Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

The technical part of today’s analysis is going to be brief, as what happened yesterday simply confirmed what I wrote in yesterday’s analysis, and at the same time not enough changed for this analysis to require a follow-up. And points made in the previous analyses, for example in Monday’s flagship issue, remain up-to-date as well.

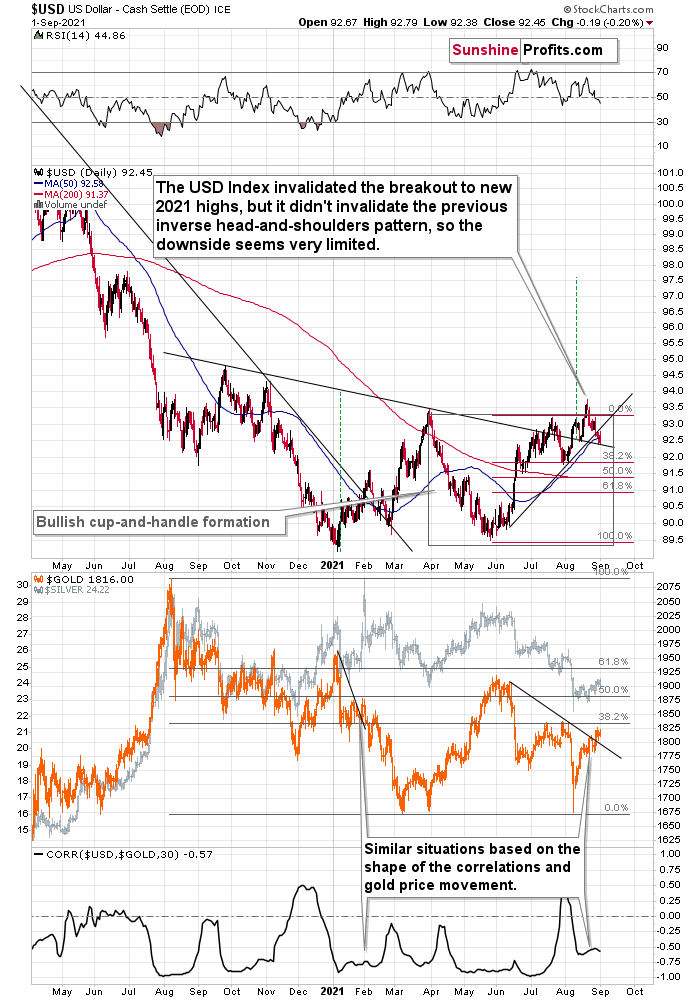

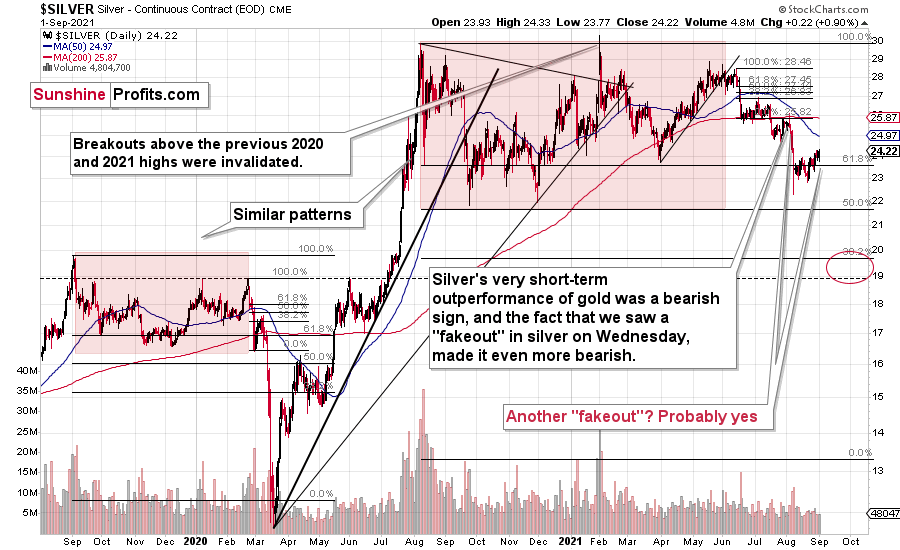

I previously wrote that the USD Index touched the neck level of its previously completed inverse head and shoulders pattern, and yesterday (Sept. 1) it simply touched this level again.

The only difference was that this time, the USDX closed at lower levels. This means that gold should have closed at higher levels – that’s if it was really starting a rally here.

Gold closed yesterday’s session $2.10 lower, which confirms the theory that this is not the start of a bigger rally, but rather the final part of a counter-trend upswing. As I discussed yesterday and on Tuesday, we might need to wait until after the U.S. Labor Day, before the decline really picks up pace.

And just as gold declined yesterday, so did mining stocks. Gold was down by 0.12% and miners were down by more than 0.6%. Miners magnified gold’s declines, which is normal for the end of a corrective upswing, and bearish.

Conversely, silver showed short-term strength.

The white metal even managed to close yesterday’s session above the previous 2021 lows. This seems bullish at first sight, but those of you who have been following my analyses for some time know that this is not bullish at all. Actually, I previously wrote that the move higher in silver is one of the things that we might see and that would not invalidate the bearish outlook.

Implications of short-term relative silver strength compared to gold are exactly the opposite – they are bearish, especially when gold miners are underperforming.

In fact, we saw the same thing before the previous major slide. In early August, silver rallied above its June lows just to decline shortly thereafter. Starting at its intraday August 4 high, silver declined by $3.81 in just three trading days. This time, we might need to wait for the U.S. Labor Day before the slide takes place, but it seems to be just around the corner.

All in all, the outlook for the precious metals sector remains very bearish for the following weeks, even though we might need to wait a few extra days for the big declines to follow.

Having said that, let’s take a look at the markets from a more fundamental point of view.

Less Is More

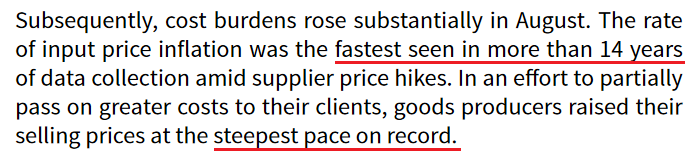

With the Delta variant upending global economic activity, the latest coronavirus strain has grinded the reopening momentum to a halt. And while the lack of “substantial further progress” allows the Fed (and other central banks) to air on the side of caution, the Delta variant has only accelerated the inflationary fervor. Case in point: IHS Markit released its U.S. manufacturing PMI on Sep. 1. And while the headline index declined from 63.4 in July to 61.1 in August, the print was labeled the “softest for four months, but nonetheless among the strongest seen in the over 14-year series history.”

More importantly, though, as “material shortages hampered output growth [and] supplier delivery times increased markedly to one of the greatest extents on record,” pricing pressures hit new all-time highs.

Please see below:

Source: IHS Markit

Source: IHS Markit

Moreover, while the Delta variant has depressed business sentiment, once the health crisis abates, renewed economic momentum should support a higher USD Index and higher U.S. Treasury yields. For context, Siân Jones, Senior Economist at IHS Markit, wrote:

“US goods producers continued to register marked upturns in output and new orders in August, as demand flourished once again. That said, constraints on production due to material shortages exerted further pressure on capacity as backlogs of work rose at a near-record rate.”

And while COVID-19 has made its presence felt, the report concluded with:

“Business confidence regarding the outlook for output over the coming year strengthened in August. Greater optimism was linked to hopes of further growth in client demand.”

Building on that theme, the Institute for Supply Management (ISM) also released its manufacturing PMI on Sep. 1. And here, the headline index increased from 59.5 in July to 59.9 in August. Moreover, “the New Orders Index registered 66.7 percent, increasing 1.8 percentage points from the July reading” and “the Backlog of Orders Index registered 68.2 percent, 3.2 percentage points higher than the July reading.”

Timothy R. Fiore, Chair of the ISM Manufacturing Business Survey Committee, wrote:

"Business Survey Committee panelists reported that their companies and suppliers continue to struggle at unprecedented levels to meet increasing demand. All segments of the manufacturing economy are impacted by record-long raw-materials lead times, continued shortages of critical basic materials, rising commodities prices and difficulties in transporting products. The new surges of COVID-19 are adding to pandemic-related issues — worker absenteeism, short-term shutdowns due to parts shortages, difficulties in filling open positions and overseas supply chain problems — that continue to limit manufacturing-growth potential. However, optimistic panel sentiment remained strong, with eight positive comments for every cautious comment.”

Likewise, while pricing pressures increased in August (though, at a slower pace), the report revealed that “16 of 18 industries reported paying increased prices for raw materials.”

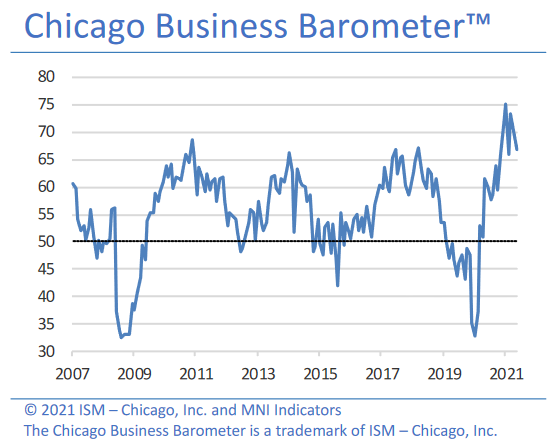

As for the regional surveys, the ISM released its Chicago Business Barometer on Aug. 31. And while the headline index decelerated month-over-month (MoM), “Order Backlogs climbed 11.6 points to 81.6, the highest reading since 1951” and “Supplier Deliveries shot up 6.3 points to a three-month high of 92.8, with one survey respondent reporting the worst delivery times in three years.”

Please see below:

Moreover, with excessive lead times accelerating the pricing pressures, inflation is showing no signs of slowing down:

Source: ISM Chicago Business Barometer

Source: ISM Chicago Business Barometer

Also sounding the inflationary alarm, the National Restaurant Association released its State of the Restaurant Industry report on Aug. 31. For context, the mid-year update covers key industry indicators and trends as of June/July through extensive surveys of restaurant operators and consumers.

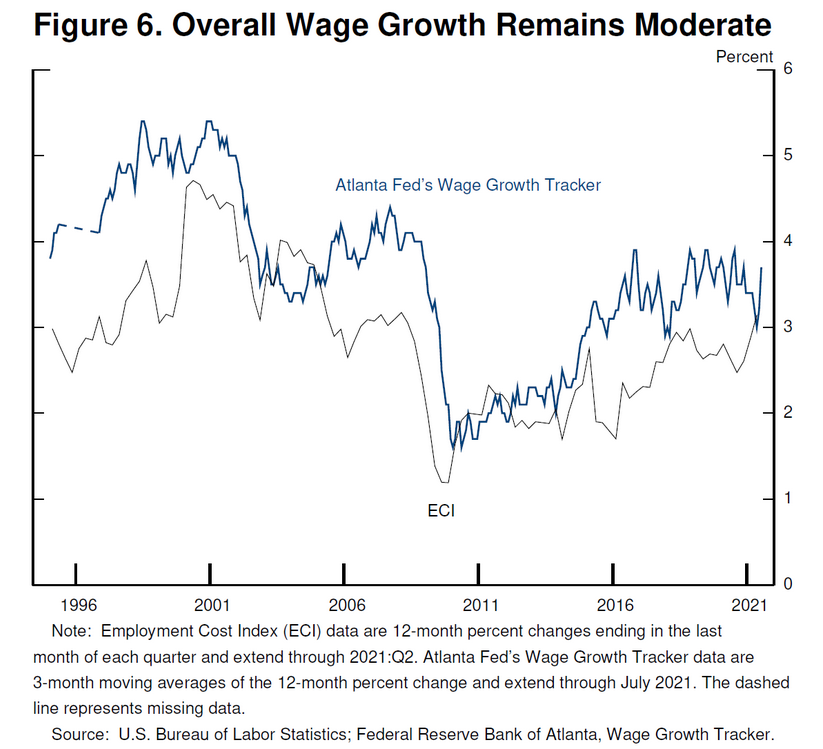

And while Fed Chairman Jerome Powell said at the Jackson Hole Economic Symposium on Aug. 27 that “we see little evidence of wage increases that might threaten excessive inflation,” the year-over-year (YoY) percentage increase in the Employment Cost Index (ECI) in the second quarter (3.55%) was the highest since 2002. For context, Powell actually cited the Atlanta Fed’s wage tracker and the ECI to support his conclusion.

Please see below:

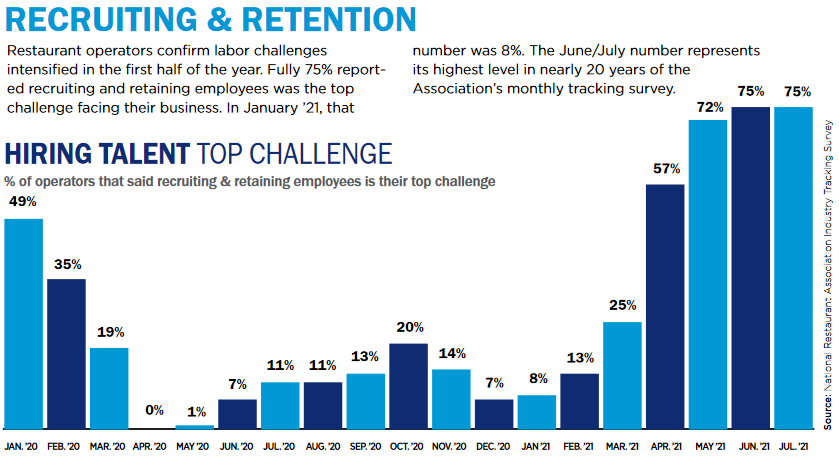

However, more representative of the current climate, average hourly earnings in the leisure & hospitality sector surged by 9.63% YoY on Aug 6. And with the National Restaurant Association revealing that “labor challenges intensified in the first half of the year” and that “75% [of respondents] reported recruiting and retaining employees was the top challenge facing their business,” wage inflation is poised to accelerate. For context, only 8% of respondents cited hiring as their “top challenge” in January but “the June/July number [75%] represents its highest level in nearly 20 years of the Association’s monthly tracking survey.”

Please see below:

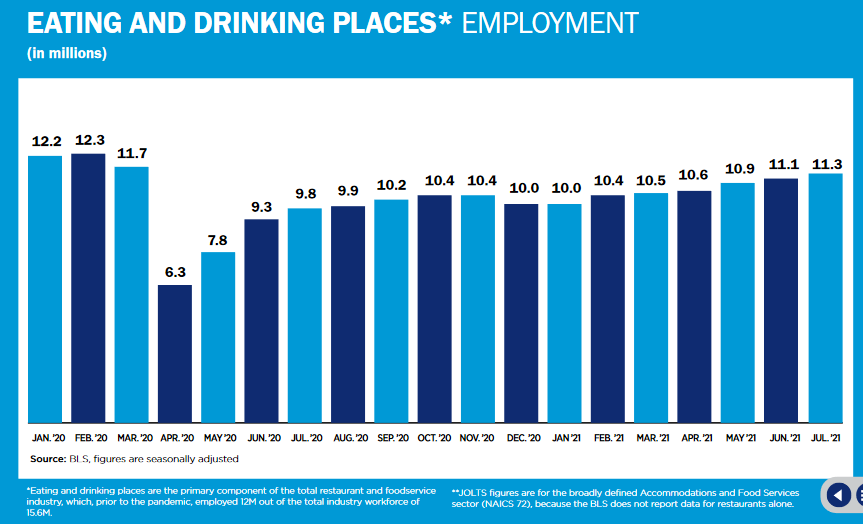

What’s more, with economics 101 and the supply/demand curve contradicting Powell’s position, staffing levels at restaurants are more than 8% below their pre-pandemic high of 12.3 million. And with the restaurants & accommodations sector home to more than 1.4 million job openings as of Jun. 30 (BLS data), the figure was more than double the January 2021 reading and was the highest since the data collection began in 2000. Thus, does it seem like wage inflation will moderate anytime soon?

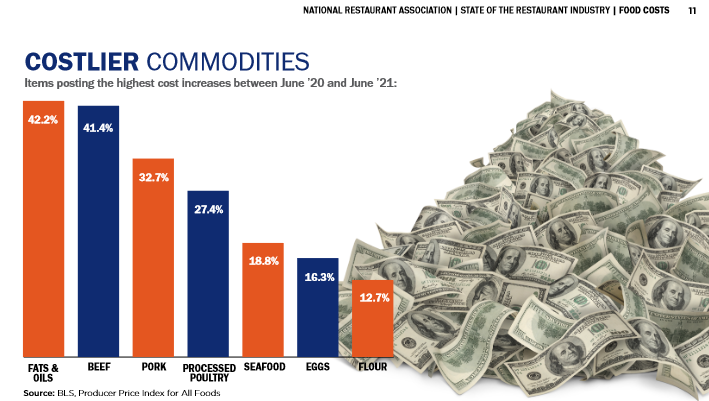

To that point, with input costs accelerating in conjunction with persistent wage inflation, restaurants are paying a hefty price to maintain operations.

And with the merry-go-round of cost-push inflation performing as expected, higher menu prices (the orange bars below) demonstrate how U.S. restaurants are not sitting idly by and watching their profit margins deteriorate.

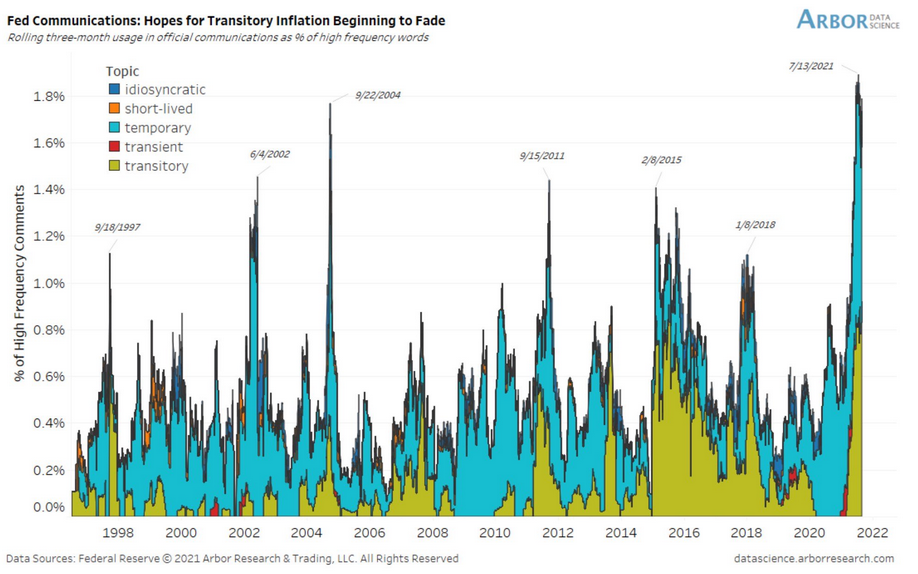

Furthermore, while Powell has parroted the “transitory” narrative on numerous occasions, Fed officials’ belief in his wisdom is starting to falter.

Please see below:

To explain, the color blocks above track Fed officials’ messaging of “transitory” and other words of a similar meaning. If you analyze the right side of the chart (though, it’s hard to make out), you can see that like-minded language peaked on Jul. 13 and has been moving lower ever since.

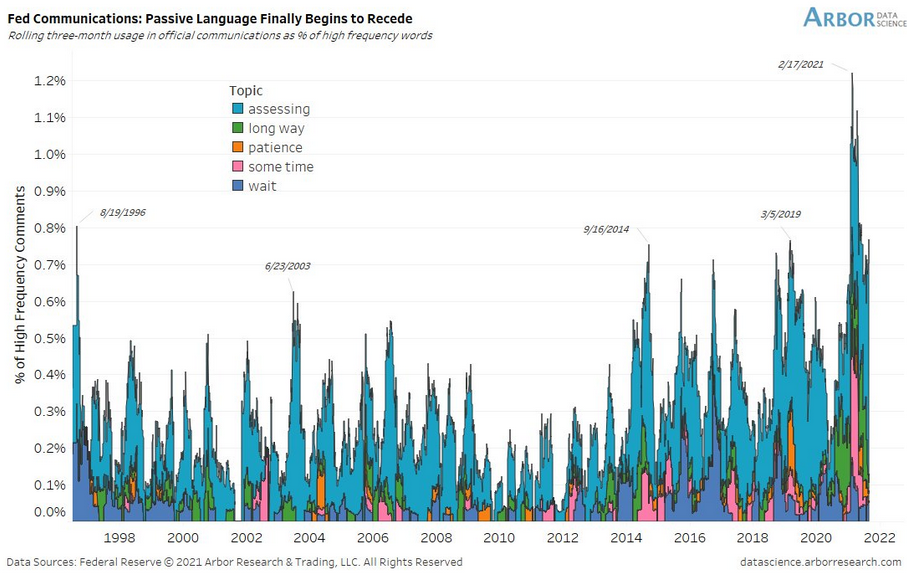

Similarly, Fed officials’ passive language has also moved sharply lower. And with terms like “patience,” “assessing” and “long way” being used increasingly infrequently, it signals that conflicting opinions and taper anxiety remain ripe within the Fed.

Please see below:

To explain, the color blocks above track Fed officials’ preference for dovish commentary. If you analyze the right side of the chart, you can see that the basket of terms has rolled over and the equilibrium has fallen to the more hawkish side of the coin.

The bottom line…

While the ADP’s private payrolls disappointed on Sep. 1 and U.S. nonfarm payrolls may follow suit on Sep. 3 due to the Delta variant (though, the ADP report and U.S. nonfarm payrolls have little to no correlation), taper momentum is still building. And with the USD Index and U.S. Treasury yields poised to benefit from the eventual announcement, precious metals investors are demonstrating heightened hesitation.

In conclusion, the PMs moved lower on Sep. 1 despite a weaker USD Index and mixed performance from U.S. Treasury yields. And with the latter’s fundamentals only obstructed by the Delta variant, progress on the health front should add to the former’s ills over the medium term. As a result, the seeds have been sown for another sharp decline in precious metals prices and it’s likely only a matter of time before the climax unfolds.

Overview of the Upcoming Part of the Decline

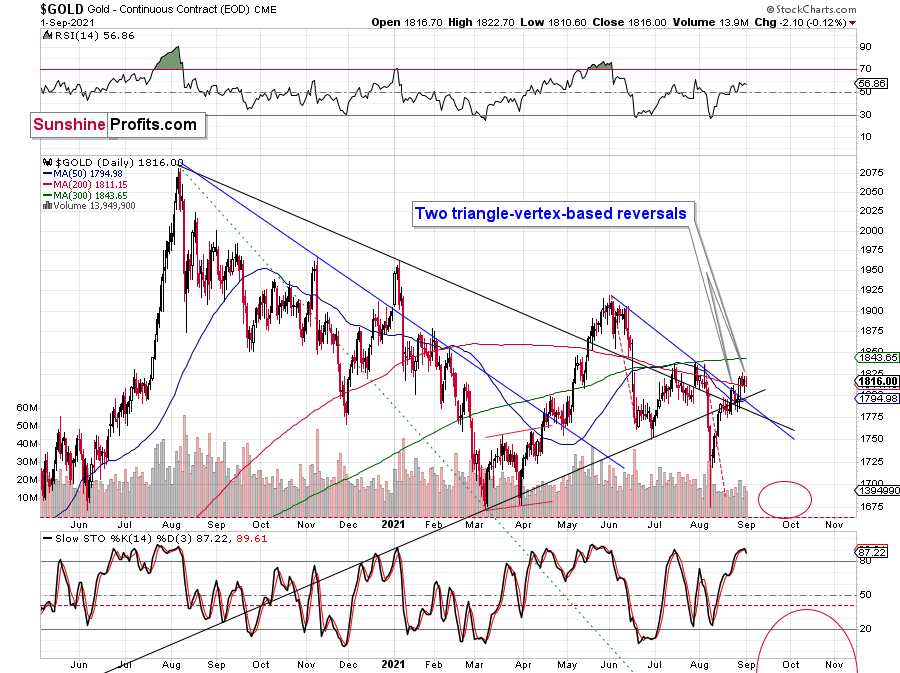

- It seems to me that the corrective upswing in gold is over or close to being over, and the big decline seems to be already underway.

- It seems that the first stop for gold will be close to its previous 2021 lows, slightly below $1,700. Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions when gold shows substantial strength relative to the USD Index while the latter is still rallying. This might take place with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This might also happen with gold close to $1,375, but it’s too early to say with certainty at this time. I expect the final bottom to take place near the end of the year, perhaps in mid-December.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

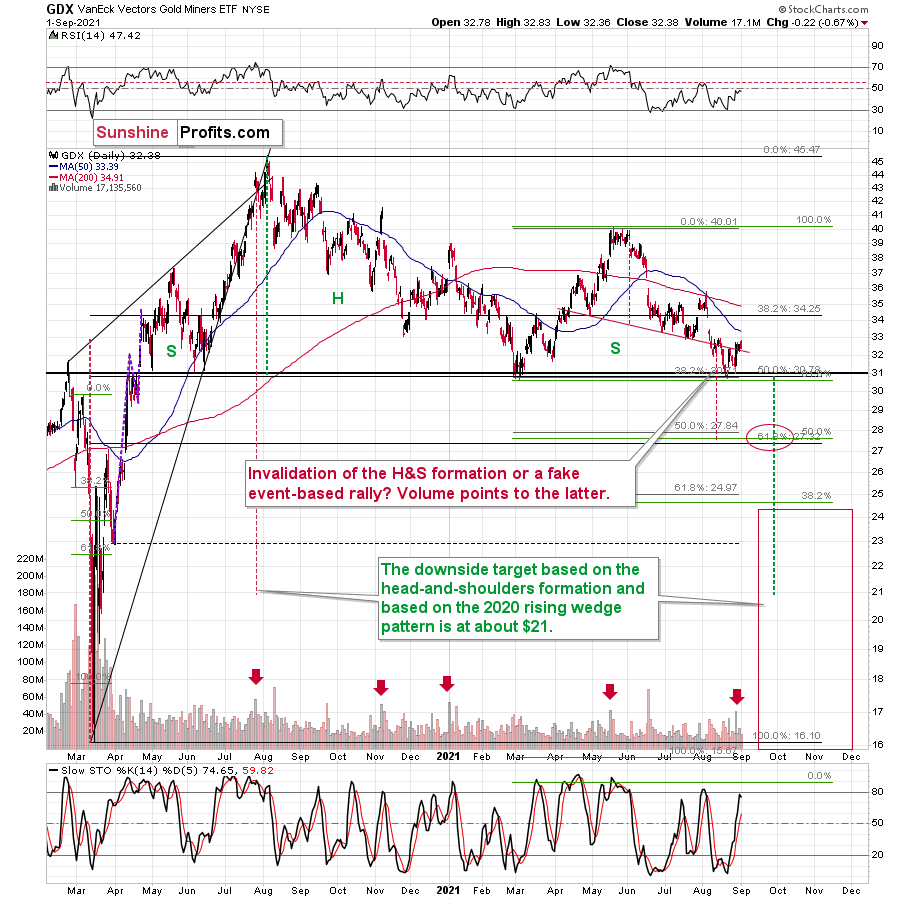

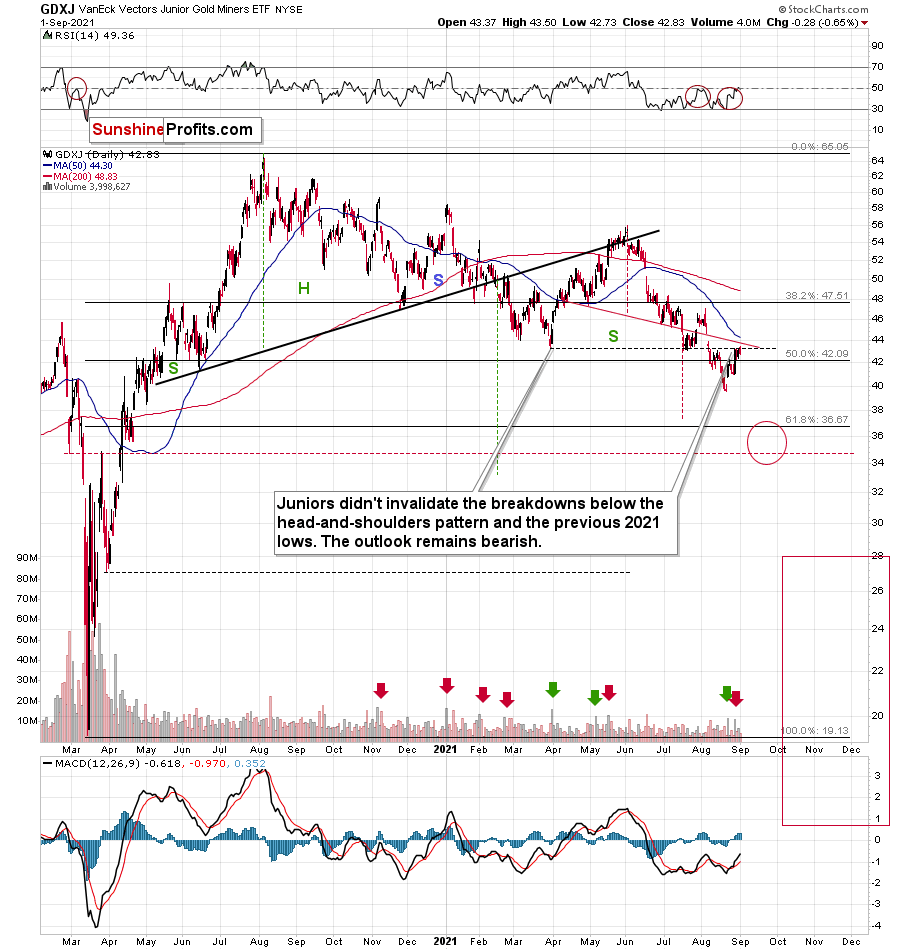

To summarize, even though we saw a sizable upswing on Friday (Aug. 27), it doesn’t seem that it changes anything with regard to the bearish medium-term trend on the precious metals market. The key breakdowns / breakdowns were either not invalidated (euro, USD Index, silver, GDXJ) or were invalidated in a way that’s suspicious / in tune with what happened during the powerful 2013 slide (GDX, HUI Index).

It seems that our profits from the short positions are going to become truly epic in the following weeks.

After the sell-off (that takes gold to about $1,350 - $1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently providing you with the possibility to extend your subscription by a year, two years or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over, and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $35.73; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $16.96; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $35.46; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,683

Gold futures upside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $11.38

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief