Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update. Our most recently featured medium-term outlook remains the same as the price moves align with our expectations (or at least are not really against them). On that account, there are parts of the previous analysis that didn’t change at all in the earlier days and are written in italics.

The key thing that happened this week is that markets (stocks, USD Index, gold, and miners) appear to have finally realized that there will be no dovish U-turn, and the corrective upswing has most likely ended. The next big moves (lower in case of the precious metals sector) are likely underway.

Let’s start today’s analysis with a recap of what recently happened on the fundamental front.

The Weekly Fundamental Roundup

While the week began with hopes of a Santa Clause rally, pessimism reigned on Dec. 15 as risk assets plunged. Likewise, with false narratives coming home to bear, the FOMC’s reality check on Dec. 14 highlighted the fundamental challenges that lie ahead.

Furthermore, while we’ve warned throughout 2022 that a dovish pivot was laughable alongside unanchored inflation, the crowd bought hope and sold reality. However, with those hopes fading, the sentiment driving the PMs’ recent bear market rallies should evaporate in 2023.

Could Pozsar’s Prediction Double the Gold Price?

With risk assets retreating on Dec. 15, the gold price suffered mightily amid the bearish liquidation; and with the FOMC’s hawkish hammer shaking the financial markets once again, we warned on Apr. 6 that investors were ignoring the ominous signs at their own peril. We wrote:

Please remember that the Fed needs to slow the U.S. economy to calm inflation, and rising asset prices are mutually exclusive to this goal. Therefore, officials should keep hammering the financial markets until investors finally get the message.

Moreover, with the Fed in inflation-fighting mode and reformed doves warning that the U.S. economy “could teeter” as the drama unfolds, the reality is that there is no easy solution to the Fed’s problem. To calm inflation, it has to kill demand. As that occurs, investors should suffer a severe crisis of confidence.

Thus, while sentiment shifted dramatically on Dec. 15, the fundamentals have been clear for many months. In addition, with nine of the last 10 bouts of rising inflation ending with recessions since 1948, the notion of a soft landing contrasted the calamities that have unfolded throughout history. As a result, while it may take more than a day’s weakness to kill the bulls’ spirit, the PMs’ medium-term outlooks remain highly bearish.

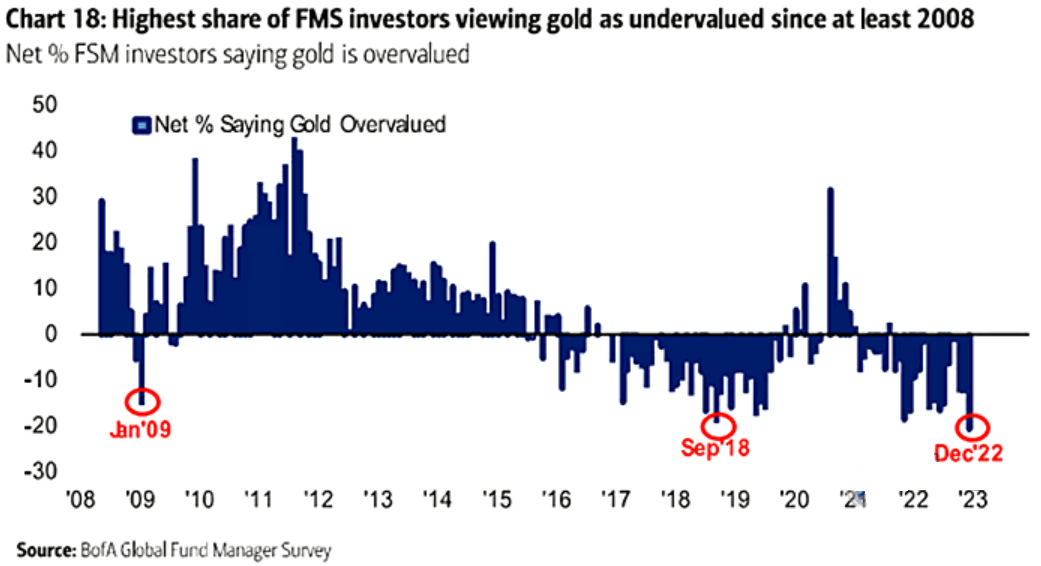

In contrast, some assume that ‘peak hawkishness’ is bullish for the gold price, as rate cuts could commence in 2023. On top of that, Bank of America’s latest Global Fund Manager Survey shows that institutional investors believe gold is materially undervalued.

Please see below:

To explain, the dark blue bars above track the net percentage of respondents that believe gold is overvalued. If you analyze the right side of the chart, you can see that the latest dark blue bar is particularly negative, which signals a degree of optimism about the yellow metal’s future prospects.

Conversely, the dark blue bars have been negative for much of 2021 and 2022, and gold has not rewarded the bulls throughout that period. Also, we’re short the GDXJ ETF, so while the gold price has performed relatively okay, the junior miners’ index has suffered mightily.

Yet, while a stronger USD Index and higher real interest rates have battered financial assets in 2022, Zoltan Pozsar, Global Head of Short-Term Interest Rate Strategy at Credit Suisse, believes the fallout from the Russia-Ukraine war could double the gold price in 2023.

In a nutshell: if Russia responds to the recently introduced $60-a-barrel oil price cap by asking for a gram of gold for two barrels of crude, the yellow metal could benefit immensely. He wrote:

“If the West is looking for a bargain, Russia can give one the West can't refuse: 'a gram for more.' If Russia countered the price peg of $60 with offering two barrels of oil at the peg for a gram of gold, gold prices double.”

He continued:

“Russia won't produce more oil, but would ensure that there is enough demand that production doesn't get shut. And it would also ensure that more oil goes to Europe than to the U.S. through India. And most important, gold going from $1,800 to close to $3,600 would increase the value of Russia's gold reserves and its gold output at home and in a range of countries in Africa.”

But, while he described the prospect as “Crazy? Yes. Improbable? No,” the prediction is more of a ‘what if’ event that falls near the low end of the probability spectrum. Essentially, it’s possible, but it’s more of a wild card that holds less weight in our view than other medium-term factors.

For example, while Russia pegged the ruble to the price of gold in March/April, the gambit only lasted ~two weeks. In addition, the USD/RUB remains well below its pre-pandemic level, so the FX market is not fretting about the EU oil price cap.

Please see below:

To explain, the candlesticks above track the USD/RUB, and if you analyze the right side of the chart, you can see that the ruble is highly valued versus the U.S. dollar relative to its recent history. Furthermore, the large spike on the right side of the chart highlights how the USD/RUB soared when investors assumed the Russia-Ukraine conflict would sink the Russian economy and the ruble.

In contrast, the ruble is far from panicking now, which highlights the lack of concern about potentially lower Russian oil prices.

Overall, it’s possible that a Russian oil-gold peg could push the yellow metal to $3,600 in 2023, but there are many possible, though not highly plausible, scenarios that could unfold. Therefore, we like to position for the most likely outcomes, which means other factors deserve higher priority.

So, while we’re mindful of the prospect, and will react accordingly if the odds increase, we expect gold to hit new lows in 2023.

Silver Sinks as the Hawks Swarm

With risk appetite taking a beating on Dec. 15, investors’ Christmas spirit seemingly disappeared before Santa Clause even arrived. As a result, while seasonality remains bullish, we warned that with the S&P 500 highly overvalued, a sharp decline could spell trouble for the silver price. We wrote on Dec. 5:

While the [S&P 500] remains elevated right now, downside risk has intensified from a fundamental, technical and sentiment perspective.

Overall, the silver price has benefited from the same false narrative uplifting several risk assets. After being shocked by 75 basis point rate hikes in 2022, the crowd believes that a step down to 50 basis points is akin to a dovish pivot. However, for those that understand history, 50 basis points are still highly hawkish. As such, the crowd is trying to create the perfect investment recipe with imperfect ingredients

Consequently, while market participants attempted to redefine a dovish pivot, the hawkish realities that upended the S&P 500 and the silver price throughout 2022 returned on Dec. 15.

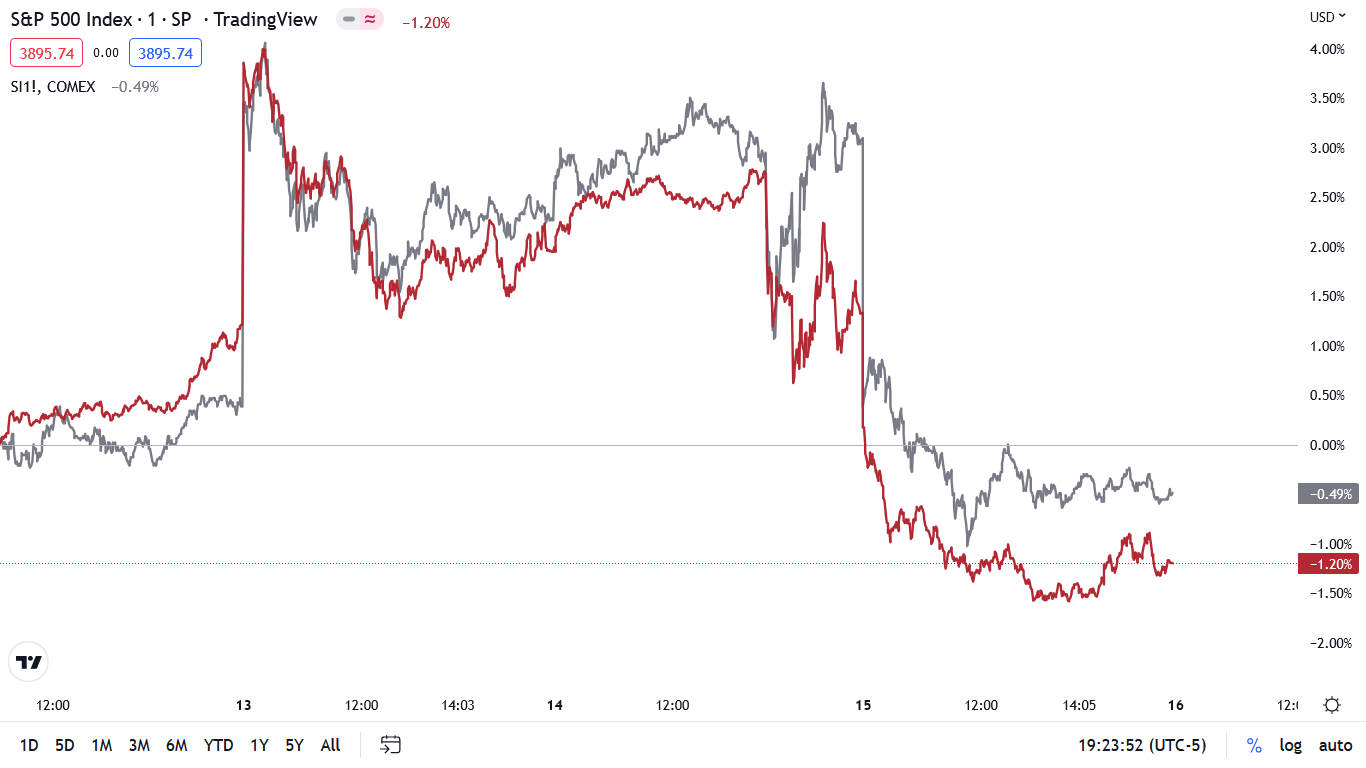

Please see below:

To explain, the red line above tracks the one-minute movement of the S&P 500, while the gray line above tracks the one-minute movement of the silver futures price. If you analyze the left side of the chart, you can see that the pair jumped after the weaker-than-expected Consumer Price Index (CPI) report was released on Dec. 13.

In contrast, after Fed Chairman Jerome Powell stated the obvious on Dec. 14, it took less than 24 hours for investors to digest the fundamental ramifications. So, while we warned that the headline CPI benefited from lower oil prices and that broad-based inflation hit new 2022 highs (the Atlanta Fed’s Sticky CPIs), the fundamentals won the daily battle.

Furthermore, the connection between the S&P 500 and the silver price highlights the challenges that should confront the white metal in 2023.

For example, silver and mining stocks are more correlated to the index than gold, and with a recession poised to materialize in 2023, drastic drawdowns of the S&P 500 often sink silver. Also, with inflation anxiety still rattling the crowd, our warnings throughout 2021 and 2022 are now more noticeable.

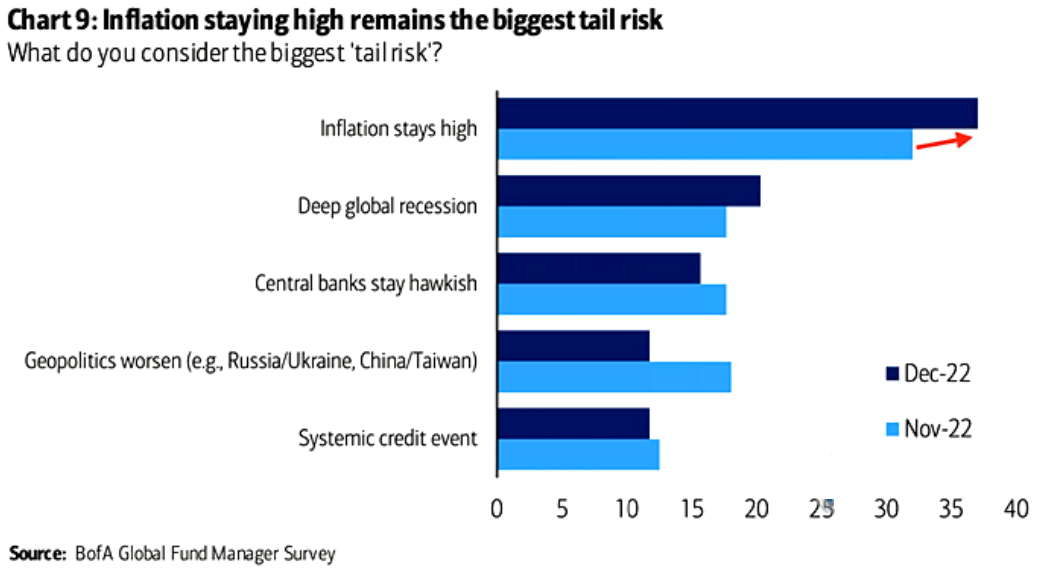

Please see below:

To explain, Bank of America's latest Global Fund Manager Survey shows that the biggest tail risk (low probability, high impact event) is that inflation remains high. However, it's the most likely outcome. The consensus materially underestimates the resiliency of inflation, and history shows the pricing pressures do not recede along a smooth glide path.

As it stands, while inflation should slow in 2023, there is a huge difference between a sharp decline to 2% and a metric that jumps around at 5%+.

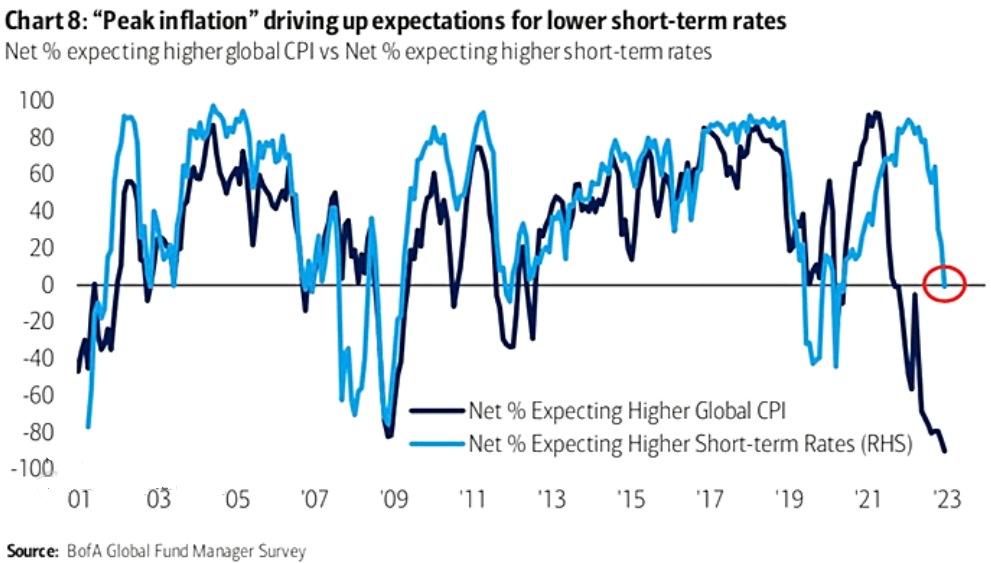

Likewise, institutional investors' beliefs contrast the medium-term fundamental backdrop.

Please see below:

To explain, the dark blue line above tracks the net percentage of respondents that expect a higher global CPI, while the light blue line above tracks the net percentage of respondents expecting higher short-term interest rates.

If you analyze the dark blue line’s sharp drop on the right side of the chart, you can see that ‘peak inflation’ is an extremely consensus opinion. Yet, declines of this magnitude often occur alongside calamities (like 2008), and the U.S. economy is far from this level of devastation.

In addition, the plight of the light blue line on the right side of the chart highlights how more fund managers are buying the notion of rate cuts in 2023.

But, that’s not how we see it. With the U.S. federal funds rate (FFR) still well below its historically-implied peak, a multitude of factors support higher short-term interest rates in 2023. So, while the silver price has benefited from the rate cut optimism, investors’ desire for pre-pandemic monetary policy should be their undoing in the months ahead.

Overall, the white metal wept as liquidations unfolded across several risk assets. However, the decline was modest relative to its recent bear market rally, which leaves the silver price well above its fundamental value. As such, with panic still missing from the financial markets, gold, silver, mining stocks and the S&P 500’s maulings likely still await us.

The Bottom Line

A dash for cash materialized on Dec. 15, as the sentiment bulls couldn’t withstand the pain any longer. With the FOMC pouring cold water on the pivot hopes and Powell saying that “ongoing hikes will be appropriate,” the FFR should continue its ascent.

Furthermore, history shows that the U.S. 10-Year real yield often peaks alongside (or near) the peak in the FFR, and both metrics are bullish for the USD Index. Thus, even without a recession-induced liquidation, the optimistic outlooks for the FFR, real yields and the USD Index makes the PMs’ medium-term backdrop highly bearish.

In conclusion, the PMs declined on Dec. 15, as the USD Index and the U.S. 10-Year real yield rose; and while the metals have had the upper hand in recent weeks, the tide should turn in 2023. As a result, while we are bullish on the PMs’ long-term prospects, we expect gold, silver and mining stocks to hit fresh lows before buying opportunities arise.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Dec. 21: The Conference Board’s Consumer Confidence Index

With weakness in the oil market reducing gasoline prices, measures of consumer confidence have increased recently. Therefore, it will be interesting to see how Americans view the inflation outlook and how their spending intentions have been affected.

- Dec. 22: Kansas City Fed Manufacturing Index

The Fed’s regional PMIs help paint a portrait of the overall U.S. economy, so monitoring the growth, inflation and employment results help to predict future government data.

- Dec. 23: Personal Consumption Expenditures (PCE) Index

While the PCE Index should mirror the CPI's monthly deceleration, it's the Fed's preferred inflation gauge, which makes it essential to monitor.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

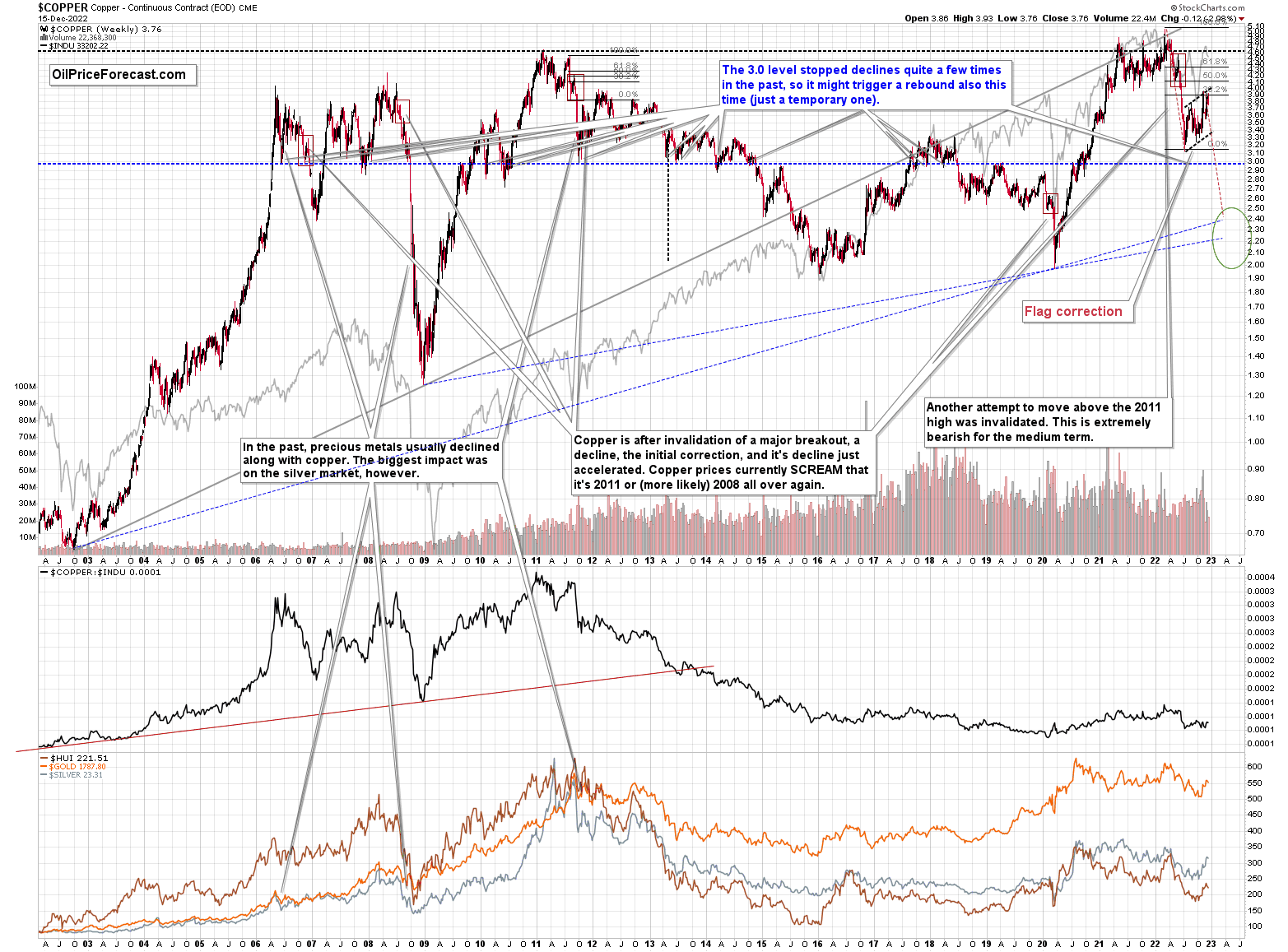

Let’s start today’s technical discussion with a quick check of copper prices.

Overall, everything I wrote about it last week remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

No market moves up or down in a straight line (well, the 2008 slide appears to have been an exception), and a short-term correction doesn’t necessarily invalidate the bigger trend. For the last couple of months, copper has been trading sideways, but it didn’t change much regarding the outlook.

In fact, it made my previous target area even more likely. You see, the consolidation patterns are often followed by a move that’s similar to the move that preceded them. In this case, the previous 2022 decline was quite significant, and if it is repeated, one can expect copper to decline well below 3.

Actually, copper could decline profoundly and bottom in the $2.0-2.4 area. That’s where we have rising, long-term support lines and also the previous – 2016 and 2020 – lows.

Flag patterns (which we just saw in copper) tend to be followed by price moves that are similar to ones that preceded them. I marked this on the above chart with red, dashed lines. This method supports a copper price’s move to around $2.4.

Given the recent flag pattern and the size of the previous decline (and its pace), it seems quite likely that it could take another 2-7 months for copper to move to about $2.4. Late March / early April seem the most likely time target given the current data.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after invalidation of a major breakout, a decline, and a correction. Copper prices currently SCREAM that it’s a variation of 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

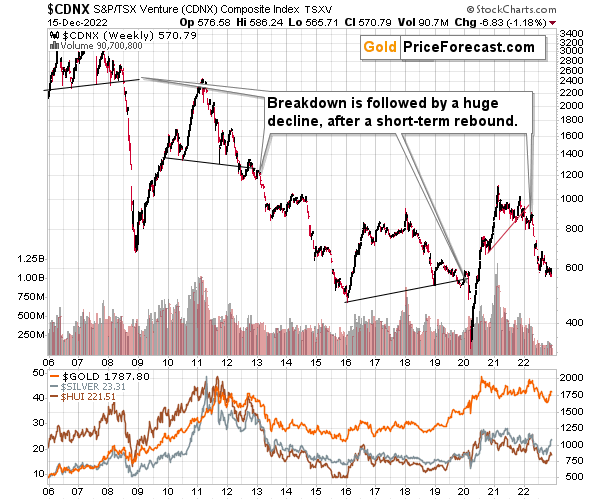

Having said that, let’s check junior miners’ really big picture.

I previously commented on the above chart in the following way:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

One thing that I would like to add today is that just like it was the case in 2008, the move higher that we saw before the final (biggest) slide in gold, silver, and gold stocks (lower part of the chart), we didn’t see a visible rally in the TSX Venture Index. Just as the index paused back then, it paused right now.

Currently, it’s trading at about 600, and back then, it consolidated at about 2500. The price levels are different, but the overall shape of the price moves (lack thereof) is similar. This serves as a signal, that the recent upswing in the PMs was not to be trusted.

The above is one of the weakest (from the technical point of view) charts that is see across the board right now. There is a strong long-term downtrend visible in the TSX Venture Index, and if stocks slide similarly as they did in 2008, the TSXV could truly plunge – perhaps even to the 300 level or lower.

Having said that, let’s turn to gold.

Let’s start with context:

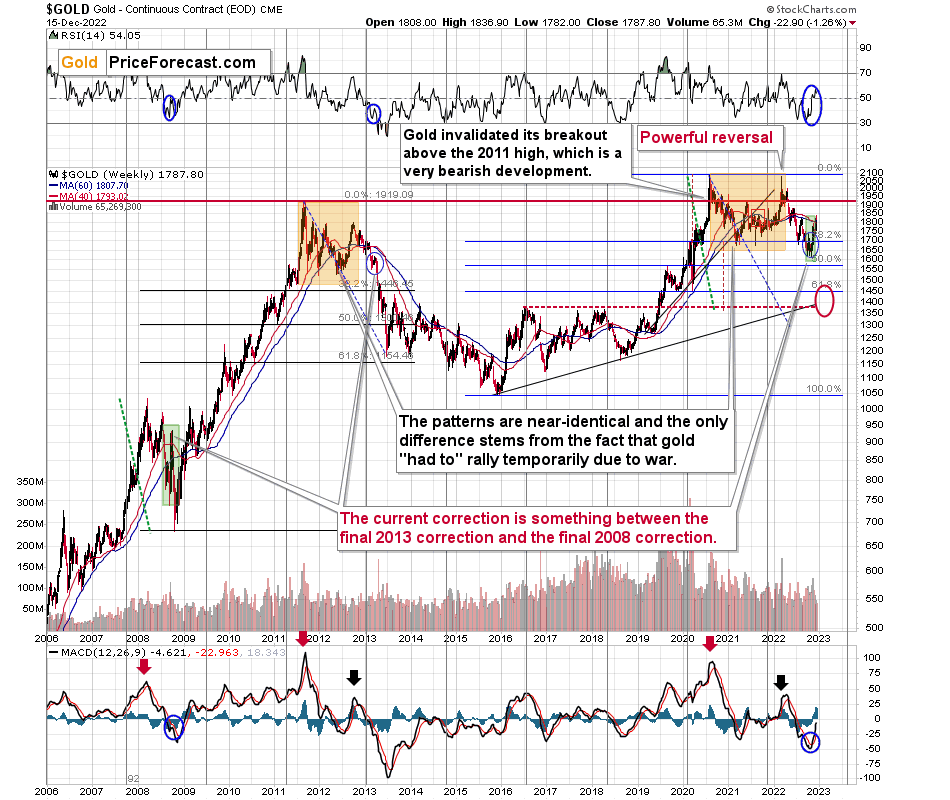

Between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet gold failed to rally to new highs.

In fact, it’s trading very close to its 2011 high, which tells you something about the strength of this market. It’s almost absent.

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. We can also spot similarities between now and 2008. The long-term gold price chart below provides details.

Looking at the gold market from a broader point of view, the corrective upswing that we saw recently is something between what we saw in 2013 and what we saw in 2008.

The recent move higher was bigger than what we saw in 2013 but smaller than what we saw in 2008.

No wonder – the current situation in general is similar to both. In fact, that’s why I’ve been writing about this dual similarity for many months now.

Back in 2013, the final of the pre-slide corrective upswings ended with gold below its 40- and 60- week moving averages (marked with red and blue, respectively).

Back in 2008, the final of the pre-slide corrective upswings took gold visibly above both above-mentioned moving averages.

And now? We saw a move above both moving averages, but only a bit above them – the move was not as profound as the one that we saw in 2008.

The most interesting thing about the above is that when gold did finally move above those moving averages in 2008, it meant that the rally was practically over and that it was the perfect time to be shorting the precious metals market – especially mining stocks.

Now, as far as the link to 2013 is concerned, it remains perfectly intact, with the additional note that the final corrective upswing is bigger this time – more like what we saw in 2008.

Gold is sometimes forced to react to some geo-political events as the safe-haven buying kicks in, but these moves are usually short-term lived. Looking at long-term charts helps to keep things in proper perspective.

Consequently, my previous comments remain up-to-date:

Based on the above chart, it’s quite clear that the situation that is now being repeated. The patterns marked with orange rectangles and blue ellipses are almost identical (also in the MACD indicator, and to a lesser extent in the RSI indicator).

Sure, the situations are not identical, as this time we had a Russian invasion of Ukraine that pushed gold temporarily higher. Other than that, the situations are extremely similar.

Based on the stage of the self-similarity and the confirmed breakdown below the $1,700 level, gold is now likely to slide.

Based on the analogy to 2013, it’s not only likely to slide, it’s likely to slide profoundly in a sharp manner. These may be the last days or hours before the slide fully begins.

How low is gold likely to go during this upcoming big medium-term decline? Perhaps as low as its 2020 low, around $1,450-1,500. Then, after a rebound, quite likely to be at or slightly below $1,400.

I realize this is far from the current price, but nonetheless, this target area appears justified in my opinion. There are two important Fibonacci retracements based on the 2015-2020 rally that gold can bounce from (it recently bounced from the 38.2% retracement). These are 50% and 61.8% retracements.

The support provided by the 61.8% retracement is strengthened by the 2020 low and the support provided by the 50% retracement is strengthened by the 2019 high.

However, based on gold’s self-similarity to 2013, it seems that we’re about to see a slide that’s bigger than what we’ve been seeing so far this year. This time – based on the similarity – gold is likely to decline profoundly, but no longer in the back-and-forth mode. If gold formed its next local low at the 50% retracement (so at about $1,560), then it might do so still within the declining, short-term trend channel (sometime in September).

However, if gold is to stick to the link to 2013, then it should decline more rapidly. In this case, the technique that can help us estimate the short-term target is the one that says that after a breakdown from a trend channel, price is likely to move approximately by as much as the height of the previous trend channel. In this case, gold could break below the trend channel soon and then decline even more. Based on the height of the trend channel, the above means that a move to the 61.8% retracement as the next downside target is more likely than a move to the 50% retracement.

I previously wrote that the above-mentioned decline in gold would likely be linked to a breakdown in the EUR/USD below 1, and we already saw both: decline in gold, and a breakdown in the EUR/USD below 1. The implications remain bearish.

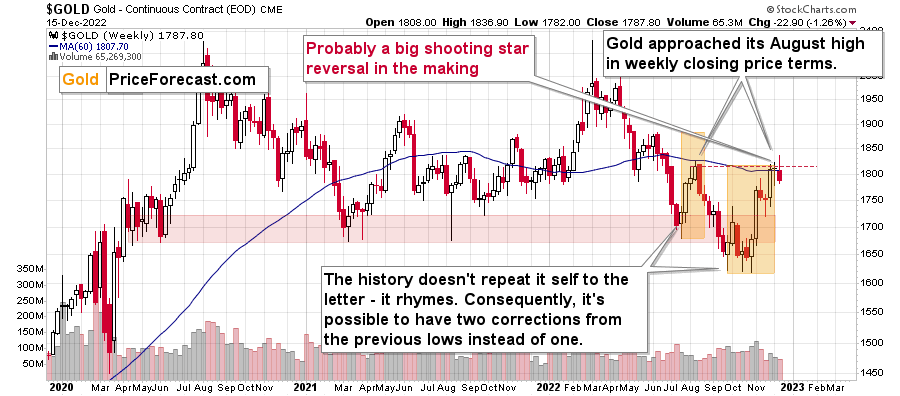

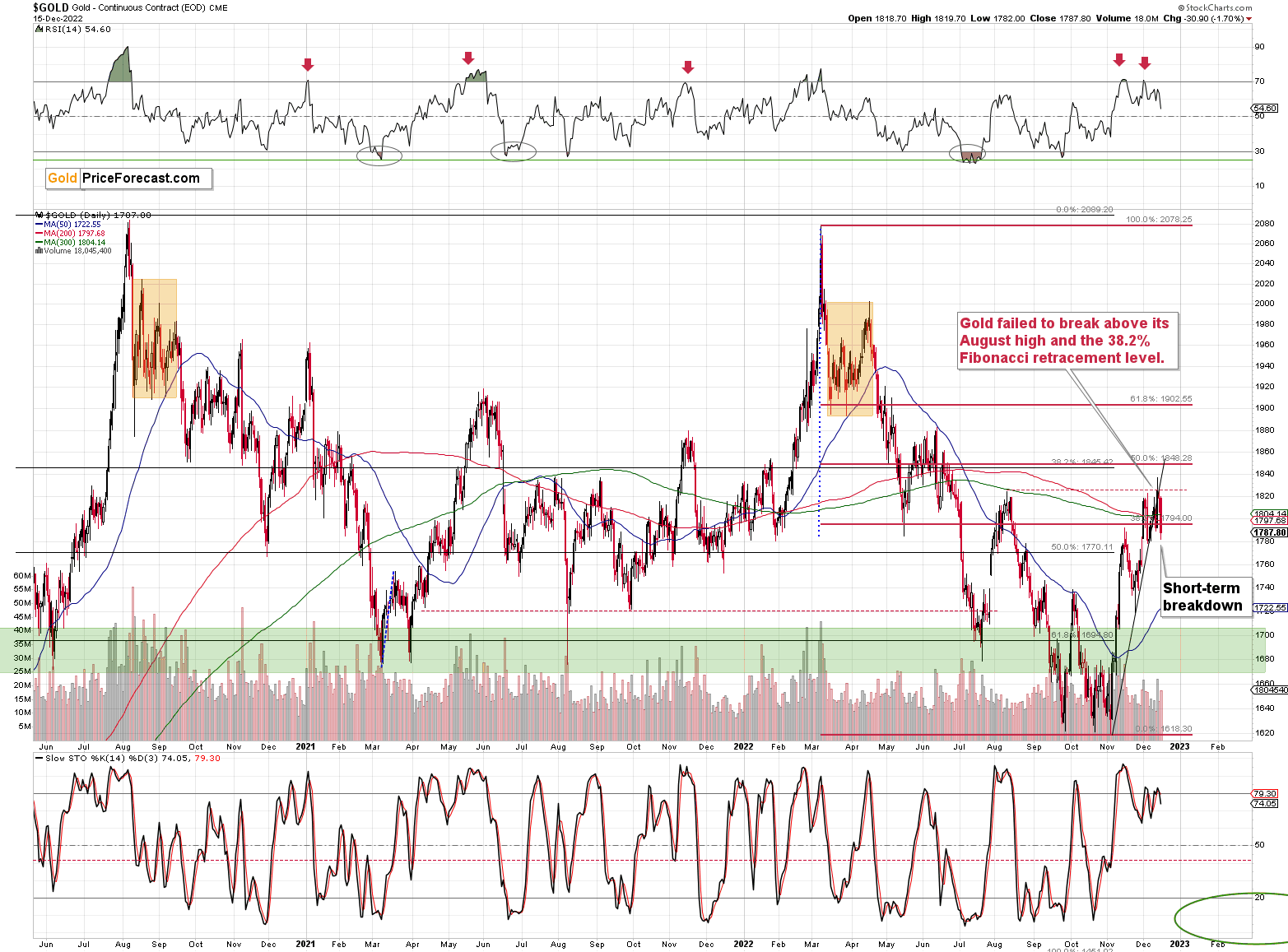

Having said that, let’s zoom in to see gold’s short-term price moves.

Gold’s rally was just stopped by the resistance provided by its previous high and its 60-week moving average). Will gold now reverse?

The above chart features gold price in terms of weekly candlesticks. As you can see, it just approached its August high.

And gold failed to move above it once again.

The resistance held.

What is even more bearish, is the fact that gold is likely about to form a weekly shooting star (reversal) candlestick. “Likely,” because the week is not over yet.

Still, given today’s pre-market moves in gold and silver (both are down), it seems that the reversal candlestick will soon be a fact.

This – along with the failed attempt to move above the August high – has profoundly bearish implications for the following weeks.

Gold, just like many other markets (i.e., stock prices), recently corrected slightly more than 38.2% of its previous move. Then it invalidated this small breakout. It happened more than once, so this bearish indication was strengthened.

The same goes for gold’s attempt to move above its August high – the one that failed. It too strengthened the bearish case fr the following weeks.

Please note that the above is taking place shortly after two sell signals from the RSI indicator, which further confirms the bearish nature of the recent price moves.

Gold’s breakdown below the rising, short-term, black support line makes the short-term outlook even more bearish.

Having said that, let’s take a closer look at the silver market.

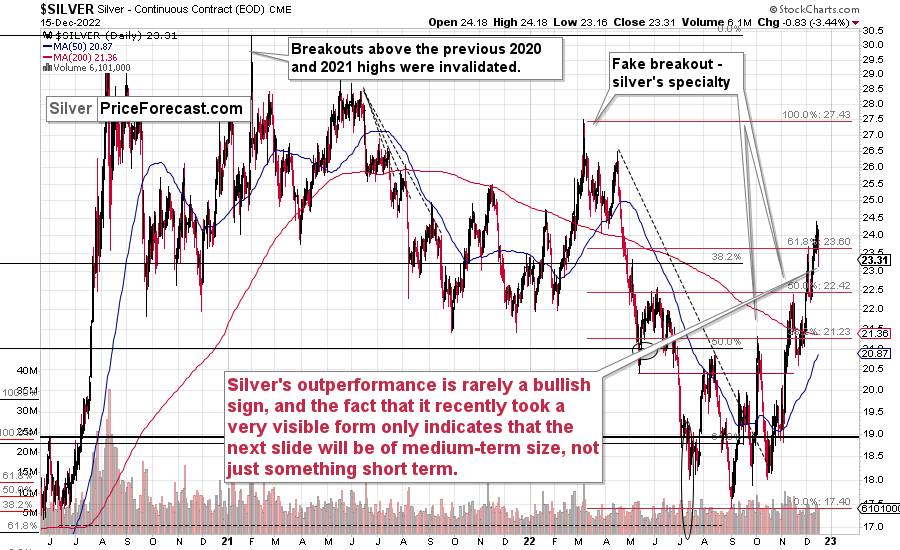

As I emphasized many times before, silver's outperformance is rarely a bullish sign, and the fact that it recently took a very visible form only indicates that the next slide will be of medium-term size, not just something short term.

Silver just invalidated its temporary breakout above the 61.8% Fibonacci retracement.

Yes, that’s a retracement that’s higher than the analogous ones in stocks, gold, and mining stocks, and… This is yet another confirmation of silver’s short-term strength.

Once again – it’s not something bullish, but very likely something bearish.

This means that the recent sizable rally is nothing more than a – sizable, but still – correction within a bigger downtrend.

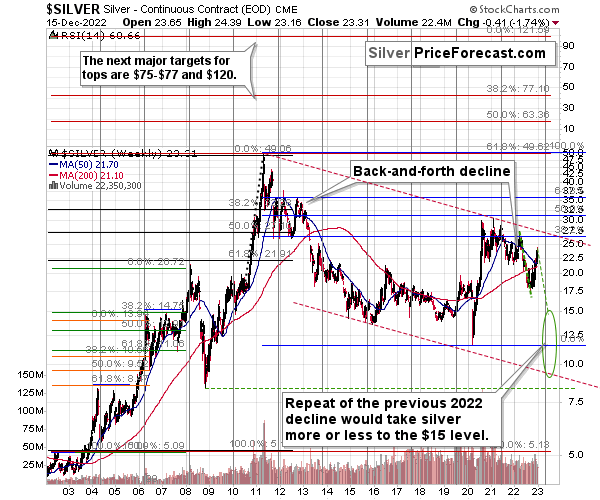

Looking at silver from a long-term point of view helps to see the forest, not just individual trees.

When looking at silver from a long-term point of view, it’s still obvious that the recent move higher was most likely just a corrective upswing.

What happens after corrections are over (as indicated by, i.e., silver’s outperformance)? The previous trend resumes. The previous trend was down, so that’s where silver is likely headed next.

Besides, the long-term turning point for silver is due in several months, and if silver repeats its previous 2022 decline, then it will bottom close to the turning point and also close to the $15 level– in the first half of 2023.

It’s likely to repeat its previous 2022, because that’s what tends to happen after flag patterns, and what you see on silver’s short-term chart between September and yesterday appears to be a flag pattern.

However, will silver only repeat its previous 2022 performance and not decline more than it already has?

Based on the analogies to 2008 and 2013, the latter is more likely. The 2013 slide was bigger than the initial decline that we saw in 2012. And the final 2008 slide was WAY bigger than what we saw before it.

Due to its industrial uses, silver is known to move more than gold, in particular when the stock market is moving in the same way as gold does. Since I think that gold and stocks are both likely to slide, silver is indeed likely to decline in a truly profound manner. Quite likely lower than just $15.

Consequently, my prediction for silver prices remains bearish, as does the outlook for the rest of the precious metals sector.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

Having said that, let’s take a look at what happened in mining stocks.

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

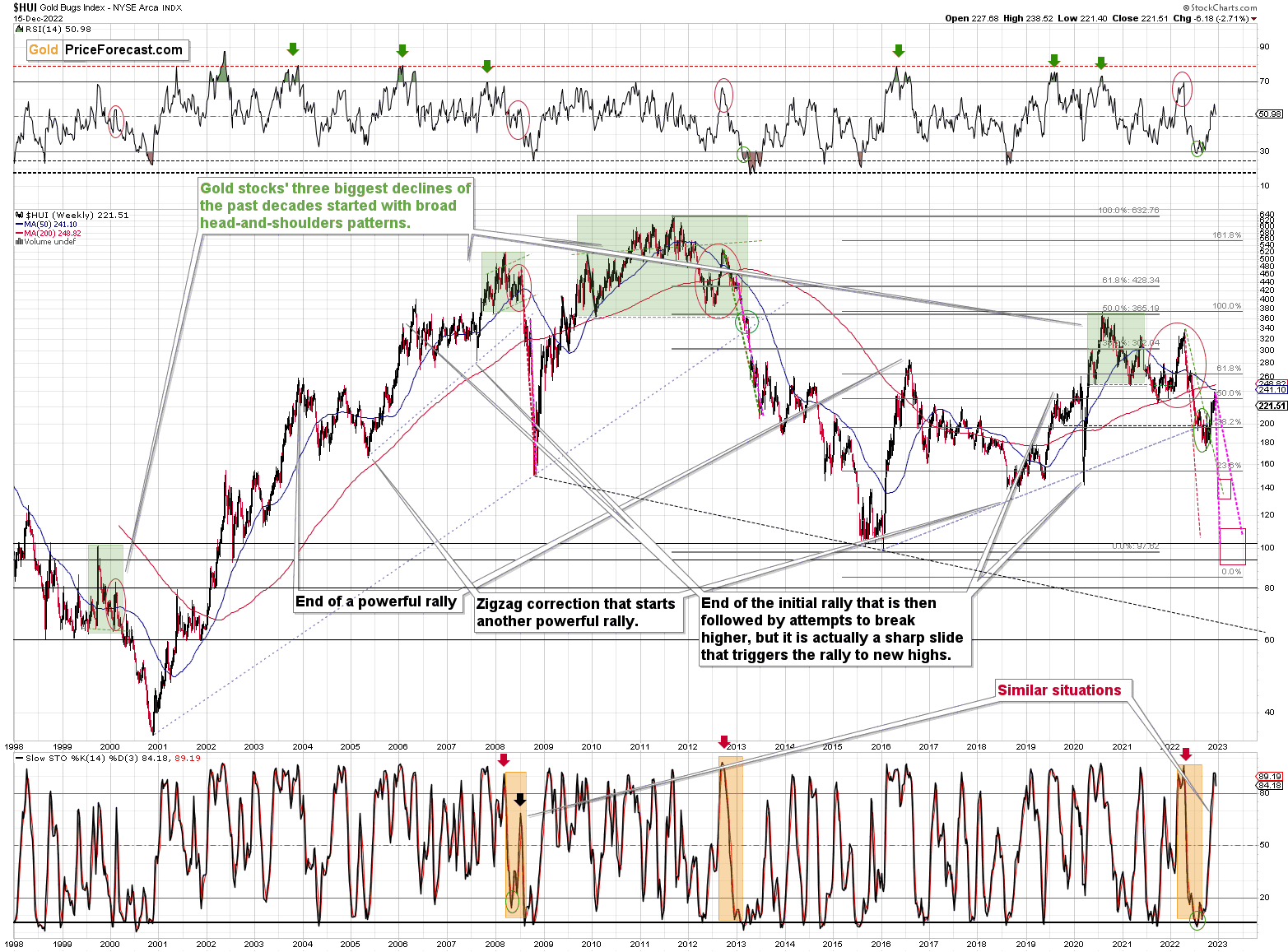

For example, right now, gold stocks are declining similarly to how they did in 2008 and in 2012-2013.

As gold was practically forced to rally recently based on geopolitical events, news, and rumors (i.a. false hope for Fed’s dovish U-turn), so were gold stocks.

Did it change anything technically?

Only a bit, and only at first sight.

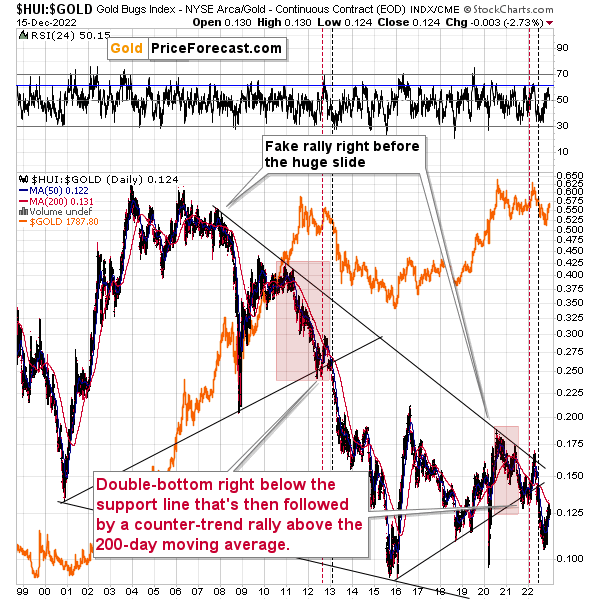

The HUI Index is a bit above its rising resistance line, but it’s trading there after it already verified a breakdown below this line.

Because the nature of the rally appears to be temporary, not only based on the analogy to 2013, but also on recent fundamental developments, I doubt that the breakout will be confirmed (as was the case with gold's short-term breakout above the 38.2% Fibonacci retracement). Please take a look at the stochastic indicator’s performance in the bottom part of the above chart. It’s currently doing practically the same thing that it did in 2008. And that – in 2008 – marked the final counter-trend top before the biggest part of the slide.

Is this time different? Those are expensive words on Wall Street.

I highlighted and copied the sharpest and final parts of the medium-term declines (2008 and 2013) to the current situation. There are quite a few other markings on the above chart, but the ones that I just mentioned are marked with the magenta color.

The analogy to 2008 points to the end of this year as being the likely moment for the final bottom.

The analogy to 2013 points to the middle of 2023 as being the likely moment for the final bottom.

The current situation is somewhat similar for both. However, it seems that what started as a primarily 2013-like move lower is becoming a 2008-like move lower. That’s based i.a. on the volatility of the recent upswing.

So, on average, early 2023 seems like a quite likely target for the final bottom.

Then again, please note that the two analogies fit right into my previous target area for the final bottom, so this target area simply remains intact.

Actually, based on both of the above, it seems that a move to 2020 lows close to the end of this year and then a correction followed by a move even lower in 2023 appear to be quite likely outcomes at this time.

How low can the HUI Index fall during the next big downswing?

As it’s the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 100-150 is my current target area for the upcoming slide in the HUI Index.

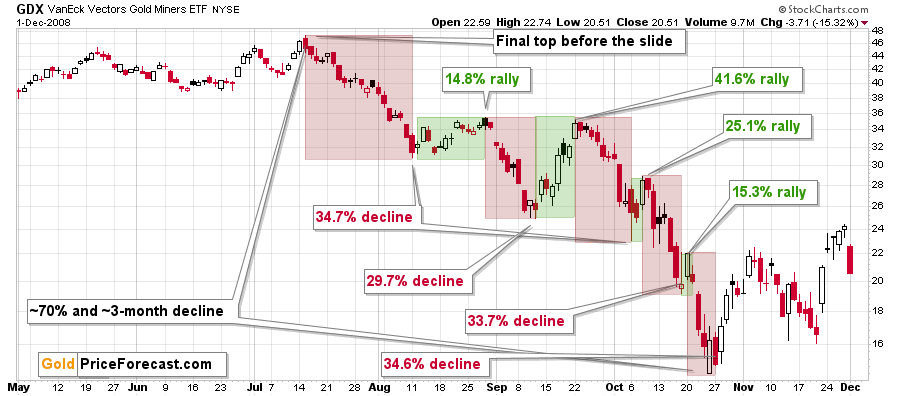

All right, let’s zoom in and see how mining stocks declined in 2008.

Back then, the GDXJ ETF was not yet trading, so I’m using the GDX ETF as a short-term proxy here.

The decline took about 3 months, and it erased about 70% of the miners’ value. The biggest part of the decline happened in the final month, though.

However, the really interesting thing about that decline – that might also be very useful this time – is that there were five very short-term declines that took the GDX about 30% lower.

I marked those declines with red rectangles. After that, a corrective upswing started. During those corrective upswings, the GDX rallied by 14.8-41.6%.

Do you know now much the GDX ETF rallied from its September 2022 bottom? It moved up by 40.7%. This means that the move higher now is practically identical with the corrective (!) upswing that we saw in September 2008. The analogy was not broken – it remains intact, and it points to much lower prices in the future.

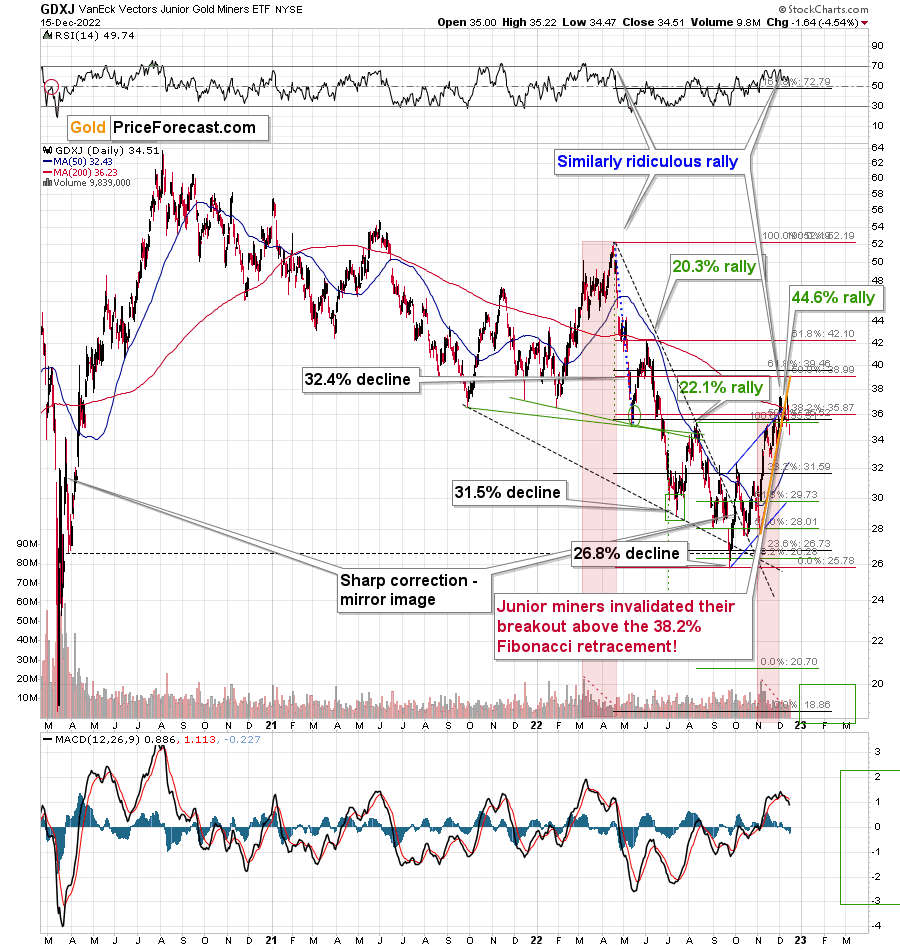

Just like gold, the GDXJ invalidated the breakout above its 38.2% Fibonacci retracement and few times, and now it also broke below the rising, short-term support line (marked with orange).

This is a powerful, bearish combination of factors, especially that miners were the first to decline – gold followed, while silver was still showing strength.

Please keep in mind that the above comes on top of the analogy that I marked with red rectangles, and my previous description thereof remains up-to-date:

The current upswing continues to be similar to what we saw in March and April, earlier this year. On the above chart I named both rallies “ridiculous” – I did so as what we see now is against that’s happening in the real interest rates, and it appears that it’s the general public that’s pushing the prices higher now.

Technically, one could say that the GDXJ formed an inverse head and shoulders pattern (the early September bottom being the left shoulder and the mid-October bottom being the right shoulder), which was just completed.

Just as the March – April rally ran its course on declining volume, we saw the same thing recently. Even the RSI was slightly below 70 at the April top, just like it was the case very recently.

Speaking of analogies, I previously wrote that the current rally is a mirror image (it’s not a crystal-clear mirror, though) of the corrective decline that we saw in late-March 2020. As it turned out, due to the most recent part of the upswing, the size of both moves became even more aligned.

And yes, this means that another decline could take the GDXJ all the way down to its 2020 low, or very close to it.

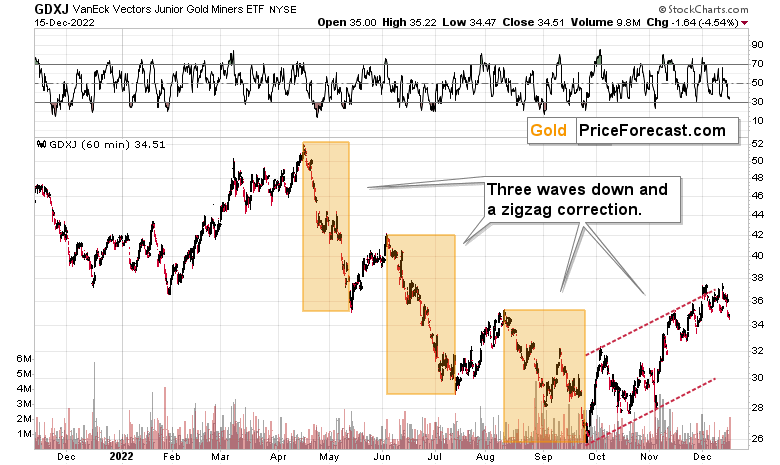

On the below chart, I marked just how perfectly the recent price moves played out according to the Elliott Wave Theory.

Of course, EWT is not the only tool that one could use, and I find other technical tools more useful, but still, this kind of pattern-following is uncanny.

The classic EWT pattern is three waves down (I marked those with orange rectangles) and then a correction consisting of two smaller waves.

That’s exactly what we have seen in recent months. The September–now pattern appears to be the above-mentioned correction. It didn’t only consist of two smaller waves higher – they were actually almost identical in terms of size and sharpness. This created a classic ABC correction (flag) pattern.

Two weeks ago, I wrote that the Dec. 1 small breakout above the upper red line didn’t have meaningful bullish implications as it hadn’t been confirmed. And indeed, it was invalidated.

Now, since this pattern is complete, another huge 3-stage move lower can – and is likely – to unfold. This is very bearish for junior mining stocks (as well as for gold, silver, and probably other commodities and stocks), and the fact that juniors are already showing weakness relative to gold (the latter was almost flat yesterday, while miners declined) serves as a bearish confirmation. As always, I can’t guarantee anything, but in my view, the profits that can be reaped on this upcoming slide can be enormous.

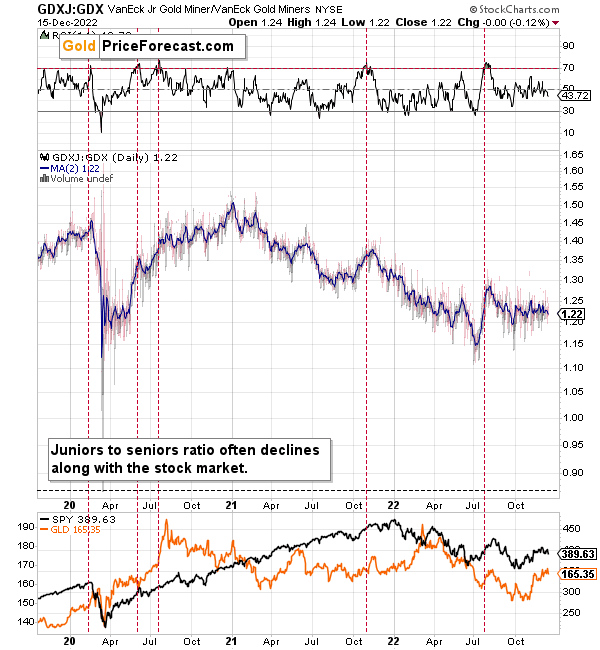

Meanwhile, the relative performance of junior miners compared to senior miners continues to deteriorate in a medium-term trend.

During this quick upswing, juniors rallied relative to seniors, but this is just a very short-term move that’s within a short-, and medium-term downtrends.

This implies bigger declines in the GDXJ in the future.

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw at the 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI to gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

Recently, we saw a quick upswing in the ratio, but that’s not a game-changer – even the biggest declines had corrections in the past.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices of gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks) and that’s exactly what’s likely to happen.

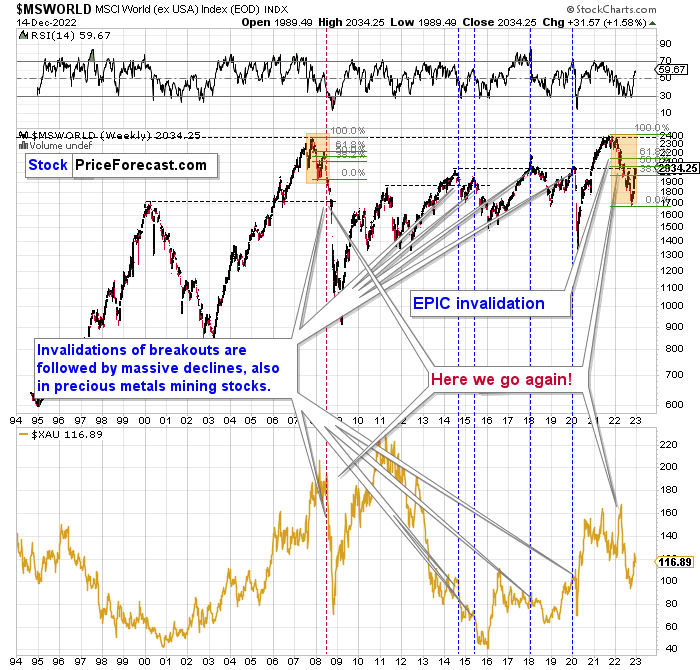

Just like what we saw in the case of copper, gold, and mining stocks, world stocks corrected about 38.2% of their preceding decline.

And recently, they corrected a bit more – almost half of the preceding decline.

Please note that the initial decline was now bigger than what we saw in 2008. Back then, stocks corrected about 61.8% of their initial decline before tumbling. If stocks are not able to do the same thing now – and they might not be – then the following slide could be even bigger than what we saw in 2008. Naturally, this would be profoundly bearish for junior mining stocks.

This means that nothing really changed, and the situation remains extremely bearish based, i.e., on the analogy to what we saw after previous invalidations of long-term breakouts.

As a reminder, in early 2022, I wrote that the situation was very bearish as invalidations of previous breakouts were usually followed by massive declines – not just in stocks but also in precious metals.

When stocks invalidated their 2006 breakout in 2008, their prices truly crumbled.

We also saw that on a smaller scale in 2014, 2015, and early 2018.

We’re seeing it right now.

To clarify, we’re actually seeing the aftermath of the invalidation. The huge decline is already taking place.

The difference between now and 2008 is that back then the slide was more volatile, and we didn’t really see a visible correction during the plunge. This time, the decline is more measured, and we saw a correction to one of the most classic retracements imaginable – the 38.2% one. This correction doesn’t change the trend, which remains down.

Based on what happened in 2008, it seems that stocks are about to move much lower in the following months.

Let’s take a look at the markets from a more short-term point of view and from the U.S. perspective.

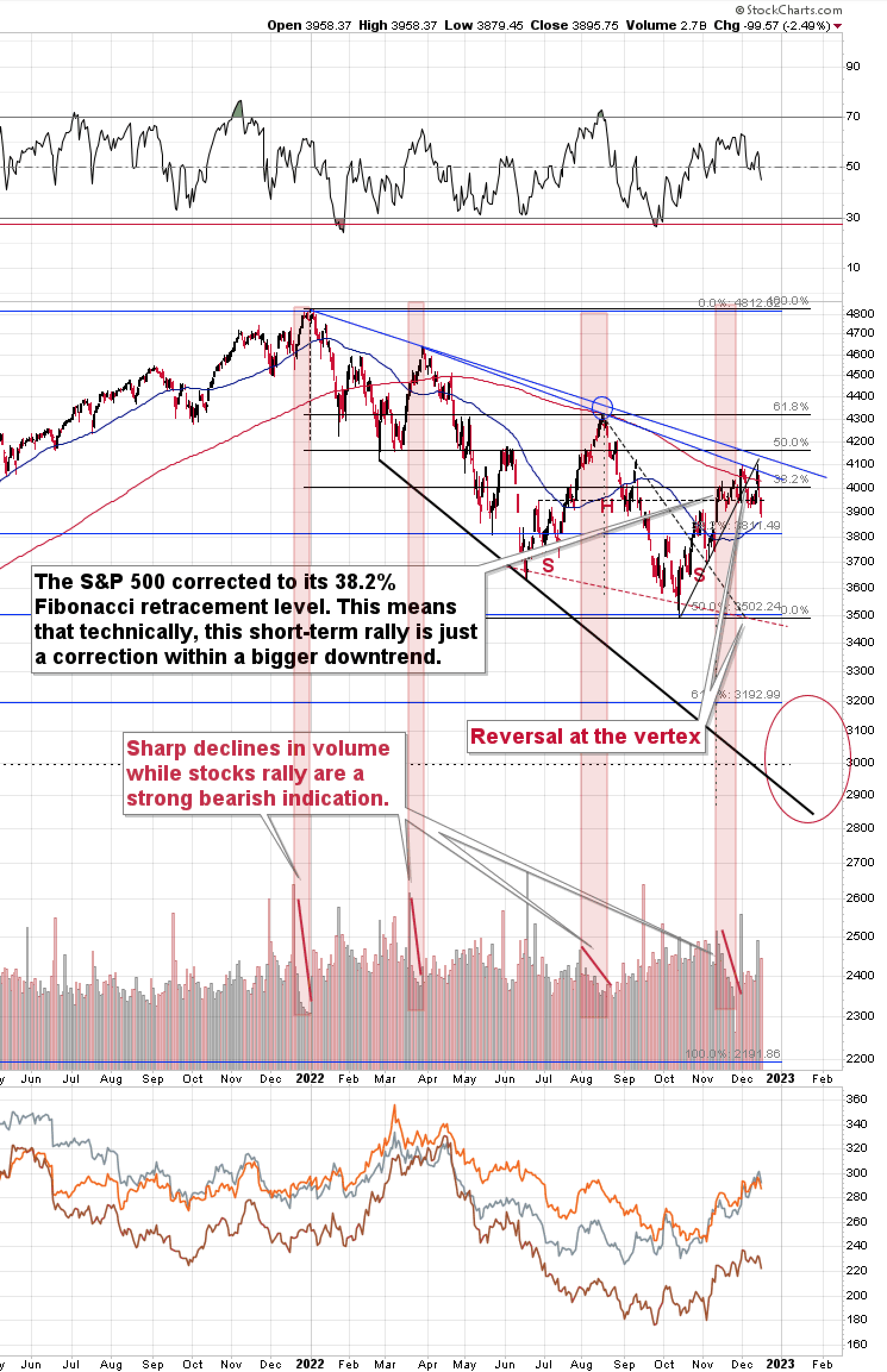

The S&500, like global stocks, corrected a bit more than the 38.2% of the previous decline. And now they turned south, invalidating this small breakout. At the same time, they broke below the rising support line, which makes the outlook even more bearish. Consequently, my previous comments on the above chart remain up-to-date:

The broad market moved lower this week, and there are two good reasons to think that this time, the small move lower is just the beginning of a much bigger move to the downside.

One of the reasons is that this move lower came right after the triangle-vertex-based turning point. The declining black and red lines (both dashed) intersect at more or less the very recent top. As their name says, those turning points mark… Well, turning points. And since the most recent short-term move was to the upside, it currently has bearish implications.

The second reason is that stocks now broke below their rising support line (marked with a solid black line), and that’s not what happened during the two previous small moves lower.

The analogy in the price-volume link (marked with red rectangles) also points to much lower prices in the stock market.

Additionally, please note that stocks tried to move above their previous highs and the declining blue resistance line – and they failed. The invalidation served as yet another sell signal.

Why is this important for gold and silver investors and traders? Because the last two big moves took place more or less in line with each other – in stocks and in precious metals (and miners). The slide in stocks could also trigger something similar in the case of commodities like crude oil. The same thing is likely to happen again this time, especially given what’s happening in the USD Index.

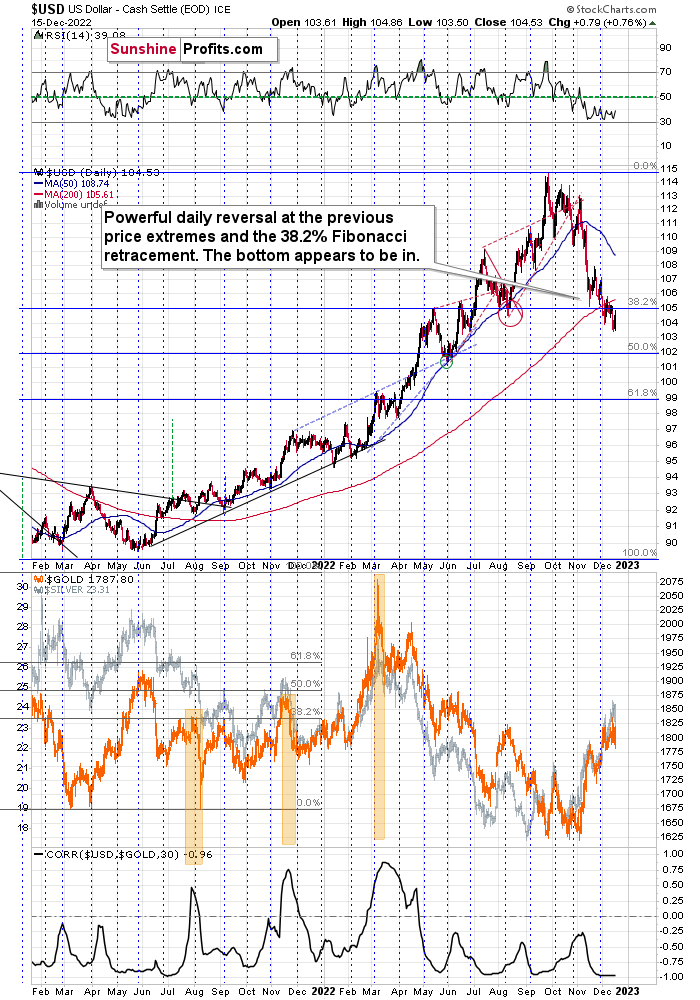

The USD Index moved a bit below the 38.2% Fibonacci retracement level, and at first sight this might seem bearish, but…

Long-term indications are more important than short-term ones, and based on what we see on the long-term USDX chart below, it seems that the small move below USD’s 38.2% retracement will be invalidated shortly.

The USD Index moved to its very strong support provided by the previous long-term highs.

The 2016 and 2020 tops (as well as the 2002 low and the 1999 top) currently serve as very strong support at about 104 level.

To clarify, the highest of those highs has 103.5 as the highest daily closing price.

This means that there was no breakdown recently.

Consequently, the outlook for the USDX remains very bullish based on the above indication.

What we saw recently appears to be nothing more than a verification of the breakout above the previous highs.

This means that gold, silver, and mining stocks are likely to decline profoundly as they are very negatively correlated with the USD Index.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

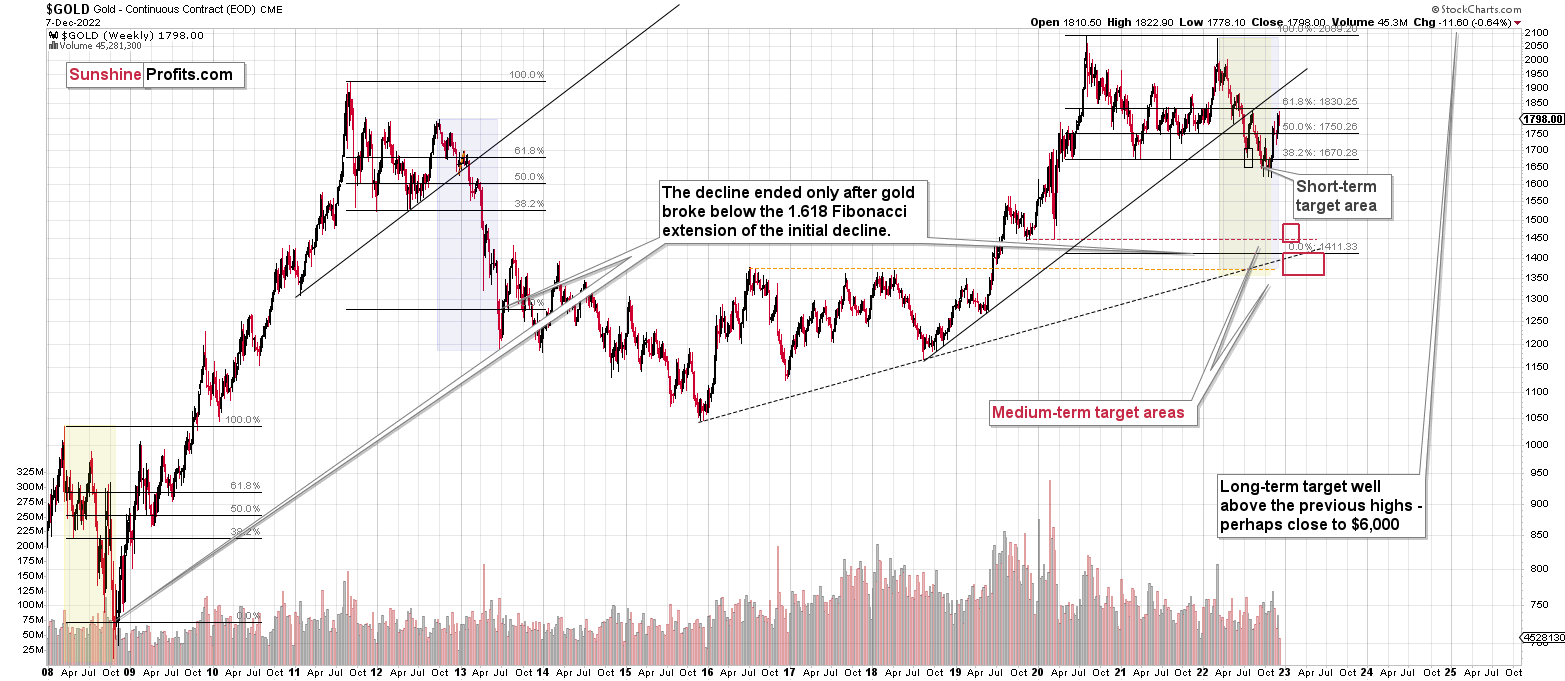

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Letters to the Editor

There are no new letters for today, but I wanted to keep the below reminder in place, just to make sure that everyone had the chance to see it:

Please note that this section is going to go away within the next 1-8 weeks, as you can add comments/questions below the article on Golden Meadow – the platform that we’re using to provide our analyses. Your notification e-mails include an invitation link that allows you to access the “Gold Trading Alerts” space.

The first premium analysis had over 30 comments below it, and once I finish writing this article, I’ll head over to the comments section and catch up on yesterday’s comments.

Also, if you haven’t had the chance to see the video, in which I’m talking about the new platform and why we essentially moved from Sunshine Profits to Golden Meadow, I strongly encourage you to do so:

Summary

Summing up, it seems that the major bottom in the USD Index is in, while the correction in stocks, gold, silver, and mining stocks is over.

The nature of the recent corrections was mostly technical. No market moves up or down in a straight line, and seeing market corrections is rather normal. he reason that markets corrected this time was an incorrect (in my opinion) expectation that the Fed would make a dovish U-turn. The fact that even the positive employment numbers were ignored as a bearish indication of further rate hikes shows the extent of the recent/current irrationality.

However, as the irrationality ends, the medium-term trend is likely to resume. In the case of junior mining stocks, this trend is downward. The latter are likely to decline profoundly based on declines in both gold and the stock market.

In my opinion, the current trading position is going to become profitable in the following weeks, and quite possibly in the following days. And while I can’t promise any kind of performance, I fully expect it to become very profitable before it’s over and to prolong our 2022 winning streak.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Friday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief