Briefly: in our opinion, full (250% of the regular size of the position) speculative short position in gold, silver, and mining stocks is justified from the risk/reward point of view at the moment of publishing this Alert.

Welcome to this week's flagship Gold & Silver Trading Alert. As we promised you previously, in our flagship Alerts, we will be providing you with bigger, more complex analyses (approximately once per week) and it will usually take place on Monday.

The last few days didn't bring any substantial market news and there were no major price changes. Gold, silver, and mining stocks took a breather after the initial part of the sharp decline and at the moment of writing these words, gold is trading a little below Thursday's closing price. Taking together the Friday's trading and today's pre-market price action, there're very little new developments to discuss.

But.

The previous week is over and we have the weekly price moves and weekly volume levels to analyze and that's exactly what we'll do today. We'll make sure that you are kept up-to-date with the key long-term factors that remain in place. We will also discuss the gold to silver ratio in greater detail.

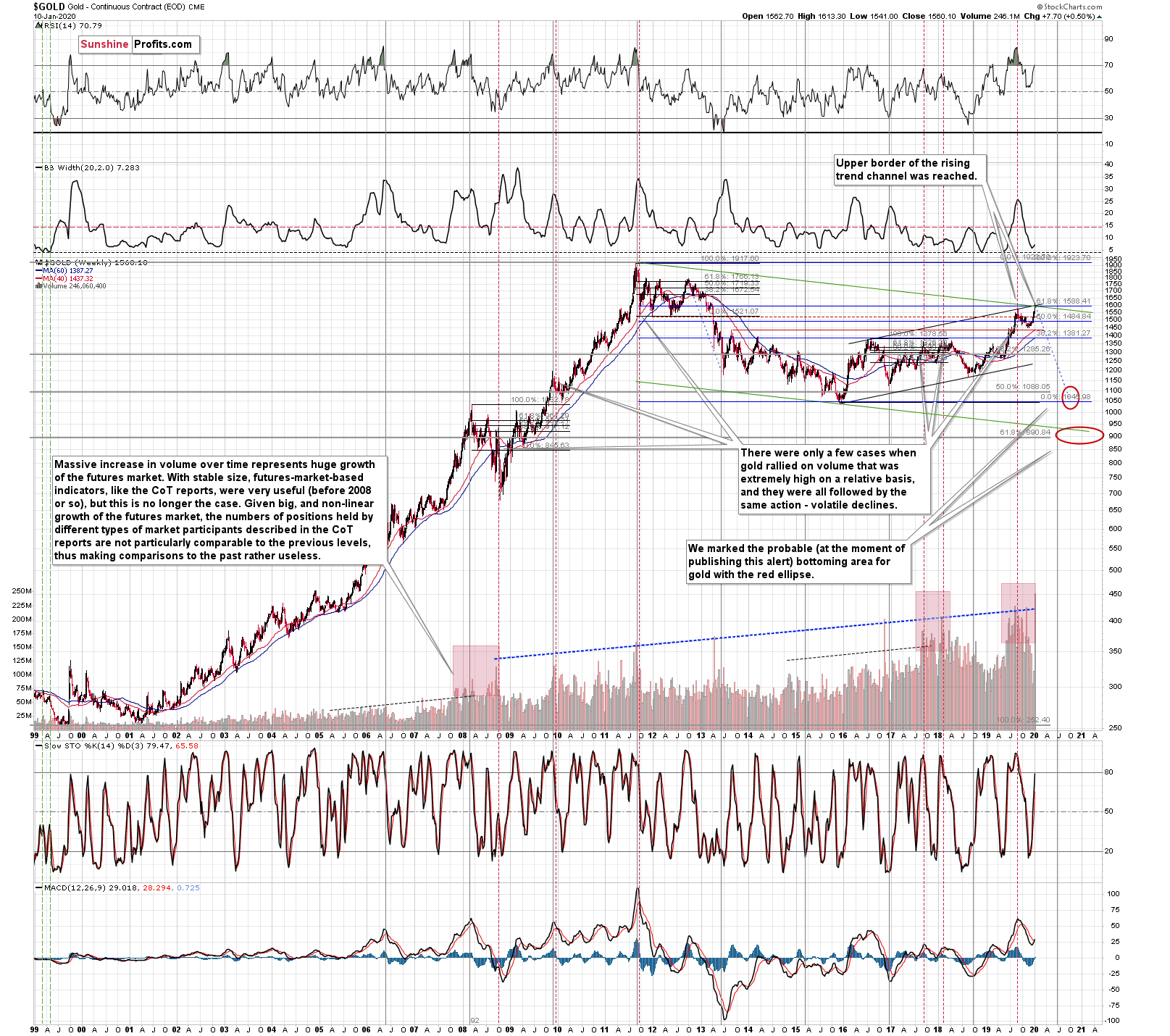

The weekly volume that we saw in gold was the highest ever and the implications are extremely important, but before we move to details, we would like to provide you with some additional - background - information.

There are three fundamental points that we would like to make before we proceed with explaining the key long-term technical factors that are likely to drive the markets in the following months. We discussed two of them previously, and one will be brand new. Let's start with the latter.

The first fundamental point of today's analysis will be the discussion of the recent jobs report. It was the only piece of news that we saw last week that was really important from the precious metals investors' point of view.

December Payrolls Below Expectations

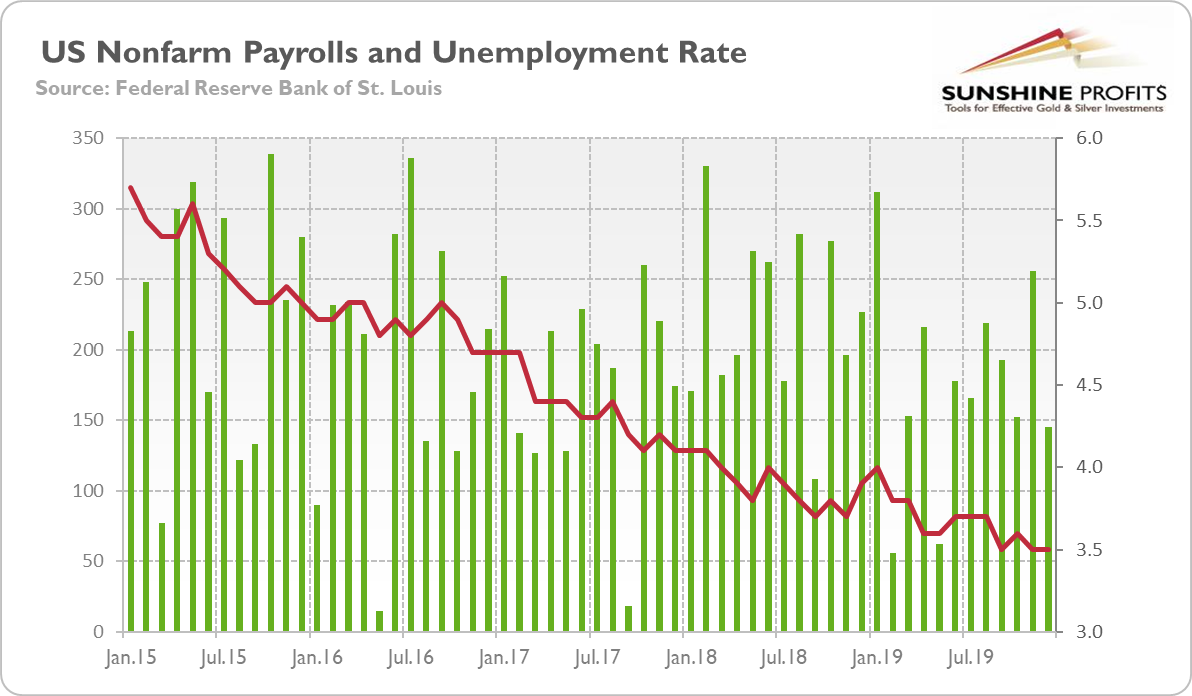

The U.S. created 145,000 jobs in December, following an increase of 256,000 in November (after a downward revision), as the chart below shows. The nonfarm payrolls came below expectations, as the analysts forecasted 165,000 new jobs. The gains were widespread, but with a leading role of retail trade (+41,200), leisure and hospitality (+40,000), and education and health services (+36,000). Manufacturing again cut jobs (-12,000), which means that industrial recession has not ended. Mining and transportation and warehousing also dismissed workers.

Chart 1: U.S. nonfarm payrolls (green bars, left axis, change in thousands of persons) and the unemployment rate (red line, right axis, %) from January 2015 to December 2019.

The surprisingly weak headline number was accompanied by downward revisions in November and October. Counting these, employment gains in these two months combined were 14,000 lower than previously reported. Consequently, the job gains have averaged 184,000 per month over the last three months, and 175,000 so far this year - still pretty good but significantly below the average monthly gain of 223,000 in 2018. In consequence, the payroll employment rose by 2.1 million in 2019, down from a gain of 2.7 million in 2018.

Although the pace of job creation has slowed down, the unemployment rate remained unchanged at 3.5, as the chart above shows. So, it is still at the 50-year low and does not send any recessionary warnings.

Last but not least, the low unemployment rate did not translate into significantly higher paychecks. The average hourly earnings for all employees on private nonfarm payrolls have increased only 2.9 percent over the last twelve months, following 3.1-percent rise in November. Actually, the pace of hourly wage growth fell below 3 percent for the first time since September 2018.

To sum up, although the December jobs report surprised the markets on the negative side, the U.S. labor market in 2019 was quite solid. While hiring has slowed, the unemployment decreased from 3.9 to 3.5 percent over the year, while the number of unemployed persons declined from 6.3 to 5.8 million. What is perhaps a bit astonishing is that the wage growth fell to 2.9 percent, which means that despite the ninth straight year of job creation and very low unemployment rate, the wage pressure is still moderate.

December Payrolls' Implications for Gold

But the U.S. labor market is still doing relatively well, which - combined with the lack of strong wage pressure - should make the Fed keep the interest rates unchanged in the foreseeable future. The fact that the U.S. central bank has no reason to hike the federal funds rate is positive for the gold prices. And indeed, the yellow metal rose on Friday, and weaker-than-expected U.S. jobs data could help here.

But beware! The resilience of the labor market also reduces the odds for a dovish move. Actually, some traders have started to price in the possibility of the interest rate hike by the end of 2020, which could harm gold. Indeed, the minutes from the last FOMC meeting indicate that the Fed officials become more optimistic about the U.S. economy in December as trade tensions with China eased, while the global economy stabilized somewhat. Thus,

while many saw the risks as tilted somewhat to the downside, some risks were seen to have eased over recent months. In particular, there were some tentative signs that trade tensions with China were easing, and the probability of a no-deal Brexit was judged to have lessened further. In addition, there were indications that the prospects for global economic growth may be stabilizing.

And the fresh remarks from the Fed officials have become even more optimistic since their last meeting. We do not expect them to return to a hawkish mode - especially in light of the liquidity crisis in the repo market - but the change in rhetoric should not be neglected.

The Link of Fundamentals and News with Price Patterns

The second fundamental point that we would like to make is the relationship between news and the price of gold. That's something that we're being asked about regularly, usually along with the question how can we compare the previous situations from the past to the current one given that the world and what's going on in it are so different now. Actually, let's quickly reply to the last one. Regardless of decade or century, people are greedy and fearful when it comes to their investments.

These two emotions make people want to buy assets that are already priced too high and to sell assets that are already priced too low. This creates tensions between logic and emotionality and overall (!) people tend to react to act relatively similarly given similar price moves and how they develop relative to what's going on in the world. The developments in the world change, but they can be either bullish, bearish, neutral, or of unknown implications. Regardless of what the news actually is, people can act based on their logic and emotionality and on their views on the implications of a given situation. It doesn't matter that the real-world developments change.

What matters is that people will react to fear and greed in relatively similar ways. Of course, there is no single type of reaction, there are multiple ways in which people react, but they are together form the reaction that we see play out over and over again. Smaller parts of the price moves are often called "patterns" or "formations" while bigger ones are trends. Seeing that one of them just formed, allows one to check the follow-up action, which was also usually alike. This means that it's likely that the same (or similar) kind of movement will take place once again.

Of course, some formations tend to work on one given market and some on another one. The longer one analyzes a given market, the more proficient they become at discovering specific price moves that are applicable to it. For instance, in general, people view strong daily performance on big volume as bullish. But it is usually the other way around in case of silver, especially, if gold is weak on that day.

Different parts of trends are characterized by different price formations e.g. it is more common for something to appear at the beginning of an uptrend (e.g. gold stocks outperforming gold) than at its end. If one is able to detect what kind of price move from the past is being repeated (to a considerable extent), then it is much easier to forecast what's likely ahead. One will know what kind of signals should they be looking for, and what kind of signals are not likely to be seen (thus, if they are seen, they serve as a huge red flag).

Whatever happens, it impacts the market through the above-mentioned mechanism. And since the patterns in which people react overall don't change (thus history rhymes), we can focus on analyzing them - and that's exactly what we do through charts, price patterns, retracements, cycles, indicators, and so on.

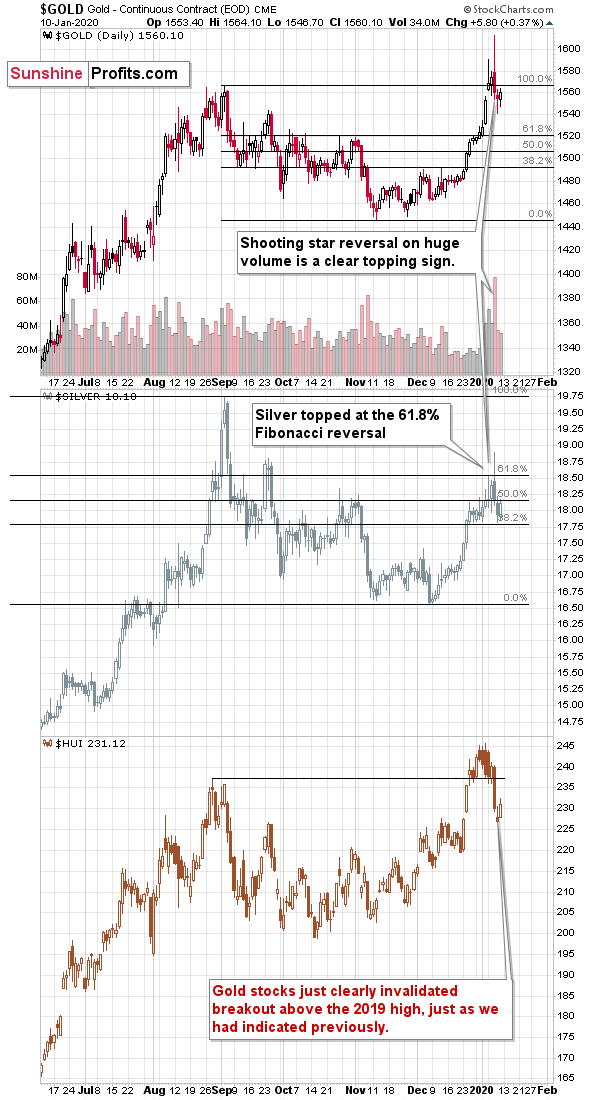

In the recent days, gold got ahead of itself in what appears to have been the final part of the corrective upswing. Gold moved to the 61.8% Fibonacci retracement level based on the 2011 - 2015 decline and it reversed in a crystal-clear manner even though it had a very important reason to move higher. The U.S. - Iran conflict escalated to the point where both sides fired missiles. Gold was forced to rally when the news hit the market, but it soon became obvious that "up" is not the true direction in which gold wants to move. Even though the tensions between U.S. and Iran remain high, gold didn't come back after the sharp (more than $50 in 24 hours) decline.

In case of gold's immediate and follow-up reactions to the recent employment numbers, we can say that it was mildly bearish overall. The immediate reaction showed that gold investors viewed the no-change decision as something bullish, but the early-Monday trading showed that it was unable to trigger any sustainable moves. The inability to hold the gains is a bearish indication, but since the price moves were not big, the implications are not huge either.

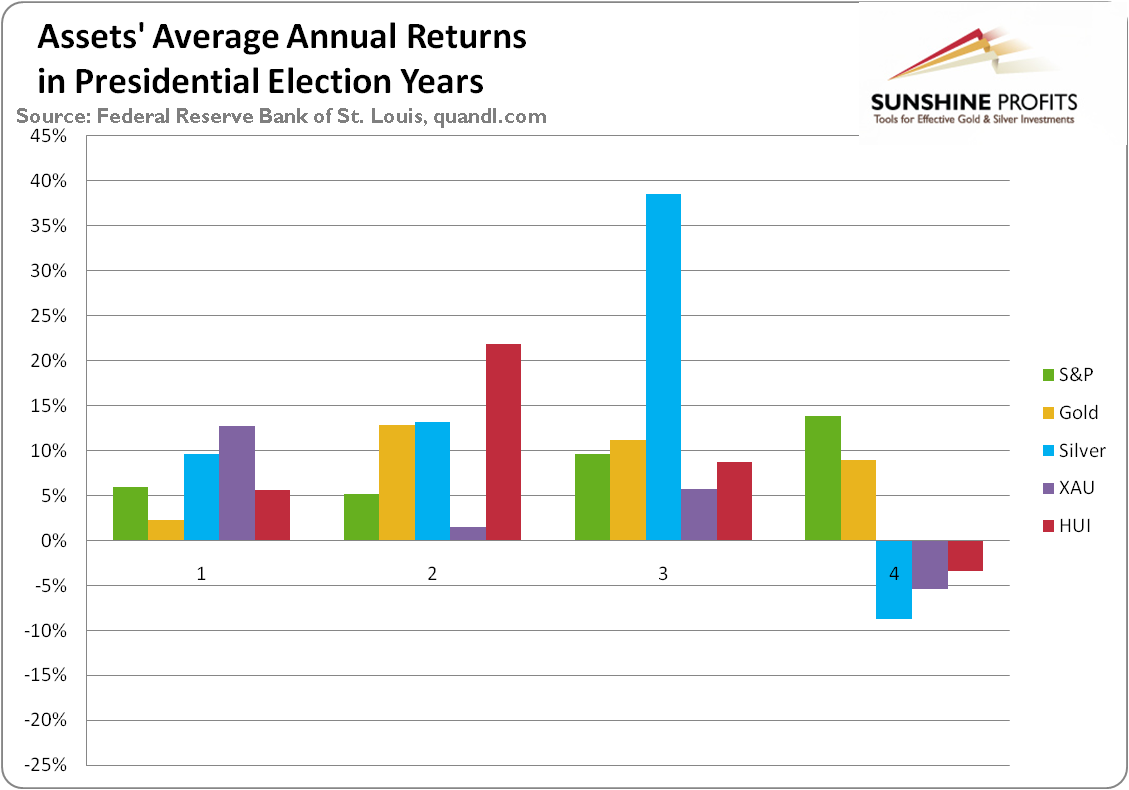

The third fundamental point that we would like to make today is the fact that we are in the final year of the U.S. Presidential cycle and this year is the worst year for silver and mining stocks. It's the only one during which they tend to decline on average.

Assets' Returns and Presidential Cycle

Average annual return of S&P (1948-2015, green line), gold (London P.M. Fix, 1972-2015, yellow line), silver (London Fix, 1972-2015, blue line), XAU Index (1984-2015, purple line) and HUI Index (1997-2015, red line) in presidential election cycles.

Gold's performance is more or less average in the election year, but in case of silver and mining stocks we see something very different. Namely, the election year is the only year when - on average - they all decline.

So, does it mean that gold won't be affected by this specific cyclicality, but silver and miners will be? Not really. It seems that the above chart shows that silver and miners - on average - lead gold lower. They perform worst in the election year and the yellow metal is the worst choice in the following year - the first year of presidency.

Silver and miners have already been performing very poorly relative to gold if we look at the long-term charts. Did silver or miners exceed their 2016 highs? They are not even close, especially silver. So, it seems that the pattern that we should be seeing at this time of the U.S. Presidential cycle, is already here and it started a bit earlier.

This means two things: even more weakness in silver and miners that we saw, and gold catching up with the decline.

As long as the tensions remain high, gold might have trouble sliding, but once they subside - and they might have just reached zenith last week - gold would likely plunge.

The fundamental background is one thing, but the technical details are another. They provide details and insights that are impossible to get by just analyzing the news. Let's see how much the recent strength in gold changed the picture, and what's going on in the most important - long-term - charts featuring gold and the related markets.

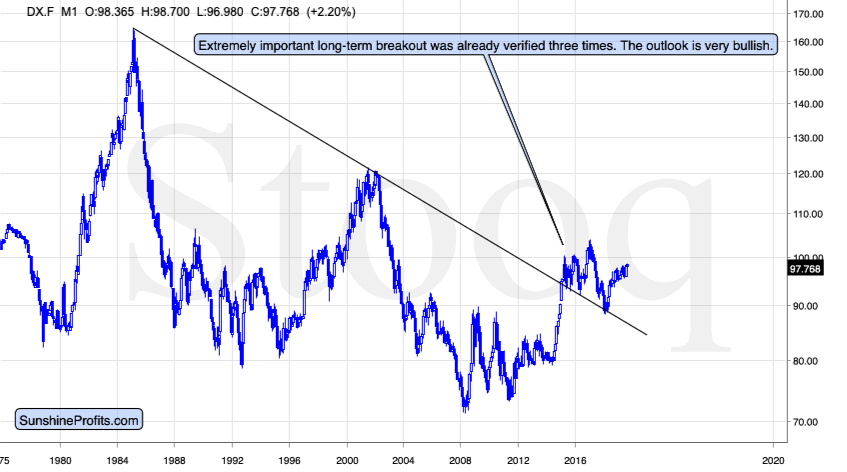

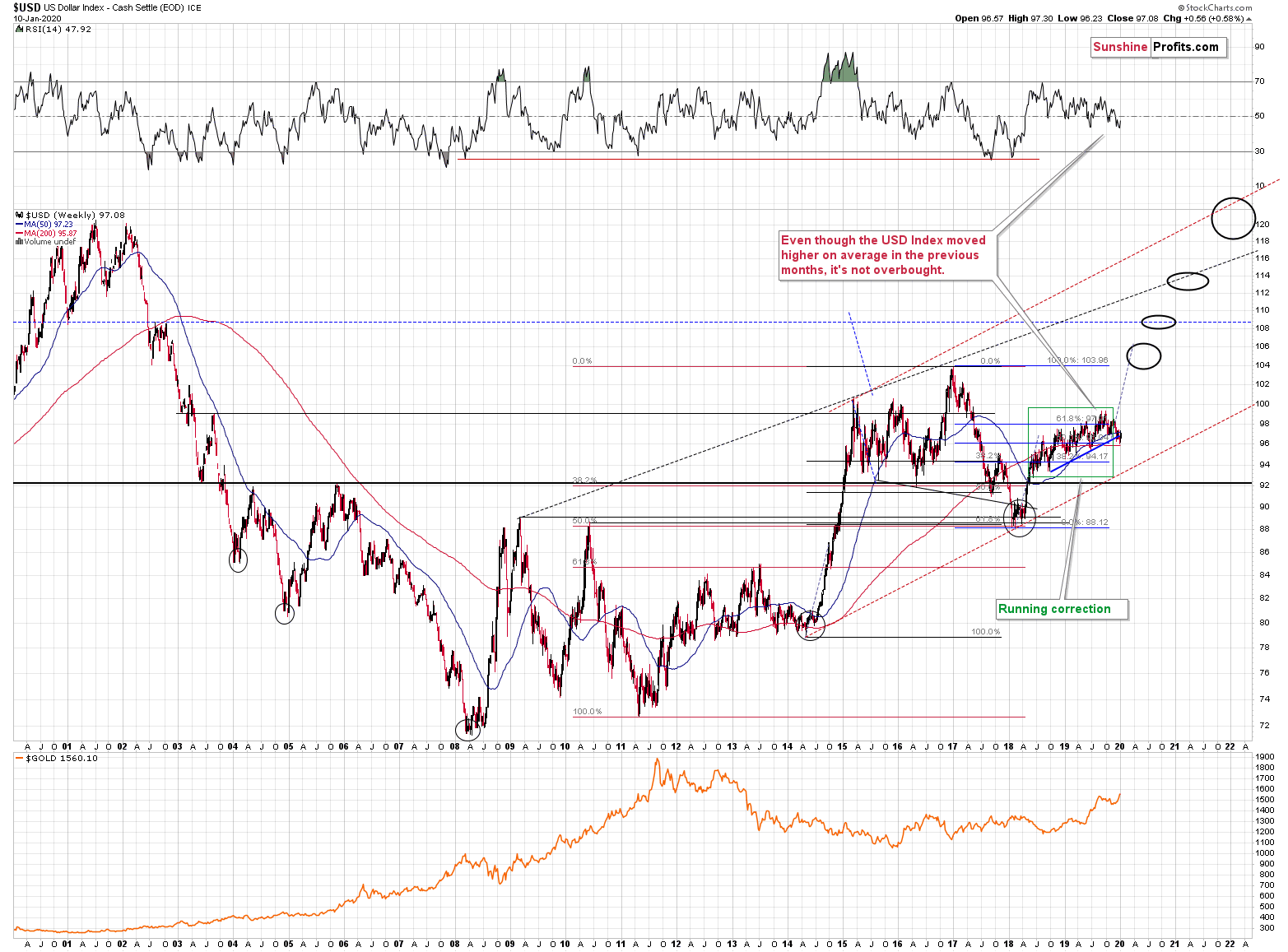

The most important point that remains intact (and unaffected by what happened in the past week) is that the USD Index is after a massive breakout that was already verified more than once. The connection with the gold market remains intact as well.

The Big Picture View of the USD Index

(please click on the charts to enlarge them)

The 2014-2015 rally caused the USD Index to break above the declining very-long-term resistance line, which was verified as support three times. This is a textbook example of a breakout and we can't stress enough how important it is.

The most notable verification was the final one that we saw in 2018. Since the 2018 bottom, the USD Index is moving higher and the consolidation that it's been in for about a year now is just a pause after the very initial part of the likely massive rally that's coming.

If even the Fed and the U.S. President can't make the USD Index decline for long, just imagine how powerful the bulls really are here. The rally is likely to be huge and the short-term (here: several-month long) consolidation may already be over.

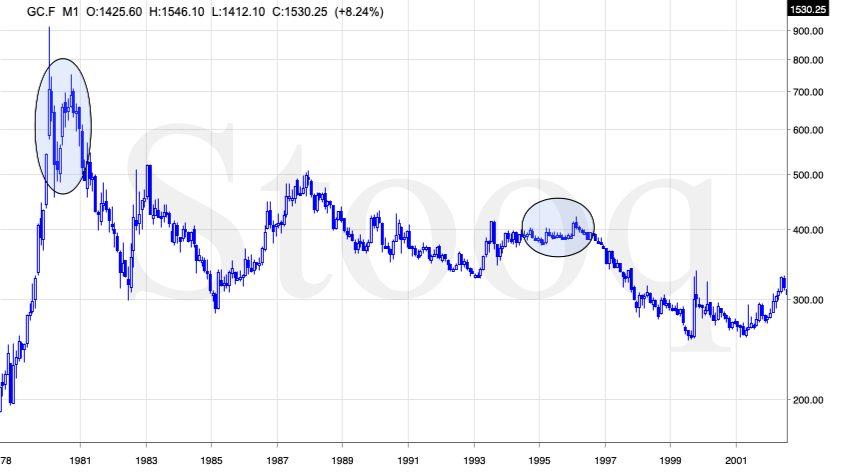

There are two cases on the above chart when the USD Index was just starting its massive rallies: in the early 1980s and in mid-90s. What happened in gold at that time?

Gold Performance When the USD Index Soars

These were the starting points of gold's most important declines of the past decades. The second example is much more in tune with the current situation as that's when gold was after years of prolonged consolidation. The early 1980s better compare to what happened after the 2011 top.

Please note that just as what we saw earlier this year, gold initially showed some strength - in February 1996 - by rallying a bit above the previous highs. The USD Index bottomed in April 1995, so there was almost a yearly delay in gold's reaction. But in the end, the USD - gold relationship worked as expected anyway.

The USD's most recent long-term bottom formed in February 2018 and gold seems to have topped right now. This time, it's a bit more than a year of delay, but it's unreasonable to expect just one situation to be repeated to the letter given different economic and geopolitical environments. The situations are not likely to be identical, but they are likely to be similar - and they indeed are.

What happened after the February 1995 top? Gold declined and kept on declining until reaching the final bottom. Only after this bottom was reached, a new powerful bull market started.

Please note that the pace at which gold declined initially after the top - in the first few months - was nothing to call home about. However, after the initial few months, gold's decline visibly accelerated.

Let's compare the sizes of the rallies in the USDX and declines in gold. In the early 80s, the USDX has almost doubled in value, while gold's value was divided by the factor of 3. In the mid-90s, the USDX rallied by about 50% from its lows, while gold's value was divided by almost 1.7. Gold magnified what happened in the USD Index in both cases, if we take into account the starting and ending points of the price moves.

However, one can't forget that the price moves in USD and in gold started at different times - especially in the mid-90s! The USDX bottomed sooner, which means that when gold was topping, the USDX was already after a part of its rally. Consequently, when gold actually declined, it declined based on only part of the slide in the USDX.

So, in order to estimate the real leverage, it would be more appropriate to calculate it in the following way:

- Gold's weekly close at the first week of February 1996: $417.70

- USDX's weekly close at the first week of February 1996: 86.97

- Gold's weekly close at the third week of July 1999: $254.50

- USDX's weekly close at the third week of July 1999: 103.88

The USD Index gained 19.44%

Gold lost 39.07% (which means that it would need to gain 64.13% to get back to the $417.70).

Depending on how one looks at it, gold actually multiplied USD's moves 2-3 times during the mid-90 decline.

And in the early 1980s?

- Gold's weekly close at the third week of January 1980: $845

- USDX's weekly close at the third week of January 1980: 85.45

- Gold's weekly close at the third week of June 1982: $308.50

- USDX's weekly close at the third week of June 1982: 119.01

The USD Index gained 39.27%

Gold lost 63.49% (which means that it would need to gain 173.91% to get back to $845).

Depending on how one looks at it, gold actually multiplied USD's moves by 1.6 - 4.4 times during the early-80 decline.

This means that just because one is not using U.S. dollars as their primary currency, it doesn't result in being safe from gold's declines that are accompanied by USD's big upswings.

In other words, the USD Index is likely to soar, but - during its decline - gold is likely to drop even more than the USD is going to rally, thus falling in terms of many currencies, not just the U.S. dollar.

Please note that there were wars, conflicts and tensions between 1980 and 2000. And the key rule still applied. Huge rallies in the USD Index mean huge declines in gold. If not immediately, then eventually.

Having covered the most important factor for the USD Index and gold, let's take a look at the other - also important - factors influencing both of these markets.

More On the USD Index and Gold

The USD Index is moving up in a rising trend channel (all medium-term highs are higher than the preceding ones) that formed after the index ended a very sharp rally. This means that the price movement within the rising trend channel is actually a running correction, which is the most bullish type of correction out there. If a market declines a lot after rallying, it means that the bears are strong. If it declines a little, it means that bears are only moderately strong. If the price moves sideways instead of declining, it means that the bears are weak. And the USD Index didn't even manage to move sideways. The bears are so weak, and the bulls are so strong that the only thing that the USD Index managed to do despite Fed's very dovish turn and Trump's calls for lower USD, is to still rally, but at a slower pace.

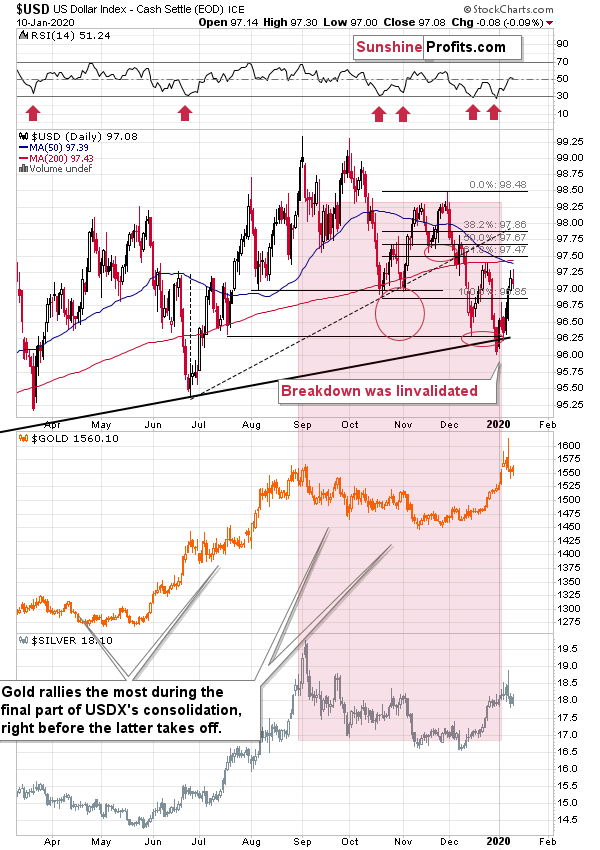

The temporary breakdown below the rising blue support line was invalidated last week as the USD Index moved over 0.5 higher. That's a technical sign that the short-term decline is over.

The weekly invalidation of breakdown confirms what we previously noted with regard to the short-term breakdown and its subsequent invalidation.

The USDX invalidated the short-term breakout and the RSI flashed a second buy signal about 2-3 weeks after generating the previous one - that's what we saw in early November right before the early-November decline in gold. This was a bullish combination and it was indeed followed by higher USDX values.

Moreover, please note that gold is below its September high, while the USD Index is still about 2 index points below its September high. Overall, gold shrugged off USD's slide in the last 4 months and it only rallied recently - at the end of USD's decline. That's what gold tends to do in smaller and bigger time-frames.

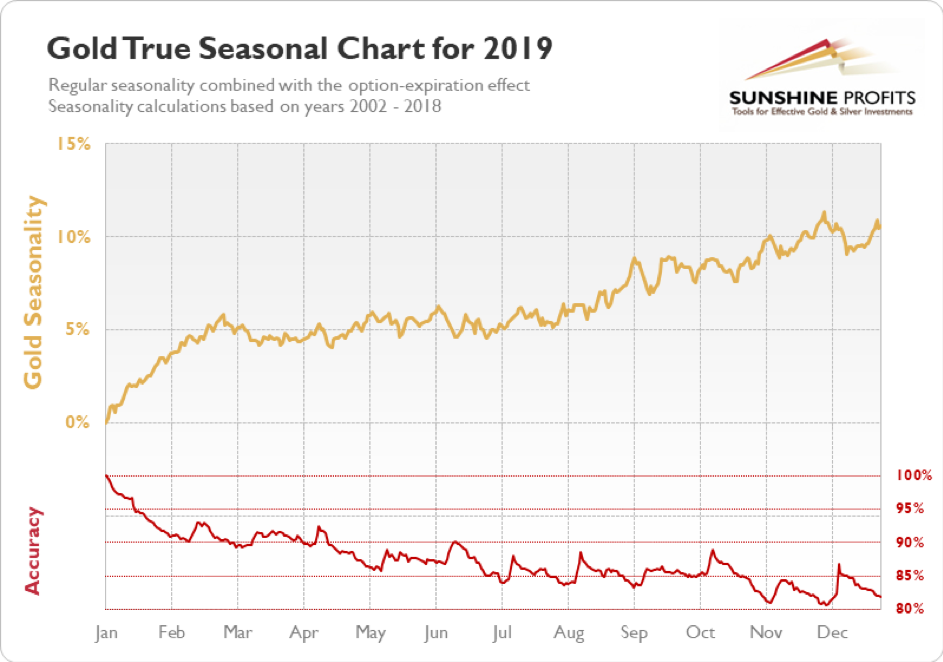

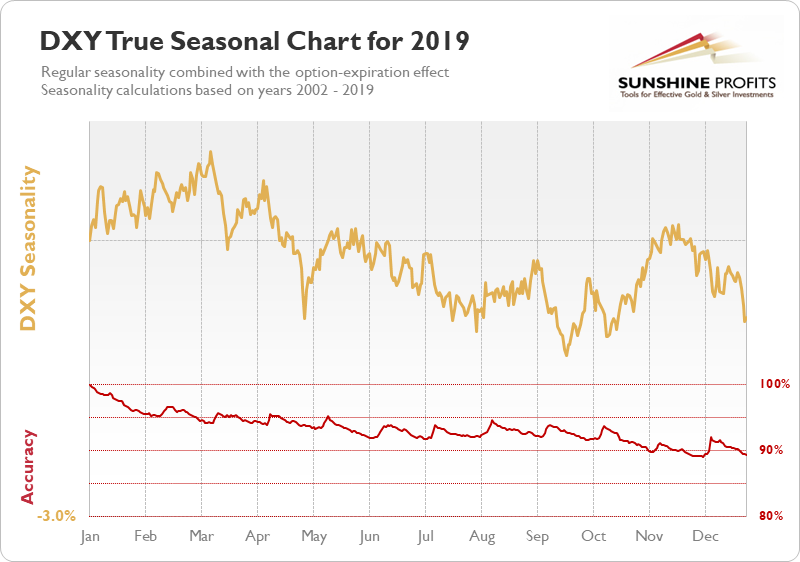

Having said that, let's take a look at the current seasonality in gold. In short, it's positive at its face value, and it's neutral once one considers the likelihood of USD Index's upswing.

As a reminder, our True Seasonal gold charts are an improved version of the regular seasonality, as they additionally estimate also the Accuracy and they are based not only on the plain seasonality, but also on the way gold price tends to move around the options expiration dates (they don't take place at exactly the same day each month, so the regular seasonality ignores this effect).

The option expiration effect is not huge in case of the yellow metal; it's more significant in case of silver. Also, this effect is not very visible in case of yearly charts, such as the one that we present below, but it becomes more useful in case of the quarterly charts that we also feature from time to time (and which you can access on your own over here). You can read more details about this effect in this report (note: the pdf file is quite heavy, so it may take a while to load).

At the beginning of the year, gold tends to rally while the USD's performance varies. Let's keep in mind that the above charts are based on the 2002 - 2018 period (we will update them based on the 2019 data shortly, but since gold rallied, and USDX declined in January 2019, they will look very much similar to the ones above, at least with regard to January) and looking at the most recent years might provide us with even more accurate insights. Let's dig deeper.

Gold rallied in early 2019, early 2018, early 2017, early 2016, early 2015, early 2014, early 2012, early 2010, and early 2008.

Gold declined in early 2011, early 2009, and early 2007.

And do you know when the USD Index rallied? In early 2011, in early 2009, and in early 2007. It also rallied in early 2012, in early 2014, and in early 2015.

In other words, half of early January USD's rallies triggered declines in gold. If the USD Index is very likely to rally shortly - and this is the case - then the better comparison than just taking the previous years into account is to focus on cases when the USD Index rallied. This means that in half (3 out of 6) cases, gold rallied, and that it declined in the remaining cases. The 50/50 performance means that the outlook is not as bullish as the seasonality would have one believe.

The outlook for the USD Index nullifies the positive effect of the seasonality.

Gold is up in January so far, silver is also up, but barely, and mining stocks are definitely down. The seasonality doesn't seem to be as bullish as many have predicted it to be. Given the recent reversal in gold and the remaining factors that we have covered and will cover today, it seems doubtful that the month will end as positive for gold as it had started. In fact, exactly the opposite seems to be in the cards.

Naturally, there are many other things that need to be taken into account while analyzing the market other than just the USD Index and gold's seasonality. For instance, the analogy in terms of the previous long-term retracements within big declines. In particular, the declines that we saw in 2008 and between 2011 and 2015.

The markets have fractal nature, meaning that the price patterns that we see in one timeframe, can also apply on a different scale, with proportionate implications. For instance, silver's tendency to outperform gold at the end of a bigger move higher - it takes place on a small scale in case of local rallies, and it's more visible in case of more medium-term moves.

In case of gold's long-term chart, the Fibonacci retracements are the thing that likely applies on a different scale right now. In today's second fundamental point, we explained why certain patterns repeat themselves despite taking place at entirely different times and under different circumstances. The Fibonacci retracements are one of the patterns that keeps on emerging in many markets, including gold. The 61.8% Fibonacci retracement is the most classic one.

In both previous cases (the 2011-2015 and 2008 declines), gold declined initially after the top (March 17, 2008, September 6, 2011) and then corrected a bit more than 61.8% of the decline before forming the final short-term top (July 15, 2008, October 5, 2012) from which the biggest declines started. The 2016 decline was also preceded by a sharp rally and it was also characterized by a temporary move back up - slightly above the 61.8% Fibonacci retracement - before the main part of the slide.

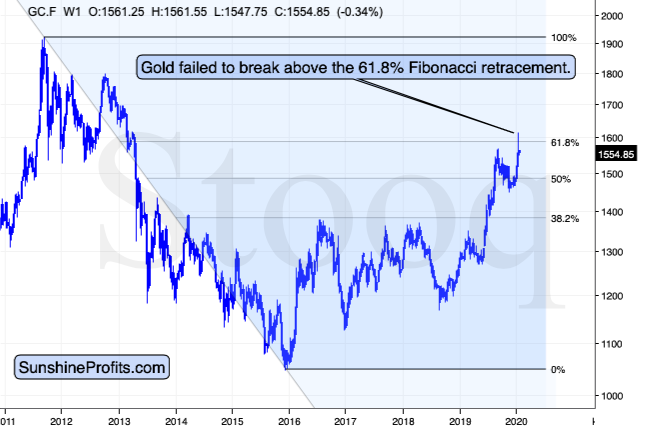

Now gold also moved to the 61.8% Fibonacci retracement level (precisely, it tried to move above it and managed to do so only very temporarily), but to one of much bigger meaning.

The 61.8% Fibonacci retracement that's based on the entire 2011 - 2015 decline is $1,588. That was the initial high in gold. It was the high that gold failed to break above.

Gold, Fibonacci Retracements and Reversals

Many people - especially those selling gold - will want to tell you that gold has been in a huge rally since late 2015. In reality, however, gold remains in a corrective mode after declining from 2011. And if you don't want to trust gold's classic retracement tool, maybe you'll trust silver or gold stocks.

Silver is mere $4 above its 2015 bottom. That's about $32 below the 2011 high. Big rally in the precious metals sector? What big rally? It's only gold that's been showing significant strength and taking a closer look reveals that it just corrected (!) 61.8% of the previous decline. It's relatively common for markets to retrace this amount before the previous trend resumes.

And gold miners? The HUI Index is about 400 index points below its 2011 high and only about 130 index points above the 2016 low.

That's a correction, not a new powerful rally. We will see one, but this is not the real deal just yet.

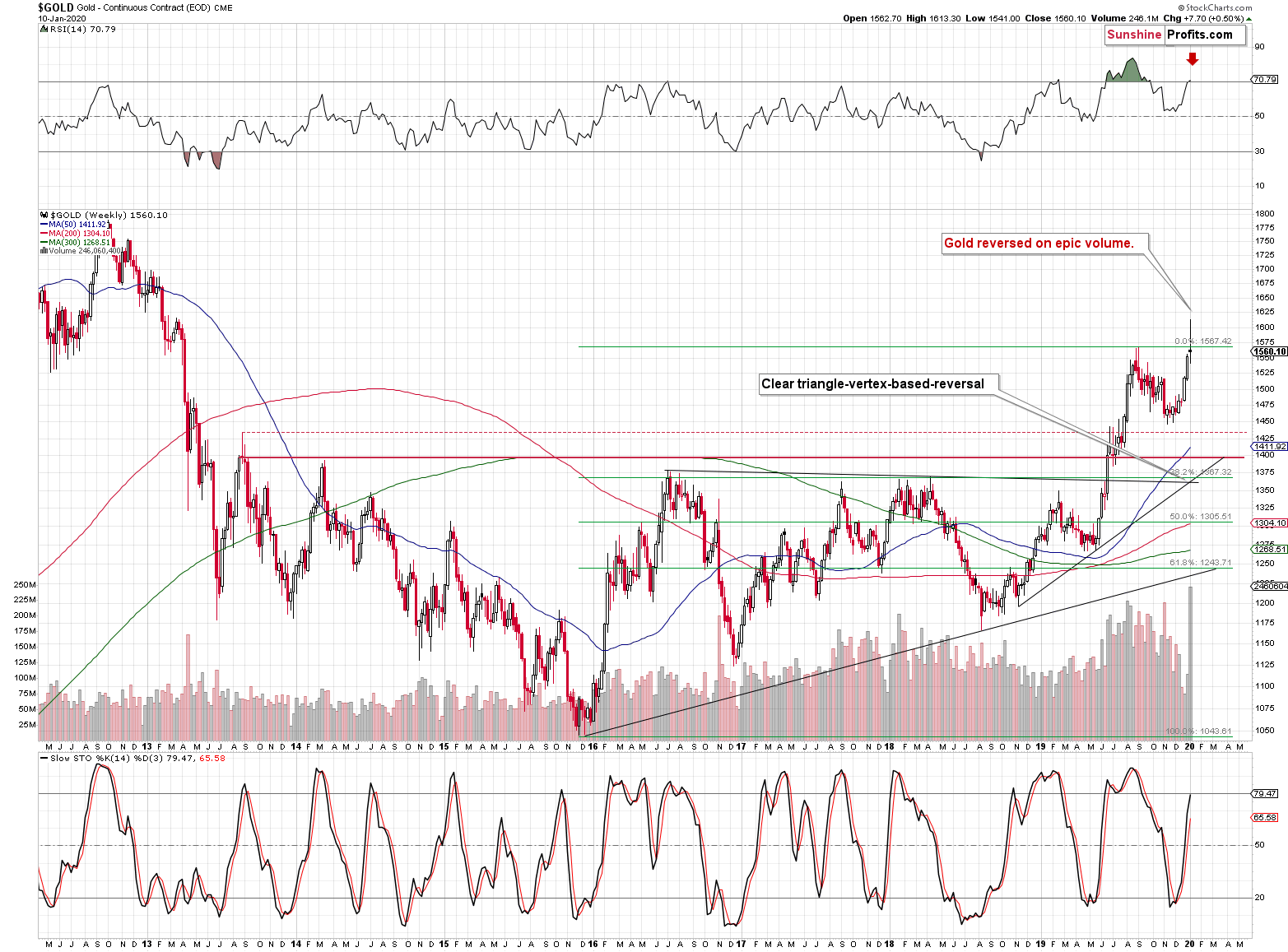

And speaking of major gold moves, please note how perfectly the long-term triangle-vertex-based reversals in gold worked.

Gold was very likely to reverse, and it did exactly that, just like we had written earlier.

Reversals should be confirmed by big volume and last week's volume was truly epic, which is a perfect bearish confirmation. It was the biggest weekly gold volume EVER.

We already wrote a lot today about gold and we will write even more, also about silver and miners. We will cover multiple signs that point to lower precious metals prices in the following weeks and months. But, last week's reversal along with the record-breaking weekly volume is alone enough to make the outlook bearish. That's how significant this reversal-volume combination is.

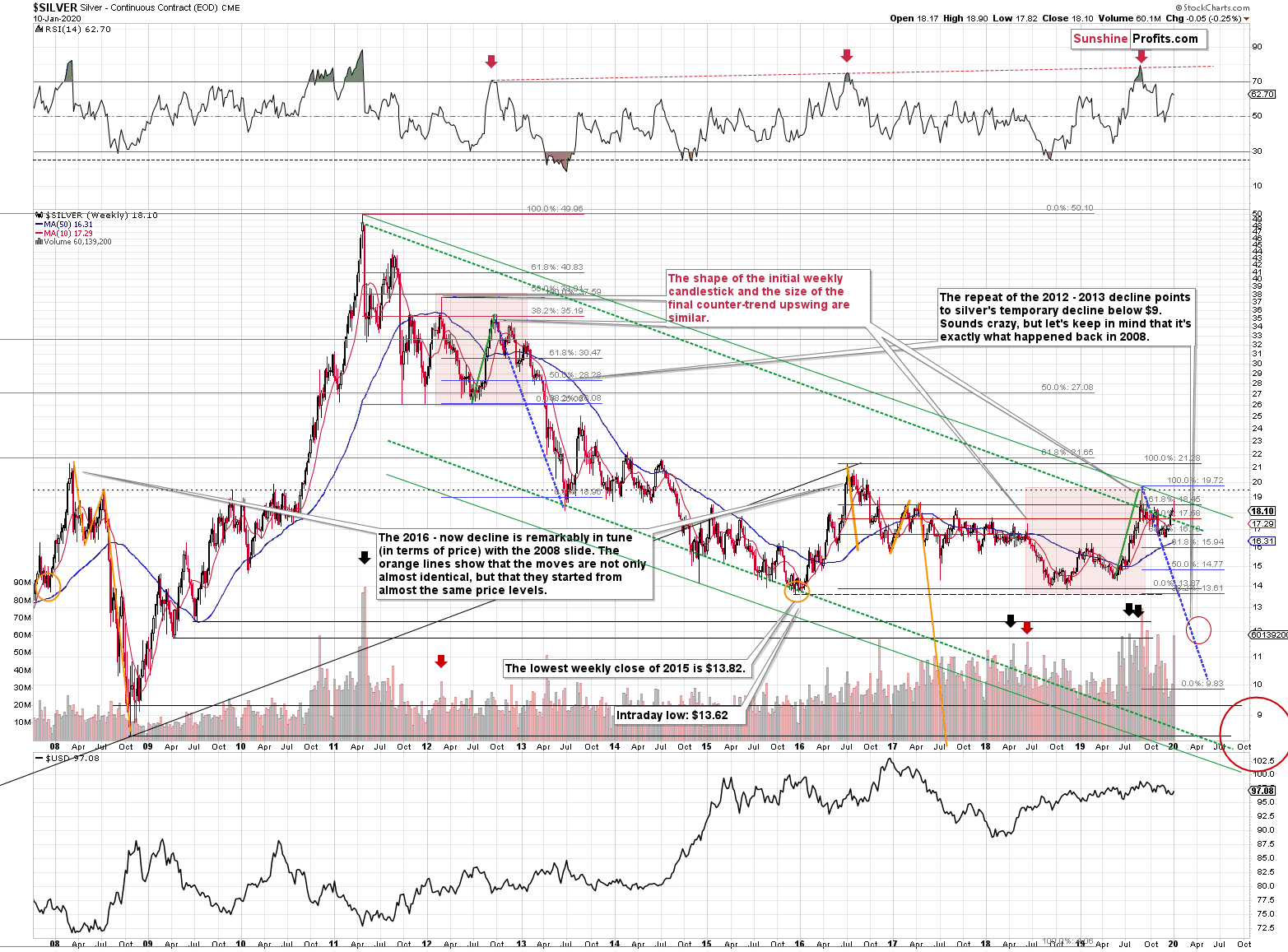

Let's take a look at gold's sister metal - silver.

Silver Shares Its Two Cents

The key analogy in silver (in addition to the situation being similar to mid-90s) continues to be the one between 2008 and the 2016 - now periods.

There is no meaningful link in case of time, or shape of the price moves, but if we consider the starting and ending points of the price moves that we saw in both cases, the link becomes obvious and very important. And as we explained in the opening part of today's analysis, price patterns tend to repeat themselves to a considerable extent. Sometimes directly, and sometimes proportionately.

The rallies that led to the 2008 and 2016 tops started at about $14 and we marked them both with orange ellipses. Then both rallies ended at about $21. Then they both declined to about $16. Then they both rallied by about $3. The 2008 top was a bit higher as it started from a bit higher level. And it was from these tops (the mid-2008 top and the early 2017 top) that silver started its final decline.

In 2008, silver kept on declining until it moved below $9. Right now, silver's medium-term downtrend is still underway. If it's not clear that silver remains in a downtrend, please note that the bottoms that are analogous to bottoms that gold recently reached, are the ones from late 2011 - at about $27. Silver topped close to $20.

The white metal hasn't completed the decline below $9 yet, and at the same time it didn't move above $19 - $21, which would invalidate the analogy. This means that the decline below $10, perhaps even below $9 is still underway.

Naturally, the implications for the following months are bearish.

Let's consider one more similarity in the case of silver. The 2012 and the 2018 - today performance are relatively similar, and we marked them with red rectangles. They both started with a clear reversal and a steady decline. Then silver bottomed in a multi-bottom fashion, and rallied. This time, silver moved above its initial high, but the size of the rally that took it to the local top (green line) was practically identical as the one that we saw in the second half of 2012.

The decline that silver started in late 2012 was the biggest decline in many years, but in its early part it was not clear that it's a decline at all. Similarly to what we see now, silver moved back and forth with lower highs and lower lows, but people were quite optimistic overall, especially that they had previously seen silver at much higher prices (at about $50 and at about $20, respectively).

The 2012 corrective upswings were actually the final chances to exit long positions and enter short ones. It wasn't easy to do it back then just as it's not easy to do so right now. But the size of the decline that followed speaks for itself. In investing and trading, what's pleasant and what's profitable is rarely the same thing.

Last week's performance - silver's huge reversal - confirms what we saw in gold. Silver's volume didn't set a new record, but it was huge nonetheless. Definitely more than enough to make silver's reversal important and reliable. It's very bearish on its own and extremely bearish when examined together with gold's reversal.

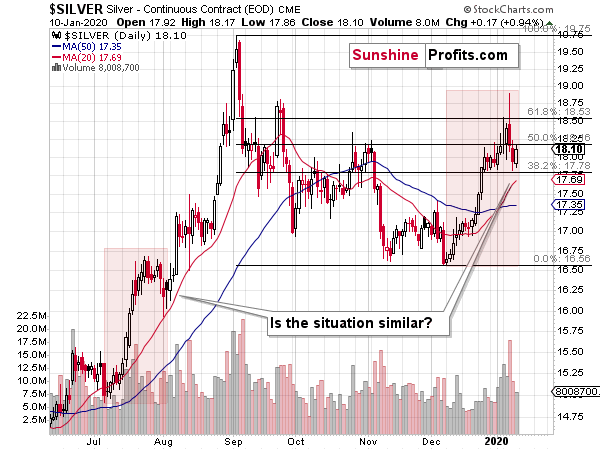

On a short-term basis, we see that silver tried to move above the 61.8% Fibonacci retracement based on the most recent decline and at the same time, it moved just a little above the 61.8% Fibonacci retracement that you can see on the previous long-term chart. Taking the 2016 top as the starting point and the 2018 low as the ending point, we get $18.45 as the retracement. Silver had moved less than 10 cents above it and then it invalidated this tiny breakout. Then it invalidated the more short-term breakout as well (the one that you see on the above chart).

The odds are that silver's December - January upswing is already over.

Before we move to mining stocks, we would like to reply to a question that we received - namely, is the situation now similar to what we saw in late July 2019. After all, it appears to be the case when looking at the silver chart.

In short, it doesn't seem very likely, even though both situations do indeed share some similarities. One similarity for instance is that the overall medium-term outlook didn't really improve despite higher gold and silver prices. Why? For instance, because none of the points that we made so far today, were invalidated based on gold and silver moving higher since July. Most importantly, the long-term outlook for the USD Index and the way gold is likely to react to USD's big upswing, remain unchanged.

Why isn't the situation just like it was back in mid-2019? The most important reason is because we recently saw both the yellow and white metals' inability to keep on rallying despite positive news. The U.S. - Iran conflict was nowhere near as critical as it is right now and yet both precious metals declined recently. That's particularly visible in case of silver, which was unable to even move above the August high during the most recent run-up.

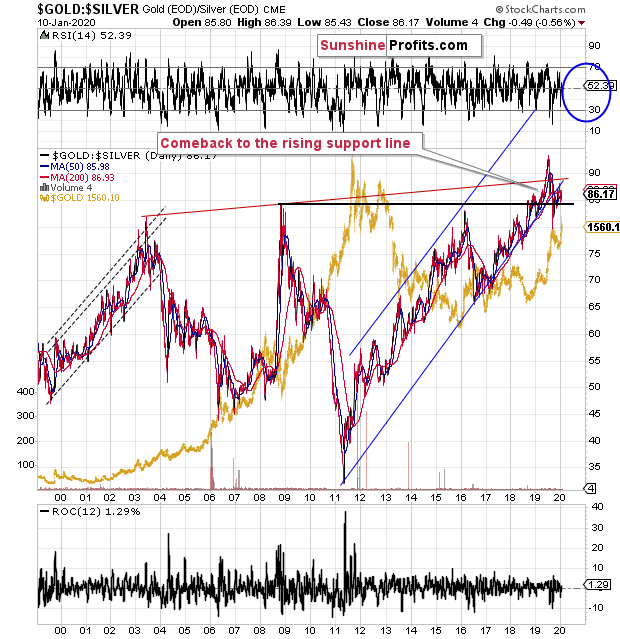

Moreover, in early July 2019 the gold to silver ratio topped after breaking above the previous highs and now it's after the verification of this breakout. Despite the sharp pullback, the ratio moved back below the 2008 high only very briefly. It stabilized above the 2008 high shortly thereafter and now it's moving slowly up once again. Well, slowly if you take the day-to-day price movement into account. In case of the long-term point of view, the strong uptrend simply resumed after a quick breather.

Anything after a breakout is vulnerable to a quick correction to the previously broken levels. On the other hand, anything after a breakout that was already confirmed, is ready to move higher and the risk of another corrective decline is much lower.

The most important thing about the gold and silver ratio chart to keep in mind is that it's after a breakout above the 2008 high and this breakout was already verified. This means that the ratio is likely to rally further. It's not likely to decline based on being "high" relative to its historical average. That's not how breakouts work.

Besides, the true, long-term resistance in the gold to silver ratio is at about 100 level. This level was not yet reached, which means that as long as the trend remains intact (and it does remain intact), the 100 level will continue to be the likely target.

Having discussed the situation in both key precious metals, let's analyze the situation in the precious metals mining stocks. As with gold and silver, there's a flagship analogy present in the gold miners.

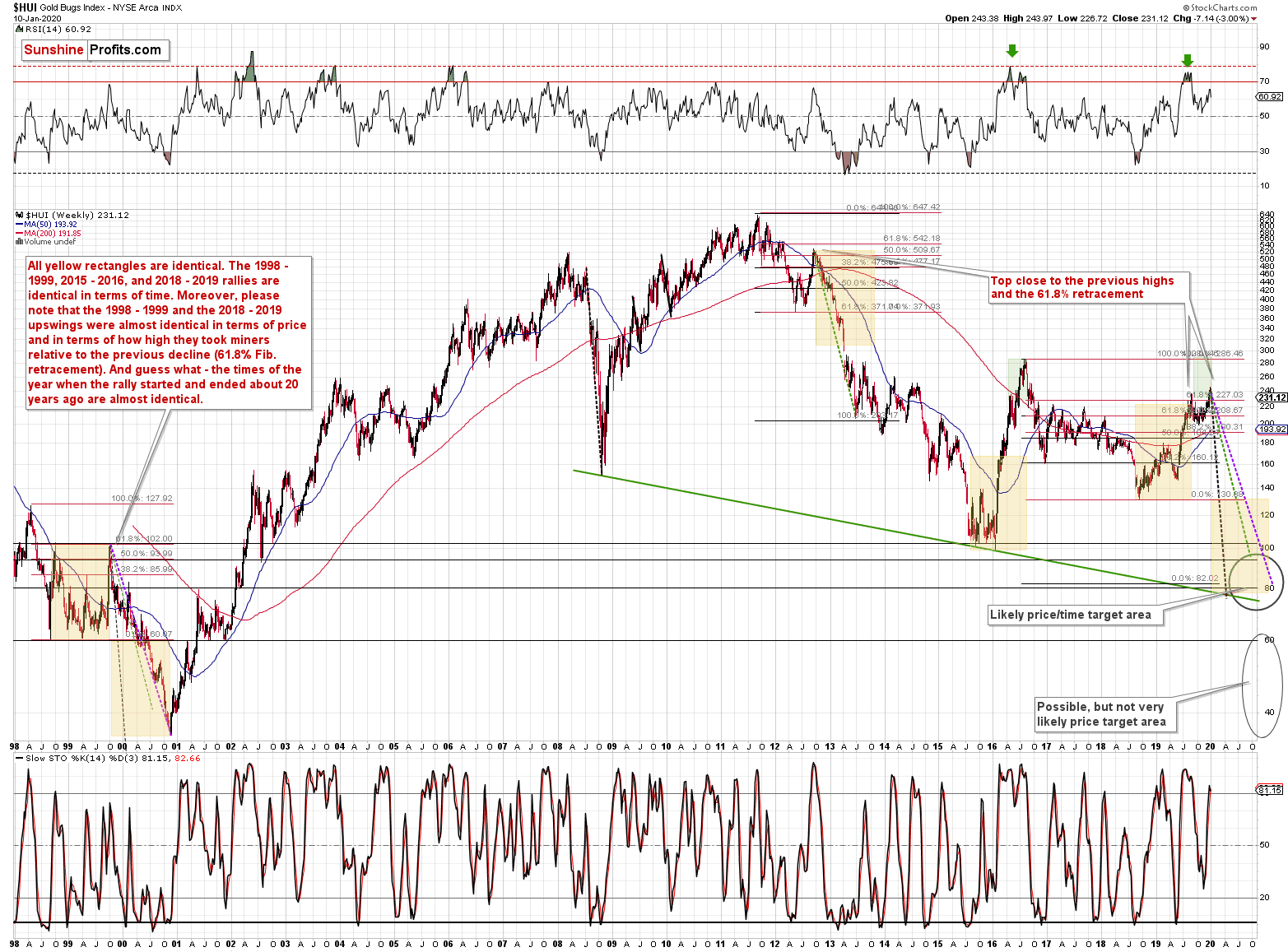

Turning to Gold Miners

In case of gold stocks, we see that the history is repeating with an almost exact 20-year delay. This might sound crazy... Until you see the chart reveakubg how precise it is, and how well it fits to what happened now and in 2012 as well.

(as a reminder, clicking on the chart will expand it)

Let's start with something relatively more familiar - the Fibonacci retracements. Back in 2012, the HUI Index retraced almost 61.8% of the preceding rally before the decline continued. That was one of the reasons that we thought that the 2019 rally won't get much above this retracement, if at all. Indeed, the August breakout above this retracement was very short-lived. The current move higher took the HUI just a little above the August high and this move was already invalidated as gold miners declined this year.

The important thing is that this is not the only time when this retracement stopped a sizable, yet counter-trend rally before a big decline.

The 1999 top formed almost exactly at the 61.8% Fibonacci retracement. That's one similarity between what happened recently and in 2012.

The second similarity is what's so exciting about this discovery. The length of the rally. All yellow rectangles on the above chart are identical. The 1998 - 1999, 2015 - 2016, and 2018 - 2019 rallies are identical in terms of time. Most importantly, the 1998 - 1999 and the 2018 - August 2019 upswings were almost identical in terms of both: time and price. And that's in addition to both rallies ending at the same Fibonacci retracement.

Let's re-state it again. Both rallies took practically the same amount of time, and the rallies were almost alike in terms of size - percentagewise.

The current move up is just a little above the August high and the breakout is not confirmed, which is why we don't yet view the current prices as the end of the rally. It's more of a double-top at this time. The rally seems to have ended in August and the only thing we see right now is a re-test of the same Fibonacci retracement.

The times of the year when the rally started and ended about 20 years ago are almost identical as well. The 1998 rally started right after the middle of the year and the same thing happened in 2018. The rally ended in the second part of 1999 and the same was / is the case right now. The month is not the same, but it's close nonetheless.

Based on the way in which the previous bear market in gold stocks ended, it seems that we have about a year of lower prices ahead of us and the HUI Index will decline at or a bit below the 80 level. That's in perfect tune with the upper one of the price target areas that we've been featuring on the above chart for some time now. The key of the additional trading techniques pointing to the 80 level or its proximity as the downside target are the early 1999, and 2011 tops as well as the early 2002 bottom, and the long-term declining support line based on the 2008 and 2016 lows.

The implications extend beyond just the final target - the analogy can tell us something important about the likely corrective upswings that we'll see along the way. Some of them will be relatively small, but there will also be those that are visible even from the long-term point of view, such as the one that we saw in early 2000.

How to detect them? Let's get back to the basics. When does a price rally, even though it remains in a downtrend? When it gets too low, too soon - at least in many cases. The key follow-up question is "too low compared to what?". And that's where the analogy to the 1999 - 2000 decline comes into play.

The purple line is the line that connects the start and the end of the 1999 - 2000 decline. The green line marks the start and the end of the 2012 - 2013 decline and the black one is based on the 2008 decline. There are two rules that we can detect based on these analogies.

First, the time after which we saw corrections during longer declines is similar to the times when the quicker decline ended. The end of the black line (early 2000) is also when we - approximately - saw the first big corrective upswing during the decline. Applying the same technique to the current top (of course, assuming that the top is being formed right now) provides us with early April 2020 as the likely bottoming target date. Naturally, it's likely to be just a short-term bottom that would be followed by a corrective upswing and then even lower prices.

Second, the chance of a corrective upswing and the chance that such upswing would be significant increases dramatically when price moves visibly below the dashed line. There are 3 dashed lines to choose from - each based on a different decline - so the question is which one should be used. It seems that the middle one is appropriate as it was most useful in 2000. The 2012-2013 decline took place mostly above the dashed line that connected its starting and ending point and it didn't have profound corrective upswings until it ended. What we saw 20 years ago, however, was very different. The price declined sharply initially, but then corrected a few times and the more price moved below the declining green dashed line, the bigger the corrective upswing was.

So, if the HUI moves visibly below the declining green dashed line, it will suggest that the miners got too low too fast and are likely to bounce back up sooner rather than later.

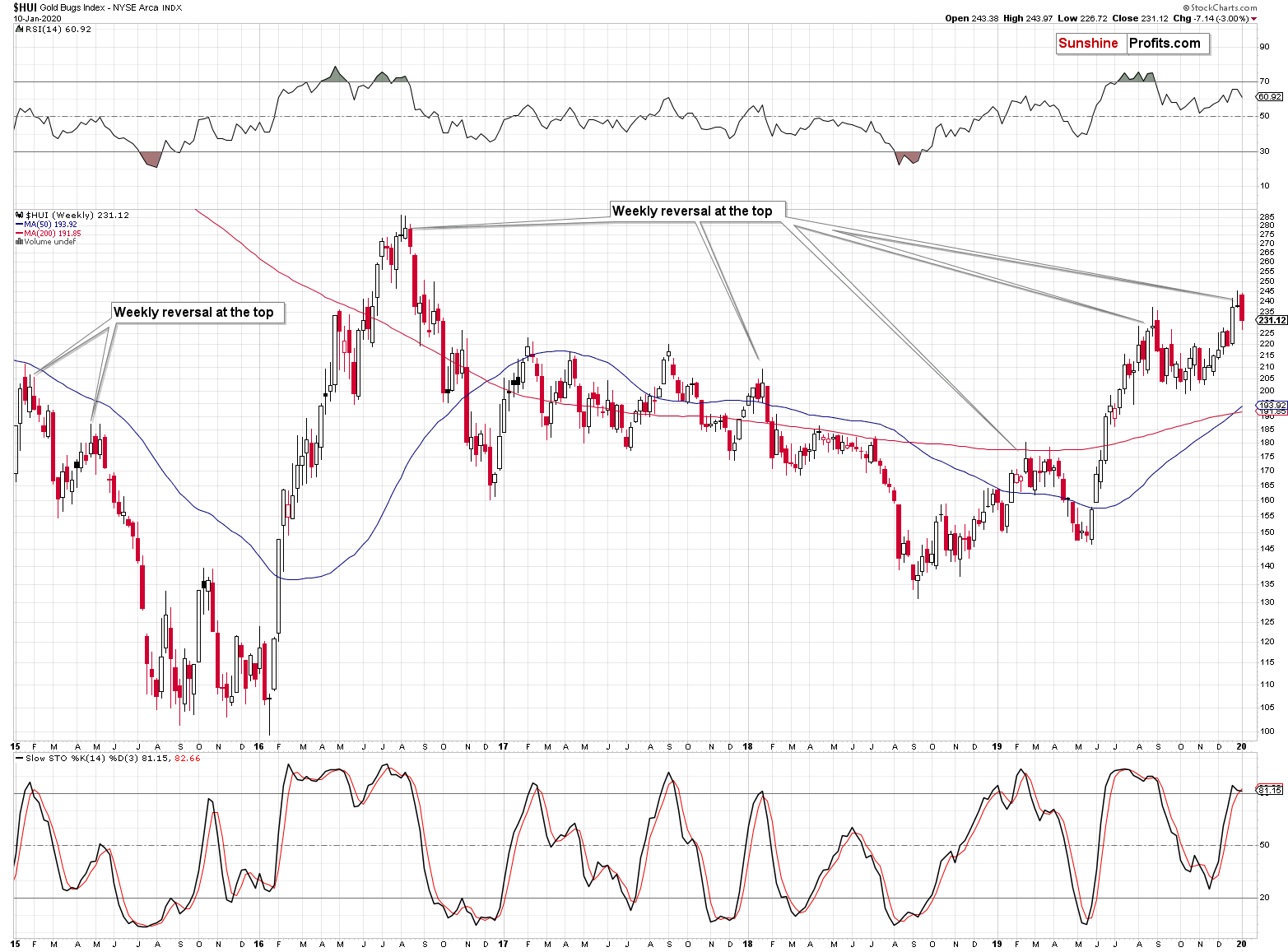

As far as the short term is concerned, the HUI Index is practically screaming in investors' ears: get out, get out now! And the scream is even louder than it was last Monday.

Last week, we wrote that we couldn't recall the date when the underperformance of gold miners relative to gold was more shocking. The implications were bearish and gold miners fell particularly hard.

So far this year, gold is up by 2.43%, silver is up by 1.03%, and gold stocks are down by 4.47%. It's not just very bearish for the precious metals market, it's truly an extreme reading.

In terms of weekly price changes, the HUI Index declined right after the clear gravestone-doji reversal, just like it was supposed to. The odds are that the reversal triggered much more than just a weekly decline.

This means that the HUI Index jus formed a clear weekly reversal. Sometimes, these reversals take form of shooting star candlesticks (mid-2015, second weekly high of 2016, early 2018, early 2019), and sometimes we get gravestone dojis (first weekly high of 2016, and right now; the August high is also somewhat similar).

In all the above-mentioned cases, the weekly reversal in the HUI Index had very important implications. Combining this with the extreme weakness that gold miners are showing relative to gold and all the retracements just reached throughout the precious metals sector, it's very likely that the rally in gold is just a very temporary development and that one should be prepared for much lower gold, silver, and mining stock prices instead.

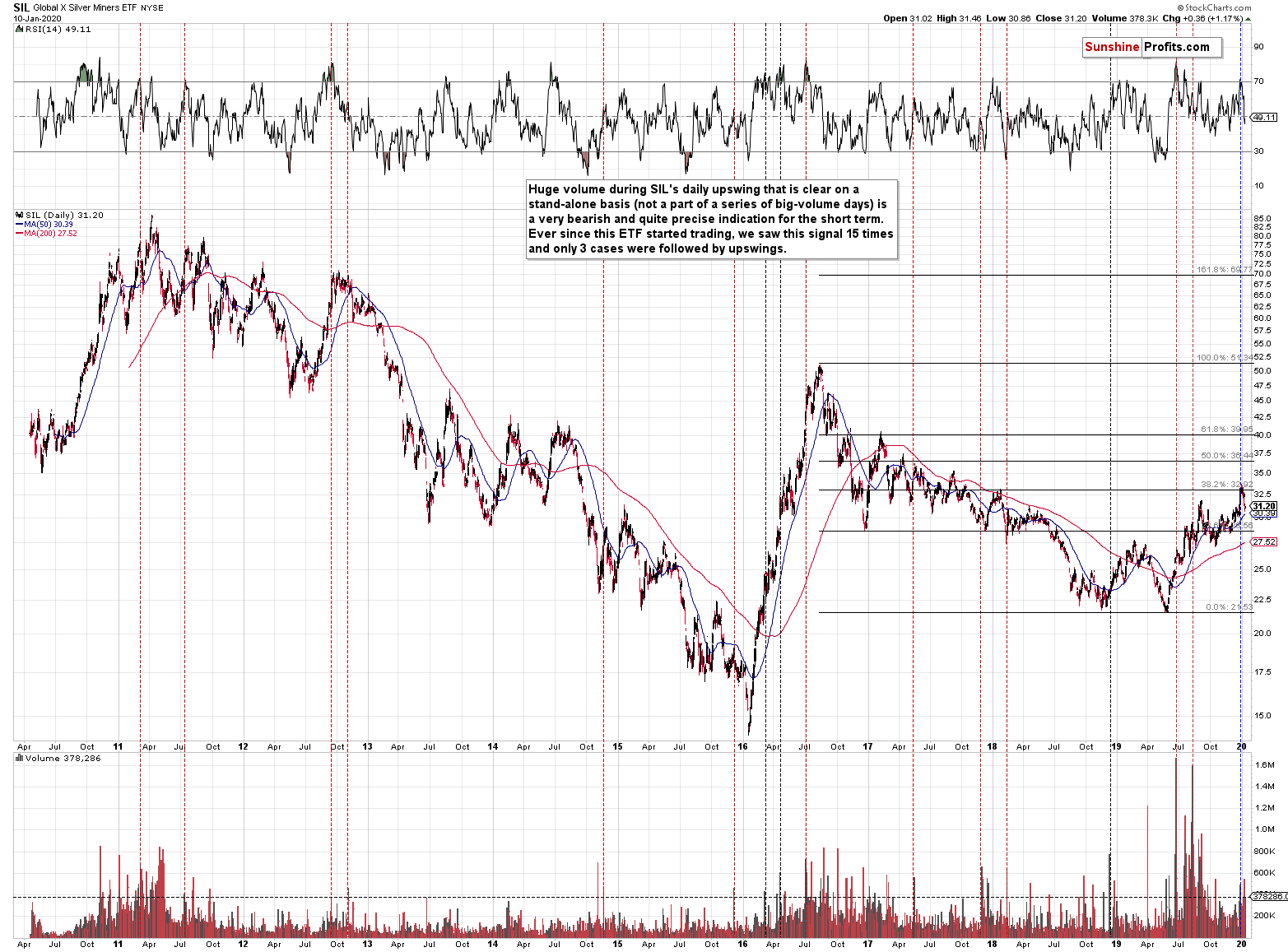

Finally, we would like to bring your attention to the fact that silver stocks reversed after the (failed) huge-volume attempt to break above the 38.2% Fibonacci retracement level.

Silver Stocks in Focus

"Silver stocks reached their new yearly high on relatively strong volume" sounded very bullish, doesn't it?

The problem was - as we had explained in the previous Alerts - that reaching the new yearly high meant that silver miners were barely able to correct 38.2% of the decline from the 2016 high. And that's compared to the decline alone. Comparing the recent rally to the one that we saw in 2016, we see that this year's upswing is barely one fifth of the previous upswing (about 50% vs about 250%). That's a very weak performance - silver miners don't really want to move higher, they are forced to move higher as gold and silver are increasing, but the size of the move emphasizes that it's not the "true" direction in which the market is really moving.

The volume is also not as bullish as it seems to be at the first sight. Conversely, huge volume during SIL's (ETF for silver stocks) daily upswing that is clear on a stand-alone basis (not a part of a series of big-volume days) is a very bearish and quite precise indication for the short term. Ever since this ETF started trading, we saw this signal 15 times and only 3 cases were followed by upswings.

Yes, the silver stocks moved sharply higher on a very short-term basis, but please note that they had moved sharply lower on a very short-term basis in early 2016. The opposite of the recent price action was what preceded the biggest and most volatile rally of the recent years. If we see a reversal and invalidation of the breakout to new 2019 highs, we'll have almost exactly the opposite situation and the implications will be even more bearish.

Moreover, let's keep in mind that silver stocks closed last week lower than they had closed the week before. Silver miners are also underperforming - it's not just the golden part of the mining stock sector that does that.

Despite the early gains, silver stocks are down by almost 6% so far this year.

Summary

Summing up, gold reversed almost exactly at its triangle-vertex-based reversals, it happened on record-breaking weekly volume, and it was confirmed by analogous reversal in silver and weakness in mining stocks, which is a perfectly bearish combination. Based on these reveresals, very weak response to the recent missile attacks, the 61.8% Fibonacci retracements that were hit, along with multiple similarities present in gold, silver, and mining stocks, as well as on the bullish situation in the USD Index, both the medium-term and short-term outlooks for the precious metals market are very bearish.

In other words, the profit potential of our trading positions remains intact. In our view, if there ever was an excellent time to enter or add to one's short positions in the precious metals sector - this is it.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short position (250% of the full position) in gold, silver, and mining stocks is justified from the risk/reward perspective with the following stop-loss orders and binding exit profit-take price levels:

- Gold futures: profit-take exit price: $1,391; stop-loss: $1,622; initial target price for the DGLD ETN: $36.37; stop-loss for the DGLD ETN: $22.89

- Silver futures: profit-take exit price: $15.11; stop-loss: $19.06; initial target price for the DSLV ETN: $24.88; stop-loss for the DSLV ETN: $14.07

- Mining stocks (price levels for the GDX ETF): profit-take exit price: $23.21; stop-loss: $30.11; initial target price for the DUST ETF: $14.69; stop-loss for the DUST ETF $5.09

In case one wants to bet on junior mining stocks' prices, here are the stop-loss details and target prices:

- GDXJ ETF: profit-take exit price: $30.32; stop-loss: $44.22

- JDST ETF: profit-take exit price: $35.88 stop-loss: $9.68

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that the in the trading section we describe the situation for the day that the alert is posted. In other words, it we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices, so that you can decide whether keeping a position on a given day is something that is in tune with your approach (some moves are too small for medium-term traders and some might appear too big for day-traders).

Plus, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one, it's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (DGLD for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn't, then we will view both positions (in gold and DGLD) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager