Quick Update

Dear readers, before we get into today’s news and stock analysis and because I’ve been receiving many questions from you, I’d like to first clarify what I mean by BUY, SELL, or HOLD. Here, I am largely referring to outperforming the S&P 500. When the conditions favor adding risk and buying the U.S. market overall, I will be issuing an "alert." I am not sure yet whether I will be moving to entry prices or target prices & stop losses, however, I have discussed this internally with the team at Sunshine Profits. In the current market environment, when fundamentals have essentially fallen to the wayside, I prefer to invest directionally rather than being married to certain levels in the market. In my view, trading with specific figures in mind can hurt long term returns if you do not let your winners run and cut your losers fast. I do update my calls daily, though, and any changes will be highlighted! Thank you again for being such great readers - I truly value your trust. Stay tuned for updates and let me know if you have any other questions!

Monday Intraday Update: In an intraday special bulletin due to the news, markets sharply declined due to fears of a new coronavirus strain. This outweighed what should have been a positive day from the stimulus package finally passing.

News Recap

- At the time of publication, the Dow Jones fell 380 points or 1.26%, the S&P 500 dropped 1.79%, and the Nasdaq lost 1.67%. The small-cap Russell 2000 index also fell 1.74%.

- A new, possibly more contagious strain of the coronavirus was discovered in the UK and sent stocks sharply downwards today.

- Due to the new strain of the virus, more severe lockdowns and travel restrictions across Europe were implemented.

- As a result of the stricter shutdown measures and travel fears, travel-related stocks and COVID-19 recovery stocks were by far the largest laggards in early trading. Norwegian (NCLH) and Royal Caribbean (RCL) cruise lines each fell more than 3%, while airlines such as American Airlines (AAL) slid 5.2%, and United Airlines (UAL) fell more than 4%.

- Hotel stocks were hurt as well such as Wynn Resorts (WYNN) and MGM (MGM) which both fell more than 4%.

- Tesla (TSLA) fell as much as 6% as it officially joined the S&P 500. Tesla has a 1.69% weighting in the index, the fifth largest. Tesla was added to the index in one fell swoop, marking the largest rebalancing of the S&P 500 in history.

- Meanwhile, Nike (NKE) hit a record high after posting strong earnings, while bank stocks surged after the Fed announced on Friday (Dec. 18) that it will allow the big banks to resume share buybacks in the first quarter of 2021. JPMorgan (JPM) shares jumped almost 3% on the news.

- Despite Monday’s losses, lawmakers finally reached an agreement on a $900 billion stimulus package. In this package, direct payments and jobless aid would be provided to struggling Americans. The announcement of the stimulus deal came after negotiations were finally resolved in rolling back the Federal Reserve’s emergency lending powers. According to Treasury Secretary Steven Mnuchin, the stimulus money will go out as soon as next week.

- The FDA officially approved Moderna’s (MRNA) vaccine for emergency use on Friday (Dec. 18) and began rolling the vaccine out on Monday (Dec. 21). Government officials plan to ship nearly 6 million doses of Moderna’s vaccine in addition to the 2.9 million Pfizer (PFE) doses already in distribution.

The general focus of both investors and analysts has appeared to be the long-term potential of 2021, specifically the second half of the year. Yet there are certainly very concerning short-term headwinds.

Inevitably, there will be a short-term tug of war between good news and bad news. The markets this morning perfectly illustrated that. Until this new coronavirus strain was discovered, the biggest factor weighing on the markets in the short-term were stimulus negotiations. COVID-19 concerns and economic shutdowns were largely baked in and overlooked. Once the stimulus package passed though, it wasn’t enough to outweigh fears of this new, allegedly more contagious virus strain that was discovered over the weekend. You truly can’t make these things up. 2020 has been something else.

Vital Knowledge’s Adam Crisafulli put it best in a note to clients:

“There was actually a lot of encouraging news this morning, although it’s being overshadowed (for now) by the gloomy headlines out of the U.K...The market has been in a tug-of-war between the very grim near-term COVID backdrop and the increasingly hopeful medium/long-term outlook (driven by vaccines) – the latter set of forces are more powerful in aggregate, but on occasion, the market decides to focus on the former, and stocks suffer as a result.”

Another thing to consider here is that the markets have likely overheated in the near-term. In my last note after the market closed on Friday (Dec. 18), I mentioned that a correction and some consolidation could be very likely in the short-term on the way towards another strong rally in the second half of 2021. While it is hard to say with conviction WHEN we could see a correction, I believe the market’s behavior today could potentially be a preview of what’s to come between now and the end of Q1 2020. We could see a potential 5% pullback before the year’s end. There is optimistic potential, but the road towards normalcy will hit inevitable speed bumps.

Before the sell-off on Monday (Dec. 21), I had been warning that the market was flashing signs of over-optimism and euphoria. In its most recent survey, for example, the American Association of Individual Investors (AAII) found that 48.1% of investors identified as being bullish - well above the historical average of 38%. With an overabundance of cocky, euphoric, and optimistic investors, the market becomes more vulnerable to selling pressure. Corrections are also way more common than people realize. Only twice in the last 38 years have we had years WITHOUT a correction (1995 and 2017). Because there has not been one since the lows of March, this is another reason why I believe we are due for one.

Despite these near-term risks, the overwhelming majority of market strategists, including myself, are bullish on equities for the second half of 2021. I almost hope for a pullback in the near-term so there can be buying opportunities for the long-term. In these times, I believe you need to have a balance of caution while looking past short-term pain and fear.

Although the economic recovery could stutter in the early half of the year, many analysts expect double-digit gains to continue in 2021. Strategists surveyed by CNBC, for example, expect an average 9.5% rise in 2021 for the S&P 500.

Additionally, according to Robert Dye, Comerica Bank Chief Economist:

“I am pretty bullish on the second half of next year, but the trouble is we have to get there...As we all know, we’re facing a lot of near-term risks. But I think when we get into the second half of next year, we get the vaccine behind us, we’ve got a lot of consumer optimism, business optimism coming up and a huge amount of pent-up demand to spend out with very low interest rates.”

Therefore, to sum it up:

While there is long-term optimism, there are short-term concerns. A short-term correction between now and Q1 2021 is very possible. But I do not believe, with conviction, that a correction above ~20% leading to a bear market will happen.

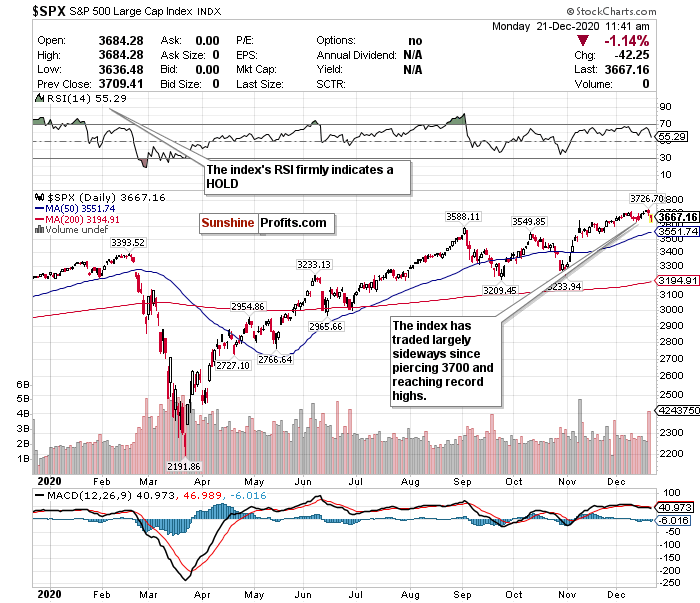

The S&P Has Long-term Upside Mixed With Uncertainty

Although the S&P 500 is off the day’s lows, it is still below the 3700-level and has largely traded sideways amidst unstable volume over the last few sessions.

While I do like where the index is at to consider “nibbling,” this is not enough of a pullback for me to call this a conviction buy. I simply believe that a larger decline and short-term correction could possibly begin before year’s end and will inevitably occur by Q1 2021.

While many analysts and strategists believe this short-term uncertainty is worth it for long-term potential, (and I tend to agree), I would prefer a sharper correction to initiate S&P exposure at a discount. There is definite upside for the second half of 2021. I would just prefer to maximize the upside if I believe that it’s possible to buy the ETF at a lower level.

Some analysts believe the S&P could have up to a 20% upside in 2021, while others caution against an overheating index. According to another survey of market strategists conducted by CNBC, a narrow majority believe that U.S. stocks will continue to rally into 2021, with the S&P 500 rising between 8% and 22% next year from these current levels. This very well could be the case- but I believe most this will happen in the next 6-12 months rather than 1-3 months.

I would prefer a drop closer to below 3600 before feeling more confident in initiating a BUY call. For now, I have the S&P 500 in a HOLD category.

For an ETF that attempts to directly correlate with the performance of the S&P, the SPDR S&P ETF (SPY) is a good option.

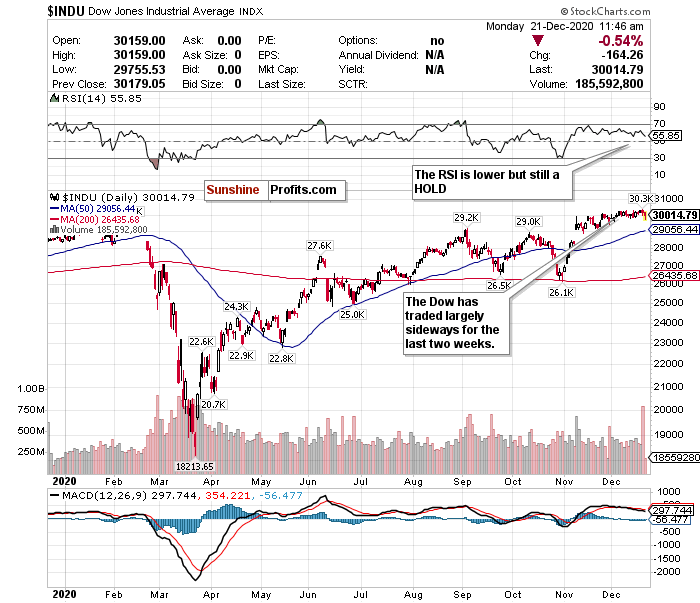

Does the Dow Approach 31,000 or 29,000 Before Mid-2021?

The Dow Jones is well off of Monday’s (Dec. 21) lows. After trading as low as around 29,650, the Dow as of the time of publication is back above 30,000. As of late though, this is an index that has largely lagged nehind the other indices and traded sideways.

I do like that it appears to no longer be overheating in the short-term. Volume has been relatively stable too except for the last two sessions thanks to Tesla. But I have too many short-term questions as to whether or not the Dow can not only stay above 30,000 for more than a week (or in this case, a day) at a time, but also let alone exceed 30,300 and hit more all-time highs.

In my opinion, it is just as likely for the Dow to approach 29,000 as it is to approach 31,000 in the early months of 2021. While I called a short-term pop if a stimulus passed, that clearly did not happen today thanks to the mutant virus strain from Britain. What will 2020 think of next?

With so much uncertainty and the RSI still firmly in hold territory, the call on the Dow stays a HOLD.

This is a very challenging time to make calls with conviction. But one thing I do believe is that if and when there is a drop in the index, it will not be strong and sharply relative to the gains since March, let alone November. I believe that we could be in a sideways holding pattern as investors digest all the news being thrown at them daily.

For an ETF that attempts to directly correlate with the performance of the Dow, the SPDR Dow Jones ETF (DIA) is a strong option.

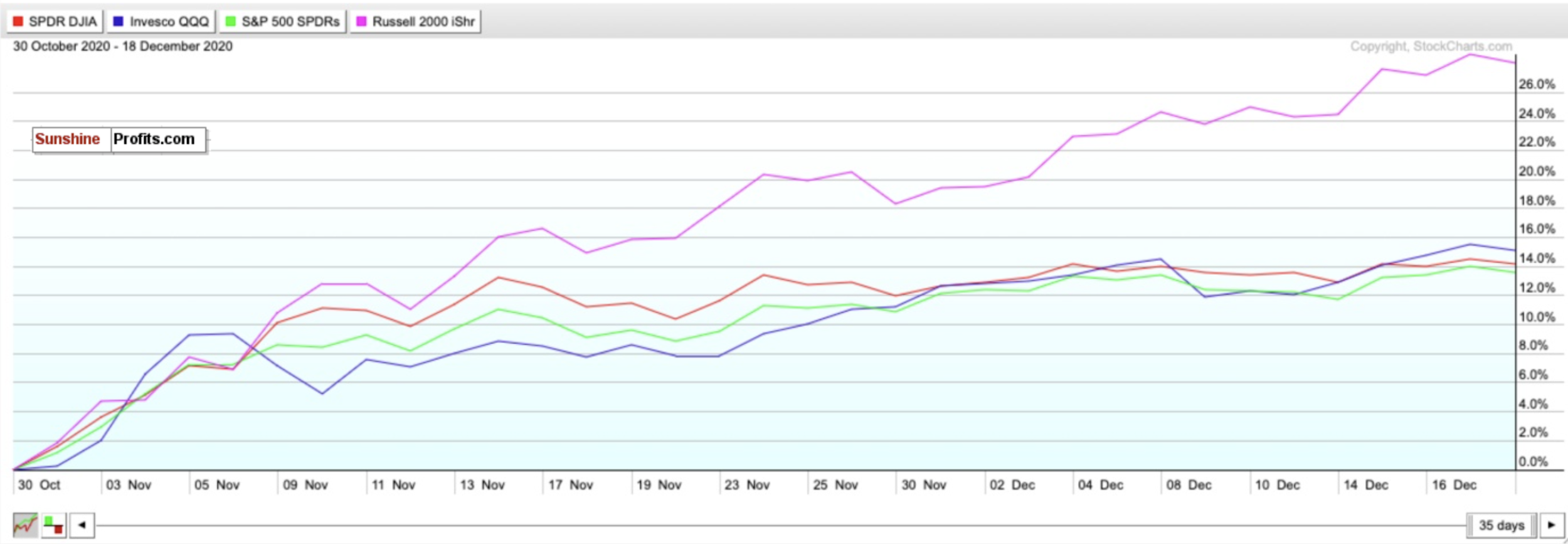

Can Small-caps Own December Too?

The small-cap Russell 2000 underperformed the major indices today. This is to be expected on “sell the news” kind of days because of all the small-cap cyclical stocks that trade on the index and depend on an economic reopening. News of this virus strain out of the UK is frankly devastating for these types of stocks because of the damage it can cause via stricter lockdowns and shutdowns.

Since November, the Russell index has been on a run that is nothing short of amazing. Just look how the iShares Russell 2000 ETF (IWM) compares to the ETFs tracking the Dow, S&P, and Nasdaq in that time frame. Since November, the IWM has risen 28%. This is at least 13% higher than all of the other major indices.

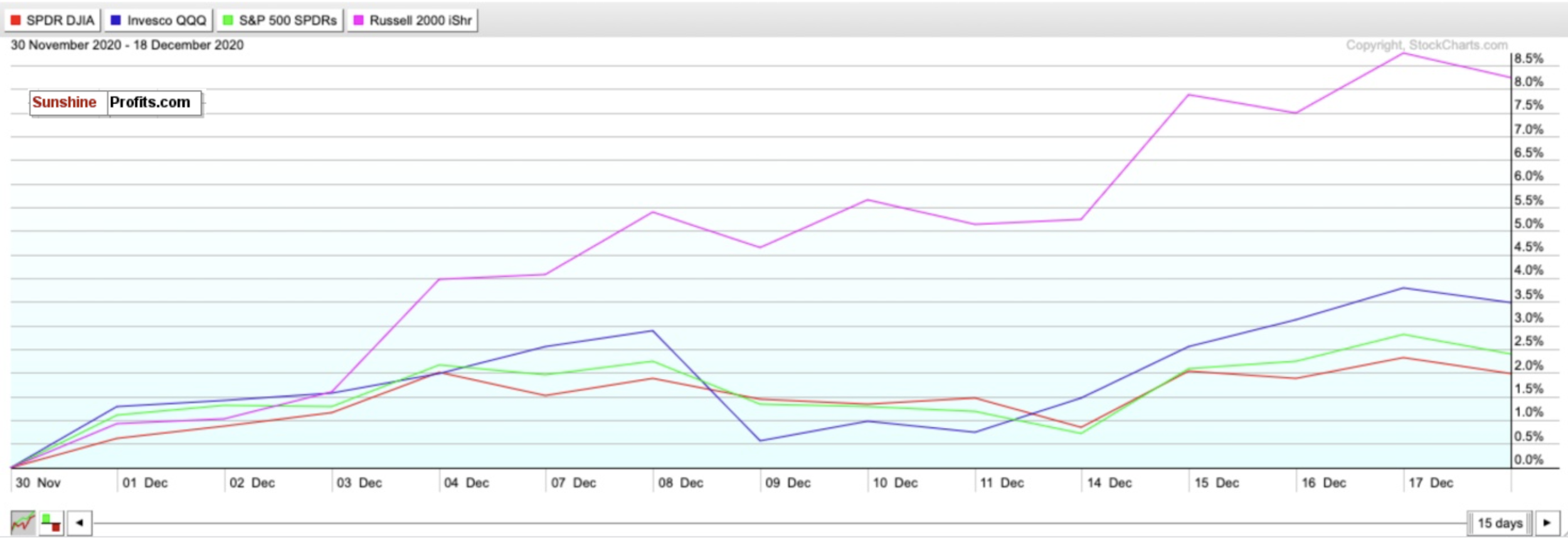

The run has not stopped in December either. The IWM Russell ETF has surged by 7.5% since the start of the month. This is nearly between 4%-6% higher than the ETFs tracking the other major indices.

Just as with tech, I do have some concerns about overheating- maybe even more so. In the short-term, small-cap stocks may have overheated the most and could experience the greatest volatility. SELL and take short-term profits if you can- but do not fully exit positions.

In the long-term, though, small-caps may be the best opportunity to bet on a 2021 economic recovery. I for one am hoping for a correction.

If there is a pullback and correction, consider small-caps a BUY and initiate positions.

Mid-Term/Long-Term

China is No Longer the Top Emerging Market - Consider Taiwan and Others

Emerging markets in both the medium-term and long-term have robust potential. But at this point, it is very country specific.

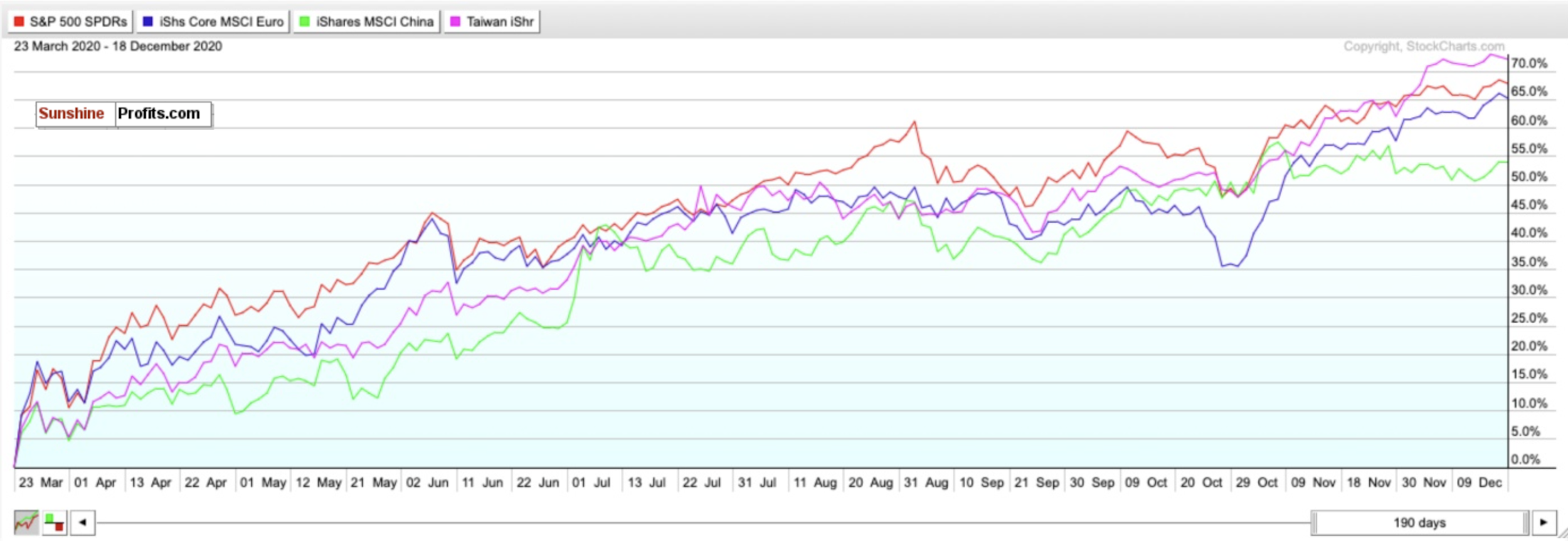

Although China garners most of the attention as a so-called “emerging market,” it has not been the top performer since markets bottomed on March 23rd and is no longer the top option for 2021. If you want China’s regional upside with less geopolitical risks or pandemic recovery baked-in, look at Taiwan. The Taiwan iShares ETF (EWT) has outperformed China in the short-term, medium-term, and long-term.

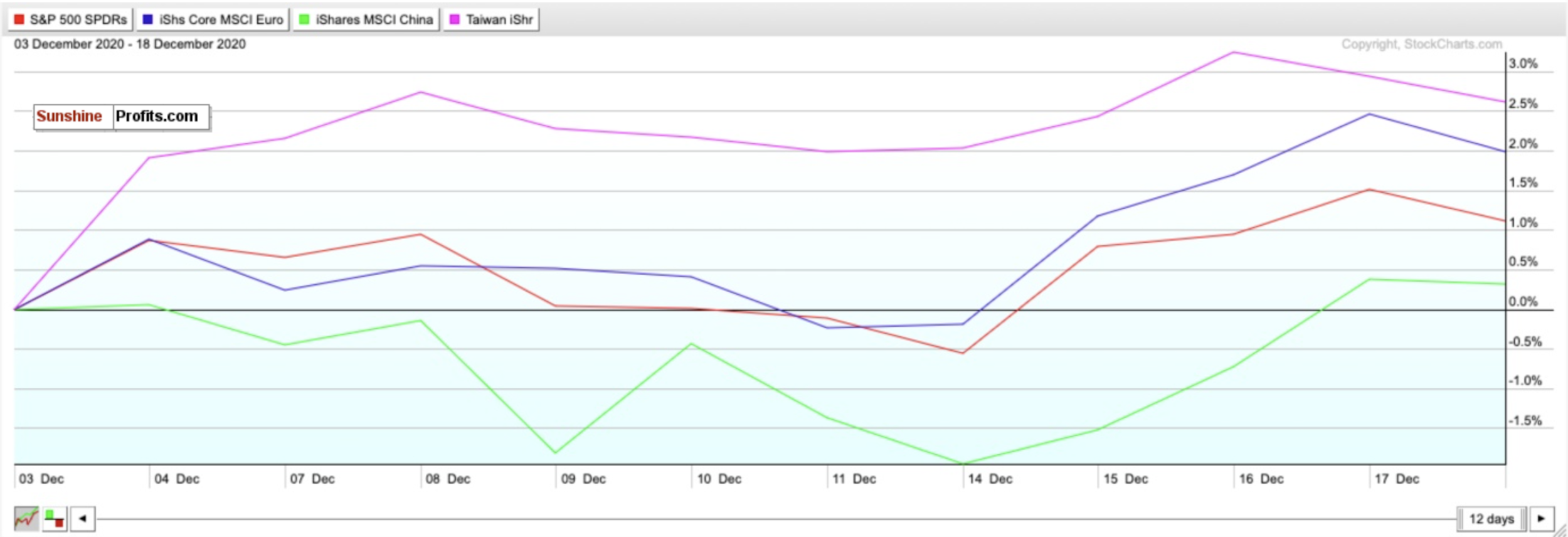

As seen in the chart below, ever since I first called the Taiwan ETF (IWT) a BUY on December 3rd, it has outperformed the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR).

China may have handled the pandemic better than other countries and continues to demonstrate its ability to handle COVID-19’s economic shocks. But keep in mind that this is a regional victory, not just China.

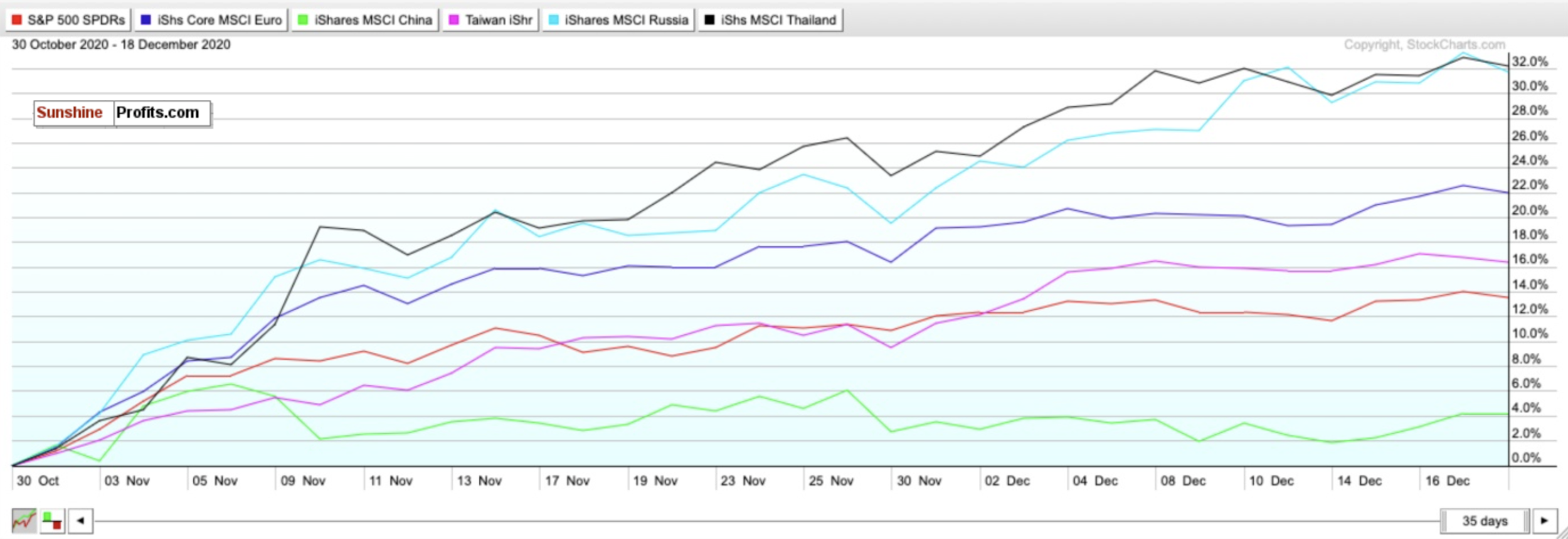

There are two other emerging markets I am very bullish on for 2021 as well: Thailand and Russia. According to a Bloomberg study based on 11 indicators of economic and financial performance, Thailand topped the list due to solid reserves and a high potential for portfolio inflows, while Russia scored second due to robust external accounts, a strong fiscal profile, and an undervalued currency.

Do you know who scored poorly on this list? China. High expectations were largely already baked in during its 2020 recovery, and there is little upside.

Do you also know who significantly outperformed the Taiwan ETF (IWT), the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR) since October 30th? The iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS).

The Thailand ETF is especially experiencing a strong pullback on Monday (Dec. 21) - so this may be a very opportune time to initiate a position.

For broad exposure to Emerging Markets, you will want to BUY the iShares MSCI Emerging Index Fund (EEM), for exposure to a regional economic power without the geopolitical risks of China, you will want to BUY the iShares MSCI Taiwan ETF (EWT). Consider the iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS) as well for 2021 upside.

The Dollar’s Plunge Will Continue

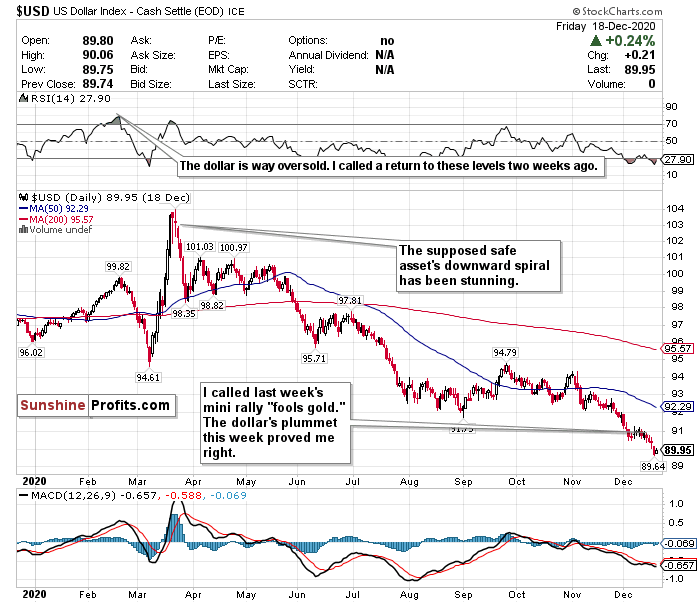

Do not – I repeat do not – be fooled by the dollar’s minor gains during the last two trading sessions. I called the dollar returning to oversold levels last week despite the currency piercing the 91-level two Wednesdays ago (Dec. 9). I believed it to be “fool's gold” and I figured that it was not the sign of any sort of breakout.

Since I called this rally a mirage on December 9th, the dollar has declined by 1%.

I still am calling out the dollar’s weakness after several weeks despite its low levels. I expect the decline to continue as well, thanks to a dovish Fed.

The world’s reserve currency is still trading below 90 and has not traded this low since April 2018.

Joe Manimbo, a senior analyst at Western Union Business Solutions, seemingly agrees with me as well and said that “the latest blow to the dollar came from the Fed, which vowed not to touch policy even if the outlook for the U.S. economy brightens as it now expects.”

Since hitting a nearly 3-year high on March 20th, the dollar has plunged about 12.25% while other currencies continue to strengthen.

Additionally, according to Barron’s, the COVID-19 vaccine(s) could benefit currencies such as the euro more than the dollar. Eurozone GDP is expected to have fallen harder in 2020 than that of the U.S., while the dollar has weakened. If vaccines jolt economies back to pre-pandemic levels, Europe will rebound more spectacularly than the U.S.

Meanwhile, the gap between the yields of U.S. Treasuries and European government bonds is narrowing. This gives investors less of a reason to hold dollar-denominated debt.

After briefly rising above an oversold RSI of 30 last week, the dollar’s RSI is now at an alarmingly low 27.90. The dollar is also significantly trading below both its 50-day and 200-day moving averages.

While the dollar may have more room to fall, this MAY be a good opportunity to buy the world’s reserve currency at a discount as the RSI is oversold. On days when COVID-19 fears outweigh any other positive sentiments, dollar exposure might be good to have since it is a safe haven. But in my view, you can do a whole lot better than the U.S. dollar for safety.

However, I have too many doubts on the effect of interest rates this low for this long, government stimulus, strengthening of emerging markets, and inflation to be remotely bullish on the dollar’s prospects over the next 1-3 years. Additionally, according to The Sevens Report, if the dollar falls below 89.13, this could potentially raise the prospect of a further 10.5% decline to the next support level of 79.78 reached in April 2014

I’m not a crypto guy either myself, but Bitcoin’s run compared to the dollar’s disastrous 2020 has to really make you think sometimes….

For now, where possible, HEDGE OR SELL USD exposure.

Pay Very Close Attention to Inflation

Pay very close attention to the possible return of inflation within the next 6-12 months. The Fed has said it will allow the GDP to heat up, and it may overshoot in the medium-term as a result. Although JP Morgan and Goldman Sachs have cut their GDP growth estimates for Q1 2021, pay close attention to what happens in Q2 and Q3 once vaccines begin to be rolled out on a massive scale. It is only inevitable that inflation will return with the Fed’s policy and projected economic recovery by mid-2021.

If you are looking to the future to hedge against inflation, look into TIPS, commodities, gold, and potentially some REITs.

In the mid-term, I have BUY calls on the SPDR TIPS ETF (SPIP), the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), the SPDR Gold Shares ETF (GLD), and the iShares Cohen & Steers REIT ETF (ICF).

Long-Term

While all of these headwinds may drive some short-term concerns, the progress made on the vaccine/treatment front cannot be ignored. With the vaccine rollout beginning, this may be the beginning of the end of the pandemic. There is certainly significant optimism for 2021 and beyond, but over the next 1-3 months, it could be a bumpy ride back to normalcy. Projections for the economy, the markets, and the pandemic are so all over the place right now, that the only real certainty is that nobody knows a thing, and nobody can predict the future. I do have a very good feeling about stocks, especially value stocks, and cyclicals, in the second half of 2021. I almost hope we see a correction within the first three months of 2021. This could be a very strong buying opportunity.

Summary

While this new mutant strain of COVID-19, and an overheating market may drive some short-term concerns, the stimulus deal, and the vaccine(s) poses significant optimism for 2021 and beyond. This should be cheered by everyone despite the gloomy sentiment today.

Until COVID-19 is eradicated, there will inevitably be a tug of war between optimism and pessimism. The mania that has consumed the markets could possibly lead to a short-term correction to end off 2020 and start 2021 as well.

Please keep in mind though that markets are forward-looking instruments and are investment vehicles that look 6-12 months down the road. Although it is very plausible that there could be some short-term uncertainty and volatility, use this as a time to find buying opportunities for the second half of 2021. Do not get caught up in fear if there is a correction.

I do not believe a crash like the one we saw March is on the horizon, but a pullback is inevitable. If this happens, do not be shy. Since markets bottomed on March 23rd, here is how the ETFs tracking the indices have performed: Russell 2000 (IWM) up 98.32%. Nasdaq (QQQ) up 82.48%. S&P 500 (SPY) up 67.70%. Dow Jones (DIA) up 64.34%.

In the long-term, markets always end up moving higher and are focused on the future rather than the present.

To sum up all our calls, in the short-term I have a SELL call for:

- Invesco QQQ ETF (QQQ) (but do not fully exit positions- trim profits)

- iShares Russell 2000 ETF (IWM) (but do not fully exit positions)

I have a HOLD call for:

- the SPDR S&P ETF (SPY),

- SPDR Dow Jones ETF (DIA)

I have a BUY call for:

- iShares Russell 2000 ETF (IWM) if it pulls back

For all these ETFs though, I am more bullish in the long-term for the second half of 2021.

For the mid-term and long-term, I recommend selling or hedging the US Dollar, and gaining exposure into emerging markets.

I have BUY calls on:

- The iShares MSCI Emerging Index Fund (EEM),

- the iShares MSCI Taiwan ETF (EWT),

- the iShares MSCI Thailand ETF (THD), and

- the iShares MSCI Russia ETF (ERUS).

Additionally, because I foresee inflation returning as early as mid to late 2021…

I also have BUY calls on:

- The SPDR TIPS ETF (SPIP),

- the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC)

- the SPDR Gold Shares ETF (GLD), and

- the iShares Cohen & Steers REIT ETF (ICF)

Thank you.

Matthew Levy, CFA

Stock Trading Strategist