The US elections are over and since the markets were not surprised by their outcome, there was no significant reaction. It seems that the markets can now return to their previous trends. But… the USD Index is down significantly today, while gold and silver are rallying. Does it mean that the trend in the precious metals is currently up?

Not necessarily. The US-elections-driven volatility could extend beyond the very initial reaction and it’s not surprising to see the move higher in the PMs and miners today and along with a move lower in the USDX. What is interesting, however, is the subtle clue that the relative changes provide.

Gold and silver are practically where they were 24 hours ago, while the USD Index is considerably lower.

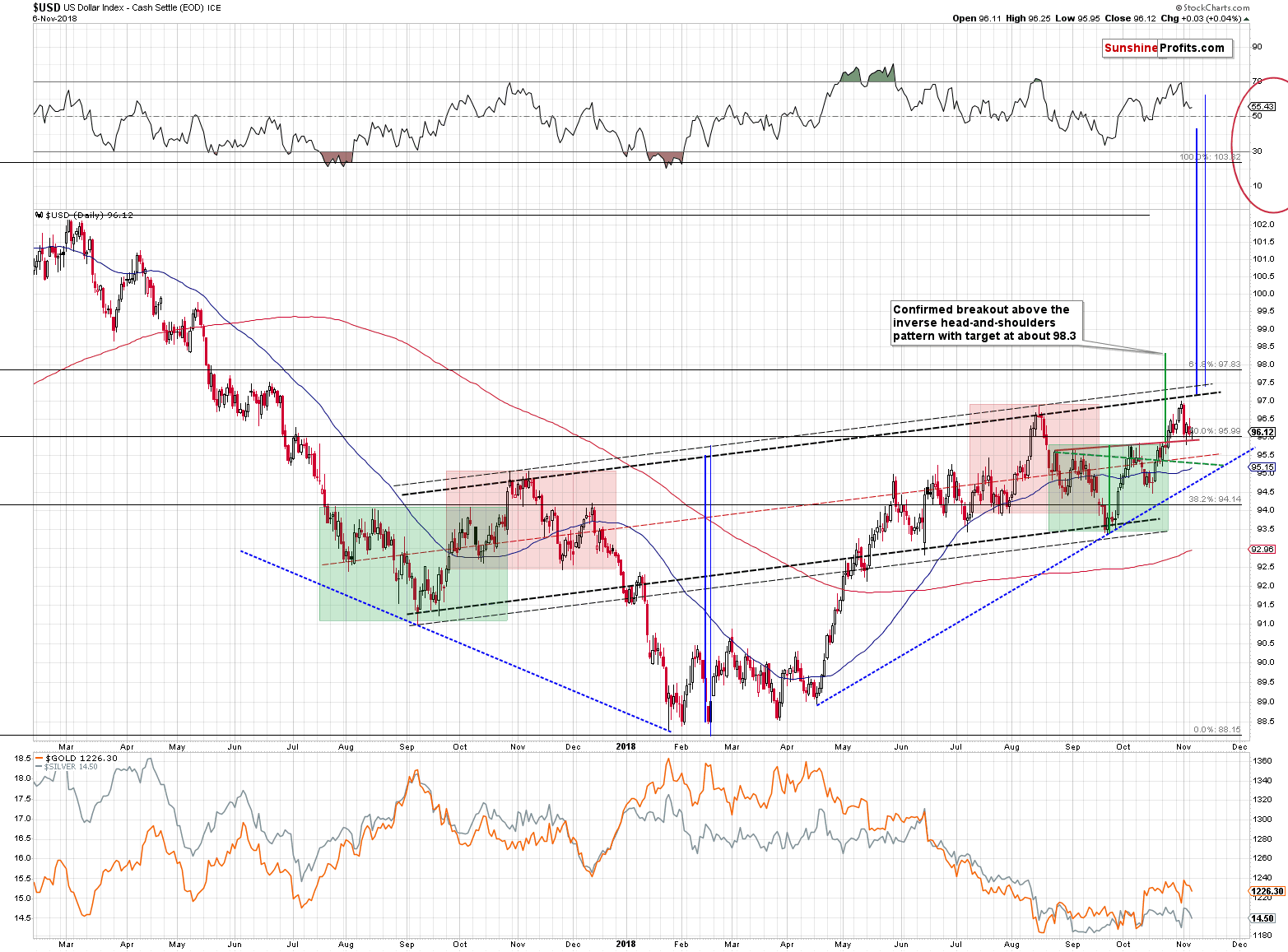

USD Index and Its Inverse H&S Pattern

Being about 0.50 lower today (at the moment of writing these words), the USD Index is already visibly below the previous November low. This is a clear sign of weakness of the precious metals sector. The PMs should be rallying, but they are not.

But doesn’t this move invalidate the recent inverse head-and-shoulders pattern?

In a way it does, and in a different – more important – way it doesn’t. The line that we’ve been featuring on the above chart and the one that’s being broken today (the rising red line) is based on the intraday highs. As you may recall, the closing prices are more important and thus the formations based on the closing prices of the USD Index can be viewed as more important as well. The neckline of the inverse head-and-shoulders pattern that’s based on the closing prices is currently at about 95.25. Today’s pre-market low (so far) is 95.68, so the USD Index didn’t invalidate the breakout above the inverse H&S pattern in terms of the closing prices. Consequently, even though we may see some short-term weakness in the USD Index (by the way, we cashed in our profits from USD-long forex positions yesterday, before today’s decline), the main trend remains up for the following weeks and months.

Moreover, please note that the reflective nature of the 2017 decline and 2018 upswing remains in place and back in 2017 the USDX moved a bit below the dashed, red line, relatively close to the dashed blue line. Even if the USD Index declines even to the neckline of the short-term inverse head-and-shoulders pattern (95.25), the above analogy will remain intact, and it will continue to favor higher prices in the following weeks and months. The outlook, therefore, remains bullish for the USDX and bearish for the precious metals market.

Since both: gold and silver are practically where they were when we published yesterday’s Gold Trading Alert, all the points that we made remain up-to-date, especially the one about the possible short-term volatility:

The implication is that this build-up in transactions that were not made but are planned may cause bigger volume today and in the rest of the week along with increased volatility. We saw something similar in late February 2018, when gold declined on very low volume. What followed was a quite sharp upswing that was invalidated before the end of the session. There are also bearish examples. For instance, in early August 2018, low volume readings were followed by a big decline.

There were also cases, when low volume was not followed by anything special, so the quality of the signal is not particularly high, but it’s important to keep the above in mind nonetheless. Why? So that any temporary price upswing doesn’t come as a surprise. Just like what we saw in February 2018, or like what we saw two years ago after Trump’s victory, the upswing would likely be very temporary. To be clear, even if we see a temporary upswing, we don’t expect it to be even close to the size of the upswing that followed Trump’s victory. The latter was a huge surprise to the markets and implications appeared very significant. We are unlikely to get a big surprise this time and the implications will not be as significant the previous ones.

The more important implication of the US elections is that they will be over soon. Sounds trivial, but it’s important that the tensions will subside. It’s likely one of the main factors that’s been preventing the precious metals market from declining.

While we’re discussing the situation in the USD Index, we would like to take this opportunity to reply to one of the questions that we recently received.

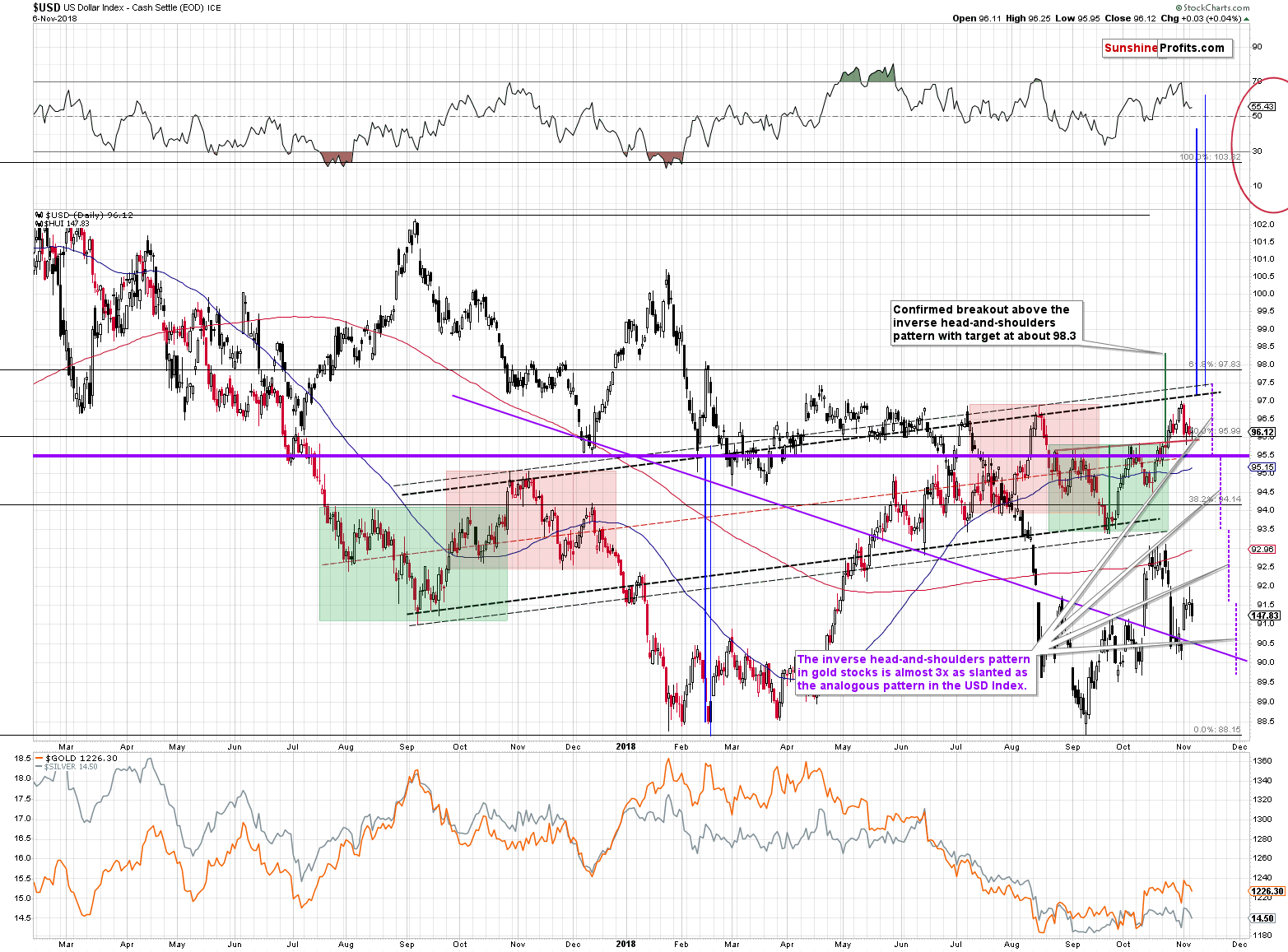

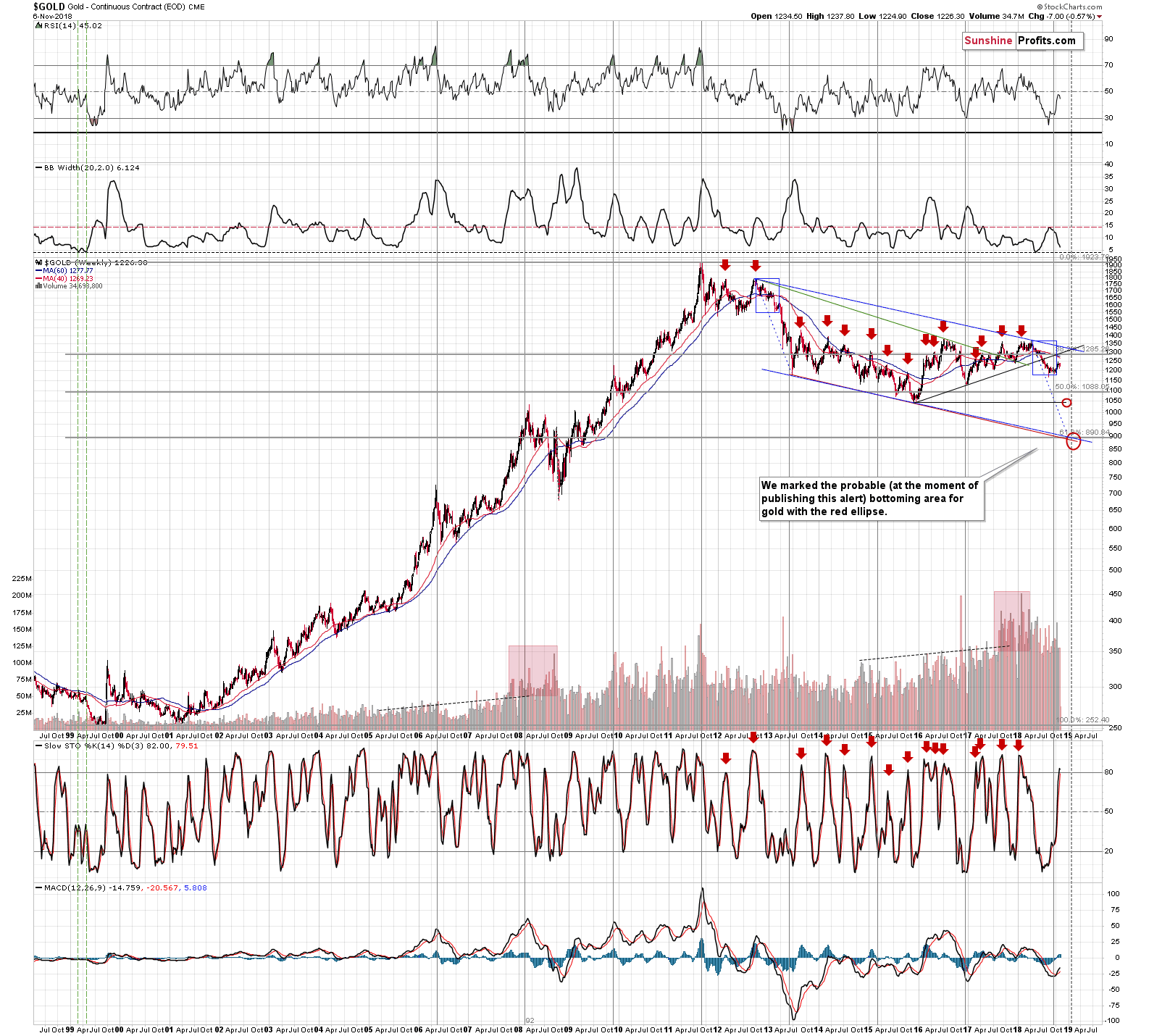

Inverse H&S in the USD Index - Too Slanted?

The question was if the medium-term inverse head-and-shoulders pattern that’s still being formed is not too slanted to be reliable. In short, it’s not even close to being too slanted. Naturally, if one features it on a chart that suppresses the time axis then it will be very slanted, but that’s not the point. In normal scale, the upward slope of the neckline of the pattern is reasonable and doesn’t appear to invalidate anything.

There are a multiple definitions of the H&S patterns, but it’s hard to find a definition that would penalize the formation for not having shoulder extremes at identical height. Most likely all of them point to any implications of the formation only after it’s completed, though.

There is an interesting note on Stockcharts’ definition:

Neckline: The neckline forms by connecting low points 1 and 2. Low point 1 marks the end of the left shoulder and the beginning of the head. Low point 2 marks the end of the head and the beginning of the right shoulder. Depending on the relationship between the two low points, the neckline can slope up, slope down or be horizontal. The slope of the neckline will affect the pattern's degree of bearishness—a downward slope is more bearish than an upward slope. Sometimes more than one low point can be used to form the neckline.

The above is about the regular H&S pattern as the website doesn’t have a specific definition for the inverse H&S, but it’s safe to assume that in case of the inverse pattern, the fragment that we put in bold would be:

The slope of the neckline will affect the pattern's degree of bullishness—an upward slope is more bullish than a downward slope.

One might ask if there is a point after which the pattern becomes too slanted, and this might be the case, but it would be at much more extreme examples than the one that we currently see in the USDX.

Interestingly, this doubt becomes ridiculous if it accompanied by one’s conviction of the meaningful nature of the recent inverse H&S in the gold stocks.

The above chart features the HUI Index (proxy for gold stocks that’s particularly useful – for instance because it’s not being impacted by ETF fees like the GDX ETF is) in the background; it’s marked with black candlesticks.

The time scale is identical, so the slant of both inverse H&S patterns is comparable. The neck level of the USDX pattern is marked with rising blacked dashed lines. We’ll use the thin dashed black line as it’s based on the intraday prices. The purple declining line the neckline (and its extensions) of the pattern in gold stocks.

At the first sight it’s clear that the neckline of the inverse H&S in the gold miners is more slanted than the one in the USD Index, but to be sure, we created the horizontal thick purple line and we put it at the necklines’ intersection. We then marked the distance between it and both lines with identical purple dashed vertical lines. This comparison allows us to see that the slant of the neckline of the inverse H&S pattern in gold stocks is more than twice the slant of the neckline of the inverse H&S pattern in the USD Index.

Consequently, if one wants to say that one of these patterns could be invalid because of its slant, it would be the pattern in mining stocks, not the one in the USD Index.

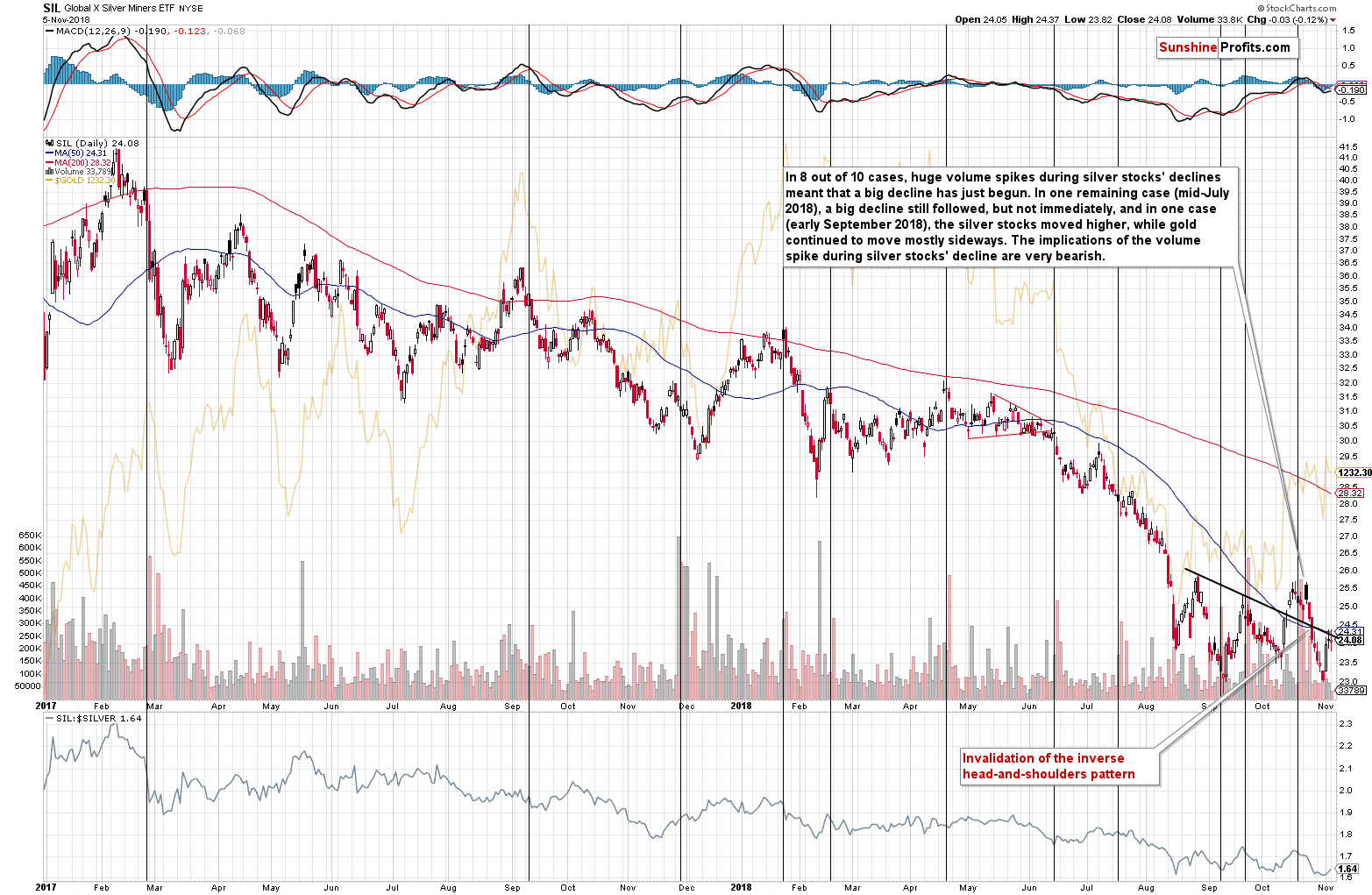

Speaking of the inverse H&S pattern in the mining stocks – did you know that this pattern doesn’t even exist anymore in case of half of the sector? The above “half” assumes a simplification that there are only gold miners and silver miners. Obviously, there are companies that mine other precious metals, but the most popular PMs are gold and silver, so this assumption is quite close to being correct from trader’s point of view.

Silver Miners and the (Lack of) Inverse H&S Pattern

The silver miners declined after the huge-volume-spike signal just like we expected them to, but the key thing that we would like to emphasize is their position relative to the previous inverse head-and-shoulders pattern. It was invalidated in case of both: gold stocks and silver stocks. But, while the HUI Index is once again above the neck level of the pattern, the silver miners are not. This means that even though there are some points of view, in which the formation appears to remain intact (the GDX ETF), it really shouldn’t be trusted. There is no formation to speak of in case of silver stocks anymore, and the HUI Index has already invalidated the formation, so even though the price is once again above the neck level, it doesn’t make the picture truly bullish even for the short term.

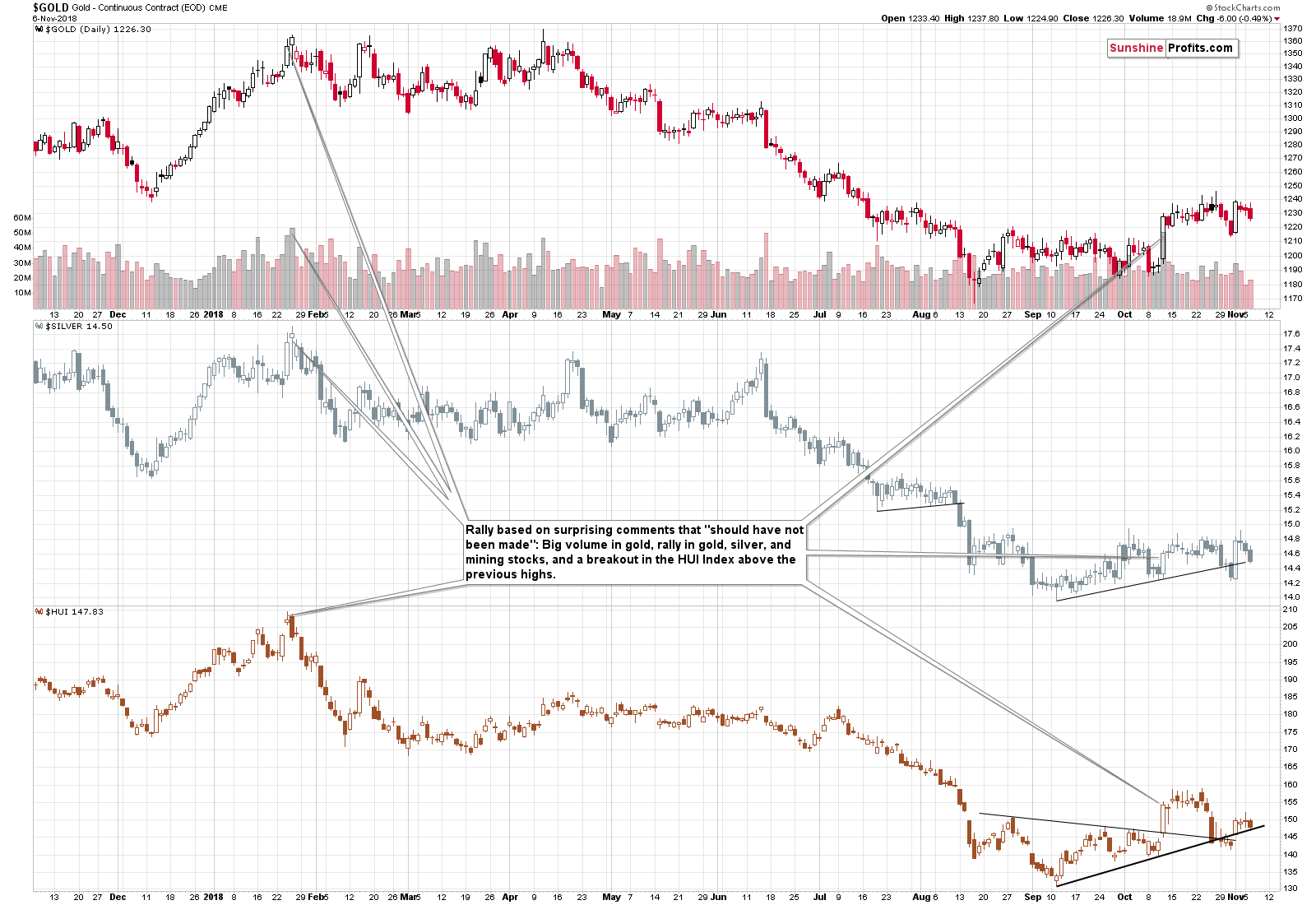

There are three more questions that we’ll address in today’s free gold analysis. One of them is about the volume that accompanied the mid-October rally in gold. The question was if the size of the volume confirmed the bullish implications of that session and if we shouldn’t view the outlook as bullish because of that.

The Comment-based Analogy and Its Implications for USDX and Gold

Our reply is that, if possible, it’s always useful to look at the context of what happened and to take it into account while discussing implications. It’s not always the case that we see what was the likely reason behind a given rally, but it was the case in mid-October. That was right after Trump publicly criticized the Fed for raising interest rates.

On October 15th, we wrote the following:

Besides, if yesterday’s action was indeed caused by Trump’s comments (which may not really represent his true opinion on the matter), we have a guideline from the past on how temporary the effect might be. In January 2018 Treasury Secretary Steven Mnuchin said that the U.S. would welcome a weaker dollar, which was something that anyone in his position should have never said, so that surprised the market. The USD Index declined and gold soared based on these comments. The next day, January 25th, 2018, gold formed its 2018 top in terms of the closing prices. In other words, in terms of the closing prices, higher gold prices were never seen since that time. The volume in gold was huge at that time. In fact, that was the only time from the recent past when gold’s volume was comparable to what we saw yesterday.

There are even more similarities. Gold stocks rallied above the previous highs just like they did yesterday. It all looked very bullish at the first sight and it generated a lot of feedback and questions. We received numerous questions recently as well, so the situation is similar also from this point of view.

The emotions were high in late January 2018 and they are high now. But, it’s our job to stick to the facts and logic and analyze the emotionality instead of being influenced by it. In the January 25th, 2018 regular Gold & Silver Trading Alert we wrote about 50% of the regular short position in gold, silver, and mining stocks, and in the intraday follow-up we increased this position to 150%. It was indeed an excellent time to enter, not exit a short position. And the same appears to be the case today. Surely, we may have temporarily (in the next several hours or so) higher prices, but the odds are that this is a shorting opportunity in disguise.

The January 2018, comments by Steven Mnuchin were followed by USDX’s bottom and the same was the case in October – the USD Index started another rally shortly after Trump’s “crazy comments”. The history repeated itself as we had indicated, and we saw a confirmation of the analogy between these two cases.

What about the precious metals? Their performance is also quite similar to what happened in January and the following months. The key fact is that the rally was mostly over after the comments-based upswing. To be 100% clear: gold, silver and mining stocks did move above the closing price of the huge-volume session, but this move was not significant (and the same thing happened in January).

What happened next? In the first half of this year, we saw back and forth movement in gold and a more decisive (but nothing epic) decline in silver and mining stocks. What happened recently? Gold just closed more or less where it had closed on October 11th – the day of the huge-volume rally. At the same time silver and mining stocks closed visibly below their respective October 11th closing prices. The history is being repeated.

Consequently, huge gold volume (and the huge volume in the GLD ETF) in mid-October is not a bullish factor. It’s a confirmation of the analogy to the late-January 2018 situation where the price moves were triggered by comments from the US officials that shocked the markets.

This analogy has bearish implications for the following weeks. In the short-term, however, it means that the upside is very limited. This analogy doesn’t say anything about the starting date of the next big breakdown in gold, but based on other factors – for instance based on the situation in the USD Index and on today’s strength of gold’s and silver’s reaction to the weakness of the former – it seems that we will not have to wait much longer.

CoT Report and Its Declining Usefulness

There was also a question about the current position in the CoT report, but we have already discussed the usefulness of the CFTC’s CoT numbers. We commented on the CoT usefulness (and limitations) in late July, 2018. As many analysts reported, the numbers were very favorable and they were about to make gold shine again. Instead, gold declined in the following weeks. Of course, silver was supposed to soar to the moon based on its own CoT situation. It was over $15.50 back then. GDX was above $21.50. Higher silver and mining stock prices were not seen since that time. To be precise, there was a small upswing in silver on the day that followed our July 25th, 2018 analysis, but in terms of the closing prices, the July 25th 2018 session was not exceeded.

In short, the gold CoT report was very useful tool about 15 years ago and its usefulness declined since that time. Moreover, it’s highly unlikely to indicate a major breakout, major breakdown or provide insights regarding the final bottoming targets and one of the reasons for it is because the commercials’ and non-commercials’ positions don’t have one set minimum or maximum at which the price reverses.

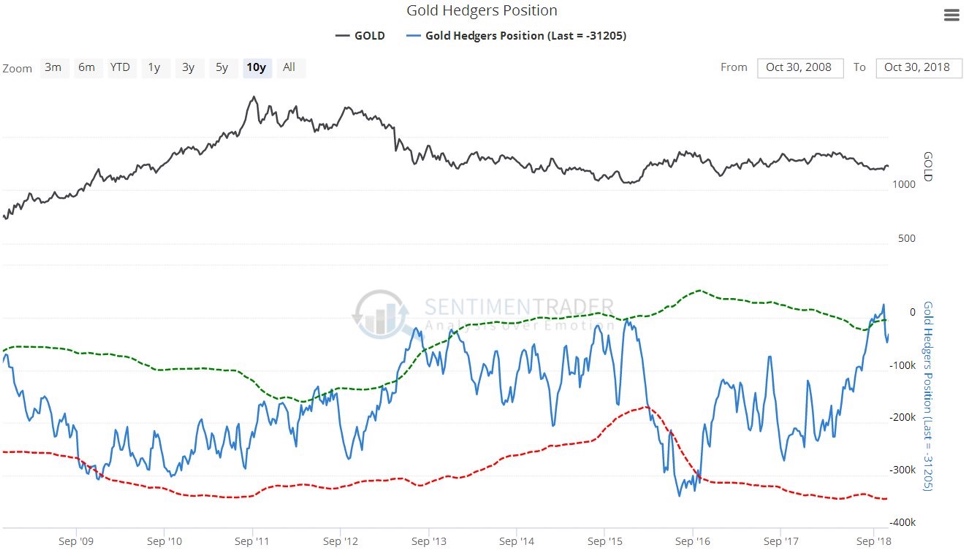

Some may say that it’s different with gold hedgers positions (in fact, the final question that we received was about these positions). But it’s not.

Please take a look at the chart below.

The above chart covers about 2 years. In the upper part of the chart you have the price of gold, and in the lower part you see the gold hedgers position. As you can see tops in the blue line correspond to bottoms in gold. Moreover, the blue line is just after a move to the previous highs and its resistance line (marked with green). Gold is also close to the previous bottoms. So, the bottom is in, right?

Let’s zoom out.

The previous chart showed you what appeared likely right before the April 2013 slide. The price of gold plunged, and the hedgers positions simply increased, well above the previous highs and above the green resistance line.

What’s the current situation? The blue line is just after a move to the previous highs and its resistance line (marked with green). Gold is also close to the previous bottoms. How can the implications be bullish, if the very similar situation from the past preceded the biggest slide of the decade?

Some may say that the position can’t increase further and thus gold can’t decline further.

But why should this be the case?

The volume level in gold futures (and in other futures contracts in general) increased substantially in the recent years. Consequently, the numbers in the CoT reports can be substantial and their swings can also be bigger than in the previous years. This further validates the point that we made earlier when discussing the declining usefulness of the CoT reports. If you look at the volume levels before 2006, they are quite stable. But, since 2007, their levels increased substantially, and we saw another big increase in 2017.

The change in the data regime is very important and every analyst should make sure that the tools that they are using remain useful in light of the change. The usefulness of the CoT-based gold signals declines and it’s very far from being the Holy Grail of signals that it’s portrayed to be.

Summary

Summing up, the outlook remains strongly bearish for the precious metals sector. Gold’s very weak reaction to today’s pre-market decline in the USD suggests that we will likely not have to wait much longer before the decline in the precious metals sector resumes, especially that the US-elections-driven tensions are likely to subside shortly.

To be clear, gold is still likely to rally to $6,000 or so, but not before declining significantly first.

On a side note, before calling us perma-bears, please note that we were bullish (in terms of long-term investments) on precious metals for years – until April 2013. We’re looking for the true bottom in the precious metals sector, not because we’re its or gold investors’ enemy. Conversely, we’re that true friend that tells you if something’s not right, even if it may be unpleasant to hear.

Naturally, the above is up-to-date at the moment of publishing it and the situation may – and is likely to – change in the future. If you’d like to receive follow-ups to the above analysis (including the intraday ones, when things get hot), we invite you subscribe to our Gold & Silver Trading Alerts today.

Thank you.

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager

Sunshine Profits - Effective Investments through Diligence and Care

Gold & Silver Trading Alerts

Forex Trading Alerts

Oil Investment Updates

Oil Trading Alerts