U.S. consumer spending rose 0.1 percent in February. What does it mean for the gold market?

Personal Income and Outlays Weak in February

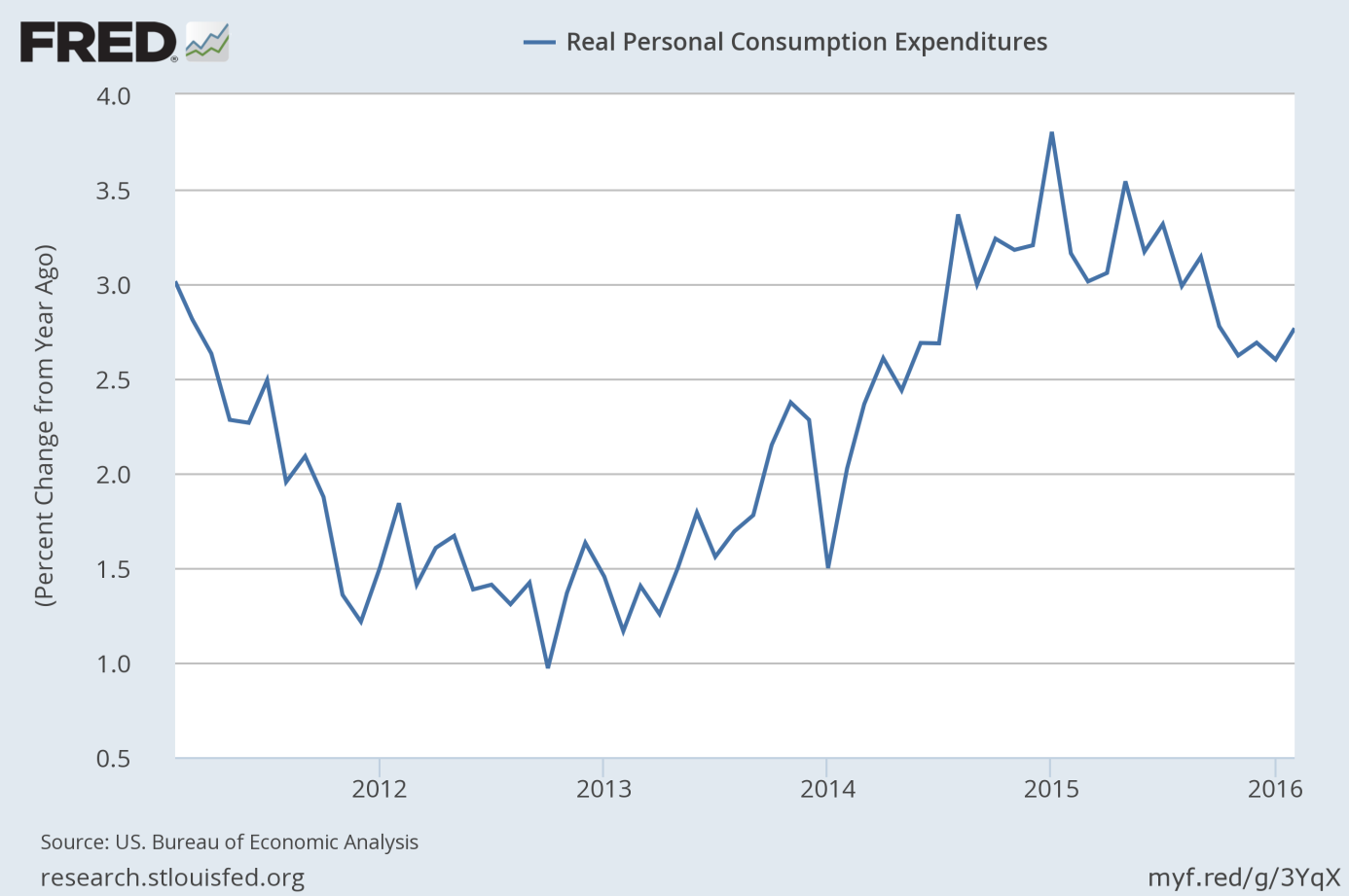

The recent personal income and outlays for February were weak and lowered the odds of a Fed hike in April. American consumers increased their spending only 0.1 percent in the last month. The number was in line with expectations, but the January data was unexpectedly lowered, from a 0.5 percent rise to only a 0.1 percent rise. It means that consumer spending is not going to pick up in the first quarter of 2016. Surely, real personal consumption expenditures accelerated slightly on an annual basis, but the annual pace of growth remained in the downward trend which started in January 2015 (see the chart below).

Chart 1: Real personal consumption expenditures from 2011 to 2016 (as percent change from year ago).

Turning to personal incomes, they rose 0.2 percent in February, however, the increase was driven mainly by rental income, interest income and transfers. Wages and salaries slipped 0.1 percent, for the first time since September 2015. It means that the U.S. labor market is not as strong as is believed and the FOMC will not see strong wage growth before its meeting in April.

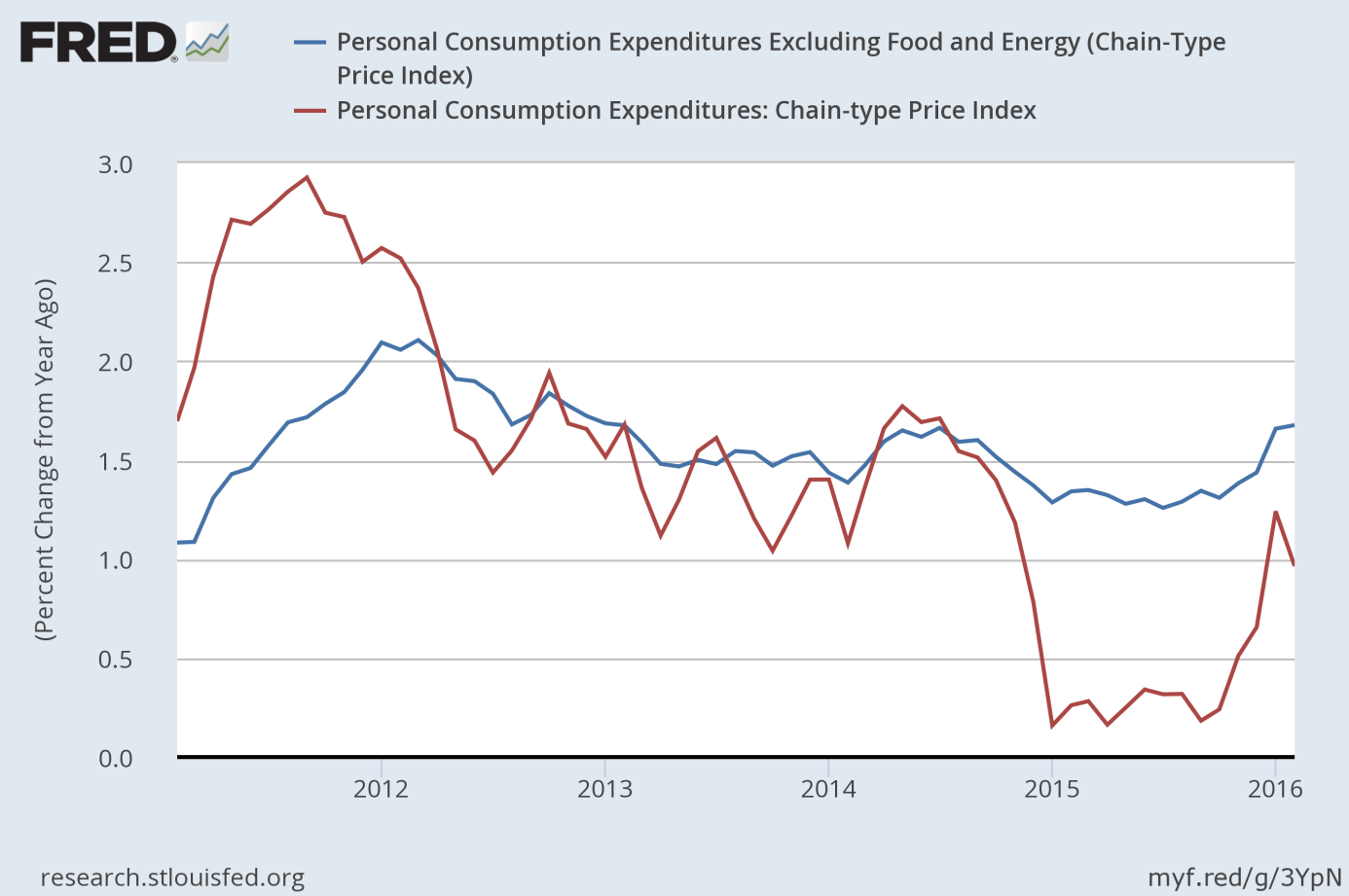

But perhaps the worst news for the Fed (and the best for gold) comes from the inflation part of the report. The price index for PCE decreased 0.1 percent in February, in contrast to an increase of 0.1 percent in January. The core PCE price index, which excludes food and energy, increased 0.1 percent, compared with an increase of 0.3 percent. On an annual basis, the PCE price index increased 1.0 percent (in contrast to a rise of 1.2 percent in January), while the core PCE price index increased 1.7 percent, just as in January. It means that inflationary pressure softened, as one can see in the chart below.

Chart 2: PCE Price Index (red line) and Core PCE Price Index (blue line) as a percent change from year ago, from 2011 to 2016.

February Personal Income and Outlays and Gold

The recent data on U.S. consumer spending, incomes and inflation resulted in downward revisions to forecasts for American GDP growth in the first quarter of 2016. Indeed, the GDPNow model forecast for real GDP growth in the first quarter of 2016 declined from 1.4 percent to merely 0.6 percent after the personal income and outlays release from the U.S. Bureau of Economic Analysis. It is a huge plunge and we could say that the report put the economy on a recession track again. It is good news for the gold market. Additionally, last week it transpired that U.S. orders for durable goods had plunged 2.8 percent in February (the third drop in four months), while orders for core capital goods declined 1.8 percent, implying that manufacturing continues to slide along the knife edge.

Consequently, the odds for a Fed hike in April are reduced. Surely, the chances were never high, but what matters are not absolute numbers, but trends. The decreased probabilities of hikes in the nearest futures should translate into higher gold prices. The decline in the price of gold before Easter was probably caused by the hawkish tone of several Fed officials and the doubled expectations of an April hike. Now, it turns out that the opinions about the U.S. economy “looking great” and “sufficient momentum evidenced by the economic data to justify a further step at one of the coming meetings” were purely nonsensical or just examples of wishful thinking. Thus, if the odds for a Fed hike plunge again, the price of gold should rise.

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview