Quick Update

In an intraday special before the Christmas holiday (Dec. 23), markets shook off late-night comments from President Trump and broadly gained. The S&P 500 is looking to end a three-day losing streak.

News Recap

- At the time of publication, the Dow Jones rose 221 points or 0.74%, the S&P 500 rose 0.54%, and the Nasdaq gained 0.08%. The small-cap Russell 2000 once again outperformed and gained 0.95%.

- In a late-night video (Dec. 22), President Trump called the $900 billion stimulus package that was just passed an unsuitable “disgrace,” and asked to be sent a “suitable bill or else the next administration will have to deliver a COVID-19 relief package.” Congress has approved the stimulus bill, but it will not become official until the president signs off.

- In his video, President Trump demanded stimulus checks for Americans to be raised from $600 to $2,000 each.

- Despite Trump’s comments, markets largely shook them off and rose on positive jobless data. U.S. jobless claims totaled 803,000 during the week ending Dec. 19 and beat the estimated 880,000.

- Core durable goods and personal income both disappointed in November.

- Pfizer (PFE) and BioNTech (BNTX) announced a second deal with the U.S. government to supply another 100 million doses of their COVID-19 vaccine. This deal brings the total amount of vaccine doses to 200 million, which will be delivered by the end of July 2021. Pfizer rose 2% on the news.

- After concerns of a new strain of COVID-19 caused markets to briefly sell-off on Monday (Dec. 21), fears were eased on Wednesday after health experts said the vaccines in production would still be effective against it.

- Cyclical sectors most dependent on an economic recovery led the markets. Energy and financials each rose 3.2% and 1.9% at the time of publication respectively, while materials and industrials also gained. Oil giants Chevron and Exxon gained more than 2%, while Diamondback Energy jumped over 8% after announcing two acquisitions this week.

- Travel stocks sharply recovered on the easing of virus fears after selling off earlier in the week. United Airlines (UAL) and Delta (DAL) each gained more than 3%, while Carnival (CCL) and Norwegian (NCL) both jumped over 6%, and Royal Caribbean (RCL) gained 3.5%. Hotel stocks also rose, such as MGM Resorts (MGM) which gained 3%, and Las Vegas Sands (LVS) and Wynn Resorts (WYNN) which gained 1.7% and 2.8%, respectively.

- COVID-19 has now killed over 318,000 Americans (and counting). The CDC announced that this is now the deadliest year in American history as total deaths are expected to top 3 million for the first time. Deaths are also expected to jump 15% from the previous year. This would mark the largest single-year percentage leap since 1918 when WWI and fatalities from the Spanish Flu Pandemic caused deaths to rise an estimated 46%.

After the S&P experienced a three-day losing streak, and markets traded largely mixed the last few sessions, investors were given an early gift before Christmas. Yet while the general focus of both investors and analysts has appeared to be the long-term potential of 2021, specifically the second half of the year, there are certainly very concerning short-term headwinds.

I do not believe that Wednesday’s (Dec. 23) trading will be the short-term norm.

Inevitably, there will be a short-term tug of war between good news and bad news. I truly believe though that these moves are manic and based on sentiment. However, I also believe a lot of the short-term good news has been baked in, and a lot of the near-term headwinds have been ignored.

I also believe that investors will either be taking profits before the year’s end and rebalancing for 2021. I think the big moves upwards are over for the rest of 2020. We could be moving sideways or downwards in the near-term.

Another thing to consider here is that the markets have likely overheated. In my note after the market closed on Friday (Dec. 18), I mentioned that a correction and some consolidation could be very likely in the short-term on the way towards another strong rally in the second half of 2021. While it is hard to say with conviction as to WHEN we could see a correction, I believe that the S&P’s three-day losing streak could potentially be a preview of what’s to come between now and the end of Q1 2020.

There is optimistic potential, but the road towards normalcy will hit inevitable speed bumps.

I do believe though that a correction is healthy and could be a good thing. Corrections happen way more often than people realize. Only twice in the last 38 years have we had years WITHOUT a correction (1995 and 2017). I believe we are overdue for one because there has not been a correction since the lows of March. This is healthy market behavior and could be a very good buying opportunity for what I believe will be a great second half of the year.

The mid-term and long-term optimism are very real, despite the near-term risks. The passage of the stimulus package only solidifies the robust vaccine-induced tailwinds entering 2021- specifically for small-cap value stocks.

In the short-term, there will be some optimistic and pessimistic days. On some days, such as Tuesday (Dec. 22), the “pandemic” market trend will happen - cyclical and COVID-19 recovery stocks lagging, and tech and “stay-at-home” stocks leading. On other days, a broad sell-off based on virus fears may occur as well. Additionally, there will also be days where there will be a broad market rally due to optimism and 2021 related euphoria. And finally, there will be days (and in my opinion, this will be most trading days), that will see markets trading largely mixed, sideways, and reflecting uncertainty.

Therefore, to sum it up:

While there is long-term optimism, there are short-term concerns. A short-term correction between now and Q1 2021 is very possible. But I do not believe, with conviction, that a correction above ~20% leading to a bear market will happen.

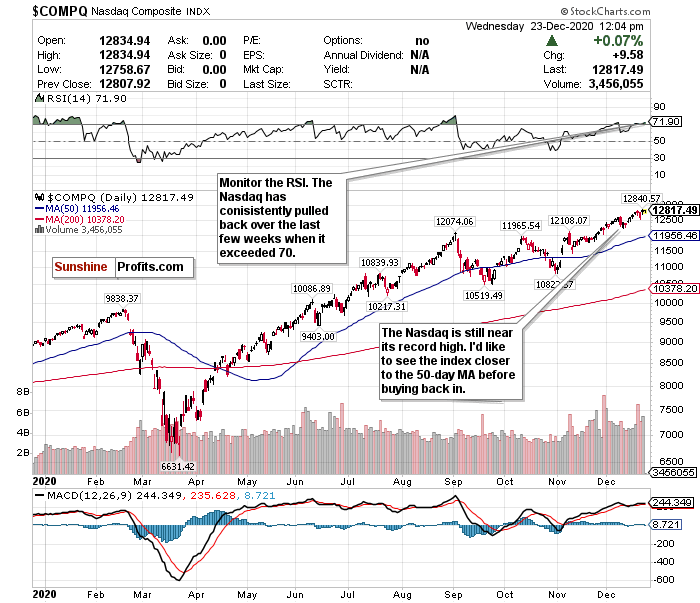

Another Nasdaq Pullback? Not if but WHEN

On Friday’s note (Dec. 18), I changed my short-term call on the Nasdaq to a SELL. While I did not say to fully exit positions, I said that now would be a good time to trim some profits before an eventual pullback. Since I made that call, the Nasdaq has been largely flat. Despite slightly gaining about 0.08% at the time of publication, it is still lagging behind the other indices.

I said to pay close attention to the RSI. While an overbought RSI does not automatically mean a trend reversal, I called keeping a very close eye on this for the Nasdaq. The Nasdaq pulled back on December 9th after it exceeded an RSI of 70, and briefly pulled back again after passing 70 again last week. We are now back above 70 and nearly back at all-time highs. Be prepared for another eventual downturn shortly.

Do not let anyone tell you “this time is different” if fears of the dot-com bubble are discussed. History repeats itself, especially in markets. I have many concerns about tech valuations and their astoundingly inflated levels. The recent IPOs of DoorDash (DASH) and AirBnB (ABNB) reflect this. I believe that more pullbacks could and should inevitably come in the short-term.

For now, take profits and SELL. Do a little rebalancing before 2021, but do not fully exit.

While tech has overheated in the short-term, my optimism and bullish thoughts for 2021 have not changed. I hope tech pulls back closer to its 50-day moving average for some quality long-term buying opportunities.

Do not forget that tech can be very helpful to own on pessimistic days because of all the “stay-at-home” names as well. This is why you should trim, take some gains, but not fully exit positions.

For an ETF that attempts to directly correlate with the performance of the NASDAQ, the Invesco QQQ ETF (QQQ) is a good option.

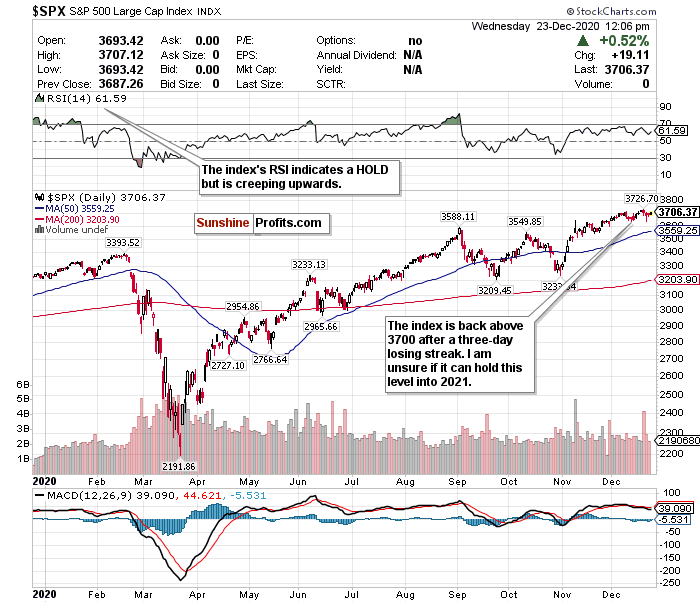

The S&P Has Long-term Upside Mixed with Uncertainty

The S&P 500 is on pace to end its three-day losing streak. I always cheer stocks going up, but I am looking for buying opportunities too. The S&P’s losing streak was simply not enough of a pullback for me to “nibble” and start buying. I would prefer it around 3600 or below. The index has also largely traded sideways as of late, and I question whether or not it can stay above 3700 for more than a week at a time.

I simply believe that a larger decline and short-term correction will inevitably occur by Q1 2021.

While many analysts and strategists believe this short-term uncertainty is worth it for long-term potential, (and I tend to agree), I would prefer a sharper correction to initiate S&P exposure at a discount. There is clear upside for the second half of 2021. I would just prefer to maximize the upside if I believe that it’s possible to buy the ETF at a lower level.

Some analysts believe the S&P could have up to a 20% upside in 2021, while others caution against an overheating index. According to another survey of market strategists conducted by CNBC, a narrow majority believe that U.S. stocks will continue to rally into 2021, with the S&P 500 rising between 8% and 22% next year from these current levels. This very well could be the case, but I believe most of this will happen in the next 6-12 months rather than 1-3 months.

For now, I have the S&P 500 in a HOLD category.

For an ETF that attempts to directly correlate with the performance of the S&P, the SPDR S&P ETF (SPY) is a good option.

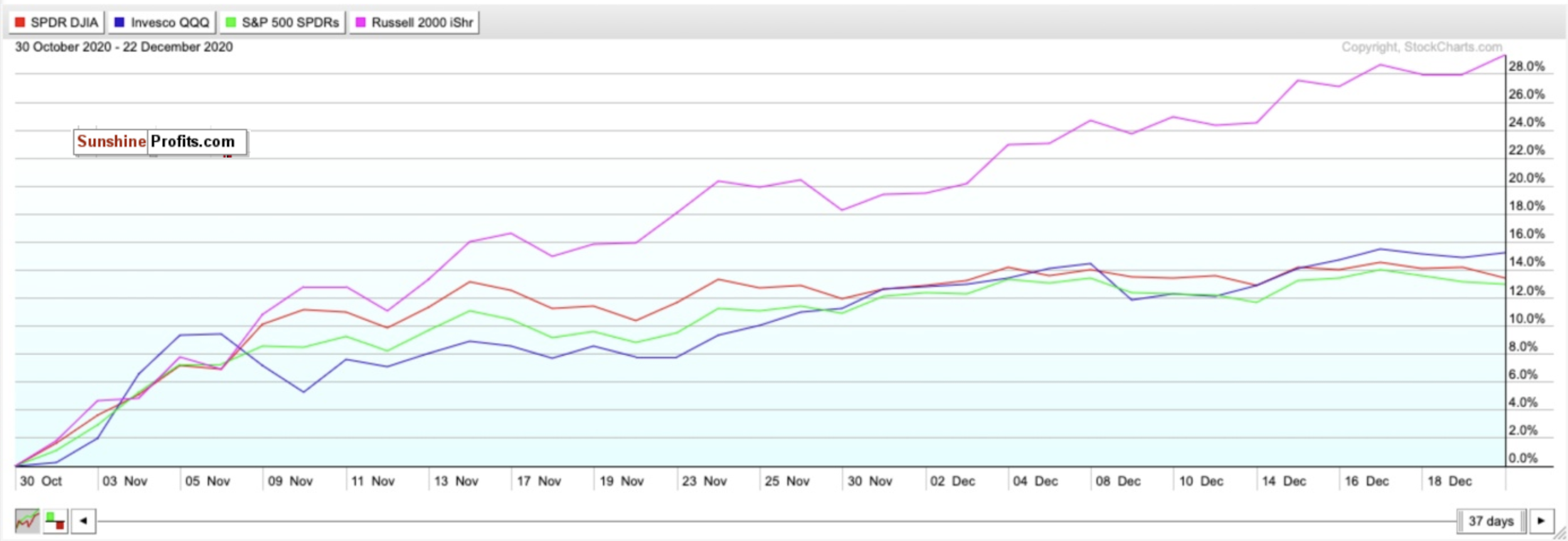

Can Small-caps Own December Too?

The Russell 2000 small-cap index once again beat the larger-cap indices and gained 1.01% on Tuesday (Dec. 22) despite the negative sentiment and sell-offs. With the broader market rally on Wednesday (Dec. 23), it appears the same thing is happening. Small-caps just keep outperforming the big boys, and won’t stop.

I do love small-cap stocks in the long-term and this small-cap rally is more encouraging than the “stay-at-home” stock rallies from April/May. This is a bullish sign for long-term economic recovery and shows that investors are optimistic that a vaccine will return life to relative normalcy by mid-2021.

As seen in the chart above, since November, the Russell index has been on a run nothing short of astounding. Just look how the iShares Russell 2000 ETF (IWM) compares to the ETFs tracking the Dow, S&P, and Nasdaq in that time frame. Since November, the IWM has risen nearly 28% and has at least doubled the returns of the ETFs tracking the other major indices.

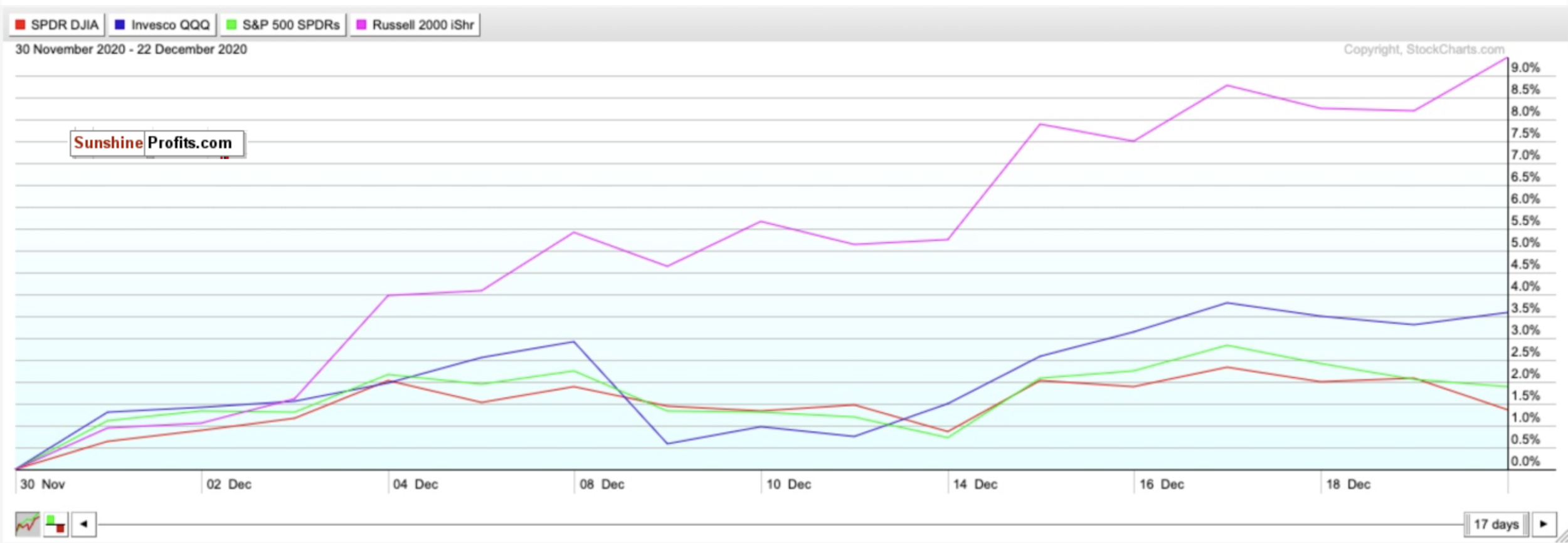

The trend has been largely the same in December as seen below:

Although the Russell index is composed mostly of small-cap cyclical stocks dependent on the recovery of the broader economy and could be more adversely affected on “sell-the-news” kind of days, its hot streak since November has seemingly not cooled off as much as other indices and sectors. But I do have some concerns about overheating in the short-term. Stocks simply just don’t always go up in a straight line. If they did, everyone and their mother would invest.

I believe a short-term pullback will eventually happen. Truthfully, I hope it does for long-term buying opportunities.

Small-cap stocks may have overheated in the short-term and could experience the greatest volatility. SELL and take short-term profits if you can- but do not fully exit positions.

If there is a pullback, this is a STRONG BUY for the long-term recovery.

Mid-Term/Long-Term

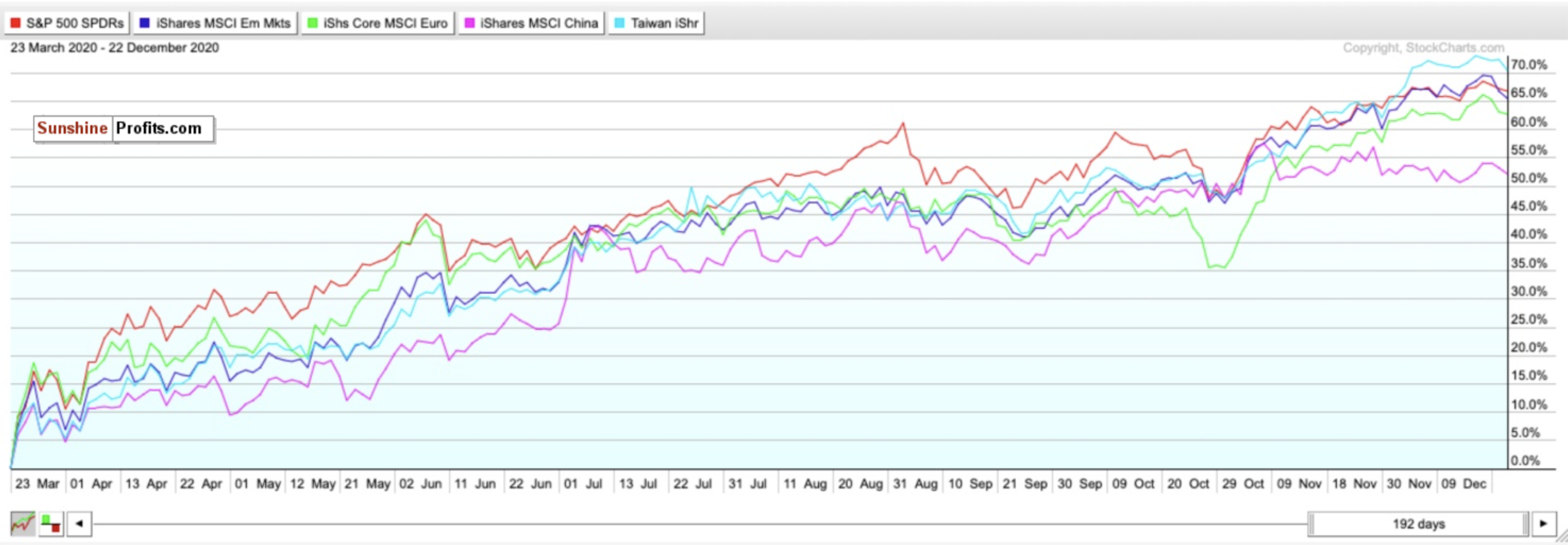

Taiwan and Others for Emerging Market Exposure - Not China

Emerging markets in both the medium-term and long-term have robust potential. But at this point, it is very country specific.

Although China garners most of the attention as a so-called “emerging market,” it has not been the top performer since markets bottomed on March 23rd and is no longer the top option for 2021. If you want China’s regional upside with less geopolitical risks or pandemic recovery baked-in, look at the Taiwan iShares ETF (EWT). Taiwan has outperformed China in the short-term, medium-term, and long-term.

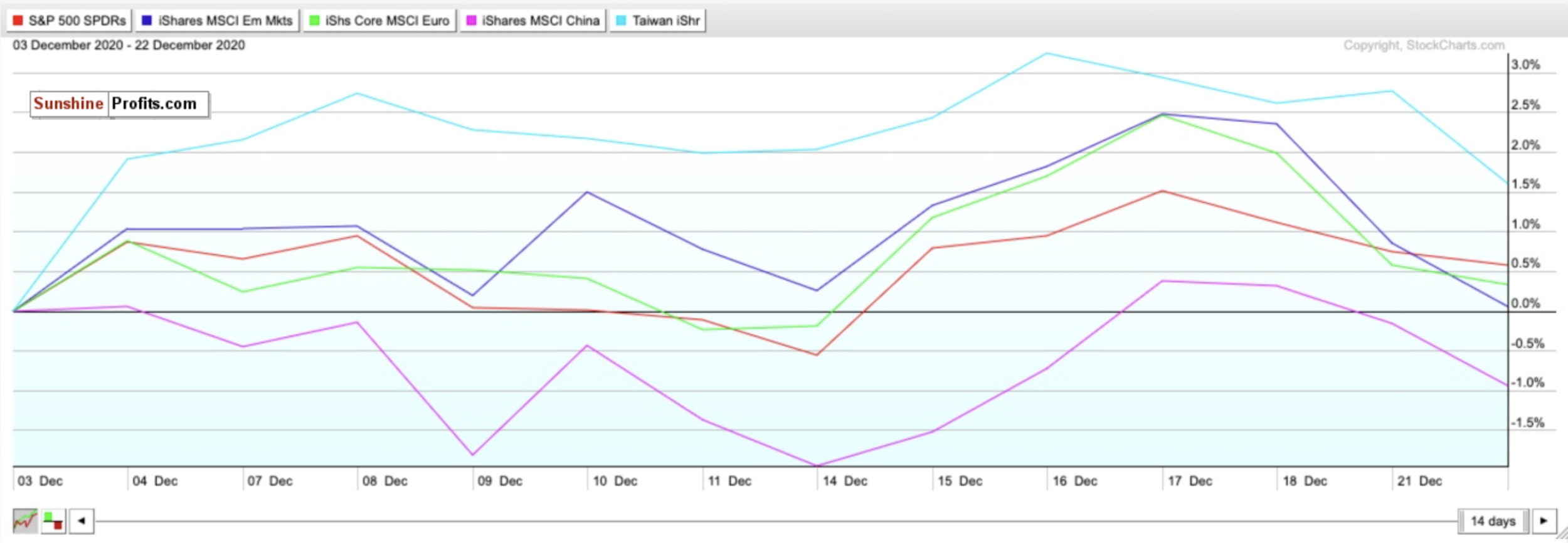

As seen in the chart below, ever since I first called the Taiwan ETF (IWT) a BUY on December 3rd it has outperformed the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR).

China may have handled the pandemic better than other countries and continues to demonstrate its ability to handle COVID-19’s economic shocks. But keep in mind that this is a regional victory, not just China.

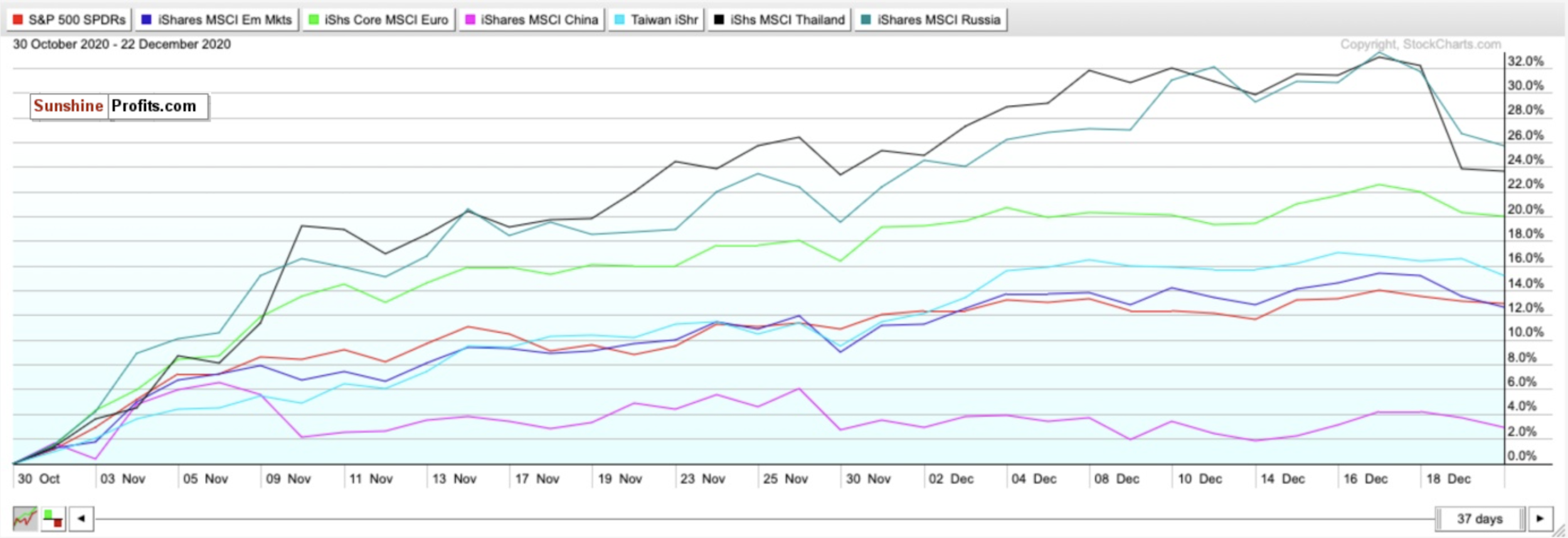

There are two other emerging markets I am very bullish on for 2021 as well- Thailand and Russia. According to a Bloomberg study based on 11 indicators of economic and financial performance, Thailand topped the list due to solid reserves and a high potential for portfolio inflows, while Russia scored second due to robust external accounts, a strong fiscal profile, and an undervalued currency.

Do you know who scored poorly on this list? China. High expectations were largely already baked in during its 2020 recovery, and there is little upside.

Do you also know who significantly outperformed the Taiwan ETF (IWT), the MSCI China ETF (MCHI), the SPDR S&P ETF (SPY), and iShares Core Europe ETF (IEUR) since October 30th? The iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS).

Both the Thailand ETF and Russia ETF also experienced strong pullbacks on Monday (Dec. 21), so this may be a very opportune time to initiate positions.

For broad exposure to Emerging Markets, you will want to BUY the iShares MSCI Emerging Index Fund (EEM), for exposure to a regional economic power without the geopolitical risks of China, you will want to BUY the iShares MSCI Taiwan ETF (EWT). Consider the iShares MSCI Thailand ETF (THD) and the iShares MSCI Russia ETF (ERUS) as well for 2021 upside.

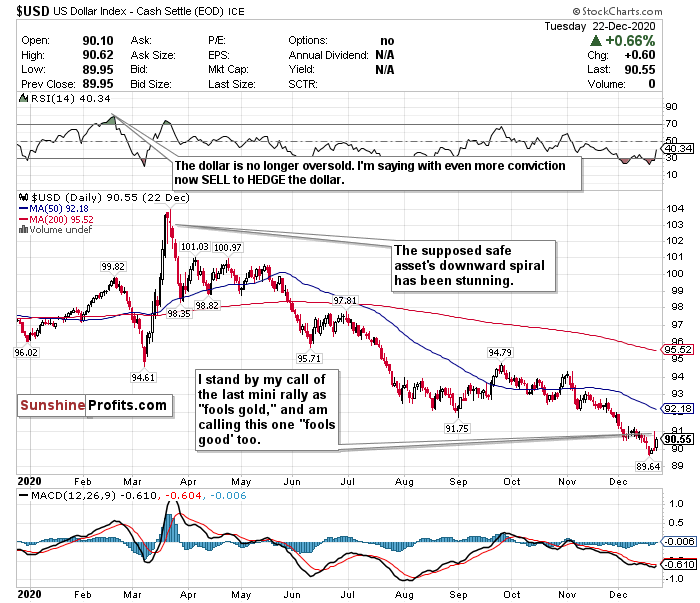

The Dollar’s Rally is a Mirage

I’m not a fan of the dollar these days and am not fooled by this latest mini-rally. I called its rally past the 91-level two Wednesdays ago “fool’s gold,” and I’m calling this rally “fool’s gold” as well.

I am still calling out the dollar’s weakness after several weeks, despite its low levels. I expect the decline to continue as well, thanks to a dovish Fed.

Joe Manimbo, a senior analyst at Western Union Business Solutions, seemingly agrees with me as well and said that “the latest blow to the dollar came from the Fed, which vowed not to touch policy even if the outlook for the U.S. economy brightens as it now expects.”

Since hitting a nearly 3-year high on March 20th, the dollar has plunged nearly 13% while emerging markets and other currencies continue to strengthen.

On days when COVID-19 fears outweigh any other positive sentiments, dollar exposure might be good to have since it is a safe haven. But in my view, you can do a whole lot better than the US dollar for safety. Despite the world’s reserve currency trading above 90 again, it is still hovering around its lowest levels since April 2018.

I have too many doubts on the effect of interest rates this low for this long, government stimulus, strengthening of emerging markets, and inflation to be remotely bullish on the dollar’s prospects over the next 1-3 years. Meanwhile, the US has $27 trillion of debt, and it’s not going down anytime soon.

Additionally, according to The Sevens Report, if the dollar falls below 89.13, this could potentially raise the prospect of a further 10.5% decline to the next support level of 79.78 reached in April 2014. I believe this is more likely to happen than the dollar piercing 91 again.

The dollar’s RSI is now back above 40 somehow as well despite significantly trading below both its 50-day and 200-day moving averages.

I’m not a crypto guy either myself, but Bitcoin’s run compared to the dollar’s disastrous 2020 has to really make you think sometimes…

For now, where possible, HEDGE OR SELL USD exposure.

Pay Very Close Attention to Inflation

Pay very close attention to the possible return of inflation within the next 6-12 months. The Fed has said it will allow the GDP to heat up, and it may overshoot in the medium-term as a result. Although JP Morgan and Goldman Sachs have cut their GDP growth estimates for Q1 2021, pay close attention to what happens in Q2 and Q3 once vaccines begin to be rolled out on a massive scale. It is only inevitable that inflation will return with the Fed’s policy and projected economic recovery by mid-2021.

If you are looking to the future to hedge against inflation, look into TIPS, commodities, gold, and potentially some REITs.

In the mid-term, I have BUY calls on the SPDR TIPS ETF (SPIP), the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), the SPDR Gold Shares ETF (GLD), and the iShares Cohen & Steers REIT ETF (ICF).

Long-Term

There is so much to worry about in the short-term. But I believe that the stimulus package and the progress made with the vaccine(s) bodes well for the second half of 2021. We may be at the beginning of the end of the pandemic. But over the next 1-3 months, this could be a very bumpy ride back. Projections for the economy, the markets, and the pandemic are so all over the place right now.

There does seem to be one consensus though: 2021 could be a big year for stocks.

I have a very good feeling about stocks, especially small-caps, value stocks, and cyclicals. I just have a much better feeling for them in the second half of 2021. I almost hope we see a correction within the first three months of 2021. This could be a very strong buying opportunity.

Summary

While the headwinds of an out-of-control pandemic and an overheating market may drive some short-term concerns, the stimulus deal and the vaccine(s) poses significant optimism for 2021 and beyond.

However, until COVID-19 is eradicated, there will inevitably be a tug of war between optimism and pessimism. The mania that has consumed the markets could lead to a short-term correction to start 2021 as well.

Please keep in mind though that markets are forward-looking instruments and are investment vehicles that look 6-12 months down the road. Although it is very plausible that there could be some short-term uncertainty and volatility, use this as a time to find buying opportunities for the second half of 2021. Do not get caught up in fear if there is a correction.

I do not believe a crash like the one we saw in March is on the horizon, but a pullback is inevitable. If this happens, do not be fearful. Since markets bottomed on March 23rd, here is how the ETFs tracking the indices have performed: Russell 2000 (IWM) up 100.48%. Nasdaq (QQQ) up 82.63%. S&P 500 (SPY) up 66.81%. Dow Jones (DIA) up 63.34%.

In the long-term, markets always end up moving higher and are focused on the future rather than the present.

To sum up all our calls, in the short-term I have a SELL call for:

- Invesco QQQ ETF (QQQ) (but do not fully exit positions- trim profits)

- iShares Russell 2000 ETF (IWM) (but do not fully exit positions- trim profits)

I have a HOLD call for:

- the SPDR S&P ETF (SPY),

- SPDR Dow Jones ETF (DIA)

I also have a long-term STRONG BUY call for:

- iShares Russell 2000 ETF (IWM) BUT IF AND WHEN IT PULLS BACK

For all these ETFs, I am more bullish in the long-term for the second half of 2021.

For the mid-term and long-term, I recommend selling or hedging the US Dollar, and gaining exposure into emerging markets.

I have BUY calls on:

- The iShares MSCI Emerging Index Fund (EEM),

- the iShares MSCI Taiwan ETF (EWT),

- the iShares MSCI Thailand ETF (THD), and

- the iShares MSCI Russia ETF (ERUS).

Additionally, because I foresee inflation returning as early as mid to late 2021…

I also have BUY calls on:

- The SPDR TIPS ETF (SPIP),

- the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC)

- the SPDR Gold Shares ETF (GLD), and

- the iShares Cohen & Steers REIT ETF (ICF)

Thank you.

Matthew Levy, CFA

Stock Trading Strategist