Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

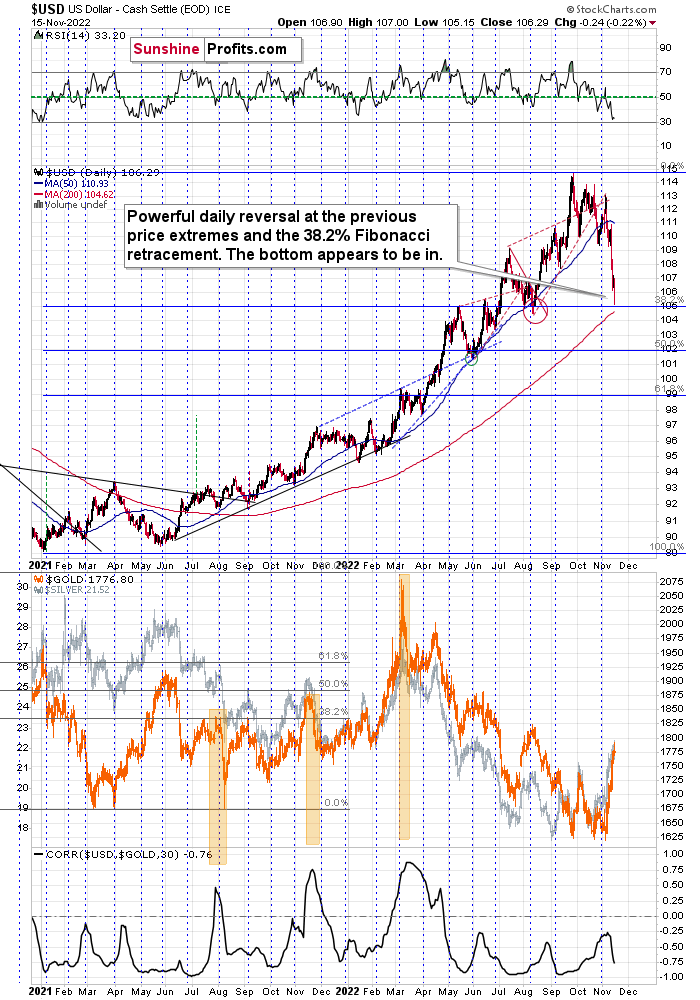

In yesterday’s analysis, I wrote the following about the USD Index:

For example, the USD Index could decline to its strong support level at the 38.2% Fibonacci retracement and the August 2022 low as well as the May 2022 high. Such a move would likely imply the RSI at about 30, which would be a crystal-clear signal for many traders that the bottom is in.

To clarify, if that happened, the USD Index would be as oversold from a short-term point of view, as it was at its 2021 bottom – when it was trading at about 90.

Here’s what happened:

The USDX moved very close to the above-mentioned support levels, and it moved back up before the end of the day. The only reason that the RSI didn’t move to 30 is because the USDX declined only on an intraday basis. This means that from the RSI’s point of view, the situation is only “very bullish,” not extremely so. However, given the reversal nature of yesterday’s session, the outlook just became even more bullish, and it seems to me that the bottom is in.

This means that the top in the precious metals market is also likely in or at hand, especially given the S&P 500’s inability to break through its own 38.2% Fibonacci retracement.

I’ll explain more in the video below:

Having said that, let’s take a look at the market from a more fundamental point of view.

More Than Meets the Eye

While the S&P 500 closed higher on Nov. 15, gold, silver, and mining stocks ended the day in the red. Yet, with the USD Index and the U.S. 10-Year Treasury yield declining, risk-on sentiment still permeates throughout the financial markets.

However, with the excitement largely driven by a ‘dash for trash,’ the leaders of this risk rally highlight why it’s unlikely to last.

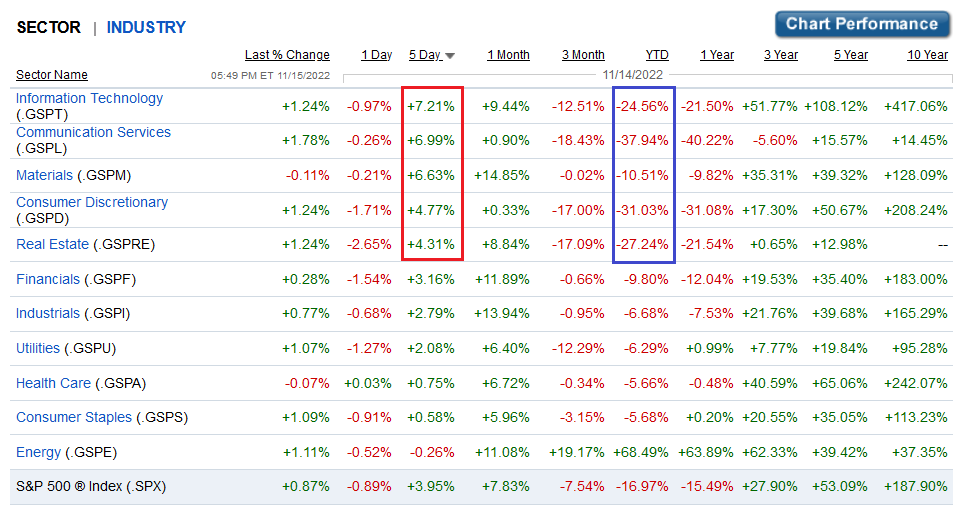

For example, the red box below shows how information technology, communication services, consumer discretionary, and real estate have been four of the five best-performing sectors over the last five days. In contrast, the blue box below shows how they are the four worst-performing sectors year-to-date (YTD).

As such, the results highlight how the S&P 500’s recent run has been led by the 2022 laggards, which means short-covering has been a substantial component.

Please see below:

Source: Fidelity

Source: Fidelity

In addition, while the materials sector is the fifth-worst-performing sector YTD, it’s been the third-best performer over the last five days. So, with the buy-the-dip crowd purchasing the most beaten-down assets, the price action is relatively normal for a bear market. Moreover, with similar 2022 countertrend rallies not stopping these sectors from hitting new lows, this time should be no different.

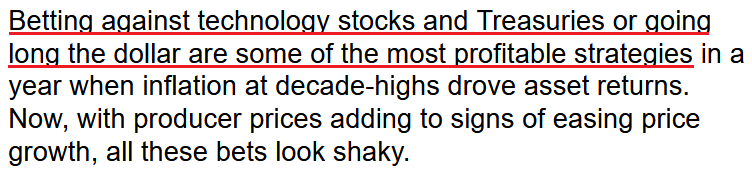

To that point, the volatility across the FX, bond, stock, and commodities markets can be explained by positioning. Bloomberg reported on Nov. 15:

“The most crowded trade on Wall Street – long inflation – is suddenly getting crushed like never before in the post-lockdown era, sparking a spate of forced deleveraging among a broad cohort of institutional funds that’s adding to cross-asset volatility (…).”

“Whether inflation has peaked or not is debatable, and investors as well as policy makers have been wrong on pretty much all price trends in recent years, time and time again. What’s less questionable is that a crowded trade threatens to unwind all at once, with short covering among fast-money funds adding to market instability.”

Please see below:

Source: Bloomberg

Source: Bloomberg

Thus, while I warned throughout 2021 that rampant inflation would force the Fed’s hand, the 2022 rise in Treasury yields and rate hike expectations means that our thesis became the consensus. Therefore, with crowded positioning unwinding in recent days, the shift has uplifted the laggards and hurt the leaders.

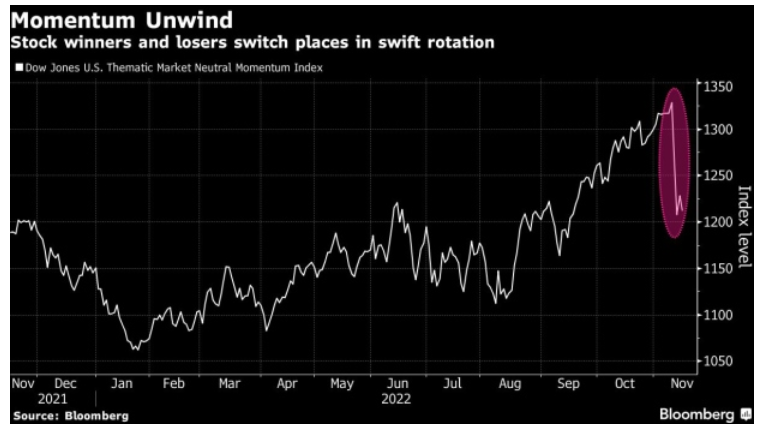

Please see below:

To explain, the white line above tracks the Dow Jones U.S. Thematic Market Neutral Momentum Index. For context, the index measures the performance of a long-high, short-low momentum asset portfolio. If you analyze the right side of the chart, you can see that the white line has declined precipitously recently.

However, while all of the data may seem troublesome, they are highly positive developments.

For example, when Bloomberg writes that “these bets look shaky” when referring to the long dollar, short bonds, and short tech, the anxiety is the preferct sentiment indicator of how the thesis is no longer the consensus. In addition, with the PMs often suffering in tandem with bonds and tech stocks (all three benefit from QE), their fortunes often rise and fall together.

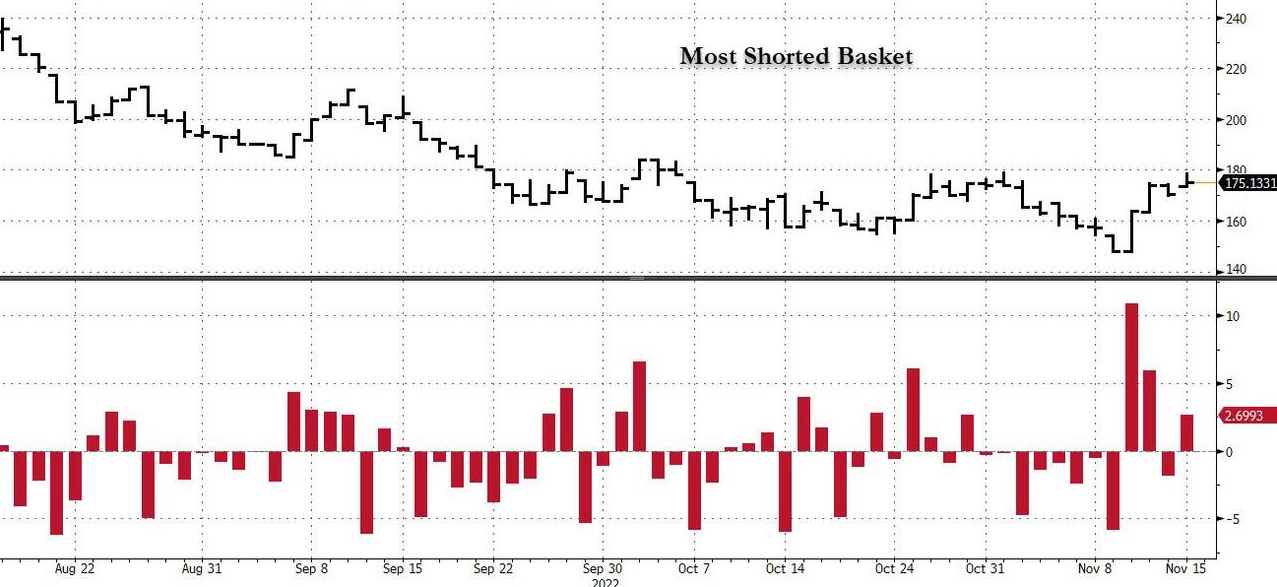

Second, the sector performance highlights why the PMs’ squeeze has likely run its course, as all of these assets will need fresh buyers to support higher prices. As evidence, Goldman Sachs’ basket of the most-shorted stocks is up by ~18% over the last four days.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the black line at the top half of the chart tracks the performance of Goldman Sachs’ most-shorted basket, while the red bars at the bottom half add visual clarity. If you analyze the right side of the chart, you can see that the red bars rose materially, which means the stock market’s short-covering surge is much less bullish than it seems.

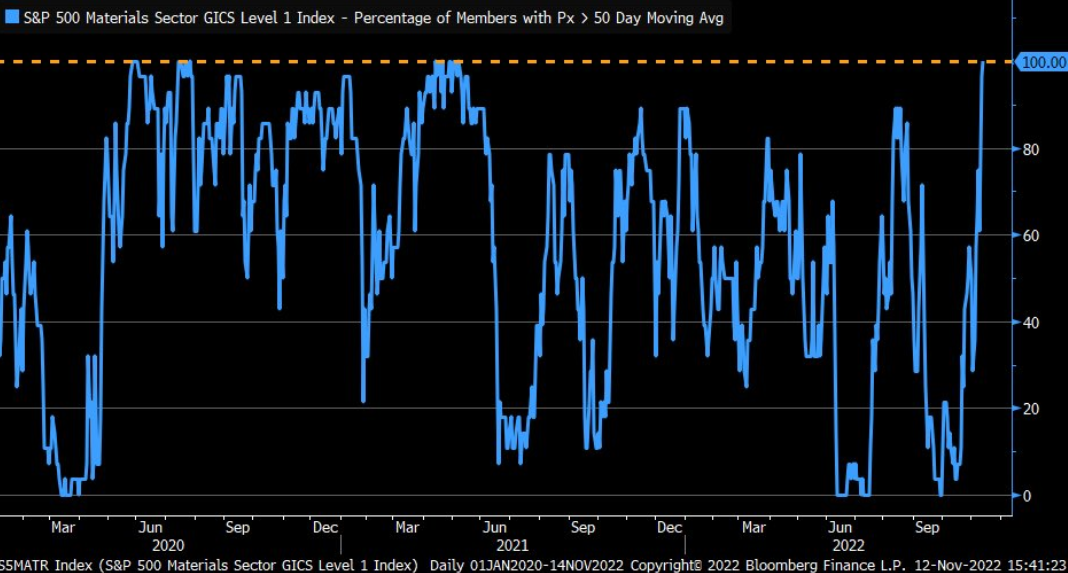

Third, I noted how the materials sector is overbought on a relative basis; and with the group declining by 0.11% on Nov. 15 (the most among all 11 S&P 500 sectors), investors may soon regret owning the PMs at these levels, especially mining stocks. I wrote on Nov. 15:

The blue line above tracks the percentage of companies in the materials sector trading above their 50-day moving average. For context, metals and mining make up roughly 14% of the sector. If you analyze the right side of the chart, you can see that the figure stands at 100%, which is a sizable shift from the 0% present in late September.

As a result, the data highlights why we’re likely much closer to the top than the bottom; and notice how abnormally high and low readings are nearly impossible to sustain? This is because periods of too much pessimism and optimism often revert to the average when investors take a thoughtful look at the fundamentals.

Therefore, since the metric can’t go any higher, a material reversal should result in substantial declines for gold, silver, and mining stocks over the medium term.

Overall, while the new narrative assumes that inflation is dead, bonds are a buy, and liquidity-fueled assets like tech stocks and the PMs are poised for new highs, the sentiment shift is bullish for our GDXJ ETF short position.

In a nutshell: when too many investors see things from our perspective, positioning gets crowded and the unwinding of bearish bets uplifts the metals. Conversely, when our thesis becomes contrarian once again, the PMs need sustainable fundamental and technical reasons to move higher, which we believe they lack.

So while the GDXJ ETF’s recent rally has not been fun, the fundamentals never changed, only sentiment did; and with that same sentiment now dangerously over-bullish, positioning supports another leg lower for gold, silver, and mining stocks.

Bad Bets

While the crowd believes that inflation will decline linearly without any economic or financial market suffering, history has been unkind to those with unrealistic expectations. In reality, inflation is highly difficult to slay, as the stop-start nature of it means that one month’s celebration is the next month’s disappointment.

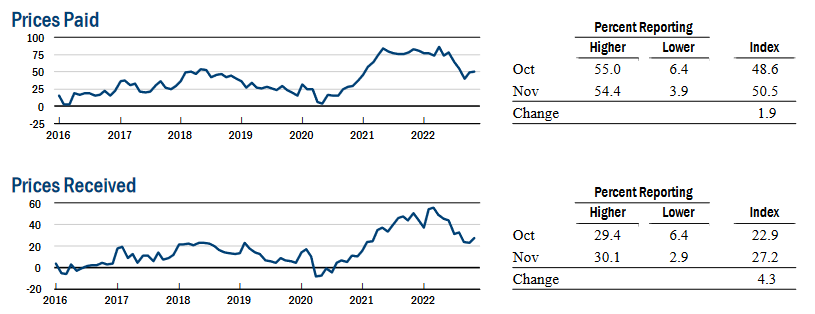

Speaking of which, with the New York Fed releasing its Empire State Manufacturing Survey on Nov. 15, the conundrum was on full display. An excerpt read:

“The prices paid index was little changed at 50.5, suggesting that input prices increased at about the same pace as last month, while the prices received index rose four points to 27.2, pointing to a small pickup in selling price increases.”

Please see below:

Source: New York Fed

Source: New York Fed

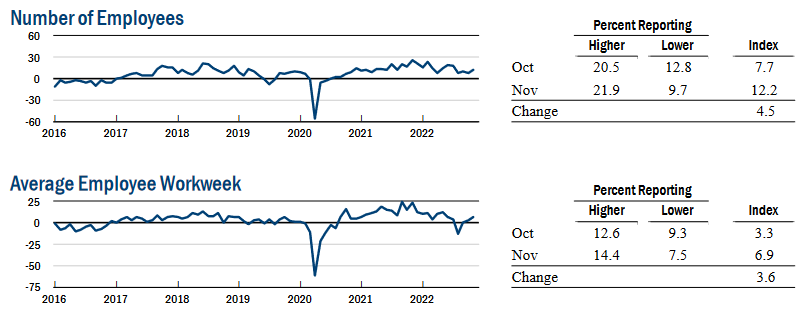

In addition:

“The index for number of employees climbed five points to 12.2, pointing to an increase in employment levels. The average workweek index edged up to 6.9, signaling a small increase in hours worked.”

Please see below:

Source: New York Fed

Source: New York Fed

As a result, the data in New York State showed re-accelerating inflation and resilient employment, both of which are bullish for the U.S. federal funds rate (FFR).

Likewise, Fed Governor Lisa Cook said on Nov. 15 that inflation is “much too high” and that “monetary policy is, as we all know, a blunt instrument;” and with U.S. employment still on solid footing, she added, “The focus for the Federal Reserve is on addressing inflation, and we want a sustainable, strong labor market.”

Also, Philadelphia Fed President Patrick Harker said on Nov. 15:

“In the upcoming months, in light of the cumulative tightening we have achieved, I expect we will slow the pace of our rate hikes as we approach a sufficiently restrictive stance. I expect we will hold at a restrictive rate for a while to let monetary policy do its work.”

So, while Fed officials want to reduce the pace of future rate hikes, no one expected the FFR to rise by 75 basis points at every meeting. Remember, our 2023 FFR projection is 4.5% to 5.5%, and Harker (and other Fed officials) were firm about wanting to “hold at a restrictive rate for a while.”

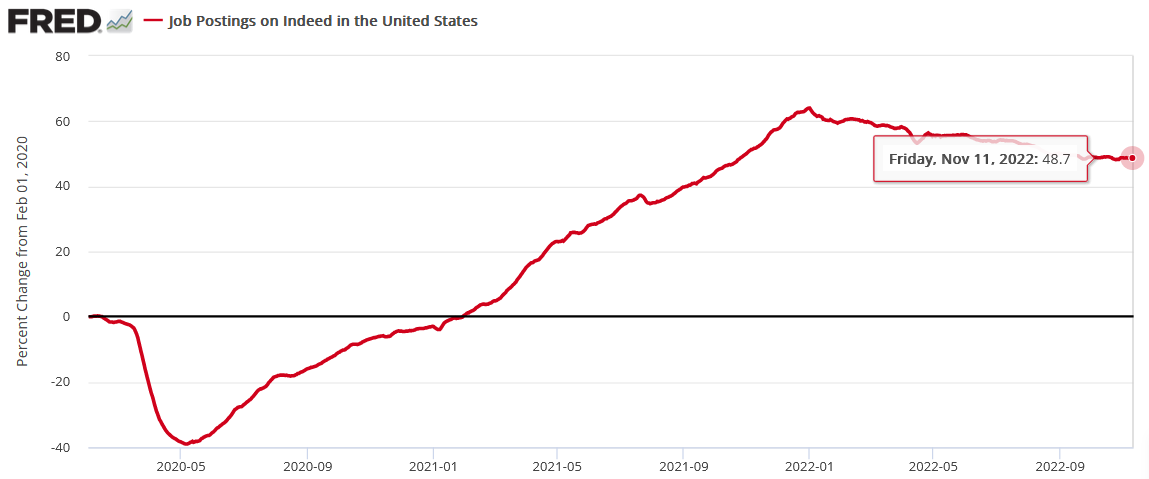

Therefore, only a major recession that culminates in a collapse in the U.S. labor market should prompt the Fed to cut the FFR; and with Indeed revealing on Nov. 14 that U.S. job postings on its site are still 48.7% above their pre-pandemic baseline (for the week ending Nov. 11), we’re far from that level of demand destruction.

As such, the medium-term outlook is bullish for the FFR, real yields, and the USD Index.

The Bottom Line

While misguided optimism has pushed risk assets higher, the pendulum has shifted from depression to euphoria. In other words, it was only a month ago that the crowd expected the S&P 500 to hit 3,400. Yet, now, all is forgotten, and a new bull market has begun. However, while sentiment can keep assets uplifted in the short term, the fundamentals are highly treacherous. Consequently, the lack of sustainable upside catalysts should prove problematic for gold, silver, mining stocks, and the S&P 500 over the medium term.

In conclusion, the PMs declined on Nov. 15, as the materials sector underperformed its peers. Moreover, while the bulls seem comfortable at the moment, their optimism should turn to pessimism in the months ahead. As a result, the PMs’ countertrend rallies should give way to new lows before this bear market ends.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

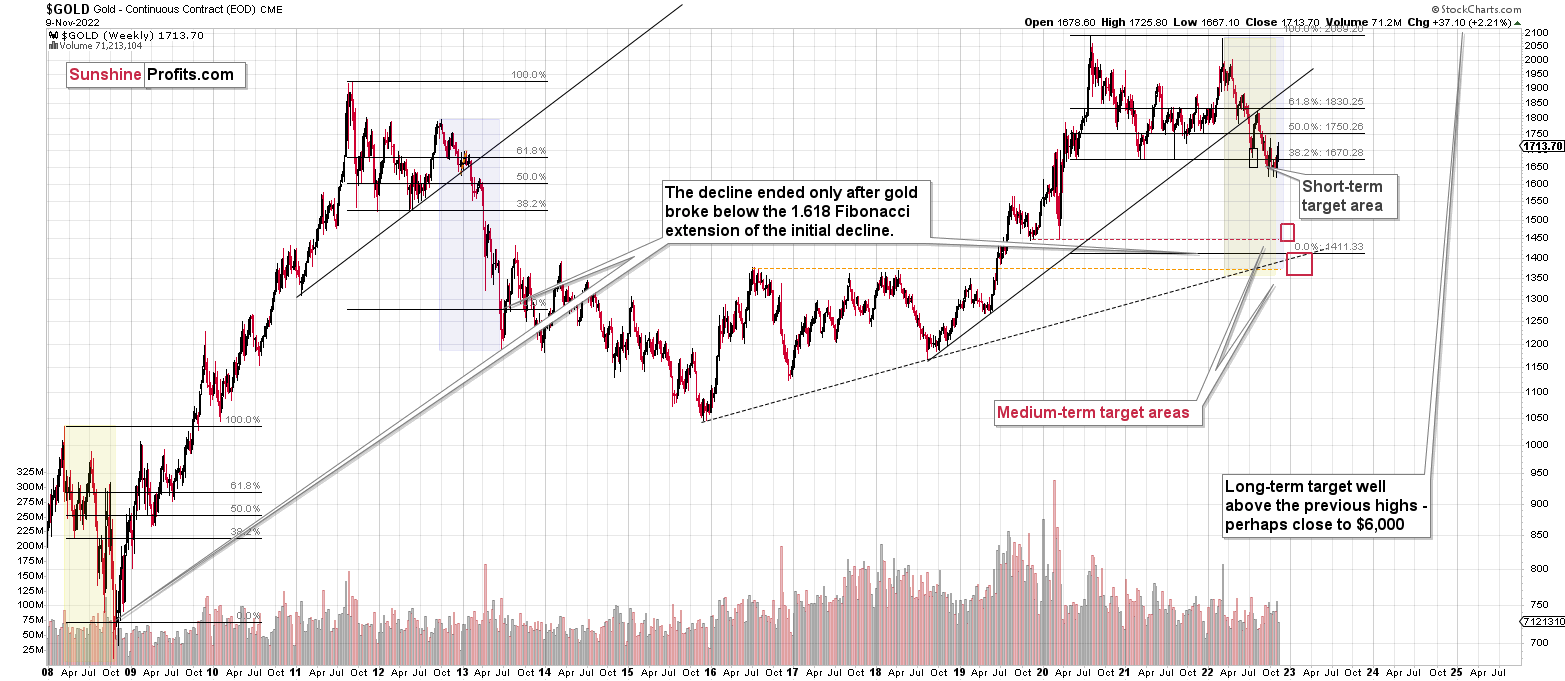

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, while the precious metals sector moved higher last week, it seems that it’s just a part of a bigger – bearish – analogy to what we saw in 2008. I realize that volatile upswings generate a lot of emotions, but taking a calm, broad look at the markets shows that nothing really changed.

In fact, I would like to take this opportunity to congratulate you on your patience with this trade (and I’m grateful for your understanding that not every corrective upswing can be “caught” in trading terms). Many investors and traders panic, and get out of the market exactly at the wrong time, but your patience and self-discipline mean that you’re poised to make the most of what the market brings us this and next year.

Moving back to the market, it appears to be yet another time when the markets are incorrectly expecting the Fed to make a dovish U-turn, and based on this, the part of the 2008 decline where we saw the biggest corrective upswing materialized.

In my opinion, the current trading position is going to become profitable in the following weeks, and quite possibly in the following days. And while I can’t promise any kind of performance, I fully expect it to become very profitable before it’s over and to prolong our 2022 winning streak.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $20.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $27.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $12.32

SLV profit-take exit price: $11.32

ZSL profit-take exit price: $74.87

Gold futures downside profit-take exit price: $1,504

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $18.47

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $46.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief