Briefly: in our opinion, full (100% of the regular position size) speculative long positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Another day, another higher close in the junior miners. And another day where profits on our long positions in the latter increased. There is a sign that the rally in the precious metals sector is close to being over.

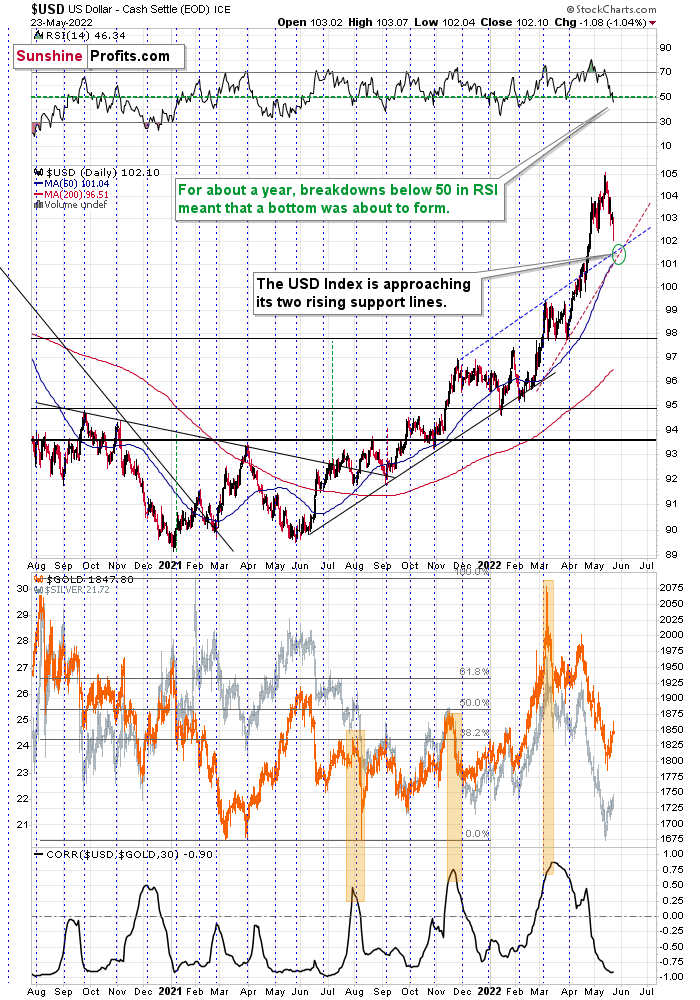

That sign is the situation in the USD Index, and the shape of the gold-USD link.

Starting with the gold-USD link, please note that while gold ended yesterday’s session higher, it was only ~$6 higher. Given that the USD Index declined by over one index point, it would be “normal” for gold to rally much more.

That’s a sign that gold is getting “exhausted”, which is another way of saying that the buying power for this particular rally appears to be drying up. Of course, one swallow doesn’t make a summer, but given the size of USD’s decline, it’s quite notable.

USD’s decline took it below its recent lows, and since it’s slightly down also in today’s pre-market trading, it seems that it can now decline further in the very near term. “Further” here shouldn’t be viewed as “by a lot”. In fact, there is a combination of rising support lines just above where the USD Index is trading right now.

The dashed lines: blue and red one are likely to stop this correction. Of course, it’s not 100% certain, but the fundamental situation continues to favor higher USD values (rising real interest rates), so significant changes don’t appear likely. The possibility is there, especially if the geopolitical situation changes, but it’s simply not likely.

Besides, the RSI just moved below 50, and while this doesn’t mean anything based on “classic” interpretation of this indicator’s signals, I would like to emphasize that practically each time when we saw something like that in the past year or so, it meant that the USD Index was about to bottom.

So, on one hand, gold no longer “wants” to react to the USD’s weakness, and on the other hand, the short-term bottom in the USD Index appears to be at hand.

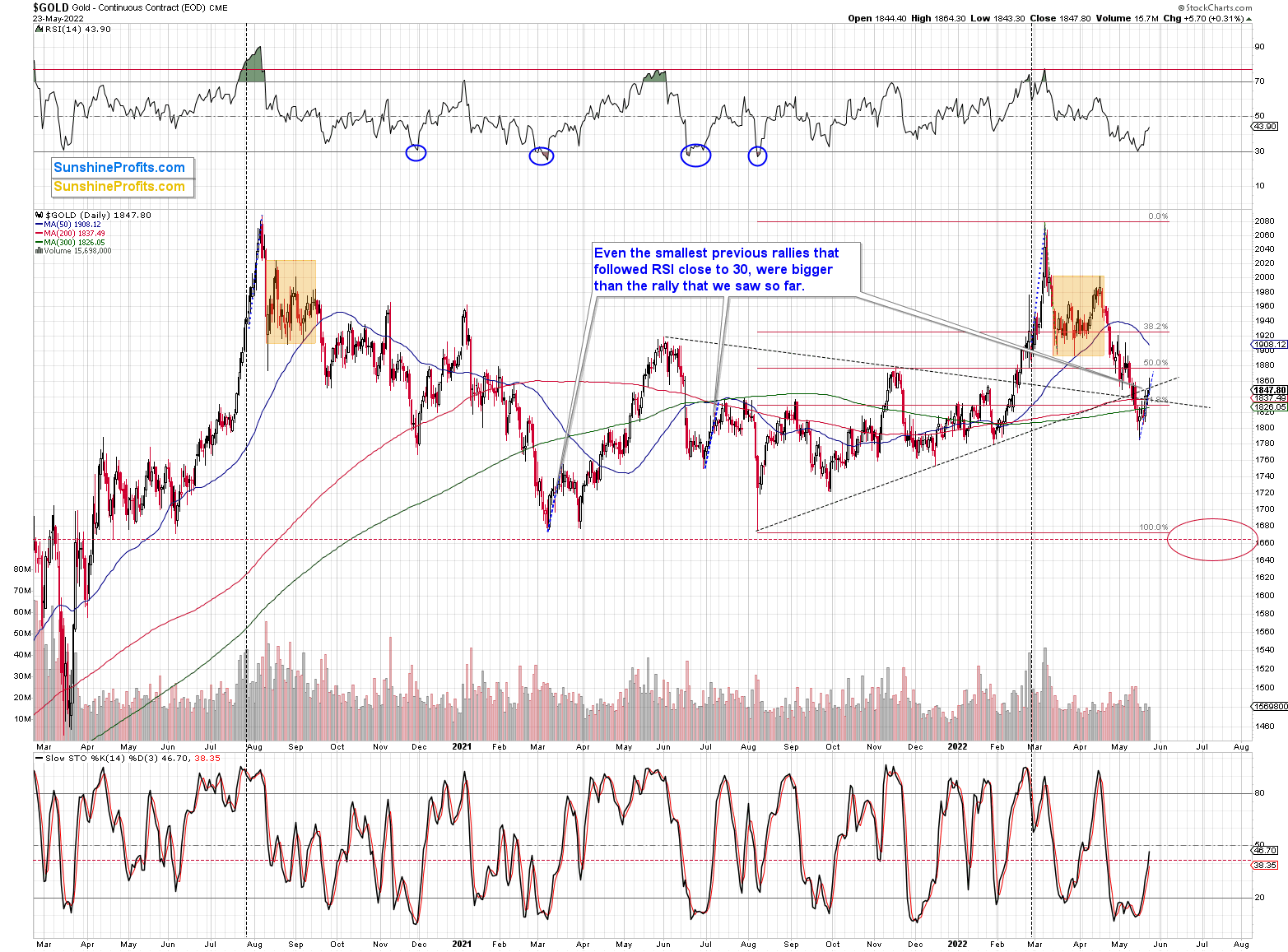

Gold itself still didn’t correct as much as it did after previous cases when the RSI touched the 30 level. I marked the smallest rallies that followed this signal in the recent past with blue, dashed lines.

If history is about to rhyme, then gold’s rally might be nearing its end, but it’s not yet there.

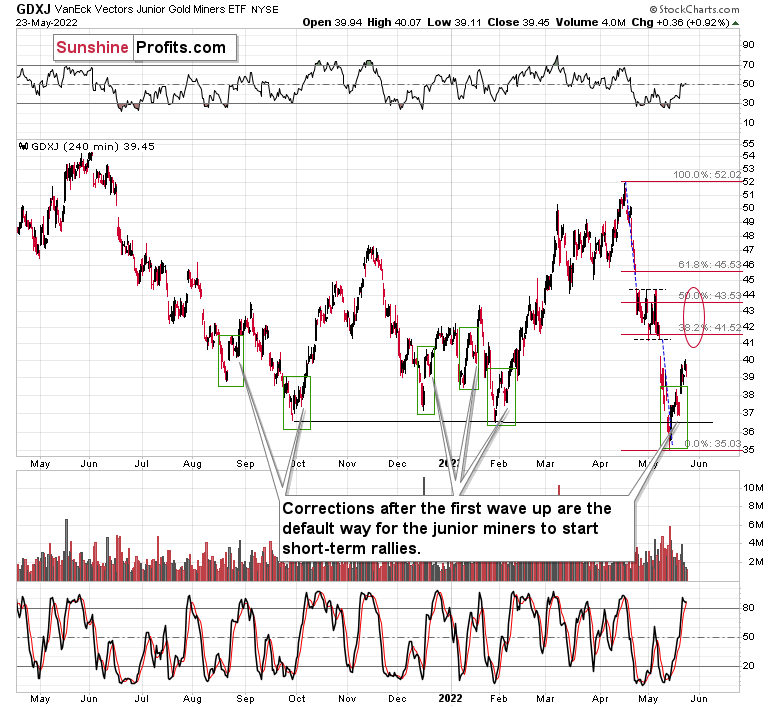

And what about the junior mining stocks?

Well, their rebound simply continues. The GDXJ ETF ended yesterday’s session 0.92% higher (GDX was up by 0.59%, silver was up by 0.23% and gold by 0.31%). They are up by almost $4 (about 10%) from May 12, when we switched from short to long positions in the USDX – more than any of the above-mentioned markets.

The USD’s decline appears to be close to its end, and the same goes for the end of the short-term rally in gold, which means that the same fate likely awaits the junior miners – their rally too is about to end, in my view.

The target area that I placed on the above chart remains up-to-date. Yesterday’s weakness in gold relative to the USD Index tells me that it’s more likely that the rally will end in the lower part of the target area – probably close to its early-May low.

Having said that, let’s take a look at the markets from a more fundamental point of view.

Follow the Herd

With investors akin to a feather on a fence post, they often move in whichever direction the wind is blowing. Therefore, with recession whispers going from a light breeze to a hurricane, those that professed the all-clear two months ago are now joining the chorus. For example, here is the latest outlook from Charles Schwab’s Chief Investment Strategist Liz Ann Sonders.

Source: Charles Schwab

Source: Charles Schwab

However, the ‘new narrative’ contrasts Sonders’ sentiment on Mar. 25:

Source: Politico

Source: Politico

As a result, while the winds of change move swiftly across Wall Street, the tug-of-war between sentiment and fundamentals has strategists running in circles. However, with some investors cheering on a recession, they hope that U.S. consumers roll over. To explain, I wrote on May 23:

While narratives move markets, the doom-and-gloom crowd is cherry-picking data to support their conclusion. Moreover, I don’t care if/when the U.S. falls into recession. I’m simply presenting an objective analysis. Also, I’ve noted on numerous occasions that investors underestimated the demand side of the inflation equation.

In addition, the recession crowd doesn’t realize that a penniless consumer is actually bullish for the S&P 500 because demand destruction reduces inflation and allows the Fed to resume QE. In contrast, resilient consumer spending keeps the Fed’s foot on the hawkish accelerator. As a result, with the latter stronger than many believe, inflation should remain uplifted, and the Fed’s liquidity drain should result in more medium-term pain for the PMs and the general stock market.

To that point, while the permabears don’t realize that their recession fears help the permabulls, it didn’t take long for the latter to rejoice.

Please see below:

Source: Business Insider

Source: Business Insider

Specifically, Fundstrat founder Tom Lee said:

"Incoming data could show labor market weakening... and thus [the] job market could be cooling at a pace faster than implied by tighter financial conditions." Moreover, “layoffs are accelerating, hitting 7,700 so far in May....We expect this to soon go parabolic, based upon anecdotal comments we have heard.”

As a result:

Source: Business Insider

Source: Business Insider

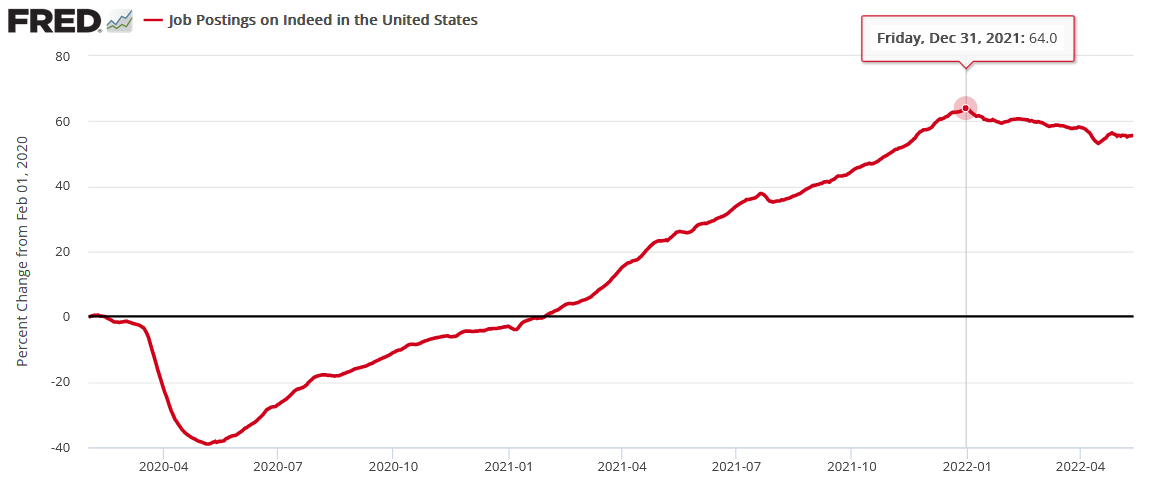

Again, the permabulls want a recession so that inflation craters and the Fed can resume QE. However, to refute Lee’s initial claim, U.S. job postings on Indeed are 55.6% above their pre-pandemic baseline. Moreover, while the figure has declined recently, it’s nowhere near falling off a cliff.

Please see below:

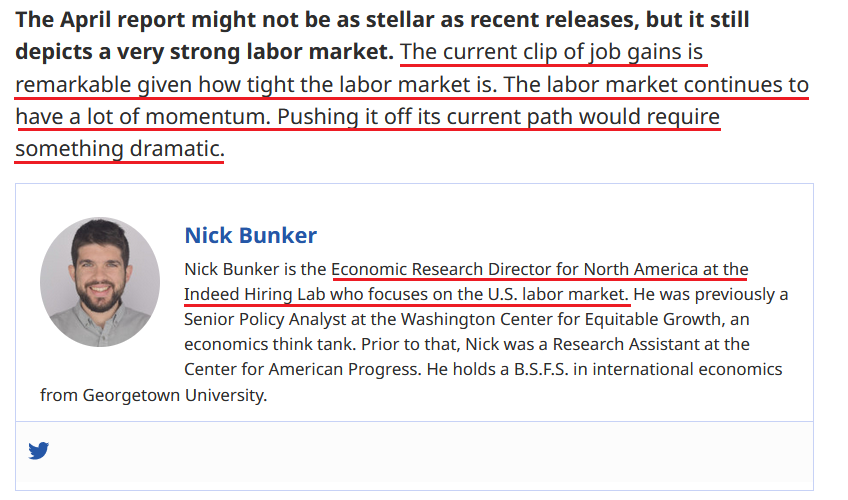

Also, Indeed released its latest jobs report on May 6. An excerpt read:

“Compared to recent reports, the April jobs numbers might seem like a letdown but in context they are quite impressive. The report contains some slight disappointments as the labor force participation rate ticked down.

“But let’s keep these numbers in perspective. Over the past three months, jobs have been added at a pace of more than a half million a month as the unemployment rate hovers just above 3.5%. Extraordinarily high levels of demand for workers is leading to fast job gains despite the low levels of joblessness. The outlook for the US economy is highly uncertain, but the labor market continues to be a source of strength.”

As a result:

Source: Indeed

Source: Indeed

Furthermore, the U.S. economy should be moderating. That's how rate hikes reduce inflation. Remember, the Fed has hiked interest rates three times (25 basis point increments), and each increase should further cool demand.

Therefore, all-time high metrics should come down. However, investors' assessments have gone from 100 to 0, and they're extrapolating that we'll decelerate from record figures to the next financial crisis in three months. In reality, the Fed has to fire plenty of hawkish bullets to solve its inflation problem.

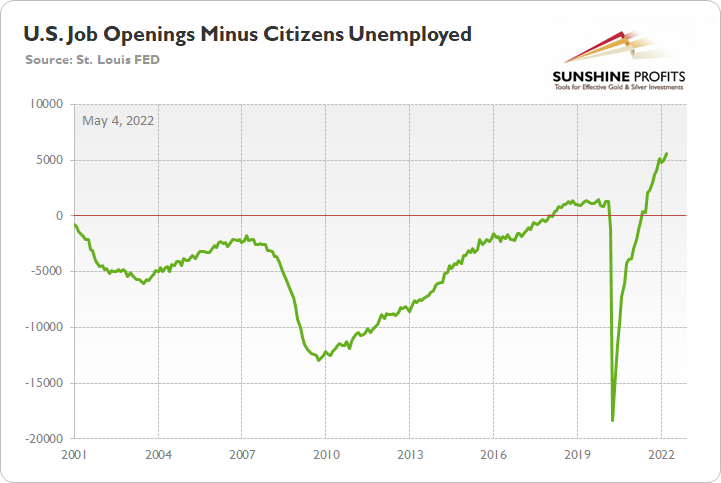

To that point, with the latest government data showing that there are 5.597 million more job openings in the U.S. than citizens unemployed, an all-time high, the U.S. labor market needs to cool substantially for inflation to subside. I wrote on May 4:

To explain, the green line above subtracts the number of unemployed U.S. citizens from the number of U.S. job openings. If you analyze the right side of the chart, you can see that the epic collapse has completely reversed and the green line is at a record high. Thus, with more jobs available than people looking for work, the economic environment supports normalization by the Fed.

As for Lee’s second point – the notion that “revenge travel” should abate – it’s another example of sentiment versus fundamentals.

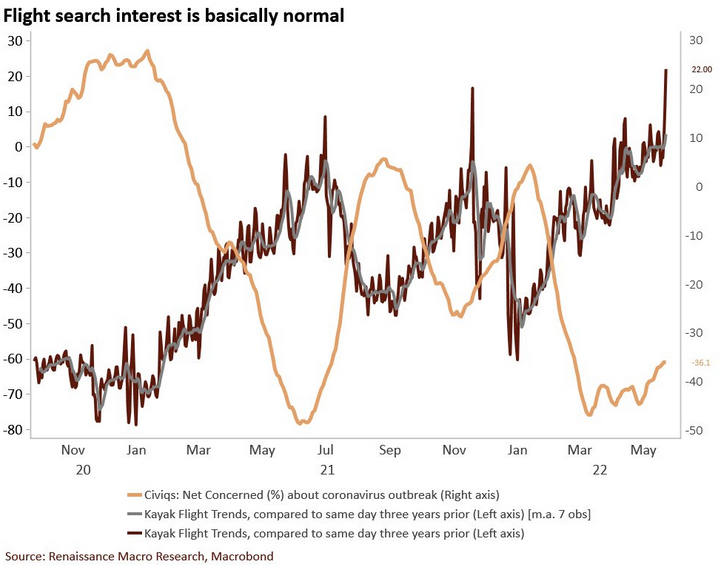

Please see below:

To explain, the dark brown line above tracks KAYAK flight searches, while the light brown line above tracks the net percentage of Americans concerned about COVID-19. As you can see, the pair have an inverse relationship.

More importantly, if you analyze the right side of the chart, you can see that KAYAK flight searches hit a new post-pandemic high. As a result, does it seem like “revenge travel” has run its course?

Moreover, I warned on Jan. 31 that pandemic deceleration and summertime spending would keep inflation uplifted. I wrote:

The U.S. economy is growing well ahead of its pre-pandemic trend. Moreover, while disruptions from the Omicron variant will likely slow growth in Q1, the outbreak should calm down when warmer weather arrives. With the season also allowing for patio dining, camping trips, and other outdoor activities that support economic growth, Q1’s weakness should be short-lived.

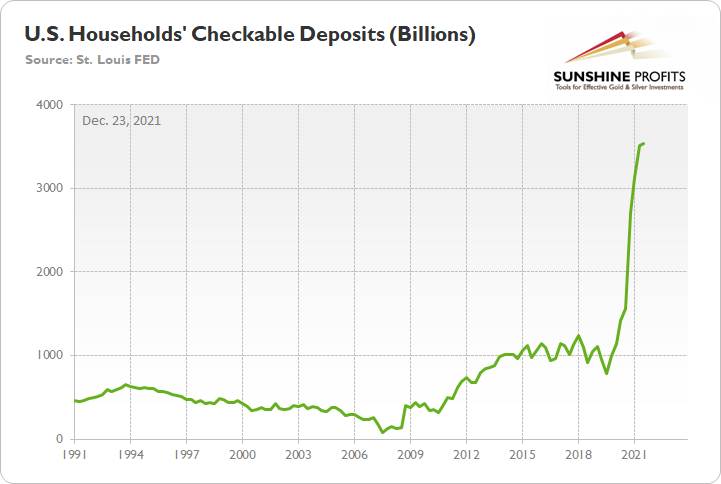

Therefore, while investors pray for consumers to run out of cash, inflation to subside, and the Fed to inject more stimulus (the faulty post-GFC thesis), wishing won’t make it come to fruition. To explain, I’ve written a lot about U.S. households’ financial strength and how unprecedented handouts led to abnormal demand and inflation. Here is a chart from Dec. 23:

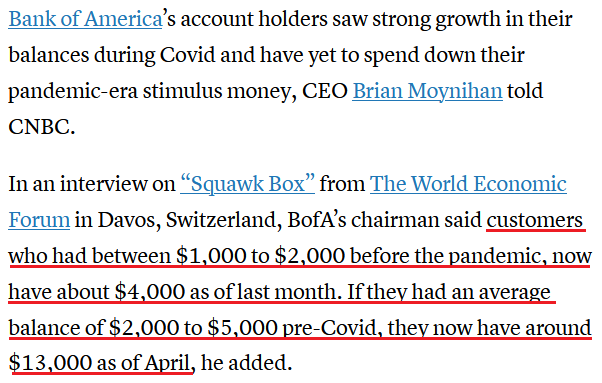

To that point, Bank of America CEO Brian Moynihan – who heads the second-largest bank in the U.S. – said on May 23 that “In the balances of our customers, they have more money. In April, their balances grew over March, and in March they grew over all the way back to mid-last year.”

As such, while investors are hung up on the dwindling personal savings rate, they miss the forest through the trees by ignoring Americans’ other demand deposit accounts.

Please see below:

Source: CNBC

Source: CNBC

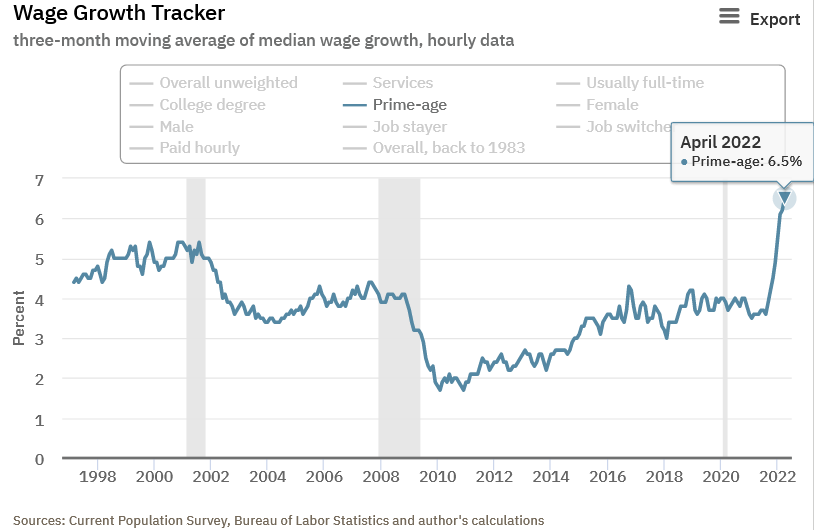

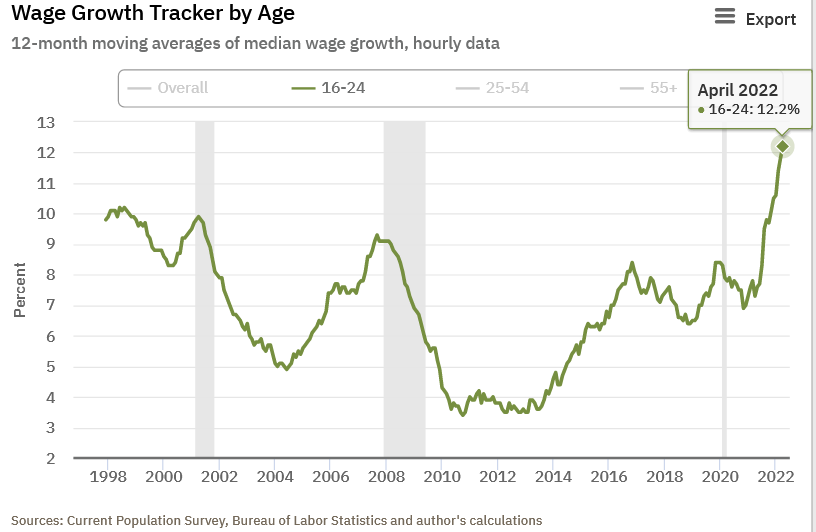

Second, the Atlanta Fed’s wage tracker shows that prime-age workers – those between 25 and 54 – saw their median three-month wage increase by a record 6.5% in April.

Please see below:

Even more revealing, the data shows that Americans aged 16-24 – often the lowest earners – saw their median three-month wage increase by a blistering 12.2% in April.

Please see below:

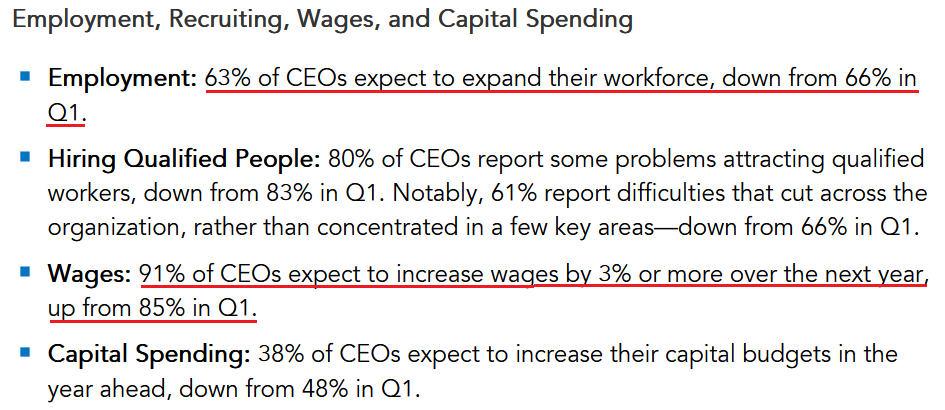

Likewise, while CEO confidence has eroded due to the changing macroeconomic backdrop, 91% of executives still plan to increase their employees’ wages. I wrote on May 18:

While consolidated CEO confidence has crashed to “levels not seen since the onset of the pandemic,” nearly two-thirds of CEOs plan to increase their workforce and more than nine out of 10 plan to increase wages. As a result, would major U.S. corporations be adding employees and paying them more if demand has fallen off a cliff?

Source: The Confidence Board

Source: The Confidence Board

The bottom line? It’s ironic how the permabears hope for a recession so that the stock market will crash and the permabulls hope for a recession so that the stock market will rally. Confused? Well, the reality is that collapsing inflation allows the Fed to perform a dovish 180 and follow the post-GFC script. Therefore, the ‘bad news is good news’ mantra will likely benefit the bulls.

Conversely, the longer inflation persists, the longer the Fed stays on the sidelines. Thus, simmering inflation and resilient consumer spending should keep the Fed on a hawkish warpath, which is bearish for the S&P 500 and the PMs.

Again, macroeconomic data declining from all-time highs represents normalization, not a crisis. Moreover, what did investors think would happen when the Fed started hiking interest rates? Of course, economic momentum would moderate. However, with a huge gap between 8%+ annualized inflation and the Fed’s 2% goal, more rate hikes are needed to alleviate the pricing pressures.

In conclusion, the PMs rallied on May 23, and our long position in the GDXJ ETF continues to pay dividends. However, while investors hope that U.S. consumers will falter and the Fed will turn dovish, the reality is that you don’t kill 8%+ annualized inflation with a 0.83% U.S. federal funds rate. As a result, more hawkish fireworks should erupt in the coming months.

Overview of the Upcoming Part of the Decline

- It seems to me that the short-term rally in the precious metals market is relatively close to being over, and if not, then at least the easy part of the long trade is getting close to being over.

- After the above-mentioned correction, we’re likely to see another big slide, perhaps close to the 2021 lows ($1,650 - $1,700).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

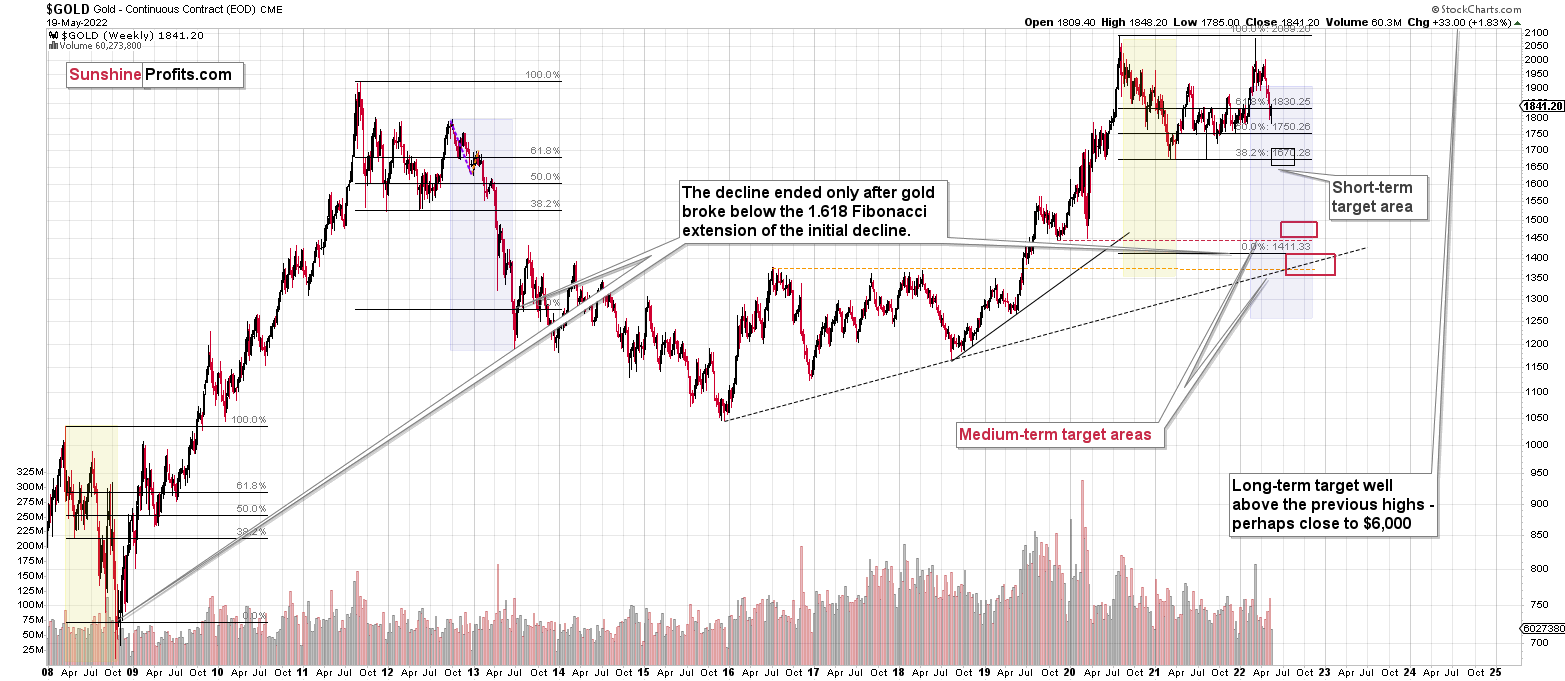

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, it seems to me that the short-term rally in the precious metals market is relatively close to being over, and if not, then at least the easy part of the long trade is getting close to being over. While our profits on this long trade have grown quickly, it seems that after they grow a bit more and the GDXJ reaches our target ($40.96), it might be a good idea to take them off the table and return to the short positions (300% of the regular position size) in the junior mining stocks (GDXJ).

As we’re now quite close to the exit level in the GDXJ, I’m re-calibrating the target for the JNUG, so it’s now slightly lower (this ETF provides 2x leverage for DAILY price moves, so it’s ultimate target depends on the path of the GDXJ, not just on its price, so it’s impossible to determine the target with 100% accuracy upfront). As the USD Index might be close to its bottom and the general stock market might not be far from its upside target, it seems to be a good idea to adjust targets for gold and silver as well by moving them lower.

The medium-term downtrend is likely to continue shortly (perhaps after a weekly or a few-day long correction). As investors are starting to wake up to reality, the precious metals sector (particularly junior mining stocks) is declining sharply. Here are the key aspects of the reality that market participants have ignored:

- rising real interest rates,

- rising USD Index values.

Both of the aforementioned are the two most important fundamental drivers of the gold price. Since neither the USD Index nor real interest rates are likely to stop rising anytime soon (especially now that inflation has become highly political), the gold price is likely to fall sooner or later. Given the analogy to 2012 in gold, silver, and mining stocks, “sooner” is the more likely outcome.

It seems that our profits from short positions are going to become truly epic in the coming months. And the profits from the current long position are likely to enhance them even further.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative long positions (100% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $40.96; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JNUG (2x leveraged). The binding profit-take level for the JNUG: $56.18; stop-loss for the JNUG: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: $22.28

SLV profit-take exit price: $20.48

AGQ profit-take exit price: $29.96

Gold futures downside profit-take exit price: $1,909

HGU.TO – alternative (Canadian) 2x leveraged gold stocks ETF – the upside profit-take exit price: $17.28

HZU.TO – alternative (Canadian) 2x leveraged silver ETF – the upside profit-take exit price: $11.28

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief