Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update.

Predicated on last week’s price moves, our most recently featured medium-term outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days and are written in italics.

There have been quite a few indications this week, so it’s difficult to pinpoint the key development that we saw. After looking at the charts right now, I’d say that one of the key developments happened way below the radar – the XAU Index corrected practically exactly as much as it did in 2012 before tumbling in a massive way. However, gold’s (likely fake) move above 2,000, the (likely real) turnaround in the USD Index close to the turn of the month, and the GDXJ’s RSI indicator above 70 are also very, very important at this time.

Quite a few things happened on the fundamental front as well, so I’ll take this opportunity to update you on those changes first and then move on to the technical ones.

The Weekly Fundamental Roundup

With relatively weak PMIs and a deceleration in JOLTS job openings garnering all of the attention this week, the recession crowd has bid bonds, and the anxiety has helped uplift the PMs. Moreover, with fears of a banking crisis helping to increase their safe-haven appeal, gold, silver, and mining stocks have outperformed.

Yet, we’ve seen this movie before, and the permabulls are often the loudest near the top. Furthermore, since the fundamentals contrast the narrative – like they did during the countertrend rallies in 2021 and 2022 – another sharp reversal should be on the horizon.

Blindfolded Investors Still Bidding Gold

It was only a month ago that investors couldn’t sell bonds fast enough. Now, they’re tripping over one another to get back in. In the process, the positioning shift has weakened the USD Index and helped lift gold, silver, and mining stocks.

Please see below:

To explain, the red line above tracks the USD Index, while the green line above tracks the U.S. 10-Year Treasury yield. More importantly, the black line above tracks the inverted (down means up) December 2023 Eurodollar futures contract.

For context, the Eurodollar is a proxy for the expected U.S. federal funds rate (FFR). And since the yield moves inversely to the price, when the Eurodollar rises, it means the crowd is pricing in a lower FFR.

Now, if you analyze the relationship, you can see that perceptions of a more hawkish Fed (a higher black line) helped uplift the USD Index and the U.S. 10-Year Treasury yield. Conversely, the vertical gray line on the right side shows how the recent banking crisis has prompted rate cuts by the end of December (lower black line), which have weighed on the USD Index and the U.S. 10-Year Treasury yield.

However, rate cuts are wishful thinking without a full-blown banking crisis, and a reversal of these expectations should rock the PMs in the months ahead.

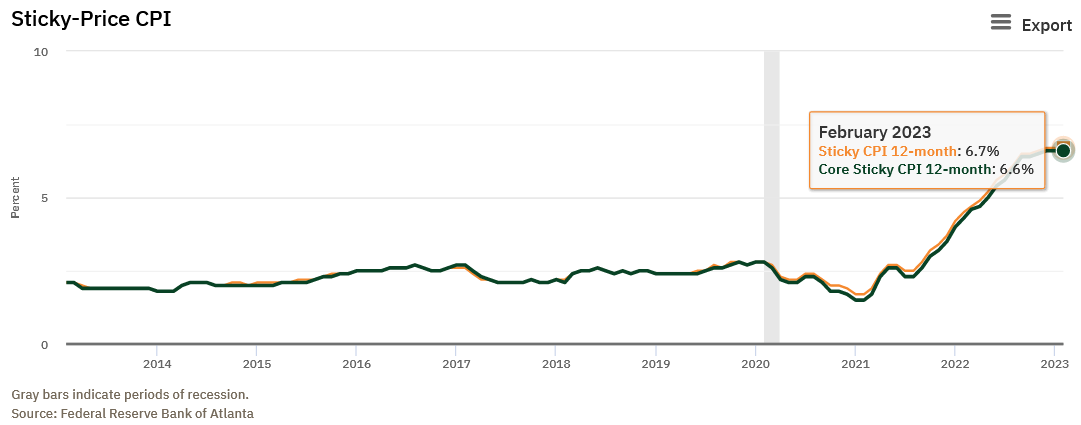

For example, while base effects have reduced the year-over-year (YoY) Consumer Price Index (CPI), those benefits will run out in a few months. Furthermore, the Atlanta Fed’s Sticky CPIs highlight the embedded nature of inflation.

Please see below:

To explain, the Sticky CPIs remain at cycle highs, despite the deceleration in the headline CPI. Therefore, the Fed has not solved its inflation problem, and investors are too eager for QE to understand the ramifications.

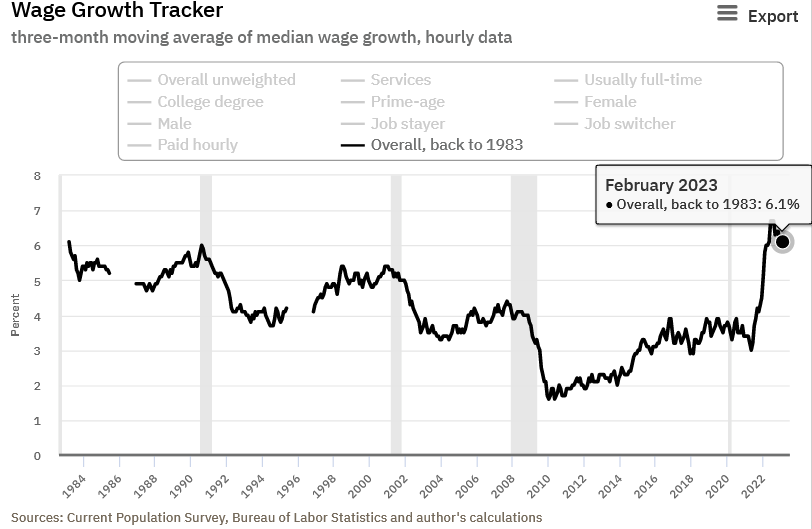

Second, the Atlanta Fed’s Wage Growth Tracker hit 6.1% in February. And if we exclude the highs set during the pandemic, 6.1% would tie the record dating back to 1983.

Please see below:

So, while the crowd assumes that demand destruction has arrived, a recession is imminent, and QE is approaching (bullish for the PMs), the fundamentals contrast that narrative. In reality, inflation has not abated, and investors’ attempts to price in a recession intensify its strength.

Remember, long-term interest rates have declined materially since the banking fears emerged. But the development is simulative because it lowers mortgage rates and makes financing more affordable. Thus, month-over-month (MoM) inflation should remain elevated until long-term interest rates are restrictive enough.

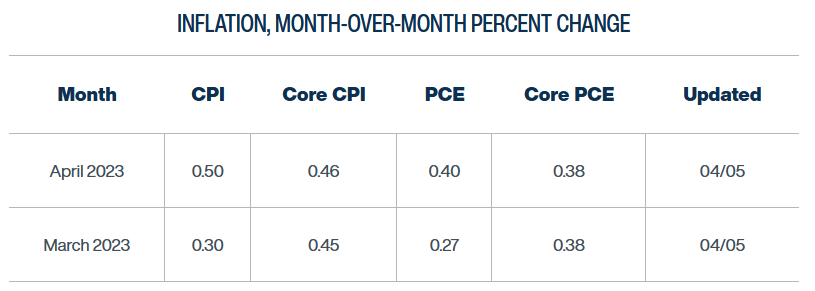

Please see below:

To explain, the figures above represent the Cleveland Fed’s expectations for various inflation metrics in March and April. If you analyze the CPI and core CPI columns, you can see that the rapid rate rise in February helped keep the MoM CPI relatively subdued at 0.30% – even though it annualizes to 3.66%. Conversely, the April reading has jumped to 0.50% MoM. And while it’s still early in the projection, a realization annualizes to 6.17%.

In addition, notice how the core CPI expectations have barely budged. They have remained in the 0.40% to 0.50% range, and neither supports rate cuts anytime soon.

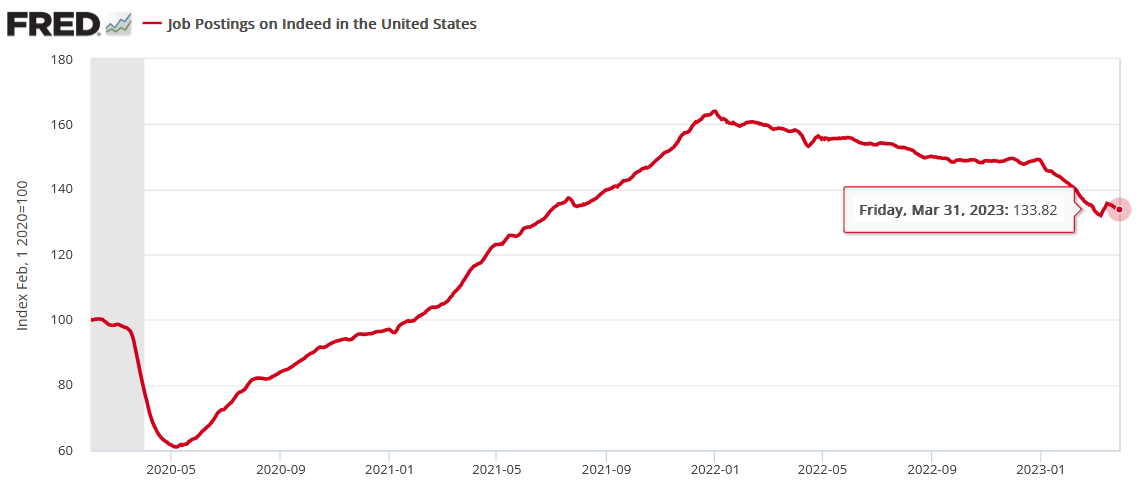

Moreover, while JOLTS job openings came in weaker than expected on Apr. 4, it was far from a surprise due to the 2023 drop in job postings on Indeed. However, the metric has stabilized recently, which signals less pivot optimism in the months ahead.

Please see below:

To explain, the 2023 decline was an ominous sign for JOLTS. But, if you analyze the right side of the chart, you can see that the metric is up slightly over the last three weeks. Therefore, the headlines should be less supportive for bonds and the PMs as we move forward.

Overall, the crowd is attempting to manufacture rate cuts because they’ve grown tired of this inflationary bear market. However, wishing won’t make it come true, and higher stock prices and lower long-term interest rates are the opposite of what’s needed to win this battle.

As such, while sentiment can keep prices decoupled from the fundamentals over the short term, don’t be surprised if panic occurs in the opposite direction in the months ahead.

Do you think a recession is imminent? How does inflation abate alongside lower long-term interest rates? And why aren’t wages falling?

You Shouldn’t Bank on Silver

While silver has benefited from the confusion over bank liquidity versus solvency, its recent gains were built on a faulty foundation. To explain, we wrote on Dec. 7:

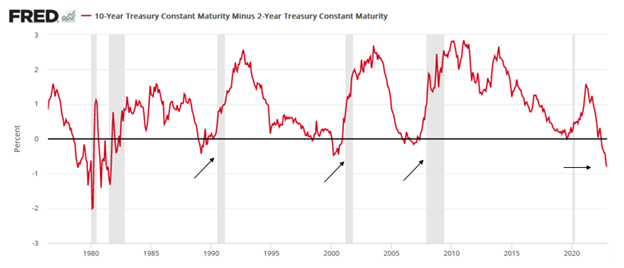

With yield curve inversion (10Y < 2Y) the talk of the town in recent days, the narrative proclaims that a recession is imminent. But that's not what we see.

For example, if you analyze the right side of the chart above, you can see that the 10-2 spread has surpassed -0.80% and is at its lowest level since the 1980s. As a result, the bond market is screaming recession. However, the three arrows in the middle show that the 10-2 spread moved from negative to positive before the last three recessions occurred.

To that point, little has changed. While the 10-to-2 spread has risen slightly, the metric remains deeply negative, and its movement does not match its behavior before the last three recessions.

Please see below:

To explain, the 10-2 spread is far from the flatline, and the current narrative is no different than December. Consequently, while it may seem like an outcome is inevitable because everyone is talking about it, the reality is that several metrics contradict the recession/pivot optimism.

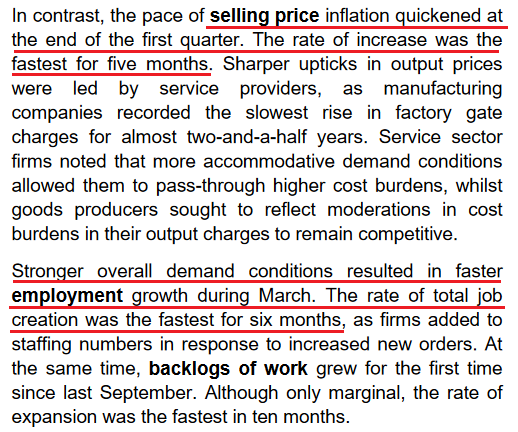

As evidence, S&P Global released its U.S. Composite PMI on Mar. 24, and the headline index increased from 50.1 in February to 53.3 in March. An excerpt reads:

“The latest index reading was the highest for almost a year and signaled a solid expansion in private sector activity (…). March data signaled a return to new order growth, with the upturn the first since last September. Although only marginal, the rise in new business was the sharpest in ten months.”

More importantly, S&P Global’s PMI highlighted resilient employment and reaccelerating inflation.

Please see below:

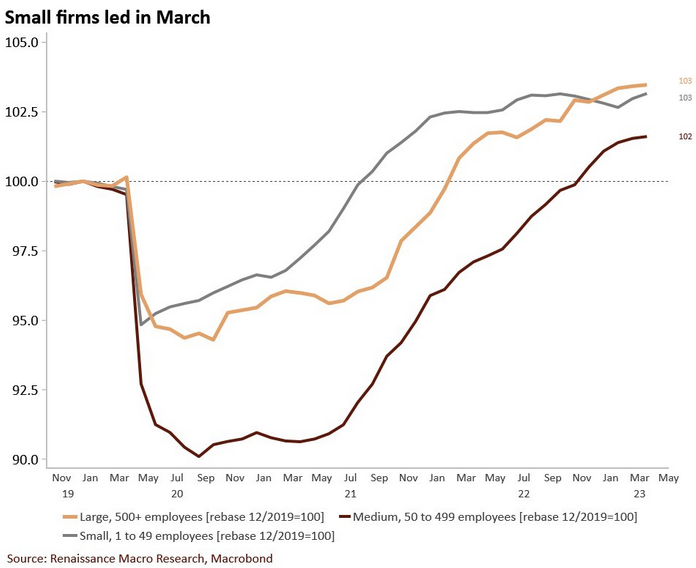

On top of that, ADP released its private payrolls report on Apr. 5. And while the metric came in below the consensus estimate, employment growth increased for small firms and hit new cycle highs for larger firms.

Please see below:

To explain, the orange, brown, and gray lines above track the hiring behavior of large, medium, and small businesses since late 2019. If you analyze the right side of the chart, you can see that the orange and brown lines hit higher highs, while the gray line bounced after a recent decline. As such, the fundamentals on the ground are much different than the sentiment on Wall Street.

To that point, while employment remains uplifted and the Atlanta Fed’s Wage Growth Tracker is only slightly below its all-time high, U.S. consumers are still flush with cash. We wrote on Mar. 31, 2022:

There is a misnomer in the financial markets that inflation is a supply-side phenomenon. In a nutshell: COVID-19 restrictions, labor shortages, and manufacturing disruptions are the reasons for inflation’s reign. As such, when these issues are no longer present, inflation will normalize and the U.S. economy will enjoy a “soft landing.”

However, investors’ faith in the narrative will likely lead to plenty of pain over the medium term (…).

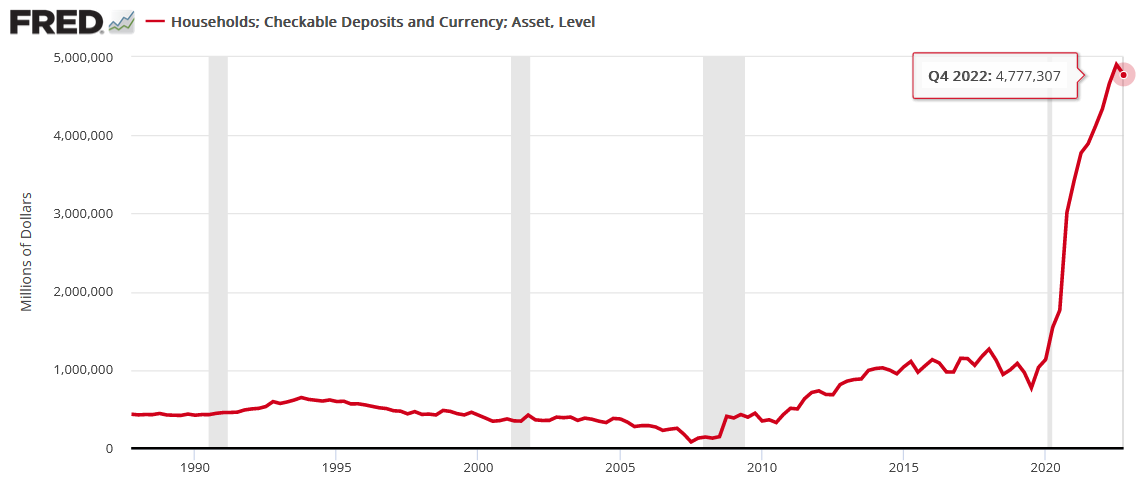

U.S. households have nearly $3.89 trillion in their checking accounts. For context, this is 288% more than Q4 2019 (pre-COVID-19). As a result, investors misunderstand the amount of demand that’s driving inflation.

So, while the prediction proved prescient as demand remained resilient throughout 2022 and inflation proved more problematic than expected, little has changed. Households’ checkable deposits have only slightly declined from their 2022 peak and are 362% above their Q4 2019 comparison.

Thus, when you combine this much cash with near-record-low unemployment and near-record-high wage inflation, investors are kidding themselves if they think demand destruction has arrived.

Remember, while silver has been a major beneficiary of the ‘bank crisis means rate cuts’ narrative, this is 2021/2022 all over again. When the crowd attempts to front-run a recession, it negates the recession due to the simulative effect of lower long-term interest rates. That’s why sentiment surrounding silver has gone from euphoric to catastrophic several times over the last two years, and we believe another shift should occur over the next several months.

Overall, the crowd continues to assume that inflation is dead and gone, and this is probably the sixth obituary written over the last 24 months. Yet each time it rises from the ashes, the PMs suffer mightily, and the narrative changes dramatically.

Do you believe the 10-to-2 spread has merit? Why would businesses hire more employees if demand was so weak? Will consumption remain elevated due to high checking account balances?

The Bottom Line

While sentiment often rules the short term, the medium-term technicals and fundamentals have demonstrated their might time and time again. Consequently, while the USD Index has suffered and the PMs have benefited, the developments have only loosened financial conditions and made inflation more problematic.

To win the war, long-term interest rates need to rise to suppress borrowing and consumption, and a realization supports higher real yields and a stronger USD Index. So, while the crowd believes QE is only a few months away, another disappointment should confront the pivot bulls in the months ahead.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Apr. 11: NFIB Small Business Optimism Index

With small businesses poised to suffer the most from a lending halt, it will be interesting to see how output, employment, and inflation fare in March.

- Apr. 12: Consumer Price Index (CPI), FOMC Minutes

The CPI should decelerate YoY due to base effects. But with MoM readings still hot, the good times will only last for so long. In addition, the FOMC will provide more clarity on the committee’s rate hike expectations.

- Apr. 13: Producer Price Index (PPI)

Since the PPI often leads the headline CPI, its performance should be monitored.

- Apr. 14: Retail Sales

Recent card data shows a deceleration in retail spending, but this fluctuates from month to month. Therefore, it’s important to focus on the medium-term trend and not overreact to one month’s print.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

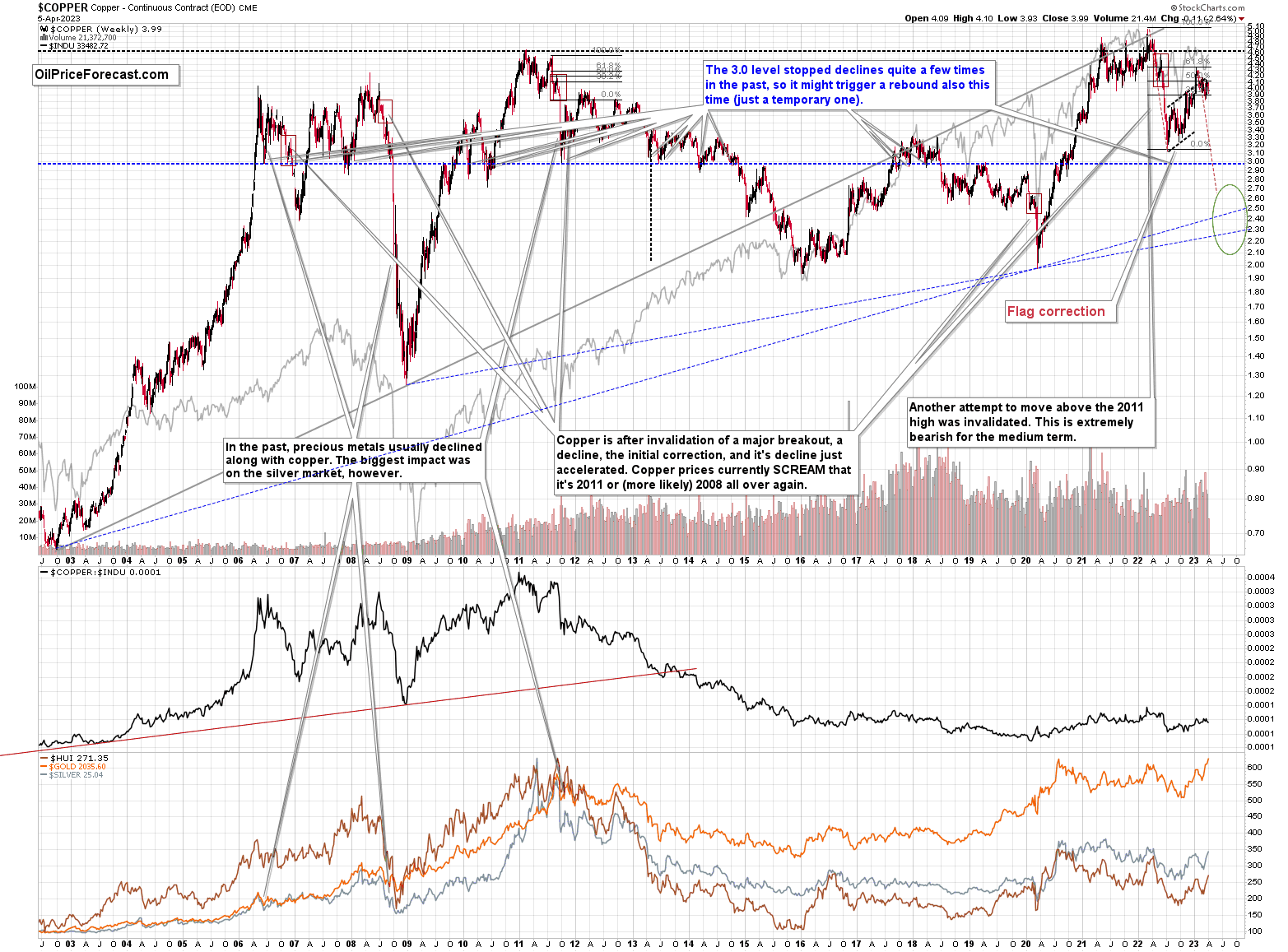

Let’s start today’s technical discussion with a quick check of copper prices.

Copper rallied recently, but it stopped at its 61.8% Fibonacci retracement level and then moved back down. Consequently, the recent move – while impressive from a day-to-day point of view – remains to be a short-term correction only.

Consequently, what I wrote about it previously remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

No market moves up or down in a straight line (well, the 2008 slide appears to have been an exception), and a short-term correction doesn’t necessarily invalidate the bigger trend. For the last couple of months, copper has been trading sideways, but it didn’t change much regarding the outlook.

In fact, it made my previous target area even more likely. You see, the consolidation patterns are often followed by a move that’s similar to the one that preceded them. In this case, the previous 2022 decline was quite significant, and if it is repeated, one can expect copper to decline well below 3.

Actually, copper could decline profoundly and bottom in the $2.0-2.7 area. That’s where we have rising, long-term support lines and also the previous – 2016 and 2020 – lows.

Flag patterns (which we just saw in copper) tend to be followed by price moves that are similar to those that preceded them. I marked this on the above chart with red, dashed lines. This method supports a copper price’s move to around $2.7.

Given the size of the previous decline (and its pace), it seems quite likely that it could take another 2-7 months for copper to move to about $2.4. May seems to be the most likely time target given the current data.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after the invalidation of a major breakout, a decline, and a correction. Copper prices currently SCREAM that it’s a variation of 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

Before moving further, I’d like to extend the copper analysis into the analysis of the situation in one of the major copper companies – FCX. That’s where there’s the “extra trading opportunity” that I described several days ago.

And it became profitable almost instantly.

What you find below is a quote from this analysis as it remains up-to-date (I’m updating the charts though). One thing that I’d like to add is that on FCX’s medium-term chart, you can see a breakdown below the rising support line, which makes the outlook even more bearish.

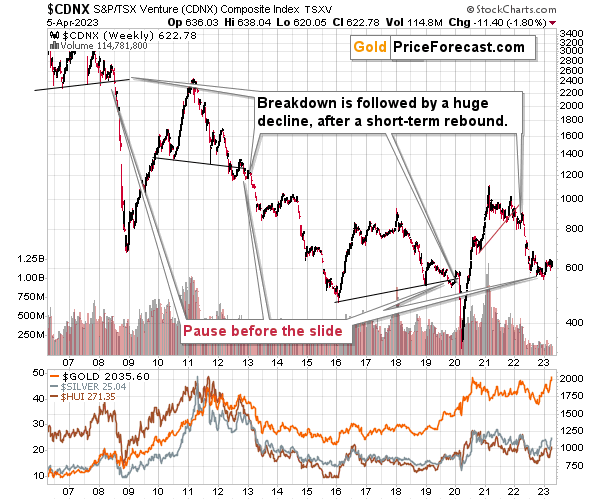

Having said that, let’s check the junior miners’ really big picture.

In short, we saw a tiny correction in the TSX Venture index, and this should be a major red flag for anyone thinking that the recent rally was a game- or trend-changer. This is a blip on the radar screen, similar to what we saw in the second half of 2021, before another big move lower.

The really important thing here is that we saw the first crack in the dam. The index declined visibly, and it might mean that the final part of the 2008-style slide has just begun.

Consequently, my previous comments on the above chart remain up-to-date:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

Just like it was the case in 2008, the move higher that we saw before the final (biggest) slide in gold, silver, and gold stocks (lower part of the chart) didn’t translate into a visible rally in the TSX Venture Index. Just as the index paused back then, it pauses right now.

Currently, it’s trading at about 600, and back then, it consolidated at about 2500. The price levels are different, but the overall shape of the price moves (or lack thereof) is similar. This serves as a signal that the recent upswing in the PMs is not to be trusted.

The above chart is one of the weakest (from a technical point of view) that is seen across the board right now. There is a strong long-term downtrend visible in the TSX Venture Index, and if stocks slide similarly as they did in 2008, the TSXV could truly plunge – perhaps even to the 300 level or lower.

The important short-term detail is that the TSXV just broke to new yearly lows. This is a major (yet barely noticed by most) indication that the next big move lower is about to start.

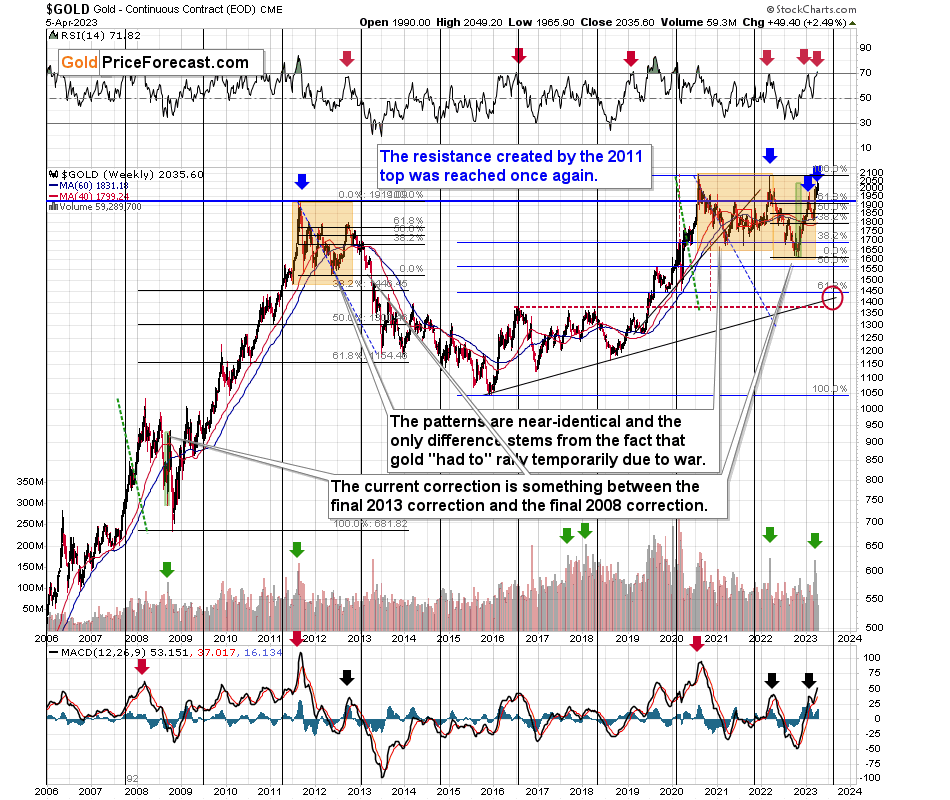

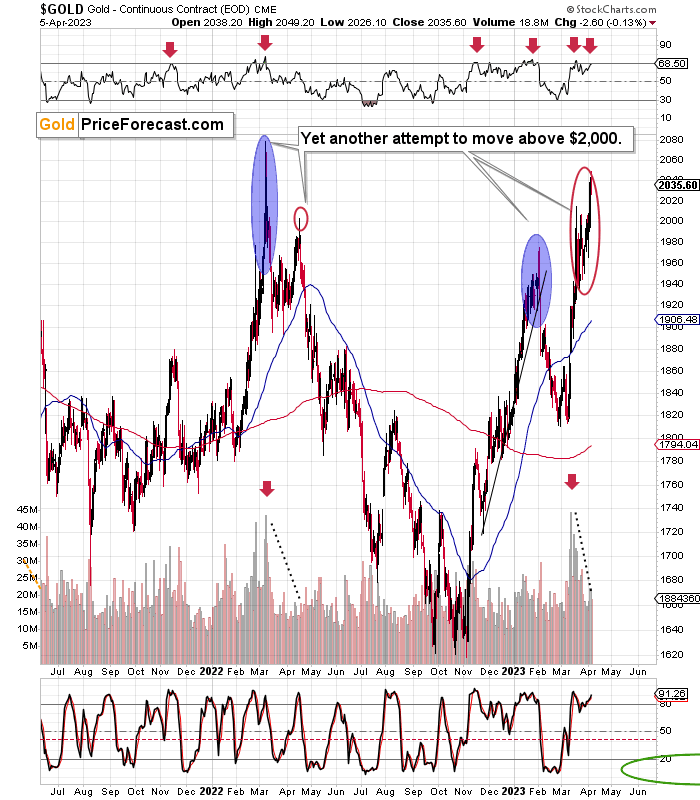

Having said that, let’s turn to gold.

Let’s start with context:

Between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet gold failed to rally to new highs.

In fact, gold was just trading well below its 2011 high, which tells you a lot about the strength of this market. It’s almost absent.

There’s a war in Europe, and billions of dollars were printed, and gold was below its 2011 highs – in nominal terms! Adjusted for inflation, it’s much lower. And silver and gold stocks’ performance compared to their 2011 highs? Come on…

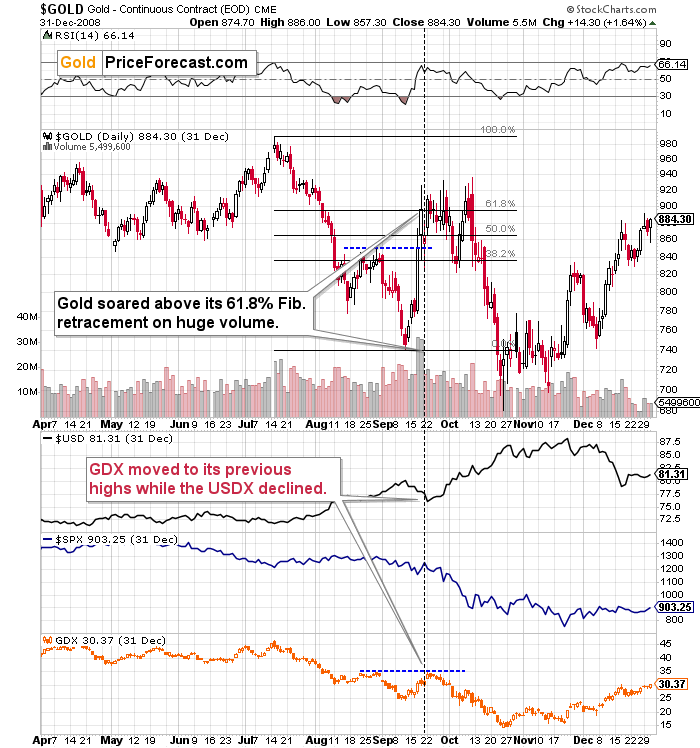

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. We can also spot similarities between now and 2008. The long-term gold price chart below provides details.

I marked the big increases in weekly volume levels during gold’s upswings with green arrows.

The most recent case is from 2022, when gold topped.

The same happened in early 2018.

That’s how gold topped in 2011.

And – most importantly – that’s exactly what we saw at the final pre-slide top in 2008.

Please note that the rapid rally that we saw in 2008 before the slide was very much in tune with what we saw recently (note: green rectangles). Consequently, it’s not a bullish game-changer.

Now, some of the high-volume weeks were accompanied by RSI at about 70, and I marked those cases with red arrows. That was the case in early 2022 and during many other major tops.

What’s most interesting is that all of gold’s previous attempts to move above $2,000 were accompanied by the RSI at or above 70. And they all failed! The history tends to rhyme, so the implications here are profoundly bearish – not just from the point of view of volume but also from the point of view of the RSI indicator.

Gold just moved above $2,000, and just as all previous attempts to move above this level failed, we’re likely to see it fail once again.

Let’s take a look at how the situation developed on the technical front back in 2008.

Gold’s final pre-slide corrective upswing was based on turmoil, uncertainty, and safe-haven buying. It was volatile, it was large, and it was accompanied by huge volume.

The RSI indicator moved a bit below the 70 level.

Sounds familiar?

Back in September and October 2008, gold even rallied above its 61.8% Fibonacci retracement level.

During that time, the USD Index declined in a relatively sharp manner, and the GDX ETF pretty much followed the stock market.

It’s exactly the same thing right now. Back then, stocks declined over time, and this time they are moving somewhat higher, but the mining-stocks link is just as it was in 2008.

Also, let’s keep in mind the situation in real interest rates. It might not be as sexy as bank collapses, but that remains one of the key reasons for gold’s decline in the following weeks/months.

Gold has a lot of catching up to do with its decline to “normalize” its link with real rates.

Technically speaking, the key thing is that gold once again tried to move above its 2011 highs, and it once again failed to do so. It invalidated this breakout in one of the most bearish ways imaginable – with a weekly reversal.

This is an extremely important sell signal. The combination of fundamental and technical factors alone is a reason to prevent one from having a long position in gold right now (except for the insurance capital, that is).

That’s one thing. Another thing is that, given the major fundamental event that I already mentioned above (the war outbreak), it’s possible for the technical patterns to be prolonged and perhaps even repeated before the key consequence materialized. Similarly to the head-and-shoulders pattern, there can be more than one right head before the breakdown and slide happen.

In gold’s case, this could mean that due to the post-invasion top, the entire 2011-2013-like pattern got two major highs instead of one. And thus, the initial decline and the subsequent correction are pretty much a repeat of what we saw in 2020 and early 2021, as well as what we saw in 2011 and 2012.

The particularly interesting fact (!) about the correction that we saw after the 2011-2012 decline (the one that was followed by the huge 2012-2013 decline) is that during it, gold corrected slightly more than 61.8% of the preceding medium-term decline. Consequently, the current situation is just like what happened back then.

And if all the above wasn’t bearish enough, please take a look at the reading of the RSI indicator based on the weekly price changes. It’s now just below 70, and guess where it was at the final top before the 2012-2013 slide? Yes, it was exactly there, too.

That’s also approximately where the RSI was at last year’s top.

The orange rectangles on the above chart represent the corrective upswings from approximately the previous local lows. There are two of them, and back in 2013, there was just one corrective upswing before gold truly plunged.

However, please remember that history doesn’t repeat itself to the letter – it rhymes. This means that two corrections instead of one are still within the scope of the similarity, especially since the first correction wasn’t as big as the 2008 one.

The current situation is truly special, as the rate hikes are something that we haven’t seen in a long time. The same goes for the level of concern about the inflation that’s “out there.” The latter implies that when faced with a decision about whether to fight inflation or help the economy, the Fed is likely to lean toward the former. And that’s bearish for assets like gold.

Let’s also keep in mind the time aspect. I wrote about it two days ago:

It is said that time is more important than price and that when the time is up, the price will reverse.

Well, since the situations are so alike, let’s check when the time for gold was “up” and when it moved sharply lower in 2008.

The first top in gold formed in mid-September 2008, and the final top formed in mid-October 2008. That was precisely 16 trading days later. In other words, gold has been moving back and forth close to the initial high for 16 trading days and then it plunged.

Consequently, if gold was trading sideways for about 16 trading days after the initial top, it would be perfectly normal and a sign that a slide was about to follow.

Well, let’s check the current status.

Gold formed its initial top on March 20, 2023.

Today is the 13th trading day after that.

This means that the current back-and-forth movement does not deviate from the 2008 pattern AT ALL!

In fact, what we saw recently in gold is perfectly normal, given its link to 2008.

Even the move above the initial high is in tune with what happened in 2008!

It also means that even if gold doesn’t plunge for a week (or even two), it won’t break the analogy by itself.

Does it mean that gold is likely to rally from here?

No, it doesn’t imply that. Gold has been unable to stay above $2,000 despite multiple attempts, and nothing suggests that this is about to change in the near term.

The RSI is close to 70, which means that gold is very close to being oversold, and the volume declined – it’s been relatively low during the most recent immediate-term run-up.

To be precise, last April, we saw a final pop-up in gold that was accompanied by a slight increase in volume. That was the final top.

We saw the same thing recently – even the slight increase in volume.

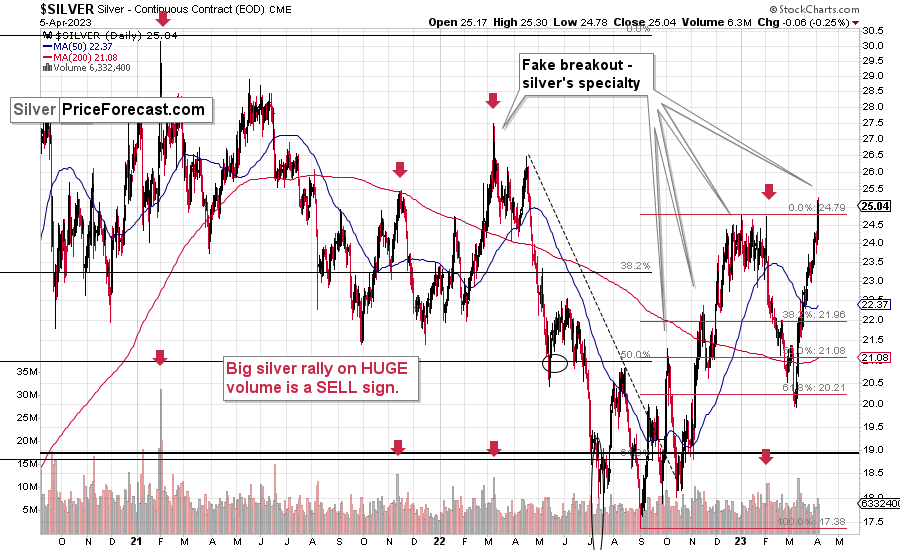

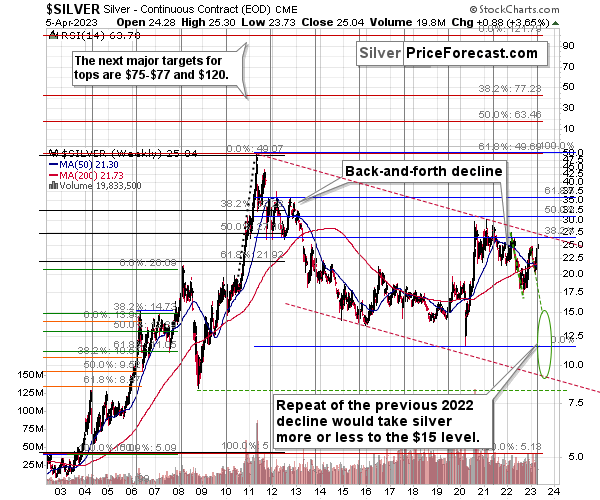

Having said that, let’s take a closer look at the silver market.

Silver soared recently, and it might seem bullish at first glance. Especially since silver just soared above its previous 2023 high.

However, it would probably seem bullish only to those, who are new to the silver market, and they haven’t noticed how silver performs – especially relative to gold – before big declines.

Yes, it tends to outperform gold at those times. And, well, we’re seeing this once again now.

In addition to the above, silver tends to “fake out” instead of breaking out right before reversing. So, is this week’s breakout a meaningful buy signal? No, it’s a warning sign for bulls.

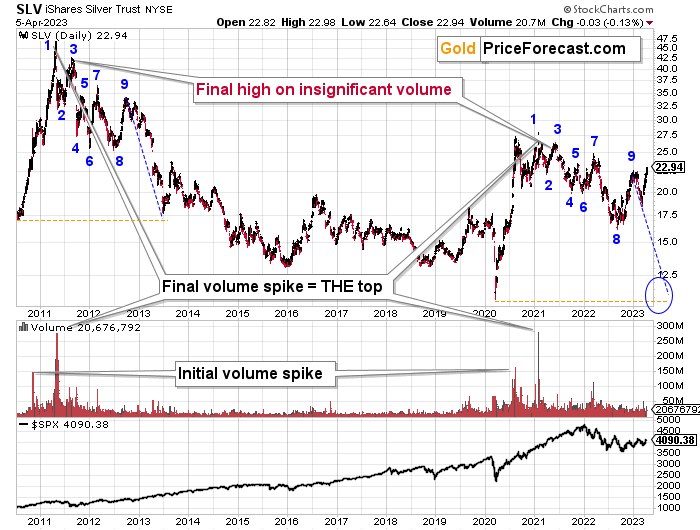

Also, while it’s not visible on the above silver chart, the white metal is currently repeating its previous post-top performance. It’s crystal-clear on the below SLV ETF chart.

However, before we move on to the SLV ETF, let’s take a moment to recall the time when everyone and their brother were bullish on silver – in early 2021.

The silver price even tried to move above the $30 level, and it succeeded in doing so… For a brief moment.

Silver was “supposed to” take off. Shot up to the moon. Based on the physical market’s tightness, silver’s availability, a short squeeze, etc. Truth be told, it’s difficult not to write this with sarcasm (and I’m not), because I remember exactly the same reasons being used to justify silver forecasts above $100 back in the early 2000s. I’ve been there and I’ve been buying silver below $5, so I know a thing or three about what kind of analyses, discussions, and rumors were “out there” at those times.

Two decades later, the silver price rallied in a rather regular manner, along with gold, and then declined – also along with gold. To be precise – I’m not ruling out any of the above – short squeeze, shortages in general, etc. However, I am saying that just because something MIGHT EVENTUALLY happen, that doesn’t mean that it IS going to happen NOW or ANYTIME SOON.

For those exceptional situations, it’s great to have some physical silver (and gold, too). However, on a day-to-day basis, the investment and trading parts of one’s capital should be governed while putting great weight on things that are actually likely to happen in regular situations.

One way to thrive while trading silver is not to take silver’s strength at face value. Just as I warned that even if silver was about to soar (and I really DO expect silver to soar above $100 in the following years), then it was very unlikely to do so again in 2021 as the bigger trend was not supporting this outcome.

Anyway, when silver was trying to break above $30, I warned you about the real bearishness of the situation. (By the way, this link also proves that I’ve been expecting the interest rates to rise before that materialized.)

Many months later, we see that what formed in early 2021 was a major top that started a major medium-term decline.

Those of you who have been following my analyses for a long time might recall this chart.

I featured it originally many months ago, and the emphasis was on the analogy in price movement and in the spikes in the SLV ETF’s volume.

Indeed – the situations proved to be analogous, and the silver price declined.

What’s remarkable is how similar the declines were.

What I added today are the counters (no, it’s not an Elliott Wave count), and I added the S&P 500 at the bottom of the chart.

The counters help to see which parts of the silver price movement are analogous. They are not identical, but they are much more similar than it seems that they “should be.” Even the “8” bottom was rather broad in both cases.

Based on this similarity, silver is now starting the main part of the slide. Its recent weakness relative to gold definitely confirms that.

Silver’s decline (and PMs decline in general) took a rather measured shape in its initial months (late 2012 – early 2013), so should we expect the same thing to happen now?

No.

The reason for this lies in the link to the stock market. Back in 2013, there was no visible decline in stocks, let alone a substantial one.

This time, we are likely to see one. And you know when we also saw some sharp declines in stocks? In 2008 and in 2020, and you can see the latter on the above chart. Silver plunged in a sharp (not measured!) manner in both cases.

Given rising interest rates and the investment public’s realization that the rates are not “about to move lower,” that is something that is likely to lead to the stock market’s sell-off. But I’ve been writing about that already.

The thing is that it has implications for the above-mentioned analogy in silver. And that is: the upcoming part of the decline in silver is likely to be sharper than what we saw in 2013. The same goes for the implications for mining stocks (and probably gold). This slide is likely already underway.

Let’s take a look at the situation from a broader point of view.

When looking at silver from a long-term point of view, it’s still obvious that the recent move higher was most likely just a corrective upswing.

What happens after corrections are over (as indicated by, i.e., silver’s outperformance)? The previous trend resumes. The previous trend was down, so that’s where silver is likely headed next.

Besides, the long-term turning point for silver seems to have already triggered a rally, and another slide can now take place – just like what we saw in 2012.

However, will silver only repeat its previous 2022 performance and not decline more than it already has?

Based on the analogies to 2008 and 2013, the latter is more likely. The 2013 slide was bigger than the initial decline that we saw in 2012. And the final 2008 slide was WAY bigger than what we saw before it.

Due to its industrial uses, silver is known to move more than gold, in particular when the stock market is moving in the same way as gold does. Since I think that gold and stocks are both likely to slide, silver is indeed likely to decline in a truly profound manner. Quite likely lower than just $15.

Consequently, my prediction for silver prices remains bearish, as does the outlook for the rest of the precious metals sector.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

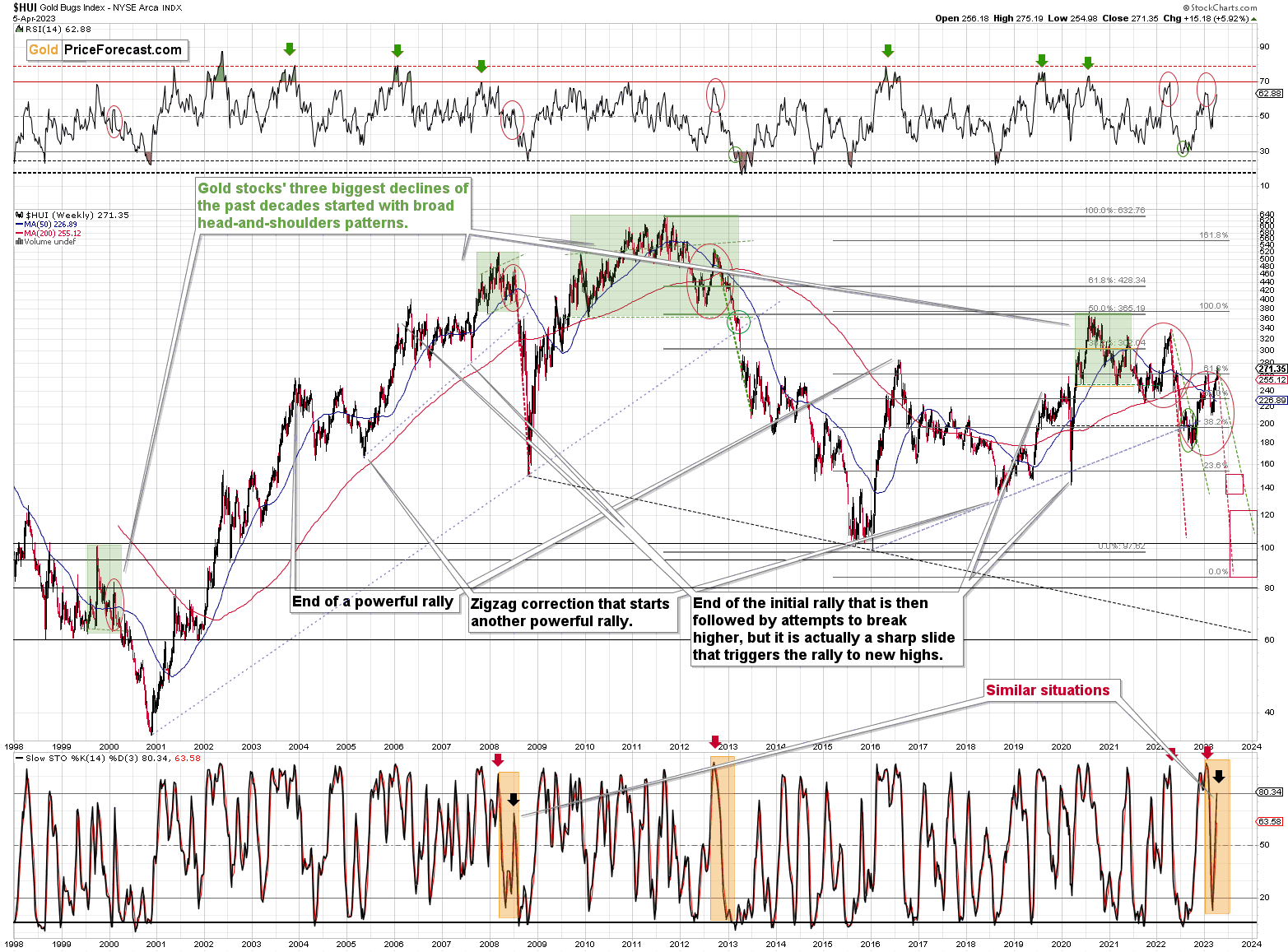

Having said that, let’s take a look at what happened in mining stocks.

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

For example, right now, gold stocks are declining – and correcting – similarly to how they did in 2008 and in 2012-2013.

Moreover, the stochastic indicator (lower part of the above chart) is currently performing just like it did at the 2008 top – so the bearish similarity between those periods is not just in gold.

In mid-2008, the HUI Index – proxy for gold stocks – was moving higher. Quite visibly so. However, it’s important to note what accompanied this final pre-slide upswing in the HUI Index in the case of the indicators.

After bottoming below 20, we saw a sharp upswing in stochastic (bottom part of the above chart). It was this upswing that marked the last moment to enter short positions (and/or exit long ones) before the slide took gold stocks much lower. Is this THE TIME right now? I can’t make any guarantees (regarding outlook or performance), of course, and I’m not making one right now. However, in my opinion, it’s highly likely that we are in the same situation right now.

The sentiment is ridiculously positive, and it was just as positive back in 2008. Pretty much nobody was expecting what arrived next – the carnage.

This time, the volatility is even bigger (which is not that odd given that more money is floating around this time), but we can see that the indicator is behaving very similarly.

What I would like you to additionally focus on here is that the “double correction” theory that I described below gold’s long-term chart is clearly visible here as well. We already saw the 2012 rally being repeated, and now we see it all over again. I marked them with red ellipses.

What are the implications? Well, obviously, they are bearish, as it was this correction in 2012 that started one of the most powerful declines of the previous decades. The RSI indicator based on the weekly prices is in a similar position to where it was at the late-2012 and 2022 tops. The consequences are clearly bearish for the following months.

My previous comments on the above chart, therefore, remain up-to-date:

The situation being what it is on the gold market (as discussed above) and the stock market (as I’ll discuss below), it seems to be only a matter of time before gold stocks slide.

For many months, I’ve been writing that the situation in the HUI Index is analogous to what we saw in 2008 and in 2013. Those declines were somewhat similar, yet different, and what we see now is indeed somewhere in between of those declines – in terms of the shape of the decline.

At first, the HUI Index declined just like it did in 2013, and the early 2022 rally appears to be similar to the late-2012 rally. However, the correction that we saw recently is also similar to the late-2012 rally.

Since history doesn’t repeat itself to the letter but rhymes, is it really that odd that we now saw two corrective upswings instead of one? Not necessarily.

This is especially the case given that the 2008 decline had one sizable correction during the big decline. It’s not clearly visible on the above chart due to the pace of the 2008 slide, but it’s definitely there. You can see it more clearly in one of the below charts.

So, no, the recent rally is not an invalidation of the analogies to the previous patterns, it continues to rhyme with them in its own way. And the extremely bearish implications for the following months remain intact.

How low can the HUI Index fall during the next big downswing?

As is the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 80-120 is my current target area for the upcoming slide in the HUI Index.

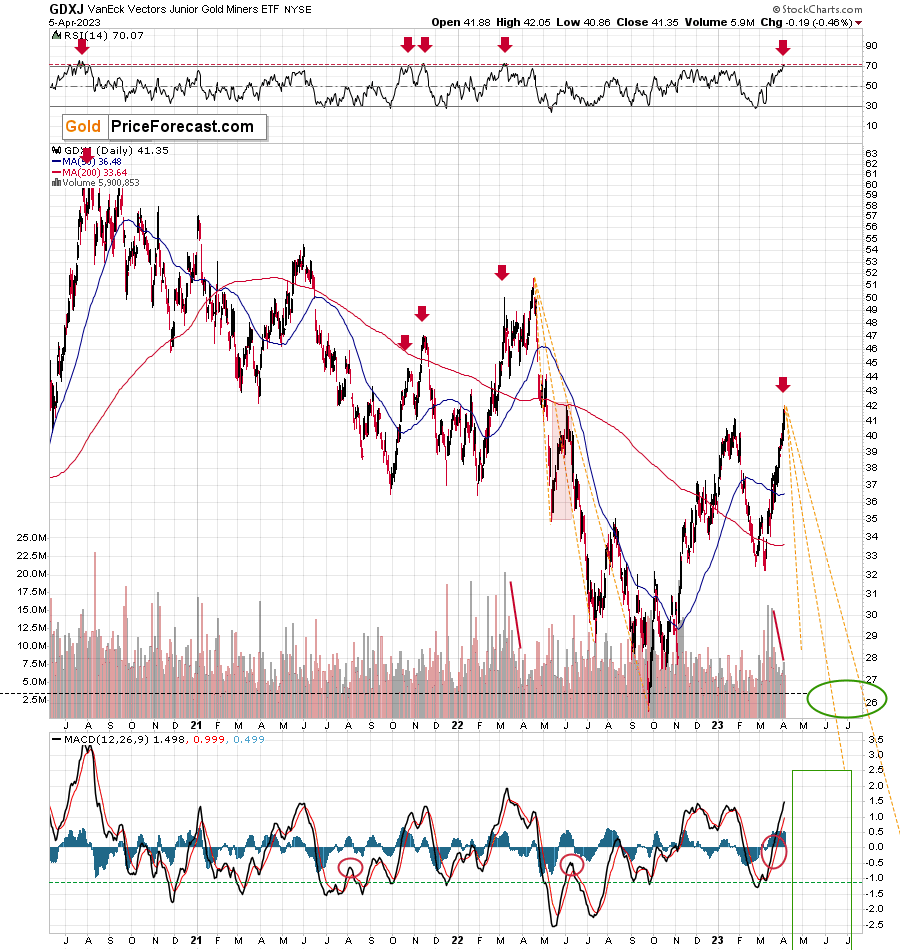

What about the short run?

I already wrote about the GDXJ’s extremely bearish indication from its RSI indicator in Tuesday’s intraday Gold Trading Alert, and here’s a graphical representation of what I wrote.

Quoting Tuesday’s (Apr. 4, 2023) intraday Alert:

The GDXJ ETF moved higher today (as gold and silver did), and as a result, the RSI based on it moved above 70.

In the recent years, it was almost always the case (and has been absolutely the case since 2021) that when GDXJ’s RSI moved above 70 that a major top formed and GDXJ was about to slide.

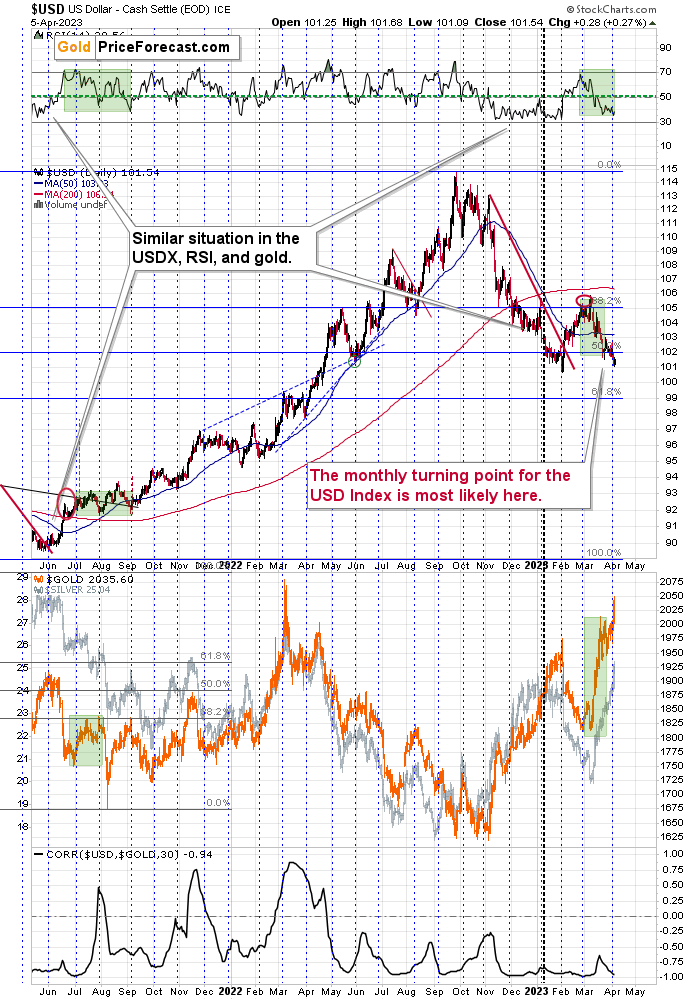

Meanwhile, the USD Index moved lower, and it’s now just a bit above its previous yearly low. Based on the analogy to 2008 (and also 2011), it seems that the bottom is in or that it’s so close that any potential downside here is likely negligible.

Consequently, the odds are that the junior miners are topping here. Even though one might “feel” that this is the time to drop the towel, and maybe even go long, the history shows that exactly the opposite is justified from the risk to reward point of view. If I didn’t have a short position in junior mining stocks right now, I would be opening one right now.

The above simply remains up-to-date.

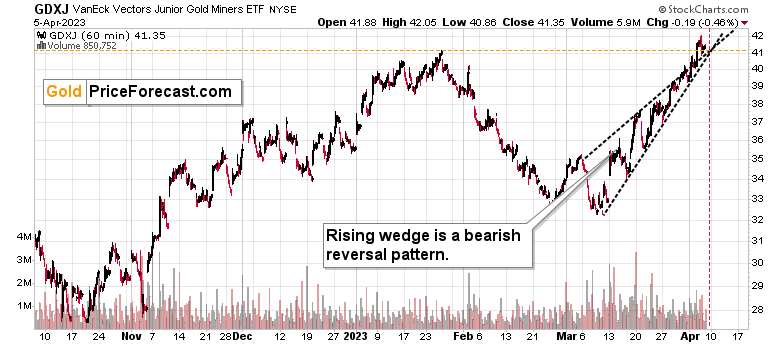

On the above hourly GDXJ chart, we see that it moved slightly above its previous 2023 high, and we see a small move above the rising wedge pattern.

Both moves were not confirmed yet, and given the situation in the USD Index, HUI Index, and gold, it seems likely that those breakouts won’t be confirmed. And once they are invalidated, they will be a very strong sell signal for the short term.

The lines creating the rising wedge will cross approximately on April 10 – next Monday. Since there is no trading in the U.S. this Friday, we have only one full session left (today).

Consequently, it could be the case that we see some sideways movement or a move lower and then a final attempt to move higher on Monday, only to see a massive failure and the start of a truly powerful decline at that time.

I wrote most of the above yesterday, and what happened yesterday confirmed it.

Patience here is likely to be extremely well rewarded.

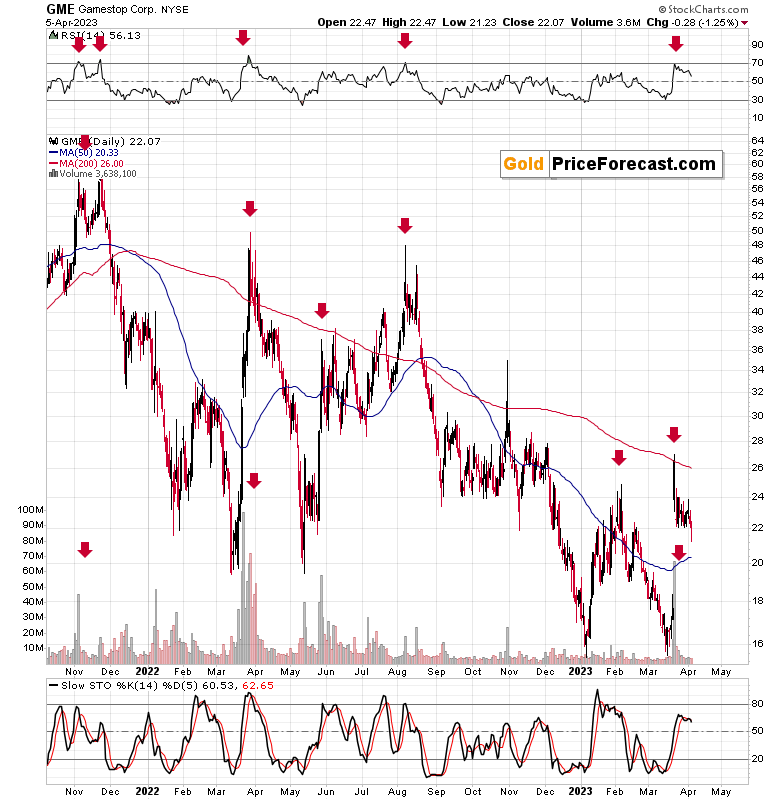

Also, let’s keep in mind the overall context – it is likely the investment public that has been buying recently, and we saw indications from several places. High volume in gold is only one indication. Another comes from the recent performance of the GME (GameStop) stock price. I wrote about it two weeks ago:

Having said all the above, it’s time to move on to the one “extra” chart that I mentioned in the opening paragraph.

It’s GME – the GameStop stock symbol.

Why GME? Because it’s one of the recently (or not so recently) popular “meme stock” that got the spotlight in 2021. The fundamentals of the company are not favorable in my view, and it’s been slowly declining from its 2021 “pumped” peak.

The thing is that since it doesn’t have a favorable fundamental situation but was popular with the investment public, it’s now a useful barometer of sentiment.

It’s likely getting cheaper for a reason, and yet, every now and then, we see sharp rallies and peaks in its price. Why would that be the case? It is most likely the phenomenon that I described previously – the worst performers get a boost at the end of the rally as the investment public enters the market.

Why is this relevant to us?

Well, please take a look at the moments that I marked with red arrows:

- November 2021

- Late March 2022

- Late May 2022

- Early August 2022

- Early February 2023

- and now.

What happened in the GDXJ at those times?

Let’s check:

- November 2021 – major top

- Late March 2022 – very close to the final top; before a huge slide

- Late May 2022 – major top

- Early August 2022 – major top

- Early February 2023 – major top

- and now.

The first two of those cases (I put them in bold) were accompanied by a big volume. The declines in the GDXJ in the following weeks were particularly big in those cases.

So, the situation in the GME makes it very likely that it was the general investment public’s buying that recently pushed the GDXJ higher. This means that this rally should not be taken at face value.

Instead – and the analysis of GME shows that – this should be treated as a very bearish indication of medium-term importance.

Since this comes on top of the link to 2008, the extremely bearish situation in world stocks, bearish confirmations in the S&P 500, and the bullish (medium-term importance, not just short-term) set-up in the USD Index, the outlook for the precious metals sector – in particular for the junior mining stocks – is currently very, very bearish. The profit potential for our short positions remains enormous.

Please note that the tops in the GME and the GDXJ didn’t necessarily form on exactly the same days – but they were still very close to each other. The implications here are very bearish for both GME and GDXJ.

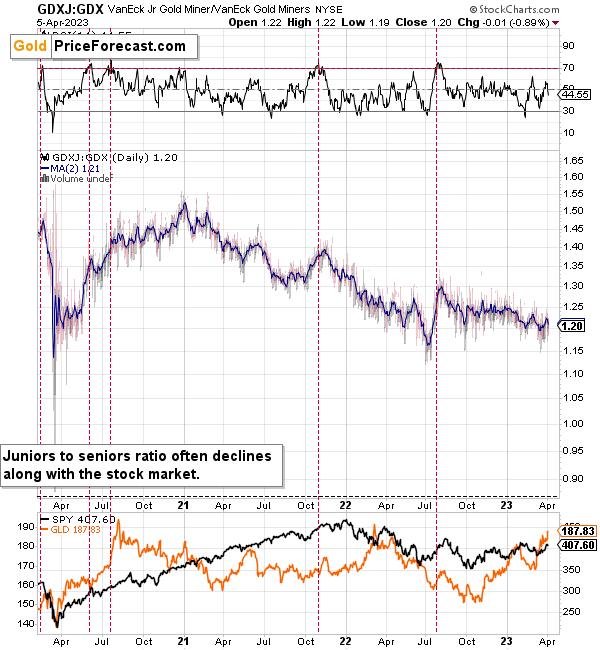

Meanwhile, the relative performance of junior miners compared to senior miners continues to deteriorate in a medium-term trend.

During this quick upswing, juniors rallied relative to seniors, but this is just a very short-term move that’s within a short- and medium-term downtrend.

This implies bigger declines in the GDXJ in the future.

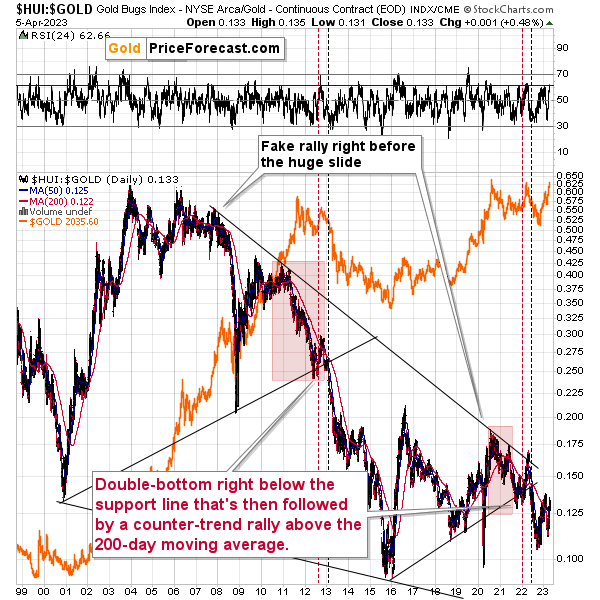

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw in 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI-to-gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

Recently, we saw a quick upswing in the ratio, but that’s not a game-changer – even the biggest declines had corrections in the past. In fact, the correction appears to be over, as the ratio declined sharply. This is yet another indication that the huge, medium-term downswing is already underway.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices for gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

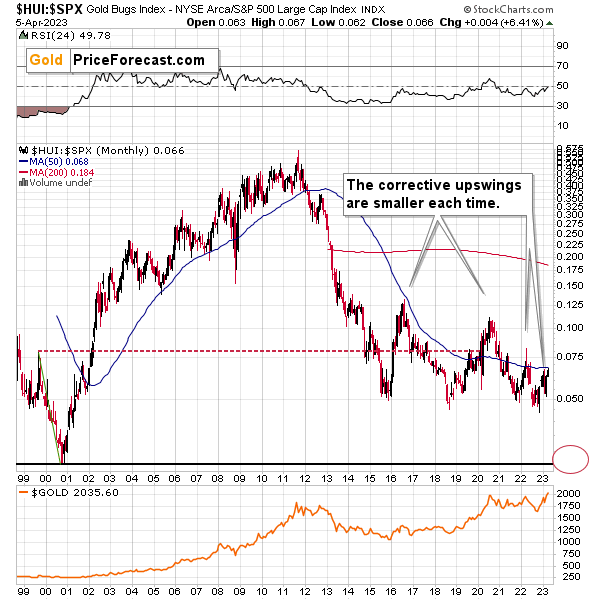

Interestingly, the situation in the gold stocks to other stocks ratio (HUI Index vs. S&P 500 Index) provides the same implications but from a different angle.

The corrective upswings that we’ve been seeing since 2015 are getting smaller and smaller. The current one is visibly smaller than what we saw last year.

Consequently, it seems that the ratio is ripe for a breakdown below the 0.05 level. The next support is provided by the all-time low of 0.026. And yes, with the ratio at 0.065 right now, this implies a decline of about 60%. If the HUI Index were to decline by 60% right now, it would have to move to about 100. If the stock market declined as well, it would imply the HUI was even lower.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks), and that’s exactly what’s likely to happen.

Just like what we saw in the case of copper and gold, world stocks corrected about 61.8% of their preceding decline. And that’s extremely bearish given the similarity to 2008.

Please note that the initial decline is now bigger than what we saw in 2008. Back then, stocks corrected about 61.8% of their initial decline before tumbling. And exactly the same thing happened recently!

Also, the RSI just turned south and back in 2008; that was the final confirmation before the waterfall selling.

Just as the 2008 rally wasn’t bullish, the most recent corrective upswing wasn’t bullish at all.

Real interest rates are rising, which is bad news for businesses! People appear to live on “hopium,” expecting the Fed to turn dovish and throw money on the market, but the data doesn’t support this outcome at all.

Given the analogy to 2008 and the fact that the initial slide was bigger this time, the following slide could be even bigger than what we saw in 2008. Naturally, this would be profoundly bearish for junior mining stocks.

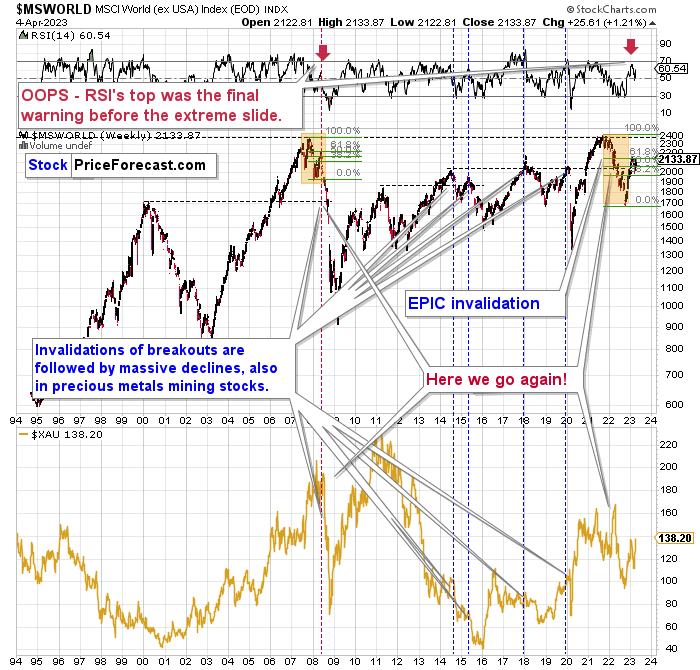

This means that nothing really changed, and the situation remains extremely bearish based, i.e., on the analogy to what we saw after previous invalidations of long-term breakouts.

As a reminder, in early 2022, I wrote that the situation was very bearish as invalidations of previous breakouts were usually followed by massive declines – not just in stocks but also in precious metals.

When stocks invalidated their 2006 breakout in 2008, their prices truly crumbled.

We also saw that on a smaller scale in 2014, 2015, and early 2018.

We’re seeing it right now.

To clarify, we’re actually seeing the aftermath of the invalidation. The huge decline is already taking place.

The difference between now and 2008 is that back then the slide was more volatile, and we didn’t really see a visible correction during the plunge. This time, the decline is more measured, and we saw a correction to one of the most classic retracements imaginable – the 38.2% one. This correction doesn’t change the trend, which remains down.

Based on what happened in 2008, it seems that stocks are about to move much lower in the following months.

The lower part of the chart features the XAU Index, a proxy for both gold stocks and silver stocks.

First of all, this comparison of mining stocks and other stocks could appear shocking, and rightfully so.

The XAU Index is well below its… 1995 highs (yes, miners are really so weak), while world stocks are much higher.

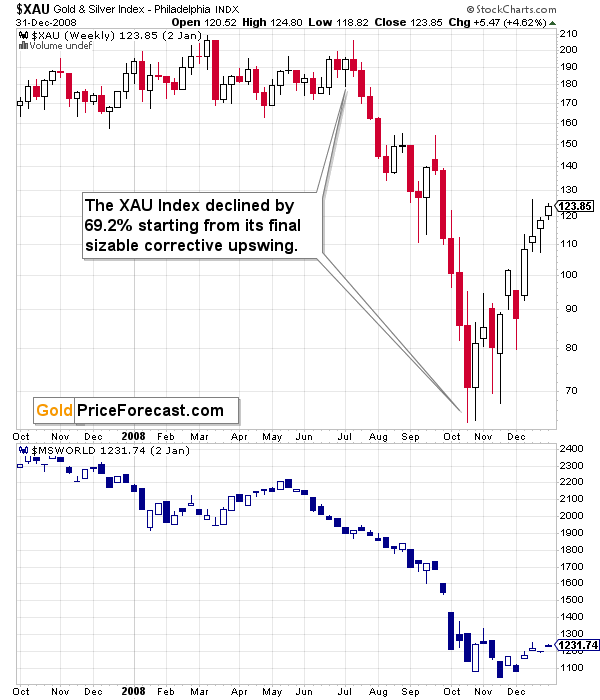

The second shocker is how far and how fast miners declined in 2008. Starting with the final corrective upswing, the mining stocks index declined by a breathtaking 69.2%!

Less than a third of the starting value.

It took just a few months for this decline to materialize.

So far this year, the XAU Index has declined by 18.7%, counting from the yearly high to yesterday’s intraday low.

And so far this year, the GDXJ ETF has declined by 19.3%, using the same measurements.

As a result, the performance of both may be roughly comparable, or — more likely — junior miners may decline more due to their closer link to the general stock market. This means that based on the above-mentioned analogy to 2008, we can’t rule out a decline by about 70% (or more!) in the GDXJ starting at the recent short-term high ($41.16).

Shaving off 70% of that value leaves us with $12.35 as the possible downside target for the GDXJ ETF.

Impossible? It has already happened! (In the XAU, as the GDXJ wasn’t trading at that time).

So, yes, the outlook for mining stocks is truly extremely bearish for the following months.

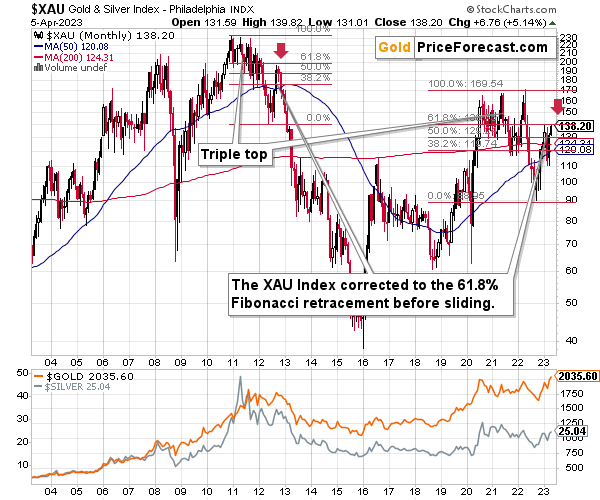

Also, speaking of the XAU Index, let’s take a look at its chart.

After all, that’s where I see one of the key developments that happened this week.

How high did the XAU Index correct in a sharp manner back in 2021 before sliding from above 200 to below 40 (eventually, and below 90 in several months)?

It corrected to more or less its 61.8% Fibonacci retracement level. And the initial slide happened after a triple-top pattern.

Interestingly, we see exactly the same thing right now. The XAU Index first declined sharply after a triple-top pattern, and now it has just corrected approximately to its 61.8% Fibonacci retracement.

This is a screaming long-term sell signal.

Also, please note the obvious. The XAU Index is not only below its 2011 high. It’s not only below its 2008 high. It’s even below its 2006 high. Yes, the situation is ridiculously bearish.

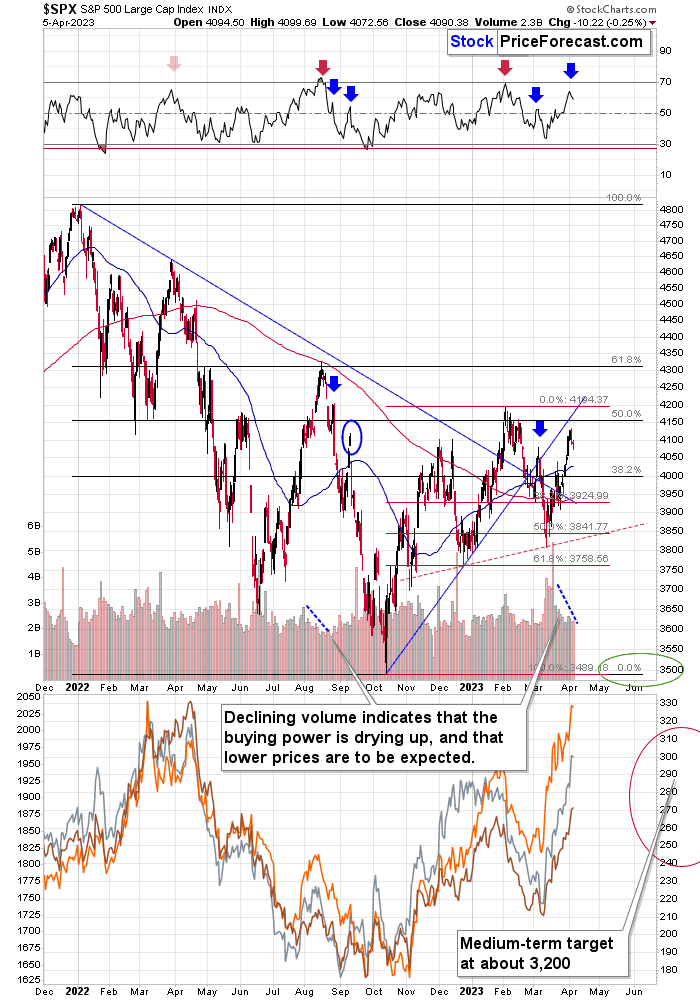

Let’s take a look at the markets from a more short-term point of view and from the U.S. perspective.

On a short-term basis, it looks like the small head-and-shoulders formation is finally going to end up being a broader head-and-shoulders formation.

The red, dashed line marks the neck level of the pattern. The right shoulder is likely forming at slightly higher levels, but besides that, the pattern is quite symmetrical.

While the RSI is not at 70, it is at the levels that stopped the March 2022 and the late 2022 rallies.

This, plus declining volume, suggests that the turnaround is either here or very, very near.

Consequently, we might not need to wait another week or two before seeing a top and the subsequent decline in junior mining stocks.

In fact, we might have just seen it, or we might see it within the next couple of days.

Why is this important for gold and silver investors and traders? Because the last two big moves took place more or less in line with each other – in stocks and in precious metals (and miners). The slide in stocks could also trigger something similar in the case of commodities like crude oil. The same thing is likely to happen again this time, especially given what’s happening in the USD Index.

The USD Index is after a sharp corrective downswing that is very similar to what happened in the USDX during the 2008 corrective rally in gold.

Please keep in mind that the USD Index tends to reverse close to the end of the month. I marked the previous such reversals with vertical dashed lines. This tendency is surprisingly (given its simplicity) useful.

And, well, we are still early in April, and we just saw a sign of strength yesterday – this might have confirmed the final bottom for this decline.

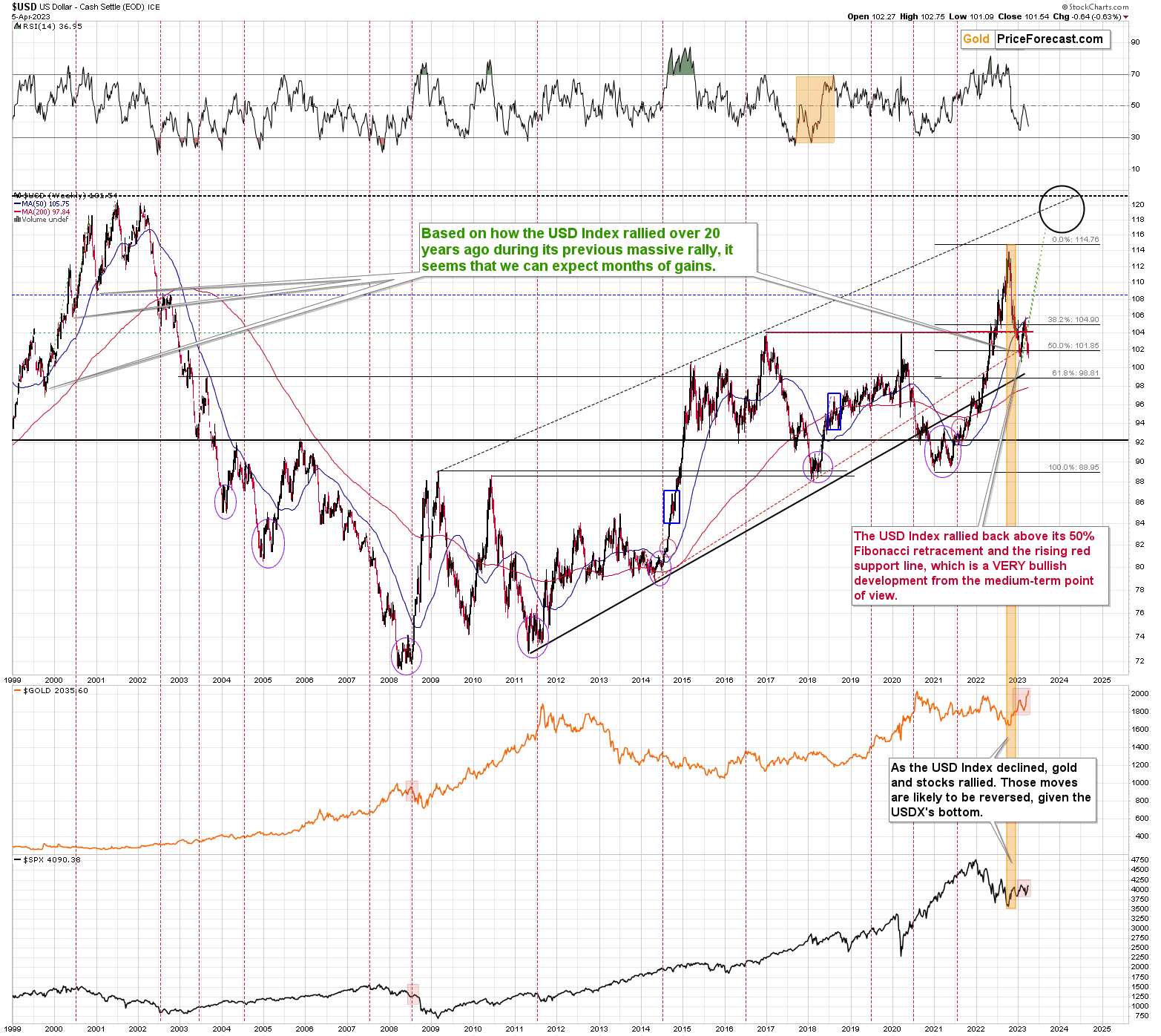

All this suggests that the USDX is ready to rally further. The most important details are present on the long-term chart, though.

Let’s zoom out.

The key thing to keep in mind is that what we see right now – along with the most recent very short-term decline – is something that we also saw in mid-2008, right before the USD Index’s sharpest rally in decades. Interestingly, we also saw it in 2011, right before gold’s top.

The preceding bottom was not a single V-shaped low, but rather a bottom that consisted of a few separate bottoms. The final short-term decline started with RSI at about 50. And guess what – the current short-term decline also started with the RSI close to 50.

Consequently, given all the other links to 2008, it seems that a big rally in the USD Index is just around the corner.

The implications are very bearish for the precious metals sector.

Given the situation on the stock market – especially in world stocks – the situation is particularly bearish for junior mining stocks.

Just as the night is darkest before the dawn, it “seems most bullish” right before the biggest slides.

Stay strong.

===

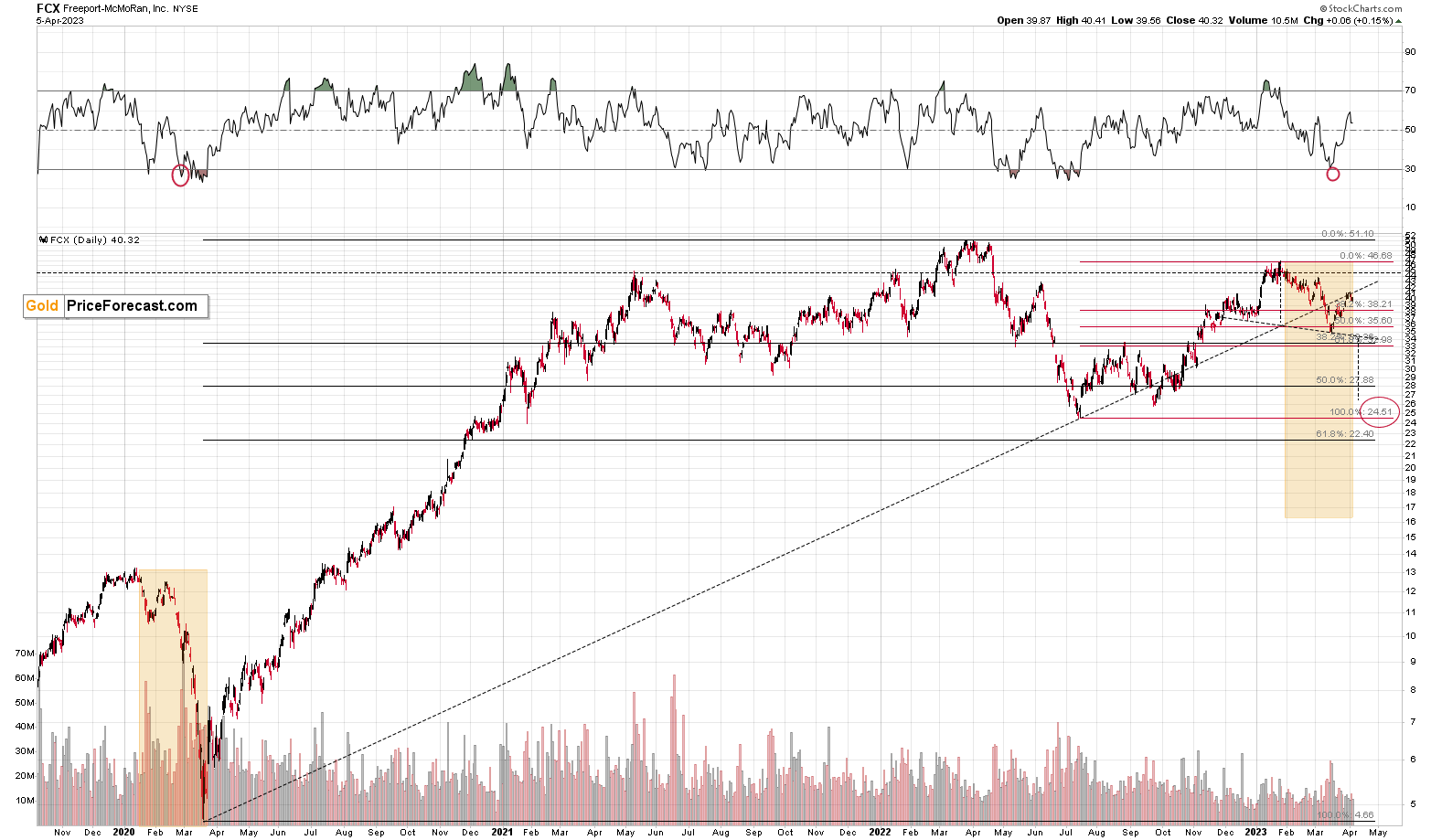

It seems that we have another trading opportunity in the FCX – another shorting opportunity.

I already wrote about FCX’s medium-term outlook (which is terrible) based on the situations in stocks, copper, and – to some extent – gold, and based on the analogy to 2008. I won’t got into those details today, but you can find them in the analysis that I posted about a month ago.

Today, I would like to emphasize that the FCX seems to have verified an important long-term breakdown, by moving to the rising resistance line and then moving back down.

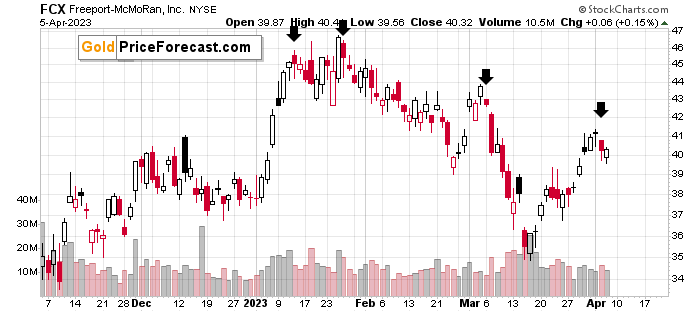

And on a short-term side of things, we see that the FCX did what had done twice right after tops.

After topping, the FCX’s price has been doing this specific initial decline that is then followed by a slight intraday corrective upswing. I marked three previous cases with black arrows. And we just saw the same thing once again.

Given all the background information that I’m not discussing today, but that I discussed previously, and given those above-mentioned short-term signs, I think that a short position in the FCX is now justified from the risk to reward point of view.

How low can the FCX fall this time? Quite possibly to the $24 - $27 area. I’ll fine-tune the target as we move closer to it, but for now, I’m treating the upper border of the above as the target.

===

On a side note, while commenting on analyses, please keep the Pillars of the Community in mind. It’s great to provide points that help others be more objective. However, it’s important to focus on the facts and discuss them in a dignified manner. There is not much of the latter in personal attacks. As more and more people join our community, it is important to keep it friendly. Being yourself, even to the point of swearing, is great, but the point is not to belittle other people or put them in a position of “shame” (whether it works or not). Everyone can make mistakes, and everyone does, in fact, make mistakes. We all here have the same goal: to have a greater understanding of the markets and pick better risk-to-reward situations for our trades. We are on the same side.

On another – and final – side note, the number of messages, comments etc. that I’m receiving is enormous, and while I’m grateful for such engagement and feedback, I’m also starting to realize that there’s no way in which I’m going to be able to provide replies to everyone that I would like to, while keeping any sort of work-life balance and sanity ;) Not to mention peace of mind and calmness required to approach the markets with maximum objectivity and to provide you with the service of the highest quality – and best of my abilities.

Consequently, please keep in mind that I will not be able to react / reply to all messages. It will be my priority to reply to messages/comments that adhere to the Pillars of the Community (I wrote them, by the way) and are based on kindness, compassion and on helping others grow themselves and their capital in the most objective manner possible (and to messages that are supportive in general). I noticed that whatever one puts their attention to – grows, and that’s what I think all communities need more of.

Sometimes, Golden Meadow’s support team forwards me a message from someone, who assumed that I might not be able to see a message on Golden Meadow, but that I would notice it in my e-mail account. However, since it’s the point here to create a supportive community, I will specifically not be providing any replies over email, and I will be providing them over here (to the extent time permits). Everyone’s best option is to communicate here, on Golden Meadow, ideally not in private messages (there are exceptions, of course!) but in specific spaces or below articles, because even if I’m not able to reply, the odds are that there will be someone else with insights on a given matter that might provide helpful details. And since we are all on the same side (aiming to grow ourselves and our capital), a to of value can be created through this kind of collaboration :).

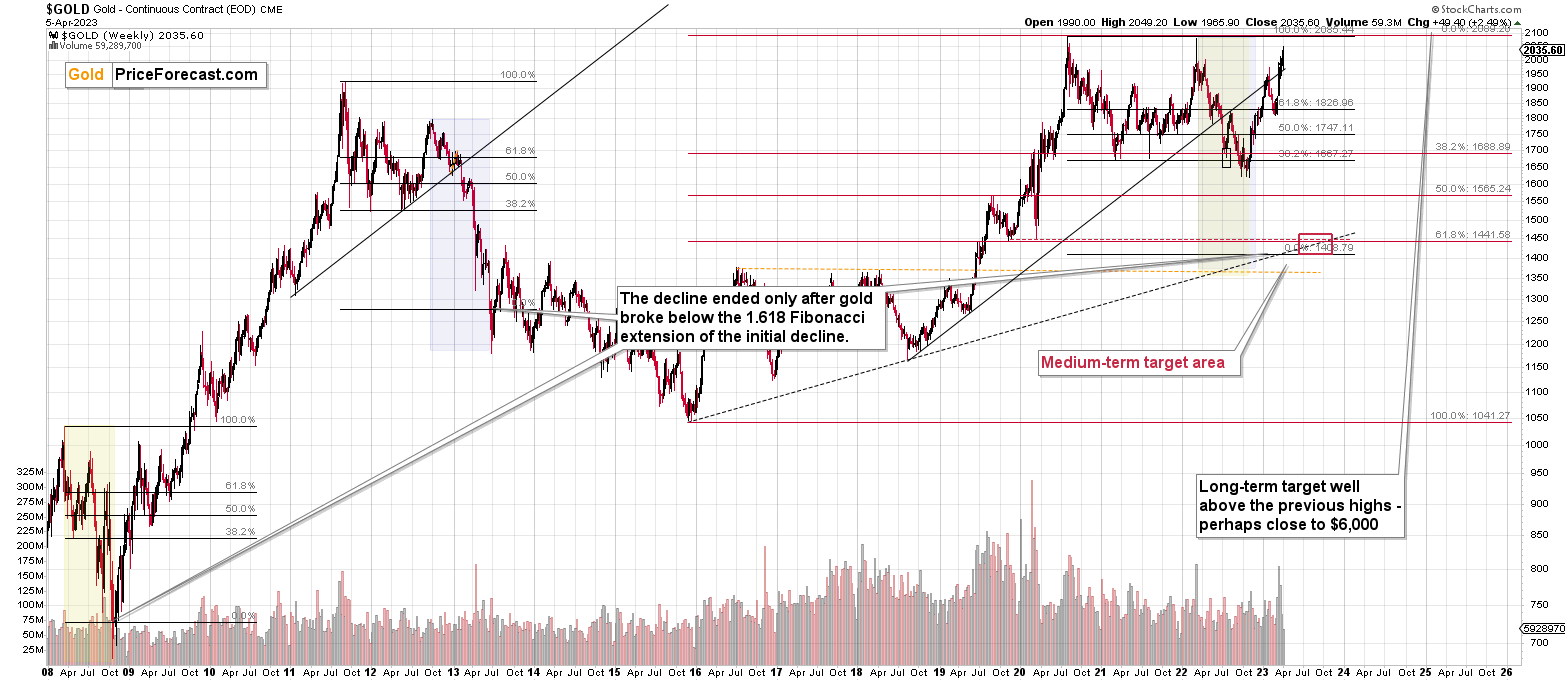

Overview of the Upcoming Part of the Decline

- It seems that we’re seeing another – and probably final – corrective upswing in gold, which is likely to be less visible in the case of silver and mining stocks.

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Letters to the Editor

Please post your questions in the comments feed below the articles, if they are about issues raised within the article (or in the recent issues). If they are about other, more universal matters, I encourage you to use the Ask the Community space (I’m also part of the community), so that more people can contribute to the reply and enjoy the answers. Of course, let’s keep the target-related discussions in the premium space (where you’re reading this).

Summary

To summarize, we recently took profits from the additional FCX trade (right before the trend reversed!) and the current short position in junior mining stocks is – in my view – poised to become very profitable in the following weeks and perhaps days. Based on the information that we have today, it seems like it might be a good moment to enter another short position in the FCX for another round of extra profits.

Things might appear chaotic in the precious metals market right now, but based on the analogy to the previous crises (2020 and 2008), it’s clear that gold, miners, and other markets are pretty much doing the same thing all over again.

The implications of this “all over” are extremely bearish for junior mining stocks. Back in 2008, at a similar juncture, GDX’s price was about to be cut in half in about a month! In my opinion, while the decline might not be as sharp this time, it’s likely to be enormous anyway and very, very, very profitable.

As a reminder, we still have a “promotion” that allows you to extend your subscription for up to three (!) years at the current prices… with a 20% discount! And it would apply to all those years, so the savings could be substantial. Given inflation this high, it’s practically certain that we will be raising our prices, and the above would not only protect you from it (at least on our end), but it would also be a perfect way to re-invest some of the profits that you just made.

The savings can be even bigger if you apply it to our All-inclusive Package (Stock- and Oil- Trading Alerts are also included). Actually, in this case, a 25% discount (even up to three years!) applies, so the savings are huge!

If you’d like to extend your subscription (and perhaps also upgrade your plan while doing so), please contact us – our support staff will be happy to help and make sure that your subscription is set up perfectly. If anything about the above is unclear, but you’d like to proceed – please contact us anyway :).

As always, we'll keep you – our subscribers – informed.

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Friday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief