For once, we have a week in 2021 where the market really didn't move all that much.

Except for weed stocks that whipsawed GameStock-like and Bitcoin and Dogecoin making waves thanks to Lord Elon, it's really been kind of a boring week for the major indices.

The S&P and Nasdaq closed at another record high Thursday (Feb. 11), while the Dow barely retreated from its own record high. The red-hot Russell has lagged this week.

However, it’s all relative. No index has moved upwards or downwards more than about 0.30% week-to-date.

It’s about time we had a week of relative quiet in the market.

The sentiment is indeed still rosy right now. The economic recovery appears to be gaining steam, and the Q1 GDP decline everyone predicted might not be as sharp as we anticipated. We could also be days away from trillions of dollars of much-needed stimulus getting pumped into the economy.

Earnings continue to impress, too, and are on pace to rise by over 20% in 2021. Since 1980, only 12 years have earnings increased by 15% or more. Except for 2018, the market gained an average of 12% in all of those years.

We could also days away from FDA approval of a one-dose vaccine from Johnson and Johnson (JNJ).

The COVID numbers and vaccine trend could truly turn the tide of things. More people in the U.S. have now been vaccinated than total cases, and the week kicked off (Feb. 8) with vaccine doses outnumbering new cases 10-1. Dr. Fauci also claims that vaccines could be available to the general public by April.

But we're not out of the woods yet. Sure this week has been calm.

But it’s almost been “too calm.”

I still worry about complacency, valuations, and the return of inflation.

“You wouldn’t know it from the sedate action in the averages,” but Wall Street is on “a highway to the danger zone,” CNBC’s Jim Cramer said.

“In a frothy market, stocks will have enormous rallies that are totally disconnected from the underlying fundamentals.”

He’s not wrong.

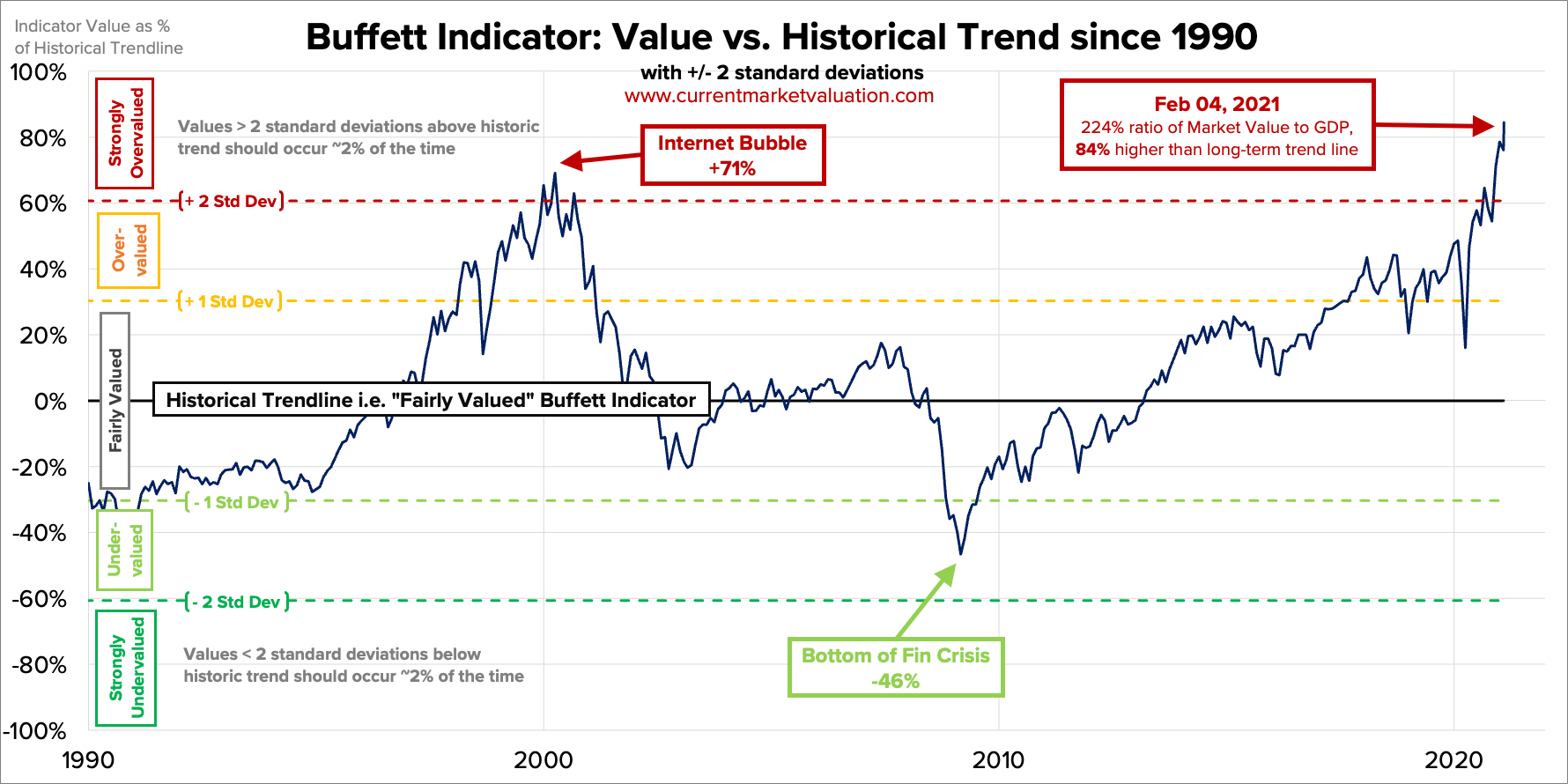

Look at the Buffett Indicator as of February 4. Where I track this indicator usually updates once a week and shows the total U.S. stock market valuation to the GDP.

If you take the US stock market cap of $48.7 trillion and the estimated GDP of $21.7 trillion, we're nearly 224% overvalued and 84% above the historical average. This ratio has not been at a level like this since the dotcom bubble.

Worse? This chart was dated February 4. The market’s only risen since then.

This is what I mean by don’t be fooled by the relative calm of this week.

The S&P 500’s forward 12-month P/E ratio is also well above its 10-year average of 15.8. The Russell 2000 is also back at a historic high above its 200-day moving average. Tech stock valuations are again approaching dotcom bust levels.

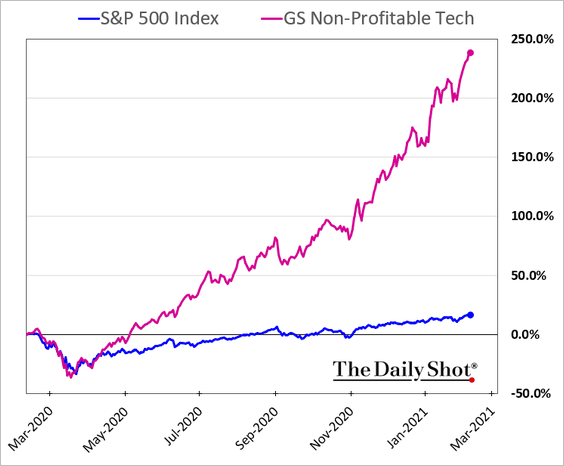

Still not sold? Look at Goldman’s non-profitable tech index. It’s approaching an absurd 250% year-over-year performance.

Bank of America also believes that a market correction could be on the horizon due to signs of overheating.

While I don’t foresee a crash like we saw last March, I still maintain that some correction before the end of Q1 could happen.

Corrections are healthy and normal market behavior, and we are long overdue for one. They are also way more common than most realize. Only twice in the last 38 years have we had years WITHOUT a correction (1995 and 2017).

A correction could also be an excellent buying opportunity for what could be a great second half of the year.

Bank of America also echoed this statement and said that “We expect a buyable 5-10% Q1 correction as the big ‘unknowns’ coincide with exuberant positioning, record equity supply, and ‘as good as it gets’ earnings revisions.”

The key word here- buyable.

My goal for these updates is to educate you, give you ideas, and help you manage money like I did when I was pressing the buy and sell buttons for $600+ million in assets. I left that career to pursue one where I could help people who needed help, instead of the ultra-high net worth.

With that said, to sum it up:

While there is long-term optimism, there are short-term concerns. A short-term correction between now and the end of Q1 2021 is possible. I don't think that a decline above ~20%, leading to a bear market will happen.

Hopefully, you find my insights enlightening. I welcome your thoughts and questions and wish you the best of luck.

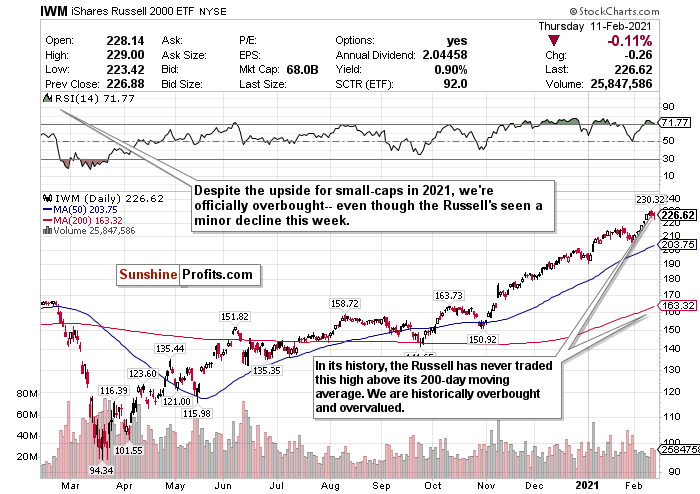

Small-Caps are Still Overbought

Figure 1- iShares Russell 2000 ETF (IWM)

The Russell 2000 small-cap index has been the laggard this week. While the larger indices are fractionally up this week, the Russell 2000 is fractionally down.

Boring but overdue.

But the Russell index needs a larger pullback. Desperately. That pains me to write because I love the Russell 2000’s outlook for 2021. Due to aggressive stimulus, friendly policies, and a reopening world, small-caps could be the biggest beneficiaries.

But the returns in the short-run need to cool off for a better entry point.

As tracked by the iShares Russell 2000 ETF (IWM), small-cap stocks have been on a rampage since November. Since the close on October 30, the IWM has gained nearly 49% and more than doubled the returns of ETFs tracking the larger indices. If you thought that the Nasdaq was red hot and frothy, you have no idea about the Russell 2000.

Since the close on January 29, the Russell has done just about the same again and gained 10.25%. It’s outperformed all the other major indices by a minimum of 4% in that period.

Not to mention, year-to-date, it’s already up a staggering 17.12%.

Small-caps are funny. They either outperform and underperform and can be swayed easily by the news. I foresaw the pullback two weeks ago coming for over a month, and unfortunately, I see the same thing happening now. But only for the short-term.

For now, though, the index is once again overbought.

While the RSI is thankfully below the 75 it had earlier in the week, it is still at a scorching 71.77 currently, and I can't justify calling this a BUY or HOLD right now. It's an excellent time to take profits.

SELL and take profits. If and when there is a deeper pullback, BUY for the long-term recovery.

Tech Remains Frothy

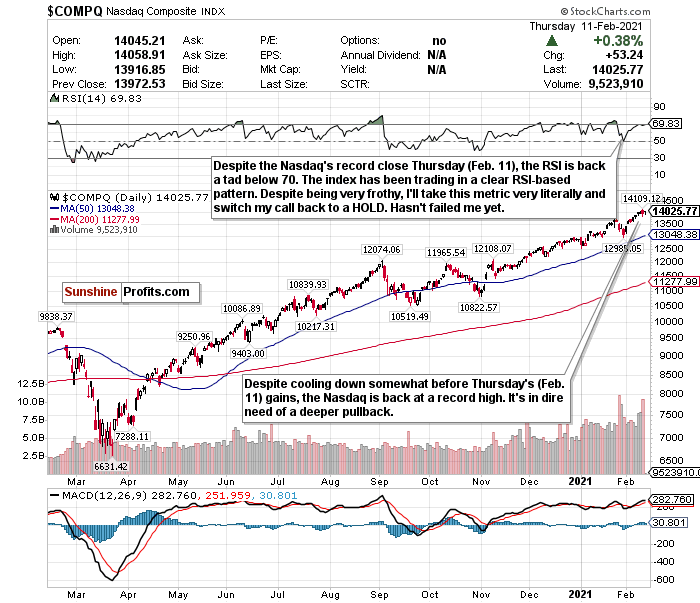

Figure 2- Nasdaq Composite Index $COMP

Tech is frothy, and valuations are absurd.

However, somehow, despite reaching another record close on Thursday (Feb. 11), the index isn't technically overbought. It's 0.17 away from being overbought according to the RSI, but it's still not overbought.

Why am I taking this so literally?

The Nasdaq is trading in a precise pattern based on the RSI.

I remain bullish on tech and the earnings that continue to crush estimates. I'm also incredibly bullish on subsectors such as cloud computing, e-commerce, and fintech for 2021.

But please monitor the RSI.

Since December, let's break down the Nasdaq and how it has reacted whenever the RSI has exceeded 70.

December 9- exceeded an RSI of 70 and briefly pulled back.

January 4- exceeded a 70 RSI just before the new year and declined 1.47%.

January 11- declined by 1.45% after exceeding a 70 RSI.

Week of January 25- exceeded an RSI of over 73 before the week and declined 4.13% for the week.

It also declined about 0.25% since exceeding a 70 RSI earlier in the week.

Every single time the RSI exceeded 70, I switched my Nasdaq call to a SELL.

The RSI is right at about 70, but technically it’s below it. I'm bullish but still concerned about valuations.

Goldman’s non-profitable tech index approaching an absurd 250% year-over-year performance just reflects my concerns and how circus-like this is becoming.

However, because of the Nasdaq’s precise trading pattern, I will follow it literally and make this a HOLD. If you took profits earlier this week when the RSI was above 70, good on you.

For an ETF that attempts to directly correlate with the performance of the NASDAQ, the Invesco QQQ ETF (QQQ) is a good option.

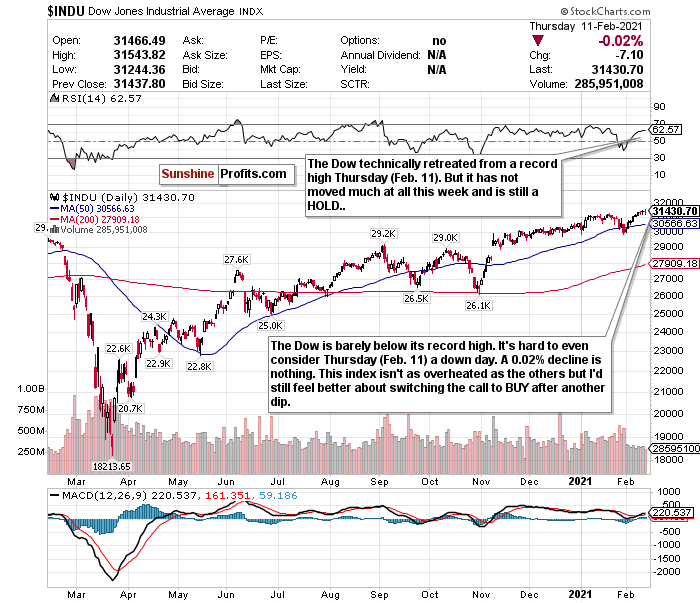

A Boring Week for the Dow

Figure 3- Dow Jones Industrial Average $INDU

The Dow still has momentum on its side, despite technically cooling off from record highs on Thursday (Feb. 11).

I really don’t know what else to say about the Dow this week besides “yawn.”

Maybe that’s not such a bad thing.

There are underlying concerns, and the market isn’t as calm as we think. But because the Dow has not heated up as much as the other indices, it is comparatively undervalued and therefore more attractive as a potential BUY.

After its downturn two weeks ago, the Dow was by far the index closest to oversold and in BUY territory. It saw a decline in 6 of 7 days and briefly saw its RSI plummet to a sub-40 level.

Since last week though, it has seen considerably more momentum, returned to positive territory for the year, and recovered all of its losses.

If you want to start initiating positions, go ahead. It’s at a solid entry point, especially considering that many analysts call for it to end the year at 35,000.

From my end, though, I still have some short-term questions and concerns and feel like the Dow could see another pullback.

My call on the Dow stays a HOLD, but this could change soon.

For an ETF that looks to directly correlate with the Dow's performance, the SPDR Dow Jones ETF (DIA) is a strong option.

Beware of Inflation

“The rich world has come to take low inflation for granted. Perhaps it shouldn’t.” -The Economist.

Outside of complacency and an overvalued market, my biggest concern has to be inflation.

Last Thursday (Feb. 4), the President of the Federal Reserve Bank of Kansas City, Esther George, told Bloomberg News that the Fed was still “far away” from achieving its goals, and that it was too soon to discuss scaling back its unprecedented massive bond-buying program.

Pay very close attention to the possible return of inflation by mid-Q2 or Q3.

George’s statement confirms that the Fed will allow the GDP to heat up and possibly overshoot in the medium-term. An aggressive stimulus could take effect this week too.

We will see what happens to GDP growth by the end of Q1 2021, but I no longer think it will sputter as much as I previously thought.

If at all.

The steepening of the yield curve reflects my inflation concerns too, and is the steepest it’s been in years. Long-term Treasury yields have risen faster than shorter-term yields, and could be a sign that Wall Street is betting on a speedier economic recovery compounded by inflation.

The 10-year breakeven rate reflects inflation risk as well.

If you are looking to the future to hedge against inflation, look into TIPS, commodities, gold, and potentially some REITs.

In the mid-term, I have BUY calls on the SPDR TIPS ETF (SPIP), the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), and the iShares Cohen & Steers REIT ETF (ICF).

Mid-Term/Long-Term

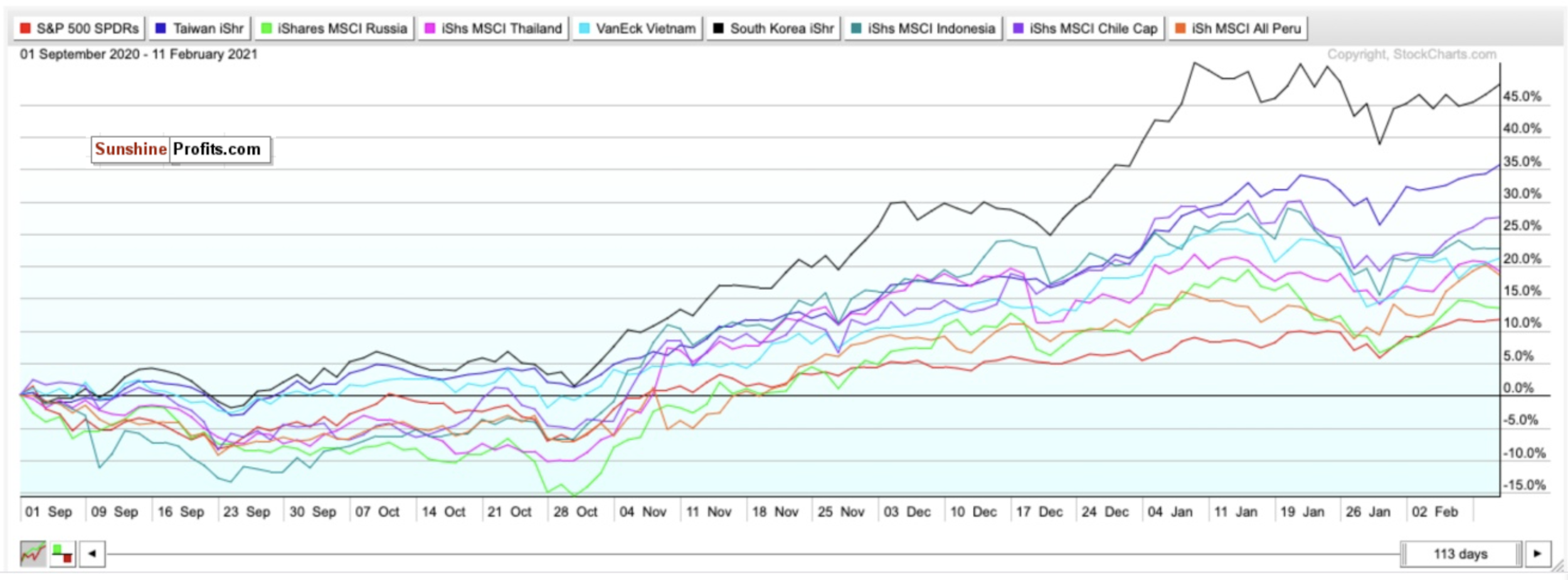

Taiwan, South Korea, and More for Best Emerging Market Exposure

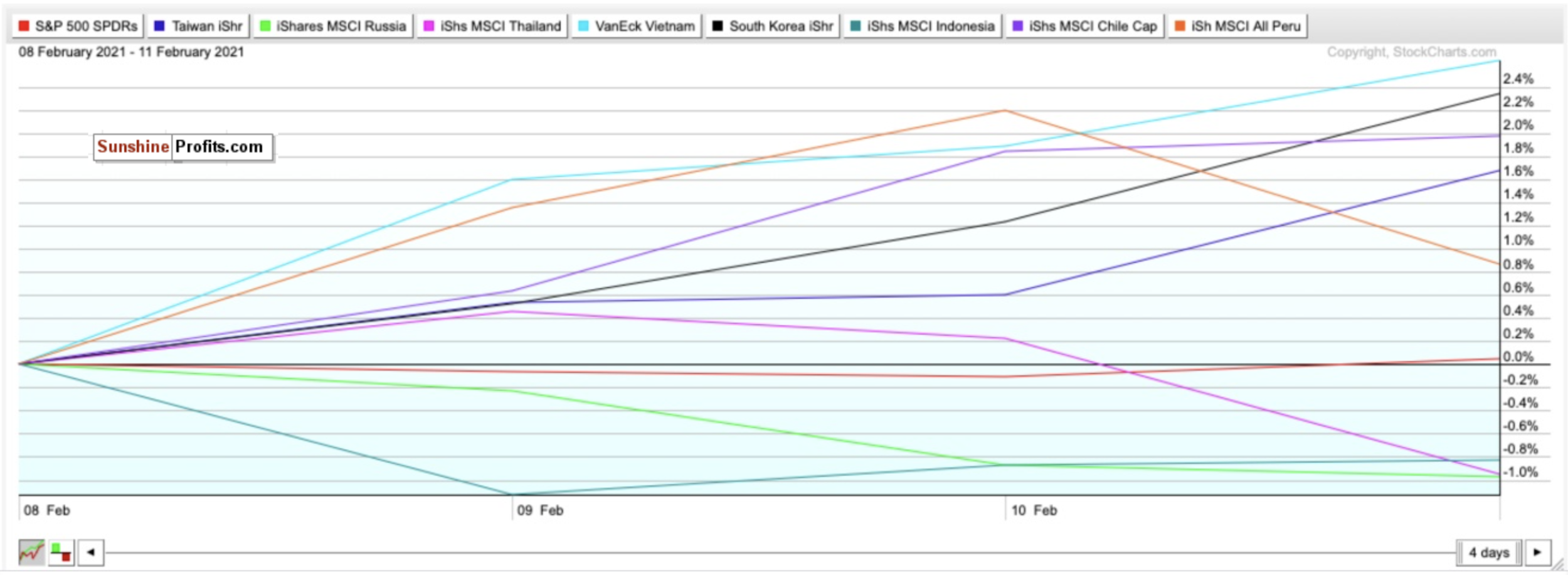

Figure 4- SPY, EWT, ERUS, THD, VNM, EWY, EIDO, ECH, EPU comparison chart- Sep. 1, 2020-Present

Since September, the SPDR S&P 500 ETF (SPY) has gained around 11.73%. When you compare that to my top emerging market picks for 2021, it has underperformed.

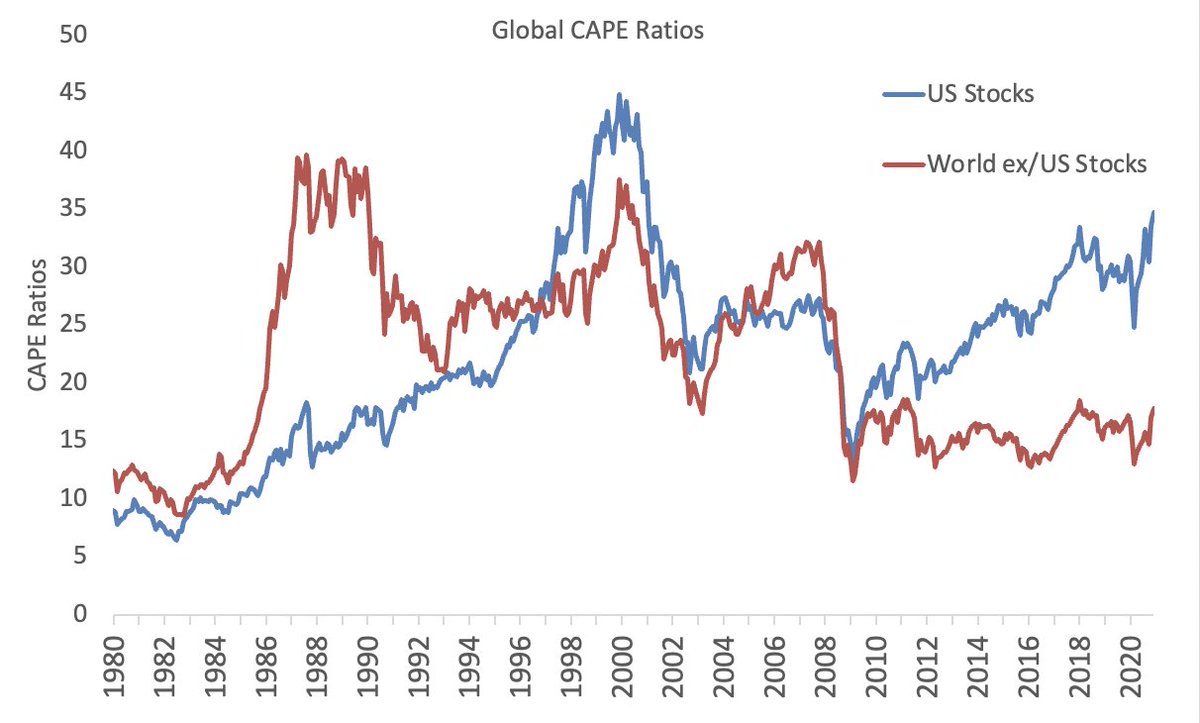

When you look at the CAPE ratio of U.S. markets compared to the rest of the world, this also seems like an awfully low bang for your buck.

The CAPE ratio takes real earnings per share (EPS) over ten years and smooths out fluctuations in corporate profits that can always occur throughout different business cycles. It’s also known as the Shiller P/E ratio.

Consider this too.

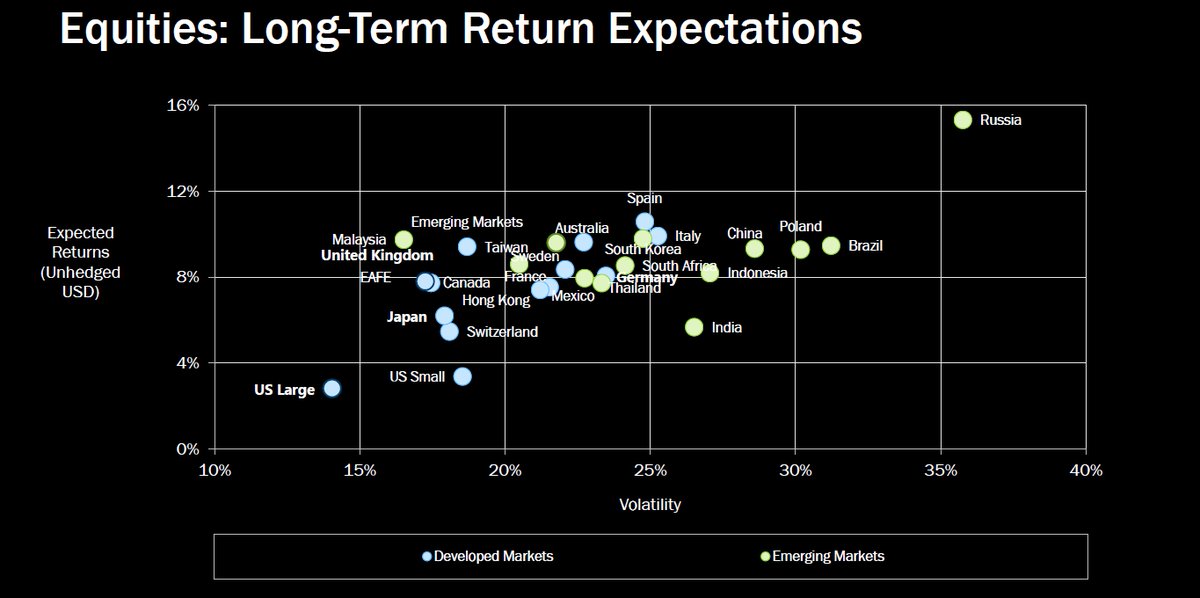

A surge in commodity prices due to a weakening dollar combined with shifting demographics could send emerging markets upwards in the long-term too.

PWC also believes that emerging markets (E7) could grow around twice as fast as advanced economies (G7) on average in the coming decades.

For 2021, the following are my BUYs for emerging markets and why:

iShares MSCI Taiwan ETF (EWT)- Developing country, with stable fundamentals, diverse and modern hi-tech economy, regional upside without China’s same geopolitical risks.

iShares MSCI Thailand ETF (THD)- Bloomberg’s top emerging market pick for 2021 thanks to abundant reserves and a high potential for portfolio inflows. Undervalued compared to other ETFs.

iShares MSCI Russia Capped ETF (ERUS)- Bloomberg’s second choice for the top emerging market in 2021 thanks to robust external accounts, a robust fiscal profile, and an undervalued currency. Red-hot commodity market (a big deal for a declining dollar), growing hi-tech and software market, increasing personal incomes. Compared to many other developed and emerging markets, Russia could have more than a 35% upside for its equities in the long-term as well.

VanEck Vectors Vietnam ETF Vietnam (VNM)-Turned itself into an economy with a stable credit rating, strong exports, and modest public debt relative to growth rates. PWC believes Vietnam could also be the fastest-growing economy globally. It could be a Top 20 economy by 2050.

iShares MSCI South Korea ETF (EWY)- South Korea has a booming economy, robust exports, and stable yet high growth potential. The ETF has been the top-performing emerging market ETF since March 23.

iShares MSCI Indonesia ETF (EIDO)- Largest economy in Southeast Asia with young demographics. The fourth most populous country in the world. It could be less risky than other emerging markets while simultaneously growing fast. It could also be a Top 5 economy by 2050.

iShares MSCI Chile ETF (ECH)- One of South America’s largest and most prosperous economies. An abundance of natural resources and minerals. World’s largest exporter of copper. Could boom thanks to electric vehicles and batteries because of lithium demand. It is the world’s largest lithium exporter and could have 25% of the world’s reserves.

iShares MSCI Peru ETF (EPU)- A smaller developing economy but has robust gold and copper reserves and rich mineral resources.

It’s been a relatively quiet week for emerging markets too. Week-to-date, Vietnam and South Korea have been the top performers, gaining over 2.3%.

When you consider that this is more than double what the S&P has done this week, though, maybe it’s not such a dull week after all.

Outside of the aforementioned country-specific ETFs, you can also BUY the iShares MSCI Emerging Index Fund (EEM) for broad exposure to Emerging Markets.

Long-Term

I remain convinced that the economic recovery is going better than expected as the progress in administering the vaccines improves. But as I keep saying, I still have concerns about complacency, overvaluation, and inflation.

For the long-term though, inflation is at the top of my list of biggest concerns.

We may be at the beginning of the end of the pandemic, and despite what could be a bumpy ride, 2021 should be a big year for stocks.

Small-caps, value stocks and cyclical stocks could significantly surge. I just will have a much better feeling for them in the second half of the year. I think we are overdue for another down week or two before entering a powerful buying opportunity for the second half of the year.

Summary

I am becoming increasingly optimistic for the second half of 2021.

However, until COVID-19 is brought under control, a battle between optimism and pessimism is inevitable.

But it’s getting better.

The crash and subsequent record-setting recovery we saw in 2020 is a generational occurrence. I can’t see it happening again in 2021. But as I said in the intro, I think a correction is inevitable.

We’re too frothy right now.

If there is a short-term downturn, though, take a breath, stay cool, and use it as a time to find buying opportunities. Do not get caught up in fear and most of all:

NEVER TRADE WITH EMOTIONS.

If you cautiously bought a little bit two weeks ago, you’re probably very happy right now. Even though the downturn to close out January wasn’t a full-blown correction, it was indeed an excellent opportunity to rebalance and add exposure.

That’s why I love down weeks—especially overdue ones.

Consider this too. Since markets bottomed on March 23rd, ETFs tracking the indices have seen returns like this: Russell 2000 (IWM) up 130.08%. Nasdaq (QQQ) up 97.27%. S&P 500 (SPY) up 77.47%. Dow Jones (DIA) up 71.36%.

In the long-term, markets always move higher and focus on the future rather than the present.

To sum up all our calls, I have a SELL calls for:

- The iShares Russell 2000 ETF (IWM)

To sum up all our calls, I have HOLD calls for:

- The SPDR S&P ETF (SPY),

- the Invesco QQQ ETF (QQQ), and

- the SPDR Dow Jones ETF (DIA)

I am more bullish for all of these ETFs for the second half of 2021 and the long-term.

I also recommend selling or hedging the US Dollar and gaining exposure into emerging markets for the mid-term and long-term.

I have BUY calls on:

- The iShares MSCI Emerging Index Fund (EEM),

- the iShares MSCI Taiwan ETF (EWT),

- the iShares MSCI Thailand ETF (THD),

- the iShares MSCI Russia ETF (ERUS),

- the VanEck Vectors Vietnam ETF Vietnam (VNM),

- the iShares MSCI South Korea ETF (EWY),

- the iShares MSCI Indonesia ETF (EIDO),

- the iShares MSCI Chile ETF (ECH),

- and the iShares MSCI Peru ETF (EPU)

Additionally, because I foresee inflation returning as early as mid to late 2021…

I also have BUY calls on:

- The SPDR TIPS ETF (SPIP),

- the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), and

- the iShares Cohen & Steers REIT ETF (ICF)

Before signing off, I just wanted to let you all know that moving forward, you can expect to see one of these newsletters every Monday, Wednesday, and Friday.

Hope everyone has a great weekend, and thank you all so much once again for reading.

Thank you.

Matthew Levy, CFA

Stock Trading Strategist