In the November edition of the Market Overview, we briefly discussed a Taylor rule, showing that adopting it would lead to significantly higher interest rates. But how goes that rule really work? It is worth analyzing it, as John Taylor, although not chosen as the next Fed Chair, may be still nominated into the Board of Governors and advocate for a more rule-based approach.

The Taylor rule can be expressed in the following equation:

Rfed = Rreal + Inf + 0.5 * (Inf - Inftarget) + 0.5 * (GDPreal - GDPpotential)

Rfed is the interest rate set by the central bank. Rreal is the assumed equilibrium real interest rate, Inf is the rate of inflation, Inftarget is the target inflation rate, GDPreal is real GDP, and GDPpotential is potential GDP, i.e. GDP corresponding with full employment. The result of subtraction of these two variables is called the output gap (expressed as y), which is the difference between the real and potential output. The formula may seem complicated, but assuming both a target rate of inflation and equilibrium of the real interest rate at 2 percent, we get a simplified form of the equation:

Rfed = 1.5 * Inf + 0.5 * y + 1

Thus, the Taylor rule is actually a simple recipe for interest-rate policy. When the economy is at full employment and price inflation is at the 2-percent target, then the central bank should set the interest rate at 4 percent. If the inflation rate increases (decreases) by 1 percentage point more, the central bank should raise (cut) the interest rates disproportionately by 1.5 percentage point to 5 percent (3 percent). If unemployment rises and the output gap falls to -1 percent, the central bank should lower the interest rate to 3.5 percent. As one can see, the central bank should be more worried about inflation than about the output gap (but it depends on the parameters used).

Although the formula is simple, the devil is in the details. First of all, the equation does not take into account other factors than inflation and output gap, such as the financial conditions (asset prices or the level of indebtedness, and so on). Hence, following the rule could make central bankers to neglect the risk of financial imbalances. If such risks materialize, gold – as a safe-haven asset – should shine.

There is also an important question as to which data should be used by the central bank: real-time data, revised data or projected data? The revised data should be better than the actual data, but this data is not available at the moment of decision. Actually, the projected data should be the best, as the central banks are interested in the future condition of the economy. But how should the central bank forecast inflation and the output gap?

It’s not so trivial question, as the inflation rate may be measured in different ways (CPI, core CPI, PPI, core PPI, PCEPI, core PCEPI, GDP deflator, etc.). And there is an even bigger problem with the output gap, as the potential GDP does not even exist (this why we call it “potential”). And what should be the equilibrium real interest rate? Taylor assumed it at a level of 2 percent, but the FOMC estimates it at just 0.75 percent. In such a case, the central bank should set the interest rate not at 4 percent, but at 2.75 percent at full employment and a 2-percent inflation rate.

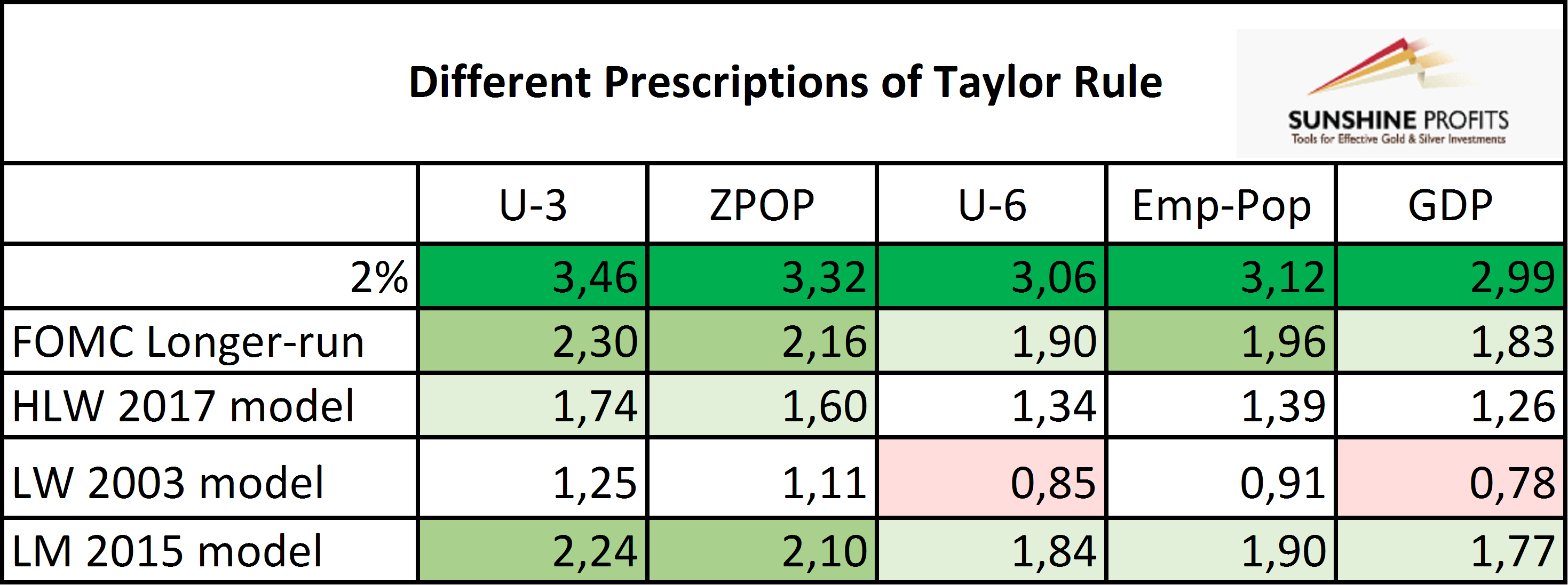

Our point is that there are actually numerous Taylor rules, such as the “lack of constant parameters and vagueness of variables imply that there is no single Taylor rule”. The implication is that by changing parameters and altering variables, we can generate various rules and different prescriptions for the monetary policy, as one can see in the table below.

Table 1: Different prescriptions of Taylor Rule depending on different measures of the output gap and equilibrium real interest rates for the third quarter of 2017.Source: Atlanta Fed.

Hence, the rule-based approach would not necessarily increase the predictability of the Fed’s policy. Actually, the rule-based approach would not really be based on automatic rules, free of discretionary policies, as the central bankers would have to choose a version of a rule and decide which one should be used. Similarly, even if your idea for gold investment comes down to investing for the long term, you are still responsible for making the decisions regarding diversification, rules for rebalancing (which can be critical), setting portfolio weights for individual assets / asset classes and possibly adjusting them. So, even if you plan to follow a rule, or a set of rules, you are still responsible for making sure these rules work in your favor. That’s the case with one’s investments and that’s the case with Fed’s monetary policy even if it’s to be rule-based.

The implication is that the introduction of the Taylor rule would not have to necessarily lead to a more hawkish monetary policy of the Fed, so the impact on the gold market would not have to be negative. Surely, interest rates should be higher under the basic version of the Taylor rule, but it would not be the case under different versions of the formula (as the table above shows, some versions of the Taylor Rule would actually imply lower interest rates in the previous quarter of 2017).

Hence, the markets’ view on the hawkishness of John Taylor – and on his bearish impact on the gold prices – is probably exaggerated. In practice, his imprint on the U.S. central bank would be more dovish than expected, as he would have to persuade the rest of the FOMC (especially since Powell is against a rule-based policy) to abide by the prescriptions of his original rule, according to which the interest rates should be much higher. Good luck with that, Mr. Taylor.

And the truth is that although the central banks, including the Fed, do not officially follow the Taylor rule, they look at it and take it into account in practice (inflation and output gap play a key role in the art of monetary policy). Hence, even if Taylor joins the FOMC, do not expect a hawkish revolution. Surely, the Fed is likely to shift towards the hawkish side, but not in a revolutionary manner. Gold may struggle in 2018, if the composition of the FOMC changes, but it will not be doomed.

If you enjoyed the above analysis and would you like to know more about the impact of changes in the Fed’s policy on the gold market, we invite you to read the December Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It's free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron, Ph.D.

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview