Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update. , our most recently featured medium-term outlook remains the same as the price moves align with our expectations (or at least are not really against them). On that account, there are parts of the previous analysis that didn’t change at all in the earlier days and are written in italics.

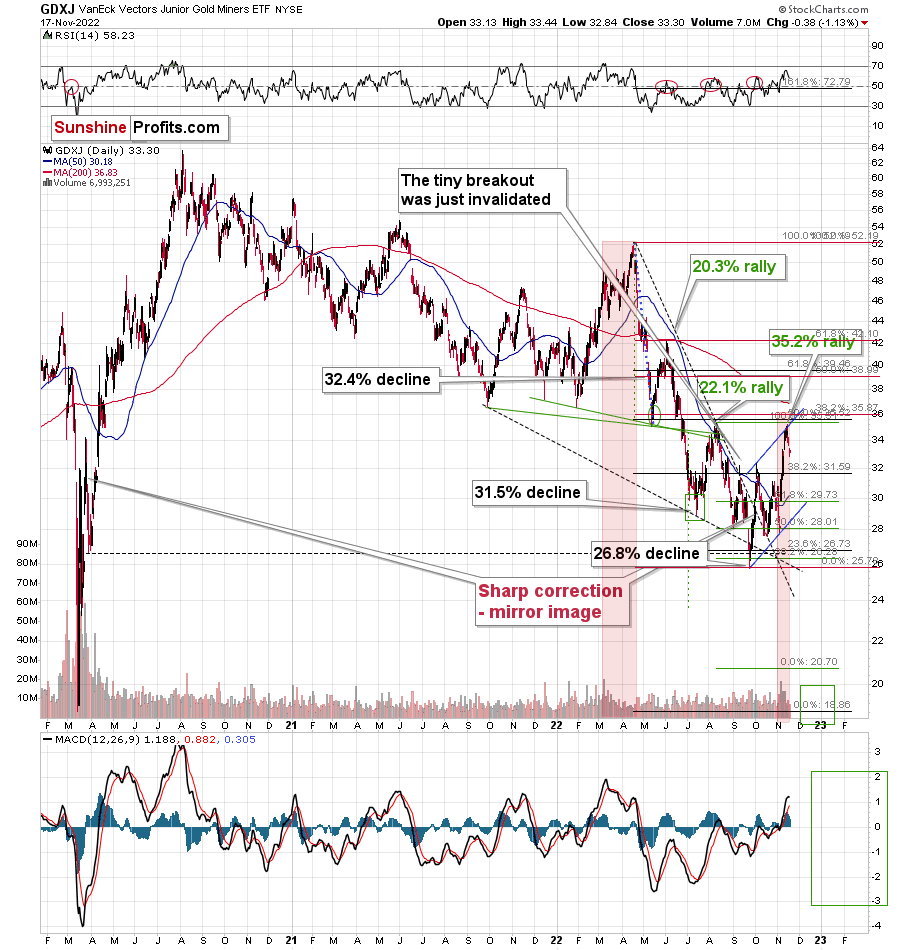

The key thing is that the corrective upswing in gold is most likely over – completely over. The shape of the price moves in the GDXJ as well as the relative performance of gold stocks vs. gold both support this scenario.

Let’s start today’s analysis with a recap of what recently happened on the fundamental front.

The Weekly Fundamental Roundup

With the S&P 500 languishing as it searches for fresh upside catalysts, gold, silver, and mining stocks ended the Nov. 17 session in the red. Moreover, while this week reversed some of the short-squeeze optimism, the PMs should confront material downside as the Fed’s inflation fight continues.

To that point, I’ve warned for months that higher interest rates would negatively impact the gold price, and with inflation, growth, and employment still resilient, officials continue to warn investors about the hawkish realities that lie ahead.

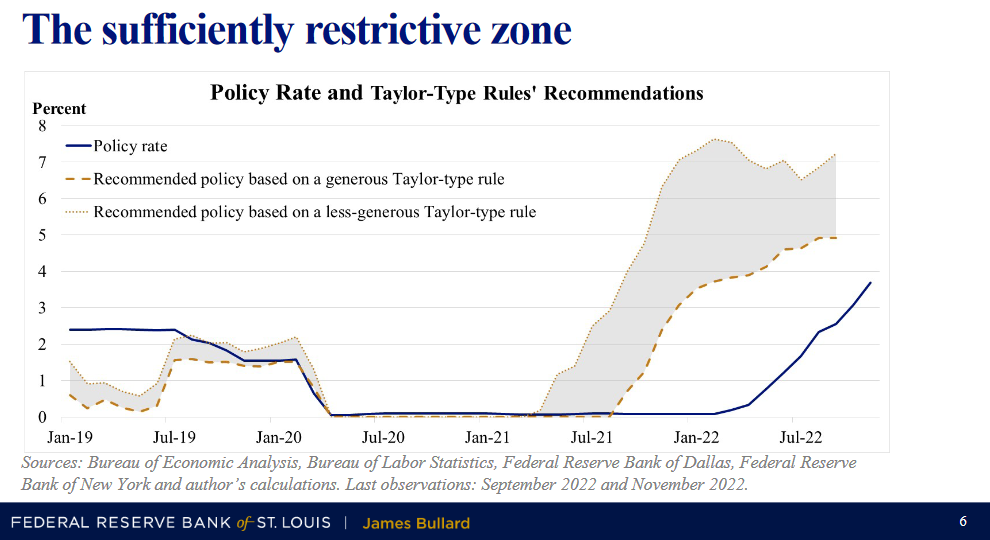

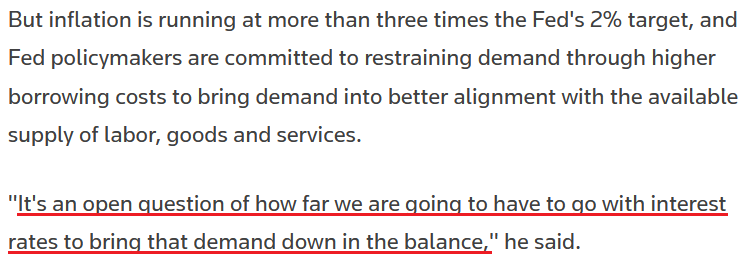

For example, St. Louis Fed President James Bullard said on Nov. 17:

“Thus far, the change in the monetary policy stance appears to have had only limited effects on observed inflation, but market pricing suggests disinflation is expected in 2023.”

However:

“The policy rate is not yet in a zone that may be considered sufficiently restrictive. To attain a sufficiently restrictive level, the policy rate will need to be increased further.”

As a result, Bullard noted that the U.S. federal funds rate (FFR) needs to reach 5% to 5.25% to be “sufficiently restrictive,” and even that may not be high enough when it’s all said and done.

Please see below:

To explain, Bullard used the Taylor Rule to approximate the appropriate FFR. If you analyze the right side of the chart, the low-end of the gray shaded area implies a ~5% FFR using “generous” (dovish) expectations.

Conversely, the high-end of the gray shaded area implies a ~7% FFR using “less-generous” (hawkish) expectations. Therefore, while the crowd continues to assume that inflation will decline with ease, historical precedent and economic logic signal the opposite.

Likewise, Minneapolis Fed President Neel Kashkari said on Nov. 17:

“I need to be convinced that inflation has at least stopped climbing, that we're not falling further behind the curve, before I would advocate stopping the progression of future rate hikes. We're not there yet.”

More importantly, Kashkari admitted that the Fed doesn't know how high the FFR needs to rise. In reality, INFLATION and employment dictate the FFR's peak, as interest rates are only restrictive when they have the desired effect on the U.S. economy. In contrast, investors assume that when Fed officials' preach patience, it means the inflation issue is solved.

However, while this uninformed belief helps underwrite short-term rallies, don't be surprised if the FFR surpasses our previously out-of-consensus estimate of 4.5% to 5.5% in 2023.

Please see below:

Source: Reuters

Source: Reuters

Also noteworthy, Fed Governor Philip Jefferson said on Nov. 17:

“Price increases have been particularly sharp for necessities like food, transportation, and shelter, which make up a substantial portion of household budgets for people on the lower end of the pay scale. Lower-income households have less in savings to buffer price increases, meaning that they not only feel the effects more forcefully, but they also feel them immediately (…).”

“Monetary policy cannot address the specific reasons that low-income households suffer the most from high inflation. But these reasons help to illustrate the importance of low inflation: low inflation is key to achieving a long and sustained expansion – an economy that works for all. Pursuing our dual mandate is the best way for the Federal Reserve to promote widely shared prosperity.”

So, while investors are eager to bring back the pre-pandemic days of stable inflation, low interest rates, and QE, it’s a fairy tale. In reality, Americans are confronted with the highest inflation in 40+ years, and the longer it persists, the worse it will be for the U.S. economy. As such, the Fed should remain hawkish, and the fundamental backdrop is bullish for the FFR, real yields, and the USD Index.

PMIs and the Gold Price

While the yellow metal has rallied sharply off its 2022 lows, the misguided optimism was driven by the belief that a dovish pivot was imminent. However, with market participants underestimating the Fed's conundrum, the PMs should suffer when reality returns.

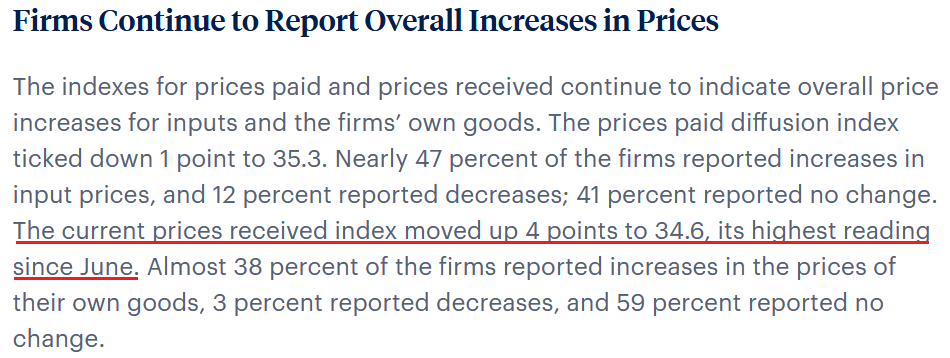

For example, the Philadelphia Fed released its Manufacturing Business Outlook Survey on Nov. 17. The headline index declined from -8.7 in October to -19.4 in November. However, the report stated:

“Firms reported overall increases in manufacturing employment, but the current employment index fell 21 points to 7.1. Although most firms (69 percent) reported steady employment levels, 19 percent of the firms reported higher employment, and 12 percent reported lower employment.”

Thus, while the employment results were relatively constructive, Philadelphia manufacturing firms noted that inflation remains problematic.

Please see below:

Source: Philadelphia Fed

Source: Philadelphia Fed

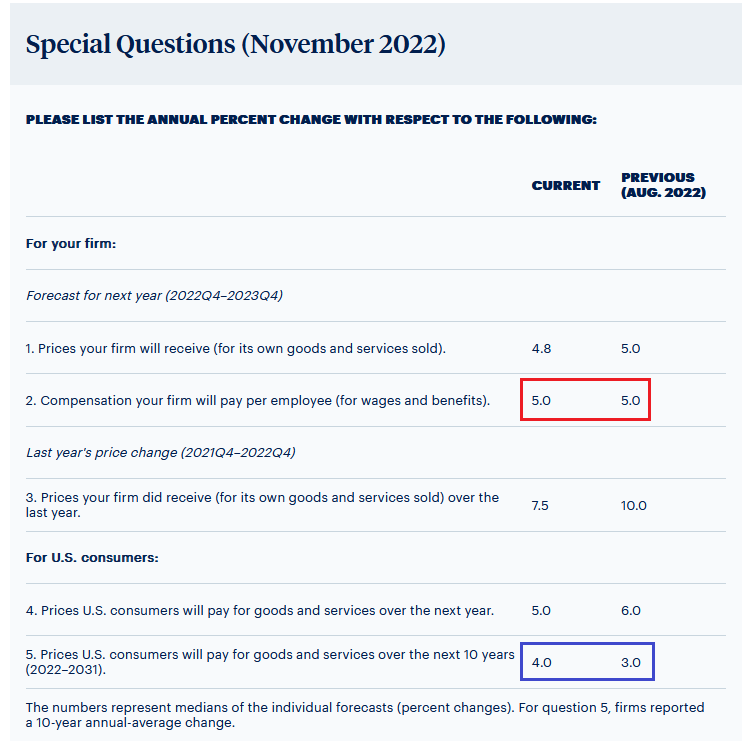

In addition, while respondents’ inflation expectations have largely declined since the “special questions” were asked in August, their estimates are still well above the Fed’s 2% target.

Please see below:

Source: Philadelphia Fed

Source: Philadelphia Fed

To explain, the red box above shows that respondents’ wage inflation expectation remained constant at 5%, while their 10-year output inflation expectation increased from 3% to 4% (the blue box). Therefore, while respondents’ 12-month output inflation expectation decreased, consistent wage inflation is why the Consumer Price Index (CPI) should remain uplifted for longer than the consensus expects.

Speaking of which, the Kansas City (KC) Fed released its Tenth District Manufacturing Activity Survey on Nov. 17. The headline index increased from -7 in October to -6 in November. However, a similar theme was present.

Regarding inflation:

“The monthly index of raw materials prices continued to slow in November and decreased compared to a year ago. Finished goods price indexes increased slightly from a month ago and compared to year-ago levels.”

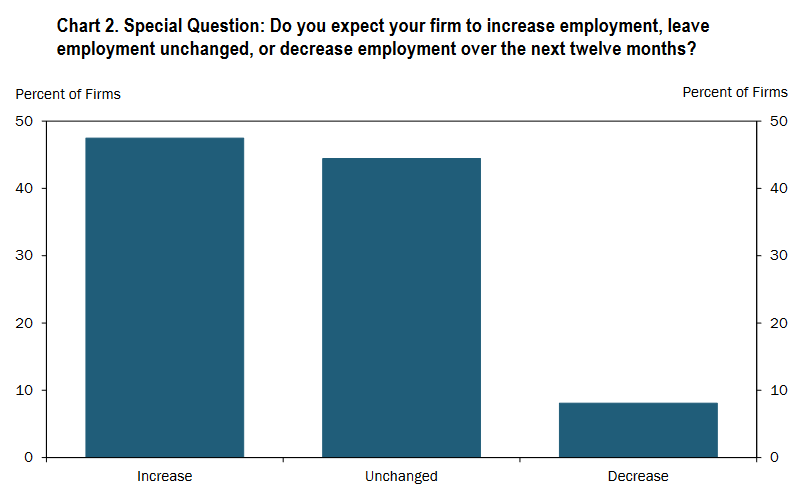

Regarding employment:

“About 47% of firms expected to increase employment over the next 12 months, 44% of firms expected to leave employment unchanged, and 8% of firms expected to decrease employment over the next 12 months.”

Please see below:

Source: KC Fed

Source: KC Fed

To explain, the two blue bars on the left highlight how 91% of KC manufacturing firms expect to maintain or increase their staffing levels over the next 12 months. As such, the results are bullish for wage inflation, which is bullish for the FFR, real yields, and the USD Index.

The report added:

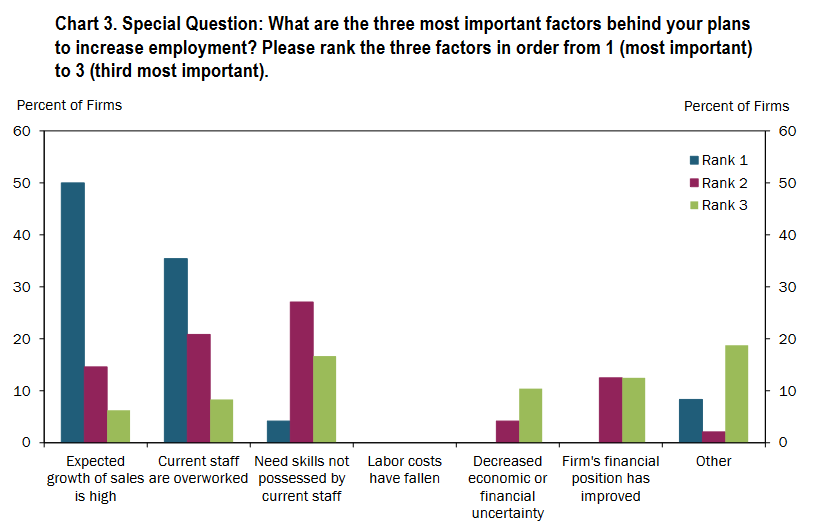

“About 71% of firms planned to increase employment because expected growth of sales is high, ranking it as one of the top three factors driving employment plans. Other firms noted that employment plans are driven by current staff being overworked or that the firm needs skills not possessed by current staff.”

Please see below:

Source: KC Fed

Source: KC Fed

To explain, the blue bars (Rank 1) on the left show how high sales growth and overworked employees are the primary reasons why KC firms plan to increase their workforce; and while I warned repeatedly that demand was much stronger than the consensus realized, resilient sales and busy staff are the opposite of demand destruction.

To that point, notice how no firms cited “labor costs have fallen” as a reason to increase their headcount? This means they continue to pay up for employees, and persistent wage inflation is why the crowd underestimates the hawkish realities that should weigh on the gold price in the months ahead.

The Bottom Line

While short-squeeze optimism still remains, investors are struggling to find bullish catalysts to push risk assets higher. Furthermore, while they want to overlook the bearish fundamentals and orchestrate a Santa Clause rally, the data continues to disappoint the pivot bulls. So, while the dip buyers were out in full force in the afternoon on Nov. 17, the strategy has been highly unprofitable in 2022, and more of the same should commence when sentiment shifts.

In conclusion, the PMs declined on Nov. 17, as the USD Index and the U.S. 10-Year real yield moved higher. However, the S&P 500’s afternoon rally showed how hope is still a popular investment strategy on Wall Street. Yet, with the fundamentals continuing to deteriorate, the optimism should turn to pessimism sooner rather than later.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Nov. 22: Richmond Fed manufacturing index

Piggybacking on the important revelations from the Philadelphia and KC Fed’s surveys, the Richmond Fed will detail the growth, inflation, and employment outlooks in Virginia.

- Nov. 23: S&P Global U.S. Composite PMI, FOMC minutes

S&P Global conducts a nationwide survey, so the results are often leading indicators of future government data. In addition, the FOMC will release the minutes from its Nov. 1-2 monetary policy meeting, and the text should provide more insight into officials’ future FFR expectations.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

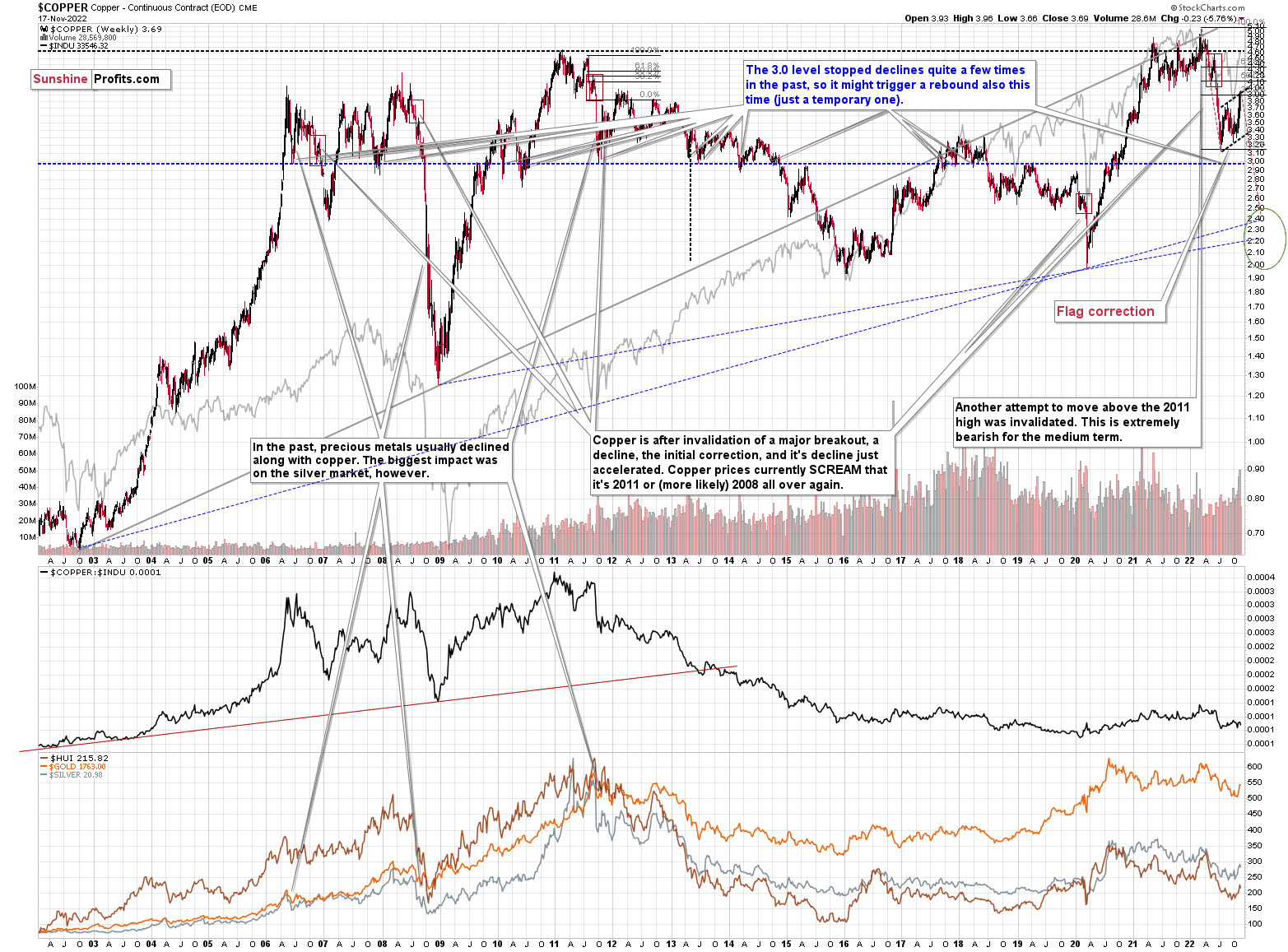

Let’s start today’s technical discussion with a quick check of copper prices.

Overall, everything I wrote about it last week (and in the previous weeks/months) remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

No market moves up or down in a straight line (well, the 2008 slide appears to have been an exception), and a short-term correction doesn’t necessarily invalidate the bigger trend. For the last couple of months, copper has been trading sideways, but it didn’t change much regarding the outlook.

In fact, it made my previous target area even more likely. You see, the consolidation patterns are often followed by a move that’s similar to the move that preceded them. In this case, the previous 2022 decline was quite significant, and if it is repeated, one can expect copper to decline well below 3.

Actually, copper could decline profoundly and bottom in the $2.0-2.4 area. That’s where we have rising, long-term support lines and also the previous – 2016 and 2020 – lows.

Flag patterns (which we just saw in copper) tend to be followed by price moves that are similar to ones that preceded them. I marked this on the above chart with red, dashed lines. This method supports a copper price increase to around $2.4.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after invalidation of a major breakout, a decline, and a correction. Copper prices currently SCREAM that it’s a variation of 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

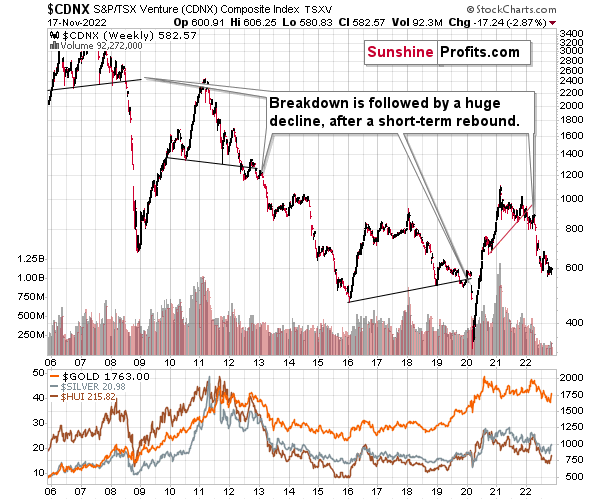

Having said that, let’s check junior miners’ really big picture.

I previously commented on the above chart in the following way:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

Having said that, let’s turn to gold.

Let’s start with context:

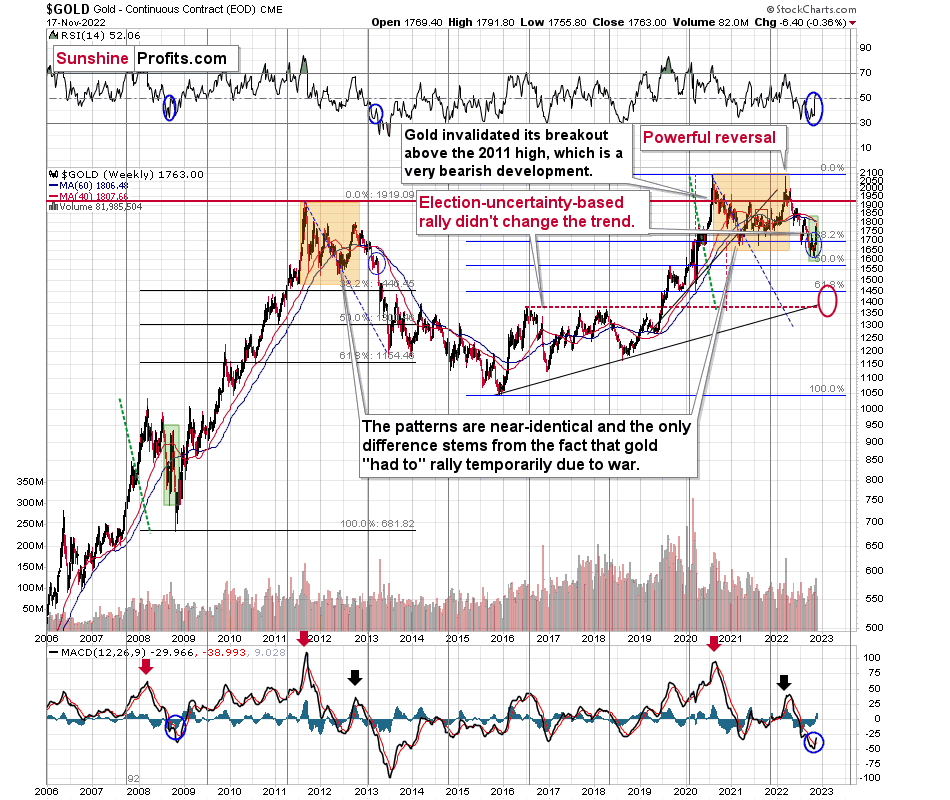

Between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet gold failed to rally to new highs.

In fact, it’s trading very close to its 2011 high, which tells you something about the strength of this market. It’s almost absent.

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. We can also spot similarities between now and 2008. The long-term gold price chart below provides details.

Looking at the gold market from a broader point of view reveals that what we saw recently is something between what we saw in 2013 and what we saw in 2008.

For many months, I've been writing that the situation is analogous to both of the preceding periods, and that the recent sharp corrective upswing fits this narrative rather than breaking it.

Last week’s weekly volume reading was the second biggest reading that we have seen this year. The record was formed in early March – at the yearly top. Does this sound bullish? No, it’s a bearish indication, as history tends to rhyme.

Returning to the 2008 comparison, please keep in mind that the sharp rally seen back then was much larger than what we saw this time. The moves higher in the RSI are similar, and I marked them with blue.

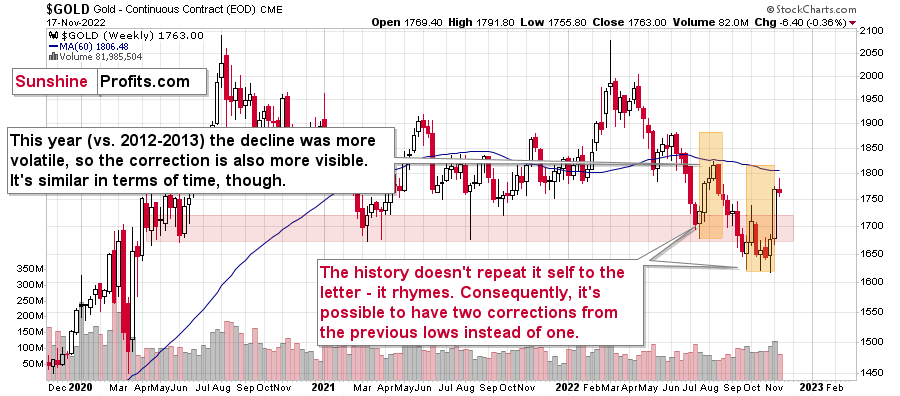

Now, as far as the link to 2013 is concerned, it remains perfectly intact, with the additional note that this time, the final correction that took the gold price back to its 60-week moving average (blue line) was bigger. That’s not that surprising given that the preceding decline was more volatile.

To clarify, it is visible, but what’s visible is still in tune with the final attempt for gold to rally in April 2013, right before the biggest part of the slide.

Gold is sometimes forced to react to some geo-political events as the safe-haven buying kicks in, but these moves are usually short-term lived. Looking at long-term charts helps to keep things in proper perspective.

Consequently, my previous comments remain up-to-date:

Based on the above chart, it’s quite clear that the situation that is now being repeated. The patterns marked with orange rectangles and blue ellipses are almost identical (also in the MACD indicator, and to a lesser extent in the RSI indicator).

Sure, the situations are not identical, as this time we had a Russian invasion of Ukraine that pushed gold temporarily higher. Other than that, the situations are extremely similar.

Based on the stage of the self-similarity and the confirmed breakdown below the $1,700 level, gold is now likely to slide.

Based on the analogy to 2013, it’s not only likely to slide, it’s likely to slide profoundly in a sharp manner. These may be the last days or hours before the slide fully begins.

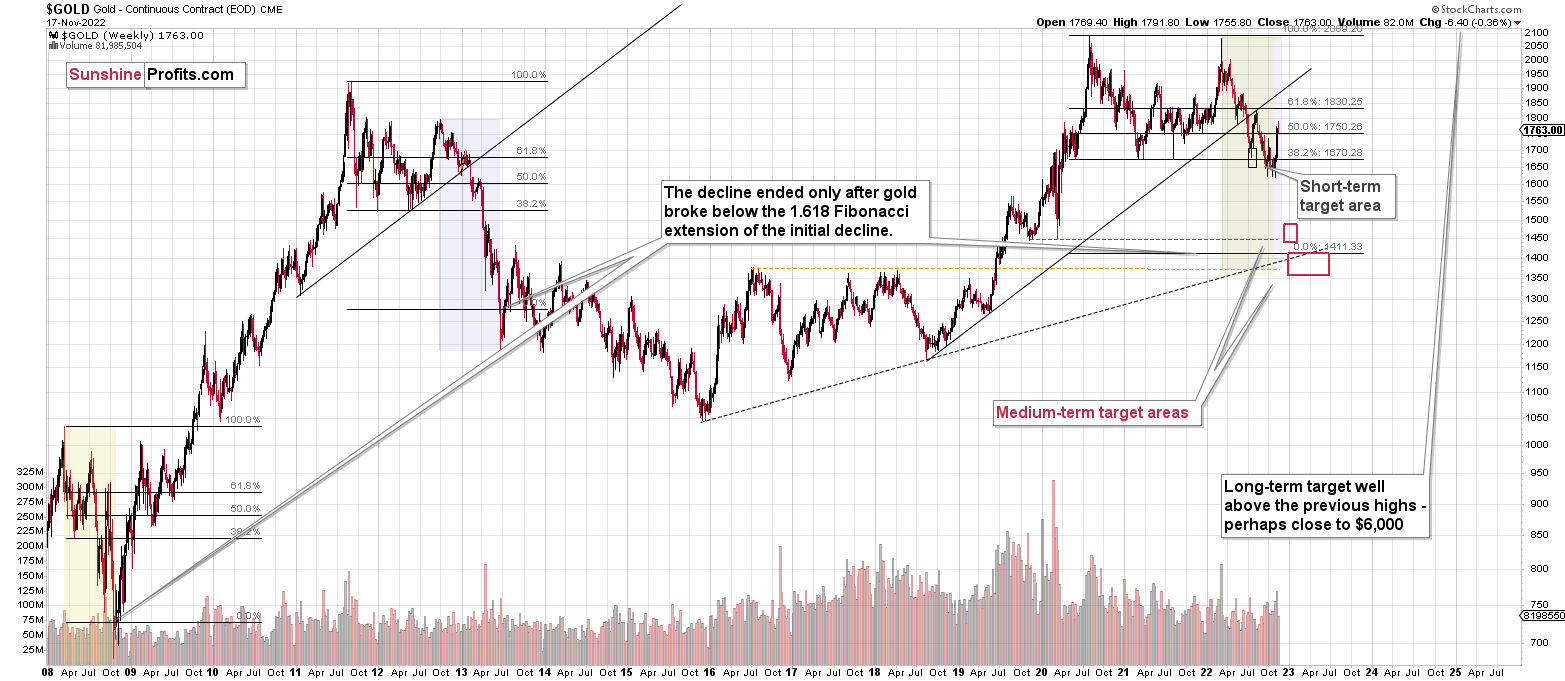

How low is gold likely to go during this upcoming big medium-term decline? Perhaps as low as its 2020 low, around $1,450-1,500. Then, after a rebound, quite likely to be at or slightly below $1,400.

I realize this is far from the current price, but nonetheless, this target area appears justified in my opinion. There are two important Fibonacci retracements based on the 2015-2020 rally that gold can bounce from (it recently bounced from the 38.2% retracement). These are 50% and 61.8% retracements.

The support provided by the 61.8% retracement is strengthened by the 2020 low and the support provided by the 50% retracement is strengthened by the 2019 high.

However, based on gold’s self-similarity to 2013, it seems that we’re about to see a slide that’s bigger than what we’ve been seeing so far this year. This time – based on the similarity – gold is likely to decline profoundly, but no longer in the back-and-forth mode. If gold formed its next local low at the 50% retracement (so at about $1,560), then it might do so still within the declining, short-term trend channel (sometime in September).

However, if gold is to stick to the link to 2013, then it should decline more rapidly. In this case, the technique that can help us estimate the short-term target is the one that says that after a breakdown from a trend channel, price is likely to move approximately by as much as the height of the previous trend channel. In this case, gold could break below the trend channel soon and then decline even more. Based on the height of the trend channel, the above means that a move to the 61.8% retracement as the next downside target is more likely than a move to the 50% retracement.

I previously wrote that the above-mentioned decline in gold would likely be linked to a breakdown in the EUR/USD below 1, and we already saw both: decline in gold, and a breakdown in the EUR/USD below 1. The implications remain bearish.

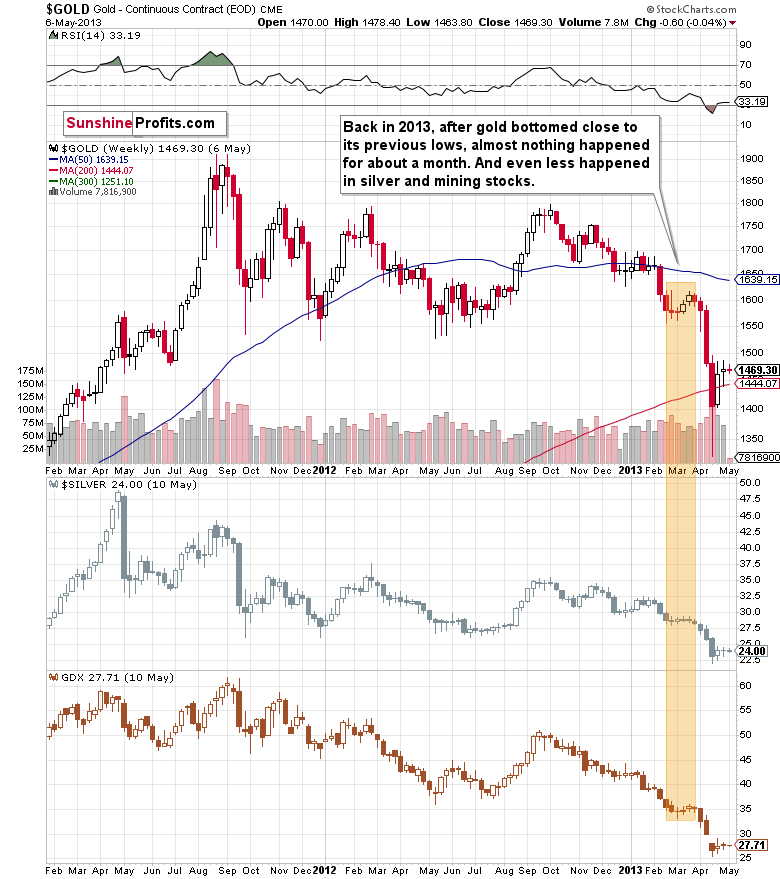

Let’s zoom in on what happened in 2013 after the analogous rebound.

Well, gold consolidated for a few weeks and plunged only after that consolidation.

That’s what we saw recently as well. Of course, we haven’t seen the big plunge yet, but the other parts of the recent price patterns are very, very similar to what we saw in 2013.

Still, let’s keep in mind that history doesn’t necessarily repeat itself to the letter – it rhymes. Consequently, it’s quite possible to have two (or three, depending on how one counts the Sep.-Nov. performance) corrections from the previous lows instead of just one.

Especially if the temporary (!) effect of geopolitical events practically forces gold to move up due to safe-haven demand.

In other words, on a more-or-less basis, gold is doing exactly what it’s been doing in April 2013, right before the biggest part of the slide.

This time, gold has been making a few attempts to break lower, as geopolitical news and rumors keep popping up.

This week’s performance so far (I’m writing this very early on Friday) features gold’s reversal. So, unless gold rallies today, we’ll have a weekly shooting star candlestick, which is a very bearish sign, especially when it’s after a rally.

Having said that, let’s zoom in to see gold’s short-term price moves.

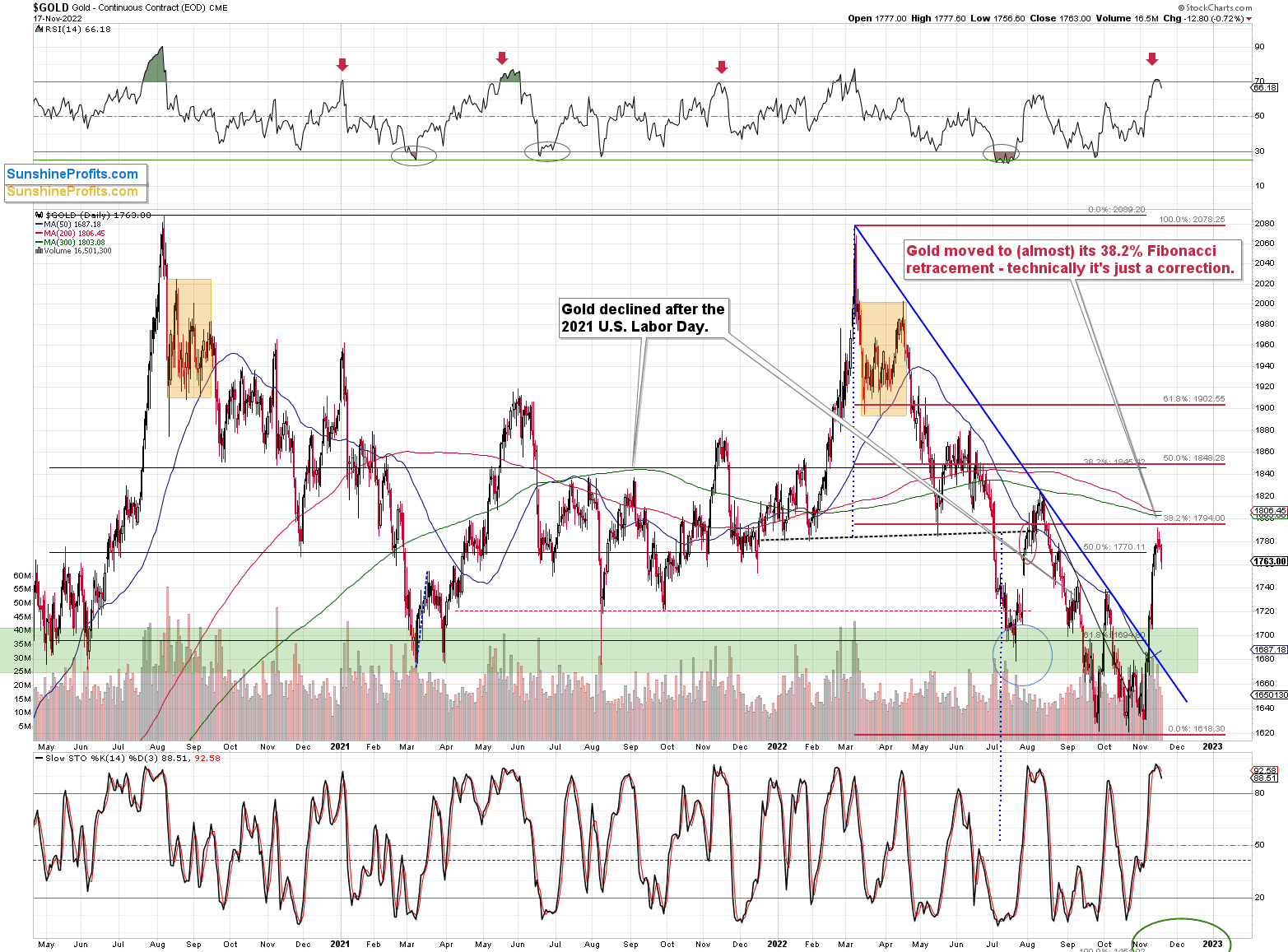

Gold, just like many other markets, recently corrected ~38.2% of its previous move.

Technically, moves that are smaller than the above percentage are usually not viewed as new rallies that would change the trend. They are too small compared to what happened previously to be considered a game-changer, or, perhaps, a trend-changer.

In fact, even moves smaller than 61.8% of the previous move are sometimes considered relatively unimportant. The ones that take the market back about 38.2% characterize strong trends – the counter-force (gold bulls in this case) is only able to trigger a rally of this size – less than half of the previous downswing.

Of course, the 38.2% Fibonacci retracement level serves as resistance on its own, and we just saw that in practice.

Not only that, the RSI moved a bit above 70 and then declined below it. This action marked major tops quite many times, including most major 2021 and 2022 tops. It seems that history is about to rhyme, and the gold price is about to slide.

The sell signal from the very overbought Stochastic indicator serves as yet another bearish confirmation.

Let’s keep in mind that the two key fundamental drivers of the gold price are: real interest rates and the USD Index.

The real interest rates are clearly headed higher (nominal rates are going up, and eventually inflation is likely to come down), which is bearish for gold.

Right now, gold continues to repeat its 2013 performance, which has extremely bearish implications for the coming weeks.

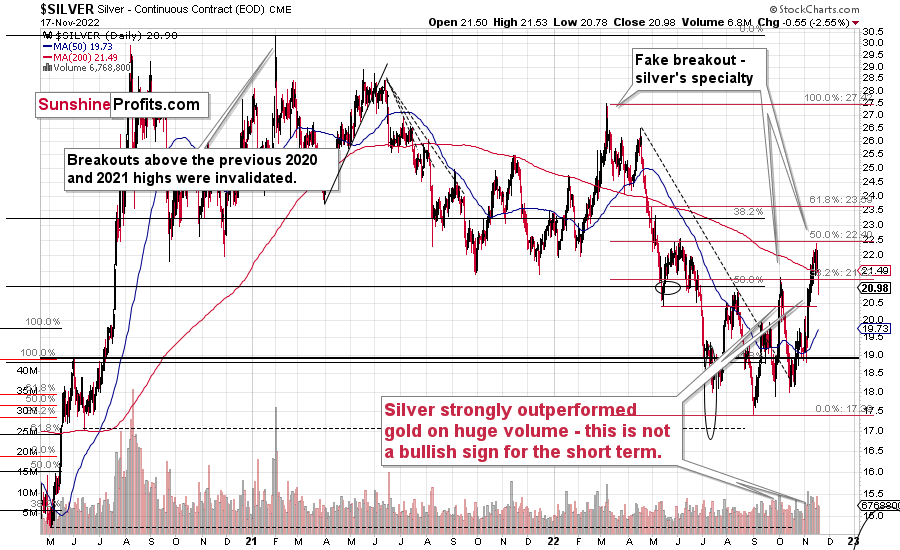

Having said that, let’s take a look at the silver market.

The key thing about the silver market remains its recent outperformance. Silver, unlike gold or mining stocks, has recovered 50% of its 2022 decline. Now it has moved back below its October 2022 high, but still, silver’s recent rally might seem bullish.

Yes, it appears bullish at first glance, but given my many years of experience on the precious metals market, I can tell you that this kind of performance (silver’s strength relative to gold) is rarely bullish. It’s usually the opposite. Silver soars and breaks above previous highs (or other important resistance lines) only to fool those who are new to this market. And then it slides.

It doesn’t have to happen each and every time, and I can’t guarantee any kind of performance, but the above really does have bearish implications right now.

As I explained in my Nov. 7 video, silver’s short-term outperformance is an important sell signal.

We have seen this indication many times before, and it’s been one of the most reliable indications that the next big move lower is at hand. Remember the spike at the 2021 top, when silver soared relative to gold? Many people thought that silver was taking off and heading straight to the moon, but I warned that this was likely a fake move, and indeed, that was the top.

There were times to be long this year (for example, I went long miners on May 12 and on July 11 – very close to local bottoms). However, in my opinion, right now is not a good time to do so. Instead, it seems to me that profits from short positions are likely to grow substantially in the following weeks.

Moreover, let’s keep in mind that the entire July-now period can be viewed as one big flag pattern, and those “continuation patterns” tend to be followed by moves that are similar to the ones that preceded them.

In this case, the move that preceded the flag was a decline from about $28. This means that another move lower in silver is likely to be huge.

Once silver breaks below its 2022 lows, it has little support all the way until its 2020 low. There’s support just below $15, but it’s not very strong, so it might not trigger anything more than a brief correction.

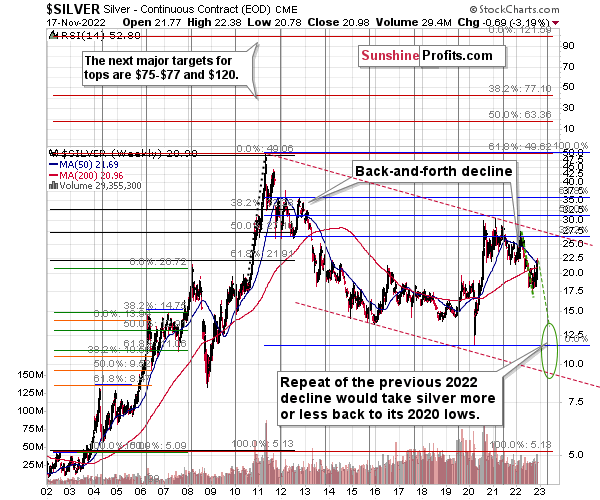

Let’s keep in mind that while gold is repeating its 2013 performance, so is silver.

As you can see on the above chart, silver corrected about 50% of the previous downswing, and this correction ended at about $30, a long time ago. Ever since, silver has been declining, and even the outbreak of war in Europe didn’t make it rally above that level.

On the above chart, you can see how silver first topped in 2011, then declined and formed another top at the cyclical turning point. Next, it declined once again, reaching the previous lows. After that, silver rallied (in 2012 and 2022), and it topped between its 50-week moving average (marked in blue) and the previous top. Now silver is declining in a back-and-forth manner (you can see it more clearly on the previous short-term silver chart).

Back in 2012, these were just the early days of a gargantuan decline, and the same appears likely to be the case this time. Interest rates are going up after all, and the Fed is determined to quench inflation.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Besides, please note that silver didn’t even manage to rally as much as copper (which tried to move to new highs recently) or most other commodities, thus being rather weak.

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

Having said that, let’s take a look at what happened in mining stocks.

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

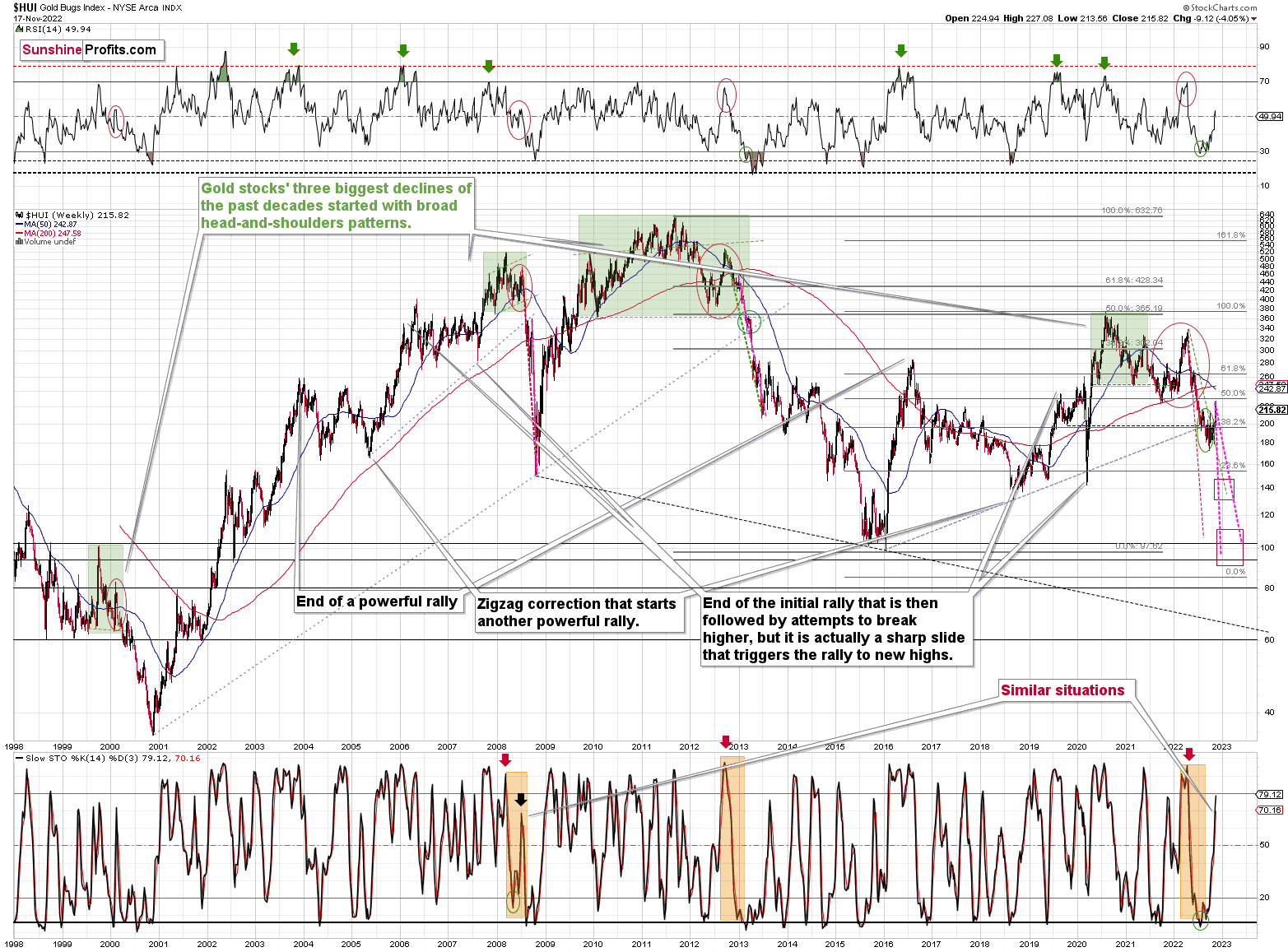

For example, right now, gold stocks are declining similarly to how they did in 2008 and in 2012-2013.

As gold was practically forced to rally recently based on geopolitical events, news, and rumors (and U.S. midterm election-based uncertainty), so were gold stocks.

Did it change anything technically?

Only a bit, and only at first sight.

The HUI Index is a bit above its rising resistance line, but it’s trading there after it already verified a breakdown below this line. And we already saw a 4%+ decline this week, so it remains doubtful if gold stocks are able to hold those gains.

Because the nature of the rally appears to be temporary, not only based on the analogy to 2013, but also on recent fundamental developments, I doubt that the breakout will be confirmed (as was the case with gold's short-term breakout).Please take a look at the stochastic indicator’s performance in the bottom part of the above chart. It’s currently doing practically the same thing that it did in 2008. And that – in 2008 – marked the final counter-trend top before the biggest part of the slide.

Is this time different? Those are expensive words on Wall Street.

I highlighted and copied the sharpest and final parts of the medium-term declines (2008 and 2013) to the current situation. There are quite a few other markings on the above chart, but the ones that I just mentioned are marked with the magenta color.

The analogy to 2008 points to the end of this year as being the likely moment for the final bottom.

The analogy to 2013 points to the middle of 2023 as being the likely moment for the final bottom.

The current situation is somewhat similar for both. However, it seems that what started as a primarily 2013-like move lower is becoming a 2008-like move lower. That’s based i.a. on the volatility of the recent upswing.

So, on average, early 2023 seems like a quite likely target for the final bottom.

Then again, please note that the two analogies fit right into my previous target area for the final bottom, so this target area simply remains intact.

Actually, based on both of the above, it seems that a move to 2020 lows close to the end of this year and then a correction followed by a move even lower in 2023 appear to be quite likely outcomes at this time.

How low can the HUI Index fall during the next big downswing?

As it’s the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 100-150 is my current target area for the upcoming slide in the HUI Index.

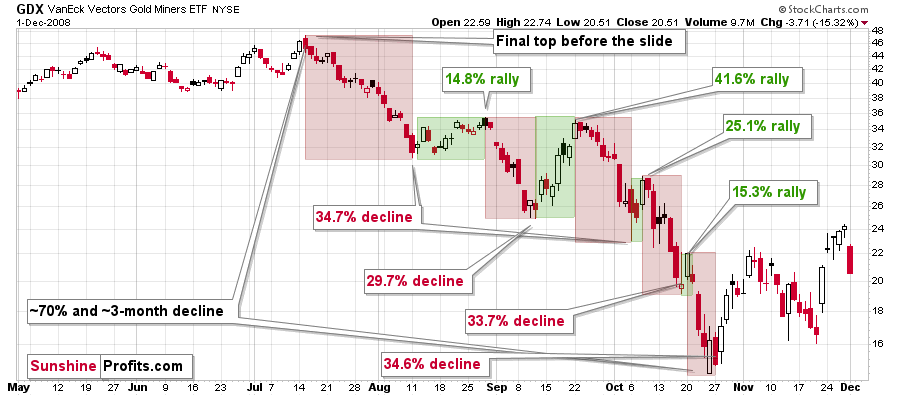

All right, let’s zoom in and see how mining stocks declined in 2008.

Back then, the GDXJ ETF was not yet trading, so I’m using the GDX ETF as a short-term proxy here.

The decline took about 3 months, and it erased about 70% of the miners’ value. The biggest part of the decline happened in the final month, though.

However, the really interesting thing about that decline – that might also be very useful this time – is that there were five very short-term declines that took the GDX about 30% lower.

I marked those declines with red rectangles. After that, a corrective upswing started. During those corrective upswings, the GDX rallied by 14.8-41.6%. The biggest corrective upswing (where GDX rallied by 41.6%) was triggered by a huge rally in gold, and since I don’t expect to see anything similar this year, it could be the case that this correction size is an outlier. Not paying attention to the outlier, we get corrections of between 14.8% and 25.1%.

Fast forward to the current situation. Let’s take a look at the GDXJ ETF.

The junior mining stocks moved sharply higher recently, and this move took place on huge volume (I spoke about it on Nov. 7). The only similarly big volume that we saw recently was at the early-March top and the January top. As history tends to rhyme, this kind of massive attention that junior miners got serves as a bearish indication.

Back in 2008, the biggest corrective upswing (the 41.6% rally) was the thing that preceded the biggest part of the medium-term decline.

This time, the volatility is not as big, but the size of the corrective upswing (assuming that it started in September) that we just saw is also greater than what we’ve seen before. Consequently, it could be the case that what happened recently is what “had to” happen given the way history decided to rhyme. Please note that we can estimate what is likely to happen based on historical analogies, but we can never be 100% certain that a given analogy will work and some others won’t.

In this case, it seems that the correction happened, even though it didn’t “have to” happen based on many other techniques. Either way, the medium-term trend remains down, so the current corrective upswing is likely to be a “thing of the past of little meaning” sooner rather than later.

Speaking of analogies, I previously wrote that the current rally is a mirror image (it’s not a crystal-clear mirror, though) of the corrective decline that we saw in late-March 2020. As it turned out, due to the most recent part of the upswing, the size of both moves became even more aligned.

And yes, this means that another decline could take the GDXJ all the way down to its 2020 low, or very close to it.

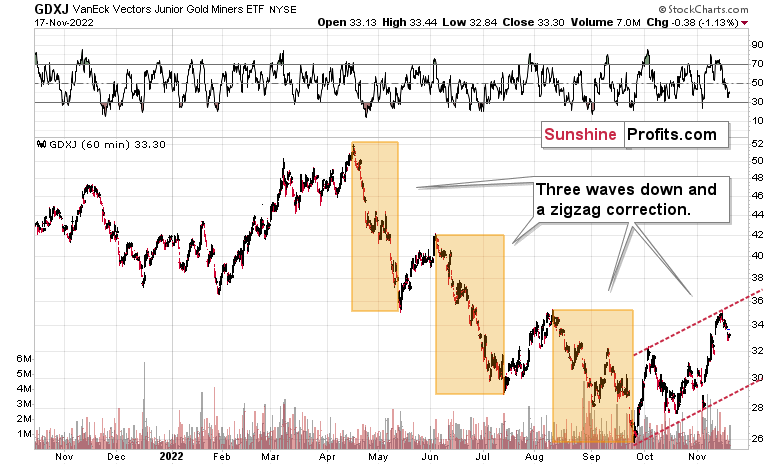

On the below chart, I marked just how perfectly the recent price moves played out according to the Elliott Wave Theory.

Of course, EWT is not the only tool that one could use, and I find other technical tools more useful, but still, this kind of pattern-following is uncanny.

The classic EWT pattern is three waves down (I marked those with orange rectangles) and then a correction consisting of two smaller waves.

That’s exactly what we have seen in recent months. The September–now pattern appears to be the above-mentioned correction. It didn’t only consist of two smaller waves higher – they were actually almost identical in terms of size and sharpness. This created a classic ABC correction (flag) pattern.

Now, since this pattern is complete, another huge 3-stage move lower can – and is likely – to unfold. This is very bearish for junior mining stocks (as well as for gold, silver, and probably other commodities and stocks), and the fact that juniors are already showing weakness relative to gold (the latter was almost flat yesterday, while miners declined) serves as a bearish confirmation. As always, I can’t guarantee anything, but in my view, the profits that can be reaped on this upcoming slide can be enormous.

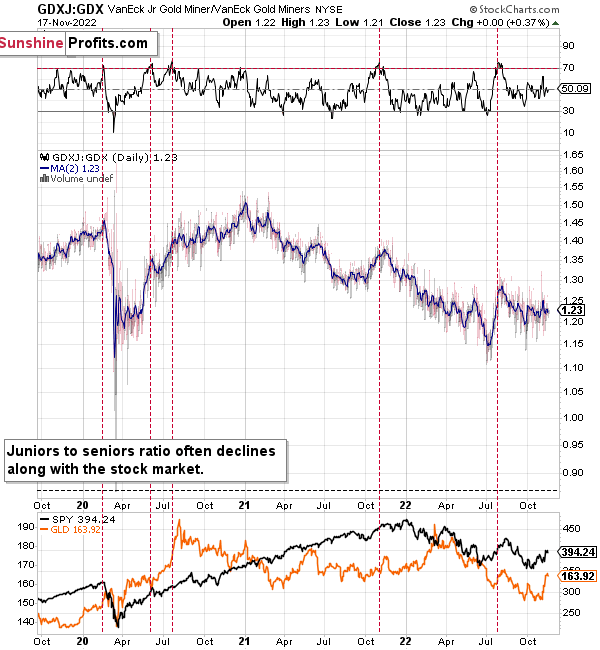

Meanwhile, the relative performance of junior miners compared to senior miners continues to deteriorate in a medium-term trend.

During this quick upswing, juniors rallied relative to seniors, but this is just a very short-term move that’s within a short-, and medium-term downtrends.

This implies bigger declines in the GDXJ in the future.

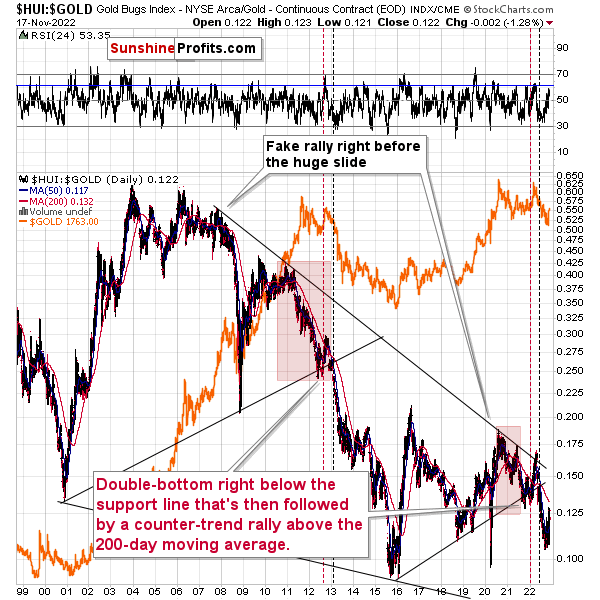

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw at the 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI to gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

Recently, we saw a quick upswing in the ratio, but that’s not a game-changer – even the biggest declines had corrections in the past.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices of gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks) and that’s exactly what’s likely to happen.

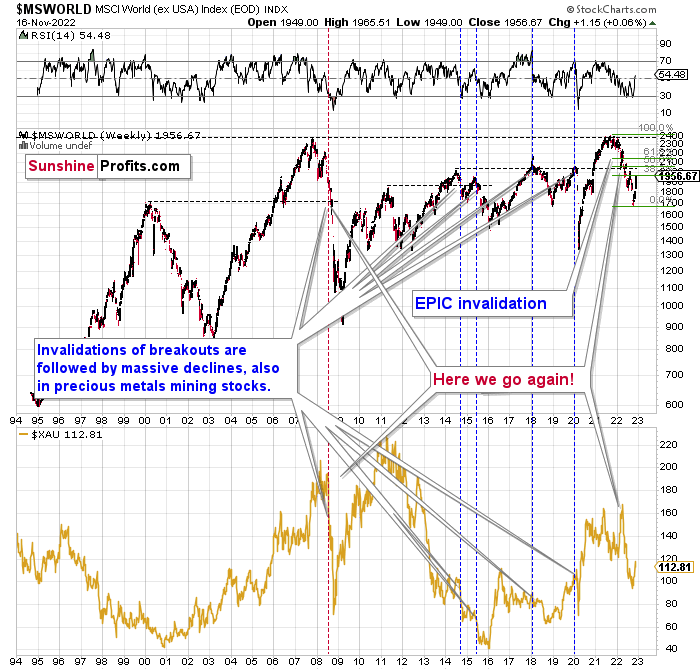

Just like what we saw in the case of copper, gold, and mining stocks, world stocks corrected about 38.2% of their preceding decline.

This means that nothing really changed, and the situation remains extremely bearish based, i.e., on the analogy to what we saw after previous invalidations of long-term breakouts.

As a reminder, in early 2022, I wrote that the situation was very bearish as invalidations of previous breakouts were usually followed by massive declines – not just in stocks but also in precious metals.

When stocks invalidated their 2006 breakout in 2008, their prices truly crumbled.

We also saw that on a smaller scale in 2014, 2015, and early 2018.

We’re seeing it right now.

To clarify, we’re actually seeing the aftermath of the invalidation. The huge decline is already taking place.

The difference between now and 2008 is that back then the slide was more volatile, and we didn’t really see a visible correction during the plunge. This time, the decline is more measured, and we saw a correction to one of the most classic retracements imaginable – the 38.2% one. This correction doesn’t change the trend, which remains down.

Based on what happened in 2008, it seems that stocks are about to move much lower in the following months.

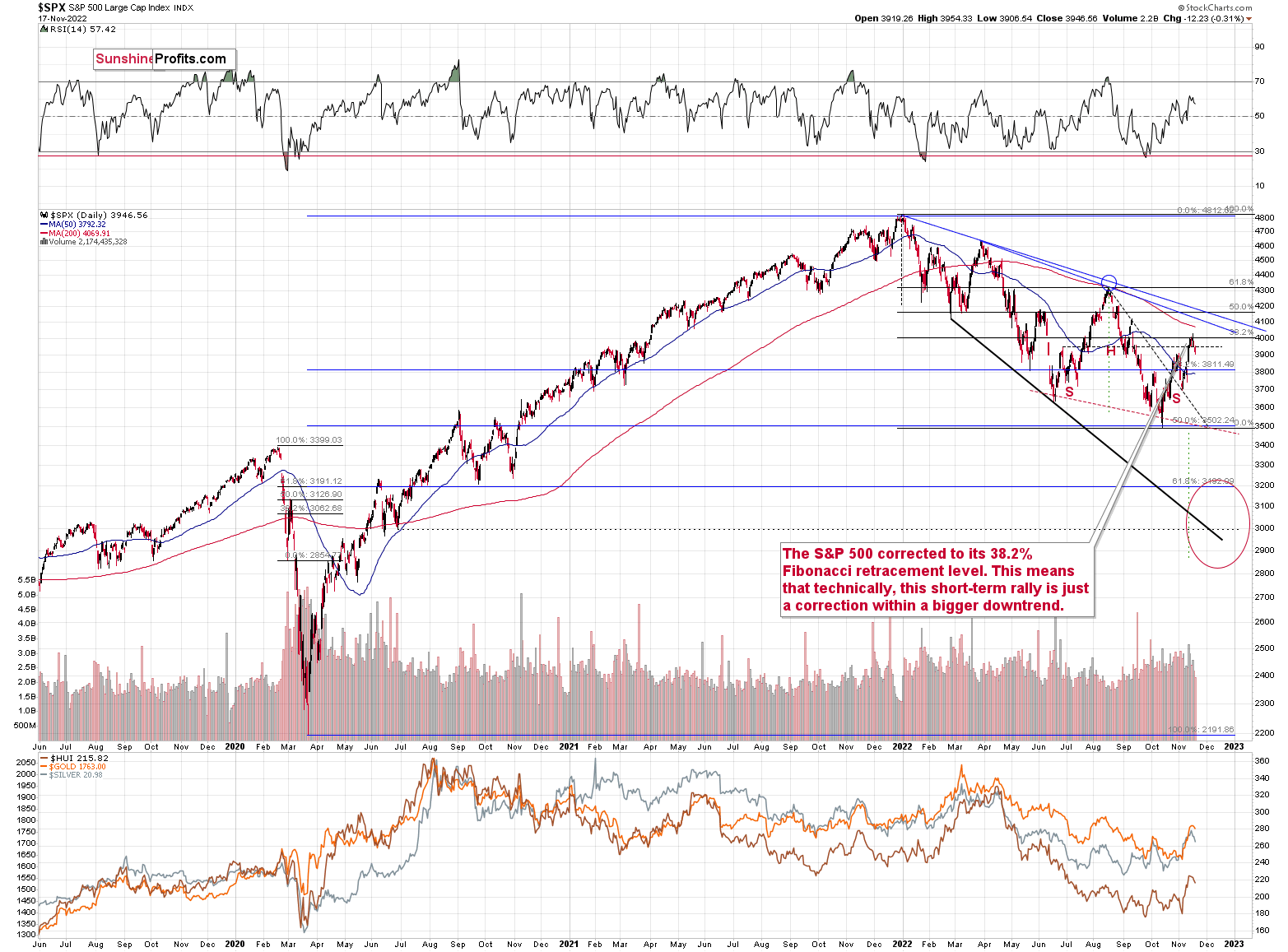

Let’s take a look at the markets from a more short-term point of view and from the U.S. perspective.

The S&500, like global stocks, corrected 38.2% of the previous decline. Now it’s declining, and it’s already moved back below the late-June high.

As real rates move higher, it seems likely that stock valuations will decline, and the technical situation supports this bearish stock price forecast.

The implications for the precious metals market are bearish, in particular for junior mining stocks.

The above would also be in tune with an extra rally in the USD Index. After all, less competitive exports are not that favorable for the U.S. economy.

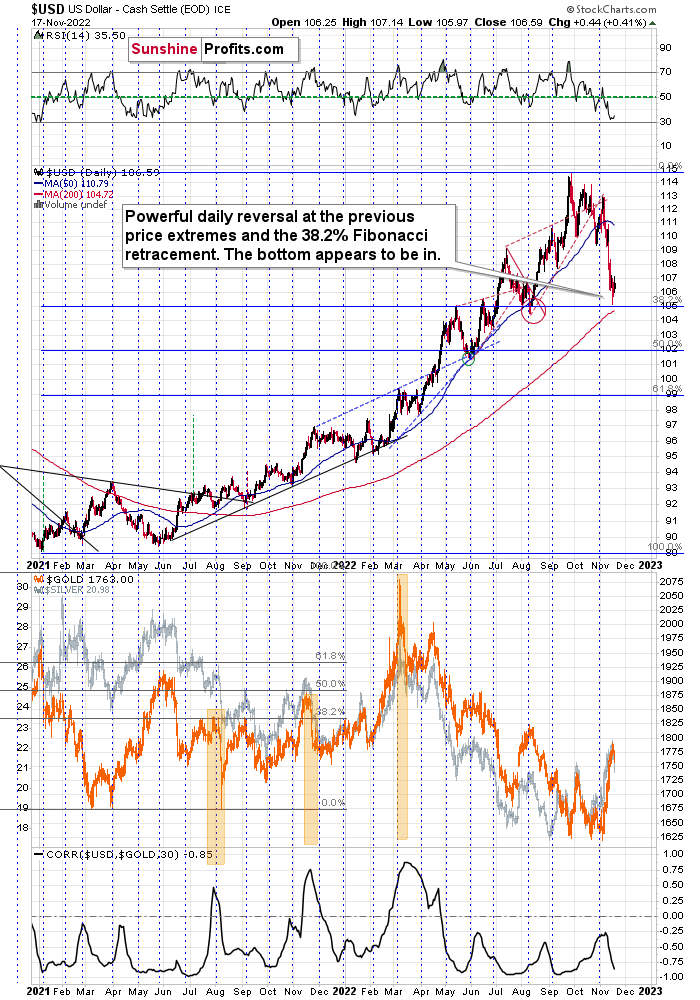

In Tuesday’s analysis, I wrote the following about the USD Index:

For example, the USD Index could decline to its strong support level at the 38.2% Fibonacci retracement and the August 2022 low as well as the May 2022 high. Such a move would likely imply the RSI at about 30, which would be a crystal-clear signal for many traders that the bottom is in.

To clarify, if that happened, the USD Index would be as oversold from a short-term point of view as it was at its 2021 bottom – when it was trading at about 90.

Despite the intraday attempt to move lower, the support held.

Consequently, what I wrote below the USDX chart remains up-to-date:

The USDX moved very close to the above-mentioned support levels, and it moved back up before the end of the day. The only reason that the RSI didn’t move to 30 is because the USDX declined only on an intraday basis. This means that from the RSI’s point of view, the situation is only “very bullish,” not extremely so. However, given the reversal nature of yesterday’s session, the outlook just became even more bullish, and it seems to me that the bottom is in.

This means that the top in the precious metals market is also likely in or at hand, especially given the S&P 500’s inability to break through its own 38.2% Fibonacci retracement.

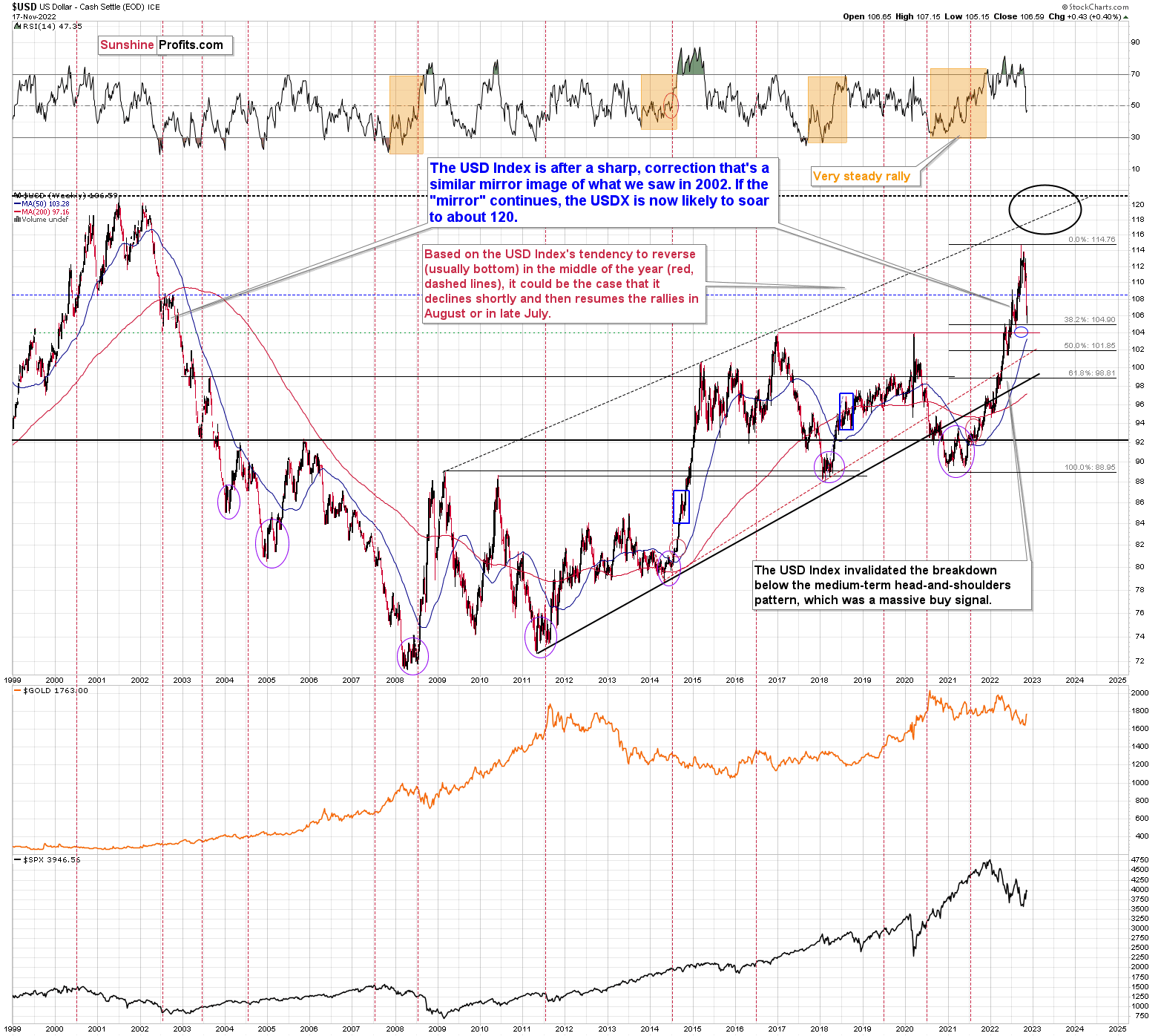

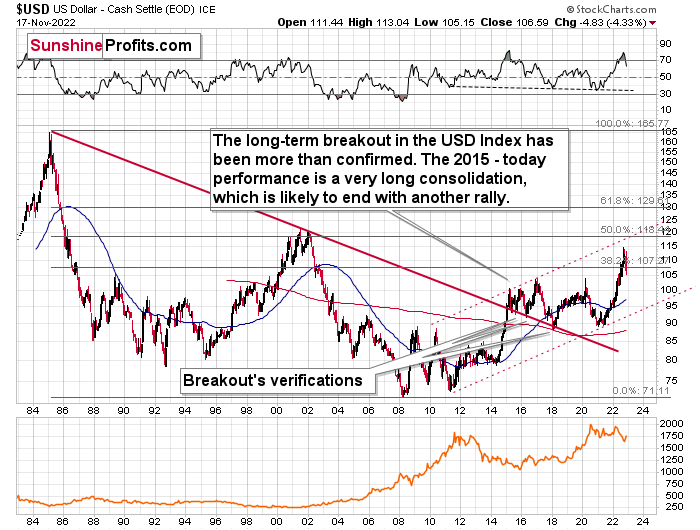

From the long-term point of view, the USD Index is currently rallying in approximately the mirror image of how it declined in 2002.

Approximately, because this time, the correction was bigger. No wonder – the preceding move was also bigger. Still, I think that the rally in the USD Index will continue as its relative (!) value to the euro and the yen is likely to grow.

Why did the USD Index decline so much recently? Technically, because no market moves in one direction without corrections – that’s just the way markets usually operate.

It seems that many (if not the vast majority) people out there are betting on the Fed’s dovish U-turn. Incorrectly so, because voters are most concerned with inflation, so that’s where the action is going to be, in my view.

It’s impossible to tell what data will cause the USD Index to move higher. Actually, no data is needed for that – the rally could continue on its own, due to technical reasons. The medium-term trend is clearly up, and we already saw a correction to the 38.2% Fibonacci retracement. This could be a good enough reason for many traders to buy heavily.

Practically whatever bullish data for the USD Index we get at this point could trigger a rally. Or it could be the case that we get bearish data for the USD Index, and it rallies anyway, because of the “sell the rumor, buy the fact” type of reaction.

That’s why focusing on technicals is more useful than trying to guess what kind of data is going to come up next, in my view.

Fundamentals dictate where the markets are headed in the long run. In the short run, they can serve as triggers (or inverse triggers due to the act-on-the-rumor-reverse-on-the-fact action), but they don’t have to. In the long run, interest rates can and likely will be raised more in the U.S. than in the EU and Japan due to their internal problems with debt If interest rates continue to rise, the bonds of various EU countries may become "problematic.” Remember the sovereign debt crisis that hit Greece in 2009? While the U.S. doesn’t really face the risk of states breaking apart (it’s not impossible, but it is unlikely), the EU already lost the UK. And those in charge of the EU would really not want that to happen. Sovereign debt crises could be a major problem in this case. Consequently, they will do a lot to avoid them.

Consequently, the rates are more likely to climb more in the U.S., and therefore the uptrend in the USD Index is likely to continue.

Based on this, it seems that one shouldn’t be surprised by a rather quick move from the current levels to about 120 – USD Index’s long-term highs. Of course, the implications for the precious metals market are profoundly bearish.

This doesn’t rule out quick corrections along the way – those don’t interrupt the big, weekly/monthly moves at all, and they don’t break the analogy. This includes the recent downswing – it didn’t invalidate the bullish medium-term uptrend.

This is extremely bearish for gold and the rest of the precious metals sector.

Before summarizing, do you remember the very, very long-term USD Index chart that I’ve been featuring for many months? The one below.

I emphasized that the USD Index was after a major breakout (in 2014/2015) that was then followed by a multi-year consolidation. The breakout was also verified in late 2017 / early 2018, when the USD Index moved back to the previously broken resistance line, and it verified it as support.

After that, it was only a matter of time before we saw a huge upswing. It certainly took a while, but the massive rally has indeed followed.

The reason why I’m mentioning this today is not to provide you with told-ya-so comments, but to emphasize that this big rally has legs. Strong legs.

On a day-to-day basis, it might seem unbelievable, temporary, random, or based on some sort of manipulation. But in reality, the writing has been on the wall for – literally – years! And those who have been following my analyses in the past were well-prepared – well in advance.

What does it tell us now? It tells us two things:

- The move to the 118 – 120 area is quite likely as there is little other strong resistance nearby.

- The top close to 118 – 120 might not be the final top for the USD Index. It could rally further (after a corrective decline from the above-mentioned area), but this might not necessarily mean that gold will decline in the following years (beyond the medium-term decline to $1,400 or so).

All in all, the outlook for the USD Index remains bullish, which has bearish implications for the medium term, but I don’t think it will prevent the precious metals market from rallying in the long run.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Letters to the Editor

Q: PR, what's your best guess as to when the stock market and miners will move substantially lower?

A: Now.

I think the move lower has already started. When will it accelerate? Perhaps after the long Thanksgiving weekend. This will be a great opportunity for everyone to calm down and re-evaluate what’s happening. What's happening is that real rates are rising, which is bad news for gold. That’s very bearish for gold, and rising rates are bearish for stocks as well.

Q: PR and the SP Team,

Thank you all for the great analysis. God bless you all on this Thanksgiving!. Do you expect global banking system crises? I understand London banking has broken trust with all the European millionaires, and Credit Suisse is in trouble, not to mention the dire U.S. banking situation. Would that lower your forecast for gold and the market? Oh yes, and Chinese banking and real estate looks like we are all in the same sad boat. Which will be the first domino to fall?

A: Thank you, and happy Thanksgiving to you and your loved ones!

I don’t expect a worldwide banking crisis anytime soon. My best bet is that the powers that be will be able to hold everything together. The situation is not as bad as it was in 2008 (yet) and they managed to keep the system afloat back then.

I was recently talking to a friend in the accounting/tax area, and she said that the regulations are being introduced and changed, and she gets the feeling that it’s all smoke and mirrors in order to make people really annoyed, so that when the powers that be introduce some kind of radical solution, it will be met with a feeling of relief and not protests.

I don’t have any proof for it, but quite a few things fit into the “let’s introduce government's cryptos.” However, we are not there yet. The stock market would have to plummet first to demonstrate that people are truly fed up with the current system and want a bigger change. In this case, wouldn’t it be convenient for the powers that be for stocks to slide?

Big inflation requires higher rates. Higher rates can cause bankruptcies, stock market collapses and other unpleasant consequences. This, in turn, could make people demand changes. Then, the government'scryptos could take over the current fiat-money-based system.

I’m not betting the farm on this scenario, but… It does seem quite realistic to me. I’ll keep you – my subscribers – informed.

Summary

Summing up, it seems that the biggest part of the 2013-like decline is taking place right now, and – while I can’t make any promises regarding performance - it seems likely to me that our big profits are about to become huge and then ridiculously big in the relatively near future.

As I have written before, the recent upswing didn’t change anything. While the mining stocks appeared “strong” recently, it seems to me that it’s just a reflection of the temporary (in my view) strength in the general stock market. And as stocks decline, mining stocks – and especially junior mining stocks – are likely to truly slide.

Things might happen very fast in the coming days, and if I plan to make any adjustments, I’ll keep you informed. Still, if the targets that I’m mentioning in the “Trading” part of the summary are reached, I think that profits should be taken off the table without an additional confirmation from me. I will probably get on the long side of the market at that time, but I’ll send a confirmation if I decide to do so.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Friday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief