Please log in to read the entire text.

If you don’t have a login yet, please select your access package.

“Do you love me?”, asked gold. “Of course, my dear”, replied Jay, but his thoughts were with others: asset purchases tapering and interest rate hikes.

“It’s complicated” – this is how many people answer questions about their romantic lives. The relationship between gold and Jerome Powell is also not a clear one. As you know, in November, President Biden announced that he would reappoint Powell for the second term as the Fed Chair. It means that gold will have to live with Jerome under the same roof for another four years.

To say that gold didn’t like it is to say nothing. The yellow metal snapped and left the cozy living room of $1,850, slamming the door loudly. In less literary expressions, its price plunged from above $1,860 on November 19 to $1,782 on November 24, 2021, as the chart below shows.

The impulsive gold’s reaction to Powell’s renomination resulted from its failed dream about a love affair with Lael Brainard. She was considered a leading contender to replace Powell. The contender that would be more dovish and, thus, more supportive of gold prices.

However, is a hawkish dove a hawk? Is Powell really a hawk? Even if more hawkish than Brainard, he still orchestrated an unprecedentedly accommodative monetary policy in response to the pandemic-related economic crisis. It was none other than Powell who started to cut interest rates in 2019, a year before the epidemic outbreak. It was he who implemented an inflation-averaging regime that allowed inflation to run above the target. Right now, it’s also Powell who claims that the current high inflation is transitory, although it’s clear for almost everyone else that it’s more persistent. I wouldn’t call Powell a hawk then. He is rather a dove in a hawk’s clothing.

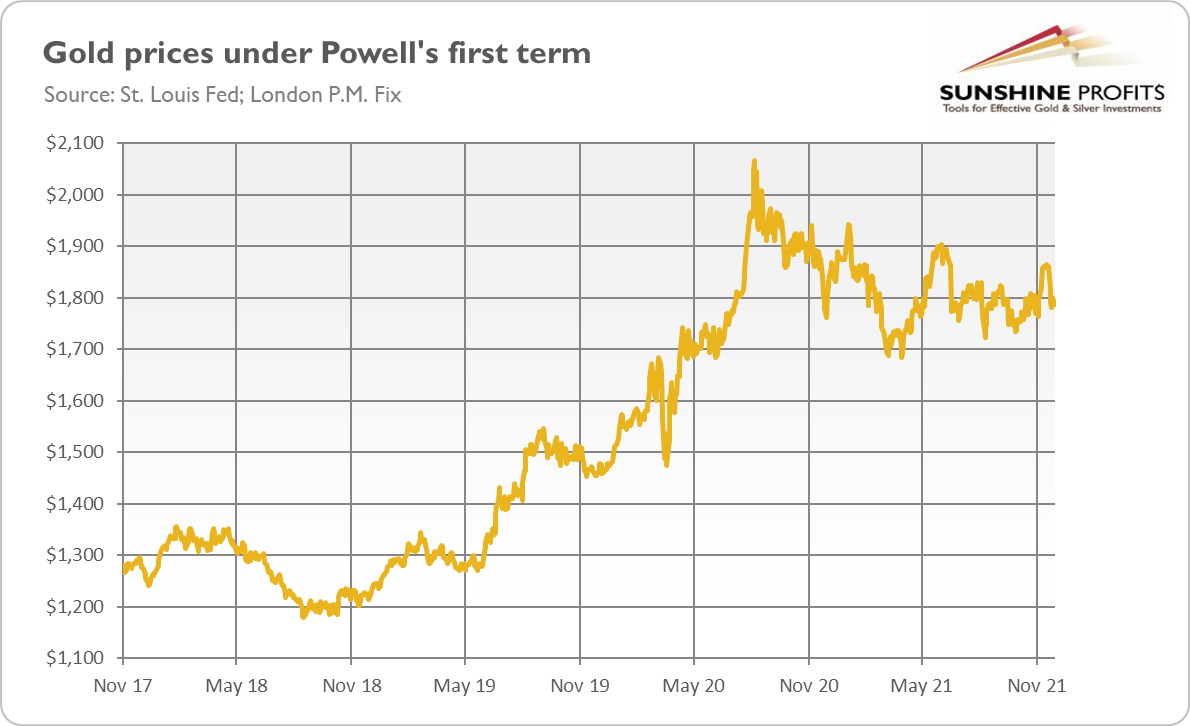

So, gold doesn’t have to suffer under Powell’s second term as the Fed Chair. Please take a look at the chart below, which shows gold’s performance in the period of 2017-2021. As you can see, the yellow metal gained about 34% during Powell’s first term as the chair of the Federal Reserve that started in February 2018 (or 40% since Trump’s November 2017 nomination of the Fed).

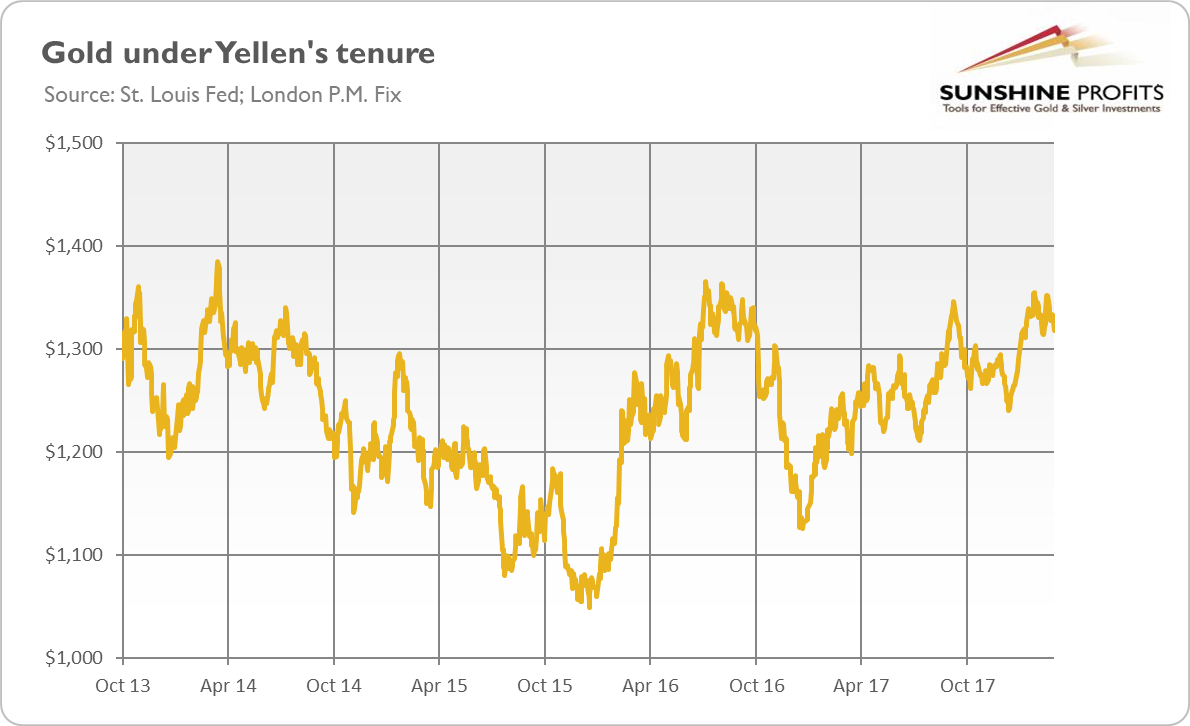

Not bad! Actually, gold performed much better back then than under Yellen’s term as the Fed Chair. During her tenure, which took place in 2014-2018, the yellow metal was traded sideways, remaining generally in a corridor between $1,100-$1,300.

I’m not saying that Yellen despised gold, while Powell loves it. My point is that gold’s performance during the tenures of Fed Chairs varies along with changes in the macroeconomic environment in which they act and the monetary stance they adopt. Gold suffered strongly until December 2015, when Yellen finally started hiking the federal funds rate. It then rebounded, only to struggle again in 2018 amid an aggressive tightening cycle. However, at the end of that year it started to rally due to a dovish shift within the Fed, and, of course, in a lagged response to unprecedented fiscal and monetary actions later in 2020.

I have bad and good news here. The former is that the macroeconomic environment during Powell’s second term could be more inflationary, demanding more hawkish actions. The Fed has already started tapering of its quantitative easing, and bets are accumulating that it could start hiking interest rates somewhere around mid-2022. What’s more, the continuation of Powell’s leadership ensures more stability and provides markets with more certainty about what to expect from the Fed in the coming years. This is bad news for safe-haven assets such as gold.

Last but not least, the composition of the FOMC is going to shift toward the hawkish side. This is because some strong doves, such as Daly and Evans, are out, while some notable hawks, such as George, Mester (and also Bullard), are among the voting members in 2022. Gold may, therefore, find itself under downward pressure next year, especially in its first half.

On the other hand, the current FOMC expresses clearly dovish bias. With mammoth public debt and elevated asset prices, aggressive tightening would simply be very risky from a financial and political point of view. So, the Fed is likely to generally remain behind the curve. By the way, Biden not only reappointed Powell for the second term as Fed Chair, but he also appointed Brainard as Vice-Chair. We also can’t exclude that Biden agreed to Powell’s second term only if he conducts “appropriate” monetary policy.

Democratic Senator Elizabeth Warren once called Powell “a dangerous man.” Well, in a way, it’s true, as powerful people can be dangerous. However, history shows that Powell doesn’t have to be a threat to gold. After all, he is not a hawk in the mold of Paul Volcker, but merely a hawkish dove, or a dove that will have to normalize the crisis monetary policy and curb inflation.

In the upcoming months, gold may struggle amid prospects of more interest rates hikes and likely strengthened hawkish rhetoric from the Fed. However, precious metals investors often sell the rumor and buy the fact. So, when the US central bank finally delivers them, better times may come for the yellow metal, and gold and Jay could live happily ever after. The End.

Thank you for reading today’s free analysis. If you enjoyed it, and would you like to know more about the links between the economic outlook, and the gold market, we invite you to read the December Gold Market Overview report. Please note that in addition to the above-mentioned free fundamental gold reports, and we provide premium daily Gold & Silver Trading Alerts with clear buy and sell signals. We provide these premium analyses also on a weekly basis in the form of Gold Investment Updates. In order to enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet though and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Arkadiusz Sieron, PhD

Sunshine Profits: Effective Investment through Diligence & Care.

-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.