Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Introduction

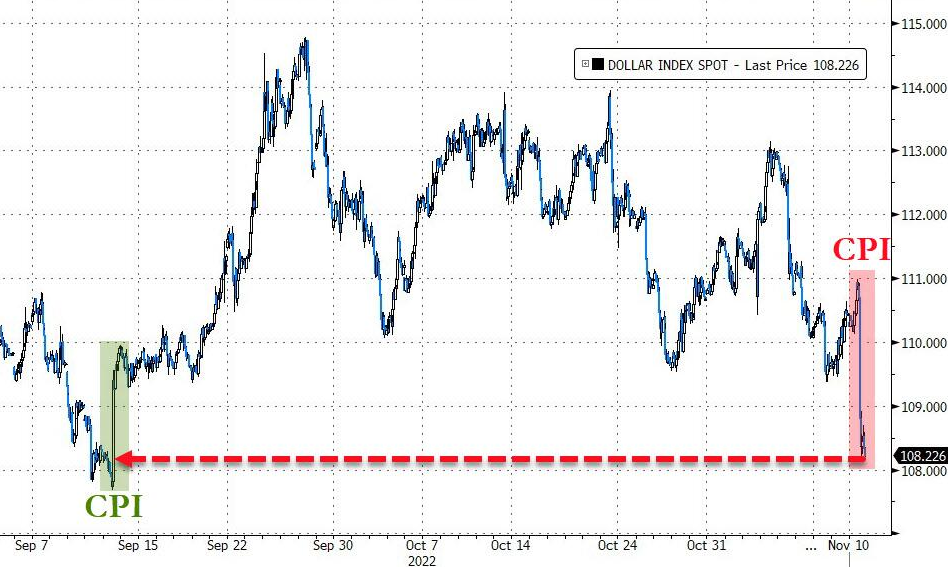

A calmer inflation print sparked panic buying on Nov. 10 - the S&P 500 soared by 5.54%. Moreover, with gold rallying by 2.33%, silver by 1.76%, the GDX ETF by 7.51% and the GDXJ ETF by 8.57%, the crowd assumes the worst is in the rearview. To that point, the USD Index fell by 2.14%, while the U.S. 10-Year real yield dropped by 27 basis points.

However, investors’ optimism is built on a faulty foundation, and a reversal of fortunes should occur sooner rather than later.

Old Habits Die Hard

With the Consumer Price Index (CPI) coming in weaker-than-expected on Nov. 10, short squeezes ran rampant and uplifted gold, silver, mining stocks and the S&P 500. For example, Goldman Sachs’ basket of the most-shorted stocks rallied by 10%, and the daily upswing was the third-largest since before the global financial crisis (GFC).

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the right side of the chart shows how the CPI release coincided with substantial short-covering and helped propel liquidity-fueled assets higher. As a result, while the price action seemed bullish on the surface, the main driver of the risk rally was an unwinding of bearish bets.

Likewise, with a cooler CPI supporting risk-on sentiment, the USD Index headed in the opposite direction.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the right side of the chart shows how the CPI release helped push the USD Index lower, as investors swapped the leaders for the laggards on Nov. 10. However, the price action was much more semblance than substance, and the bulls are missing the forest through the trees.

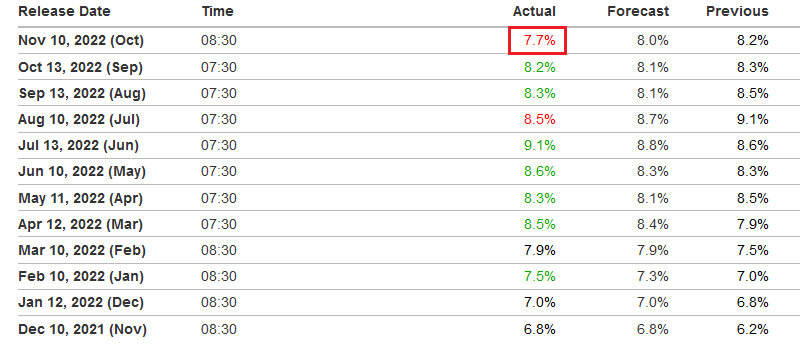

For starters, while the CPI missed the mark on Nov. 10, it was only the second time in the last 12 months that inflation underperformed expectations. Therefore, the crowd is way ahead of themselves here, and normalizing the metric to 2% is a challenge that’s far from priced in.

Please see below:

Source: Investing.com

Source: Investing.com

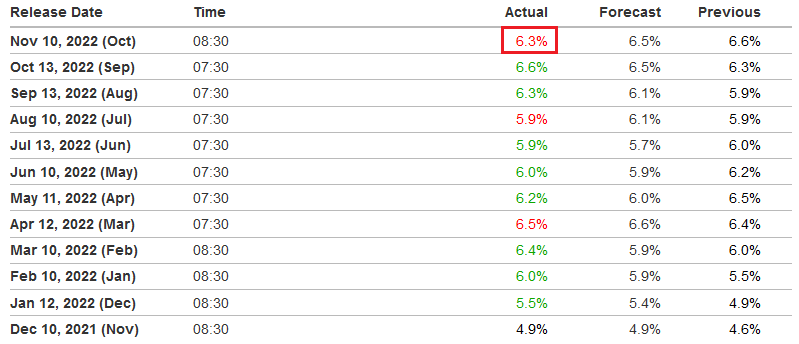

Second, the core CPI – which excludes the inflationary impact of food and energy – only missed the consensus estimate for the third time in the last 12 months. Moreover, the October figure is still higher than the results from April, May, June and July (released one month later). Thus, the exuberance on Wall Street materially contrasts the Fed's realized progress.

Please see below:

Source: Investing.com

Source: Investing.com

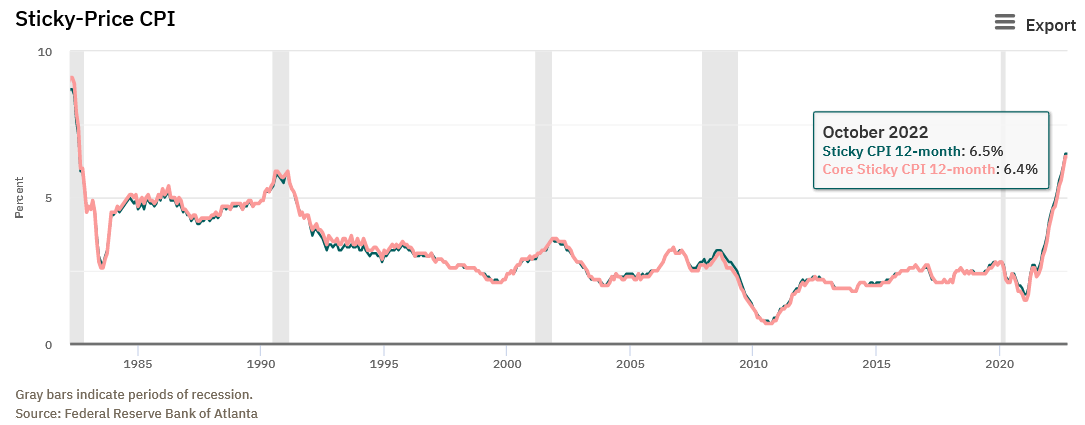

Third, while investors celebrated the CPI’s mild deceleration, they didn’t realize that the Atlanta Fed’s Sticky CPI’s remained at their 2022 highs.

Please see below:

To explain, the blue and pink lines above track the year-over-year (YoY) percentage changes in the Sticky and core Sticky (excluding food and energy) CPIs. If you analyze the right side of the chart, you can see that both metrics are at their highest levels since 1982.

For context, the Atlanta Fed highlighted the reliability of the Sticky CPI. Researches stated:

“The Sticky CPI is calculated from a subset of goods and services included in the CPI that change price relatively infrequently. Because these goods and services change price relatively infrequently, they are thought to incorporate expectations about future inflation to a greater degree than prices that change on a more frequent basis. One possible explanation for sticky prices could be the costs firms incur when changing price.”

Furthermore, the October 2022 readings of 6.5% and 6.4% match the peaks from September, so while inflation may seem like an old problem, investor sentiment is significantly out of touch with reality.

All in all, the price action on Nov. 10 was unkind to our GDXJ ETF short position. However, the recent rally is another example of hope overpowering reality. In the real world, normalizing inflation is challenging because it often plateaus or reverses higher when central banks show patience.

In addition, the headline CPI's 0.44% month-over-month (MoM) increase annualizes to 5.41%. Therefore, if the MoM pace continues at this rate, the headline CPI will still be ~2.7x higher than the Fed's 2% target.

As such, I noted on Nov. 7 that investors' lack of historical knowledge should be their undoing over the medium term. I wrote:

Bridgewater Associates is the largest hedge fund in the world, with more than $100 billion in assets under management (AUM). Co-CIO Bob Prince wrote on Oct. 11:

Going forward, the policy choices will be far more challenging when the goals of full employment and stable prices are at odds and the contraction in employment has not been sustained for long enough to bring down wage growth.

“For most central banks, at that stage there is a tendency to pause and see how things transpire. Such a pause tends to give markets a celebratory reprieve, producing a period of very good asset returns and a pickup in growth, both of which conspire to prevent wages and inflation from settling at the desired level, which necessitates the next round of tightening.”

Please see below:

Source: Bridgewater Associates

Source: Bridgewater Associates

Fed Officials Weigh In

With Fed officials behaving as Prince explained, attempts to balance inflation and growth have occurred throughout history. However, the lesson from those debacles is that when the Fed tries to create the perfect ending, it fails at both objectives. As a result, officials’ appetite for patience is normal but highly unlikely to prevent a recession.

On the dovish side, Kansas City Fed President Esther George said on Nov. 10:

“Without question, monetary policy must respond decisively to high inflation to avoid embedding expectations of future inflation. A more measured approach to rate increases may be particularly useful as policymakers judge the economy's response to higher rates….

“I continue to see several advantages for a steady and deliberate approach to raising the policy rate.”

Dallas Fed President Lorie Logan said on Nov. 10:

“I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving….This morning's CPI data were a welcome relief, but there is still a long way to go. Inflation is much too high.”

Philadelphia Fed President Patrick Harker said on Nov. 10:

“I am in the camp of wanting to get to what would clearly be a restrictive stance, somewhere north of four-ish, you know, 4.5%, and then I would be okay with taking a brief pause, seeing how things are moving; and then if we have to, we can continue to tighten.”

San Francisco Fed President Mary Daly said on Nov. 10:

“I would rather move [the U.S. federal funds rate (FFR)] a little bit higher and have to come back then to move a little bit less high and to then tell people we’re going to go higher, because at some point it does seep into inflation expectations.

“I don’t want to be over tightening to the point where we throw the economy into a sharp recession, but if we are talking about a rate hike on either side, I want to fully get inflation sustainably down to 2% on average.”

On the hawkish side, Cleveland Fed President Loretta Mester said on Nov. 10:

“Given that inflation has consistently proven to be more persistent than expected and there are significant costs of continued high inflation, I currently view the larger risks as coming from tightening too little….

“I believe monetary policy will need to become more restrictive and remain restrictive for a while in order to put inflation on a sustainable downward path to 2%.”

Minneapolis Fed President Neel Kashkari said on Nov. 9:

“I think we are on a good path right now: I think we are united in our commitment to getting inflation back down to 2%.... Any talk of a pivot is entirely premature.” The economy is a “long, long, long way” from the point where inflation and employment conflict.

So, while several Fed officials made the rounds, some preached caution while others were more forceful. However, the key point is that no one is talking about rate cuts, and a slower pace of rate hikes is not a pivot.

Remember, while Harker mentioned “a brief pause” near 4.5%, the rest either favored smaller rate increases or maintaining the current path. Therefore, while rate hikes of 25 and 50 basis points would have been considered materially hawkish in 2021, the recent string of 75 basis point increases make them seem relatively dovish.

However, their impact on the U.S. economy is the same, and the FFR’s peak is much more important than the pace at which it rises. As such, investors are attempting to manufacture a dovish pivot, and as Prince wrote, “there is a lot of room for markets to be blindsided” in the months ahead.

The Bottom Line

While investors celebrated the mild drop in the CPI, their willingness to assume that inflation will decline linearly should be their downfall. Throughout 2022, bear market rallies have uplifted gold, silver, mining stocks and the S&P 500 as uninformed narratives are powerful. However, their short shelf life has culminated with new lows once reality re-emerged. Thus, we expect a similar outcome over the medium term.

