Briefly: in our opinion, full (250% of the regular size of the position) speculative short position in gold, silver, and mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

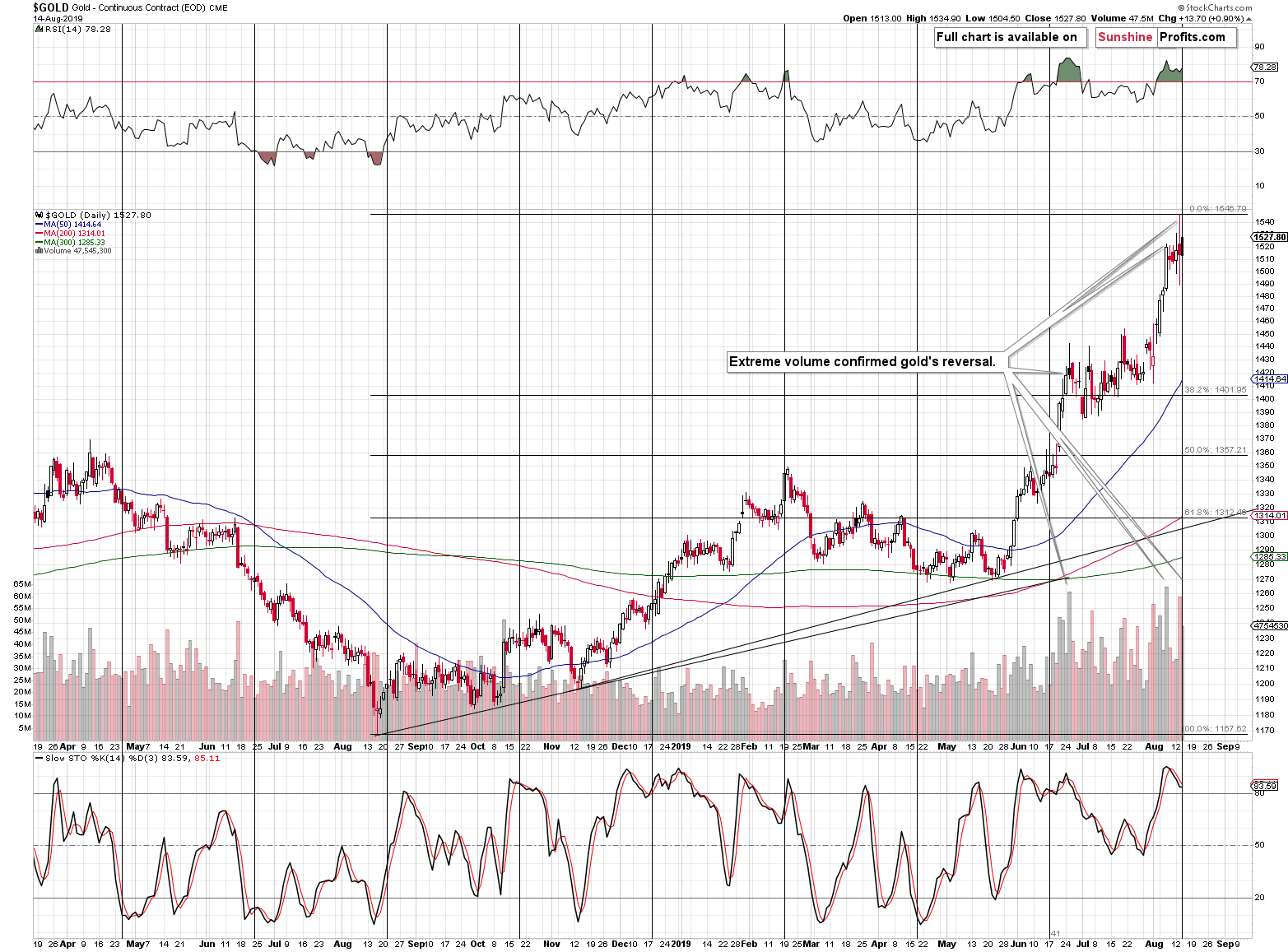

Gold bulls appear to be shaking off Tuesday's steep plunge. In today's gold Alert, we'll look under the hood of yesterday's upswing. This ties well with the detailed analysis we've brought you yesterday - we'll look at several key gold ratio. Such 360-degrees view will reveal what has changed with this gold rally, and what has not. Get ready for some illuminating parallels!

In yesterday's Alert we reviewed gold, silver, gold stocks, and silver stocks form the long-term point of view. The take-away was that it was actually only gold that showed strength from the long-term point of view. Silver stocks are on the other end of the performance spectrum, with their inability to move significantly higher - they barely corrected 25% of the decline from their 2016 high. Gold miners and silver miners are not that extremely weak, but still very weak overall. Instead of moving above their 2016 highs, they corrected only about half of the preceding decline. That's very weak compared to what gold did. All in all, the precious metals market overall didn't move visibly higher from the long-term point of view - only gold did.

In today's analysis we would like to expand yesterday's analysis by supplementing it with detailed analysis of the gold to silver ratio, and the gold stocks to gold ratio.

Let's start with the former.

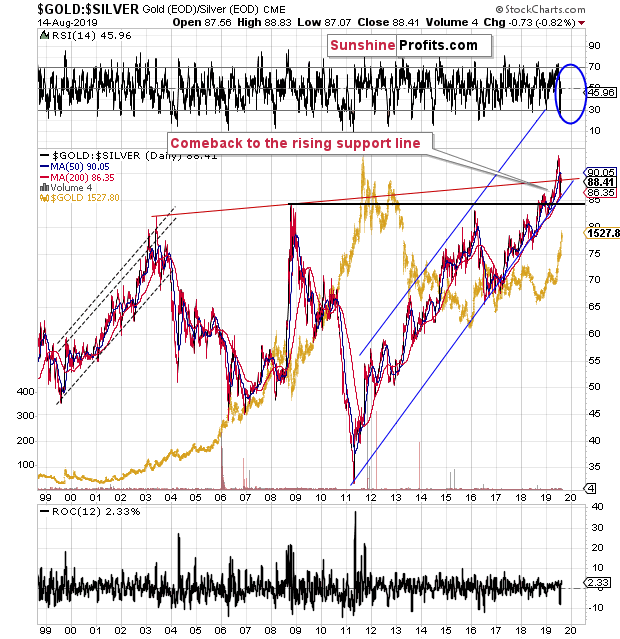

The Key Precious Metals Ratios

Earlier this year, the gold to silver ratio significantly broke above the previous highs and then it corrected this move. The important thing about the most recent downswing is that it didn't take the ratio back below the rising long-term support line and therefore that the uptrend remains intact. Even at first sight, the most recent downswing simply looks like a correction within a bigger uptrend.

This is significant, because the biggest moves in the precious metals sector tend to happen in the opposite direction to the ratio. Looking at the 2008 and 2011 performance provides confirmation. Of course, this doesn't have to be the case each and every time, but it's likely to be.

Since the uptrend in the ratio remains intact, so does by extension the downtrend in the precious metals market, gold's recent gains notwithstanding.

Please note that the mid-2012 rally in gold was accompanied by a correction in the gold to silver ratio that's relatively similar to the current one. It didn't change the major trend, it was just a correction. Back in 2012, most investors were convinced that another big rally in gold was starting, while it was really the final chance to get out of gold before it crashed. The same appears likely to be the case this time.

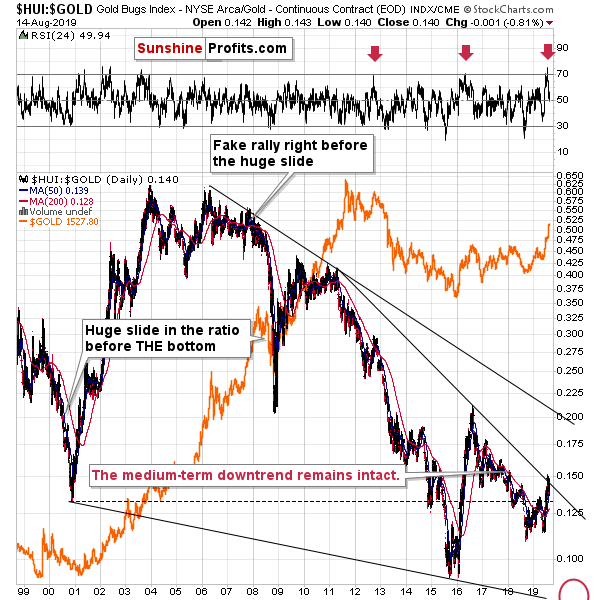

That's what we can say about the gold to silver ratio; and what about the one between gold miners and gold?

They both have to be related as gold miners' profits depend on gold and the stock prices depend on profits to a large extent. The way this relationship changes over time can tell us a lot about the precious metals sector.

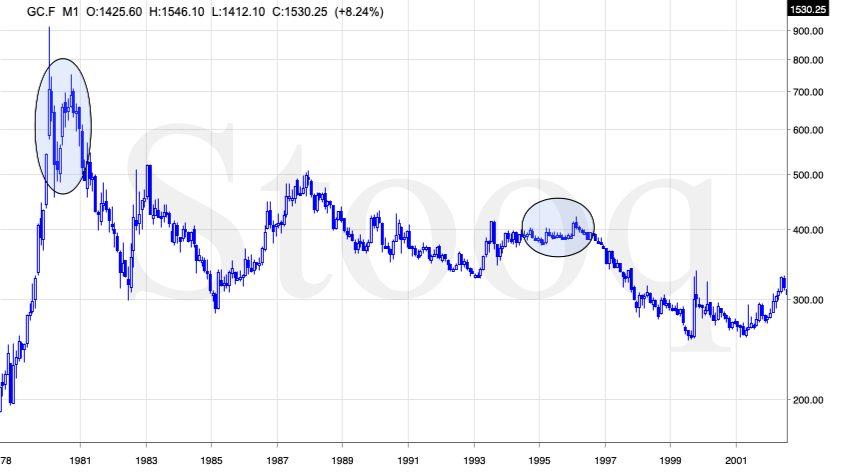

In case of the long-term relationship, gold stocks have shown one specific characteristic - they soar and outperform gold in the early parts of the major rallies. This was the case in 2008 and - most importantly - this was the case in 2000. The above chart is another way to look at the performance of HUI Index (proxy for gold stocks) and gold that we described yesterday:

In fact, gold miners are barely above their 2008 low from the long-term point of view.

And that's how the new bull market is supposed to start? With weak gold mining stocks despite sharply higher gold prices? Something's not right here, is it? Please take a look at what happened between 2000 and mid-2002. The HUI Index soared from below 35.31 to above 154.99. Its value increased over 4 times! And how much did mining stocks gain from their 2018 bottom? Less than 70%.

(note: in yesterday's Alert, we made a typo - the bottom that we compared to the 2000 bottom is 2018, not 2008 - we corrected this in this quote and in yesterday's Alert as well)

Why are we comparing these two periods? Because gold moved about 30% higher from its 2018 bottom and more or less the same characterized the 2000 - mid-2002 rally. To be precise, back then gold rallied only a bit above 25%, so miners' past rally is even more profound on a relative basis.

Gold mining stocks are simply not showing the long-term strength that they should if this was the beginning of a new bull market in the precious metals sector.

The above chart shows the 2000 - 2002 performance as a sharp rally in the ratio. Keeping it in mind, please look at what happened since the 2018 bottom. The move is tiny. That's why we think this move higher is just a correction, not the start of a new powerful upswing in the entire precious metals sector.

Moreover, do you remember what else happened between late-2000 and early-2002, when gold was just starting its massive bull market?

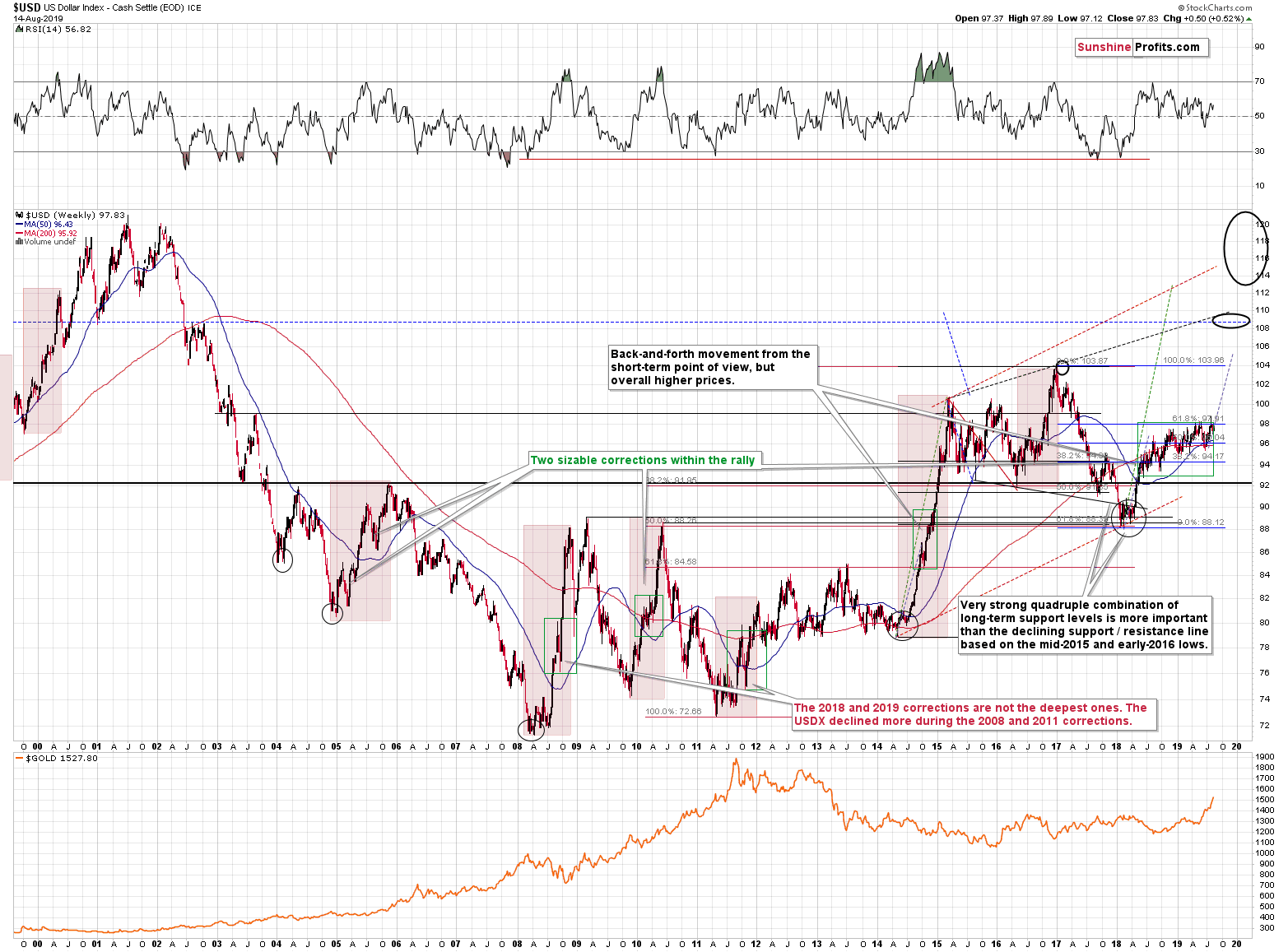

The USD Index was topping at about 120.

And do you know what the USD Index is doing right now?

The USD Index: Crawling Higher

It's holding up extremely well despite Trump's calls for lower USD values, the major shift in Fed's policy (moving from rate hike policy to rate cut policy). The only thing that the above combination of strong bearish factors was able to do, was to prolong USD's consolidation. Consolidation, during which the currency moves higher on average anyway. Running corrections like that are typical of the strongest of the bull markets.

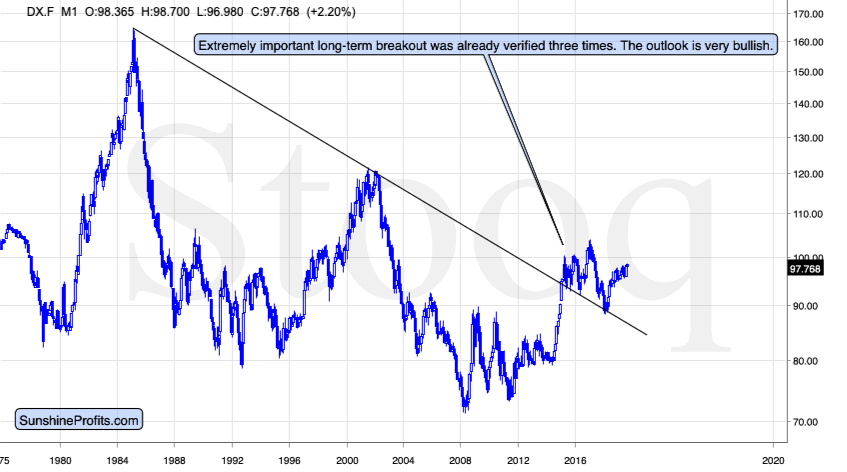

Even though the above chart appears to be very long-term, it's not long-term enough and it misses the most important technical development of the previous years.

The 2014-2015 rally caused the USD Index to break above the declining very-long-term resistance line, which was verified as support three times. This is a textbook example of a breakout and we can't stress enough how important it is.

The most notable verification was the final one that we saw in 2018. Since the 2018 bottom, the USD Index is moving higher and the consolidation that it's been in for about a year now is just a pause after the very initial part of the likely massive rally that's coming.

If even the Fed and the U.S. President can't make the USD Index decline for long, just imagine how powerful the bulls really are here. The rally is likely to be huge and the short-term (here: several-month long) consolidation may already be over.

There are two cases on the above chart when the USD Index was just starting its massive rallies: in the early 1980s and in 1995. What happened in gold at that time?

These were the starting points of gold's most important declines of the past decades. The second example is much more in tune with the current situation as that's when gold was after years of prolonged consolidation. The early 1980s better compare to what happened after the 2011 top.

Please note that just as what we see right now, gold initially showed some strength - in February 1996 - by rallying a bit above the previous highs. The USD Index bottomed in April 1995, so there was almost a yearly delay in gold's reaction. But in the end, the USD - gold relationship worked as expected anyway.

The USD's most recent long-term bottom formed in February 2018 and gold seems to have topped right now. This time, it's a bit more than a year of delay, but it's unreasonable to expect just one situation to be repeated to the letter given different economic and geopolitical environments. The situations are not likely to be identical, but they are likely to be similar - and they are.

What happened after the February 1995 top? Gold declined and kept on declining until reaching the final bottom. Only after this bottom was reached, a new powerful bull market started.

But gold just rallied so significantly in the last several months!

... And that's most likely what people were saying in early 1995, while they were buying at the top.

It's easy to get carried away by momentum and emotions that it generates. We're here for you to analyze the market as objectively and with as much cold logic as possible. And the key points in gold's supposedly bullish story simply don't add up. Not yet.

Before summarizing, let's take a look at the short-term price moves.

Short-Term PMs Check

Gold moved and closed the day higher, but there was no new intraday high. This can be explained by the cyclical turning point, which is exactly today. In a way, gold seems to have topped on Tuesday, when it invalidated the small breakout above the 2011 and 2012 lows and when it temporarily moved above the April 2013 price gap. But, looked at the same situation from the perspective of closing prices, gold topped yesterday - just as the cyclical turning point would suggest.

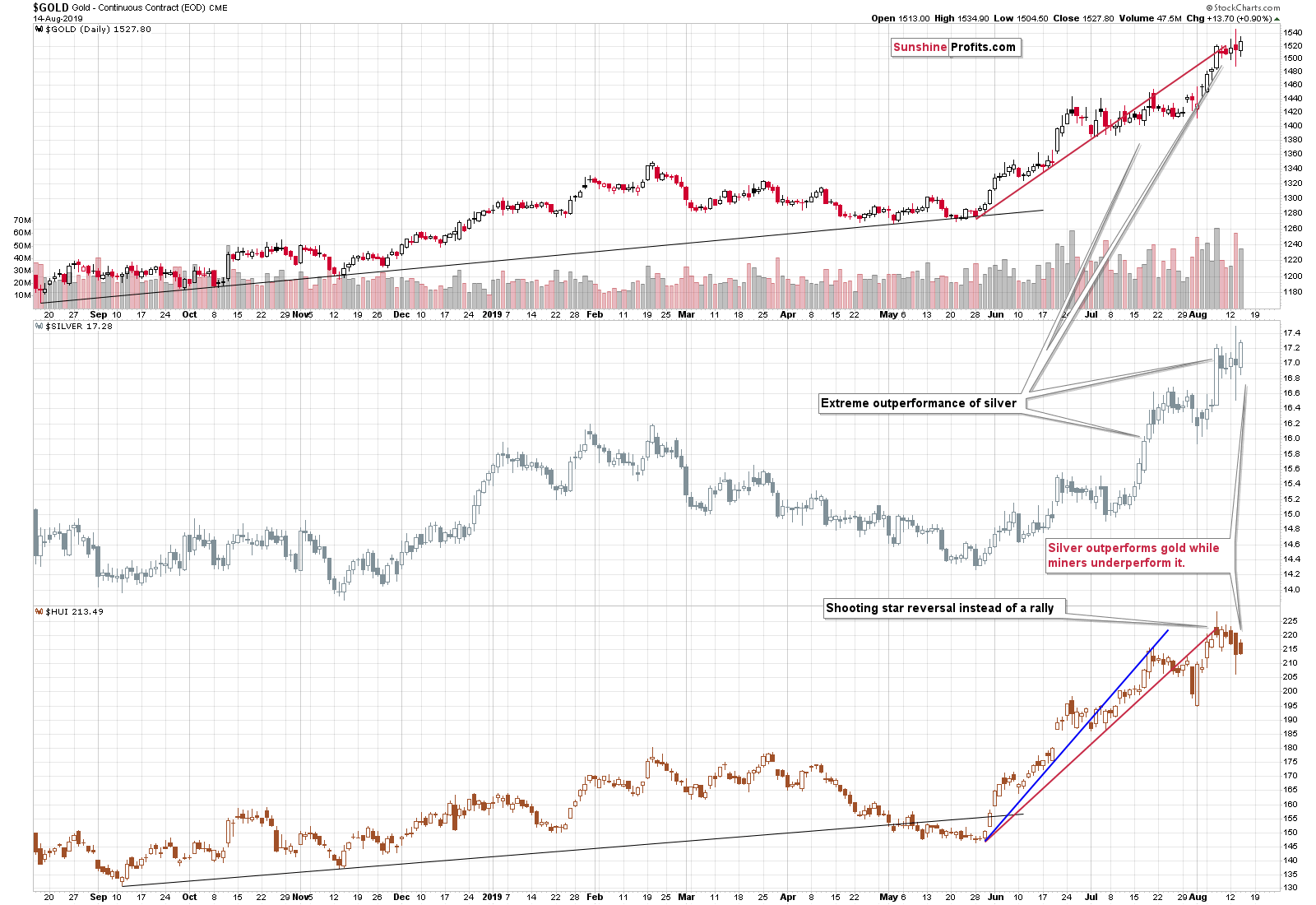

What is most remarkable about yesterday's performance is what silver and mining stocks did.

They both repeated their already-screaming signs that we saw in the previous days. Silver outperformed on a very short-term basis, and gold stocks underperformed.

The fact that we saw so many days when silver outperformed, while gold miners underperformed means that the implications of these signals are even stronger. They appear to be pointing to something much bigger than just a short-term decline. This is in perfect tune with what we wrote earlier today, and in the previous days. The decline that's likely on the horizon is not a small or even medium-sized one. It's likely to be huge.

Summary

Summing up, taking the big investment picture into account, out of the following: gold, silver, gold stocks, silver stocks, the recent upswing was only visible in case of gold. Most of the precious metals portfolio: silver, gold miners, and silver miners suggest that what we saw in the last several months is nothing more than a corrective upswing within a bigger downtrend. The analysis of gold to silver and gold stocks to gold ratios confirms the very bearish outlook for the medium term. The situation in the USD Index is very bullish for the following months and this suggests that gold's recent action was likely a fake upswing, similar to the 1995-1996 one. Mining stocks' recent weakness and silver's strong performance in the very short term both suggest that one should be prepared for much lower, not higher precious metals prices.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short position (250% of the full position) in gold, silver, and mining stocks is justified from the risk/reward perspective with the following stop-loss orders and exit profit-take price levels:

- Gold: profit-take exit price: $1,241; stop-loss: $1,552; initial target price for the DGLD ETN: $51.87; stop-loss for the DGLD ETN $25.37

- Silver: profit-take exit price: $13.81; stop-loss: $17.73; initial target price for the DSLV ETN: $39.08; stop-loss for the DSLV ETN $18.27

- Mining stocks (price levels for the GDX ETF): profit-take exit price: $17.61; stop-loss: $33.37; initial target price for the DUST ETF: $32.28; stop-loss for the DUST ETF $5.78

In case one wants to bet on junior mining stocks' prices (we do not suggest doing so - we think senior mining stocks are more predictable in the case of short-term trades - if one wants to do it anyway, we provide the details), here are the stop-loss details and target prices:

- GDXJ ETF: profit-take exit price: $23.71; stop-loss: $48.42

- JDST ETF: profit-take exit price: $73.32 stop-loss: $9.67

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that the in the trading section we describe the situation for the day that the alert is posted. In other words, it we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices, so that you can decide whether keeping a position on a given day is something that is in tune with your approach (some moves are too small for medium-term traders and some might appear too big for day-traders).

Plus, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one, it's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (DGLD for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn't, then we will view both positions (in gold and DGLD) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

=====

Latest Free Trading Alerts:

The yield curve inversion just got more pronounced. Not only the spread between 10-year and 3-month Treasuries, now also the spread between 10-year and 2-year turned negative. That sends a warning signal about the state of the real economy. About a recession on the horizon. Some might argue that the yield curve's predictive power has diminished with all the unorthodox monetary policies since the Great Recession. Yet, it's a valid reason to worry - how does gold welcome this message?

Is Widening Yield Curve Inversion Lifting Gold Prices Up?

=====

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager