Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update. Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

Let’s start today’s analysis with a recap of what recently happened on the fundamental front.

The Weekly Fundamental Roundup

While the Bank of Canada’s (BoC) lower-than-expected 50 basis point rate hike elicited hope that the Fed could follow suit, the recent bear market rally crashed when Fed Chairman Jerome Powell pushed back against a dovish pivot on Nov. 2.

Furthermore, with gold, silver mining stocks and the S&P 500 falling again on Nov. 3, I warned on Oct. 26 that the bulls were pushing their luck. I wrote:

With two of the four largest companies in the S&P 500 suffering, the squeeze may have already run its course. Moreover, while positioning is still heavily short, the index offered tactical value near 3,600, not 3,850.

In addition, with the bearish medium-term fundamentals rearing their ugly head, and the Fed poised to raise interest rates by 75 basis points next week, stocks offer a poor risk-reward proposition when the U.S. federal funds rate (FFR) should hit 4%.

Also, the PMs confront the same problem when risk-free assets offer a 4% return. As such, the Fed’s inflation fight should continue to drive money out of risk assets and into cash, and the prospect is highly bearish for the PMs.

Thus, with the S&P 500 ending the Nov. 3 session at 3,719.89, the air has come out of the bullish balloon; and with the PMs down on their luck, the reality is that a 4% risk-free return looks quite attractive when risk assets confront land mines at every turn. As a result, the bearish rotation should continue as the FFR presses higher in the months ahead.

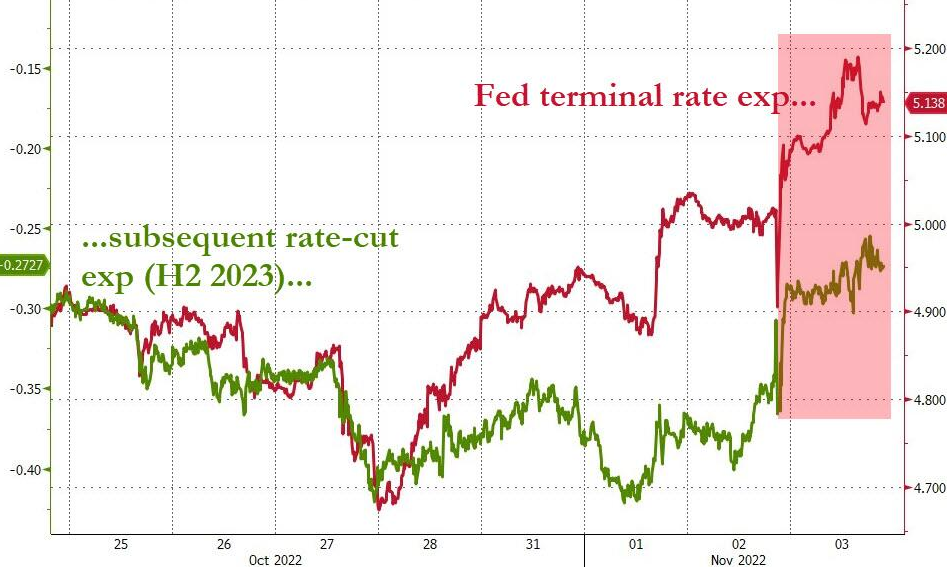

To that point, rate hike expectations hit a new 2022 high on Nov. 3.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the red line above tracks the expected peak in the FFR implied by the futures market, while the green line above tracks the inverted (down means up) rate cuts expected thereafter. As you can see, hawkish expectations have increased materially in recent days, and the red line approached 5.20% on Nov. 3 before settling near 5.14%. Therefore, the crowd is realizing that inflation is unlikely to abate anytime soon.

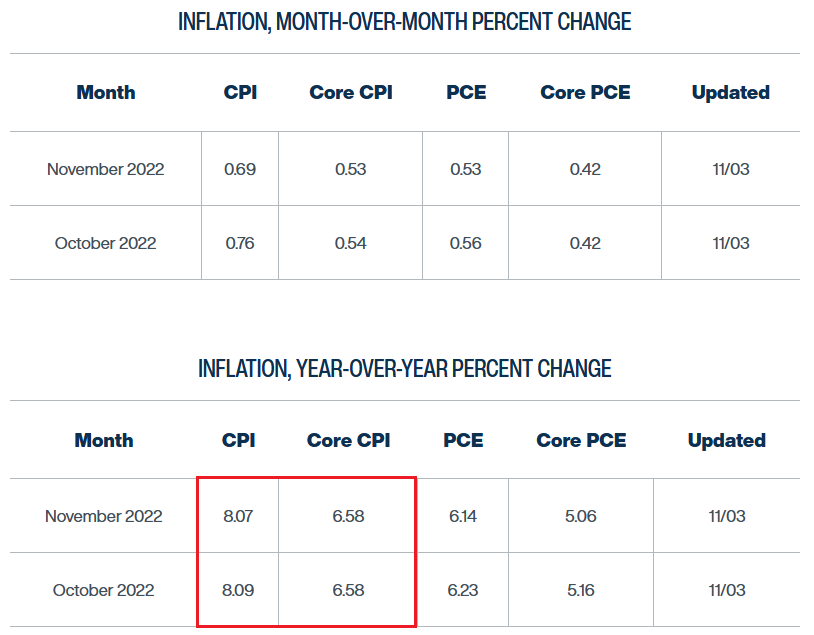

As evidence, the Cleveland Fed updated its inflation nowcast on Nov. 3; and with little to no progress expected in October or November, the Fed is still a long way from achieving its 2% objective.

Please see below:

Source: Cleveland Fed

Source: Cleveland Fed

To explain, the first two rows at the top show that the Cleveland Fed expects the headline Consumer Price Index (CPI) to increase by 0.76% month-over-month (MoM) in October and 0.69% MoM in November. Moreover, the realizations would equate to year-over-year (YoY) increases of more than 8%.

Likewise, the Cleveland Fed expects the core CPI to hit 6.58% YoY in October and November, which is only six basis points below the 2022 high of 6.66% YoY. Thus, the Fed is miles away from any noticeable inflation progress.

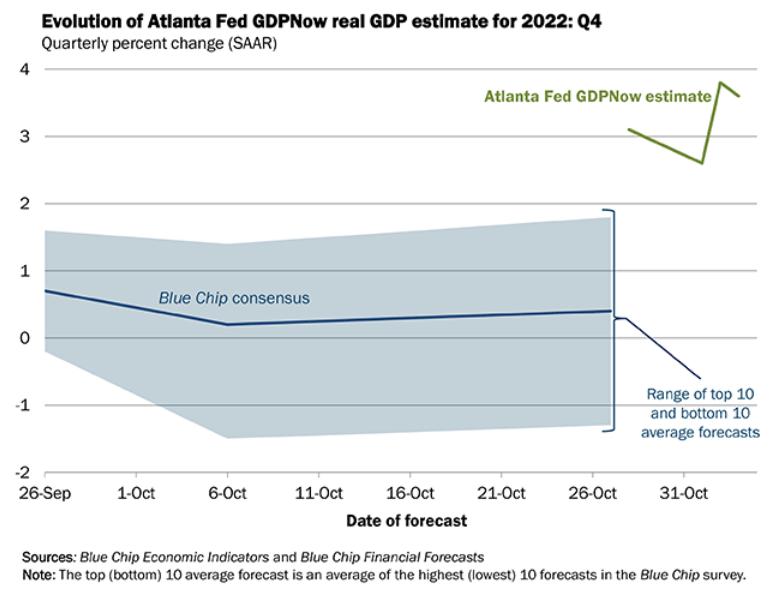

In addition, the Atlanta Fed updated its fourth-quarter real GDP growth expectation on Nov. 3. For the sake of objectivity, it’s an early projection that can change materially as the data evolves. However, with its Q3 real GDP growth projection proving quite prescient, the strength is noteworthy. The report stated:

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 3.6 percent on November 3, up from 2.6 percent on November 1.”

Please see below:

To explain, the green line above tracks the Atlanta Fed’s Q4 real GDP growth estimate, while the blue line above tracks the Blue Chip Consensus (investment banks). If you analyze the right side of the chart, you can see that the green line remains highly elevated. As a result, the weak data the bulls hope for has not materialized, and the trend is profoundly bullish for the FFR, real yields, and the USD Index.

Employment Fuels the Fed

With the U.S. labor market still on solid footing, employment strength allows the Fed to focus all of its attention on inflation. Therefore, unless job opportunities plunge, the central bank should keep pushing the FFR higher.

To that point, the NFIB released its Small Business Jobs Report on Nov. 3. NFIB Chief Economist Bill Dunkelberg said:

“The labor shortage remains a challenging problem for small business owners. Because of staffing shortages, small business owners are less able to take full advantage of current sales opportunities and continue to make business adjustments to compensate.”

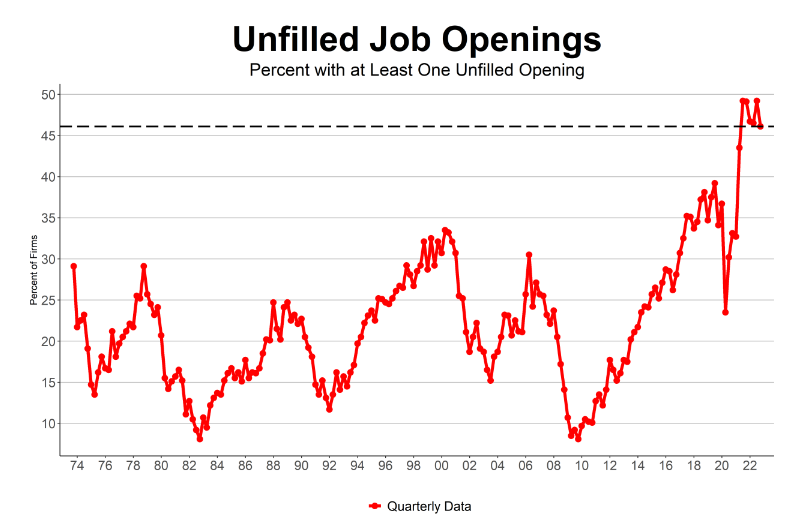

As such, the net percentage of small businesses with at least one unfilled job opening has barely budged despite the Fed’s 2022 rate hike crusade.

Please see below:

Source: NFIB

Source: NFIB

More importantly, the report added:

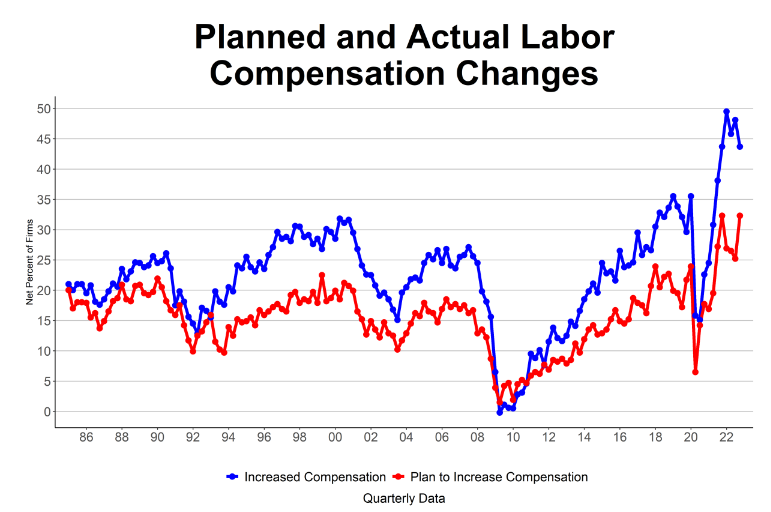

“A net 44% reported raising compensation, down one point from September but just six points below the 48-year record high set in January. A net 32% plan to raise compensation in the next three months, up nine points from September. This will put continued pressure on prices.”

Please see below:

Source: NFIB

Source: NFIB

To explain, the blue line above tracks actual compensation changes, while the red line above tracks planned compensation changes. If you analyze the right side of the chart, you can see that the red line is back at its all-time high, which means small businesses plan to increase their employees' wages even more in the months ahead, and the prospect is highly inflationary.

Therefore, while the crowd often assumes that a specific FFR will automatically cure inflation, the reality is that it's an iterative process that requires higher interest rates until progress materializes; and with history showing that even our 2023 FFR estimate of 4.5% to 5.5% is on the conservative side, the FFR will need to rise until enough demand destruction unfolds that wages and prices cool.

Please see below:

Source: NFIB

Source: NFIB

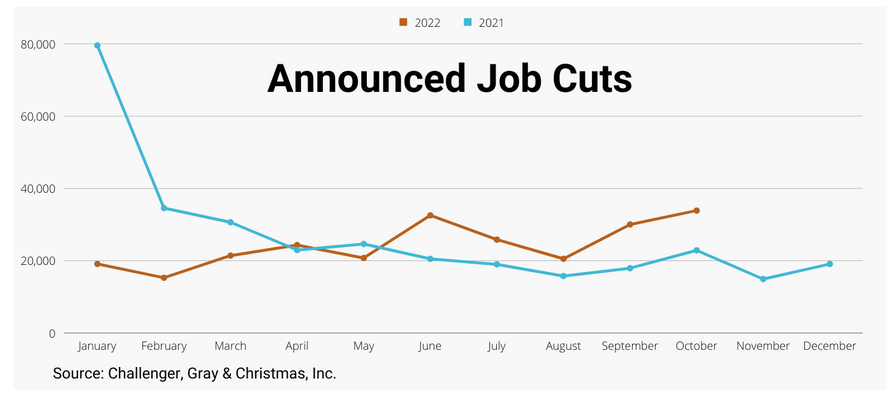

Finally, while most of the recent employment data has been bullish for Fed policy, Challenger, Gray & Christmas Inc.’s job cuts report was mixed. An excerpt read:

“U.S.-based employers announced 33,843 job cuts in October a 13% increase from the 29,989 cuts in September. It is 48% higher than the 22,822 cuts announced in the same month last year.”

However:

“So far this year, employers announced plans to cut 243,338 jobs, down 16% from the 288,043 cuts announced in the first nine months of 2021. It is the lowest recorded January-October total since Challenger began tracking monthly job cut announcements in 1993.”

As such, while the MoM results were weak, the nine-month results were strong. Also, when analyzing the overall picture, employment remains resilient because spirited job openings provide Americans with fallback options if they’re laid off. Thus, job openings are the key indicator, and they will need to decline dramatically for the Fed to change course.

The Bottom Line

With the pivot crowd losing another 2022 battle, their hopes have been crushed time and time again. Likewise, I warned on Oct. 24 that ignoring reality is not a sound investment strategy. I wrote:

The pivot drama on Oct. 21 was no different than the previous iterations throughout 2022. In a nutshell: something creates hope for a dovish shift, and investors run with the narrative. However, when the fundamentals signal the opposite, and it becomes evident later on, the optimism evaporates. Therefore, this time should be no different.

So, with the fundamentals continuing to unfold as expected, gold, silver, mining stocks and the S&P 500 should confront more downside in the months ahead.

In conclusion, the PMs declined on Nov. 3, as the FOMC’s reality check continued to haunt risk assets. Moreover, the USD Index surged by 1.42% and the U.S. 10-Year real yield soared by 17 basis points to match its 2022 high of 1.74%. As a result, the PMs’ main fundamental adversaries continue to wreak havoc.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Nov. 7: The Conference Board’s Employment Trends Index (ETI)

With employment one-half of the Fed’s dual mandate, continuous monitoring of the U.S. labor market is essential.

- Nov. 8: NFIB Small Business Optimism Index

While the NFIB’s labor report provided an early look at small businesses’ hiring activity and expectations in October, the Nov. 8 release will cover other important metrics like growth and output inflation.

- Nov. 10: Consumer Price Index (CPI)

With the CPI often moving markets, investors pay close attention to the data. However, with the Cleveland Fed projecting a headline increase of 0.76% MoM in October (8.09% YoY), the bulls may resent the results.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

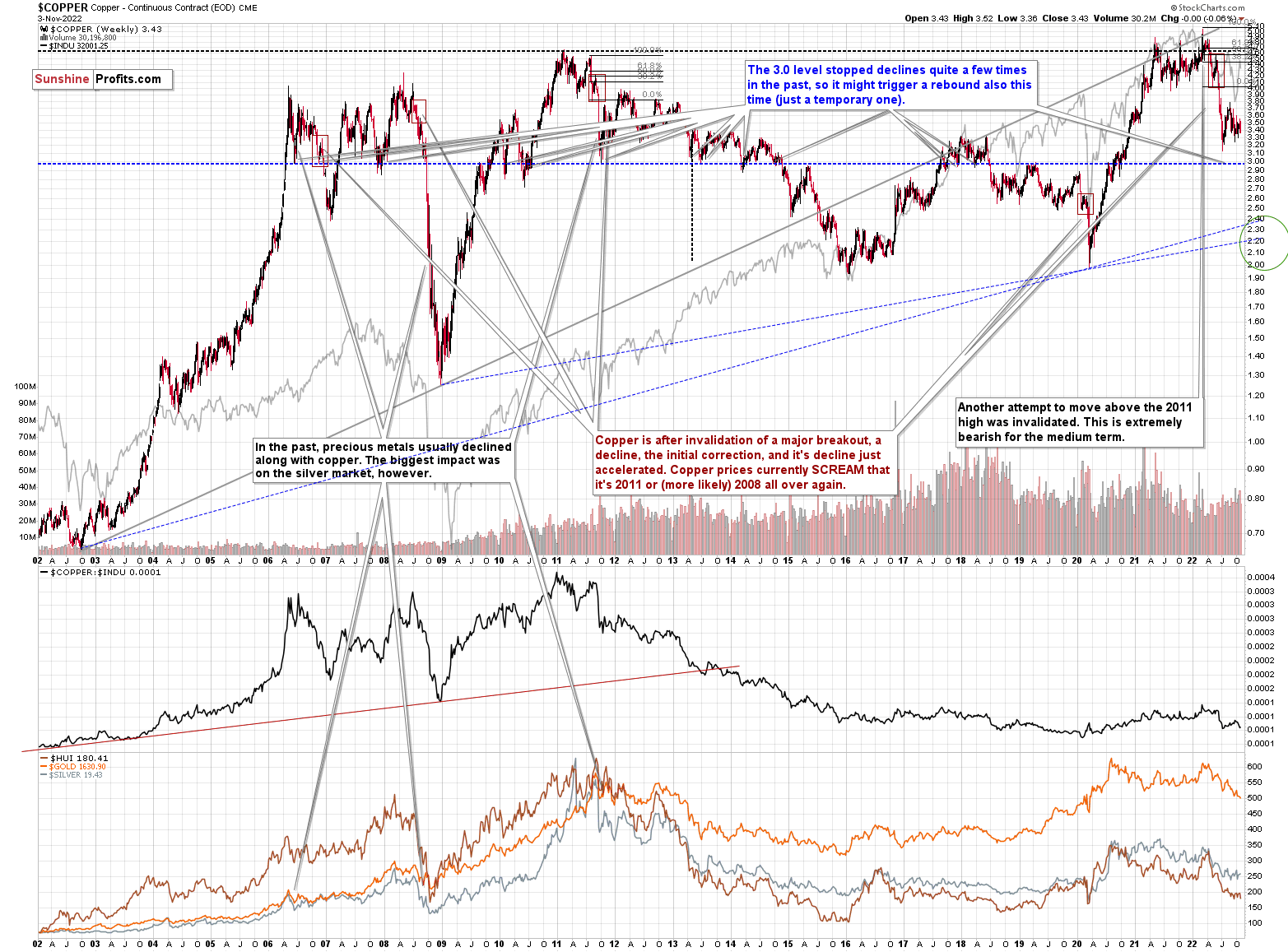

Let’s start today’s technical discussion with a quick check of copper prices.

Overall, everything I wrote about it last week (and in the previous weeks/months) remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

It seems to me that there might be some kind of smaller corrective upswing or a pause when copper moves to about $3.0, but that it would then decline profoundly once again, only to bottom in the $2.0-2.4 area. That’s where we have rising, long-term support lines and also the previous – 2016 and 2020 – lows.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after invalidation of a major breakout, a decline, the initial correction, and its decline just accelerated. Copper prices currently SCREAM that it’s 2011 or (more likely) 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

No market moves in a straight line, up or down, but since we just saw a corrective upswing, the downtrend might now resume.

Based on the recent short-term move lower, it seems that the downtrend has already resumed.

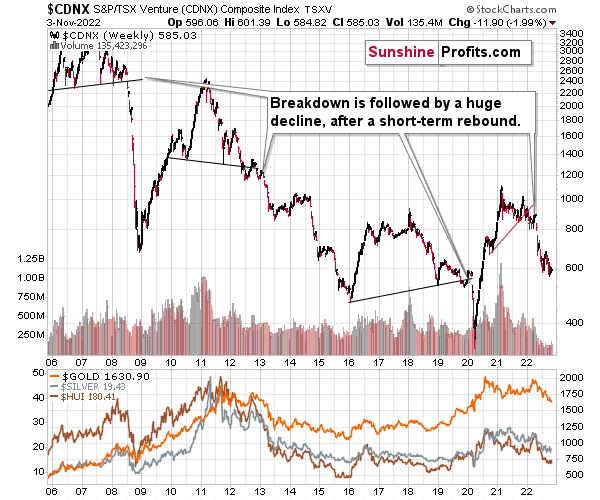

Having said that, let’s check junior miners’ really big picture.

I previously commented on the above chart in the following way:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

Having said that, let’s turn to gold.

Let’s start with context:

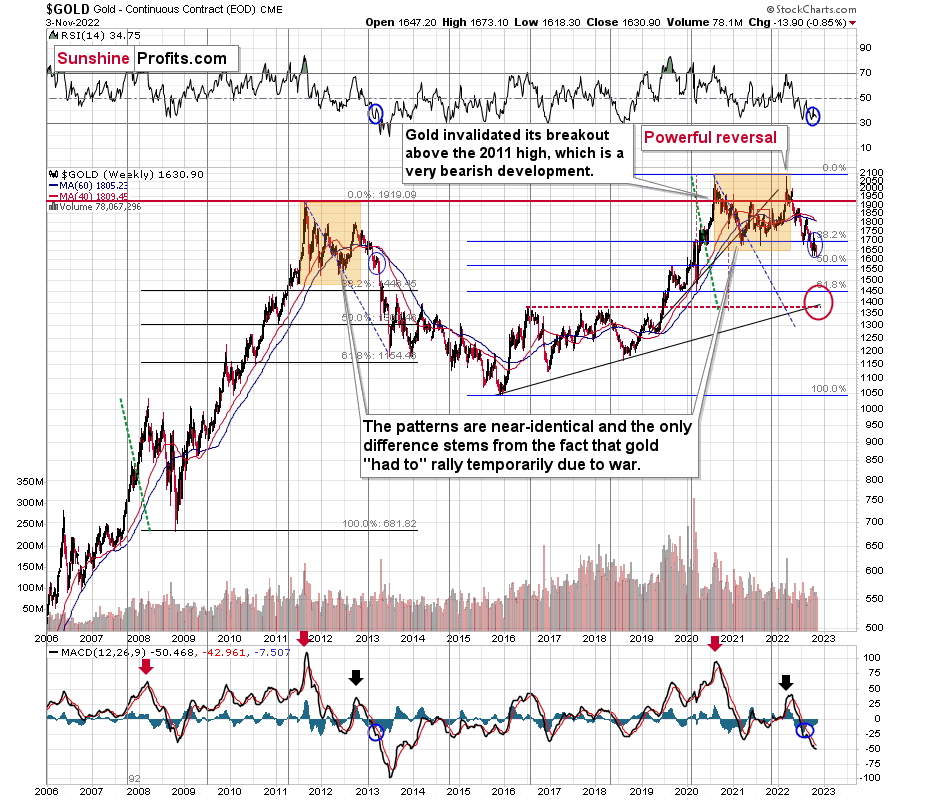

Between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet, gold failed to rally to new highs.

In fact, it’s trading very close to its 2011 high, which tells you something about the strength of this market. It’s almost absent.

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. The long-term gold price chart below provides details.

Basically, the key thing about gold’s long-term chart is that it doesn’t show any important changes. The downtrend continues in tune with the 2013 price action, and the very recent rally is barely visible.

To clarify, it is visible, but what’s visible is still in tune with the final attempt for gold to rally in April 2013, right before the biggest part of the slide.

Gold is sometimes forced to react to some geo-political events as the safe-haven buying kicks in, but these moves are usually short-term lived. Looking at long-term charts helps to keep things in proper perspective.

Consequently, my previous comments remain up-to-date:

Based on the above chart, it’s quite clear that the situation that is now being repeated. The patterns marked with orange rectangles and blue ellipses are almost identical (also in the MACD indicator, and to a lesser extent in the RSI indicator).

Sure, the situations are not identical, as this time we had a Russian invasion of Ukraine that pushed gold temporarily higher. Other than that, the situations are extremely similar.

Based on the stage of the self-similarity and the confirmed breakdown below the $1,700 level, gold is now likely to slide.

Based on the analogy to 2013, it’s not only likely to slide, it’s likely to slide profoundly in a sharp manner. These may be the last days or hours before the slide fully begins.

How low is gold likely to go during this upcoming big medium-term decline? Perhaps as low as its 2020 low – to the $1,450-1,500 area. And then, after a rebound, quite likely to or slightly below $1,400.

I realize this is far from the current price, but nonetheless, this target area appears justified in my opinion. There are two important Fibonacci retracements based on the 2015-2020 rally that gold can bounce from (it recently bounced from the 38.2% retracement). These are 50% and 61.8% retracements.

The support provided by the 61.8% retracement is strengthened by the 2020 low and the support provided by the 50% retracement is strengthened by the 2019 high.

However, based on gold’s self-similarity to 2013, it seems that we’re about to see a slide that’s bigger than what we’ve been seeing so far this year. This time – based on the similarity – gold is likely to decline profoundly, but no longer in the back-and-forth mode. If gold formed its next local low at the 50% retracement (so at about $1,560), then it might do so still within the declining, short-term trend channel (sometime in September).

However, if gold is to stick to the link to 2013, then it should decline more rapidly. In this case, the technique that can help us estimate the short-term target is the one that says that after a breakdown from a trend channel, price is likely to move approximately by as much as the height of the previous trend channel. In this case, gold could break below the trend channel soon and then decline even more. Based on the height of the trend channel, the above means that a move to the 61.8% retracement as the next downside target is more likely than a move to the 50% retracement.

I previously wrote that the above-mentioned decline in gold would likely be linked to a breakdown in the EUR/USD below 1, and we already saw both: decline in gold, and a breakdown in the EUR/USD below 1. The implications remain bearish.

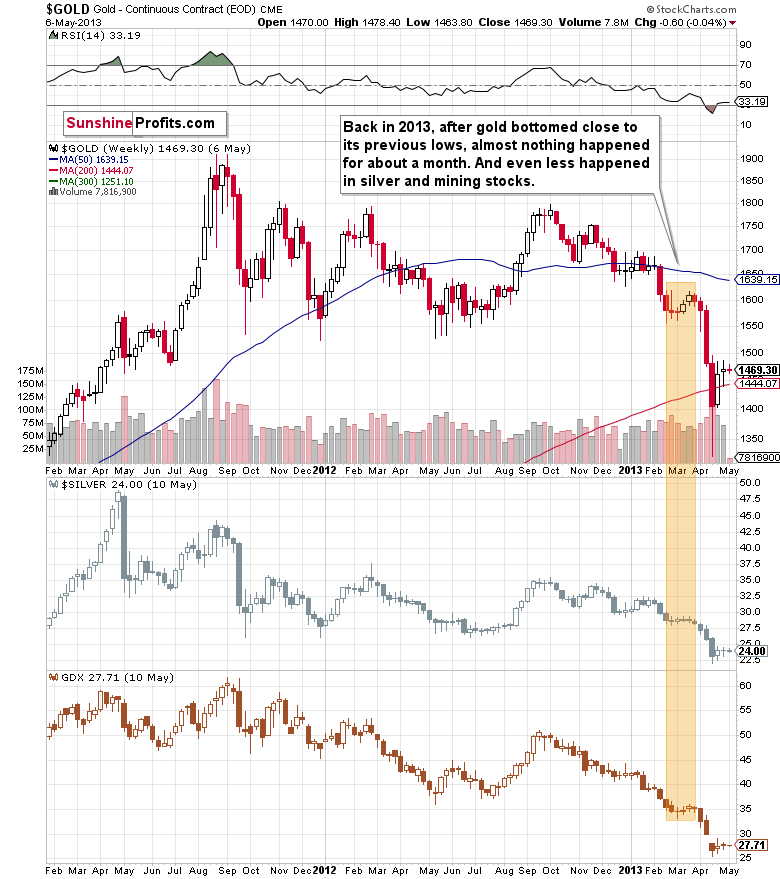

Let’s zoom in on what happened in 2013 after the analogous rebound.

Well, gold consolidated for a few weeks and plunged only after that consolidation.

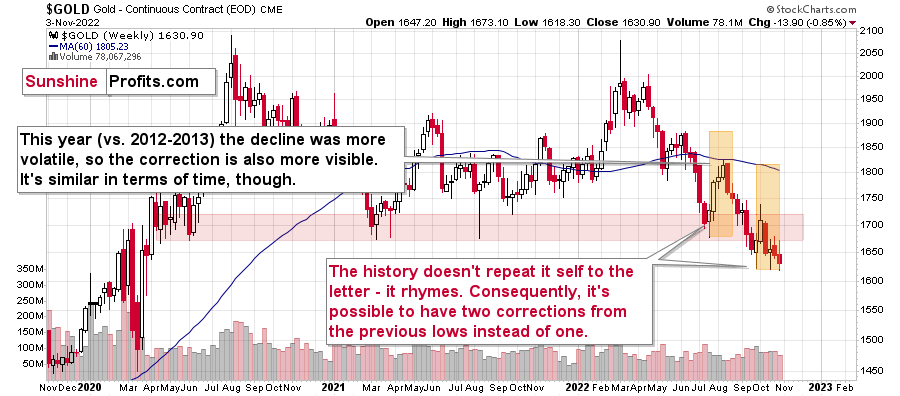

That’s what we saw recently as well. Of course, we haven’t seen the big plunge yet, but the other parts of the recent price patterns are very, very similar to what we saw in 2013.

Still, let’s keep in mind that history doesn’t necessarily repeat itself to the letter – it rhymes. Consequently, it’s quite possible to have two corrections from the previous lows instead of just one.

Especially if the temporary (!) effect of geopolitical events practically forces gold to move up due to safe-haven demand.

In other words, on a more-or-less basis, gold is doing exactly what it’s been doing in April 2013, right before the biggest part of the slide.

This time, gold has been making a few attempts to break lower, as geopolitical news and rumors keep popping up. However, all they are able to trigger are rebounds, and those rebounds are getting smaller each time. This is a bearish confirmation, as it tells us that the bulls’ strength and buying power are drying up. And when they finally do give up, and the decline starts, there will be many people that are able to sell (after all, they had just bought recently), thus contributing to the decline’s volatility.

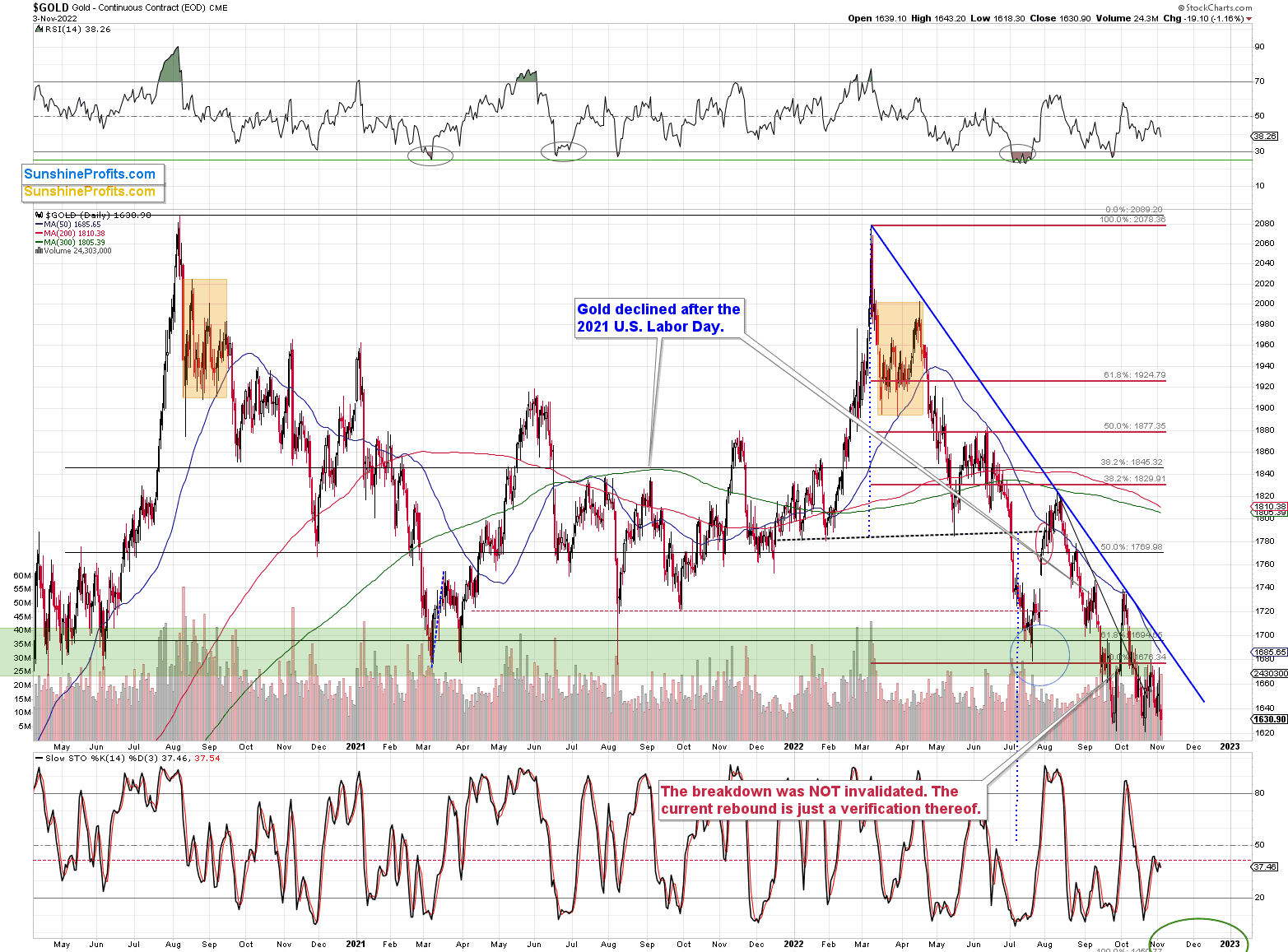

Please note that last week gold closed at a fresh 2022 weekly low, and lower lows confirm that the downtrend continues.

Having said that, let’s zoom in to see gold’s short-term price moves.

The above chart shows in greater detail what I already wrote above – the rebounds are getting smaller. It seems that at some point, all the market would get (assuming there was yet another bullish piece of news / rumor) is an intraday upswing.

In fact, that could be exactly what we are seeing in today’s pre-market trading. Gold futures are up by about $20, which is practically as much as they declined yesterday. This is not a bullish development, it’s a part of a broader bearish pattern, in which the corrective upswings are getting smaller and smaller.

On the other hand, a single bearish piece of news / rumor that surprises the market could trigger waterfall selling and a decline that’s similar to what we saw in 2013.

That’s exactly how the markets can remain self-similar and overall technical while reacting to news on a day-to-day basis.

All kinds of news hit the markets on a daily basis. The more important ones are less frequent, but there are myriads of detailed, less important announcements made each day. Sure, gold will react to bullish news by rallying, and it will likely react to bearish news by declining. BUT, how MUCH will the market move given a certain piece of news / rumor is a completely different manner?

Imagine something bullish happening. Should gold rally by $5? Or $15? Or $75?

It’s impossible to tell!

If something bearish happens, should gold decline by $5? Or $15? Or $75?

Again, it’s impossible to tell – that is, if you’re looking at fundamentals alone.

However, if you know – beforehand – what the market is likely to do, then you can expect it to mostly ignore news / rumors that are against what the market “wants” to do, and that the reaction to whatever is in tune with what the market “wants” to do (technical reasons) will be amplified. So, while on a day-to-day basis, it might seem like gold is following the news, it’s just that, once you zoom out, it becomes obvious that it actually does what it’s been doing under similar circumstances in the past.

Right now, gold continues to repeat its 2013 performance, which has extremely bearish implications for the coming weeks.

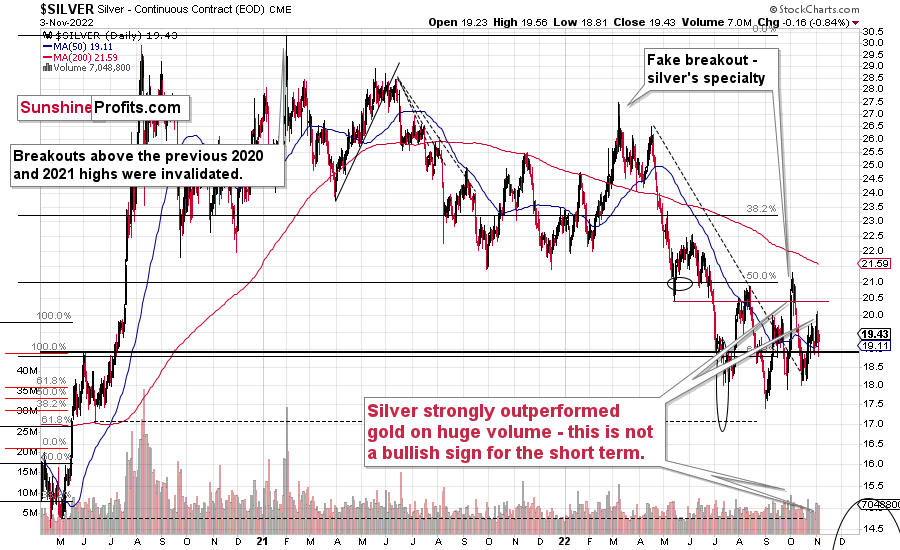

Having said that, let’s take a look at the silver market.

In short, silver was recently quite generous in proving us with signals. Sell signals.

Those came when silver outperformed gold on a very short-term basis.

Three weeks ago, I commented on the above silver chart in the following way:

Just like gold, silver reversed, and just like it’s the case with gold, I’m not buying the supposedly bullish narrative here. I don’t think anything more than a brief rebound is likely and it’s quite possible that there will actually be no additional rally – silver is down by almost 1% so far in today’s pre-market trading.

Silver’s slide from above $21 to below $19 has been very sharp, so it’s natural to see some sort of breather. It doesn’t necessarily have to be bullish.

When in doubt, take a step back and think about what really changed. And, well, nothing changed. Real rates are still going to move higher. The situation, being as bad as it is on many levels, is still better than the situation (in monetary / fiscal terms that is) in the Eurozone and Japan. Consequently, the USD Index has good reasons to strengthen.

Since real rates and the USDX are the main fundamental drivers for gold, and the technicals for gold continue to support the medium-term downtrend’s continuation, the big surprises for the precious metals sector are likely to be to the downside. The pace at which silver has declined recently appears to confirm that.

[The above was about the sharp early-October rally]

Indeed, silver declined profoundly. It moved much lower, practically erasing its recent rally. No wonder – the rally was based on an unfounded expectation of Fed’s dovish U-turn, which is unlikely to happen anytime soon.

What’s next?

Well, what happened next was another rally, based on similarly dovish expectations. However, it was nowhere close to being as big as the preceding one that was based on similar premises. This time, silver didn’t manage to move above its Sep. highs, and the rally was quickly erased.

This tells us two things.

First, that bulls’ buying power might have dried up or almost dried up because this time, the fundamental reasoning for a dovish U-turn was stronger (it’s not likely to happen in my view, but the reasoning for a softening of the Fed’s approach was indeed more reasonable this time), and yet the market didn’t respond as positively.

Second, the local top might already be in.

Silver also rallied and outperformed gold on a very short-term basis on Wednesday, which served as yet another bearish confirmation.

Moreover, let’s keep in mind that the entire July-now period can be viewed as one big flag pattern, and those “continuation patterns” tend to be followed by moves that are similar to the ones that preceded them.

In this case, the move that preceded the flag was a decline from about $28. This means that another move lower in silver is likely to be huge.

Once silver breaks below its 2022 lows, it has little support all the way until its 2020 low. There’s support just below $15, but it’s not very strong, so it might not trigger anything more than a brief correction.

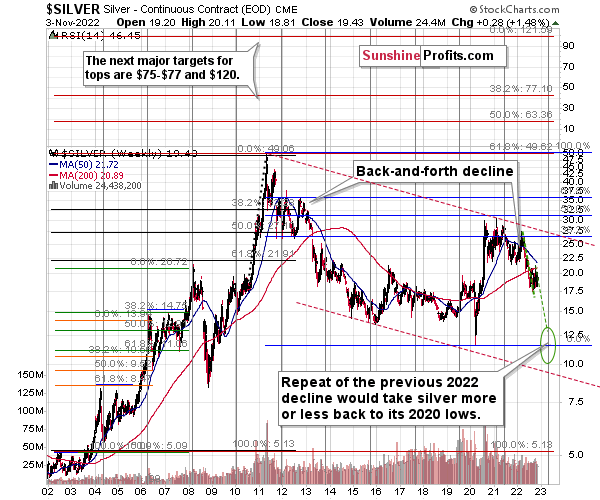

Let’s keep in mind that while gold is repeating its 2013 performance, so is silver.

As you can see on the above chart, silver corrected about 50% of the previous downswing, and this correction ended at about $30, a long time ago. Ever since, silver has been declining, and even the outbreak of war in Europe didn’t make silver rally above that level.

On the above chart, you can see how silver first topped in 2011, then declined and formed another top at the cyclical turning point. Next, it declined once again – to the previous lows. After that, silver rallied (in 2012 and 2022), and it topped between its 50-week moving average (marked in blue) and the previous top. Now silver is declining in a back-and-forth manner (you can see it more clearly on the previous short-term silver chart).

Back in 2012, these were just the early days of a gargantuan decline, and the same appears likely to be the case this time. Interest rates are going up after all, and the Fed is determined to quench inflation.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Besides, please note that silver didn’t even manage to rally as much as copper (which tried to move to new highs recently) or most other commodities, thus being rather weak.

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

Having said that, let’s take a look at what happened in mining stocks.

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

For example, right now, gold stocks are declining similarly to how they did in 2008 and in 2012-2013.

As gold was practically forced to rally recently based on geo-political events, news, and rumors, so were gold stocks.

Did it change anything technically?

Not really.

The verification of the breakdown below the rising, long-term support line simply continued. The fact that we haven’t seen a profound slide yet, but verifications’ continuation, doesn’t change the likelihood of seeing the former soon.

In fact, gold stocks’ inability to break back above the rising support/resistance line despite bullish news / rumors tells us that the market really does want to move lower from here, not higher.

Since the analogies to 2013 and 2008 were not invalidated because of this upswing, my previous comments on the above chart remain up-to-date:

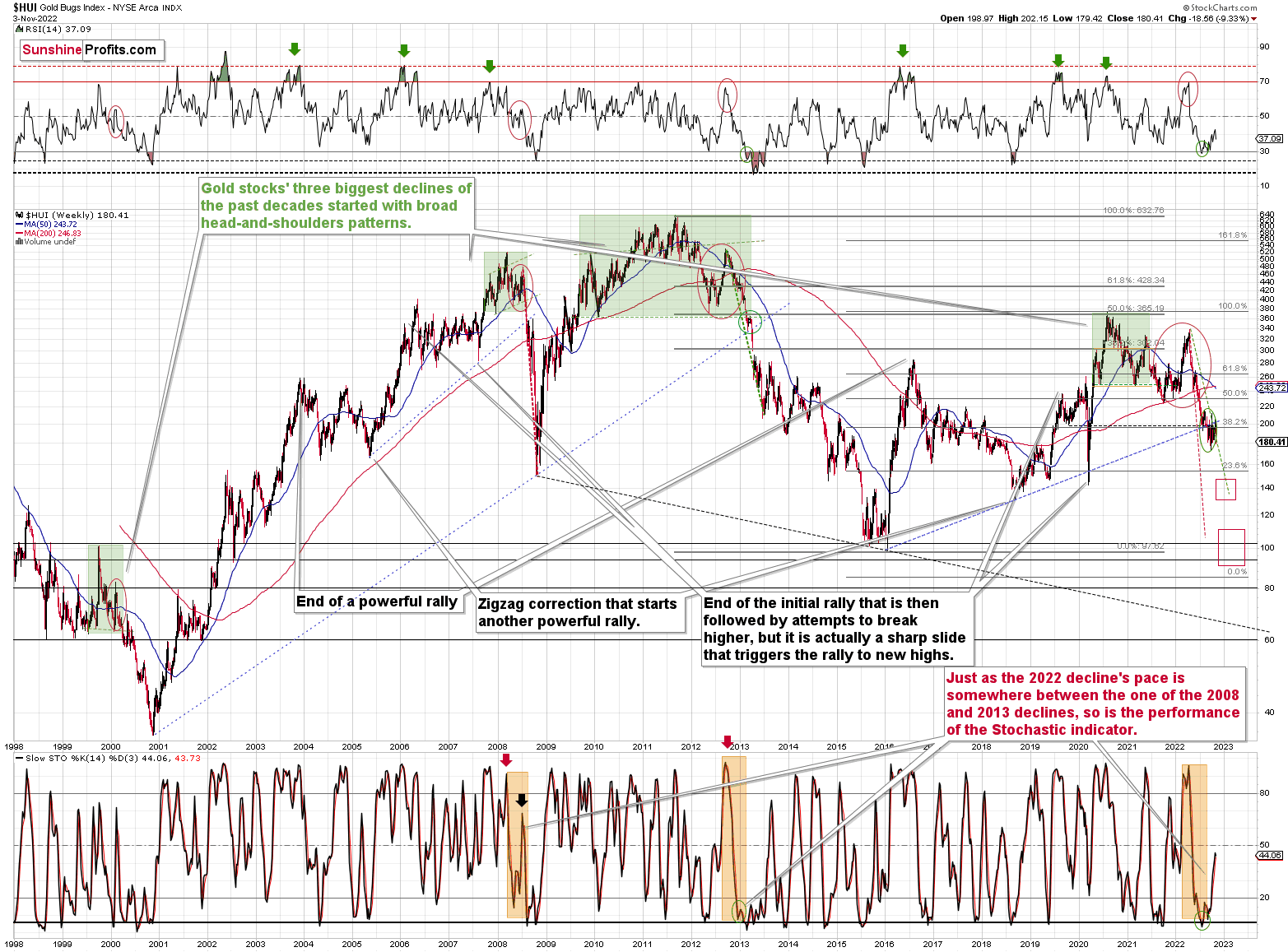

The key analogies in the case of the HUI Index (I’m using this chart as it has the most long-term scope) are to 2008 and 2013.

In 2008, there was a move higher in the stochastic that accompanied a sharp – but temporary – upswing that was then followed by a much bigger decline.

In 2013, there was a series of tiny upswings that didn’t really change anything.

Right now, we see something in between the above.

On multiple occasions, I wrote that the situation right now is somewhat similar to what we saw in 2013 (mostly), but it also has a 2008 vibe to it.

Even so, the pace at which gold stocks are declining is between both declines: the 2008 and 2013 ones. I marked this with dashed lines.

Please note the green, dashed line that starts at the late-2012 top and the one that starts at the 2022 top. Those lines are identical. You can see that back in 2012 and 2013, the HUI Index traded above this line. This time, it’s trading below it – gold stocks are declining faster.

Faster declines imply sharper corrections – as emotions get hotter.

So, does Stochastic’s performance indicate an even bigger rally here? Not necessarily.

Was the current rally very likely based on stochastic? Possible – yes, but very likely – no. The link to 2013 is still more visible and more important.

How low can the HUI Index fall during the next big downswing?

As it’s the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 120-150 is my current target area for the upcoming slide in the HUI Index.

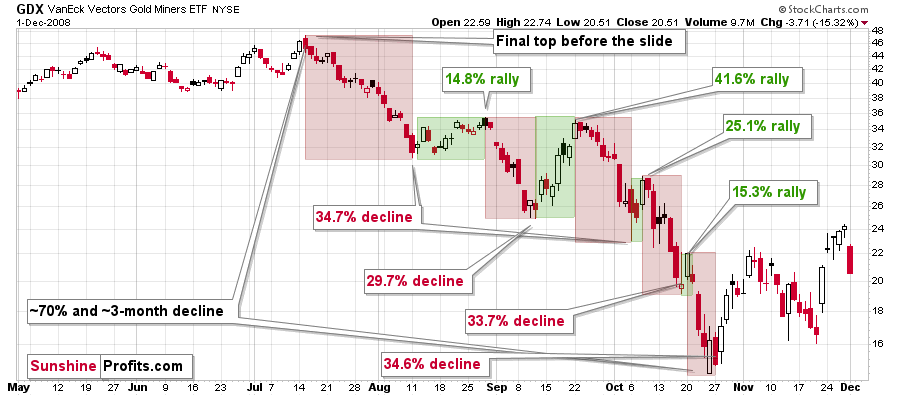

All right, let’s zoom in and see how mining stocks declined in 2008.

Back then, the GDXJ ETF was not yet trading, so I’m using the GDX ETF as a short-term proxy here.

The decline took about 3 months, and it erased about 70% of the miners’ value. The biggest part of the decline happened in the final month, though.

However, the really interesting thing about that decline – that might also be very useful this time – is that there were five very short-term declines that took the GDX about 30% lower.

I marked those declines with red rectangles. After that, a corrective upswing started. During those corrective upswings, the GDX rallied by 14.8-41.6%. The biggest corrective upswing (where GDX rallied by 41.6%) was triggered by a huge rally in gold, and since I don’t expect to see anything similar this year, it could be the case that this correction size is an outlier. Not paying attention to the outlier, we get corrections of between 14.8% and 25.1%.

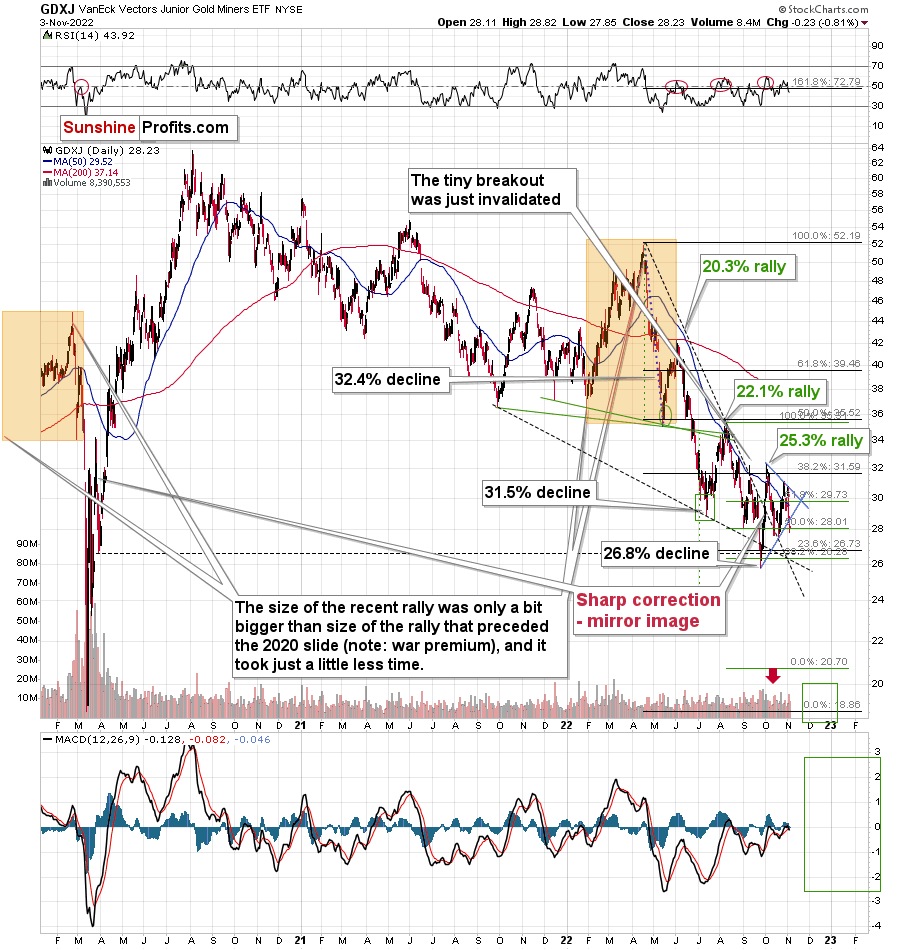

Fast forward to the current situation. Let’s take a look at the GDXJ ETF.

The key technical event that we saw this week is the breakdown below the triangle pattern (marked with blue lines). Yesterday, there was a second close below the lower border of the triangle, so the breakdown is almost verified. If the GDXJ closes below it today as well (which would also be the weekly close), the breakdown will be fully confirmed, and it will open the door to much lower prices.

Please note that the vertex of the triangle is in mid-November, which suggests that we might see a major reversal at that time. Of course, I’ll keep you – my subscribers – posted.

Right now, we are after three declines that took the GDXJ about 30% lower.

If history is to repeat itself to the letter, then we can expect to see two more big slides. Of course, they don’t have to be limited to just 30%. The GDXJ could slide much lower in each case.

For example, a quick slide to 2020 lows (slightly below $20) would be in perfect tune with the above – as a single decline. We could then see a rebound, and another powerful slide.

That’s what seems most likely in my view – at least from the medium-term point of view.

As far as the recent short-term developments are concerned, then the thing that I would like to emphasize is that they don’t change the bearish outlook – at all.

The only thing that we really saw was another GDXJ’s attempt to rally above its 50-day moving average. This attempt didn’t fail based on yesterday’s closing prices, but given today’s decline in GDXJ’s London trading (by ~3.5%), it’s quite likely that this attempt will be invalidated shortly – quite likely today.

Each previous attempt to rally above the 50-day MA failed (since April, that is) and it was followed by big declines. It also has bearish implications this time.

Additionally, please note that the RSI just jumped above 50, and ever since the April 2022 top, these levels in the RSI meant that local tops were in. I marked that with red ellipses in the upper part of the chart.

There’s also one additional factor explaining why this counter-trend bounce might be so volatile – that’s because the mirror image of this decline – the 2020 rally – also features a sharp correction around those price levels.

This time, the correction doesn’t have to be as big as the move that led to it was not as sharp.

Now, as you may recall, I previously had a downside target of about $26, but I ended up resigning from it. I continue to think that this decision was justified from the risk to reward point of view (given the data that we had available at that time), as there were previously corrective upswings, and it was not a no-brainer that we’re going to see a rebound also one more time.

However, as geopolitics came into play this time, the counter-trend rally has indeed materialized. Since it doesn’t make much sense to try to predict those near-term geopolitical events – the world is too unpredictable, it’s better to focus on the part of the picture where we can actually gain an extra edge over other market participants. That is recognizing trends and tendencies. Once the very short-term dust settles, the markets are likely to get back to their previous trends and surprise those who assume that short-term geopolitical events have a lasting impact on the markets. They don’t. If that was the case, gold would be above $2,000 at this time, as that’ where it soared based on the Russian invasion. Well, the war didn’t end, and yet gold is at about $1,700.

Indeed, the RSI appears to have topped in the area that I marked, just like it did twice earlier this year. It seems that the decline can now continue, regardless of the immediate-term performance.

At this point, you might be wondering why junior miners are not trading at their previous 2022 lows, just like gold is, and what does this “strength” mean.

In short, it’s most likely due to the stock markets’ performance. It rallied recently, and some of the bullishness spilt over to mining stocks. What does it imply?

Well, as the stocks are likely to slide, the small bullish impact is likely to turn into a huge bearish impact. And if stocks don’t slide, but rally instead, then juniors are still likely to decline more than gold and silver in percentage terms, but their decline would not be as dramatic in this case.

In my view, a decline in stocks is still the most likely outcome – and I think that junior miners will be affected to a great extent. And yes, this means that I expect (no promises, of course) that our profits on the short positions in junior mining stocks are going to soar in the coming weeks.

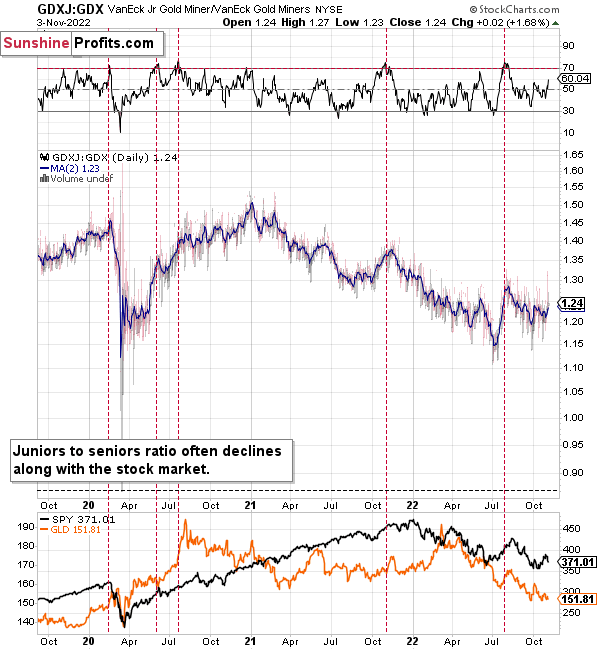

Meanwhile, the relative performance of junior miners compared to senior miners continues to deteriorate in a medium-term trend.

During this quick upswing, juniors rallied relative to seniors, but this is just a very short-term move that’s within a short-, and medium-term downtrends.

This implies bigger declines in the GDXJ in the future.

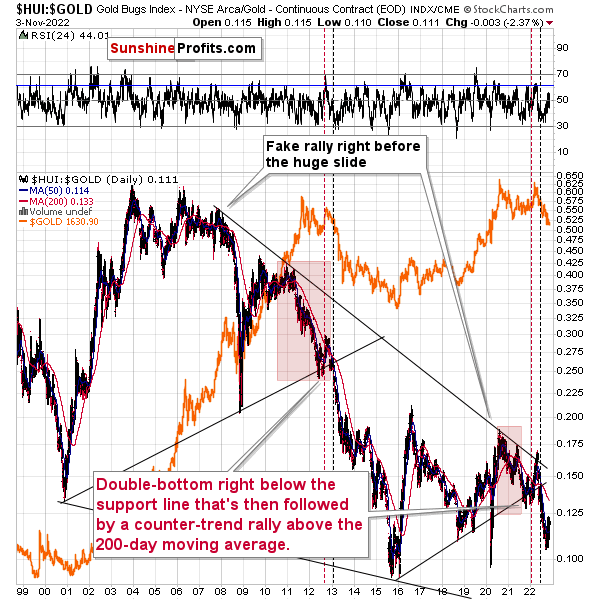

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw at the 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI to gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

Recently, we saw a quick upswing in the ratio, but that’s not a game-changer – even the biggest declines had quick corrections in the past.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices of gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks) and that’s exactly what’s likely to happen.

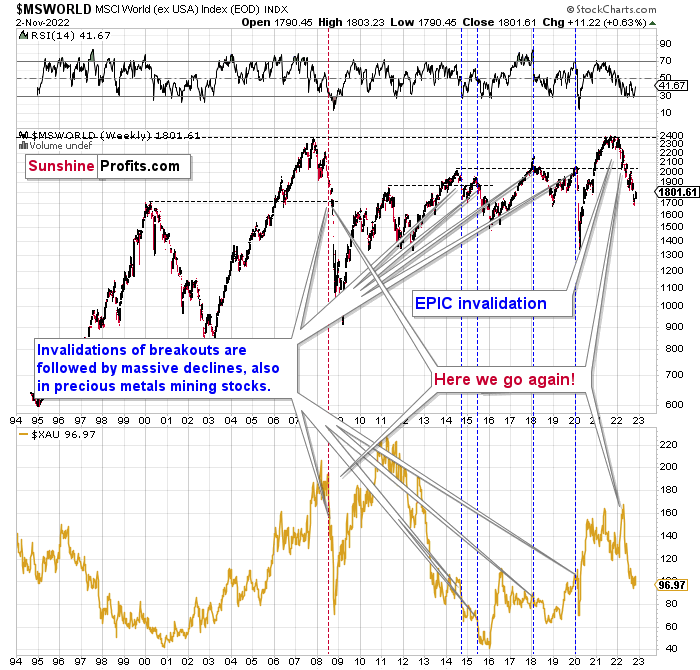

The technical picture in the case of world stocks remains extremely bearish, and my previous comments on it were just confirmed.

After a brief pause, the freefall continues, just like in 2008. This has profoundly bearish implications for the mining stocks that declined severely back then.

Here’s what I’ve been writing about the above chart for quite a few weeks now:

World stocks have already begun their decline, and based on the analogy to the previous invalidations, the decline is not likely to be small. In fact, it’s likely to be huge.

For context, I explained the ominous implications on Nov. 30. I wrote:

Something truly epic is happening in this chart. Namely, world stocks tried to soar above their 2007 high, they managed to do so, and… failed to hold the ground. Despite a few attempts, the breakout was invalidated. Given that there were a few attempts and that the previous high was the all-time high (so it doesn’t get more important than that), the invalidation is a truly critical development.

It's a strong sell signal for the medium - and quite possibly for the long term.

From our – precious metals investors’ and traders’ – point of view, this is also of critical importance. All previous important invalidations of breakouts in world stocks were followed by massive declines in mining stocks (represented by the XAU Index).

Two of the four similar cases are the 2008 and 2020 declines. In all cases, the declines were huge, and the only reason why they appear “moderate” in the lower part of the above chart is that it has a “linear” and not a “logarithmic” scale. You probably still remember how significant and painful (if you were long, that is) the decline at the beginning of 2020 was.

All those invalidations triggered big declines in the mining stocks, and we have “the mother of all stock market invalidations” at the moment, so the implications are not only bearish, but extremely bearish.

World stocks have declined below their recent highs, and when something similar happened in 2008, it meant that both stocks and gold and silver mining stocks (lower part of the chart) were about to slide much further.

The medium-term implications for mining stocks are extremely bearish.

However, let’s get back to the short- and medium-term points of view.

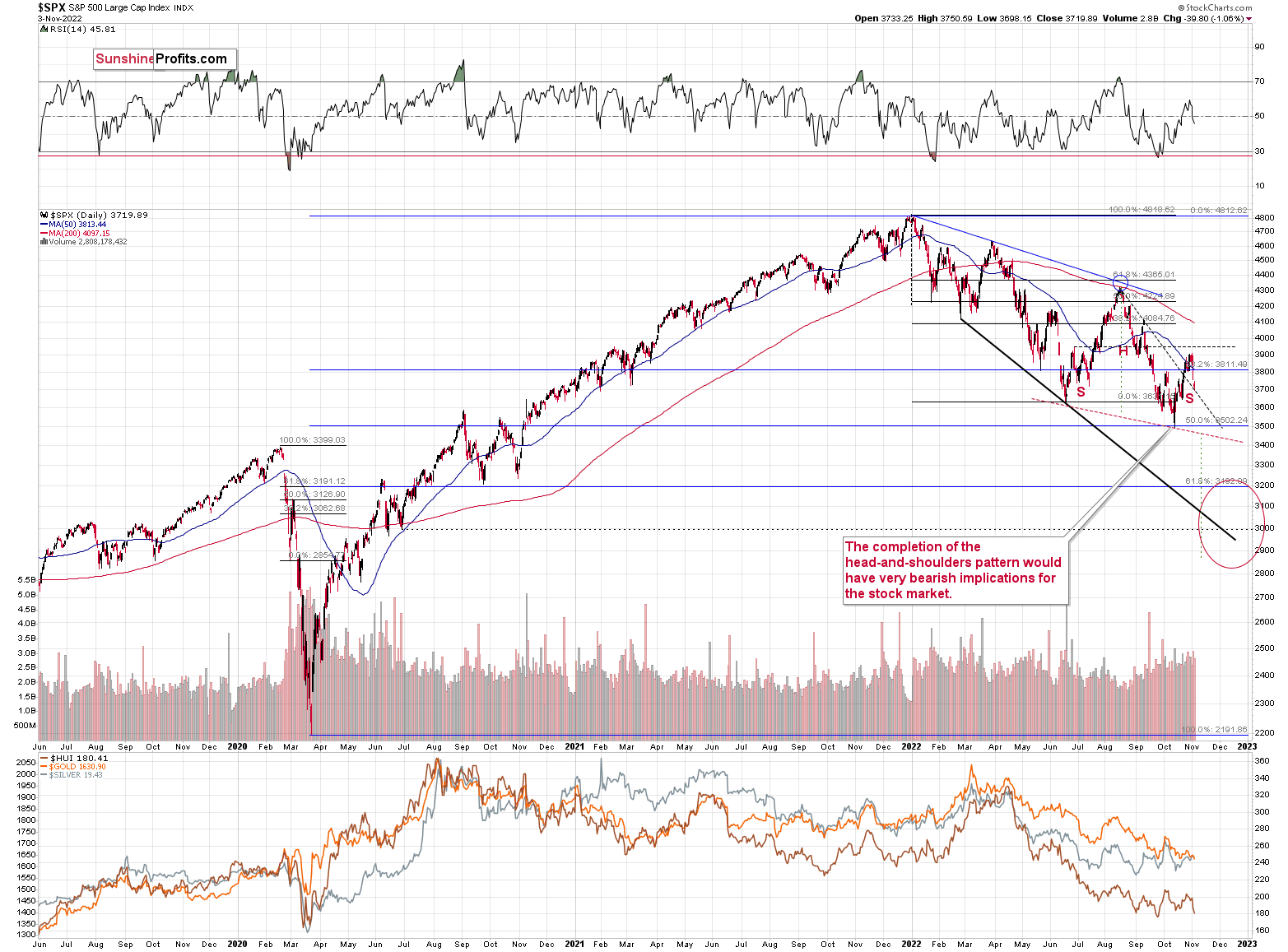

Stocks are after quite a volatile short-term decline, and based on how the prices shaped in the previous months, it could be the case that the right shoulder of a medium-term head-and-shoulders pattern is being formed.

If this pattern is completed – that appears likely in my view – the implications will be very bearish for the short term. Not just for the stock market but also for mining stocks (particularly juniors).

Another thing that could serve as a sell signal in the near future is an invalidation of the breakout above the declining black dashed resistance line. Interestingly, this breakout is only visible when we look at the index itself, but it’s not visible in the case of the index futures.

I commented on it on Nov. 2 in the following way:

However, once we zoom in and focus on S&P 500 index futures, it becomes clear that the situation is much more bearish than it seems at first glance.

The index futures have longer trading hours than the index, so the above chart includes a broader data range. In many cases, the U.S. session would be key and overnight trading wouldn’t be that important, but in the case of the S&P 500 index futures, those trades are important as this extremely popular index/futures is being traded all over the world, and the sizes of those transactions are not minor.

In other words, paying attention to the S&P 500 index futures is a good idea.

The above chart shows that we just saw a failed attempt to break above the declining resistance line, the October highs, and the 50% Fibonacci retracement based on the August-October decline. This is a powerfully bearish combination.

On top of that, yesterday’s session took the form of a daily reversal.

And yes, this is all bearish news for the stock market.

This, in turn, means that the positive impact that the stock market had on the prices of mining stocks is likely to be reversed. This, plus the bearish implications of gold and silver charts, tells us that the very bearish outlook for mining stocks (especially junior mining stocks) remains up-to-date – at least for the next few weeks-months. In my view, they are likely to rally in the very long run, but not without a bigger decline first.

Indeed, stocks declined shortly thereafter, and technical indications preceded fundamental developments (FOMC) as it’s often the case.

This is yet another example of why it’s a great idea to examine the charts for clues instead of passively waiting for the news to hit the market, or why it’s worthwhile to try to guess what kind of news will appear. Sometimes, the latter is useful, but chart analysis is useful almost at all times.

Every now and then I’m being asked “what if” questions, and the “what if” is followed by a scenario that is almost obviously going to make the market move in a way that’s unfavorable to the current position. In almost all cases, the reply is about comparing what’s possible and what’s likely. Just because something is possible (you could be hit by a meteor made of gold the second you get outside) doesn’t make it likely. The reason we’re analyzing charts so thoroughly (and why we cover so many of them – actually, I look at many more charts than I feature even in the longest analyses) is to estimate what’s likely before any type of news hits the market.

After all, if the market wants to move in a certain way, it will just more or less ignore news that pushes it in the other direction while magnifying its reactions to the news that push it in the direction it wants to move.

As interest rates are likely to go up, the stock market is likely to go down – perhaps as low as 3,200 on a short-term basis – and then – after a correction – even lower.

Most interestingly, though, such a decline would likely have a devastating effect on the prices of mining stocks (especially junior mining stocks) and silver. There might be some impact on gold, too.

The above would also be in tune with an extra rally in the USD Index. After all, less competitive exports are not that favorable for the U.S. economy.

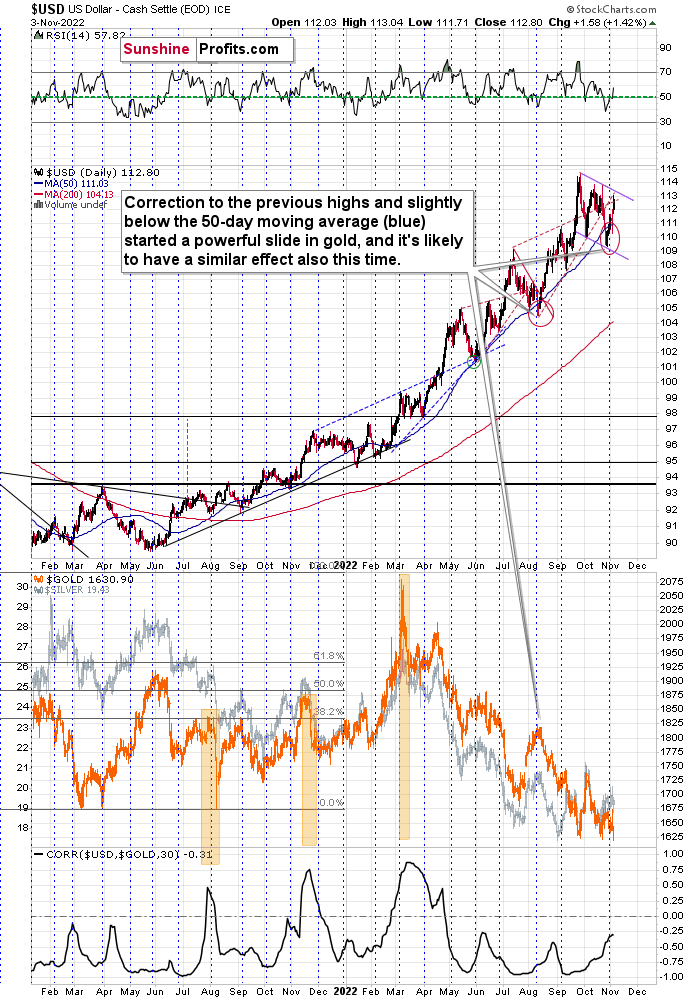

Last week, I commented on the above chart in the following way:

Back in August, USD’s correction to the previous highs and slightly below the 50-day moving average (blue) started a powerful slide in gold, and it's likely to have a similar effect this time as well.

This is particularly likely to also be due to the following:

- The USD Index corrected in a near-perfect zig-zag (ABC) manner, which is the most classical way for a market to correct.

- The turn of the month is almost here (only two sessions left in October), and the USDX tends to reverse (mostly from bottoms, at least recently) at those times. Perhaps the bottom is already in.

- Gold’s reaction to the most recent decline in the USD Index was much lower than what we saw before the August top. This tells us that gold really wants to decline here.

Indeed, the USD Index rallied, and it approached its previous highs. Conversely, gold declined, and it approached its recent lows. In fact, gold declined slightly below its recent lows, while the USD Index didn’t hit its previous highs. This is yet another proof of gold’s weakness.

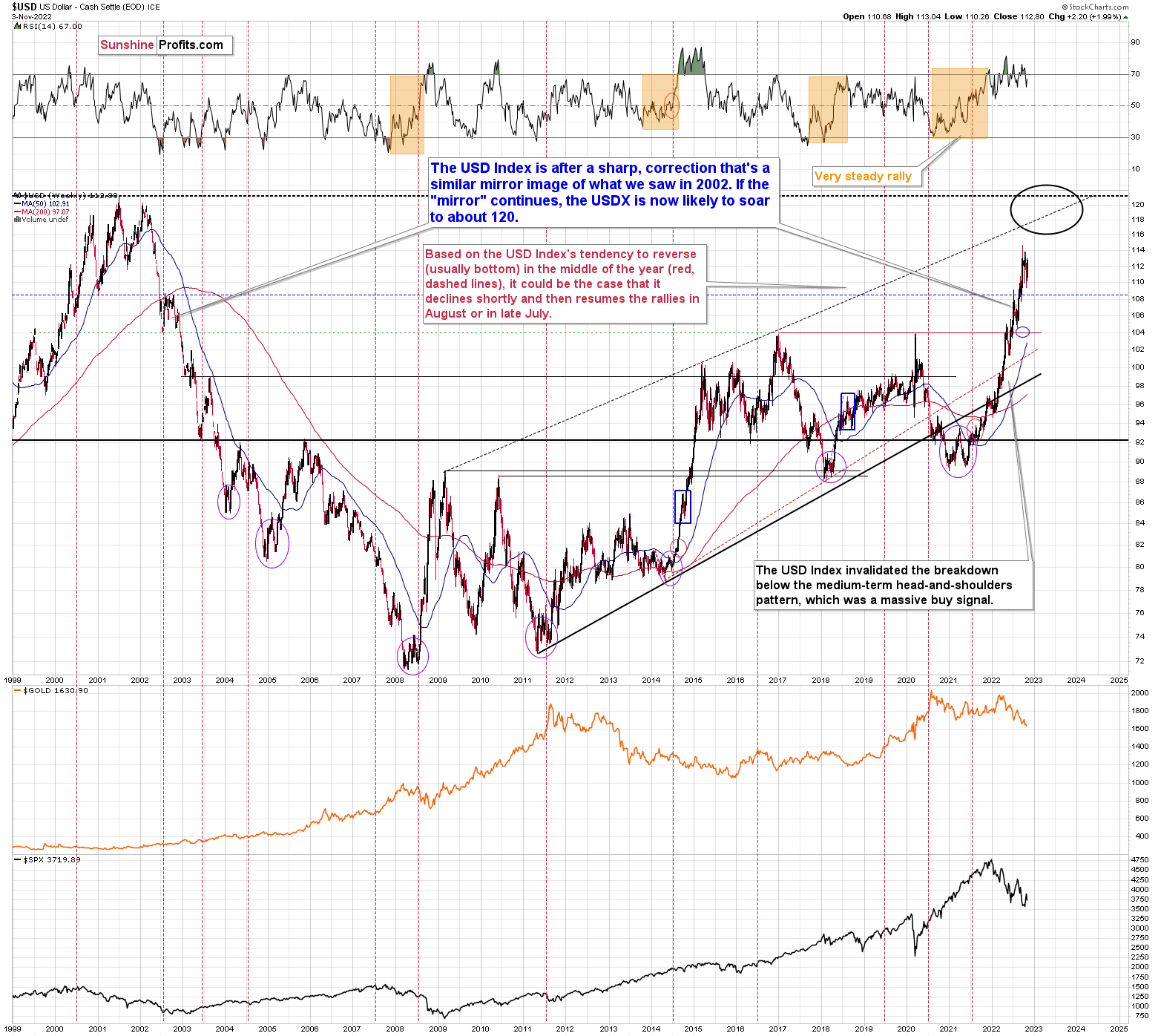

From the long-term point of view, the USD Index is currently rallying in approximately the mirror image of how it declined in 2002. Based on this, it seems that one shouldn’t be surprised by a rather quick move from the current levels to about 120 – USD Index’s long-term highs. Of course, the implications for the precious metals market are profoundly bearish.

This doesn’t rule out quick corrections along the way – those don’t interrupt the big, weekly/monthly moves at all, and they don’t break the analogy. This includes the recent downswing – it didn’t invalidate the bullish medium-term uptrend.

This is extremely bearish for gold and the rest of the precious metals sector.

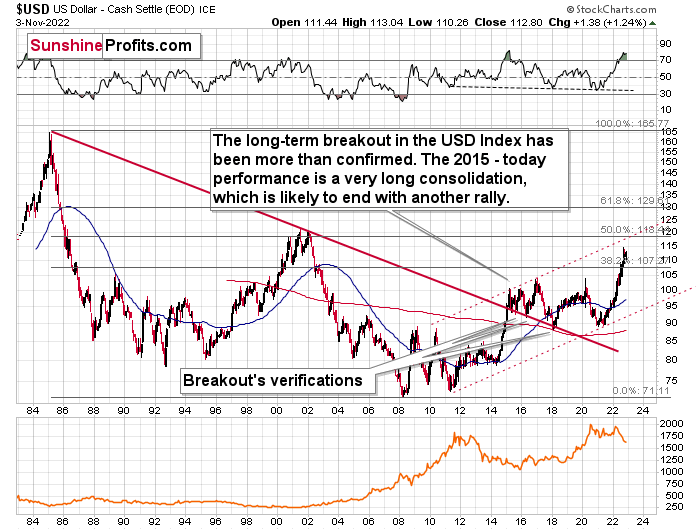

Before summarizing, do you remember the very, very long-term USD Index chart that I’ve been featuring for many months? The one below.

I emphasized that the USD Index was after a major breakout (in 2014/2015) that was then followed by a multi-year consolidation. The breakout was also verified in late 2017 / early 2018, when the USD Index moved back to the previously broken resistance line, and it verified it as support.

After that, it was only a matter of time before we saw a huge upswing. It certainly took a while, but the massive rally has indeed followed.

The reason why I’m mentioning this today is not to provide you with told-ya-so comments, but to emphasize that this big rally has legs. Strong legs.

On a day-to-day basis, it might seem unbelievable, temporary, random, or based on some sort of manipulation. But in reality, the writing has been on the wall for – literally – years! And those who have been following my analyses in the past were well-prepared – well in advance.

What does it tell us now? It tells us two things:

- The move to the 118 – 120 area is quite likely as there is little other strong resistance nearby.

- The top close to 118 – 120 might not be the final top for the USD Index. It could rally further (after a corrective decline from the above-mentioned area), but this might not necessarily mean that gold will decline in the following years (beyond the medium-term decline to $1,400 or so).

All in all, the outlook for the USD Index remains bullish, which has bearish implications for the medium term, but I don’t think it will prevent the precious metals market from rallying in the long run.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over and that the next big move lower is already underway.

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

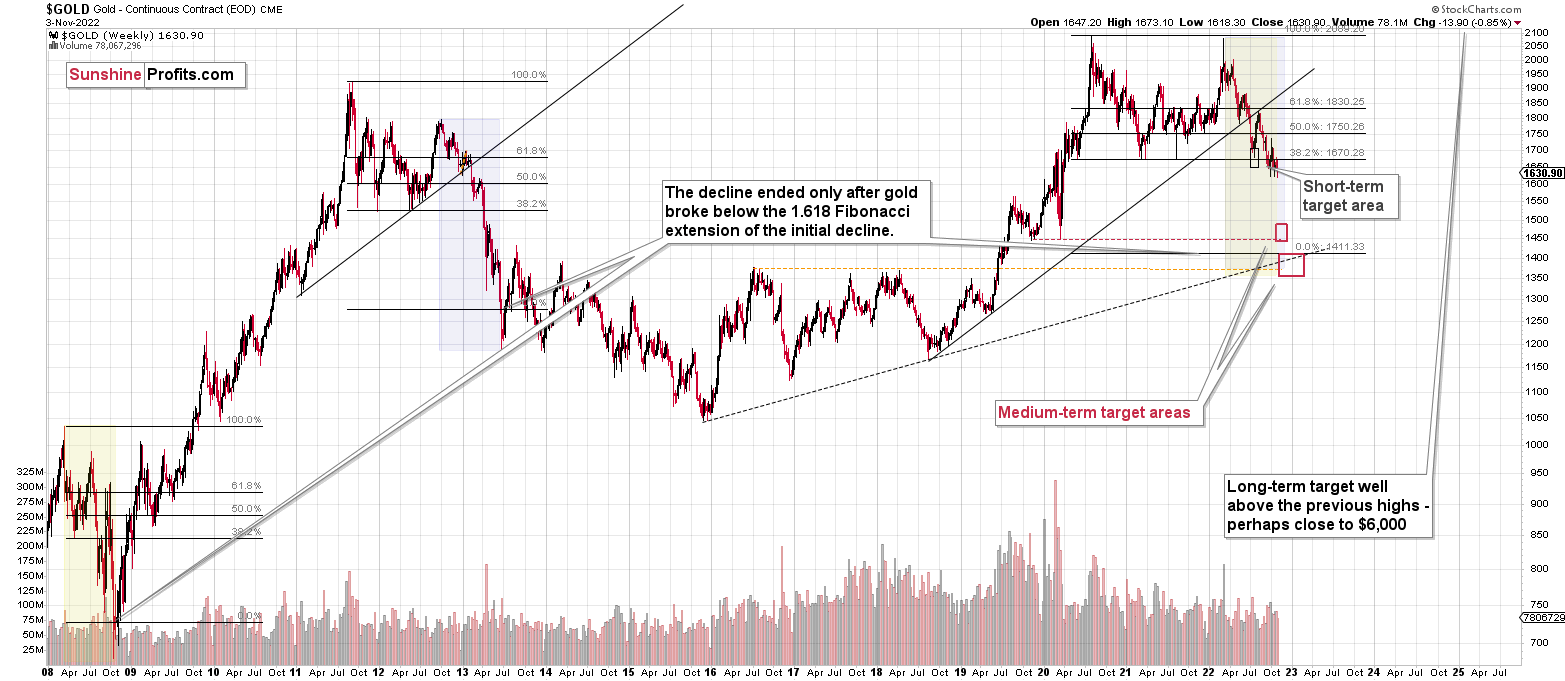

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, it seems that the biggest part of the 2013-like decline is taking place right now, and – while I can’t make any promises regarding performance - it seems likely to me that our big profits are about to become huge and then ridiculously big in the relatively near future.

As I have written before, the recent upswing didn’t change anything. While the mining stocks appeared “strong” recently, it seems to me that it’s just a reflection of the temporary (in my view) strength in the general stock market. And as stocks decline, mining stocks – and especially junior mining stocks – are likely to truly slide.

Things might happen very fast in the coming days, and if I plan to make any adjustments, I’ll keep you informed. Still, if the targets that I’m mentioning in the “Trading” part of the summary are reached, I think that profits should be taken off the table without an additional confirmation from me. I will probably get on the long side of the market at that time, but I’ll send a confirmation if I decide to do so.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Friday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief