum, he’s advocating for 12 or more rate hikes by the end of 2022. Therefore, while the gold price remain sanguine due to the Russia-Ukraine conflict, the potential for seven to 12+ rate hikes is profoundly bearish. Moreover, with financial conditions already tight and poised to tighten further, these environments are often unkind to the entire commodity complex.

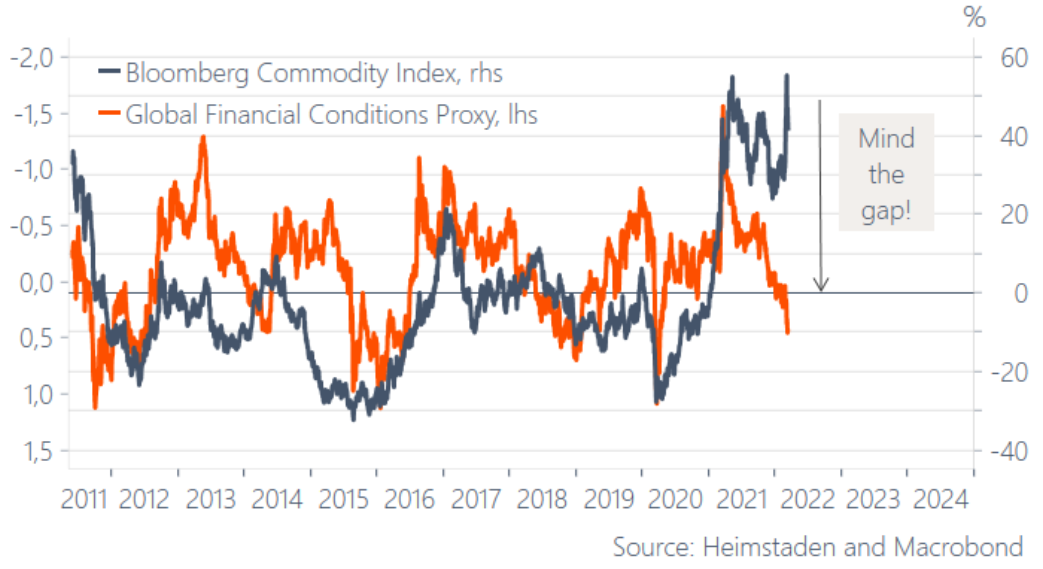

Please see below:

To explain, the blue line above tracks the year-over-year (YoY) percentage change in the Bloomberg Commodity Index, while the orange line above tracks the inverted YoY percentage change in global financial conditions. For context, inverted means that the latter’s scale is flipped upside down and that a falling orange line means that financial conditions are tightening.

If you analyze the relationship, you can see that tighter financial conditions often result in weaker performance by commodities.

Moreover, with the Fed poised to raise interest rates several times in the coming months, the liquidity drain should intensify. As a result, the PMs may suffer sharp declines when the profound divergence reverts to its historical norm.

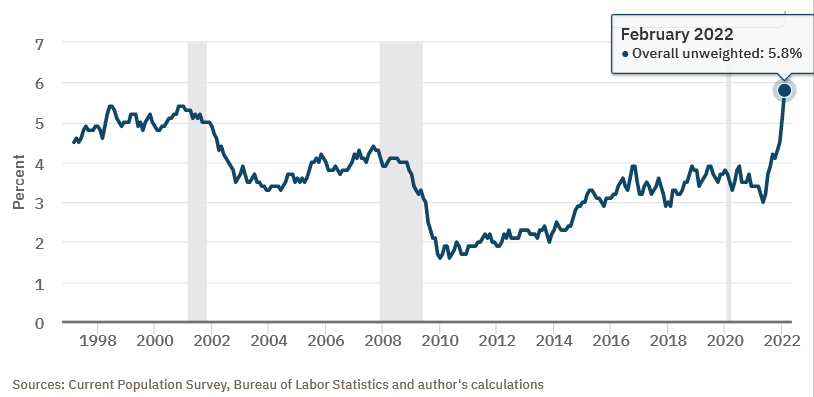

Furthermore, with the Fed still behind the inflation curve, a 25 basis point rate hike does little to calm the pricing pressures, and with the Atlanta Fed’s wage tracker hitting an all-time high in February, the wage-price spiral is unlikely to unwind without swift monetary intervention.

Please see below:

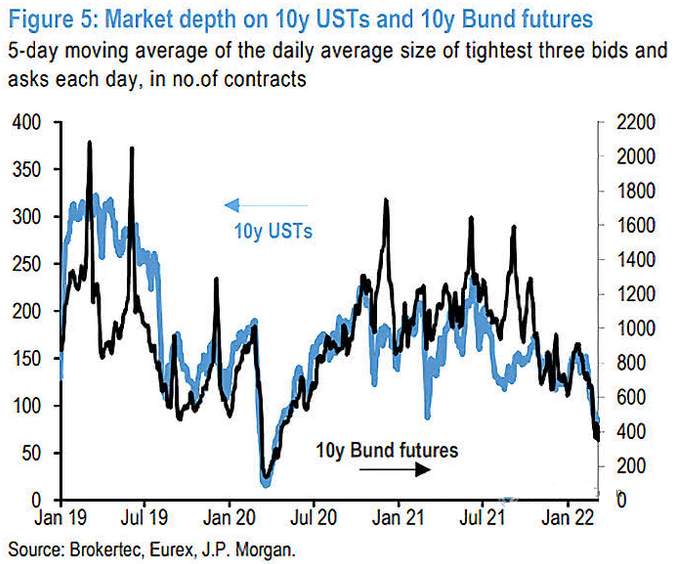

Finally, I noted previously that Treasury market depth continues to deteriorate. To explain, I wrote on Mar. 16:

The U.S. 10-Year Treasury yield rallied again on Mar. 15 and closed at another 2022 high of 2.15%. Moreover, with liquidity in the futures market continuing to deteriorate, more yield spikes could be on the horizon.

Please see below:

To explain, the black and blue lines above track the market depth for 10-Year Treasury and Bund (German bonds) futures. If you analyze the right side of the chart, you can see that the five-day moving average of the tightest bid-ask settlements continues to decline. As a result, a shallow market has resulted in more contracts being settled with wider bid-ask spreads.

In turn, this creates liquidity risk, as buyers may not be there when large sellers want to unwind 10-Year Treasury futures positions. Due to that, yields often spike when sellers outweigh buyers. As such, the more the blue line declines, the more it increases the chance of a taper-tantrum-like event.

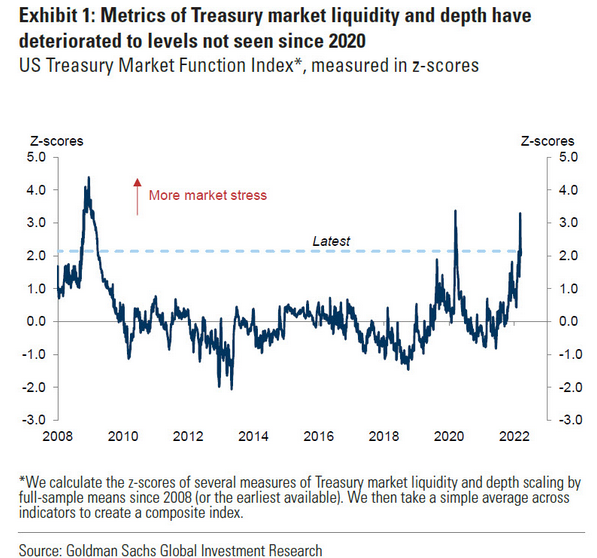

To that point, with data from Goldman Sachs singing a similar tune, the lack of liquidity in the Treasury market is near crisis levels. As a result, the Fed’s hawkish disposition could spark a rapid rise in interest rates.

Please see below:

To explain, the blue line above tracks the z-score of Treasury market liquidity, or lack thereof. If you analyze the right side of the chart, you can see that the liquidity crunch is more than three standard deviations above its average. As a result, if large sell orders can’t find any bids, a rapid rise in U.S. Treasury yields could profoundly impact the PMs.

The bottom line? While the prices of silver and gold have ridden the momentum of the Russia-Ukraine conflict, their medium-term fundamentals are worse now than they were in 2021. Back then, the Fed parroted the “transitory” narrative, and the PMs could take solace in their dovish pushback. However, the inflation outlook has worsened in the last few months, and the commodities’ fervor is only accelerating the problem. Moreover, when doves like Kashkari turn hawkish, the game has changed. As a result, the PMs may learn this lesson the hard way over the medium term.

In conclusion, the PMs declined on Mar. 18, as bearish realities are starting to catch up with gold, silver, and mining stocks. However, war premiums are still embedded, and they haven’t priced in the implications of the Fed’s battle with inflation. As such, sharp slides should confront the PMs over the next few months as the Fed’s rate hike cycle starts to have its desired effect.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Gold and Silver Turn a Deaf Ear to Fed’s Hawkish Threats

March 18, 2022, 9:40 AMWhile the week was full of drama, the Fed and the implications of its future monetary policy was the most important fundamental development to hit the newswire.

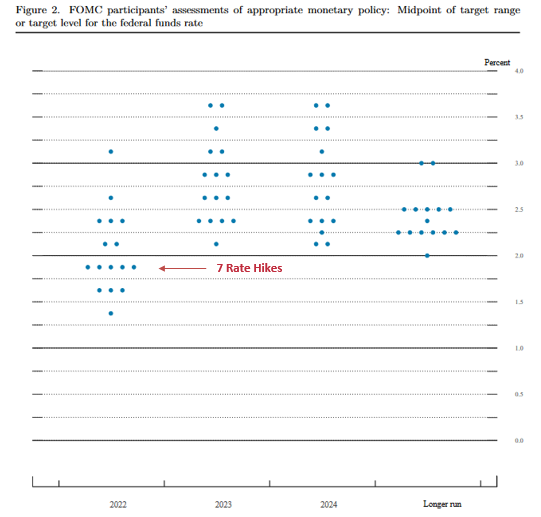

For example, the FOMC announced a 25 basis point rate hike on Mar. 16, and the median projection (the five dots below) is for six more rate hikes in 2022 (seven in total). Moreover, with six meetings left on the FOMC’s 2022 schedule, it implies consecutive rate hikes for the next several months.

Please see below:

Source: U.S. Fed

Source: U.S. FedMoreover, with FOMC officials’ median estimate increasing from three rate hikes in December to seven rate hikes in March, the hawkish ante has been upped with every new release of their Summary of Economic Projections (SEP).

However, while the developments are fundamentally bullish for the USD Index and U.S. Treasury yields, the PMs are behaving as if none of that matters. Moreover, with the Russia-Ukraine conflict distracting gold, silver, and mining stocks from domestic fundamental realities, their recent strength is a function of momentum, not medium-term technicals or fundamentals.

To explain, I spent a lot of time covering the S&P Goldman Sachs Commodity Index (S&P GSCI) this week and noted that it could act as the fundamental canary in the coal mine.

For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products, and two precious metals. However, energy accounts for roughly 54% of the index’s movement.

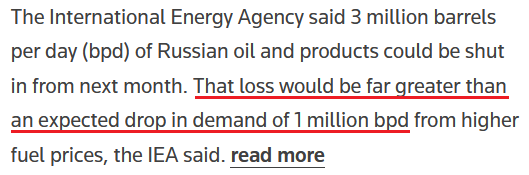

Furthermore, with the index rising and falling sharply in a matter of days, the PMs have been along for the ride. However, with the International Energy Agency (IEA) lighting a fire under crude on Mar. 17, it released a report outlining the potential shortfall of Russian oil in April. It stated:

“The prospect of large-scale disruptions to Russian oil production is threatening to create a global oil supply shock. We estimate that from April, 3 mb/d of Russian oil output could be shut in as sanctions take hold and buyers shun exports. OPEC+ is, for now, sticking to its agreement to increase supply by modest monthly amounts. Only Saudi Arabia and the UAE hold substantial spare capacity that could immediately help to offset a Russian shortfall.”

With financial markets all about expectations, the potential for a shortfall sent WTI 6.95% higher on Mar. 17.

Please see below:

Source: Reuters

Source: ReutersMoreover, since energy accounts for roughly 54% of the S&P GSCI’s movement and momentum begets momentum, the PMs are borrowing optimism and ignoring fundamentals. However, the short-term phenomena will likely result in sharp drawdowns over the medium term.

Please see below:

To explain, the red line above tracks the four-hour movement of the S&P GSCI, while the gold line above tracks the gold futures price. If you analyze their behavior before Russia invaded Ukraine, you can see little to no connection.

However, if you focus your attention on the price action since the Feb. 24 invasion, you can see that it’s become all one trade. Moreover, the weak fundamental outlook that caused gold to underperform the S&P GSCI in early 2022 has only intensified since the Fed meeting. However, despite that, momentum investors are following the trend and rallies in crude are sparking rallies in the metals.

As a result, the PMs’ rallies on Mar. 17 were more about momentum. However, with their medium-term fundamentals heading in the opposite directions, sharp drawdowns should materialize once the ‘all-for-one’ trade unwinds.

To that point, while the PMs may assume that the Fed won’t follow through on its hawkish forecast, the reality is that the U.S. economic outlook is bullish for hawkish Fed policy.

To explain, I wrote on Mar. 9:

The blue line above tracks the S&P 500, while the orange line above tracks Citigroup’s Economic Surprise Index. For context, a surprise occurs when an economic data point outperforms economists’ consensus estimate.

If you analyze the right side of the chart, you can see that the orange line bottomed in January and has been moving higher ever since. As a result, the U.S. economy remains in a healthy position, and as long as this is the case, it keeps the pressure on the Fed to raise interest rates at its next several monetary policy meetings.

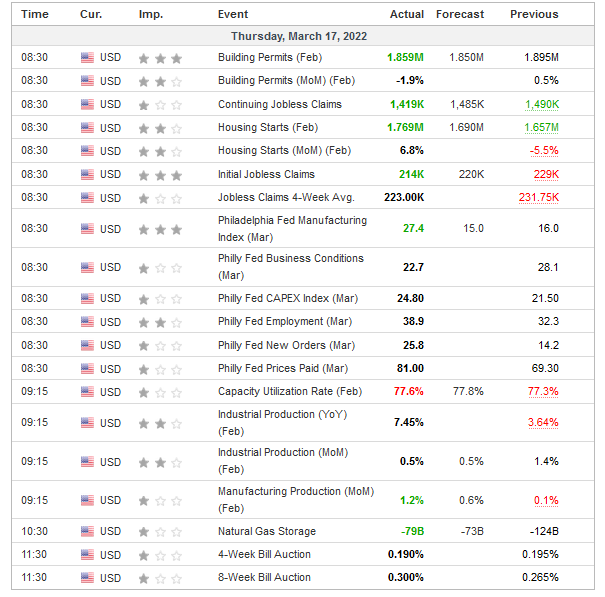

To that point, with more data released on Mar. 17, the outperformances continued.

Please see below:

Source: Investing.com

Source: Investing.com The U.S. Economy Condition

To explain, building permits, housing starts, manufacturing production, initial and continuing jobless claims, and the Philadelphia Fed’s manufacturing index all outperformed expectations on Mar. 17. As a result, they add upward momentum to Citigroup’s Economic Surprise Index. Moreover, with the Fed’s hawkish disposition dependent on the health of the U.S. economy, Thursday’s data only enhances the prospects of more rate increases.

For example, I wrote on Mar. 17: Powell noted during his press conference that there are ~1.7 job openings for every unemployed U.S. citizen. He added that “all signs are that this is a strong economy, one that will be able to flourish in the face of less accommodative monetary policy.”

Moreover, with continuing jobless claims hitting a new post-pandemic low on Mar. 17, the Fed’s maximum employment mandate remains on the hawkish side of the spectrum.

Please see below:

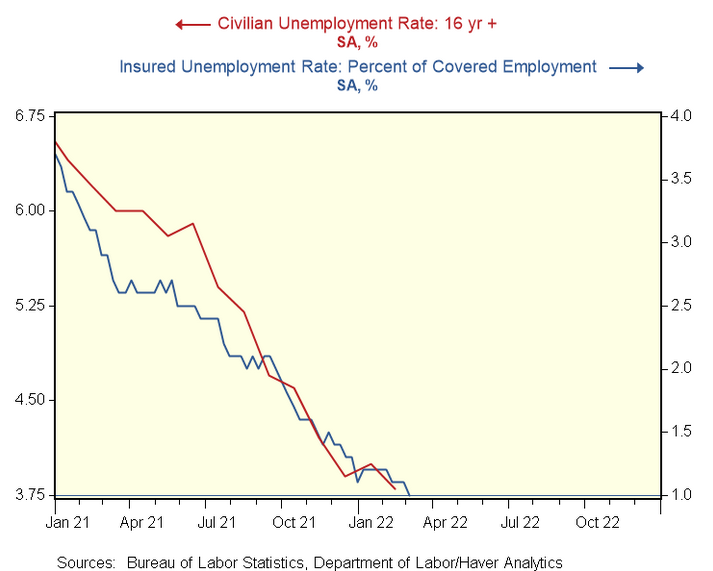

To explain, the red line above tracks the civilian unemployment rate, while the blue line above tracks the insured unemployment rate. For context, the latter calculates the number of U.S. citizens collecting unemployment as a percentage of the U.S. labor force. Moreover, the metric dropping to 1% on Mar. 17 highlights how U.S. labor market strength should keep the Fed’s foot on the hawkish accelerator.

Second, I also noted on Mar. 17 that the critical development is Powell’s view of the U.S. economy. In a nutshell: if Powell believes the U.S. economy is in a healthy position, then he’ll raise interest rates until he no longer thinks that’s the case. With his remarks on Mar. 17 signaling more hawkish policy to come, the PMs should suffer the consequences over the medium term.

Please see below:

Source: CNBC

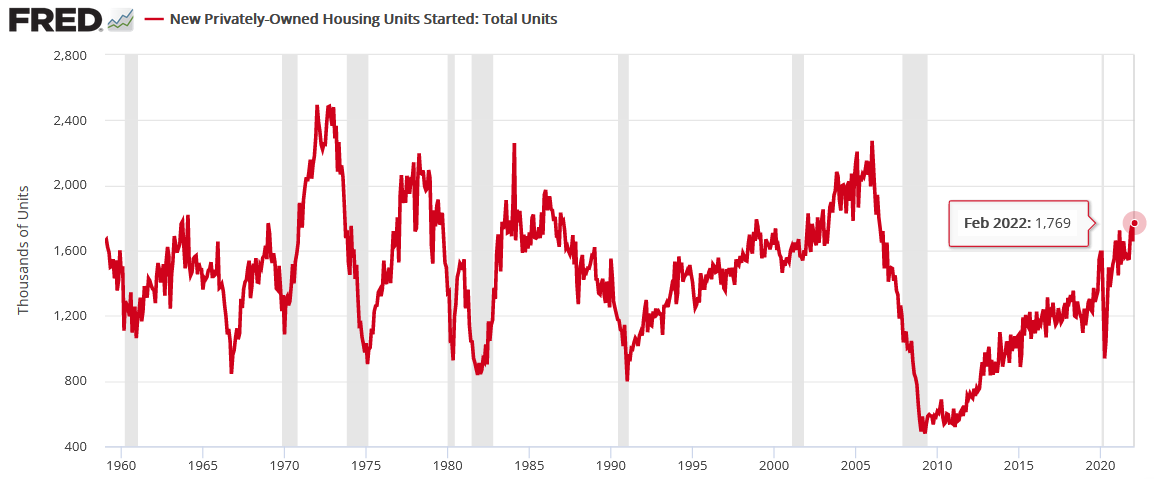

Source: CNBCIn addition, I noted above that U.S. housing starts outperformed expectations on Mar. 17. With the metric hitting a new 2022 high of 1.769 million, the data supports Powell’s assertion that the U.S. economy is nowhere near a recession.

Please see below:

To explain, the red line above tracks U.S. housing starts, while the gray bars above track U.S. recessions. If you analyze the connection, notice how U.S. housing starts always peak and decline in advance of U.S. recessions. Moreover, the relationship has been present since before 1960. As a result, with U.S. housing starts hitting a new post-pandemic high on Mar. 17, it adds more fuel to the Fed’s hawkish fire.

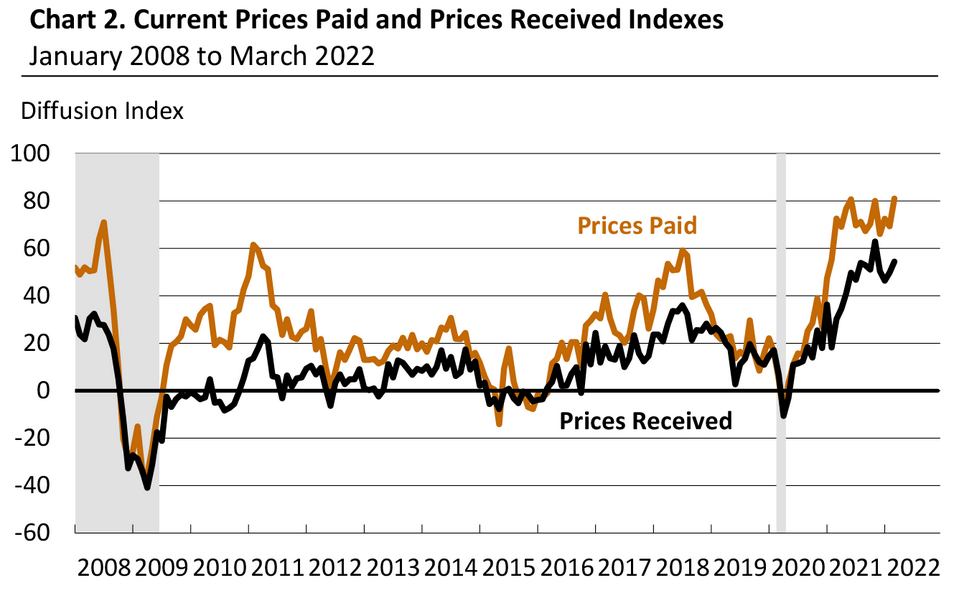

On top of that, while inflation remains extremely problematic, the latest survey data shows that pricing pressures are still headed in the wrong direction. For example, I noted above how the Philadelphia Fed’s manufacturing index outperformed expectations on Mar. 17. Well, the report also stated that “price increases become more widespread:”

“The prices paid index climbed 12 points to 81.0, its highest reading since June 1979. More than 87 percent of the firms reported increases in input prices, while 6 percent reported decreases; 7 percent of the firms reported no change. The current prices received index increased 5 points to 54.4. Nearly 57 percent of the firms reported increases in prices received for their own goods this month, 2 percent reported decreases, and 38 percent reported no change.”

Please see below:

Source: Philadelphia Fed

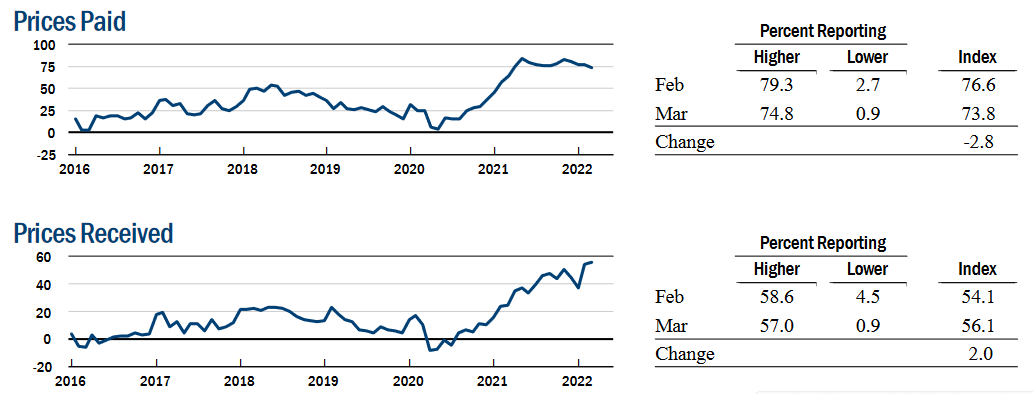

Source: Philadelphia FedSimilarly, the New York Fed’s Empire State Manufacturing Index was released on Mar. 15. The report revealed:

“The prices paid index edged down three points to 73.8, while the prices received index rose two points to a record high of 56.1, signaling ongoing substantial increases in both input prices and selling prices.”

Please see below:

Source: New York Fed

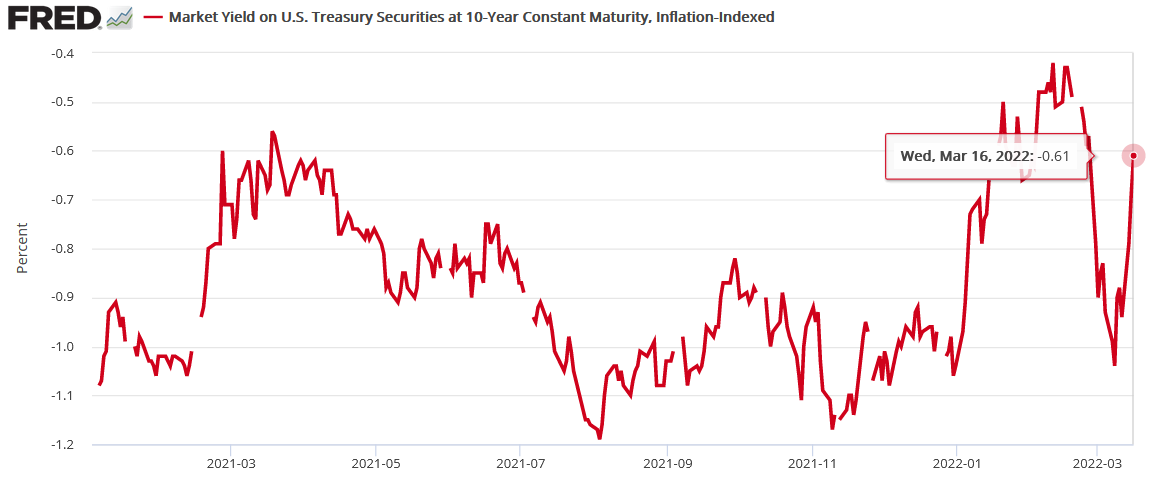

Source: New York FedFinally, while the Russia-Ukraine conflict resulted in a safe-haven bid for U.S. Treasuries, that gambit has already unraveled. In the process, the sharp decline in the U.S. 10-Year real yield has also reversed, and with even higher real yields required to calm inflation, the PMs will likely regret dismissing all of these fundamental warning signs.

The bottom line? While it was an eventful week on the fundamental front, the realized data only strengthened the PMs' bearish thesis. For months I've been warning that surging inflation and a resilient U.S. economy would elicit a hawkish shift from the Fed. Moreover, with each monetary policy meeting and each SEP release, the Fed continues to increase its hawkish directives. As a result, while the PMs seem inclined to ignore these developments right now, history implies that the tranquility won't last.

What to Watch for Next Week

With another full slate of U.S. economic data releases next week, the most important ones are as follows:

- Mar. 22: Richmond Fed manufacturing and services indexes

With output and inflation metrics providing insight into the state of play in March, it will be interesting to see if the data mirrors the results from the New York and Philadelphia Fed’s manufacturing surveys.

- Mar. 23: New home sales

With housing starts and building permits outperforming expectations on Mar. 17, new home sales will tell us how consumers are reacting to U.S. mortgage rates that have increased sharply amid the rise in U.S. Treasury yields.

- Mar. 24: Durable goods orders, ISM and IHS Markit PMIs, the KC Fed manufacturing index

More comprehensive than the regional surveys (like New York, Richmond, Philadelphia, KC, etc.), the ISM and IHS Markit PMIs cover the entire U.S. As a result, the readings on output, employment, and inflation are the most important data points of the week.

- Mar. 25: Michigan consumer sentiment, pending home sales

Like in prior months, it will be interesting to see how consumers respond to higher oil prices, higher mortgage rates and the overall inflationary environment. In addition, pending home sales will piggyback on the implications of the other housing data.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see outperformance alongside higher employment and inflation, the Fed will need to push up real yields to reduce demand and calm the pricing pressures. If that occurs, the outcome is profoundly bearish for the PMs.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Fed’s Actions Will Affect Gold. Are There Any Positives?

March 17, 2022, 10:21 AMThe Fed will want to keep inflation under control, and that could have miserable consequences for gold and miners. Will we see a repeat from 2008?

The question one of my subscribers asked me was about the rise in mining stocks and gold and how it was connected to what was happening in bond yields. Precisely, while short-term and medium-term yields moved higher, very long-term yields (the 30-year yields) dropped, implying that the Fed will need to lower the rates again, indicating a stagflationary environment in the future.

First of all, I agree that stagflation is likely in the cards, and I think that gold will perform similarly to how it did during the previous prolonged stagflation – in the 1970s. In other words, I think that gold will move much higher in the long run.

However, the market might have moved ahead of itself by rallying yesterday. After all, the Fed will still want to keep inflation under control (reminder: it has become very political!), and it will want commodity prices to slide in response to the foregoing. This means that the Fed will still likely make gold, silver, and mining stocks move lower in the near term.

In particular, silver and mining stocks are likely to decline along with commodities and stocks, just like what happened in 2008.

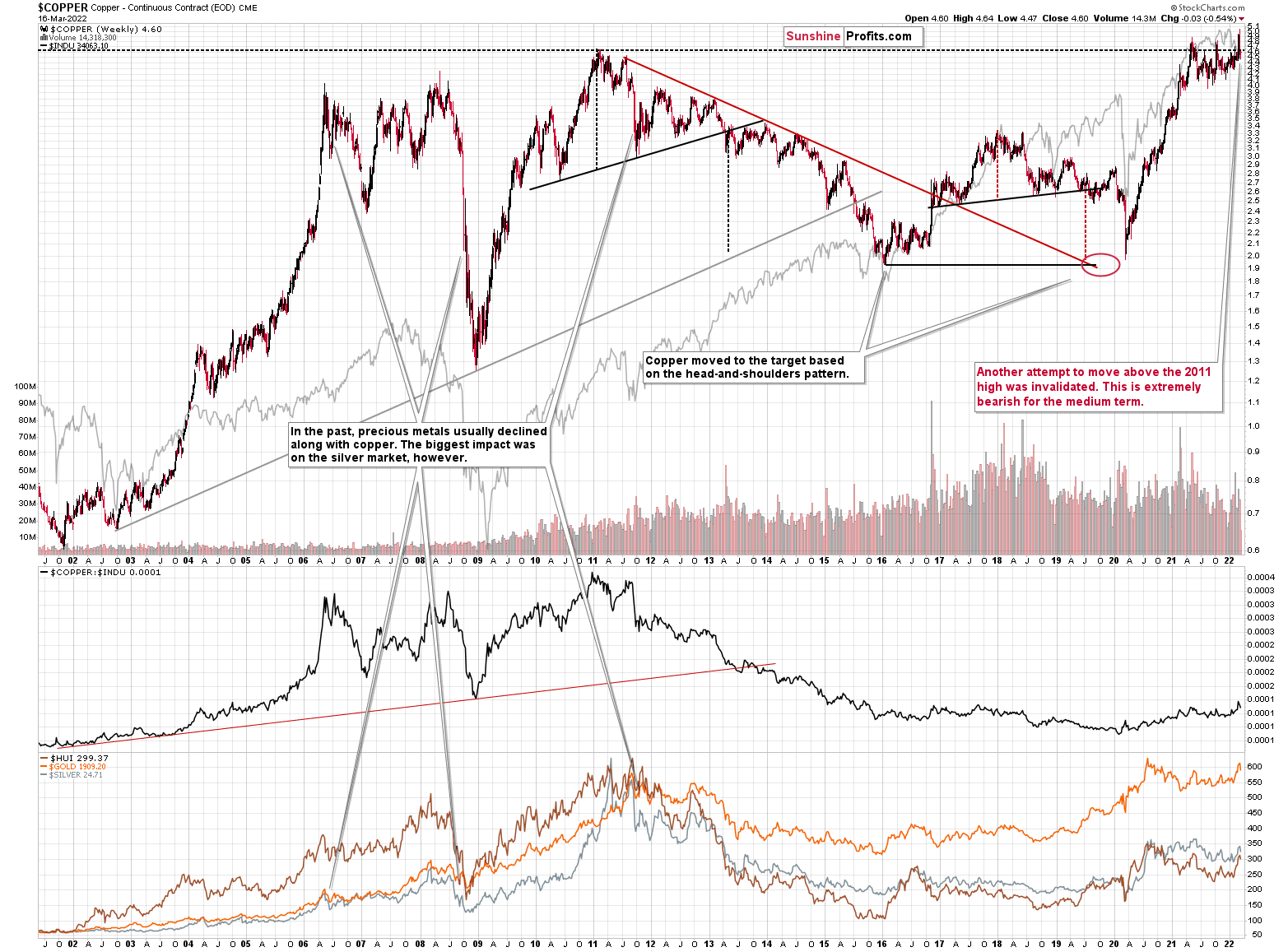

Speaking of commodities, let’s take a look at what’s happening in copper.

Copper invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

Yes, it might be difficult to visualize this kind of move given the recent powerful upswing, but please note that it’s in perfect tune with the previous patterns.

The interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged. The GDXJ was not trading at the time, so we’ll have to use a different proxy to see what this part of the mining stock sector did.

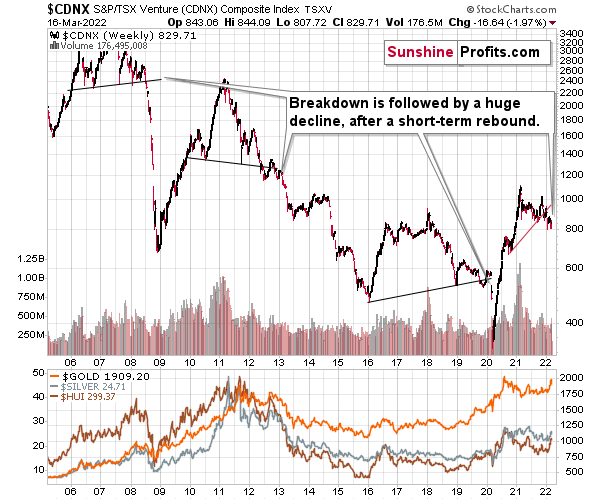

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

In fact, the outlook for the next few days is rather unclear, as different groups of investors can interpret yesterday’s developments differently. However, once the dust settles, the precious metals sector is likely to go down significantly.

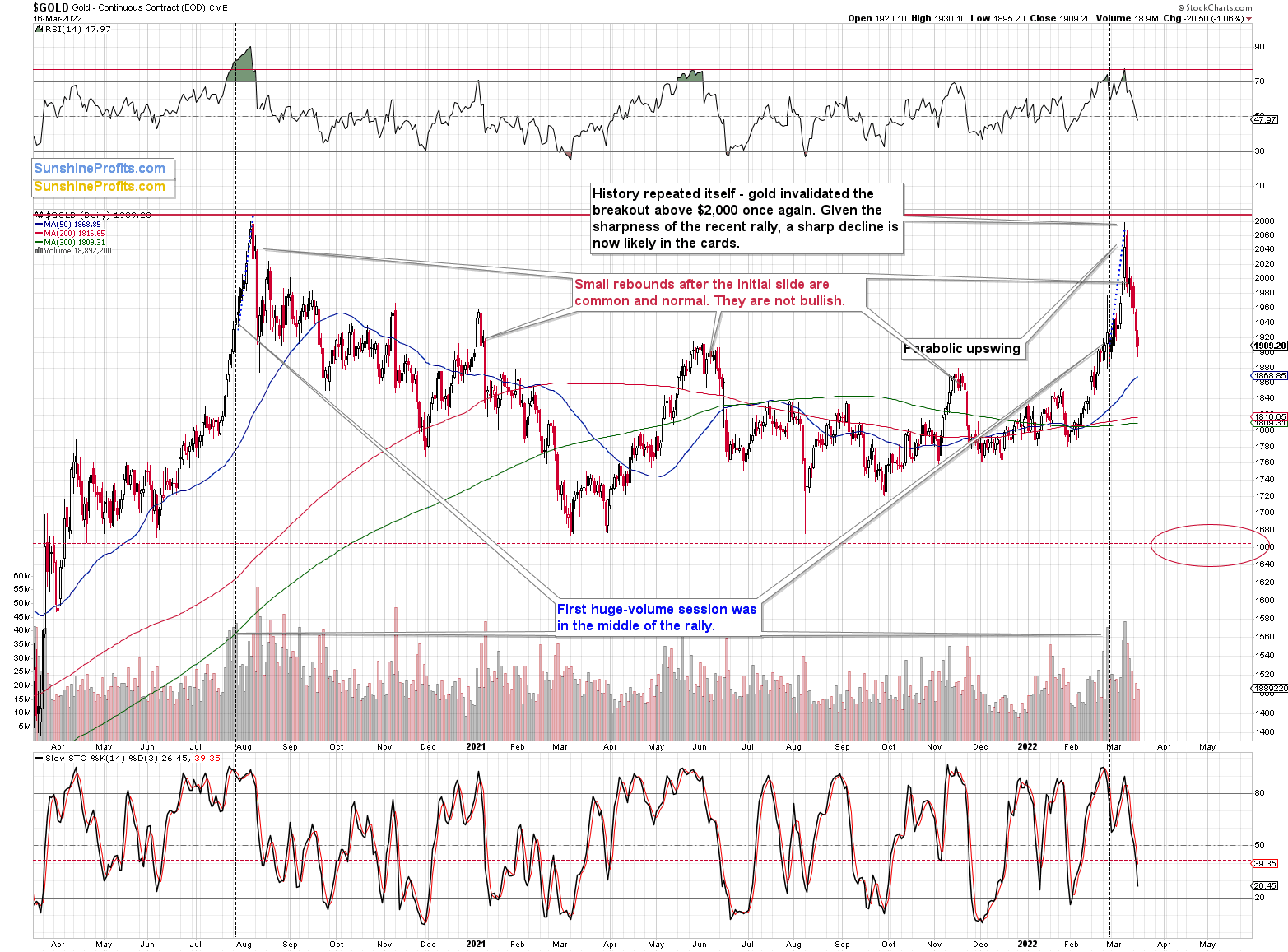

Gold is up in today’s pre-market trading, but please note that back in 2020, after the initial post-top slide, gold corrected even more significantly, and it wasn’t really bullish.

This time gold doesn’t have to rally to about $2,000 before declining once again, as this time the rally was based on war, and when we consider previous war-based rallies (U.S. invasion of Afghanistan, U.S. invasion of Iraq, Russia’s invasion of Crimea), we know that when the fear-and-uncertainty-based top was in, then the decline proceeded without bigger corrections.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM