The indices hit record highs yet again to close off the first week of 2021 and weighed unrest, poor jobs data, and further prospects of economic stimulus.

News Recap

- Both the Dow and S&P 500 closed the week off with four-day win streaks. The Dow climbed 56.84 points, or 0.2%, at 31,097.97. The S&P 500 rose 0.6% to 3,824.68, and the Nasdaq popped 1% to 13,201.98. The small-cap Russell 2000 declined 0.25%.

- The Dow and S&P 500 each gained more than 1% on the week, while the Nasdaq gained 2.4%, and the Russell 2000 surged by nearly 6%. These gains to start the year came despite the unprecedented unrest and invasion of the Capitol by Trump supporters on Wednesday (Jan. 6).

- Despite Democrats winning full control of the Senate, the Dow briefly declined 200 points midday after moderate Democrat Senator Joe Manchin from West Virginia told The Washington Post that he would “absolutely not” support a round of $2,000 stimulus checks. Manchin mildly walked back those comments later in the day and said he was “undecided,” and not outright opposed to it.

- The U.S. economy lost 140,000 jobs in December, according to the Labor Department. This is significantly worse than the estimated gain of 50,000 according to economists polled by Dow Jones.

- The 10-year yield rose to its highest level since March 20, and broke above 1.1%.

- Coca-Cola (KO) rose 2.2% to lead the Dow higher. The consumer discretionary and real estate sectors each rose more than 1%, lifting the S&P 500. The Nasdaq got a boost from Tesla, which popped 7.8%.

The first week of 2021 largely continued where 2020 left off- with turmoil, tension, and a barrage of news. Another 2020 pattern continued to kick off the new year- a resilient market.

A week that started off with a sharp sell-off concluded with sharp weekly gains, all-time highs, and a four-day winning streak for the Dow and S&P 500. This is despite the first assault on the U.S. Capitol since 1814, despite COVID-19 cases continuing to wreak havoc, and despite a disastrous jobs report.

How could this be?

The results of the Georgia election can first and foremost be credited for the market surge.

Although tech initially plummeted due to fears of higher taxes and stricter regulations, with full Democrat control of the Presidency, Senate, and House, there is finally clarity and expectations of further spending and government stimulus.

Although President-elect Joe Biden had promised to pass a measure for bigger stimulus checks if Democrats secured control of the Senate, comments from West Virginia Senator Joe Manchin, a moderate Democrat, spooked investors for a time on Friday (Jan. 8). Although Manchin briefly walked these comments back, according to Bill Miller, founder of Miller Value Partners, “Nothing is going to get passed if they can’t get the moderates in the Democratic Party, or the Republican Party for that matter, to go along with (further stimulus).”

President-elect Biden said Friday (Jan. 8) that a new aid package would be “in the trillions of dollars.” This comes after Goldman Sachs stated that it expects another big stimulus package of around $600 billion. Value stocks and small-cap stocks have surged as a result of these prospects.

Despite the prospect of further stimulus that could heat up the economy, the short-term tug of war between good news and bad news will continue. Many of these moves upwards or downwards are based on emotion and sentiment, and there could be some serious volatility in the near-term. Although markets have kicked off the new year with excitement from the “Blue Wave”, consider this.

Stocks have overstretched valuations, the Capitol was invaded, the pandemic is out of control, and the vaccine roll-outs have been clunky at best.

Even though the markets saw a nice weekly gain to kick off 2021 and the 10-year treasury is at its highest level in months, a correction between now and the end of Q1 2020 is likely.

National Securities’ chief market strategist Art Hogan also believes that we could see a 5%-8% pullback as early as this month.

Generally, corrections are healthy, good for markets, and more common than most realize. Only twice in the last 38 years have we had years WITHOUT a correction (1995 and 2017). I believe we are long overdue for one. We haven’t seen a correction since March 2020. This is healthy market behavior and could be a very good buying opportunity for what I believe will be a great second half of the year.

While there will certainly be short-term bumps in the road, I love the outlook in the mid-term and long-term once the growing pains of rolling out vaccines stabilize. The pandemic is awful and the numbers are horrifying. But despite this, and despite the horrendous jobs report, there is one report released this past week that could be a step in the right direction - the ISM manufacturing data.

The consensus is that 2021 could be a strong year for stocks. According to a CNBC survey which polled more than 100 chief investment officers and portfolio managers, two-thirds of respondents said the Dow Jones will most likely finish 2021 at 35,000, while five percent also said that the index could climb to 40,000.

Therefore, to sum it up:

While there is long-term optimism, there are short-term concerns. A short-term correction between now and Q1 2021 is very possible. I don’t think that a correction above ~20% leading to a bear market will happen.

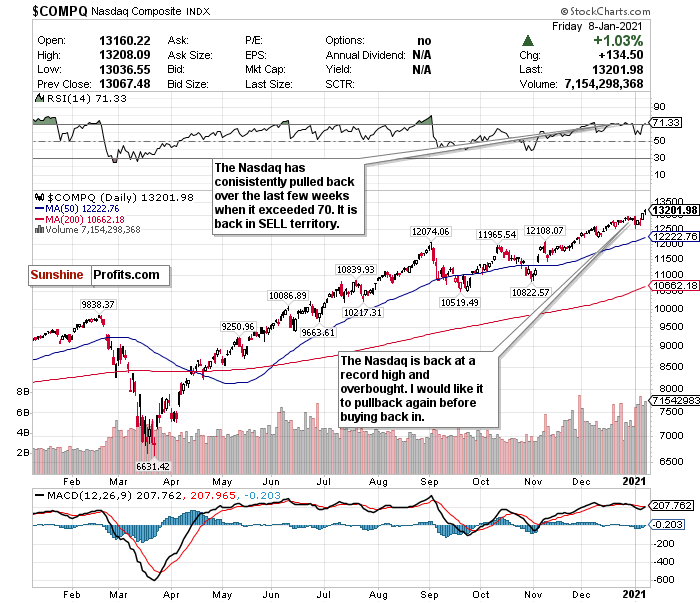

The Nasdaq’s RSI is Above 70 Again...You Know What That Means…

Figure 1 - Nasdaq Composite Index ($COMP)

I changed my short-term call on the Nasdaq to a HOLD on January 5. I liked the Nasdaq’s declines to start 2021, especially after overheating. The RSI was no longer overbought as well. The Nasdaq, however, is overbought once again. While an overbought RSI does not automatically mean a trend reversal, with the Nasdaq, always keep a close eye on this.

The Nasdaq pulled back on December 9th after it exceeded an RSI of 70, and briefly pulled back again after passing 70 again three weeks ago. We exceeded a 70 RSI again before the new year, and what happened on the first trading day of 2021? A decline of 1.47%. I think that another decline is imminent after the Nasdaq gained 2.4% on the week.

Tech can rally at any time and witness a plunge at any time. Truly, as with small-caps, the sector could move sideways before seeing a correction sooner rather than later.

Although there are also tailwinds for tech, they are specific to subsectors. Do what you can to research what subsectors of tech are most in-demand, and what subsectors are innovating, disrupting, and changing our world. While tech has overheated in the short-term, my optimism and bullish thoughts for 2021 have not changed. I hope the Nasdaq pulls back closer to its 50-day moving average for some quality long-term buying opportunities.

I have some concerns with the Democrats winning Senate control, and the potential consequences it could have for the sector. While it may not happen in 2021, a Democrat-controlled Congress could raise taxes and high growth companies. Further regulation for big tech companies could be imminent as well. Additionally, love him or hate him, the censorship of President Trump across social media platforms raises questions about what constitutes free speech and what is stepping over the line for censorship. Expect social media stocks to be hit hard in the near-term due to this controversy.

Tech has also overheated as it is, and there are signs of a bubble. Do not let anyone tell you “this time is different” if fears of the dot-com bubble are discussed. History repeats itself, especially in markets. I have many concerns about tech valuations and their astoundingly inflated levels. The recent IPOs of DoorDash (DASH) and AirBnB (ABNB) reflect this.

Because the RSI is back in SELL territory, I’m switching my call from HOLD back to SELL. But do not fully exit positions. Tech still has some upside. Remember that tech can also be very helpful to own on pessimistic days because of all the “stay-at-home” names.

Once the RSI drops to a minimum of 67, I’m switching back to HOLD. The Nasdaq is trading in a clear pattern.

For an ETF that attempts to directly correlate with the performance of the NASDAQ, the Invesco QQQ ETF (QQQ) is a good option.

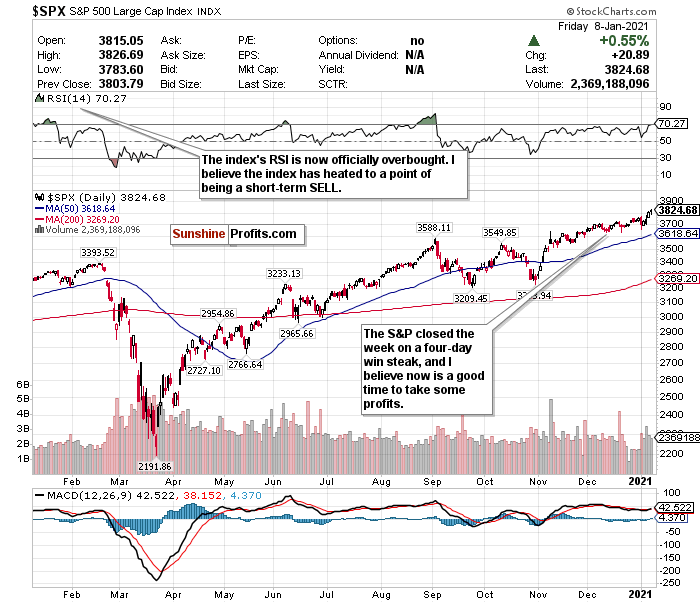

Despite Long-term Upside, the S&P 500 Has for Now Overheated

Figure 2 - S&P 500 Large Cap Index $SPX

The S&P 500 has been trading as a streaky index as of late and reflects the broader tug-of-war between good and bad news. The large-cap blue-chip index seemingly goes on multiple day winning streaks and losing streaks on a weekly basis. After beginning 2021 at a record high, the index saw its worst one-day sell-off since October on Monday (Jan. 4), and then went on a four-day win streak.

Judging by the RSI exceeding 70, and the way it has traded the last four sessions, more sell-offs could be on the horizon. While I always cheer stocks going up and hitting records, I also want buying opportunities. I would like to see this blue-chip large-cap index drop to around 3600 or below before making a BUY call for the long-term. For now, my near-term outlook is murky, I believe the index has overheated, and I am switching my call to a short-term SELL. As well, a short-term correction could inevitably occur by the end of Q1 2021. This is the perfect time to take profits, but do not fully exit positions.

While many analysts and strategists believe this short-term uncertainty is worth it for long-term potential, (and I tend to agree), I maintain that for now the index has overheated. I would like to see a sharp correction before initiating S&P exposure at a discount. There is clear upside for the second half of 2021. I would just prefer to maximize the upside if it’s possible to buy the ETF at a lower level.

Some analysts believe the S&P could have up to a 20% upside in 2021, while others caution against an overheating index. According to another survey of market strategists conducted by CNBC, a narrow majority believe that U.S. stocks will continue to rally into 2021, with the S&P 500 rising between 8% and 22% in 2021. This very well could be the case - but I suspect that most of this will happen in the next 6-12 months rather than 1-3 months.

For an ETF that attempts to directly correlate with the performance of the S&P, the SPDR S&P ETF (SPY) is a good option.

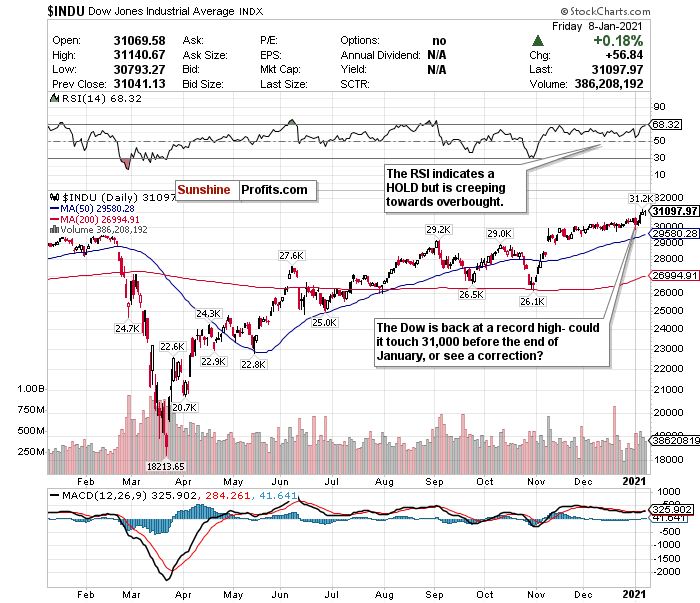

Does the Dow Approach 31,500 or 29,000 Before Mid-2021?

Figure 3

I’ve switched most of my calls for the indices to SELL calls due to what I think are irrational and overly excited moves higher to kick off the new year. I do not see the Dow being as overheated as much as the S&P, Nasdaq, or Russell.

Whenever I seemingly question if the Dow has more room to run towards record highs, it hits them. It defies logic, frankly. If the Dow can still hit all-time highs despite the Capitol building being invaded by hooligans, then what can stop the index?

Be that as it may, I still have many short-term questions for the Dow Jones, and believe it is just as likely to touch 29,000 as it is 31,500 before March. After trading as low as around 29,650 at one point before the new year (Dec. 21), the Dow has remained firmly above 30,000 for weeks and is now above 31,000.

Yet despite some long-term optimism, for now, my short-term questions take precedence. I don’t like how COVID-19 is trending (who does?), I am disappointed in the vaccine roll-out, and I am concerned about short-term economic headwinds.

While a 35,000 call to close out 2021 is a bit aggressive, I think that the second half of 2021 could show robust gains for the index.

With so much uncertainty and the RSI creeping towards overbought, the call on the Dow stays a HOLD. I am closely monitoring the RSI in the event that it exceeds 70.

This is a very challenging time to make a call on the Dow with conviction. But one thing I foresee is that if and when there is a drop in the index, it will not be strong and sharply relative to the gains since March 2020. It’s more likely than not that we will be in a sideways holding pattern until vaccines are available to the general public by mid-2021.

For an ETF that attempts to directly correlate with the performance of the Dow, the SPDR Dow Jones ETF (DIA) is a strong option.

Mid-Term/Long-Term

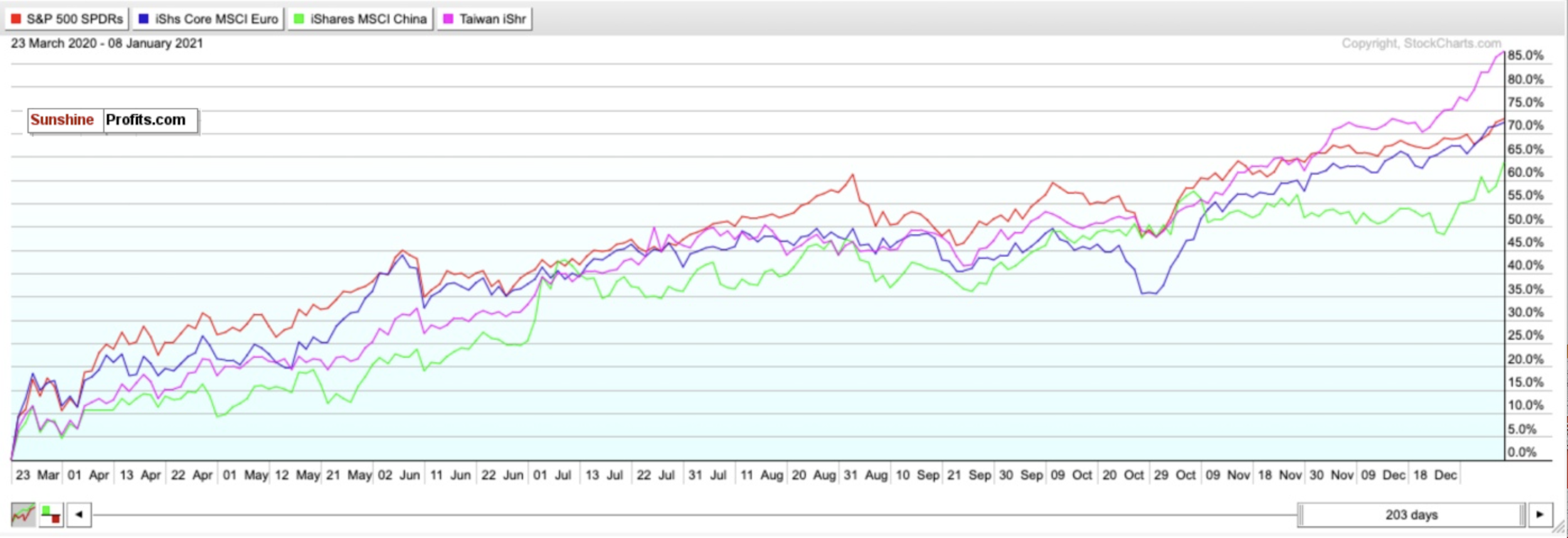

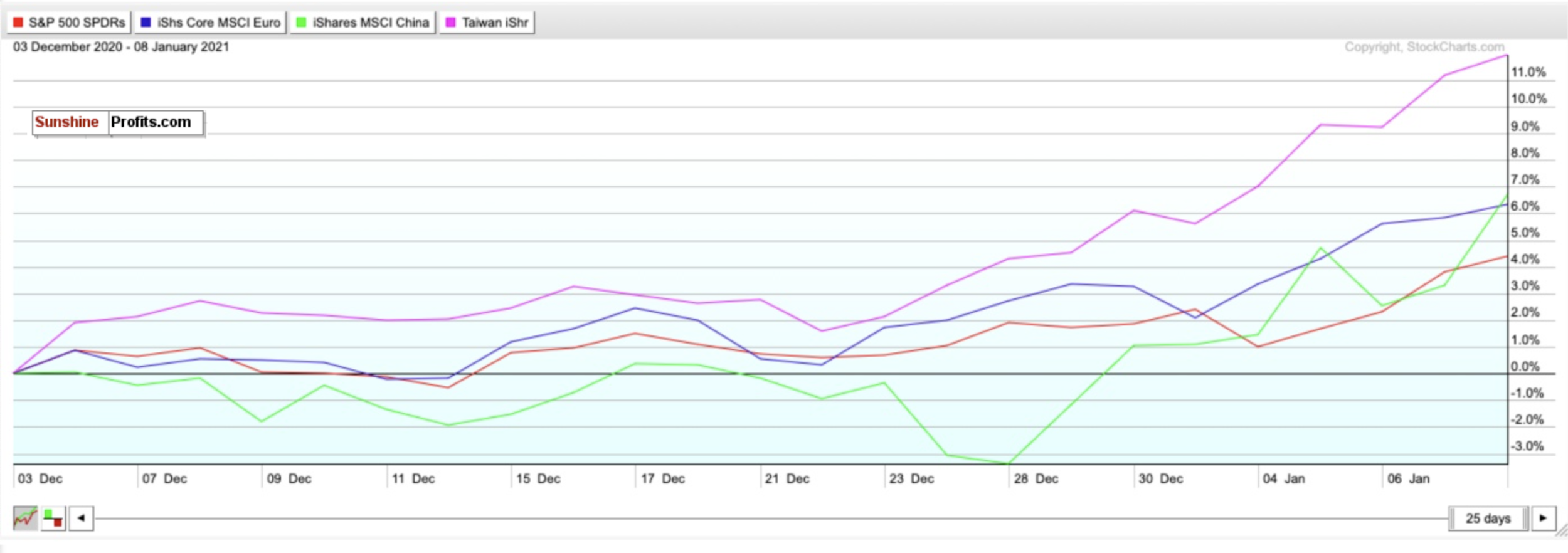

Taiwan and Others for Emerging Market Exposure - Not China

Figure 4

Although I am quite excited about emerging markets in both the medium-term and long-term, it is very country-specific.

China garners most of the attention as a so-called “emerging market.” But it is truly hard to consider it an emerging market any longer and has not been a top performer since markets bottomed on March 23rd. The country is not a top option for 2021 for international exposure. While China has regional upside, it also has geopolitical risks and has had its economic recovery baked-in.

Look at the Taiwan iShares ETF (EWT) as an alternative. Taiwan has outperformed China in the short-term, medium-term, and long-term.

As seen in the chart below, ever since I first called the Taiwan ETF (IWT) a BUY on December 3rd it has outperformed the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR).

The EWT has gained 11.97% while the MSCI China ETF (MCHI) has barely gained half of that. The Taiwan ETF has also outperformed the SPY S&P 500 ETF and the IEUR ETF which tracks Europe.

Figure 5

China may have handled the pandemic better than other countries and continues to demonstrate its ability to handle COVID-19’s economic shocks. But keep in mind that this is a regional victory, not just China.

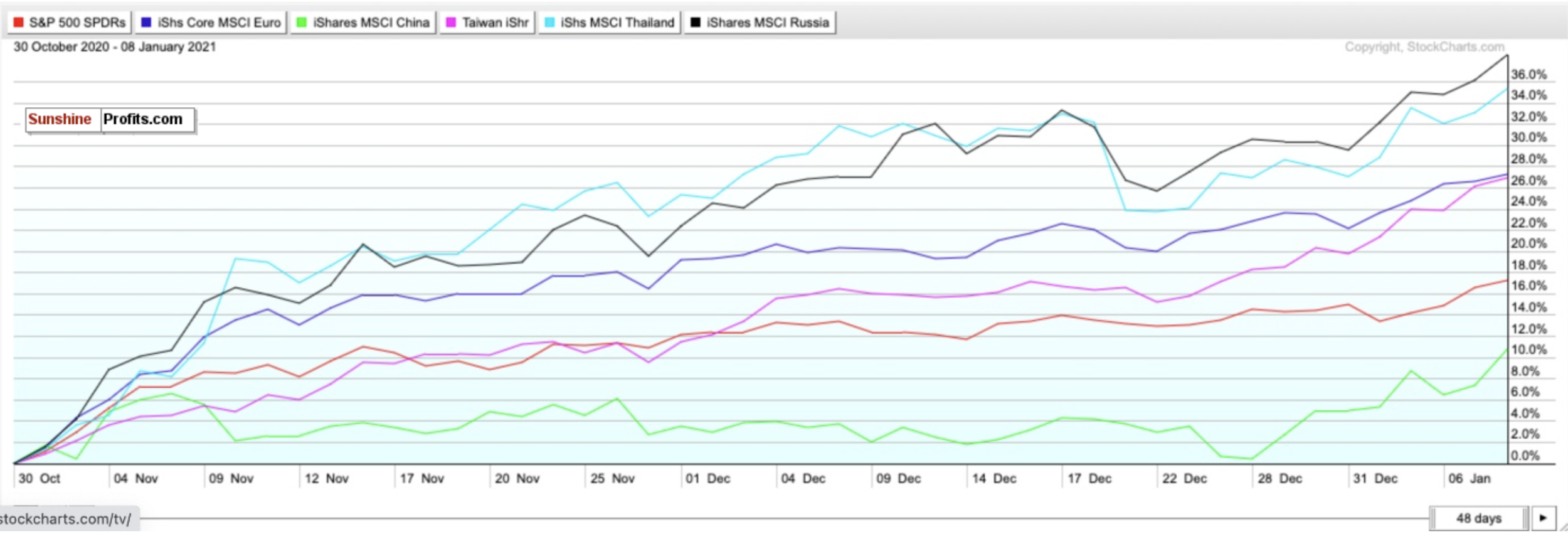

There are two other emerging markets I am very bullish on for 2021 as well - Thailand and Russia. According to a Bloomberg study from December 16th based on 11 indicators of economic and financial performance, Thailand topped the list due to solid reserves and a high potential for portfolio inflows, while Russia scored second due to robust external accounts, a strong fiscal profile, and an undervalued currency.

Do you know who scored last on this list? China. High expectations were largely already baked in during its 2020 recovery, and there is no longer upside.

Do you also know who significantly outperformed the Taiwan ETF (IWT), the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR) since October 30th? The iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS).

Figure 6

For broad exposure to Emerging Markets, you will want to BUY the iShares MSCI Emerging Index Fund (EEM), for exposure to a regional economic power without the geopolitical risks of China, you will want to BUY the iShares MSCI Taiwan ETF (EWT). Consider the iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS) as well for 2021 upside.

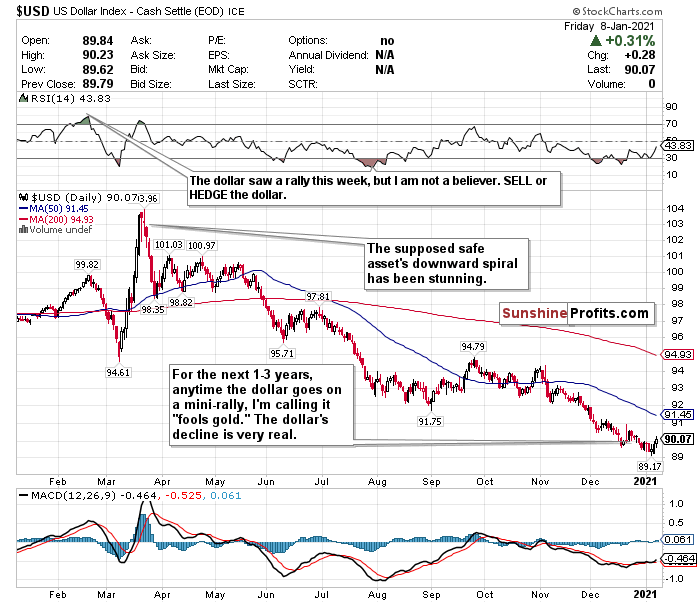

The Dollar Has Rallied but I’m not Sold

Figure 7

Although the U.S. Dollar ticked up somewhat this week, I do not have faith in the greenback as a safe asset. I’m still calling out the dollar’s weakness after several weeks despite its rally and expect the decline to restart thanks to a dovish Fed and multiple headwinds.

Any time the U.S. Dollar rallies, I am calling it “fool’s gold.” Since I started doing these newsletters about a month ago, I have consistently said that any minor rally the dollar experienced would be a mirage. Since it briefly pierced the 91-level on December 9th, it has fallen nearly 1.11%. Despite experiencing another mini-rally and nearly piercing the 91-level again on December 22, I remained steadfast in my bearish outlook of the dollar. Since the open on December 23rd, the U.S. Dollar has declined nearly another 0.53%.

Although the dollar is back above the 90-level, I don’t think this will last.

Since hitting a nearly 3-year high on March 20th, the dollar has plunged nearly 12.76% while emerging markets, foreign currencies, precious metals, and cryptocurrencies continue to strengthen. Gold for example reached an 8-week high on Tuesday (Jan. 5), and Bitcoin continues to hit all-time highs.

On days when COVID-19 fears outweigh any other positive sentiments, dollar exposure might be good to have since it is a safe haven. But in my view, you can do a whole lot better than the U.S. dollar for safety.

I have too many doubts on the effect of interest rates this low for this long, government stimulus, strengthening of emerging markets, and inflation to be remotely bullish on the dollar’s prospects over the next 1-3 years. Meanwhile, the U.S. has $27 trillion of debt, and it’s not going down anytime soon.

Another headwind to consider for the dollar is Democrat control of the government. Because Democrats now have control over both the executive and legislative branches of the government, more aggressive stimulus could be imminent, bringing further devaluation of the dollar.

Additionally, according to The Sevens Report, if the dollar falls below 89.13, this could potentially raise the prospect of a further 10.5% decline to the next support level of 79.78 reached in April 2014. Despite the dollar’s rally this week, I believe we are closer to this point than most realize.

Where possible, HEDGE OR SELL USD exposure.

Pay Very Close Attention to Inflation

Pay very close attention to the possible return of inflation within the next 6-12 months. The Fed has said it will allow the GDP to heat up, and it may overshoot in the medium-term as a result. GDP growth may falter in Q1 2021 but pay close attention to what happens in Q2 and Q3 once vaccines begin to be rolled out on a massive scale. It is only inevitable that inflation will return with the Fed’s policy and projected economic recovery by mid-2021.

If you are looking to the future to hedge against inflation, look into TIPS, commodities, gold, and potentially some REITs.

In the mid-term, I have BUY calls on the SPDR TIPS ETF (SPIP), the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), the SPDR Gold Shares ETF (GLD), and the iShares Cohen & Steers REIT ETF (ICF).

Long-Term

There is so much to worry about in the short-term. But I’m convinced that economic stimulus and the progress made with the vaccine(s) bodes well for the second half of 2021. We may be at the beginning of the end of the pandemic, but over the next 1-3 months, this could be a very bumpy ride back.

There does seem to be one consensus though: 2021 could be a big year for stocks.

I have a very good feeling about stocks, especially small-caps, value stocks, and cyclicals. I just have a much better feeling for them in the second half of 2021. I almost hope we see a correction within the first 3 months of 2021. This could be a very strong buying opportunity.

Summary

The current headwinds are very concerning. Nobody likes living through a pandemic, and nobody likes seeing their Capitol Building ransacked by thugs. This was quite the week to start off the new year.

With that being said, I am optimistic for the second half of 2021 despite the bumpy path there. Until COVID-19 is eradicated, there will inevitably be a tug of war between optimism and pessimism.

A short-term correction to start 2021 is inevitable, but do not let this scare you. Remember - corrections are NORMAL and markets tend to look 6-12 months down the road. Although it is very plausible that there could be some short-term uncertainty and volatility, use this as a time to find buying opportunities for the second half of 2021. Do not get caught up in fear if there is a correction.

I doubt that a crash like the one we saw in March is on the horizon, but a pullback of some sort is coming. Do not be fearful though. Since markets bottomed on March 23rd, here are how the ETFs tracking the indices have performed: Russell 2000 (IWM) up 110.89%. Nasdaq (QQQ) up 88.10%. S&P 500 (SPY) up 73.10%. Dow Jones (DIA) up 69.31%.

In the long-term, markets always end up moving higher and are focused on the future rather than the present.

To sum up all our calls, in the short-term I have a SELL call for:

- the iShares Russell 2000 ETF (IWM) (but do not fully exit positions- trim profits),

- the Invesco QQQ ETF (QQQ) (but do not fully exit positions- trim profits), and

- the SPDR S&P ETF (SPY) (but do not fully exit positions- trim profits)

I have a HOLD call for:

- the SPDR Dow Jones ETF (DIA)

I also have a long-term STRONG BUY call for:

- the iShares Russell 2000 ETF (IWM) BUT IF AND WHEN IT PULLS BACK

For all these ETFs, I am more bullish in the long-term for the second half of 2021.

For the mid-term and long-term, I recommend selling or hedging the U.S. Dollar, and gaining exposure into emerging markets.

I have BUY calls on:

- The iShares MSCI Emerging Index Fund (EEM),

- the iShares MSCI Taiwan ETF (EWT),

- the iShares MSCI Thailand ETF (THD), and

- the iShares MSCI Russia ETF (ERUS).

Additionally, because I foresee inflation returning as early as mid to late 2021…

I also have BUY calls on:

- The SPDR TIPS ETF (SPIP),

- the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC)

- the SPDR Gold Shares ETF (GLD), and

- the iShares Cohen & Steers REIT ETF (ICF)

Thank you.

Matthew Levy, CFA

Stock Trading Strategist