In conclusion, the PMs rallied on Nov. 10, as the ‘peak inflation’ crowd made another attempt at calling the bottom. Moreover, with the USD Index and U.S. Treasury yields declining sharply, the crowd believes a new bull market is on the horizon. However, the optimism is misguided, and the historical implications of how this all ends couldn’t be clearer.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

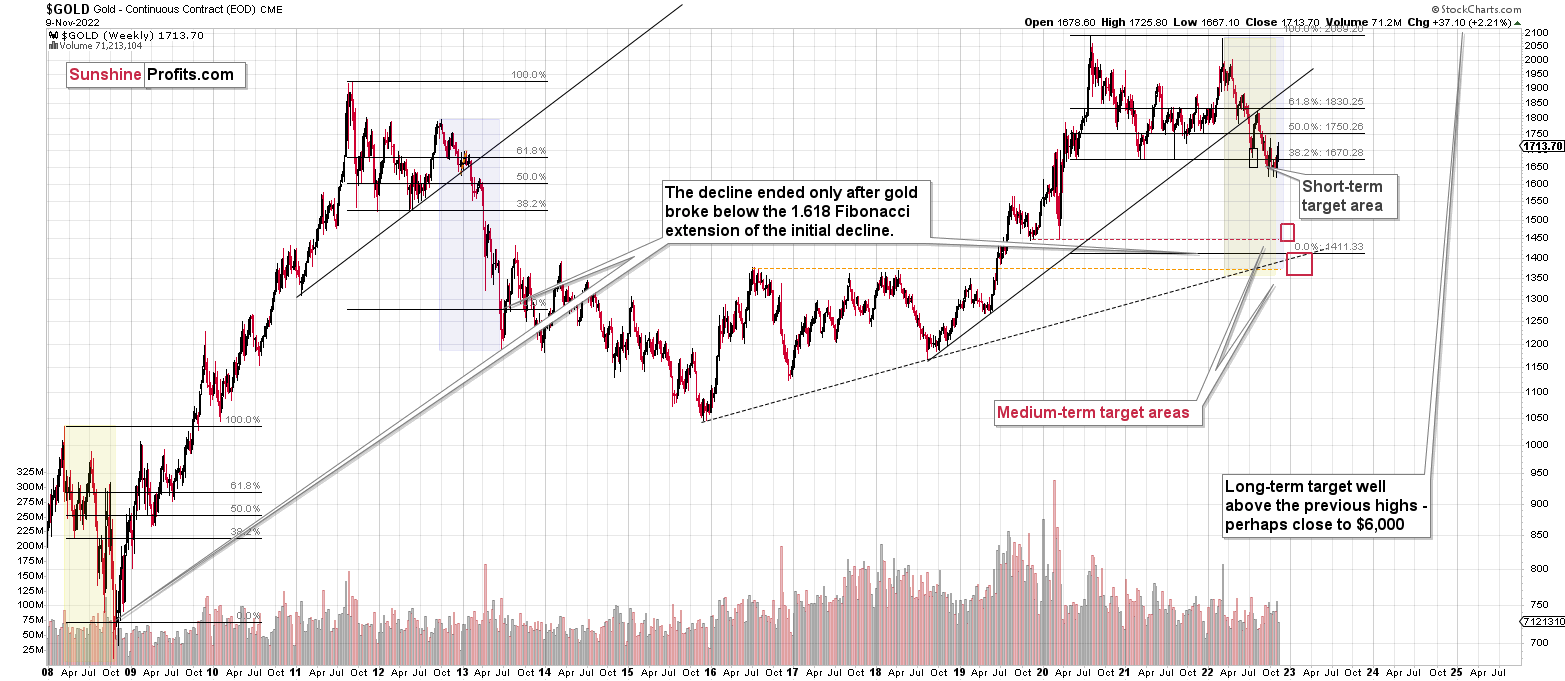

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, it seems that the biggest part of the 2013-like decline is taking place right now, and – while I can’t make any promises regarding performance - it seems likely to me that our big profits are about to become huge and then ridiculously big in the relatively near future.

As I have written before, the recent upswing didn’t change anything. While the mining stocks appeared “strong” recently, it seems to me that it’s just a reflection of the temporary (in my view) strength in the general stock market. And as stocks decline, mining stocks – and especially junior mining stocks – are likely to truly slide.

Things might happen very fast in the coming days, and if I plan to make any adjustments, I’ll keep you informed. Still, if the targets that I’m mentioning in the “Trading” part of the summary are reached, I think that profits should be taken off the table without an additional confirmation from me. I will probably get on the long side of the market at that time, but I’ll send a confirmation if I decide to do so.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $20.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $27.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $12.32

SLV profit-take exit price: $11.32

ZSL profit-take exit price: $74.87

Gold futures downside profit-take exit price: $1,504

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $18.47

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $46.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief