Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Many times in your life, you have probably observed or experienced the accuracy of the saying that while two dogs are fighting for a bone, a third runs away with it. It can be said that gold is taking advantage of a similar situation, and while the market, economy, and world of politics are slightly in turmoil, the yellow metal is slowly climbing.

As the dollar continued its consolidation on February 1, gold proudly hovered above the $1,800 mark. As you know, as long as the precious metals don’t space out, they can use the falling USDX to improve their performance. It so happened that, thanks to mixed signals from European and US financial authorities, which investors interpreted in their own way, the dollar basket suffered some losses. Yesterday I wrote:

Although the ECB seems extremely dovish, especially compared to the Fed, and inflation figures remain relatively low, the Eurozone’s currency enthusiasts are counting on some bold moves. The fervor of the euro bulls fazed the greenback, which, interestingly, was also the case in almost all similar situations last year.

Another demotivating factor for the USDX may have been the somewhat shy tone some Fed officials took on Monday about the withdrawal of economic aid in the face of rampant inflation. The general plans of the US federal reserve to raise interest rates in March have not changed though, so it turns out that some investors interpreted the signals in their own way and the optimism regarding both precious metals and the EUR/USD pair is temporary.

In fact, while the ECB will still have a chance to comment, so far, despite its dovish approach, the bank did not have to say or do anything special to strengthen the European currency in the EUR/USD pair, because the Fed got it covered. To the delight of the euro – and probably gold – bulls, the Federal Reserve’s officials did not speak in unison on Monday, when commenting on monetary policy plans.

Of course, it is known that the Fed continues its hawkish tactic and intends to fight inflation with a heavy weapon, which will be raising interest rates. The fact that the first step in a monetary tightening will be taken in March is already taken for granted. However, when the Federal Reserve announced a week ago that it was planning to raise interest rates earlier – and possibly more aggressively – than expected just several months ago, now the choir began to sing unevenly.

Some of the Fed’s members suggested that future rate hikes were likely to be data-driven and not necessarily automatic. In addition, apart from the fact that it is not known how much the first raise will be, the pursuit of neutrality was mentioned. Some views on what the Fed should do after the initial rate hike, shared on Monday, became a source of volatility. Among other things, the interpretation of such uncertain statements helped raise the price of gold.

In addition to the above, there is another factor supporting yellow metal stocks.

Russia Breaks the Silence

After several weeks of absence from public life, during which fears were mounting in Western capitals that Russia was preparing an invasion of Ukraine, President Vladimir Putin broke his silence. During a press conference in the Kremlin, Putin told reporters that he was not satisfied with the US response to Russian demands. Previously, Russia demanded that NATO withdraw its troops and infrastructure from Eastern Europe, claiming that the alliance would never accept Ukraine. He also presented a potential scenario suggesting that if Ukraine is admitted to NATO, there may be a conflict over the Crimea.

In his first public comments on the crisis in Ukraine that has worsened since December, the Russian leader accused the US of ignoring Russian security proposals and of using Ukraine as a tool to obstruct Russia's actions.

Although Putin has said he is ready to enter into dialogue with the West, at the same time, Russia continues to deploy thousands of troops and weapons on the border with Ukraine, according to the world's media. Both President Joe Biden and US Secretary of State Antony Blinken consider Putin to be unpredictable. As Blinken told the press, the authorities are not sure whether the Russian leader has already made a decision about his next move and what it is, so they must be prepared for different results.

Ukraine does not remain indebted. The country has announced that it intends to increase its armed forces, as many European leaders have pledged to support it in the current stalemate with Russia. According to the media, tensions between Ukraine and Russia have not subsided.

The improvement in gold's position was due to similar news in mid-January. However, at the time, I wrote that such rallies were insignificant, and that it was specific military actions, rather than rumors of tension and deterioration in the geopolitical situation, that could lead to a real breakthrough in the market.

Later in the text, I will also explain other reasons why the optimism of precious metals is likely to turn out to be temporary and turn into pessimism in the medium term.

A Value Trap

While the USD Index declined again on Feb. 1, the pullback is more of a corrective downswing within a medium-term uptrend. For example, stock market optimism often results in bids for 'risk-on' currencies. With the dollar outperforming in recent weeks, investors' see 'value' in currencies like the euro and the CAD.

However, they're more of a value trap. The USD Index remains in an uptrend, and the dollar basket also rallied after approaching its 50-day moving average on Feb. 1. As a result, the recent consolidation is a normal occurrence, and there isn't much cause for concern.

Similarly, while mining stocks attempt to retrace some of their recent losses, the general stock market has helped uplift their performance. However, their idiosyncratic technical and fundamental outlooks remain bearish. As such, the short-term support from the S&P 500 should dissipate sooner rather than later. For context, I wrote previously:

Once one realizes that GDXJ is more correlated with the general stock market than GDX is, GDXJ should be showing strength here. If stocks don’t decline, GDXJ is likely to underperform by just a bit, but when (not if) stocks slide, GDXJ is likely to plunge visibly more than GDX.

Having said that, let's take a look at the situation from a fundamental point of view.

Digging a Deeper Hole

While the PMs remain relatively upbeat, their fundamental outlooks continue to worsen. For example, with the Fed now fighting inflation, rate hikes should commence in the coming months. However, in the meantime, the ground is already shifting beneath the PMs’ feet.

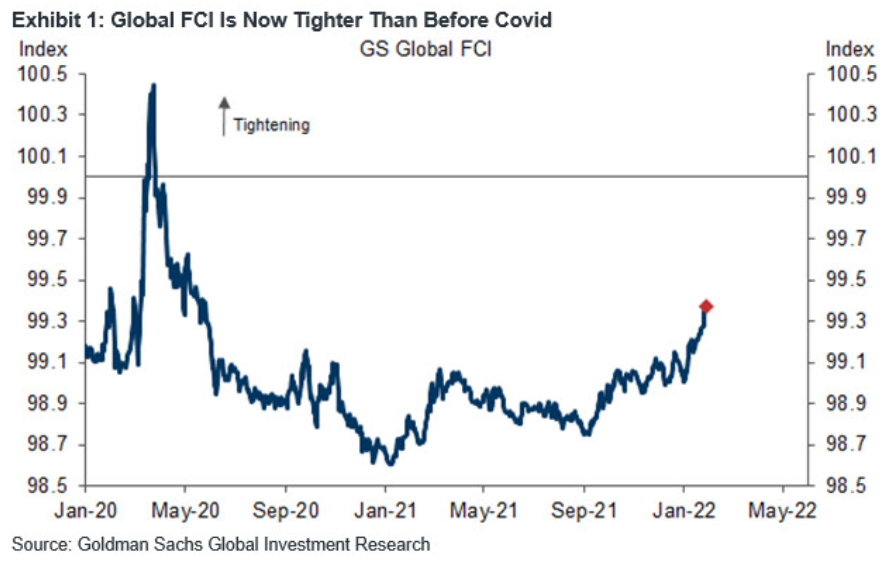

Please see below:

To explain, the blue line above tracks Goldman Sachs' Financial Conditions Index (FCI). For context, the index is calculated as a "weighted average of riskless interest rates, the exchange rate, equity valuations, and credit spreads, with weights that correspond to the direct impact of each variable on GDP." In a nutshell: when interest rates increase alongside credit spreads, it's more expensive to borrow money and financial conditions tighten.

To that point, if you analyze the right side of the chart, you can see that the FCI has surpassed its pre-COVID-19 high (January 2020). Moreover, the FCI bottomed in January 2021 and has been seeking higher ground ever since. In the process, it's no coincidence that the PMs have suffered mightily since January 2021. To that point, with the Fed poised to raise interest rates at its March monetary policy meeting, the FCI should continue its ascent. As a result, the PMs' relief rallies should fall flat, like in 2021.

Likewise, while the USD Index has come down from its recent high, it's no coincidence that the dollar basket bottomed with the FCI in January 2021 and hit a new high with the FCI in January 2022. Thus, while the recent consolidation may seem troubling, the medium-term fundamentals supporting the greenback remain robust.

Furthermore, Fed hawks remain focused on inflation, and while investors' positioning may seem contradictory, Fed officials' transition from hawkish rhetoric to hawkish policy should help the USD Index surpass 98 in the coming months.

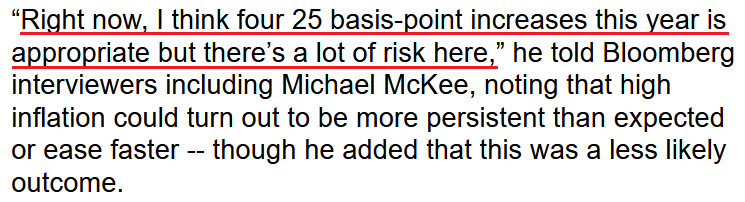

To explain, Philadelphia Fed President Patrick Harker told Bloomberg on Feb. 1 that a 50 basis point rate hike in March shouldn't be expected. For context, the prospect was always unrealistic. However, investors seemed to buy into the notion for a short time. He said:

“I would be supportive of a 25 basis-point increase in March. Could we do 50? Yeah. Should we? Well, I’m a little less convinced of that right now. But we’ll see how the data turn out in the next couple of weeks.”

However, Harker still expects four rate hikes for 2022, as long as inflation remains elevated.

Please see below:

Source: Bloomberg

Source: Bloomberg

Moreover, it’s important to remember that Fed Chairman Jerome Powell uses his deputies to deliver monetary messages. For example, during his Dec. 15 press conference, Powell was asked if he postponed his “hawkish policy stance” until after he was reappointed for a second term. I wrote about his response on Dec. 16:

As one of the most important quotes of the press conference, Powell admitted:

“My colleagues were out talking about a faster taper and that doesn’t happen by accident. They were out talking about a faster taper before the president made his decision. So it’s a decision that effectively was more than entrained.”

And while Powell sounded a little rattled during the exchange, his slip highlights the importance of Fed officials’ hawkish rhetoric. Essentially, when Clarida, Waller, Bostic, Bullard, etc., are making the hawkish rounds, “that doesn’t happen by accident.” As such, it’s an admission that his understudies serve as messengers for pre-determined policy decisions.

To that point, a chorus of Fed officials reiterated their hawkish expectations over the last two days, and, as Powell said, “that doesn’t happen by accident.”

San Francisco Fed President Mary Daly said:

“We definitely are poised for a March increase. But after that, I want to see what the data brings us.”

Richmond Fed President Thomas Barkin said:

“I'd like us to be better positioned. Better positioned is somewhere closer to neutral, certainly, than we are now and I think the pace of that just depends on the pace of inflation."

Atlanta Fed President Raphael Bostic said:

“When I started looking at this year, I had three moves or three rate increases in mind. And March increasingly was looking like it's the right time to do that.”

Kansas City Fed President Esther George said:

“It is in no one's interest to try to upset the economy with unexpected adjustments. I do think the Federal Reserve is going to have to move deliberately in its decisions to begin to withdraw accommodation."

St. Louis Fed President James Bullard said:

“We are cognizant of the inflation issue, we’re moving on the policy rate, but we’re also going to move on the balance sheet so we’re not that far from reaching neutral if you are willing to consider both of those.”

Thus, it’s clear that the Fed is on autopilot. In contrast, the ECB hasn’t achieved its rate hike criteria. Thus, while the EUR/USD’s recent rally hurts the USD Index, should we be concerned? To explain, I wrote on Feb. 1:

While the USD Index may come under pressure this week, it’s the same old story: euro bulls bid up the EUR/USD in hopes that the ECB will say or do something hawkish. And in the process, dollar weakness spreads to other currency pairs, and the USD Index suffers. However, once the short-term sentiment highs dissipate, the fundamentals reign supreme. And with the Fed all but certain to raise interest rates in March and the ECB poised to disappoint once again, the EUR/USD’s downtrend should continue over the medium term.

All in all, it’s important not to overreact to short-term fluctuations. While it seems like the USD Index has fallen out of favor and the PMs are back in investors’ good graces, the reality is that other currencies bounced off of relatively oversold levels, and positioning shifts occurred. However, the USD Index suffered several countertrend declines in 2021. As a result, the recent weakness is far from a regime change, and its robust fundamentals should rule the day over the medium term.

Finally, since Fed officials’ hawkish forecasts depend on the direction of inflation and the U.S. economy, the outlook for both remains resilient. For context, the Omicron variant will likely depress Q1 GDP growth. However, I noted on Jan. 31 that warmer weather should shift the narrative. I wrote:

The U.S. economy is growing well ahead of its pre-pandemic trend. Moreover, while disruptions from the Omicron variant will likely slow growth in Q1, the outbreak should calm down when warmer weather arrives. With the season also allowing for patio dining, camping trips, and other outdoor activities that support economic growth, Q1’s weakness should be short-lived.

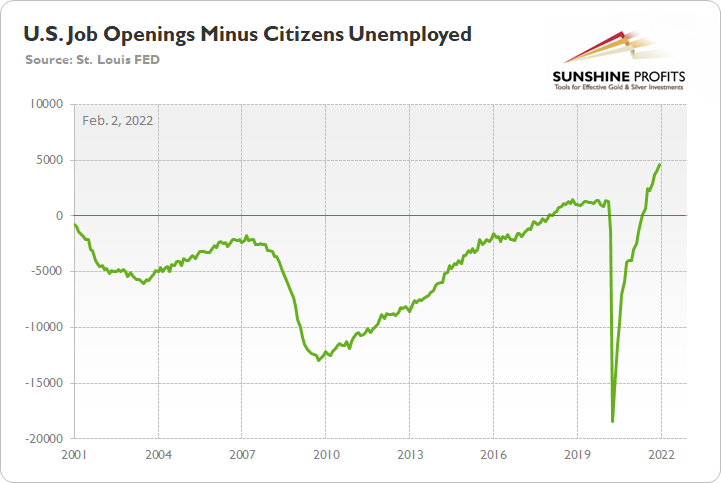

Supporting the thesis, the U.S. Bureau of Labor Statistics (BLS) revealed on Feb. 1 that U.S. job openings came in at 10.925 million, well ahead of the 10.300 million expected. Moreover, there are now 4.606 million more job openings in the U.S. than unemployed citizens.

Please see below:

To explain, the green line above subtracts the number of unemployed U.S. citizens from the number of U.S. job openings. If you analyze the right side of the chart, you can see that the epic collapse has completely reversed and the green line is now at an all-time high. Thus, with more jobs available than people looking for work, the economic environment supports normalization by the Fed.

The bottom line? While short-term price moves may seem material, false narratives are built on foundations of sand. While several castles crumbled in 2021, prophecies of the dollar’s demise have risen once again. However, with the fundamentals signaling more dollar strength over the medium term, it’s likely only a matter of time before the USD Index’s bullish ascent continues.

In conclusion, the PMs rallied on Feb. 1 and the USD Index continued its consolidation. However, with financial conditions already tight and poised to tighten further, the pullback lacks fundamental credibility. Moreover, with the U.S. economy still on solid ground, the Fed has little reason to perform a dovish 180. As a result, the PMs’ optimism should turn to pessimism over the medium term.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over or close to being over, and that gold, silver, and mining stocks are now likely to continue their medium-term decline.

- It seems that the first (bigger) stop for gold will be close to its previous 2021 lows, slightly below $1,700. Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,375, but at the moment it’s too early to say with certainty.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Administrative Info for This Week

I – PR – will be traveling this week, which means that the analyses will take a slightly different shape.

Regular analyses will include only the fundamental parts of the analyses, and while the technical details will not be posted regularly, I’ll still be monitoring the markets for most days, and I’ll send you intraday Alerts, if the situation requires it (in particular, if some extra changes are required in the trading or investment positions).

To be precise, the target levels presented in the “Trading capital” part below summary are “binding”, which means that if the price touches a given level, the trade should be executed (in my opinion, that is; it’s your capital, and you can do whatever you want with it) without waiting for my confirmation. I’m usually sending them for additional clarification, anyway, but this likely won’t be the case next week. In other words, if you haven’t placed an exit order on your trades, yet you’d like to apply the above suggestion, it might be a good idea to place those exit orders right away.

By “most days”, I mean that I know that there will be two days when I’ll have no access to any internet / electronics whatsoever, but I don’t know which days those will be. So, conservatively, I’ll provide you with a game-plan for the next week below. This way, my intraday comments are not that important as you’re up-to-date in advance, and if it’s necessary for me to provide you with an intraday update and I have the ability to do so, let’s treat it as an “extra value” that is not necessary (you’ll already be up-to-date because of the below details), but welcome. The gameplan is really an answer to the following question:

What to do next, if the exit levels are reached and the market then moves significantly?

Basically, there could be three scenarios in this case:

- If – after reaching the exit levels – the price moves back up significantly, then it would be a good idea to re-enter the short position in the GDXJ at $35.94 (at 300% of the size of the regular position, so the same size of the position that we have right now).

- If – after reaching the exit levels – the price moves lower significantly (in other words, it doesn’t bottom, but keeps falling), then I think it would be a good idea to re-enter the short position in the GDXJ at $31.47.

- If – after reaching the exit levels – the GDXJ price moves back-and-forth and/or doesn’t move to any of the prices in the previous points, then I think no additional action would be necessary.

The first scenario is positive (we gain more by re-entering short positions at higher prices), and the second scenario is negative (we gain less by re-entering short positions at lower prices). The third scenario is neutral.

The most likely outcome, in my view, is that the GDXJ ETF price will either not manage to get to the $34.63 target next week, or that it will manage to do so, and then it will rebound just a little or trade sideways (third scenario).

After all, let’s keep in mind that mining stocks tend to show strength before gold does, and things are not as volatile as they were in early 2020. This means that the short-term bottom is likely to be rather normal, meaning a situation where miners first show strength by declining just a little while gold declines more, then perhaps rally somewhat while gold doesn’t decline or declines just a little. It takes time for the above to take place.

Consequently, the most likely outcome, in my view, is that next week, the profits on the short position in the junior mining stocks will simply grow while we keep the positions intact.

All in all, you’re already equipped with the strategy for the next week, and the odds are that it won’t be necessary to take action, anyway.

Summary

Summing up, it seems to me that the corrective upswing is over, and that gold, silver, and mining stocks are now likely to continue their medium-term decline.

Please note that if mid-January rally was indeed based on supposedly increased tensions regarding Ukraine, then it’s likely that this rally is not going to be significant, and it might already be over. The “supposedly shocking” news already hit the market, and without any real follow-up (material) action, like Russian troops marching across the border with Ukraine, it seems that there’s nothing additional that markets could rally on. The market already “knows” that the tensions are very high and the chance for military conflict is high, regardless of whether that’s true or not. There’s not much more that can be said to increase that even further – only real action is likely to do it – and seeing such action is very unlikely in my view.

I continue to think that junior mining stocks are currently likely to decline the most out of all parts of the precious metals sector.

From the medium-term point of view, the key two long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

It seems that our profits from the short positions are going to become truly epic in the following months.

After the sell-off (that takes gold to about $1,350 - $1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $34.63; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $14.98; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $25.48; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $19.12

SLV profit-take exit price: $17.72

ZSL profit-take exit price: $38.28

Gold futures downside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $11.79

HZD.TO – alternative (Canadian) inverse 2x leveraged silver ETF – the upside profit-take exit price: $29.48

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief