Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update. Our most recently featured medium-term outlook remains the same as the price moves align with our expectations (or at least are not really against them). On that account, there are parts of the previous analysis that didn’t change at all in the earlier days and are written in italics.

The key thing that happened this week was that the Bank of Japan hopped on the hawkish train, which caused some turmoil on the markets. While the immediate-term implications were rather erratic, the ultimate implications for the precious metals sector are bearish. Just as when all monetary authorities were printing more and more money, it was bullish for gold, when they are now doing the opposite and increasing interest rates, it’s bearish for gold.

Let’s start today’s analysis with a recap of what recently happened on the fundamental front.

The Weekly Fundamental Roundup

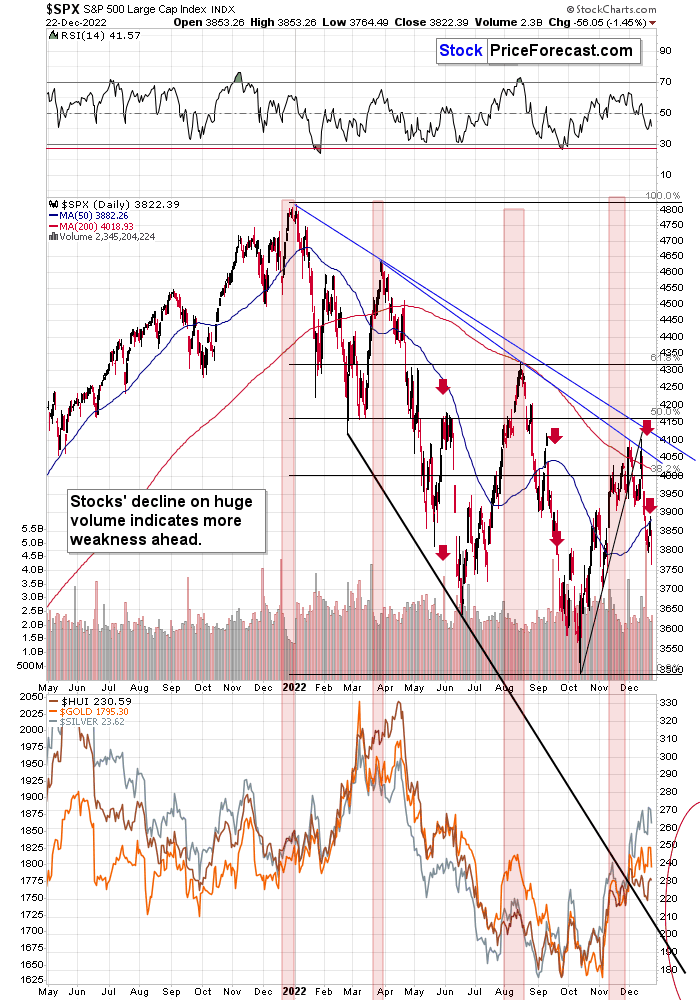

It was a pump-and-dump week for the S&P 500, as rally attempts fizzled and the index was stuck in the red as of the Dec. 22 close. However, gold, silver and mining stocks have outperformed the S&P 500, as the crowd assumes that the PMs are a safe place to hide.

But, the chilling developments that help upend the general stock market should also haunt the metals in the months ahead. With the Fed on a hawkish warpath and evaporating liquidity depressing the outlook for risk assets, cash returns of 4.25%+ reduce the appeal of bullish bets. As a result, while the S&P 500 has noticed, it’s likely a long way down before the ramifications are truly priced in.

Fundamentals Frighten the Gold Bulls

Gold was under heavy pressure on Dec. 22, as a sell-off across U.S. equities helped upend the yellow metal. Moreover, while the negativity should accelerate as the Fed’s inflation fight intensifies in 2023, we warned on Aug. 12 that the bear market had plenty of room to run. We wrote:

While the consensus and the media want you to believe that the bear market is over, their lack of fundamental objectivity highlights why narratives are so destructive. Remember, if normalizing inflation and reducing its balance sheet were so easy, the Fed would have done it already.

Think about it: the Fed was so cautious about tapering its asset purchases that officials waited until inflation was so unanchored that it couldn’t be ignored. But now, the Fed will hike interest rates to 3.4%, sell $95 billion in bonds per month and increase the U.S. unemployment rate to 3.7% (the Fed’s 2022 SEP projections) while the S&P 500 hits new highs? All the while, reducing the YoY headline CPI to 2%, even though it’s never been done since 1954 without the FFR coming within ~50 basis points of the cycle peak. Good luck.

So, with more hawkish data hitting the wire on Dec. 22, the S&P 500 remains on its back foot, and the fundamentals continue to unfold as expected.

Please see below:

Source: Investing.com

Source: Investing.com

To explain, U.S. third-quarter real GDP was revised upward again on Dec. 22, with the metric improving from 2.9% to 3.2%. The official press release stated:

“The ‘third’ estimate of GDP released today is based on more complete source data than were available for the ‘second’ estimate issued last month. In the second estimate, the increase in real GDP was 2.9 percent (…).

“Real GDP turned up in the third quarter, increasing 3.2 percent after decreasing 0.6 percent in the second quarter. The upturn primarily reflected accelerations in nonresidential fixed investment and consumer spending, a smaller decrease in private inventory investment, and upturns in state and local as well as federal government spending that were partly offset by a larger decrease in residential fixed investment. Imports turned down.”

Thus, while the crowd was fretting about a potential recession during the summer, the reality is that resilient inflation and a higher-than-expected U.S. federal funds rate (FFR) are the primary fundamental risks to asset prices.

To that point, the release also showed that the GDP Price Index and the quarterly core Personal Consumption Expenditures (PCE) Index outperformed expectations (shown in the red box above). As such, while we’ve warned repeatedly that inflation should linger for much longer than the consensus realizes, its stubbornness should weigh heavily on the gold price in 2023.

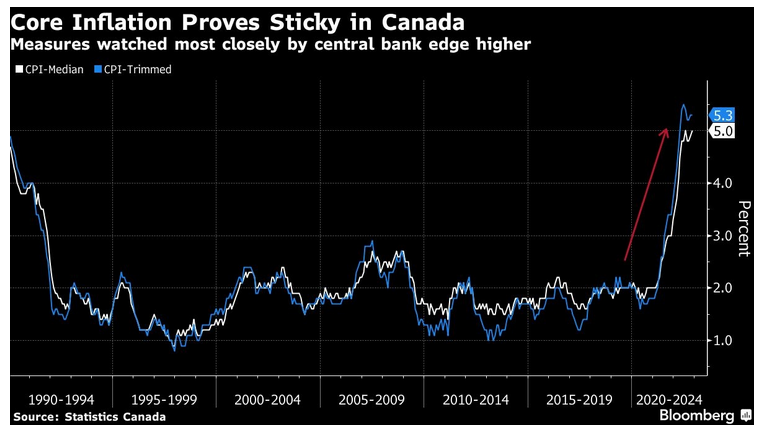

Furthermore, we’ve noted how the U.S. and Canada often have intertwined monetary policies; and with the latter’s Consumer Price Index (CPI) outperforming on Dec. 21, the hawkish ramifications are significantly underestimated.

Please see below:

Source: Investing.com

Source: Investing.com

Likewise, while North American central banks were way off with their “transitory” claims in 2021, the crowd still has faith in their projections. Yet, with inflation not cooperating, interest rates should rise materially before it’s all said and done.

Please see below:

To explain, the white and blue lines above track the year-over-year (YoY) percentage changes in the Canadian median and trimmed CPIs. For context, both are adjusted metrics that use items near the 50th percentile of the CPI basket.

If you analyze the right side of the chart, you can see that both are near 30+-year highs, and they re-accelerated in November, which highlights the challenging nature of inflation. In a nutshell: history shows that inflation tends to jump around after becoming unanchored, which contrasts the consensus belief in a smooth glide lower.

Therefore, with the crowd highly uninformed about the economic weakness required to normalize inflation, more bouts of panic should confront the financial markets in the months ahead.

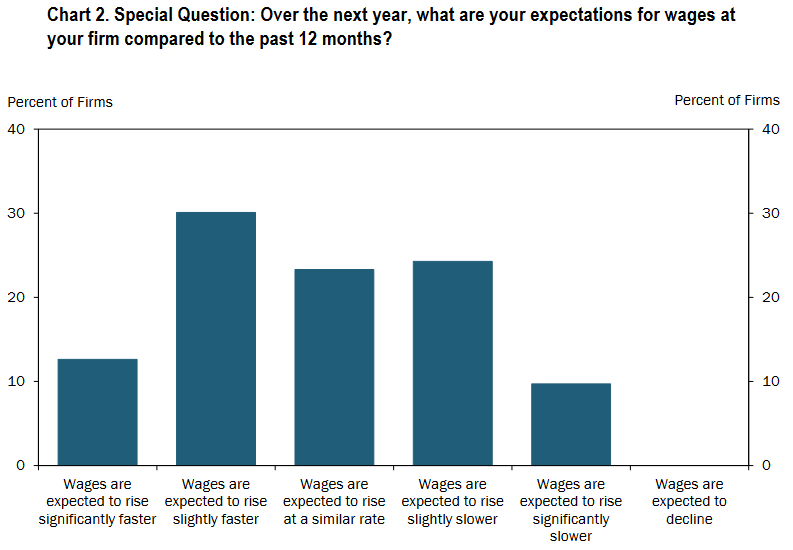

In addition, the Kansas City (KC) Fed released its Tenth District Manufacturing Activity Survey on Dec. 22. The headline index declined from -6 in November to -9 in December, while “the monthly employment index fell from 3 to 0, its lowest level since 2020 but still indicative of flat employment for the month.”

More importantly, this month’s “special questions” revealed:

“In December, 43% of firms expected wages to rise faster compared to the past 12 months, while 23% of firms expected wages to rise at a similar rate and 35% of firms expected wages to rise more slowly.”

Please see below:

Source: KC Fed

Source: KC Fed

To explain, the three blue bars furthest to the left show that 66% of KC manufacturing firms expect wages to increase significantly faster, faster, or in line with the current data, and the results are profoundly bullish for the FFR.

Moreover, notice how no respondents said that “wages are expected to decline?” This is highly inflationary. For context, we wrote on Dec. 21:

Wage inflation is the canary in the coal mine because Americans can afford price increases that much their salary increases; and if wages are running at 5%+, Americans can afford 5%+ output inflation. Consequently, the U.S. labor market imbalance does not support a 2% inflation rate anytime soon.

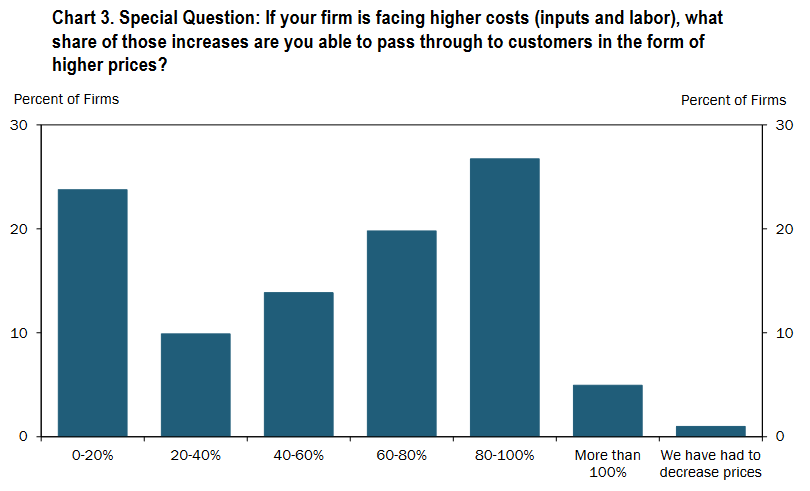

Continuing the theme, the KC Fed report also noted:

“About 27% of all firms facing higher costs (inputs and labor) were able to pass through 80 to 100% of increased costs, while a quarter of firms could only pass through 0 to 20%.”

Please see below:

Source: KC Fed

Source: KC Fed

To explain, the blue bars in the middle show that roughly 65% of KC manufacturing firms are passing through 40% to 100%+ of their inflationary input costs. Thus, demand destruction has not materialized despite the FFR’s rapid rise in 2022, and the crowd is ignoring history at their own peril.

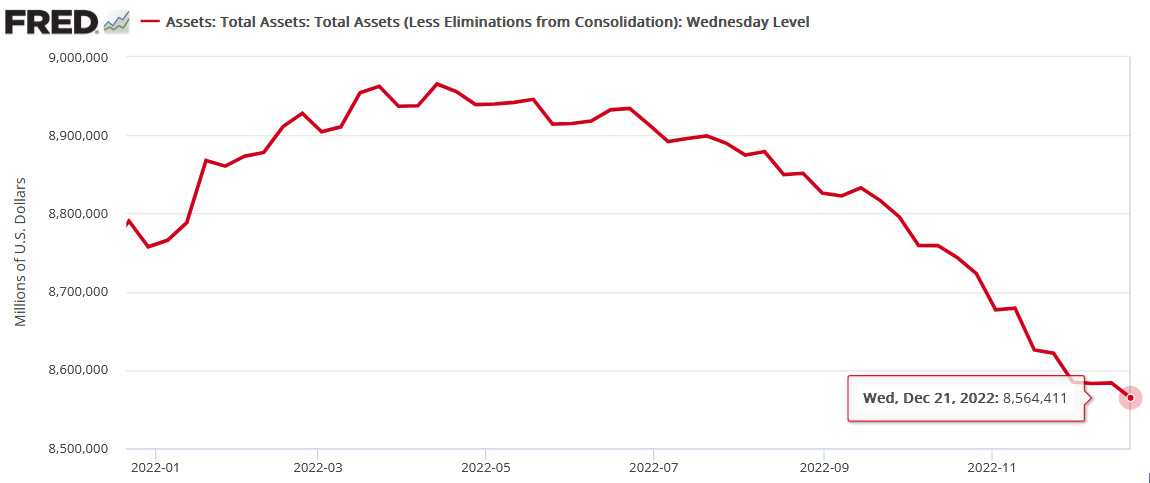

Finally, the second piece of the liquidity puzzle surrounds quantitative tightening (QT); and with the Fed’s balance sheet hitting a new 2022 low on Dec. 21 (updated on Dec. 22), gold is severely mispriced given the fundamental backdrop that should arise in 2023.

Overall, the gold price suffered mightily on Dec. 22, though, despite the sharp sell-off, it’s still materially overvalued. Furthermore, the U.S. 10-Year real yield hit a new monthly high of 1.48%, which is a 40 basis point increase from its Dec. 2 close. As such, we expect considerable downside for the PMs in 2023.

Fear Grips the S&P 500 and Silver

With fear making a slight comeback on Dec. 22, silver couldn’t escape the negativity; and while we’ve highlighted the depressed behavior of the Cboe Volatility Index (VIX), the metric rose by more than 9%.

Yet, the dip buyers helped the S&P 500 close well off its intraday lows, and the VIX closed well off its intraday highs, meaning the crowd still hopes to orchestrate a Santa Clause rally. But, with the bearish fundamentals creating a crisis of confidence, we warned on Oct. 26 that the bulls were throwing good money at a bad investment. We wrote:

With two of the four largest companies in the S&P 500 suffering, the squeeze may have already run its course. Moreover, while positioning is still heavily short, the index offered tactical value near 3,600, not 3,850.

In addition, with the bearish medium-term fundamentals rearing their ugly head, and the Fed poised to raise interest rates by 75 basis points next week, stocks offer a poor risk-reward proposition when the FFR should hit 4%.

Thus, with the S&P 500 ending the Dec. 22 session at ~3,822, the dip buyers are now in the red and cash is king. Likewise, market participants’ inflation optimism is misguided, and the recent data and a hawkish FOMC have suppressed investor sentiment.

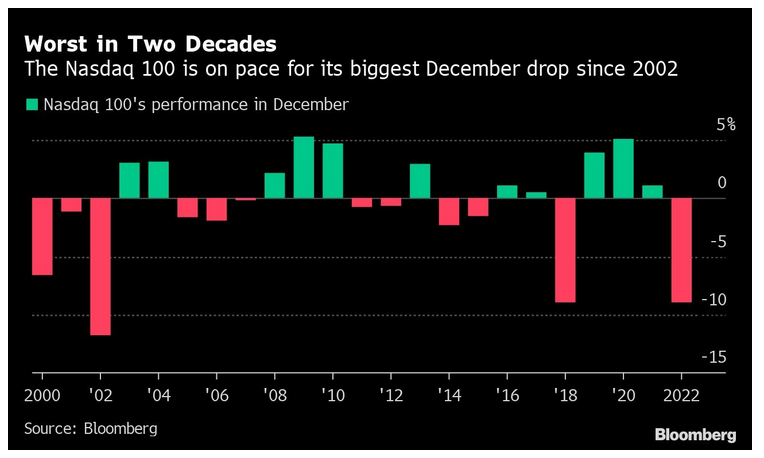

Please see below:

To explain, the red and green bars above track the NASDAQ 100’s December performance from 2000 until now. If you analyze the right side of the chart, you can see that the index is on track for its “biggest December drop since 2002.” As a result, the liquidity beneficiates have been taken to the woodshed.

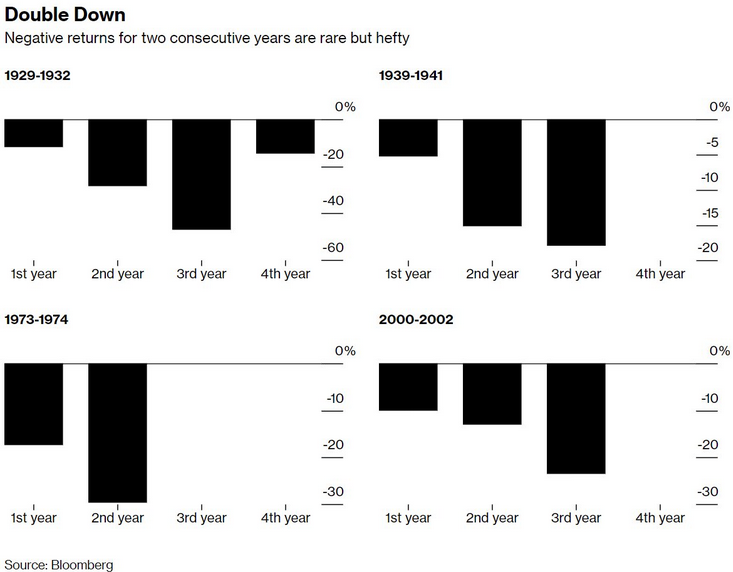

More importantly, while the stock market bulls highlight how down years often don’t repeat (which is true), periods with major fundamental imbalances (like this one) don’t follow that roadmap.

Please see below:

To explain, the charts above show how consecutive years of negative S&P 500 returns are rare but highly damaging. If you analyze the chart at the bottom left, 1973-1974 rivals the current environment because the fundamental backdrops are so similar.

With unanchored inflation forcing the FFR much higher in 1973-1974 (and it was still rising during the recession), the S&P 500 declined dramatically before a sustainable rally unfolded; and with the Fed far from solving its inflation conundrum, strength should be sold until the S&P 500 reflects its fundamental value.

To that point, billionaire hedge fund manager David Tepper said on Dec. 22:

“I’m leaning short on the equity markets. I think the upside/downside just doesn’t make sense to me when I have so many central banks telling me what they are going to do. This is a tough level [for the S&P 500] to talk about robust returns.”

He added:

“Why are we still putting these high multiples like when we had 1% rates? I have to put multiples that are realistic to the market.”

Furthermore, while we’ve warned that the FFR should continue its ascent in the months ahead, Tepper said, “I think [the Fed is] worried about that inflation rate that’s going to be stubborn at 3.5%, 3.75%, 4%.”

As such, he also expects higher short-term interest rates in 2023.

Please see below:

Source: CNBC

Source: CNBC

So, while the white metal has dismissed many of these issues, the fundamental problems that confront the S&P 500 should come for silver in 2023: higher interest rates, QT and a likely recession that has Morgan Stanley predicting a ~20% drop in S&P 500 earnings per share (EPS) are highly bearish for silver. Remember, financial markets are interconnected, and tremors in one market often shake others.

Therefore, with little economic damage unfolding in 2022, outside of lower commodity prices and a weaker U.S. housing market, we believe risk assets have a lot more downside in 2023 before their final lows are reached.

The Bottom Line

While reality has returned to the general stock market, gold, silver and mining stocks remain in la-la land. In a nutshell: they assume that the myriad of problems confronting the S&P 500 doesn’t apply to them. However, that belief is short-sighted, and the PMs (especially silver and mining stocks) endure epic drops when panic-induced liquidations unfold. Thus, while inflation and interest rate shocks dominated in 2022, a recession shock should hit in 2023.

In conclusion, the PMs declined on Dec. 22, as the USD Index and the U.S. 10-Year real yield rallied. But, while the metals prioritize the former’s consolidation over the latter’s monthly surge, we expect both metrics to hit new highs over the medium term, and a realization is profoundly bearish for the PMs.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Dec. 27: Dallas Fed manufacturing index

The Fed’s regional PMIs are puzzle pieces that help create the whole jigsaw, so the growth, inflation and employment results are important to monitor.

- Dec. 28: Richmond Fed manufacturing and services indexes, Dallas Fed services index

Adding more color, the Richmond and Dallas Fed’s surveys will provide more insight into the fundamental backdrop.

- Dec. 30: Chicago PMI

Rounding out the final week of 2022, the ISM will detail the economic findings in Illinois.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

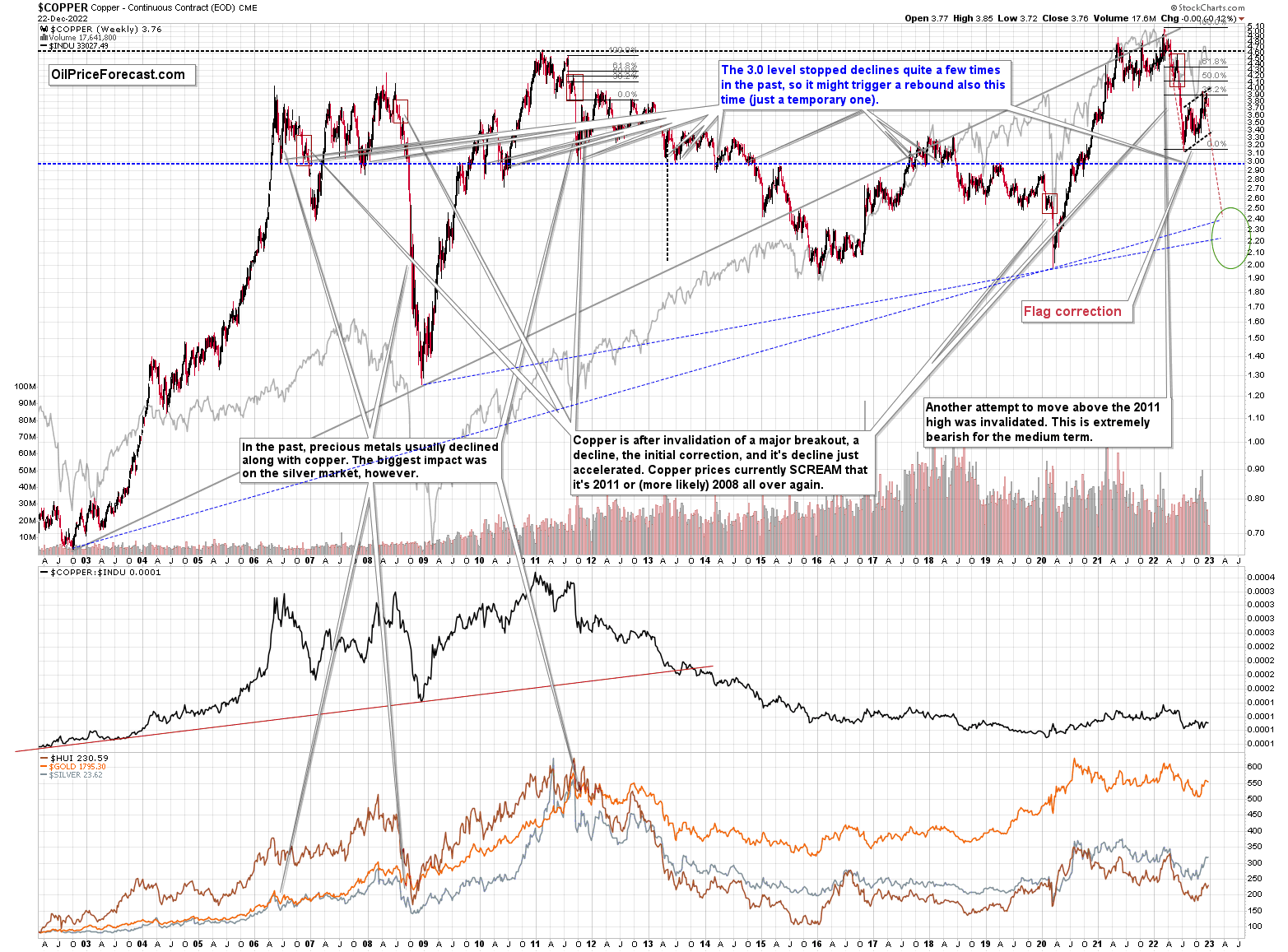

Let’s start today’s technical discussion with a quick check of copper prices.

Overall, everything I wrote about it last week remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

No market moves up or down in a straight line (well, the 2008 slide appears to have been an exception), and a short-term correction doesn’t necessarily invalidate the bigger trend. For the last couple of months, copper has been trading sideways, but it didn’t change much regarding the outlook.

In fact, it made my previous target area even more likely. You see, the consolidation patterns are often followed by a move that’s similar to the move that preceded them. In this case, the previous 2022 decline was quite significant, and if it is repeated, one can expect copper to decline well below 3.

Actually, copper could decline profoundly and bottom in the $2.0-2.4 area. That’s where we have rising, long-term support lines and also the previous – 2016 and 2020 – lows.

Flag patterns (which we just saw in copper) tend to be followed by price moves that are similar to ones that preceded them. I marked this on the above chart with red, dashed lines. This method supports a copper price’s move to around $2.4.

Given the recent flag pattern and the size of the previous decline (and its pace), it seems quite likely that it could take another 2-7 months for copper to move to about $2.4. Late March / early April seem the most likely time target given the current data.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after invalidation of a major breakout, a decline, and a correction. Copper prices currently SCREAM that it’s a variation of 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

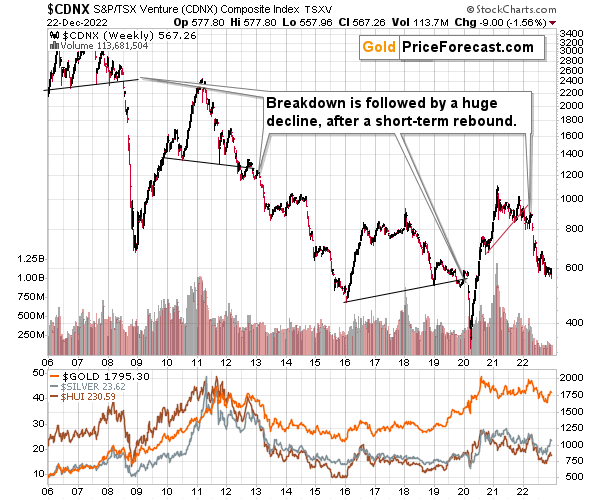

Having said that, let’s check junior miners’ really big picture.

I previously commented on the above chart in the following way:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

Just like it was the case in 2008, the move higher that we saw before the final (biggest) slide in gold, silver, and gold stocks (lower part of the chart), we didn’t see a visible rally in the TSX Venture Index. Just as the index paused back then, it paused right now.

Currently, it’s trading at about 600, and back then, it consolidated at about 2500. The price levels are different, but the overall shape of the price moves (lack thereof) is similar. This serves as a signal, that the recent upswing in the PMs was not to be trusted.

The above is one of the weakest (from the technical point of view) charts that is see across the board right now. There is a strong long-term downtrend visible in the TSX Venture Index, and if stocks slide similarly as they did in 2008, the TSXV could truly plunge – perhaps even to the 300 level or lower.

The important short-term detail is that the TSXV just broke to new yearly lows. This is a major (yet barely noticed by most) indication that the next big move lower is about to start.

Having said that, let’s turn to gold.

Let’s start with context:

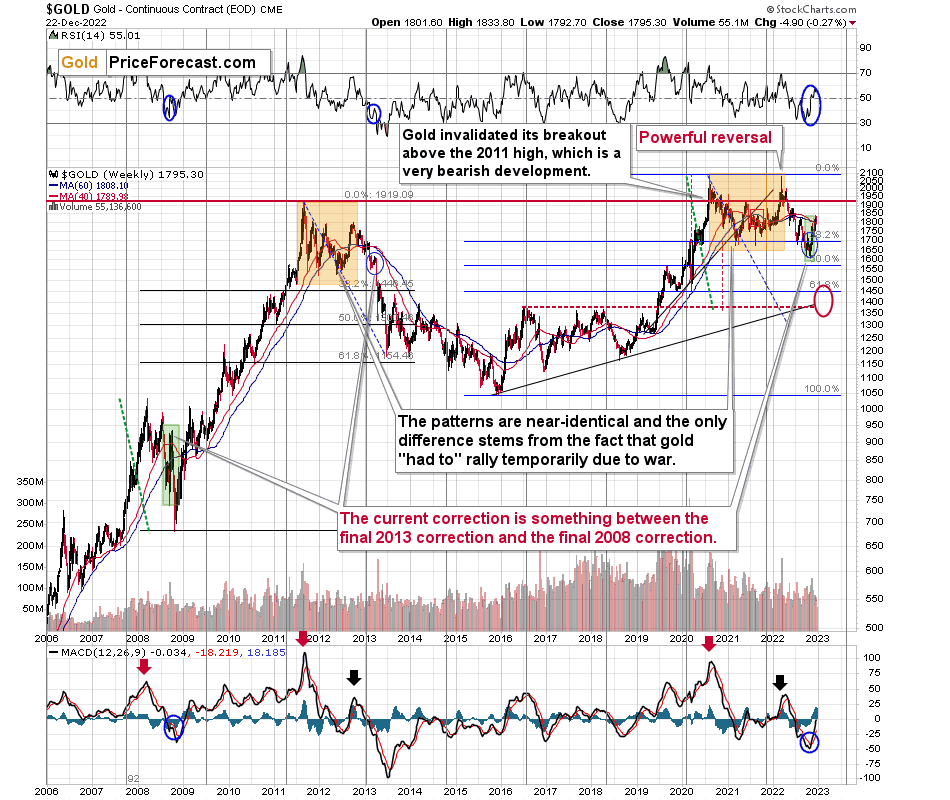

Between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet gold failed to rally to new highs.

In fact, it’s trading very close to its 2011 high, which tells you something about the strength of this market. It’s almost absent.

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. We can also spot similarities between now and 2008. The long-term gold price chart below provides details.

Looking at the gold market from a broader point of view, the corrective upswing that we saw recently is something between what we saw in 2013 and what we saw in 2008.

The recent move higher was bigger than what we saw in 2013 but smaller than what we saw in 2008. And so far this week, gold is down by a few dollars, so nothing really changed.

No wonder – the current situation in general is similar to both. In fact, that’s why I’ve been writing about this dual similarity for many months now.

Back in 2013, the final of the pre-slide corrective upswings ended with gold below its 40- and 60- week moving averages (marked with red and blue, respectively).

Back in 2008, the final of the pre-slide corrective upswings took gold visibly above both above-mentioned moving averages.

And now? We saw a move above both moving averages, but only a bit above them – the move was not as profound as the one that we saw in 2008.

The most interesting thing about the above is that when gold did finally move above those moving averages in 2008, it meant that the rally was practically over and that it was the perfect time to be shorting the precious metals market – especially mining stocks.

Now, as far as the link to 2013 is concerned, it remains perfectly intact, with the additional note that the final corrective upswing is bigger this time – more like what we saw in 2008.

Gold is sometimes forced to react to some geo-political events as the safe-haven buying kicks in, but these moves are usually short-term lived. Looking at long-term charts helps to keep things in proper perspective.

Consequently, my previous comments remain up-to-date:

Based on the above chart, it’s quite clear that the situation that is now being repeated. The patterns marked with orange rectangles and blue ellipses are almost identical (also in the MACD indicator, and to a lesser extent in the RSI indicator).

Sure, the situations are not identical, as this time we had a Russian invasion of Ukraine that pushed gold temporarily higher. Other than that, the situations are extremely similar.

Based on the stage of the self-similarity and the confirmed breakdown below the $1,700 level, gold is now likely to slide.

Based on the analogy to 2013, it’s not only likely to slide, it’s likely to slide profoundly in a sharp manner. These may be the last days or hours before the slide fully begins.

How low is gold likely to go during this upcoming big medium-term decline? Perhaps as low as its 2020 low, around $1,450-1,500. Then, after a rebound, quite likely to be at or slightly below $1,400.

I realize this is far from the current price, but nonetheless, this target area appears justified in my opinion. There are two important Fibonacci retracements based on the 2015-2020 rally that gold can bounce from (it recently bounced from the 38.2% retracement). These are 50% and 61.8% retracements.

The support provided by the 61.8% retracement is strengthened by the 2020 low and the support provided by the 50% retracement is strengthened by the 2019 high.

However, based on gold’s self-similarity to 2013, it seems that we’re about to see a slide that’s bigger than what we’ve been seeing so far this year. This time – based on the similarity – gold is likely to decline profoundly, but no longer in the back-and-forth mode. If gold formed its next local low at the 50% retracement (so at about $1,560), then it might do so still within the declining, short-term trend channel (sometime in September).

However, if gold is to stick to the link to 2013, then it should decline more rapidly. In this case, the technique that can help us estimate the short-term target is the one that says that after a breakdown from a trend channel, price is likely to move approximately by as much as the height of the previous trend channel. In this case, gold could break below the trend channel soon and then decline even more. Based on the height of the trend channel, the above means that a move to the 61.8% retracement as the next downside target is more likely than a move to the 50% retracement.

I previously wrote that the above-mentioned decline in gold would likely be linked to a breakdown in the EUR/USD below 1, and we already saw both: decline in gold, and a breakdown in the EUR/USD below 1. The implications remain bearish.

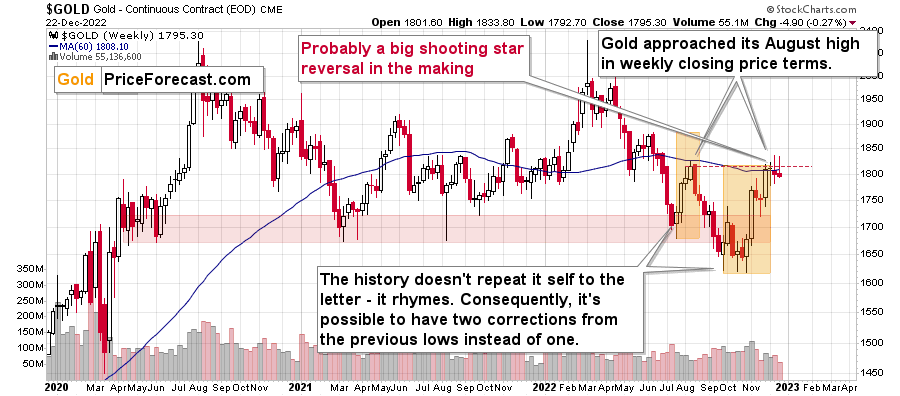

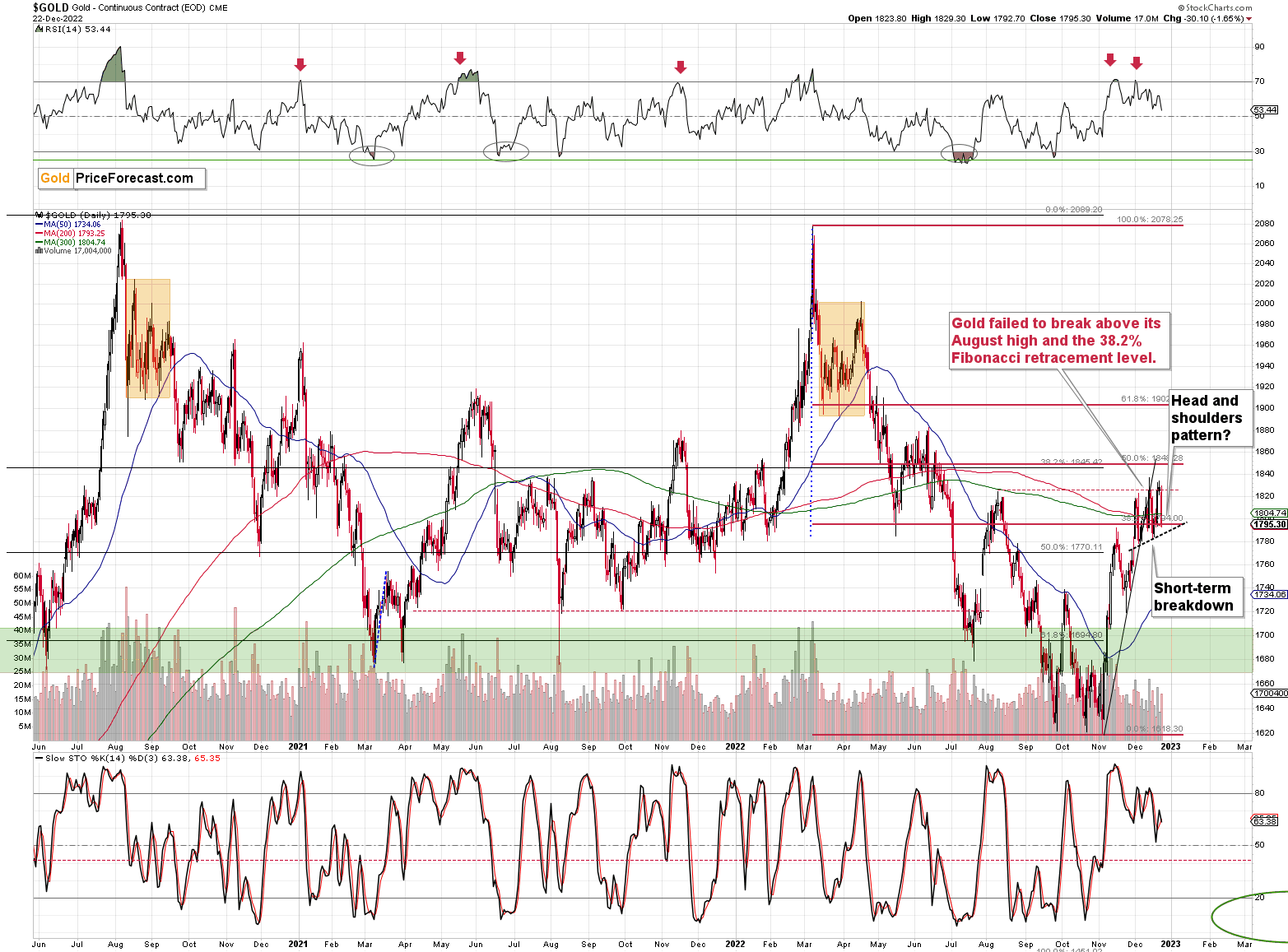

Having said that, let’s zoom in to see gold’s short-term price moves.

Gold’s rally was just stopped by the resistance provided by its previous high and its 60-week moving average. Will gold now reverse?

The above chart features gold price in terms of weekly candlesticks. As you can see, it just approached its August high.

And gold failed to move above it once again.

The resistance held.

What is even more bearish is the fact that gold is likely about to form another weekly shooting star (reversal) candlestick, the second in a row. “Likely,” because the week is not over yet.

This is a very powerful bearish indication, especially that it has now been repeated.

Given today’s pre-market moves in gold and silver (both are up just slightly, with gold trading below $1,800), it seems that the reversal candlestick will soon be a fact.

This – along with the failed attempt to move above the August high – has profoundly bearish implications for the following weeks.

Gold, just like many other markets (i.e., stock prices), recently corrected slightly more than 38.2% of its previous move. Then it invalidated this small breakout. It happened more than once, so this bearish indication was strengthened.

The same goes for gold’s attempt to move above its August high – the one that failed. It too strengthened the bearish case for the following weeks.

Please note that the above is taking place shortly after two sell signals from the RSI indicator, which further confirms the bearish nature of the recent price moves.

Gold’s breakdown below the rising, short-term, black support line makes the short-term outlook even more bearish.

And now, based on this week’s failed attempt to rally once again, gold is likely to form a head and shoulders top pattern. For now, this formation is just potential, as we’ll need to see a confirmed breakdown below the neck level (dashed, black line) first.

Given rising real interest rates and the USD Index that has likely formed its medium-term bottom, the foregoing is very likely. Having said that, let’s take a closer look at the silver market.

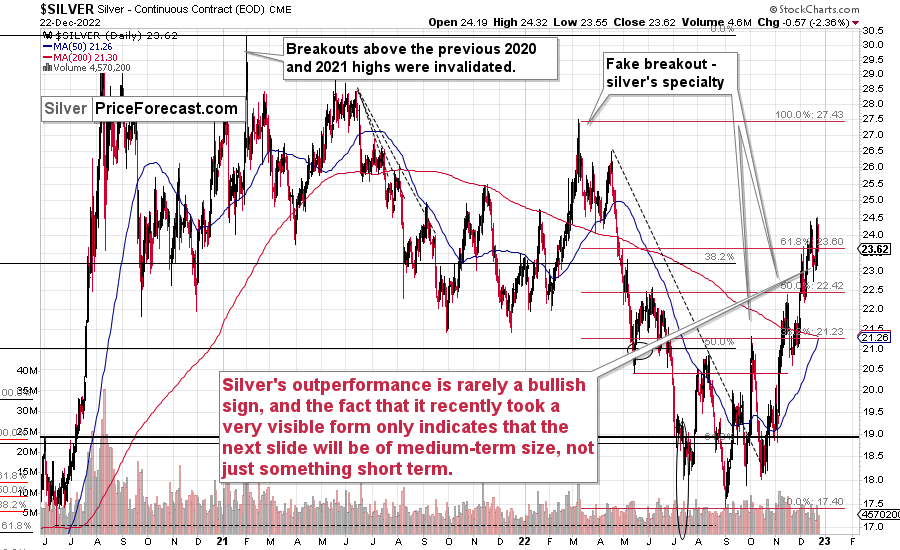

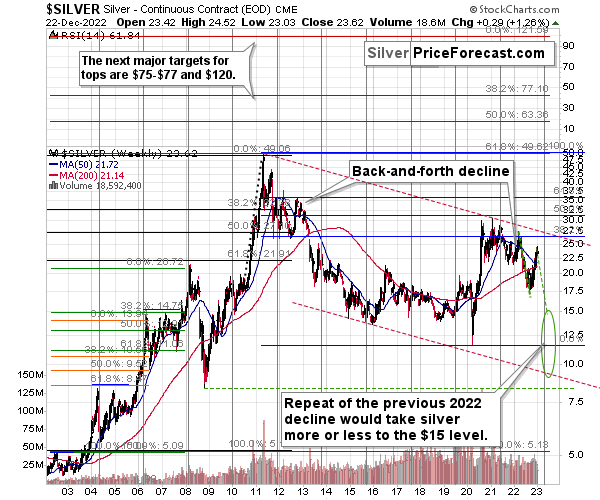

Please note how silver recently outperformed ecently. While gold just topped below its recent short-term high, silver moved slightly above it.

As I emphasized many times before, silver's outperformance is rarely a bullish sign, and the fact that it recently took a very visible form only indicates that the next slide will be of medium-term size, not just something short-term.

Silver recently invalidated its temporary breakout above the 61.8% Fibonacci retracement, and it seems that it’s about to do it again.

Yes, that’s a retracement that’s higher than the analogous ones in stocks, gold, and mining stocks, and… This is yet another confirmation of silver’s short-term strength.

Once again – it’s not something bullish but very likely something bearish.

This means that the recent sizable rally is nothing more than a – sizable, but still – correction within a bigger downtrend.

Looking at silver from a long-term point of view helps to see the forest, not just individual trees.

When looking at silver from a long-term point of view, it’s still obvious that the recent move higher was most likely just a corrective upswing.

What happens after corrections are over (as indicated by, i.e., silver’s outperformance)? The previous trend resumes. The previous trend was down, so that’s where silver is likely headed next.

Besides, the long-term turning point for silver is due in several months, and if silver repeats its previous 2022 decline, then it will bottom close to the turning point and also close to the $15 level– in the first half of 2023.

It’s likely to repeat its previous 2022, because that’s what tends to happen after flag patterns, and what you see on silver’s short-term chart between September and yesterday appears to be a flag pattern.

However, will silver only repeat its previous 2022 performance and not decline more than it already has?

Based on the analogies to 2008 and 2013, the latter is more likely. The 2013 slide was bigger than the initial decline that we saw in 2012. And the final 2008 slide was WAY bigger than what we saw before it.

Due to its industrial uses, silver is known to move more than gold, in particular when the stock market is moving in the same way as gold does. Since I think that gold and stocks are both likely to slide, silver is indeed likely to decline in a truly profound manner. Quite likely lower than just $15.

Consequently, my prediction for silver prices remains bearish, as does the outlook for the rest of the precious metals sector.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

Having said that, let’s take a look at what happened in mining stocks.

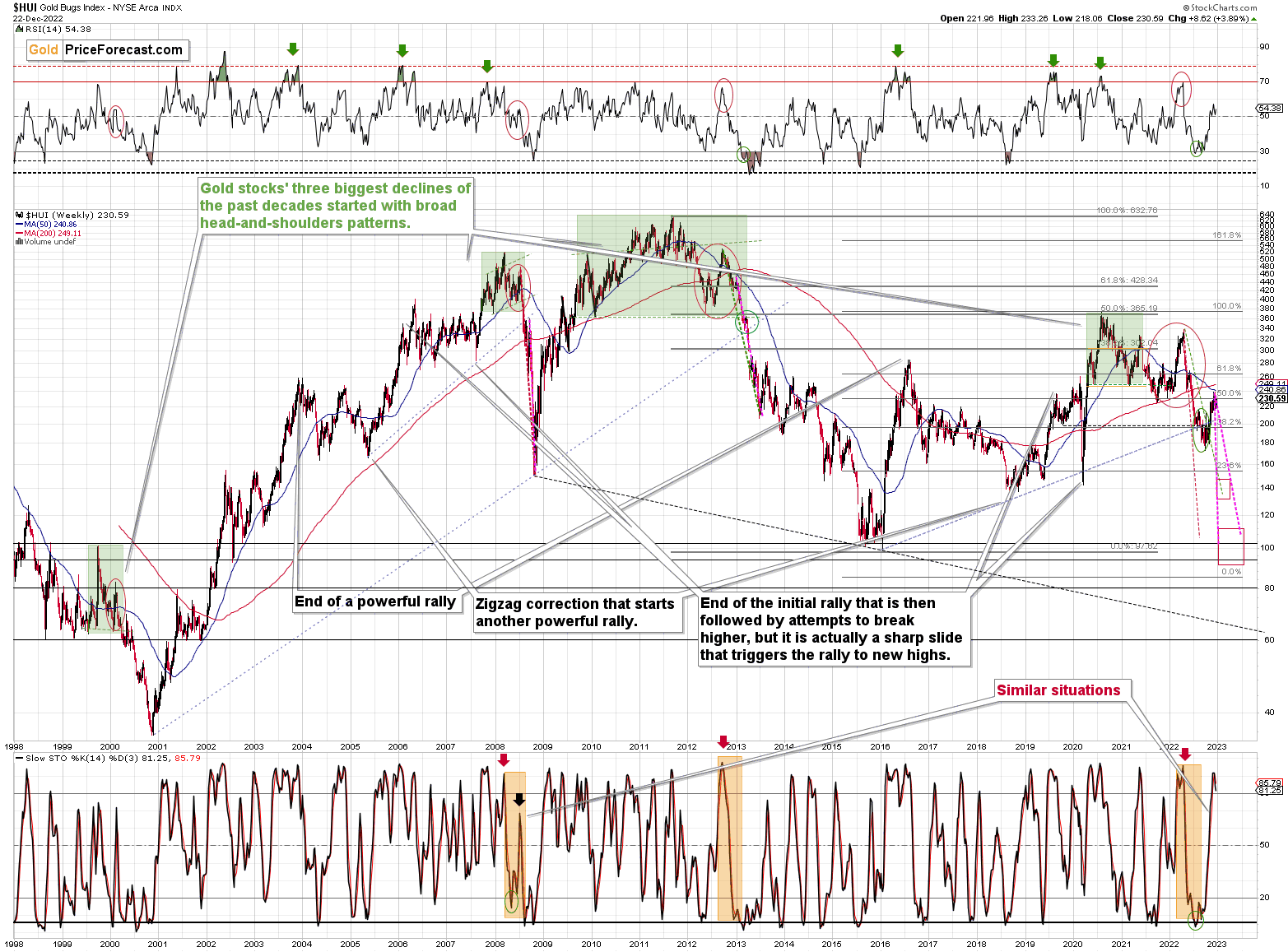

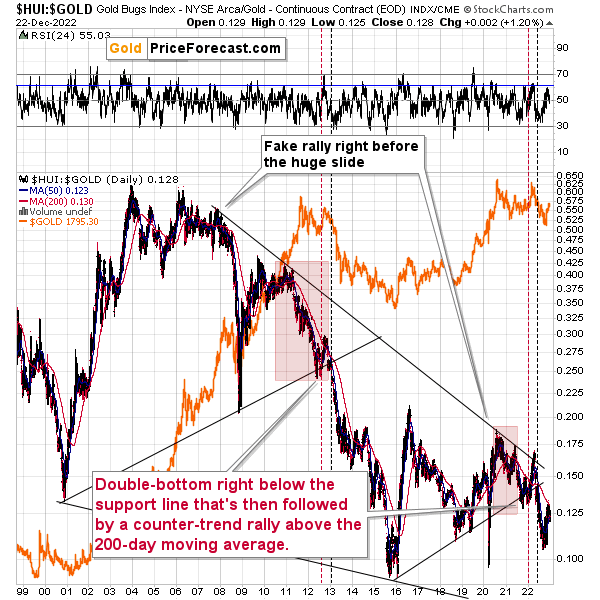

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

For example, right now, gold stocks are declining similarly to how they did in 2008 and in 2012-2013.

As gold was practically forced to rally recently based on geopolitical events, news, and rumors (i.a. false hope for Fed’s dovish U-turn), so were gold stocks.

Did it change anything technically?

Only a bit, and only at first sight.

The HUI Index is a bit above its rising resistance line, but it’s trading there after it already verified a breakdown below this line.

Because the nature of the rally appears to be temporary, not only based on the analogy to 2013, but also on recent fundamental developments, I doubt that the breakout will be confirmed (as was the case with gold's short-term breakout above the 38.2% Fibonacci retracement). Please take a look at the stochastic indicator’s performance in the bottom part of the above chart. It’s currently doing practically the same thing that it did in 2008. And that – in 2008 – marked the final counter-trend top before the biggest part of the slide.

Is this time different? Those are expensive words on Wall Street.

I highlighted and copied the sharpest and final parts of the medium-term declines (2008 and 2013) to the current situation. There are quite a few other markings on the above chart, but the ones that I just mentioned are marked with the magenta color.

The analogy to 2008 points to the end of this year as being the likely moment for the final bottom.

The analogy to 2013 points to the middle of 2023 as being the likely moment for the final bottom.

The current situation is somewhat similar for both. However, it seems that what started as a primarily 2013-like move lower is becoming a 2008-like move lower. That’s based i.a. on the volatility of the recent upswing.

So, on average, early 2023 seems like a quite likely target for the final bottom.

Then again, please note that the two analogies fit right into my previous target area for the final bottom, so this target area simply remains intact.

Actually, based on both of the above, it seems that a move to 2020 lows close to the end of this year and then a correction followed by a move even lower in 2023 appear to be quite likely outcomes at this time.

How low can the HUI Index fall during the next big downswing?

As it’s the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 100-150 is my current target area for the upcoming slide in the HUI Index.

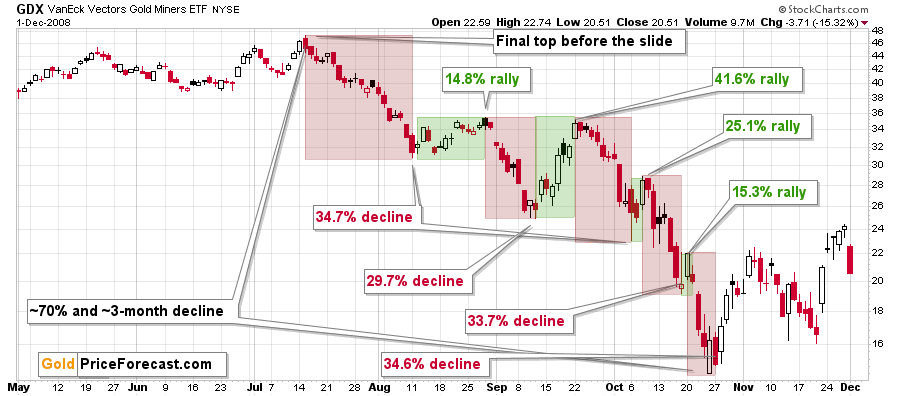

All right, let’s zoom in and see how mining stocks declined in 2008.

Back then, the GDXJ ETF was not yet trading, so I’m using the GDX ETF as a short-term proxy here.

The decline took about 3 months, and it erased about 70% of the miners’ value. The biggest part of the decline happened in the final month, though.

However, the really interesting thing about that decline – that might also be very useful this time – is that there were five very short-term declines that took the GDX about 30% lower.

I marked those declines with red rectangles. After that, a corrective upswing started. During those corrective upswings, the GDX rallied by 14.8-41.6%.

Do you know now much the GDX ETF rallied from its September 2022 bottom? It moved up by 40.7%. This means that the move higher now is practically identical with the corrective (!) upswing that we saw in September 2008. The analogy was not broken – it remains intact, and it points to much lower prices in the future.

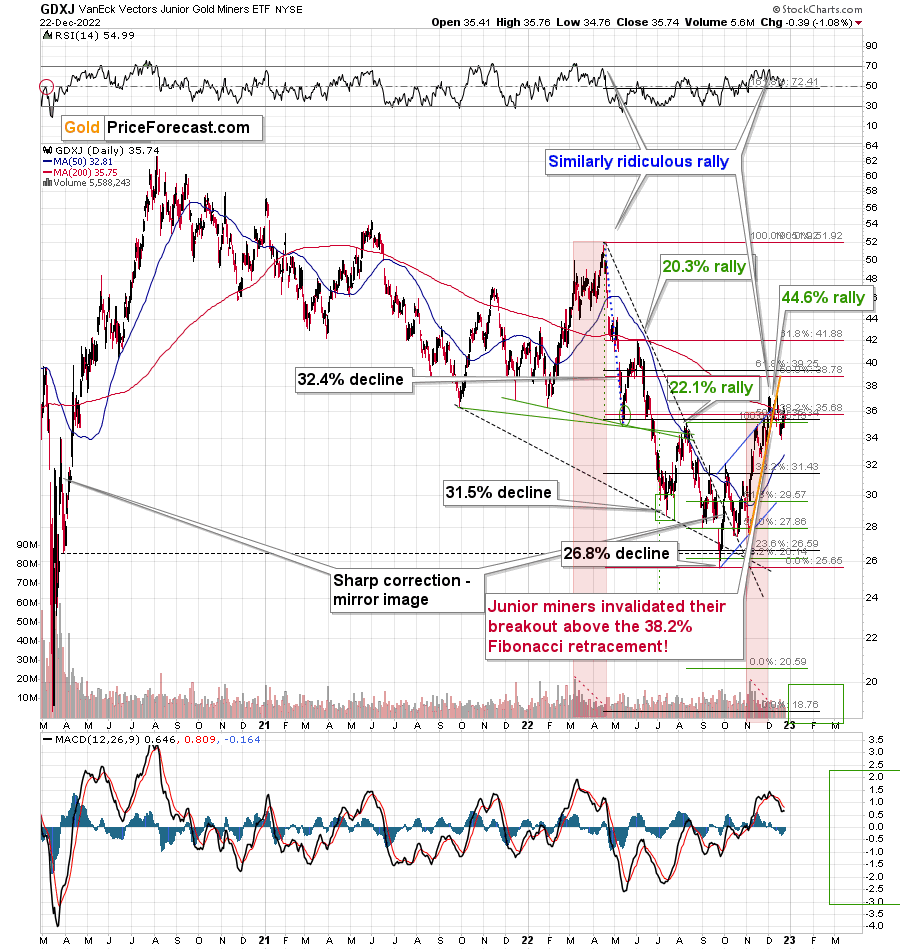

Just like gold, the GDXJ invalidated the breakout above its 38.2% Fibonacci retracement and few times, and now it also broke below the rising, short-term support line (marked with orange).

This is a powerful, bearish combination of factors, especially that miners were the first to decline – gold followed, while silver was still showing strength.

Please keep in mind that the above comes on top of the analogy that I marked with red rectangles, and my previous description thereof remains up-to-date:

The current upswing continues to be similar to what we saw in March and April, earlier this year. On the above chart I named both rallies “ridiculous” – I did so as what we see now is against that’s happening in the real interest rates, and it appears that it’s the general public that’s pushing the prices higher now.

Technically, one could say that the GDXJ formed an inverse head and shoulders pattern (the early September bottom being the left shoulder and the mid-October bottom being the right shoulder), which was just completed.

Just as the March – April rally ran its course on declining volume, we saw the same thing recently. Even the RSI was slightly below 70 at the April top, just like it was the case very recently.

Speaking of analogies, I previously wrote that the current rally is a mirror image (it’s not a crystal-clear mirror, though) of the corrective decline that we saw in late-March 2020. As it turned out, due to the most recent part of the upswing, the size of both moves became even more aligned.

And yes, this means that another decline could take the GDXJ all the way down to its 2020 low, or very close to it.

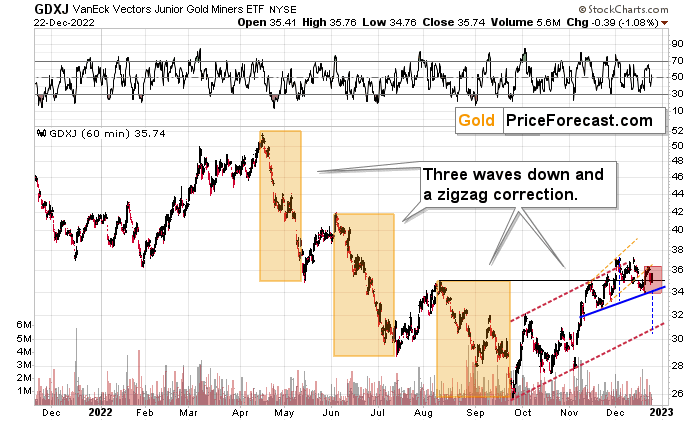

On the below chart, I marked just how perfectly the recent price moves played out according to the Elliott Wave Theory.

Of course, EWT is not the only tool that one could use, and I find other technical tools more useful, but still, this kind of pattern-following is uncanny.

The classic EWT pattern is three waves down (I marked those with orange rectangles) and then a correction consisting of two smaller waves.

That’s exactly what we have seen in recent months. The September–now pattern appears to be the above-mentioned correction. It didn’t only consist of two smaller waves higher – they were actually almost identical in terms of size and sharpness. This created a classic ABC correction (flag) pattern.

Three weeks ago, I wrote that the Dec. 1 small breakout above the upper red line didn’t have meaningful bullish implications as it hadn’t been confirmed. And indeed, it was invalidated.

Now, since this pattern is complete, another huge 3-stage move lower can – and is likely – to unfold. This is very bearish for junior mining stocks (as well as for gold, silver, and probably other commodities and stocks), and the fact that juniors are already showing weakness relative to gold (the latter was almost flat yesterday, while miners declined) serves as a bearish confirmation. As always, I can’t guarantee anything, but in my view, the profits that can be reaped on this upcoming slide can be enormous.

Also, this week’s move up in junior miners is not a bullish thing, either.

First of all, they haven’t moved above the lower border of the accelerated trend channel (marked with orange). This means that this week’s upswing was likely just a verification of the breakdown below it.

Second, if we see a decline soon, which seems likely, it could become the right shoulder of a potential head-and-shoulders pattern. I marked the theoretical right shoulder with a red rectangle and the neck level with a blue rectangle. In short, when we see a confirmed breakdown below $34 in the GDXJ, we’re likely to see a move even lower – to $30.5 or so. Then, I’d expect to see something similar to what we saw in August, earlier this year – a small correction that is followed by another decline.

This time, however, I think that the medium-term decline will be much bigger than what we saw in the middle of the year. This is based not just on the bullish medium-term outlook for the USD Index but also on the analogies in gold price, silver price, and precious metals mining stocks: to 2013 and 2008. It seems that the history is rhyming, and the correction right before the biggest slide appears to be over or about to be over.

Yesterday’s (Dec. 22) relatively weak decline is not yet a sign of strength either – miners have recently underperformed gold, so what we saw yesterday might have simply been a daily breather in this relative underperformance.

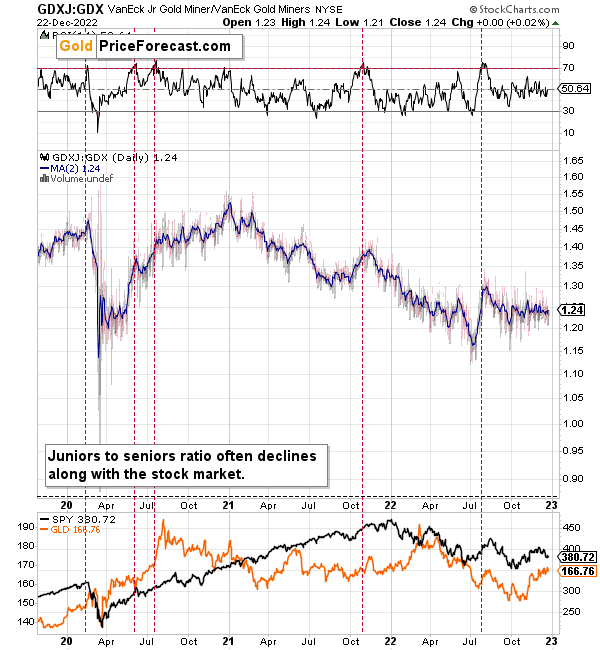

Meanwhile, the relative performance of junior miners compared to senior miners continues to deteriorate in a medium-term trend.

During this quick upswing, juniors rallied relative to seniors, but this is just a very short-term move that’s within a short-, and medium-term downtrends.

This implies bigger declines in the GDXJ in the future.

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw at the 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI to gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

Recently, we saw a quick upswing in the ratio, but that’s not a game-changer – even the biggest declines had corrections in the past.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices of gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks) and that’s exactly what’s likely to happen.

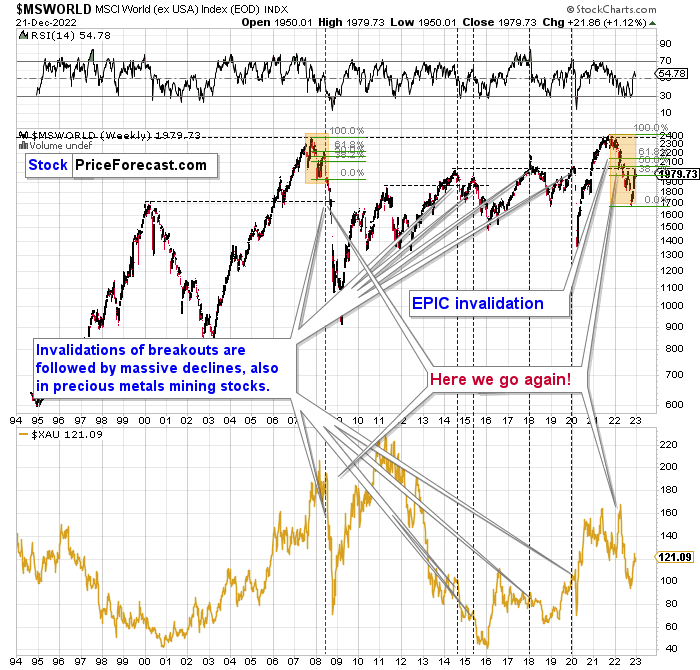

Just like what we saw in the case of copper, gold, and mining stocks, world stocks corrected about 38.2% of their preceding decline.

And recently, they corrected a bit more – almost half of the preceding decline.

Please note that the initial decline was now bigger than what we saw in 2008. Back then, stocks corrected about 61.8% of their initial decline before tumbling. If stocks are not able to do the same thing now – and they might not be – then the following slide could be even bigger than what we saw in 2008. Naturally, this would be profoundly bearish for junior mining stocks.

This means that nothing really changed, and the situation remains extremely bearish based, i.e., on the analogy to what we saw after previous invalidations of long-term breakouts.

As a reminder, in early 2022, I wrote that the situation was very bearish as invalidations of previous breakouts were usually followed by massive declines – not just in stocks but also in precious metals.

When stocks invalidated their 2006 breakout in 2008, their prices truly crumbled.

We also saw that on a smaller scale in 2014, 2015, and early 2018.

We’re seeing it right now.

To clarify, we’re actually seeing the aftermath of the invalidation. The huge decline is already taking place.

The difference between now and 2008 is that back then the slide was more volatile, and we didn’t really see a visible correction during the plunge. This time, the decline is more measured, and we saw a correction to one of the most classic retracements imaginable – the 38.2% one. This correction doesn’t change the trend, which remains down.

Based on what happened in 2008, it seems that stocks are about to move much lower in the following months.

Let’s take a look at the markets from a more short-term point of view and from the U.S. perspective.

The S&500, like global stocks, corrected a bit more than the 38.2% of the previous decline. And now they turned south, invalidating this small breakout. At the same time, they broke below the rising support line, which makes the outlook even more bearish. Consequently, my previous comments on the above chart remain up-to-date:

The broad market moved lower this week, and there are two good reasons to think that this time, the small move lower is just the beginning of a much bigger move to the downside.

One of the reasons is that this move lower came right after the triangle-vertex-based turning point. The declining black and red lines (both dashed) intersect at more or less the very recent top. As their name says, those turning points mark… Well, turning points. And since the most recent short-term move was to the upside, it currently has bearish implications.

The second reason is that stocks now broke below their rising support line (marked with a solid black line), and that’s not what happened during the two previous small moves lower.

The analogy in the price-volume link (marked with red rectangles) also points to much lower prices in the stock market.

Additionally, please note that stocks tried to move above their previous highs and the declining blue resistance line – and they failed. The invalidation served as yet another sell signal. It’s aśbsolutely no wonder that we’re seeing a significant short-term decline right now.

Why is this important for gold and silver investors and traders? Because the last two big moves took place more or less in line with each other – in stocks and in precious metals (and miners). The slide in stocks could also trigger something similar in the case of commodities like crude oil. The same thing is likely to happen again this time, especially given what’s happening in the USD Index.

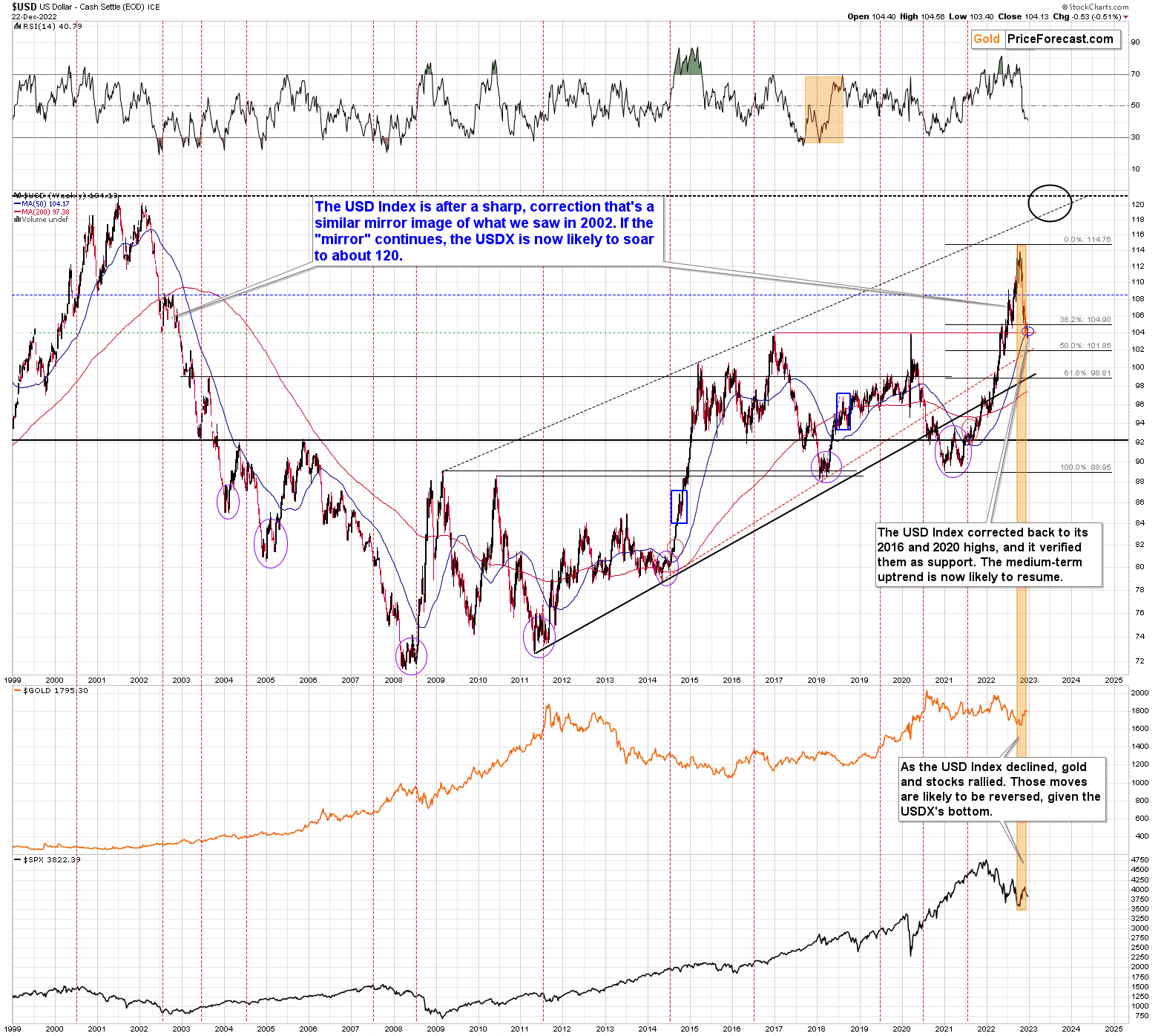

The USD Index moved a bit below the 38.2% Fibonacci retracement level, and at first sight this might seem bearish, but…

Long-term indications are more important than short-term ones, and based on what we see on the long-term USDX chart below, it seems that the small move below USD’s 38.2% retracement will be invalidated shortly.

The USD Index moved to its very strong support provided by the previous long-term highs.

The 2016 and 2020 tops (as well as the 2002 low and the 1999 top) currently serve as very strong support at about 104 level.

To clarify, the highest of those highs has 103.5 as the highest daily closing price.

This means that there was no breakdown recently, and any tiny attempts were quickly invalidated.

Consequently, the outlook for the USDX remains very bullish, based on the above indication.

What we saw recently appears to be nothing more than a verification of the breakout above the previous highs.

This means that gold, silver, and mining stocks are likely to decline profoundly as they are very negatively correlated with the USD Index.

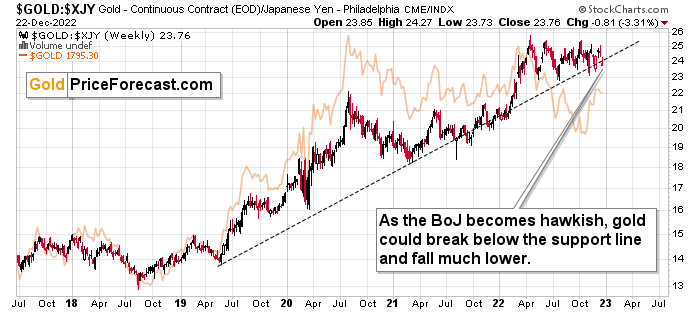

Before summarizing, I would like to add a note about the reasons behind the recent weakness in the USD Index.

In short, it was not about the U.S. dollar’s weakness – it was about the yen’s strength.

So, what is the real implication for gold?

It’s easier to understand the implication based on a counter-example. Remember when all the monetary authorities around the world were getting more and more dovish and they kept printing more and more money? That was bullish for gold, right?

Ok, so, now what we see is the opposite. The monetary authorities around the world are getting more and more hawkish, and the Bank of Japan appears to be finally joining the hawkish party, and that’s bearish for gold.

This remains true despite any short-term price movements caused by individual currency exchange rate changes. So, even if the yen continues to strengthen relative to the dollar for some time, gold might not be willing to react to it for much longer.

Why? Because in the short-term markets are particularly emotional. “OMG, USDX fell, let’s buy gold!” can dominate traders’ way of feeling/thinking (on a side note, “feenking” could be a new verb to describe the situation when one thinks that they are thinking about something, but actually they are just rationalizing their feelings).

Then, as the traders have some time to think about what’s really happening, they could sell gold as it becomes less and less appealing, given that fiat money can (at least for now…) provide more interest payments.

As you can see on the above chart, gold priced in the Japanese yen has been in a rather steady long-term uptrend for years. It’s close to the support line, though.

Based on the hawkish indications from the Bank of Japan, it seems that we might finally see a confirmed breakdown below this line, and when we do, the decline that could follow could be huge.

The buying pressure from the yen holders might have been a major driving force behind the rally in gold that we saw in the last few years. And as the interest rates in Japan increase, gold’s gleam to yen holders is likely to begin to wane.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

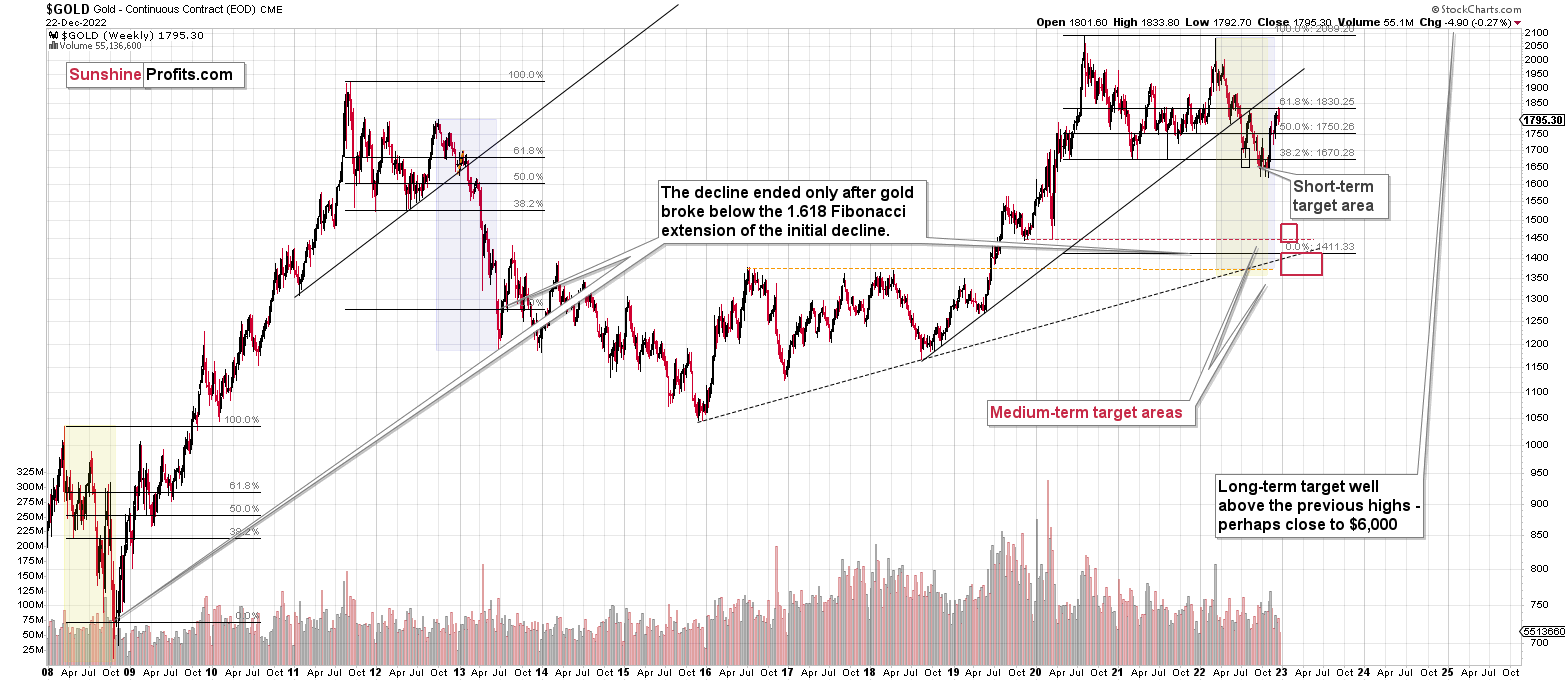

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Letters to the Editor

We received a few messages over e-mail, but as we are moving to our new platform, we will be transferring them below the articles as comments – and that’s where we’ll be replying to them.

Asking your questions below the articles or in the spaces called “Ask the Community” or “Position Sizes” directly will help us deliver a reply sooner. In some cases, someone from the community might reply and help even before we do.

Please remember about the Pillars of our Community, especially about the Kindness of Speech Pillar.

Also, if there’s anything that you’re unhappy with, it’s best to send us a message at [email protected].

Please note that this section is going to go away within the next 1-8 weeks, as you can add comments/questions below the article on Golden Meadow – the platform that we’re using to provide our analyses. Your notification e-mails include an invitation link that allows you to access the “Gold Trading Alerts” space.

Also, if you haven’t had the chance to see the video, in which I’m talking about the new platform and why we essentially moved from Sunshine Profits to Golden Meadow, I strongly encourage you to do so:

Summary

Summing up, it seems that the major bottom in the USD Index is in, while the correction in stocks, gold, silver, and mining stocks is over.

The nature of the recent corrections was mostly technical and rumor-based. The rumor was that the Fed would be making a dovish U-turn soon, and it recently became clear that this was not going to be the case. Consequently, the corrective upswing is likely to be reversed, and medium-term downtrends are likely to resume.

In my opinion, the current trading position is going to become profitable in the following weeks, and quite possibly in the following days. And while I can’t promise any kind of performance, I fully expect it to become very profitable before it’s over and to prolong our 2022 winning streak.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Friday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief