Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Nothing really changed during yesterday’s trading and nothing major is happening in today’s pre-market trading, so today’s technical analysis will be rather brief – points made previously simply remain up-to-date:

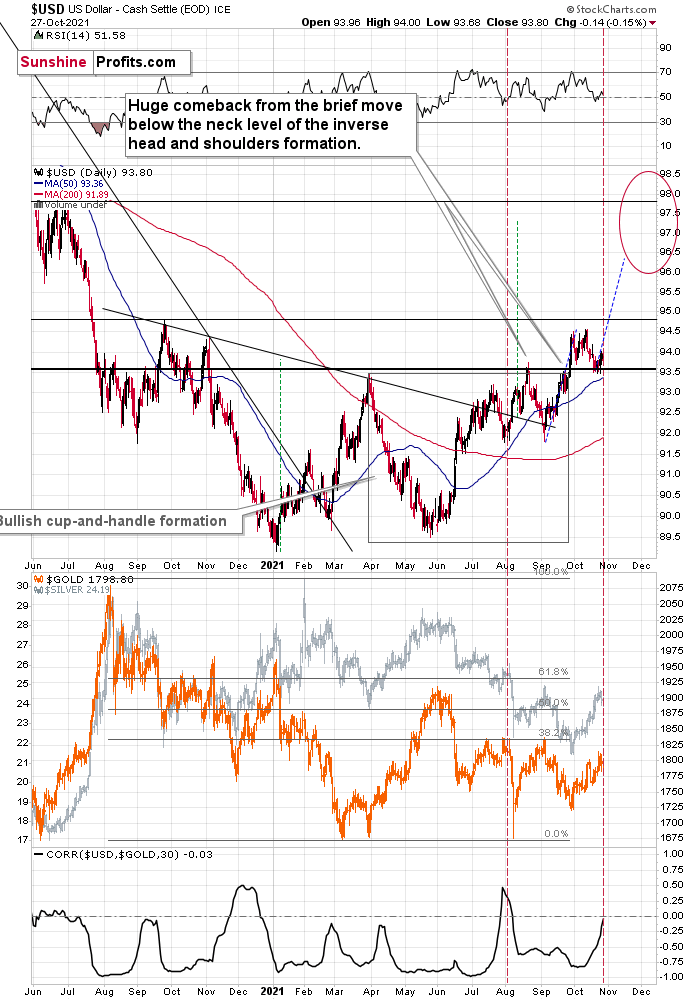

The situation now appears to be the same as it was at the beginning of August, where the bottom also took several days to form, but when the USD Index finally moved higher once again, gold plunged. To be precise, back then, the bottom formed over 5 trading days, and yesterday was the fifth trading day of the current bottom. On the sixth day – back then – the USDX did very little and gold declined modestly, and it was the seventh day when the action really started. And… the short-term decline was over on the very next day. It was not easy to catch this decline if one wanted to wait for a big confirmation that it was indeed taking place. It seems that the same – patient – approach is justified in the current situation.

The RSI indicator (upper part of the chart) continues to confirm this similarity.

On Tuesday, the USD Index ended the session 0.13 higher, so – just as in early August – it moved very little. Gold declined modestly back then, and, well, it moved lower by $13.40 on Tuesday, so it seems that it fits well. Gold moved up by $5.40 yesterday and it’s up by $5 in today’s pre-market trading (at the moment of writing these words), so it seems that history might repeat itself to a very big degree.

So far, very little is happening, but this might be the calm before the storm. Please note that even the increase in the correlation between gold and the USD Index (lower part of the above chart) confirms the early-August – now link. That’s the last time when the correlation was as high as it is right now.

If the history repeated itself to the letter, we would have a $100+ decline in gold this week. But since history rhymes more than it repeats, I think it’s more realistic to simply expect gold to fall substantially soon, without giving the decline just 2 days to materialize.

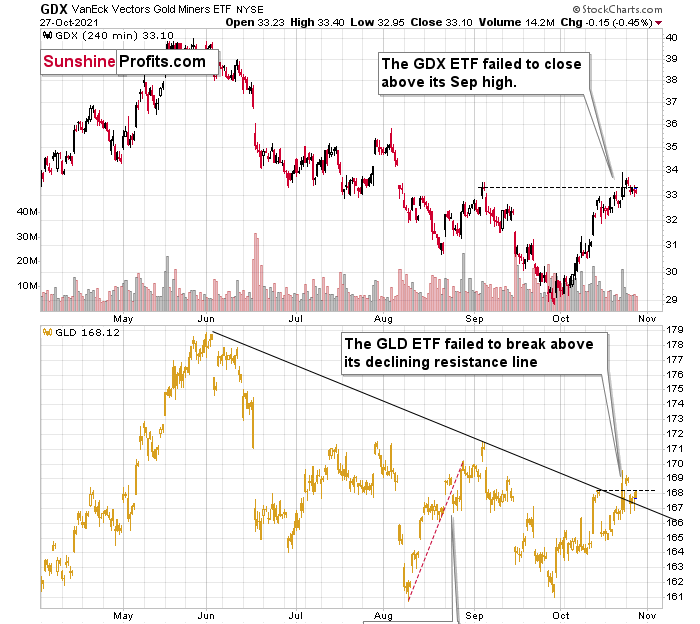

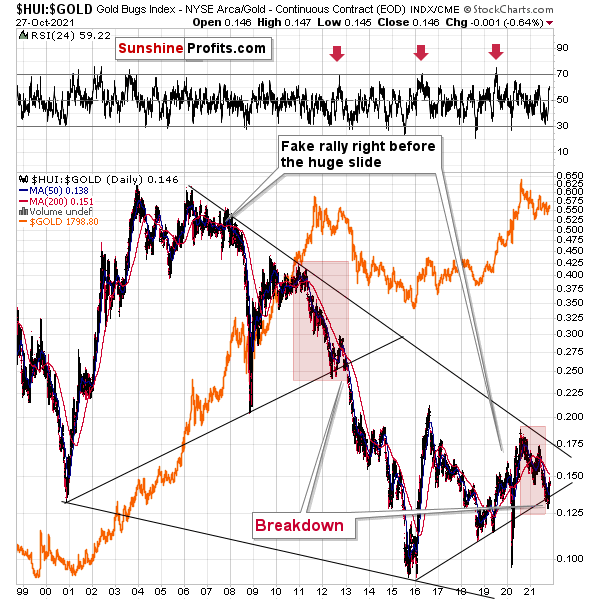

On Tuesday, I described the above chart as “another attempt”. Mining stocks (GDX ETF) once again failed to hold the move above their September highs, which is – of course – bearish. GLD failed to hold above its previous October highs as well. It did manage to close above the declining resistance line based on the previous highs, but given today’s pre-market rally, it’s doubtful if GLD will be able to hold this level for long.

There are different rules for confirming a breakout or breakdown, but in the precious metals sector, based on almost two decades of experience in it, I prefer to see three closes above or below a certain level to view the breakout or breakdown as confirmed. Gold / GLD hasn’t confirmed its breakout just yet (so far we’ve seen two daily closes in the GLD above the resistance/support line), and it seems to me that it won’t confirm it soon. Instead, another – big – downswing seems to be just around the corner.

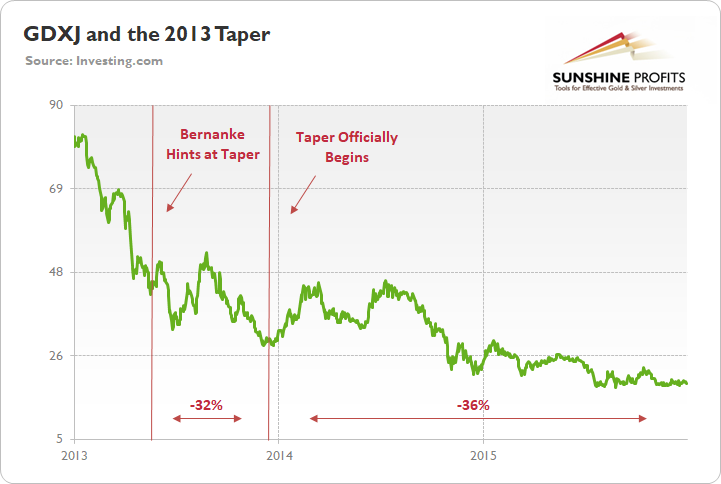

Also, let’s keep in mind how mining stocks (seniors and juniors) reacted to the previous tapering announcement. They moved higher only very initially, but then fell substantially.

To explain, the green line above tracks the GDXJ ETF from the beginning of 2013 to the end of 2015. If you analyze the left side of the chart, you can see that when Fed Chairman Ben Bernanke hinted at tapering on May 22, 2013, the GDXJ ETF declined by 32% from May 22 until the taper began on Dec. 18.

Moreover, the onslaught didn’t end there. Once the taper officially began, the GDXJ ETF enjoyed a relief rally (similar to what we’re witnessing now) as long-term interest rates declined, and the PMs assumed that the worst was in the rearview.

All in all, the technical picture for the precious metals sector looks bearish, even though the recent short-term corrective upswing might make one think otherwise.

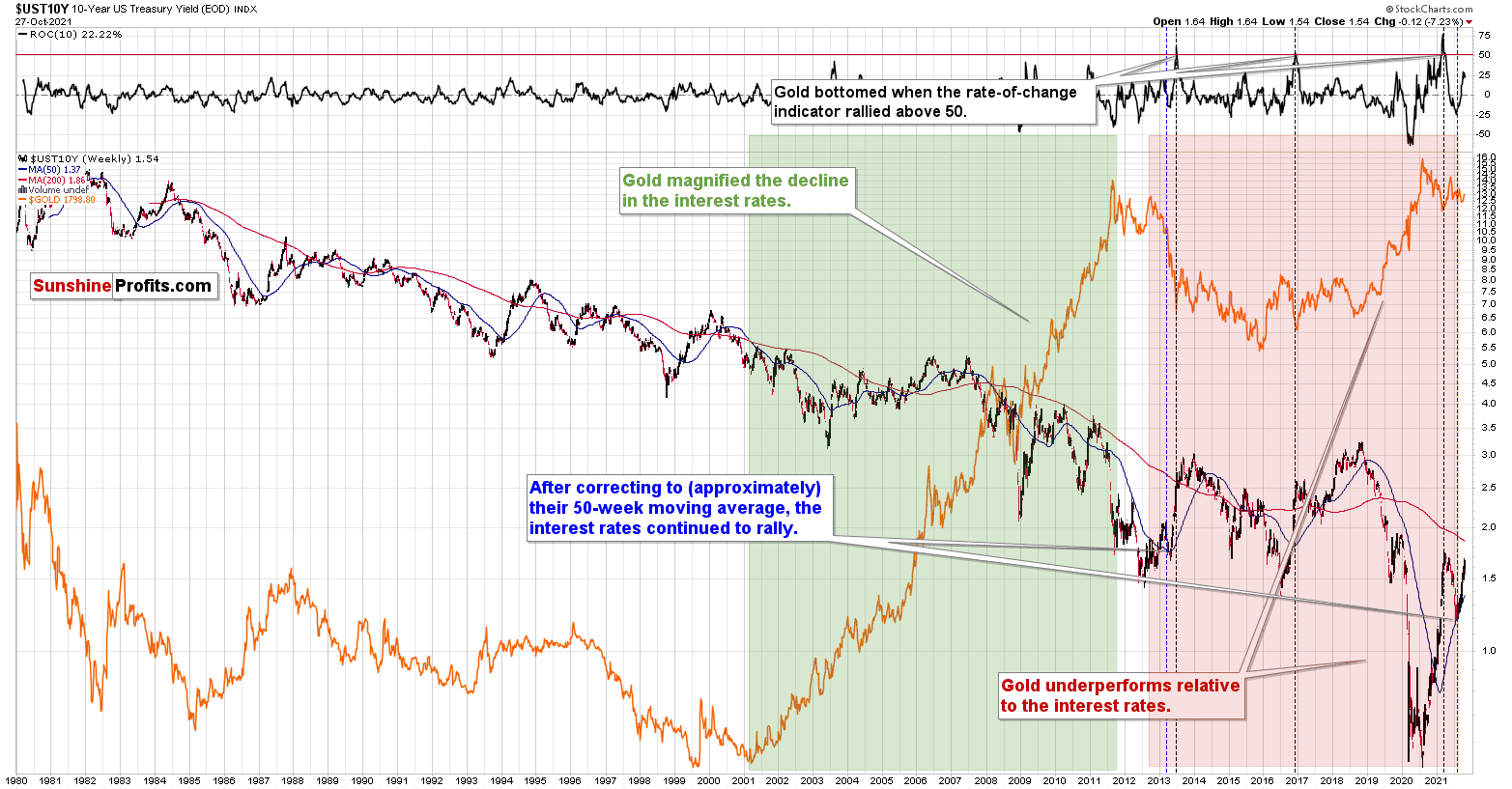

I was asked to comment on the recent developments in the 10-year yield – in my view, it continues to point to the similarity between now and the early part of 2013, right before the decline accelerated substantially.

The 10-year yield was after a profound rally and a short-term correction to its 50-week moving average, and now it’s rallying once again. This is what happened in early 2013 as well, and it then resulted in much lower gold prices over the following weeks. Will the situation repeat itself? It’s quite possible.

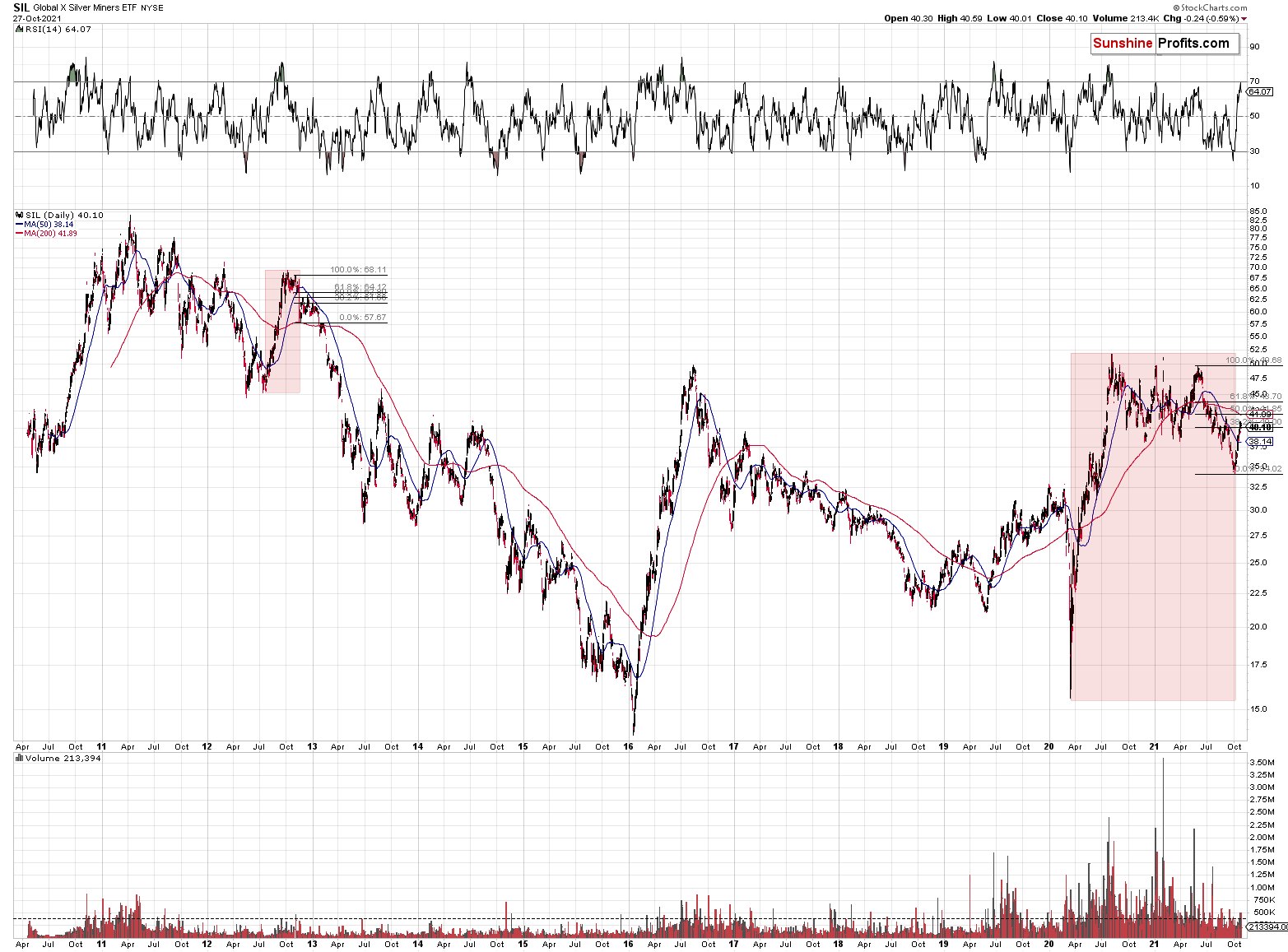

I was also asked about the recent performance of silver stocks.

In short, they performed quite well in the short term, but their performance so far this year has been very poor – much worse than the performance of the general stock market.

In the very recent past, silver stocks performed quite well relative to silver, just as gold stocks performed quite well relative to gold. However, as you’ve read in Monday’s flagship Gold & Silver Trading Alert, this is likely just a form of correction of the previous huge decline in the mining stock to metal ratios.

The question about the relative strength of mining stocks is effectively the question about the chart below.

The comeback above the rising resistance line was something that we also saw right before the huge 2013 slide. Consequently, just because we saw short-term strength in silver stocks and gold stocks vs. silver and gold, it doesn’t change the bearish case for the following weeks/months. Also, please note that yesterday mining stocks ended the day lower even though gold ended it higher, so the trend might have already reversed.

Having said that, let’s take a look at the markets from a more fundamental point of view.

A Sign of Things to Come

With the S&P 500 closing at the lows on Oct. 27 and mining stocks following suit, surging inflation is starting to rattle the financial markets. For example, the Bank of Canada (BoC) announced on Oct. 27 that it “is ending quantitative easing (QE) and moving into the reinvestment phase, during which it will purchase Government of Canada bonds solely to replace maturing bonds.”

And while the hawkish revelation is bullish for the CAD and bearish for the USD/CAD, the latter recovered roughly half of its intraday losses on Oct. 27. Moreover, while the USD/CAD accounts for 9.1% of the USD Index’s movement, the EUR/USD (57.6% of the USD Index’s movement) is the most important currency pair.

To that point, with the European Central Bank (ECB) poised to reiterate its dovish stance today and the Fed already pre-announcing its taper plans, U.S.-Eurozone inflation differentials should accelerate the Fed’s hawkish outperformance over the next several months.

To explain, the Dallas Fed released its Texas Service Sector Outlook Survey on Oct. 26. And while the headline index increased from 14.5 in September to 19.6 in October, the report revealed:

“Wage and price pressures rose in October to extremely high levels. The wages and benefits index increased to 34.7, a record high in the survey’s 14-year history. The selling prices index rose to 22.7, while the input prices index climbed to 47.0 – its highest reading since 2008.”

Likewise, the Dallas Fed’s Texas Retail Outlook Survey (also released on Oct. 26) sang a similar tune:

“Retail price pressures remained highly elevated in October, while wage pressures accelerated. The selling prices index slipped five points to 45.5 – still near a record-high level – while the input prices index rose from 50.1 to 56.3. The wages and benefits index spiked nearly 14 points to 38.3, near the survey’s record high.”

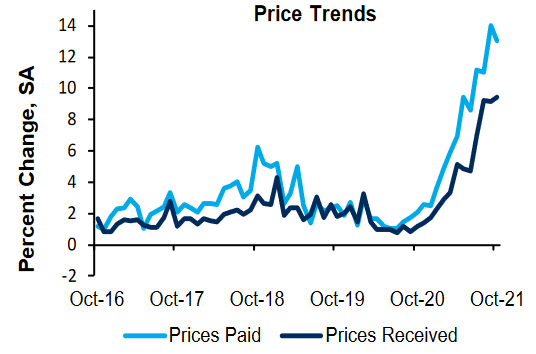

Moreover, the Richmond Fed also released its Fifth District Survey of Manufacturing Activity on Oct. 26. The headline index increased from -3 in September to 12 in October, and the prices received index hit a new all-time high.

Please see below:

Source: Richmond Fed

Source: Richmond Fed

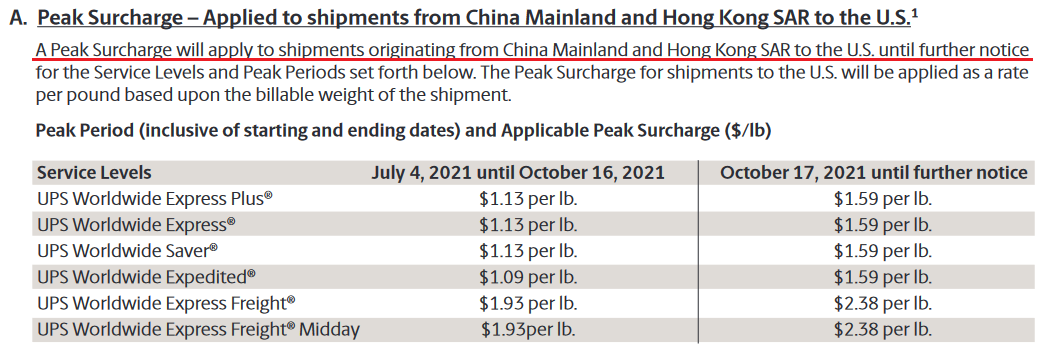

On top of that, the largest U.S. corporations continue to sound the inflationary alarm. For example, United Parcel Service (UPS) – a Fortune 500 company and one of the world's largest shipping couriers – released its third-quarter earnings on Oct. 26.

Prior to the print, UPS announced on Oct. 8 that it’s increasing its surcharges on U.S. “shipments originating from China Mainland and Hong Kong SAR” anywhere from 23% to 46% “until further notice.” For context, China accounts for 17.2% of YTD U.S. imports and ranks first among countries where the U.S. imports goods (Mexico is second at 13.8%).

Please see below:

Source: UPS

Source: UPS

And while UPS also increased its surcharges for several other types of foreign shipments to the U.S., the company announced on Oct. 26 that its domestic rate increases would hit the wire in the coming days:

Source: UPS/The Motley Fool

Source: UPS/The Motley Fool

Also sounding the inflationary alarm, Kimberly-Clark – the maker of Cottonelle, Huggies and Kleenex that has 46,000 employees worldwide – released its third-quarter earnings on Oct. 25. CEO Michael D. Hsu said that “higher inflation and supply chain disruptions increased our costs well beyond the expectation we established just last quarter.”

Moreover, he added that “we had expected commodity prices to ease in the second half of 2021; instead, prices for resin and pulp increased further in the third quarter and are now expected to stabilize at a meaningfully higher level than our prior estimate.”

In addition, while Hsu was light on the specifics, he said that “further pricing actions” are already in the works and CFO Maria Henry said that she expects the cost-push inflationary spiral to continue for the foreseeable future.

Please see below:

Source: Kimberly-Clark/The Motley Fool

Source: Kimberly-Clark/The Motley Fool

Making three of a kind, 3M – which has a market cap of more than $100 billion – released its third-quarter earnings on Oct. 26. CFO Monish Patolawala said that we’re “facing a lot of inflation…. I think the big issue that we have seen as inflation is coming faster than anybody thought…. I would say we don't see the raw material or the inflation environment slowing down in any way. I think you're going to see that volatility.”

As for wage inflation:

“It's a global item, but it's more pronounced right now for us in the U.S. So we are seeing higher cost, whether it is cost driven by some of the items Mike mentioned as well as with the demand that we have, we are spending more money on overtime. And also we are seeing cost of inflation, which is labor cost that comes through us, through outsource manufacturing hard goods that we buy, we're also seeing inflation on that.”

As a result:

Source: 3M/Seeking Alpha

Source: 3M/Seeking Alpha

For context, I warned on Mar. 30 that companies wouldn’t sit idly by and watch their profit margins erode.

I wrote:

Didn’t Powell insist that near-term inflation was only “one-time” and “transient?” Well, despite government-issued CPI data failing to capture the effect of the Fed’s liquidity circus, pricing pressures are popping up everywhere. Think about it: with corporations’ decision tree left to raising prices or accepting lower margins, which one do you think they’re likely to choose?

Finally, McDonald’s – the world's largest fast-food restaurant chain – released its third-quarter earnings on Oct. 27. CEO Chris Kempczinski said the following about wage inflation:

“It's a very challenging staffing environment in the US, a little bit less so in Europe, but still challenging in Europe. In the U.S. for us, we are seeing, as I've mentioned a few calls ago that there is wage inflation. Our franchisees are increasing wages over 10% year-to-date [and] our McOpCo restaurants were up over 15% on wages.”

On top of that:

“Pricing and cost pressures are a bigger focus over the last few quarters than they had been previously. Last quarter, I think I talked about how we were seeing roughly a 6% increase year-over-year in the U.S. We are still seeing that and that's pretty much the level we expect for the full-year 2021 over 2020 right around that 6. And that's really to cover both labor cost pressures and commodity cost pressures that we're seeing.”

More importantly, though:

Source: McDonald’s/The Motley Fool

Source: McDonald’s/The Motley Fool

The bottom line? With inflation surging and the figures coming out of corporate earnings calls nowhere near the Fed’s 2% annual target, the Nov. 2/3 taper announcement will likely be a hawkish appetizer. Right now, investors expect the Fed to hold off on interest rate hikes until well into 2022. Moreover, Fed Chairman Jerome Powell said on Oct. 22 that “I don’t think it is time to raise rates.”

Despite that, though, the Fed remains materially behind the inflation curve. And with commodity inflation, wage inflation and rent inflation creating the perfect storm, the Fed will likely have to accelerate its tightening cycle to calm the pricing pressures. Moreover, with the PMs suffering mightily when the Fed turns hawkish, they’re unlikely to celebrate the inflationary anxiety that should grip the Fed over the next few months.

In conclusion, the PMs were mixed on Oct. 27 and mining stocks continued their underperformance. And after the USD Index shrugged off the intraday volatility, the dollar basket continues to showcase strength when faced with adversity. Moreover, with a taper announcement only cementing the greenback’s fundamental foundation and more hawkish rhetoric from the Fed poised to enhance the U.S. dollar’s uptrend over the medium term, the 2021 theme of ‘USD Index up, PMs down’ should remain alive and well over the next few months.

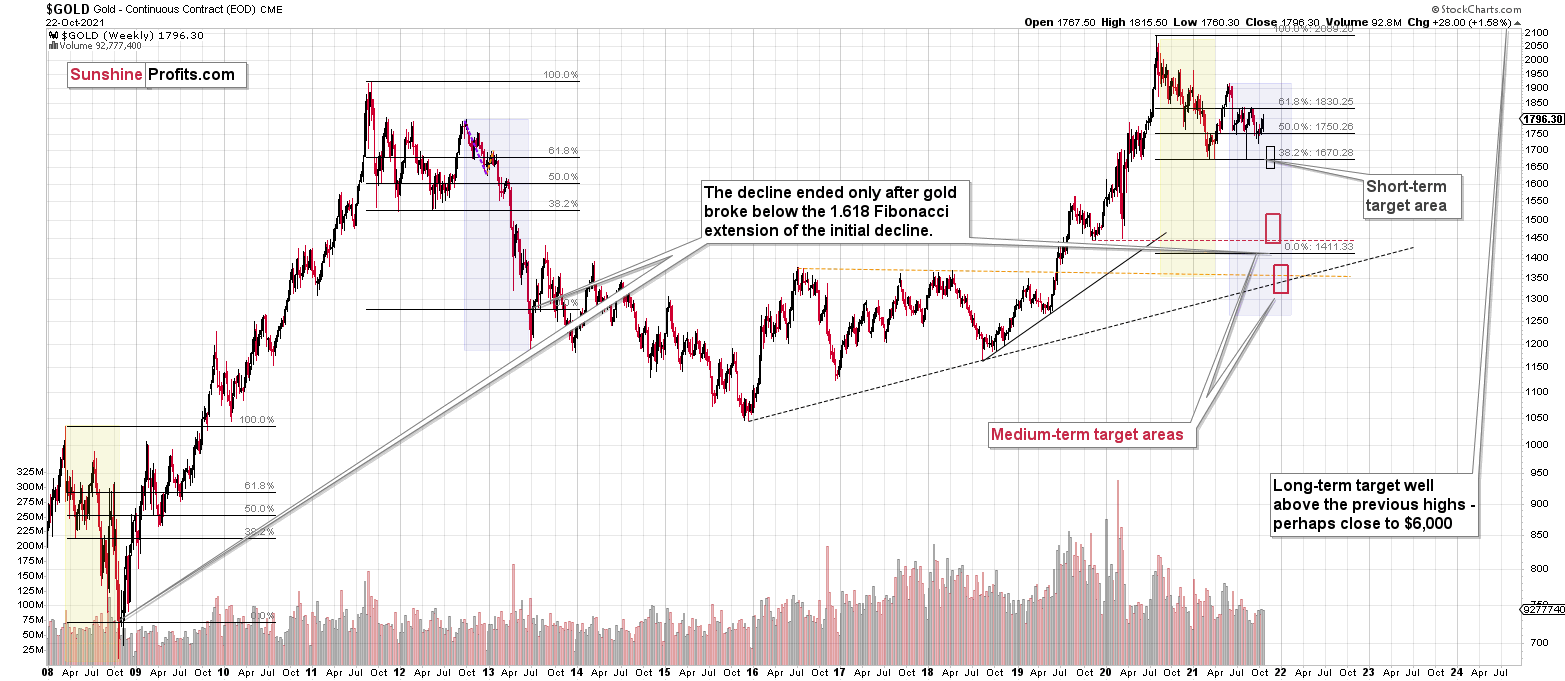

Overview of the Upcoming Part of the Decline

- It seems to me that the current corrective upswing in gold is over, and the next short-term move lower is about to begin. Since it seems to be another short-term move more than it seems to be a continuation of the bigger decline, I think that junior miners would be likely to (at least initially) decline more than silver.

- It seems that the first stop for gold will be close to its previous 2021 lows, slightly below $1,700. Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time. Before the next big slide, I will likely prefer to get back to the short position in the junior mining stocks.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions when gold shows substantial strength relative to the USD Index while the latter is still rallying. This might take place with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This might also happen with gold close to $1,375, but it’s too early to say with certainty at this time. I expect the final bottom to take place near the end of the year, perhaps in mid-December.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

To summarize, the outlook for the precious metals sector remains extremely bearish for the next few months. Since it seems that the PMs are starting another short-term move lower more than it seems that they are continuing their bigger decline, I think that junior miners would be likely to (at least initially) decline more than silver.

From the medium-term point of view, the key two long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

It seems that our profits from the short positions are going to become truly epic in the following months.

After the sell-off (that takes gold to about $1,350 - $1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently providing you with the possibility to extend your subscription by a year, two years, or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over, and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $35.73; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $16.18; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $32.08; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $19.12

SLV profit-take exit price: $17.72

ZSL profit-take exit price: $41.38

Gold futures downside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $12.48

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief