Gold behaves like a currency. This has extremely important consequence: gold cannot be valued like assets which generate cash flows or even as commodities whose value can be at least estimated looking at the balance of demand and supply. Does it mean that gold is a mere speculation play? No! You have to remember that gold belongs to the currencies. As they have no cash flows, they cannot be valued, but they can be priced against other currencies.

The same applies to gold. It has no “true” which value we can estimate and to which it should converge. On the contrary, the price is the only real number we have and can act on. We see lot analysts who try to estimate the value of gold based on some links – which are allegedly set in stone – between the price of gold and the money supply or the level of the federal debt. And they estimate the “fair” value of gold at either $500 or $20,000. It’s a pure nonsense.

Investors have to remember that there are two games in the world of investing: the pricing game and the value game (see the table below). Since gold is neither a cash generating asset nor a commodity, we have to play the pricing game.

Table 1: Pricing vs. value game

| SunshineProfits.com | ||

|---|---|---|

| Two Types of Investment Game | Pricing Game | Value Game |

| Philosophy | The prices are all you have | Investment has a fair or true value |

| How to win the game? | You predict the future price direction and trade accordingly | You estimate the value of an asset, and buy (sell) it when under(over)valued |

| Key drivers | Demand & supply affected by investors' sentiment | Cash flows - their dynamics and risk |

Source: Own elaboration based on aswathdamodaran.blogspot.com

We will tell you how the gold pricing game really works. The price of the yellow metal is determined by demand and supply (and not by cash flows, etc.). But they are not affected by annual production and consumption – have you ever consumed a currency? – but by mood and momentum.

Would you like to know how to win the gold pricing game? In the world of cash generating assets you have to estimate the value of the asset and buy (sell) undervalued (overvalued) assets, with hope that the market price will eventually converge with the fundamental value. It doesn’t work with gold. If you want to win here, you have to guess the future direction of the price and trade ahead of the movement. You gain if you are right more often than wrong and you can exit the market before the trend reverses.

Just to make sure that you understand us correctly. By saying that the gold’s demand and supply are determined by mood and momentum, we are not implying that gold trading is merely a speculative play and fundamentals don’t matter. After all, we write fundamental analyses of the precious metals. And there really are a few fundamental factors which drive the gold prices. But their influence on gold occurs via investors’ moods.

Let’s elaborate on that. Gold behaves like currency, right? And what determines the price of each currency? Well, currencies which serve better as a medium of exchange and store of value appreciate, while currencies which don’t hold purchasing power depreciate. So the purchasing power parity works well, at least in the long term. Gold investors should know it the best, as the yellow metal is perceived to be excellent store of value over time and a hedge against inflation.

This is why people still demand gold, after all, although it is not the means of payment. They buy the shiny metal when they lose confidence in the fiat currencies, especially in the U.S. dollar. So, as you can see, one of the most important fundamental factors in the gold market is the level of confidence in the current monetary system based on fiat currencies with the greenback as the world reserve currency – which is, well, subjective and psychological in a sense.

Let’s take an example. The rise in the U.S. national debt is fundamentally positive for gold, as it should weaken the trust in the greenback. But the level of trust in the government differs over time and geographically – traders tend to trust the Uncle Sam or Japan even if they hold higher debts than Argentina. A lot also depends on the broader macroeconomic context and the general sentiment: in one year, investors can shrug off all negative news about the debt bubble, just to panic a few months later.

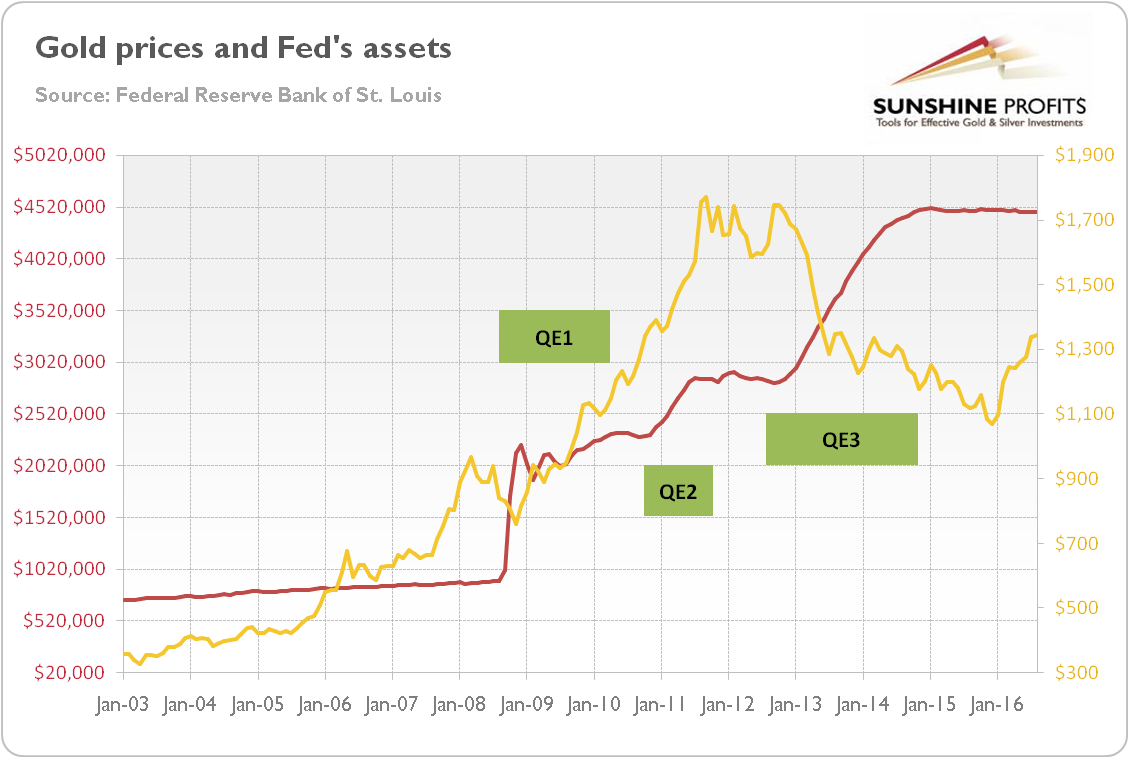

Remember quantitative easing? Gold soared after the first two rounds, but dropped after the third one, as one can see in the chart below. Why? Sentiment changed, as the confidence in the Fed and the U.S. economy returned. Again, it doesn’t mean that fundamentals don’t matter. The QE3 was indeed fundamentally negative for gold, but others factors were also in play – and they outweighed the QE3.

Chart 1: The price of gold (London P.M. Fix, yellow line, right axis) and the Fed’s assets (red line, left axis, in billions of $) from 2003 to 2016.

The bottom line is that gold behaves like a currency. So the gold investing is more like the pricing game, not the value game. There are no cash flows, while industrial use is minuscule – hence, we cannot determine the intrinsic value of gold, but we can try to guess the future price direction. It is affected by the market sentiment – but investors shouldn’t fall into nihilism, according to which fundamentals don’t matter for the precious metals market. The market sentiment doesn’t switch out of nothing, but it depends eventually on the changes in objective reality and fundamental drivers. On the other hand, the above observations make it crystal clear that the analysis of sentiment and tools that serve this purpose: technical analysis, cycles, self-similar patterns and so on, is clearly justified from the fundamental point of view.

If you enjoyed the above analysis and would you like to know more about the gold’s nature and our philosophy of investing, we invite you to read the April Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign me up!

Thank you.

Arkadiusz Sieron, Ph.D.

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview