In our regular gold trading alerts, we focus on the short- and medium-term outlook and we rarely discuss the very long-term issues or price targets. The reason is simple – the long-term issues and price targets don’t change often, so usually there’s little new to say about them. Consequently, it’s been a long time since we last discussed our view on gold’s explosive upside potential. In fact, it’s been so long that those who do not take the time to read our analyses thoroughly and those who have been reading them for only a short while may think that we are bearish on gold in the long run. Or that we’re perma-bears. Naturally, it’s nonsense and those who have been diligently following our articles know it. What we’re aiming for is to help investors position themselves to make the most of the upcoming rally in the precious metals market and one of the best ways to do it is to help people prepare for the final bottom in gold.

Of course, buying close to the bottom is pointless unless a big rally is going to follow. In today’s analysis we want to tell you how big this rally is likely to be. Well, you have already read it in the title of this article, but the key question is if the above is just a simple round number that we “wish” gold to reach, or if it is based on reasonable arguments. We don’t want you to take our word for it – we’ll show you how we arrived at $6,000 as the minimum target for gold.

But first, we would like to discuss a few reasons that could help to push gold well above the previous highs.

Dollargeddon

The medium-term outlook for gold is very bearish based on multiple technical developments and we discussed it thoroughly on Monday. Even based on some of the fundamental factors, one can expect a decline or a continuation in the sideways trend. Why? Well, there is acceleration in global economic growth combined with still subdued inflation. Hence, U.S. real interest rates (especially short yields) should rise. Another reason is that the U.S. economy (and the overall economy) is less fragile than the euro area, so there are more downside risks related to the euro than to the greenback.

However, gold prices are likely to go up in the coming years, as there are many potential triggers which are likely to support the yellow metal’s performance in the long run. We’ll briefly discuss the most important factors below:

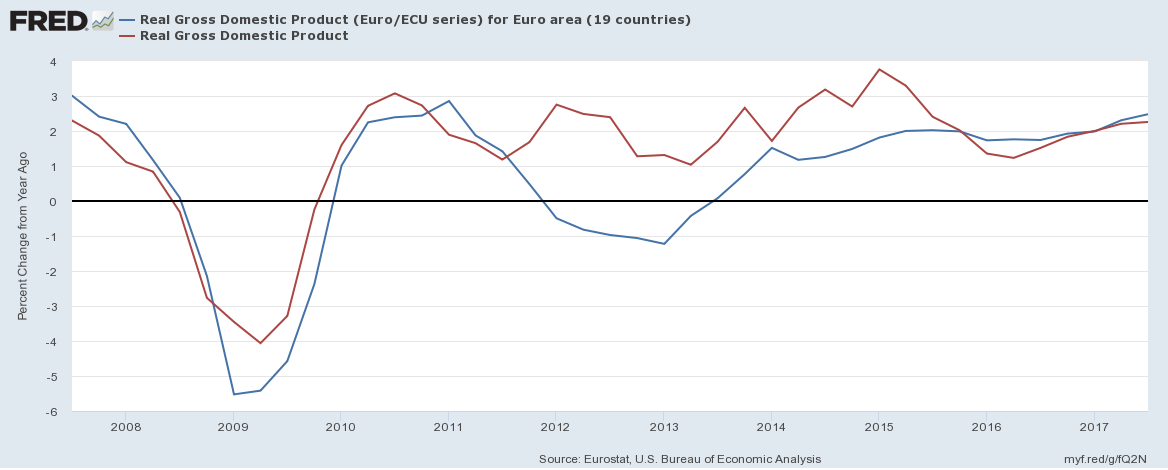

- Synchronized global growth and the narrowing divergence between the U.S. economy (the key economy using the U.S. dollar) and other major economies, particularly the euro area (see the chart below). Hence, in the long run (!), we expect downward pressure on the greenback from the euro. In other words, the U.S. is in a later stage of the business cycle than the euro area – hence, the latter may now relatively improve its position or even outperform the former economy. If this happens, we will see the appreciation of the euro against the U.S. dollar, which should be bullish for gold.

Again, we are not discussing the medium-term outlook here, which remains very bullish for the USD. We mean the very long term and the outlook in terms of years (not necessarily this and the next year, though).

- Low real interest rates – the major central banks may find themselves behind the curve. In other words, inflation is quite likely to surprise the central bankers. An unexpected rise in prices would lower real interest rates, which would support gold prices. The yellow metal is considered by many investors an inflation hedge and it shines in the periods of low real interest rates.

- The current U.S. economic expansion and the bull market in U.S. equities are both very long. At some point in the future the next stock market crash or recession will occur. Importantly, the next crisis is likely to hit with low interest rates and big central bank balance sheets in place. Hence, the potential for supporting the economy will be somewhat limited. Investors will worry about the impotence of the central banks, which will increase the safe-haven demand for gold.

- Similarly, the next crisis will hit when room for more expansionary fiscal policy is limited. Public debts are huge in many countries. In particular, there is a possibility that the U.S. tax reform combined with some infrastructure spending will boost the U.S. fiscal deficit, deteriorating the fiscal position of the country. In such case, gold should shine.

- The huge size of the derivatives market. Warren Buffett called it a time bomb and when/if it explodes (more precisely: implodes), gold would get a huge boost. You can think about gold as an insurance against tail risks. The major slowdown in the Chinese economy is an example of a black swan which could shake the global economy and increase the safe-haven demand for gold.

Having discussed why gold is likely to move much higher in the coming years, let’s check how high it might actually go. Naturally, it’s impossible to make a detailed prediction based on the fundamental trends alone, so in order to do it, we’ll apply other techniques that are based on the analogies to what already happened in the past. After all, history tends to repeat itself to a considerable degree as the driving forces (fear and greed) behind price moves don’t change.

Few Words on Methodology

We’re going to show you two ways of obtaining the long-term target for gold and they will have one thing in common – we won’t rely on classic fundamental measures such as supply and demand. We don’t want to get into the details here, but to make a long story short, gold behaves more like a currency than a commodity and its flows are more important for the price than yearly supply and demand figures. Moreover, classic fundamental analysis can only tell you what the true value of a given asset (here: gold) should be, but that’s not really what we’re interested in. Markets tend to become very overbought at the tops, so the above estimation would likely significantly understate the real target for gold’s long-term top.

Consequently, instead of applying the classic, yet most likely imprecise techniques, we’ll use those that are likely to provide more reliable targets, even if they might seem controversial.

Gold’s Analogy to the Previous Bull Market

The first method is to check how the current rally compares to the one seen three decades ago. After all, long-term bull markets go from undervalued to overvalued and since history tends to repeat itself, then a look at the previous bull market should tell us how high gold should move this time as well. Gold has been traded globally during both bull markets and since human psychology doesn’t change much (investors are as greedy and as fearful as they were decades ago), we can expect the entire size of the bull market to be repeated.

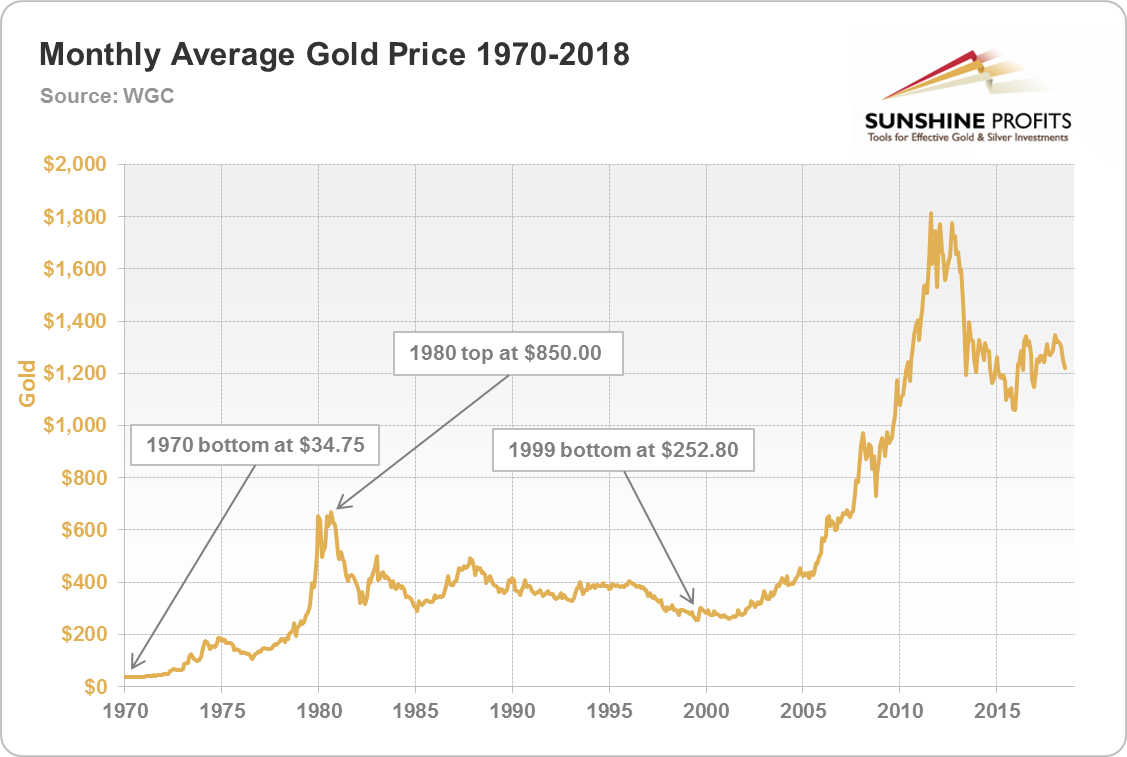

The question is – in what terms. Definitely not in nominal terms because both bull markets started from different price levels ($34.75 vs. $252.80) and thus a similar price move allows for much greater appreciation of capital as the entry price would have been several times lower. Moreover, the value of the dollar is a big issue when comparing prices from different decades. To make it more difficult, we can’t simply adjust the prices for inflation, because the way inflation is measured has not been consistent over time. One way to avoid the above problem is to use alternative inflation data, but we’ll do something more straightforward.

We’ll use relative valuations. How many times did gold multiply its price during the previous bull market? That’s the exact question that defines how much money was to be made in dollar terms. Inflation was soaring, but something similar could be the case in the final months of the current gold bull market as well. Consequently, not only is that not a problem – relative valuation accounts for this specific aspect.

So, how many times did the price of gold increase during the previous bull market? Gold rallied from $34.75 to about $850, which means that its price increased 24.46 times. Gold’s bottom in the case of the current bull market was $252.80. Multiplying the latter by the former gives us $6,184 as the future price prediction for gold. This may seem too simple, but it really does take quite a few things into account.

Some may say that the above analogy is incorrect, because under the gold standard gold’s price was kept artificially low and thus the comparison to the initial price will give us a rally that’s too big. In other words, the assumption here would be that if gold’s price hadn’t been fixed, it would not have got as low as it did and thus, gold wouldn’t have multiplied as many times.

Certainly, this could have been the case, but… There’s one small detail that confirms that we can indeed use the mentioned technique. The detail is that once gold’s price was allowed to float it didn’t soar immediately. Conversely, the move higher was rather normal, just like prices of undervalued assets increase in value during regular bull markets.

If gold had soared from $35 to $100 or so overnight, then we could view $100 as the first real price of gold and start the analogy from that price. But, nothing like that happened. There was a gradual price increase during which gold also corrected and declined. Yes, the fact that gold wasn’t allowed to trade freely under the gold standard was a significant bullish factor for the entire 70s bull market, but other bull markets have other underlying fundamentals that can be just as bullish. Just because the gold standard ended only once doesn’t mean that the 70s bull market was very different from the other ones. We’ll comment on that in greater detail in the following part of this essay.

Gold Compared to the General Stock Market

Comparing gold to the general stock market is very useful as both asset classes are often viewed as alternatives. Both are impacted by inflation, so their ratio should not be affected by the latter. Moreover, the ratio already proved to be useful on an approximate basis – the last major top and major bottom were somewhat in tune with the previous extremes. Consequently, this tool should be very useful in estimating how high gold can rally before THE top is in.

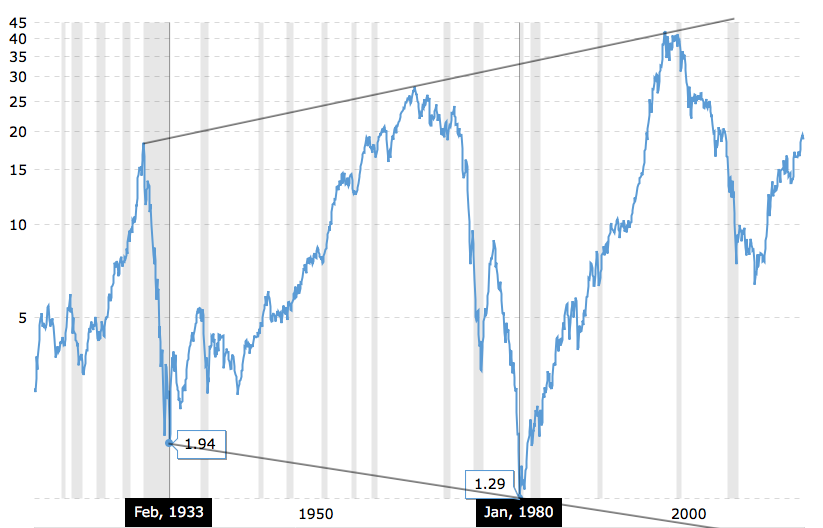

Let’s take a look at the Dow to gold ratio charts below.

The price of gold is in the denominator of the Dow to gold ratio, so in order to predict the top in gold, we’re going to predict the bottom in the ratio.

The ratio is a great long-term tool, because it clearly shows what asset class dominates the market and in what part of the bull or bear market gold and stocks currently are. The major top in the ratio was seen about 20 years ago and it has declined to much lower levels since that time. Right now, we are witnessing a corrective upswing that those who are short- or medium-term oriented view as a big rally. Indeed, even from the medium-term point of view, the rally is sizable, but we should keep in mind that something very similar took place in the mid-70s and it was only a corrective upswing, not the beginning of a new decade-long rally. This time, the rally in the ratio is bigger than it was in the 70s, but please note that the entire history of the chart is characterized by an increase in volatility in both directions, so a bigger corrective upswing this time is not something odd. Conversely, it seems to be in tune with the above tendency.

So, given the increased volatility in both directions, it seems that the corrections should be characterized by bigger volatility than the previous ones as well. The upswing in the ratio that started in 2011 is bigger than one that we saw in the mid-70s, but this seems rather natural in light of the overall increase in the volatility. Since the extent to which the current upswing is bigger than the mid-70s correction is rather natural, it doesn’t seem that the move higher is anything more than just a correction. Therefore, as far as big, long-term moves are concerned, it seems that the ratio is still not done declining. In consequence, gold is most likely not done rallying, even though it’s been moving lower for about 7 years now.

But how low can the ratio go? There are several ways in which we can determine the likely target and they are all based on the fact that history tends to repeat itself. The question is in what way it will repeat.

The ratio could simply move to one of the previous bottoms. The previous bottoms are at 1.94 and 1.29. Both could serve as the key support and the same goes for any level between them. The average is 1.615. Overall, we can assume that the ratio is likely to move below 2 before the final bottom in it and the final top in gold are seen.

Now, since the moves in both directions are getting wider, it seems much too conservative to assume that the ratio will move only to the upper of the above targets – the 1.94 level. Actually, even 1.29 is reasonably conservative as it only assumes a move to the previous extreme, not below it, which seems likely if the widening continues.

What seems most likely, however, is that the widening of extremes will continue. In this case, we can expect gold to move to the declining very long-term support line, just as it rallied all the way to the rising very long-term resistance line almost 20 years ago. Consequently, the question becomes when will the ratio cross the line and at what level. While this is not our official prediction, for the sake of this article, let’s assume that gold will top in 5 years. The line is not visible on the above chart, but knowing the price and date of the previous extremes we can calculate the correct amount. In March 2018 it’s 0.93, and in March 2023, it will be at 0.89. All in all, it’s approximately at 0.9.

The above is very important from the psychological point of view. With the ratio at 1, gold’s price will be equal to the value of the Dow Jones Industrial Average and everyone and their brother will notice that. No financial journalist will allow this fact to remain unnoticed. There will be theories about a new paradigm in which all that’s not from or about precious metals is trash and any other asset class is useless. This should trigger very emotional buying of gold by the general public, which would likely result in the final parabolic blow-off in gold prices. Then, 10% - 11% above the value of the Dow Jones Industrial Average, gold could form its multi-year top.

Will the ratio really decline as low? It’s impossible to know for sure, but it’s seems very likely that we’ll see the Dow to gold ratio below 2 in the coming years and values below 1 could really be seen.

OK, with established targets for the ratio, the question becomes where the Dow will be during gold’s top.

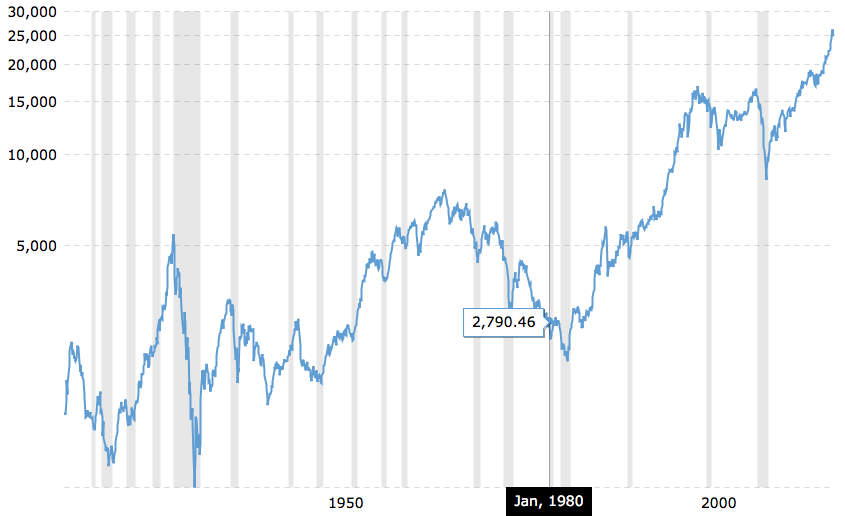

At the moment of writing these words, Dow is very close to the $25,000 mark. Given the above estimates for the Dow to gold ratio, this implies gold topping at least at $12,500 and possibly above $25,000 – even at $27,500 or so.

These levels could be achieved, but it doesn’t seem all that likely. In the past, the general stock market declined along with the ratio. In the case of the 1930s, it’s obvious as the price of gold was fixed – the ratio’s movement was based solely on the stock market’s slide.

So, how low will the stock market decline? To be clear – the Dow doesn’t have to decline, but based on the above long-term cycles in the Dow to gold ratio, it’s likely to. The big Dow decline that preceded the 1980 bottom in the ratio was smaller than the one that preceded the 1933 bottom, so if this trend continues the upcoming corrective downswing could be lower as well. The above assumption seems to have some fundamental backing, as the tendency now is to throw money at the declining stock market and hope for the best (remember Bernanke in 2008?). With money being pumped into the stock market during the next big downswing, the size of the decline may indeed be limited and, for the same reason, the final topping price for gold could be higher.

Still, if history is to repeat itself to at least some extent, the Dow should decline, and the decline should not be minor. About 50 years ago, the Dow topped at about 7,500 and started a decline that ended in June 1982 below 2,100. The top in gold and the bottom in the Dow to gold ratio, however, formed earlier, with the Dow at about 2,800. This means that the price of the Dow was cut by over 62% (by the way, that’s remarkably close to the classic Fibonacci retracement of 61.8%, isn’t it?). The decline of the 1930s cut Dow by more than 85%, so it was even more extreme. But can we really expect Dow to decline by as much in light of the money-printing policy? Not necessarily, but since the 80s decline was 23% smaller than the one from the 30s, then maybe we’ll see a similar decrease also this time. In this case, we would be looking at a decline of about 39%. This is remarkably close to another classic Fibonacci retracement – 38.2%, so maybe there’s something to this very rough approximation.

At the moment of writing these words, we can’t know if a long-term top in the Dow is already in, but let’s assume that it is. If not, then it would imply a higher target for the final low and thus a bigger gold price target for the final top.

Cutting 38.2% from 25,000 leaves us with 15,450. If the decline is even bigger huge (but still smaller than the one from the 80s), we might see a 50% decline from the top. That would give us 12,500 as the target.

The methodology used above is more of an educated guess than a detailed multi-factor-based estimation, but since we’re using it to estimate ballpark figures (in order to confirm or invalidate more precise targets based on other techniques), it seems useful.

So, the lowest target for gold that we can obtain based on the above is a decline to 12,500 in the Dow along with a move to only 2 in the Dow to gold ratio. This means that gold is likely to rally at least to $6,250. We have already discussed the optimistic (for gold) target – 25,000 in the Dow (perhaps a correction to the current levels after a rally to 30,000 instead of a bigger decline?) accompanied by a Dow to gold ratio below 1 implies gold north of $25,000.

A more moderate target that’s based on the averages of the predictions is based on 15,450 in the Dow along with 1.29 as the target for the Dow to gold ratio. The above implies gold at about $12,000.

That’s also relatively close to $12,500, which is a geometric average of the two remaining targets based on the extreme predictions ($6,250 and $25,000). We’re using the geometric average instead of the arithmetic one as that’s more useful when multiplications are involved in the calculations and that’s the case here.

Summing up, the overall target price range for gold based on the Dow to gold ratio analysis is $6,250 - $25,000, and the most probable target for gold is $12,000. Of course, it will not be seen overnight and most likely we won’t see gold at those levels by next week either. The above prices are something that might be reached in the next several (4-7) years, but we don’t want to get into the details regarding timing in this essay as don’t want to turn it into a book. We’ll get back to this issue in future analyses.

Gold Price and Beer

Yes, you read that right.

Beer is a tangible asset and its value over time should be quite stable (unless you open it and put it in sunlight). The demand for beer should not change a lot over time and demand for it is rather stable as well – at least in the regions of the world where beer is the preferred alcoholic beverage. Consequently, it might be useful to compare the price of gold to the price of beer in a similar way to how we just compared the value of gold to the Dow.

Assuming that history repeats itself, we’ll be able to check how high gold rallied in terms of beer and thus know what to expect during the current bull market as history tends to repeat itself. That’s yet another way of eliminating the changes in the way inflation is measured over time.

Before moving further with this topic, please note that this is not really a separate way of projecting gold’s topping price, but a supplement to the previous section that should either confirm or invalidate it. Having said the above, let’s take a closer look at the data.

Naturally, there are different kinds of beer, different brands and so on, so we’ll have to use a standard measure.

Ever heard of Oktoberfest?

The Munich beer festival allows us to standardize the type of beer that we’ll use in the calculations and makes the gold-beer ratio comparable over time.

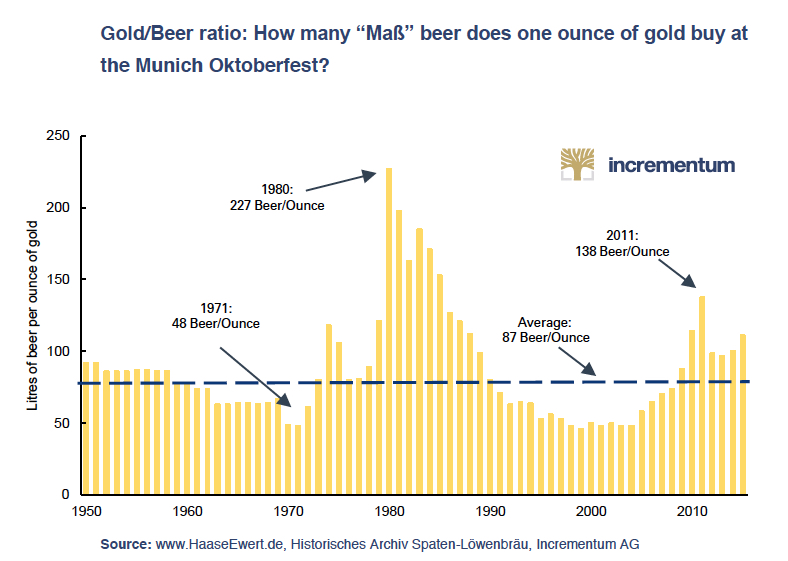

The above chart shows exactly that. The first thing that catches the eye is the fact that the 2011 top in gold is nowhere close the 1980 high. So, if gold is to only match the previous top, it will need to move considerably higher – about 1.64 higher than during the 2011 top. This gives us an estimate of about $3,165.

The second thing is that both bull markets started from approximately the same price level, which suggests that the ratio is indeed meaningful. Once gold reached its minimum reasonable value in real terms (here: in terms of beer), it stopped declining.

But, there’s something else that the above chart shows – the average at which the ratio was trading. Just like most markets and most ratios move from oversold to overbought, the gold to beer ratio moved from being below the average to being above it. The thing is that before the 70s bull market in gold started, the ratio was oversold for about 10 years, but before the current bull market started, the ratio was oversold for about 14 years.

Generally, the longer it takes for the base of a given move to form, the bigger the move is. In this case, the longer time below the average suggests a bigger and longer upswing above it. So far it seems to be working. The 2000 - 2011 rally in the ratio is about 30% bigger than the 1970 -1976 upswing.

If the rest of the rally is also proportional, then we can expect gold to more than double, as the final top in the ratio in the 1980 was more than twice the rally that we saw between 1970 and 1976. In fact, the initial rally was then repeated with the factor of 1.5. Let’s not get into the details of predicting beer prices and assume that the latter are not changing much nowadays (after all, the reported inflation numbers are indeed very low). This allows us to use the analogy in the case of the price of gold in regular USD terms.

The 1999 bottom was at about $253 and gold topped at about $1,924, so the size of the rally was $1,671. Multiplying it by 1.5 and adding it to the 2011 top of $1,924 provides us with the target of $4,430.50. Adding back some of the inflation that the above does not take into account and that is likely to be seen before gold tops, let’s round it to $5,000.

Is the above a precise target for gold? Not even close. But it does a good job at showing that we can arrive at an estimate close to the one that was based on the previous methodology. Therefore, rather than being a prediction technique on its own, the above serves as a confirmation of the previous $6,184 target, by providing a counter-balance to the $12,000 target based on the Dow to gold ratio.

But This Time It’s Different!

The first thought of many investors after looking at the above relative valuation of gold in terms of the U.S. stock market and after seeing the comparison between the size of the previous bull market and the current one is that they both don’t apply, because the fundamental situation in the 70s was different than the current one. After all, gold might have rallied because of the previous breakdown of the gold standard and due to stagflation. Plus, the oil shock and extremely hawkish Volcker also played a very important role and both seem to be one-time events.

Indeed, the situation is different, but this by itself is no reason to dismiss the analogy. Was the fundamental situation in silver alike in 1980 and in 2011? It was completely different. There was no change in the monetary regime, no rampant stagflation, the price of oil was well below its 2008 high and many investors don’t even remember who Paul Volcker is and how high rates can be increased.

Yet, silver topped at almost an identical price level. How was that possible? Some may say that it was accidental but… Come on – silver could have topped at $44, $45, or $39, or $61 or any other nearby price level, and yet it topped almost exactly as it did about 30 years earlier. That doesn’t look like a coincidence.

The Dow to gold ratio itself shows that the values can be repeated with approximate, yet uncanny precision despite differences in the economic environment. The winter of 1933 and the winter of 1980 might have both been similarly cold, but that’s when the direct similarity ends. In 1933 there was no oil shock, no change in the monetary system and instead of putting pressure on the stock market, Paul Volcker might have put pressure on his parents to get more sweets as he was only 5 years old at that time.

The economic surrounding was different and yet the ratio between Dow and gold bottomed between 1 and 2 in both cases. Interestingly, the tops in the ratio also follow a very specific pattern, each being proportionately higher than the previous one, even though it’s obvious that the times when they were formed were very different.

So, maybe it’s something else that investors should be focusing on instead of making sure that the situation repeats itself to the letter. After all, history doesn’t repeat, but it rhymes. The key question is – what’s the rhyme.

The rhyme – the common denominator of both cases is the investors’ willingness to buy a given asset. Whether this demand is triggered by a major technical breakout, by a change in the monetary system, or by a stock market crash is of secondary meaning. Consequently, just because we’re not assuming that the situation from the 70s and 80s will repeat itself doesn’t mean that the analogy in the size of the long-term rally or the prediction for the Dow to gold ratio is pointless. This is especially the case since we are not trying to get the final binding price here – we want to get a good ballpark estimate of what’s to come so that we know how to put the upcoming developments into proper perspective.

For instance, by knowing that gold can rally to about $6,000 or so, we won’t be inclined to view the entire bull market as over when gold forms a temporary top at $2,500 or so.

But, can we really expect something big to happen that is a direct trigger for a big and sharp rally in the gold prices?

Enter Nikolai Kondratiev

As we explained in our March Market Overview, something significant could and in fact is quite likely to happen in the next several years once we are in the Kondratiev cycle’s summer stage.

Wait. What summer? It’s still cold where I live.

Let’s start with the general concept that we already discussed in the mentioned report. The idea of “super-cycles” was developed in 1925 by Russian economist Nikolai Kondratiev who identified three phases of the cycles and believed that their key drivers were social shifts (changes in inequality, opportunity). However, the theory has been refined over the years and it is currently divided into four “seasons”:

- Spring: economic upswing, technological innovation which drives productivity, low inflation, bull market in stocks, low level of confidence (winter’s legacy);

- Summer: economic slowdowns combined with high inflation and bear market in stocks, this phase often ends in conflicts;

- Autumn: the plateau phase characterized by speculative fever, economic growth fueled by debt, disinflation and high level of confidence;

- Winter: a phase when the excess capacity is reduced by deflation and economic depression, debt is repaid or repudiated. There is stock market crash and high unemployment, social conflicts arise.

The above theory was modified by other economists. In particular, Joseph Schumpeter significantly modified the original concept, linking the cycles to innovations. Their accumulation leads to technological revolutions, which transforms societies and launches Kondratiev waves.

There have been five such revolutions in the modern capitalist economies:

- The Industrial Revolution (started about 1771)

- The Age of Steam and Railways (1829)

- The Age of Steel and Heavy Engineering (1875)

- The Age of Oil, Electricity, the Automobile and Mass Production (1908)

- The Age of Information and Telecommunications (1971)

We currently live in the fifth age, but the sixth technological revolution is coming. Brace yourself for The Age of Cybernetics, High Technology and Clean Energy. Just think about all these technology breakthroughs: nanotechnology, biotechnology, renewable energy, machine learning, artificial intelligence, 3D printing, Internet of Things, robotics, electrical and autonomous vehicles, etc.

What does it all imply for the gold market? Well, before we answer this question, let’s relate the debt cycles to the Kondratiev waves. In the autumn phase, there is speculative fever, as economic growth is fueled by debt and anticipation of ever increasing asset prices. We believe that that phase occurred and was ended by the Great Recession. Then, winter came: the stock market crashed and the unemployment rate soared. And – importantly – there was asset price deflation and debt deleveraging (deflation would have been larger if the central banks hadn’t introduced ZIRP and quantitative easing). Interest rates were ultra low, but didn’t boost the credit expansion, as deleveraging dominated. Households didn’t want to take on new debt, since they had to pay back their previous loans.

It implies that we are enjoying the spring right now. There is an economic upswing, inflation is low and interest rates are more or less stable (or used to be stable until recently). Stocks are in a bullish trend, but confidence remains low. However, we can be at the transition point towards summer, as the next technological revolution is approaching. Higher inflation also looms on the horizon. Interest rates are rising as well.

The final stages of the Kondratiev cycles are often accompanied by severe conflicts, often military ones, as technological revolutions associated witch each cycle lead to social changes, creating turmoil.

The diffusion of technology takes time – and it occurs with pain along the way. Technological innovations lead to social changes, which can create conflicts or even wars (the new technology empowers certain people who threaten the old elite). Some analysts argue that the third cycle actually peaked with World War I and ended with World War II. As Kondratiev wrote:

It is during the period of the rise of the long waves, that is during the period of high tension in the expansion of economic forces, that, as a rule, the most disastrous and extensive wars and revolutions occur.

The implications are clear. The new technological revolution will bring prosperity, but it will be born in pain. And what is the best cure for pain? You are right, shiny gold, which hedges against economic turmoil.

Summing up, even if we can’t be 100% certain what the trigger that pushes gold into a speculative parabolic upswing will be, it’s something that should factor into our analyses. Moreover, if there is likely to be a reason for the price of gold to soar, then relative valuations are likely to be helpful in estimating the ballpark figures regarding the possible target for the big rally.

Summary

Summing up, the price of gold is like to soar very high in the upcoming years and the likely target range for the final top in gold is $5,000 - $12,000. If we had to pick one specific price out of that range that’s most likely to stop gold’s parabolic upswing, it would be the $6,184 level, which implies that gold’s price would be multiplied by the same amount as it was during the bull market that we saw about 40 years ago.

Consequently, the gold market is definitely worth paying attention to, even if the medium-term outlook is not yet bullish. In fact, it’s exactly what makes it worth the extra effort. Declining prices along with a very bullish long-term outlook mean that there will be an ultimate bottom that will serve as a tremendous buying opportunity. The time that we have left until THE bottom is all that we have left to prepare for it. If you’re interested, we have prepared a series of articles in which we help investors prepare for the upcoming buying opportunity. You can access it and start preparing for gold’s epic buying opportunity using this link.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief, Gold & Silver Fund Manager

Gold & Silver Trading Alerts

Forex Trading Alerts

Oil Investment Updates

Oil Trading Alerts