Please log in to read the entire text.

If you don’t have a login yet, please select your access package.

Revolution, baby! There is growing acceptance for an aggressive fiscal policy, which could be supportive for gold prices from the fundamental, long-term point of view.

We live in turbulent times. The pandemic is still raging and will most likely have lost lasting effects on our society. But a revolution is also happening right before our eyes. And I don’t mean another storming of the U.S. Capitol or the clash of individual investors with big fish on Wall Street. I have in mind something less spectacular but potentially more influential: a macroeconomic revolution.

I refer here to the growing acceptance of easy fiscal policy. In the aftermath of the Great Recession, the central banks adopted an aggressive monetary policy, slashing interest rates to almost zero and introducing quantitative easing. It has become a new norm since then.

But fiscal policy was another kettle of fish. Although almost nobody cared about balanced government budgets, people at least pretended to worry about overly large fiscal deficits and an overly quick accumulation of public debt. For example, while Obama wanted $1.8 trillion in fiscal stimulus in a response to the global financial crisis of 2007-09, Congress passed a package of about $800 billion, as Republicans opposed larger spending. But in March 2020, Congress passed the CARES act worth about $2 trillion (and additional significant stimulus in December 2020), with the full support of Republicans.

Even Germany – the country famous for its fiscal conservatism – ran a fiscal deficit in 2020 and – what’s more – agreed to issue bonds jointly with other EU countries, although it was previously a taboo. The International Monetary Fund (IMF), another bastion of economic orthodoxy, which advocated for austerity and balanced budgets for years, gave up during the epidemic and started to call for more fiscal stimulus to fight the economic crisis.

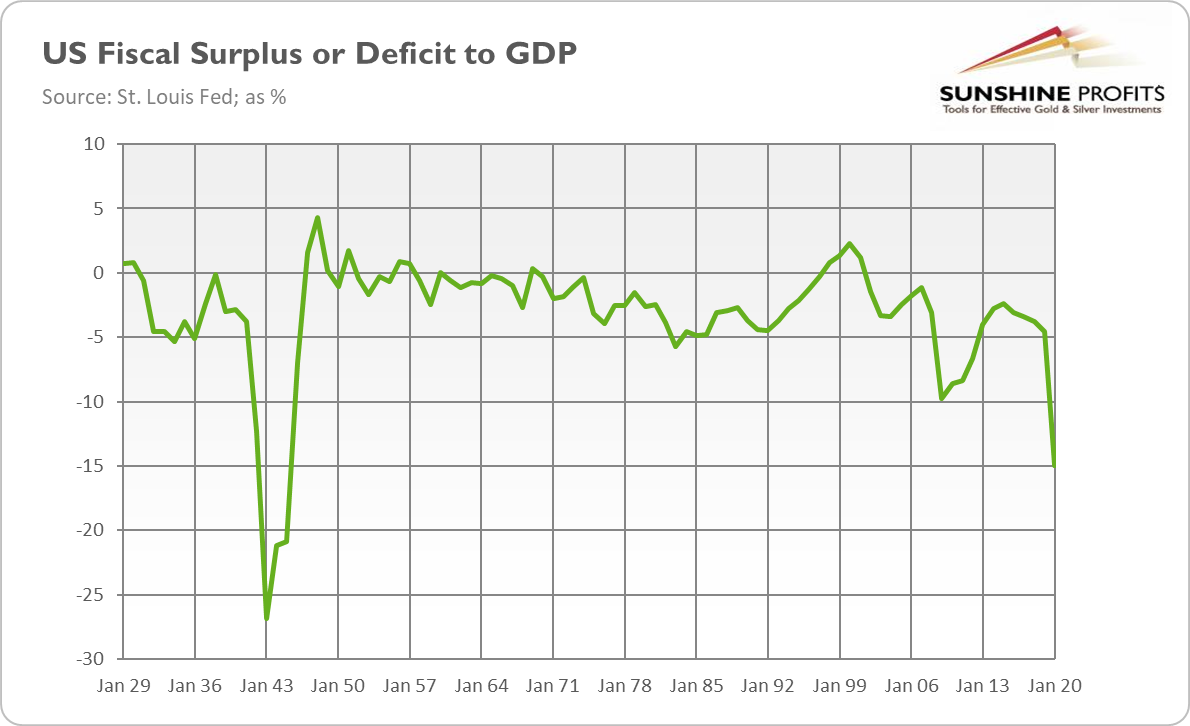

And this fiscal revolution is already seen in data. As the chart below shows, the U.S. fiscal deficit has increased from 4.6 percent of GDP in 2019 (which was already at an elevated level) to 15 percent of GDP in 2020, the highest level in the post-war era.

According to the IMF’s Fiscal Monitor Update from January 2021, fiscal deficits amounted to 13.3 percent of GDP, on average, in advanced economies, in 2021, a spike from 3.3 percent seen in 2019. As a consequence, the gross global debt approached 98 percent in 2020 and it’s projected to reach 99.5 percent of the world’s GDP by the end of this year.

What is important to note here is that government support wasn’t limited mainly to the financial institutions and big companies (such as automakers), as was the case in 2009, but it was distributed more widely. There was a huge direct money transfer to Main Street, including checks for practically all citizens. This is important for two reasons.

First, money flowing into the economy through nonfinancial institutions and people’s accounts may be more inflationary. This is because money doesn’t stay in the financial market where it mainly raises asset prices, but it’s more likely to be spent on consumer goods, boosting the CPI inflation rate. Higher officially reported inflation (and relatively lower asset prices) should support gold, which is seen by investors as an inflation hedge.

Second, the direct cash transfer to the people creates a dangerous precedent. From now, each time the economy falls into crisis, people will demand checks. It means that fiscal responses would have to be increasingly larger to meet the inflated expectations of the public. It also implies that we are approaching a universal basic income, with its mammoth fiscal costs and all related negative economic and social consequences.

Summing up, we live in revolutionary times. The old paradigm that “central banks are the only game in town” has been replaced by the idea that fiscal policy should be more aggressively used. Maintaining balanced budgets is also a dead concept – who would care about deficits when interest rates are so low?

However, assigning a greater role to fiscal policy in achieving macroeconomic goals increases the risk of higher inflation and macroeconomic instability, as politicians tend to be pro-cyclical and reckless. After all, the economic orthodoxy that monetary policy is better suited to achieve macroeconomic stability didn’t come out from nowhere, but from awful experiences of the fiscal follies of the past. I’m not a fan of central bankers, but they are at least less short-sighted than politicians who think mainly about how to win the next election and stay in power.

Hence, the growing acceptance of easy fiscal policy should be positive for gold prices, especially considering that it will be accompanied by an accommodative monetary policy. Such a policy mix should increase the public debt and inflation, which could support gold prices. The caveat is that investors have so far welcomed more stimulus flowing from both the Fed and the Treasury. But this “go big” approach of Powell and Yellen increases the longer-term risk for the economy, which could materialize – similar to the pandemic – sooner than anyone thought.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, the current (past?) crisis and the gold market, we invite you to read the April Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe though, and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Effective Investment through Diligence & Care.

-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short or medium term. In order to determine the latter, many additional factors need to be considered (i.e., sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.