Briefly: gold and the rest of the precious metals market are likely to decline in the next several weeks/months and then start another powerful rally. Gold’s strong bullish reversal/rally despite the USD Index’s continuous strength will likely be the signal confirming that the bottom is in.

Welcome to this week's Gold Investment Update.

Predicated on last week’s price moves, our most recently featured medium-term outlook remains the same as the price moves align with our expectations (and we not only took profits from two previous short positions, but we profited on the rebound, and expect more gains in the months ahead). On that account, there are parts of the previous analysis that didn’t change at all in the earlier days and are written in italics.

This week was all about pivot optimism, as weaker economic data and a depressed CPI helped alleviate investors’ interest rates fears. And with the bond market rally supporting the PMs’ fundamental outlooks, they too believe that easier monetary policy will create prosperity. However, the economic trends continue to align with our thesis, and the technicals also point to considerable downside. As such, we believe the bearish duo will dominate over the medium term.

We’ll begin today’s alert by dissecting the fundamentals, and then dive into the technical aspects that have proven so prescient over the last several months.

Bad Data Uplifts Gold

While inflation hysteria has rattled the Treasury market for some time, we warned that the pricing pressures are old news and recession risks are the next fundamental catalyst. As a result, while gold exudes pivot optimism, and assumes that lower interest rates are the new bull case, the fundamentals continue to align with our medium-term expectations. We wrote on Oct. 6:

No one was more bullish on inflation than us throughout 2021, as we warned that higher commodity prices, rental prices and consumer spending would push the headline Consumer Price Index (CPI) higher. However, with the leading data moving in the opposite direction now, the anxiety uplifting U.S Treasury yields is misguided…. So, while the crowd remains fixated on inflation, they’re likely behind the curve once again.

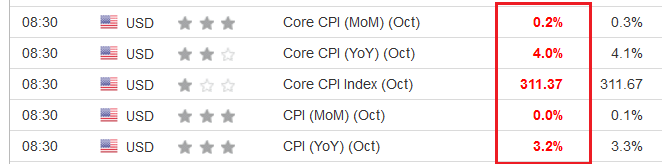

To that point, with the CPI missing across the board on Nov. 14, the economic cycle remains on schedule.

Please see below:

To explain, the inflation deceleration witnessed this week was far from a surprise. And while silver celebrated the weakness, investors believe that decent growth and subdued inflation make for a soft landing. However, that outcome is unlikely to materialize, and major downside should confront risk assets as the economic backdrop worsens.

Please see below:

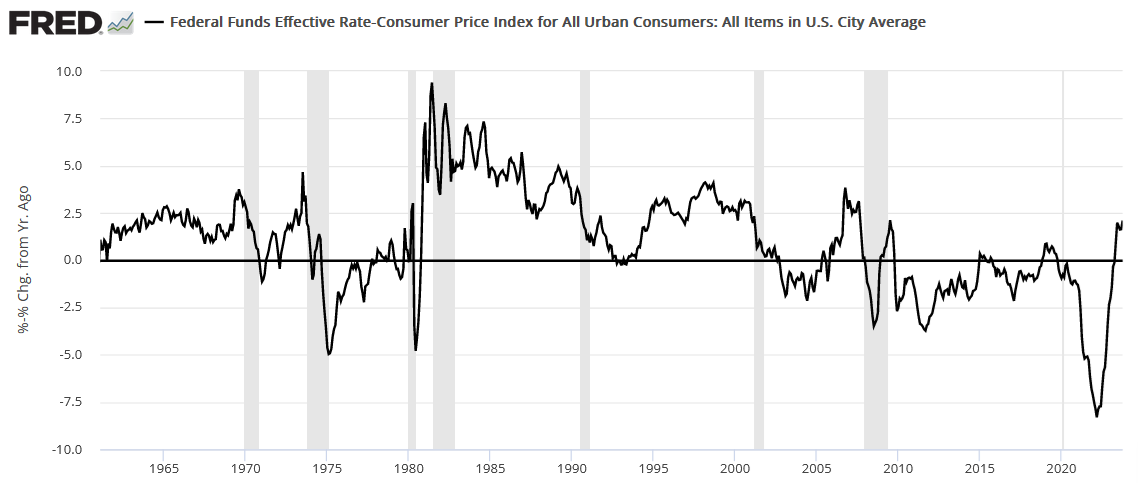

To explain, the black line above tracks the real U.S. federal funds rate (FFR). The metric subtracts the year-over-year (YoY) percentage change in the headline CPI from the FFR. And if you analyze the right side of the chart, you can see that it’s gone from deeply negative to north of 2%. Moreover, with the rise poised to continue as disinflation occurs, higher real interest rates should boost the USD Index and make their presence felt in the real economy.

Job Losses

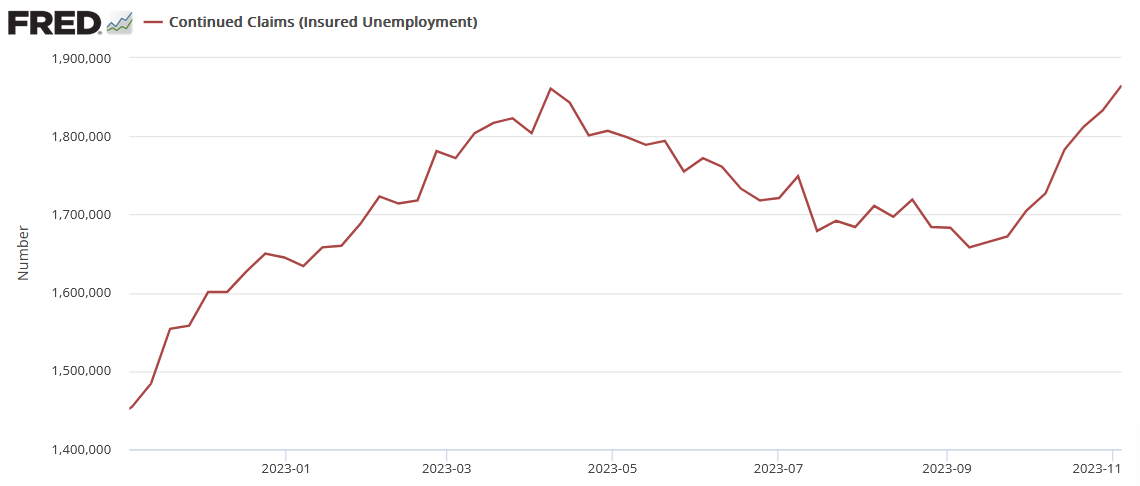

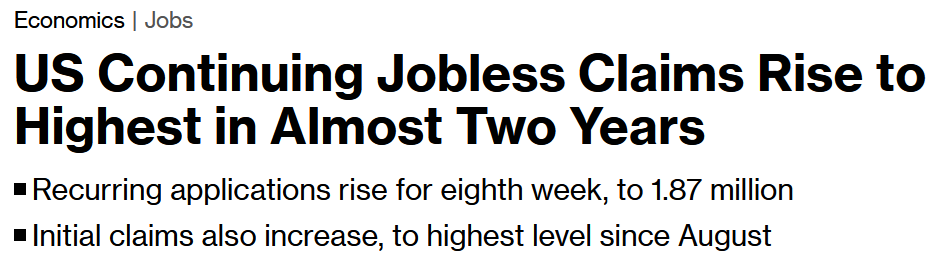

While the crowd ignores the medium-term ramifications, continued unemployment claims rose for their eighth consecutive week on Nov. 16. Furthermore, we warned that higher long-term interest rates would suffocate consumer spending, and the employment weakness should intensify in 2024.

Please see below:

To explain, continued jobless claims have been on a straight line higher recently, and the metric tallies the number of Americans that file for unemployment benefits more than once. And while crude oil has crashed along the way, the PMs should feel the pain as bad news becomes bad news once again.

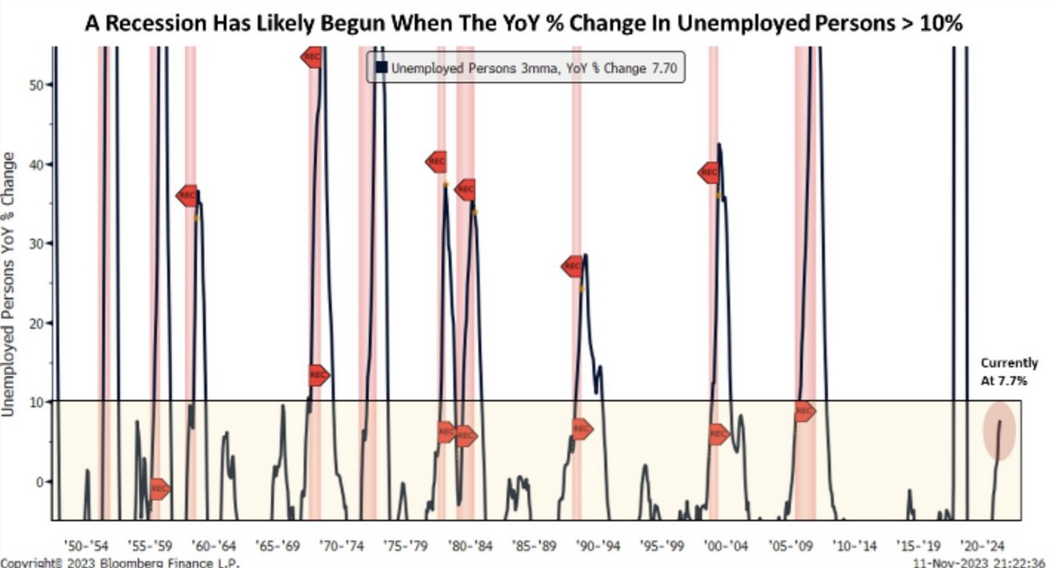

As further evidence, the recent rise in unemployed persons is reaching a threshold that aligns with historical recessions. Remember, the labor market is typically the last shoe to drop, and layoff headlines have been plentiful recently. As such, while soft landing optimism is always present prior to recessions, we believe a meaningful economic contraction is in the cards.

Please see below:

To explain, the black line above tracks the YoY percentage change in unemployed persons, while the vertical pink bars represent recessions. If you analyze the horizontal black line, you can see that U.S. recessions were triggered when the metric exceeds 10%. And with a reading of 7.7% on the right side of the chart, it shouldn’t be long until the >10% threshold is reached. Consequently, the PMs’ pivot optimism is likely living on borrowed time.

Overall, the fundamentals continue to follow our medium-term roadmap. We warned that inflation, a hawkish Fed and higher interest rates were the bear case in 2021/2022. Now, those catalysts have passed, and a recession should cause the next Minsky Moment that crushes the S&P 500. Remember, a recession is far from priced in, and a shift in sentiment should lead to meaningful drawdowns for several risk assets.

Silver’s Rock and a Hard Place

From war premiums to pivot hopes, silver sees sunny skies, as the international and domestic fundamental outlooks increase investors’ enthusiasm. However, the excitement is misguided, as silver often declines precipitously when recessions arrive. And with an economic downturn poised to bite in 2024, the white metal’s recent rally could be short-lived.

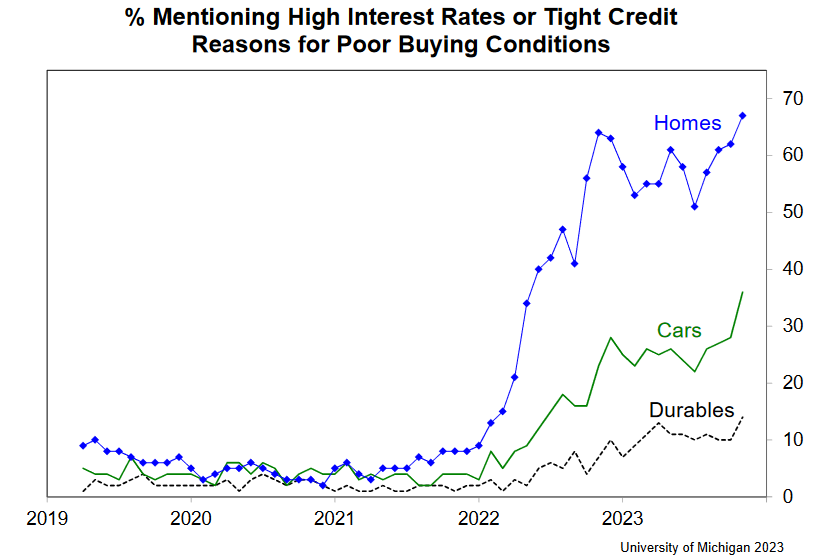

For example, the University of Michigan released its Index of Consumer Sentiment on Nov. 10. Director Joanne Hsu said:

“Consumer sentiment slipped for the fourth straight month, falling 5% in November. While current and expected personal finances both improved modestly this month, the long-run economic outlook slid 12%, in part due to growing concerns about the negative effects of high interest rates.”

Please see below:

To explain, the blue, green and black lines above track the percentage of respondents mentioning high interest rates or tight credit conditions as reasons for avoiding purchasing homes, cars or other durable goods. If you analyze the right side of the chart, you can see that all three lines have risen recently, which highlights the impact of higher long-term interest rates. Moreover, we cautioned this would occur on Oct. 6. We wrote:

As for the medium-term outlook, we’ve warned on numerous occasions that higher long-term interest rates (not the FFR) create recessions. And with the recent rate surge dominated by the long end, the chickens should come home to roost in the months ahead.

So, while gold bounces and silver remains uplifted for now, their price action could look much different in 2024.

Unhappy Holidays

While the ‘bad news is good news’ narrative continues to percolate throughout the financial markets, that should shift as bad economic data worsens. And with cyclical assets like oil showcasing immense fear, mining stocks and silver should play catch-up over the medium term.

Please see below:

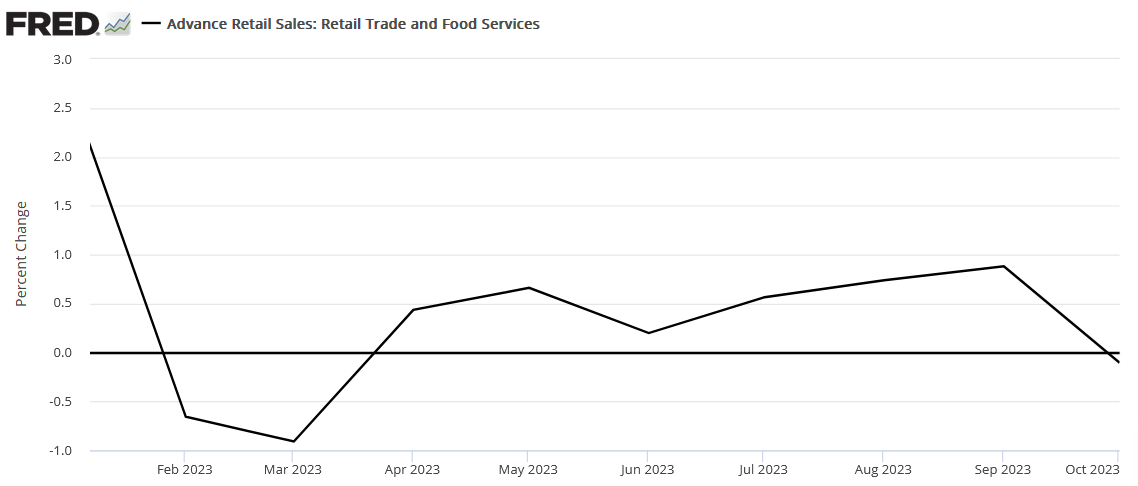

To explain, the drop on the right side of the chart above highlights how U.S. retail sales went negative month-over-month (MoM) for the first time since March. And with weak holiday sales poised to bite as well, the trend should continue as the unemployment rate rises.

Please see below:

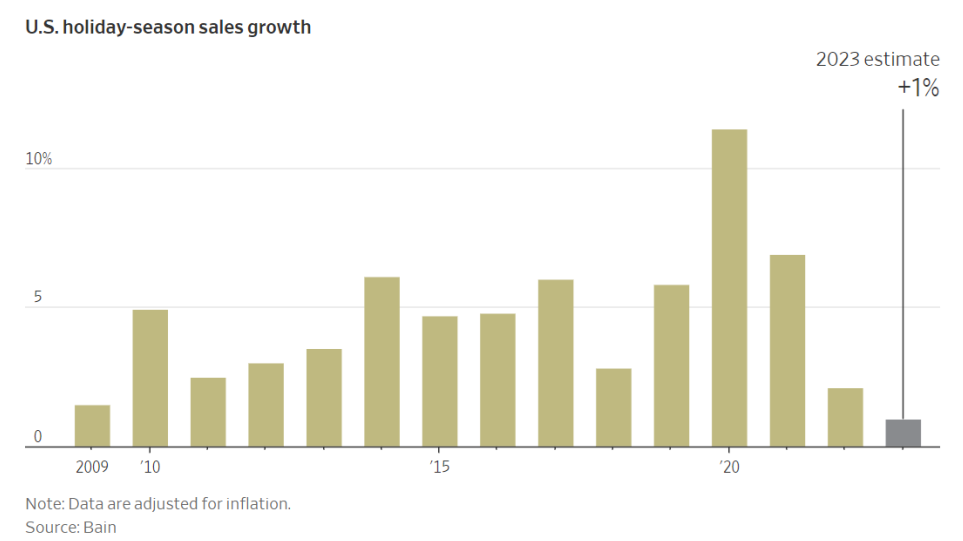

To explain, Bain Capital projects that U.S. holiday sales growth will come in at 1% YoY in 2023, which would be the lowest print dating back to 2009. Consequently, the ominous expectation highlights the tepid economic backdrop, and a continued decline should culminate with a 2024 recession, which is bullish for the USD Index.

As further evidence, Walmart – the largest U.S. retailer – released its third-quarter earnings on Nov. 16. CEO Doug McMillon said:

“In the U.S., we may be managing through a period of deflation in the months to come. And while that would put more unit pressure on us, we welcome it, because it’s better for our customers.”

CFO John David Rainey added:

“Our events have been strong. We’ve been pleased with those. Halloween was good overall. But in the last couple of weeks of October, there were certainly some trends in the business that made us pause and kind of rethink the health of the consumer.”

Thus, while we warned repeatedly that a recession, not inflation, has become the primary risk to financial assets, the medium-term outlook should be fraught with peril.

Overall, little has changed to alter our fundamental outlook. Higher interest rates are having their desired effect, and boom-and-bust cycles have occurred several times throughout history. As such, with over-optimism dominating the U.S. economy in 2021 and 2022, a major reversal should occur in 2024. And if that happens, mining stocks, silver, and the S&P 500 could suffer substantial declines.

The Bottom Line

Right now, risk assets assume that the U.S. economy will weaken to the point where it eradicates inflation, but not weaken enough to cause a recession. The theory is highly unrealistic, and also contrasts historical precedent. Therefore, if (when) the narrative is debunked, a profound re-pricing of gold, silver and mining stocks should sink the trio to new lows.

In conclusion, the PMs rallied on Nov. 16, as pivot optimism dominates for the time being. But, the good times are unlikely to last, and we think more pain confronts risk assets before long-term buying opportunities emerge.

Technically Speaking

While the PMs benefited from a few fundamental rallies, please note that the technicals remain profoundly bearish. Moreover, economic data releases rarely have lasting power, as one month’s or week’s optimism can turn to next month’s or week’s pessimism. Consequently, gold, silver and mining stocks’ medium-term downtrends are more relevant than a short-term data reprieve.

Furthermore, the charts have been highly accurate in recent months, and my comments from Nov. 16 explain why the current noise is much more semblance than substance. I’ll start with quoting what I wrote in the intraday Gold Trading Alert:

Earlier today, I wrote that many positive surprises have already happened for the precious metals market and that now it was time for them to move lower – as the normalcy and regular sentiment get back. And yet, we saw another surprise – this time from the initial jobless claims, which were higher than expected.

The precious metals sector moved higher, but… What we see so far today serves as yet another indication that a bigger move to the downside is about to follow. The two additional signs are:

- Very strong performance of silver – I already commented on it previously, but today we see another show of the same thing, which makes the bearish implications even clearer.

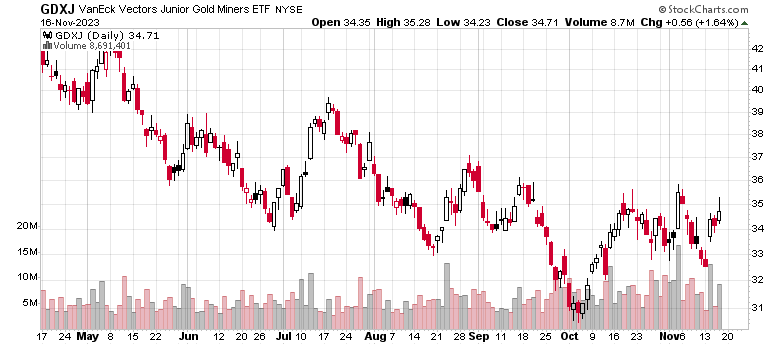

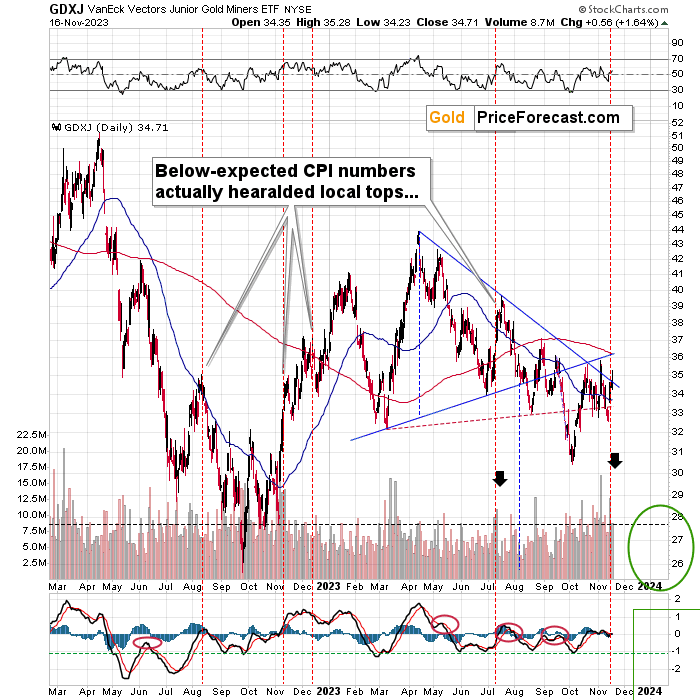

- The GDXJ is reversing, creating a shooting star reversal candlestick.

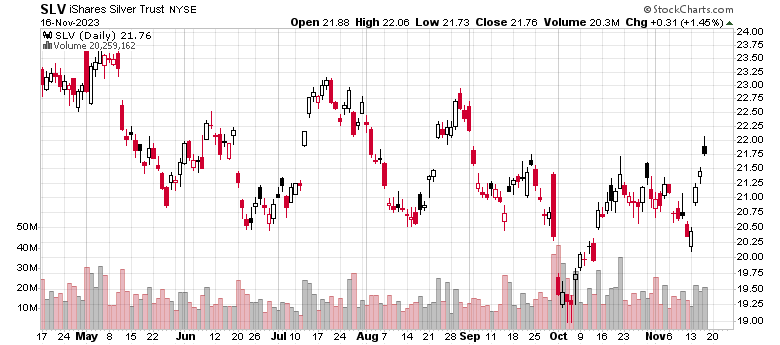

Silver moved clearly above its October highs, and while it already reversed, it’s still obvious that it outperformed on an immediate-term basis.

Junior miners are not above their October highs, and the reversal is quite clear. Of course, the session is not over yet, but so far, the reversal has slightly bearish implications. Silver’s outperformance has strongly bearish implications, so together they serve as a very strong bearish indication – which is in line with what I wrote in today’s regular analysis.

All in all, the outlook for the precious metals market remains bearish, and it’s likely that the profits on our short positions in junior miners will increase in the following weeks.

The thing that I’d like to add after the end of yesterday’s session is that the volume that accompanied GDXJ’s reversal was big enough to make the reversal important, and the fact that silver reversed before the end of the day as well. It still ended visibly higher, so what I wrote above remains up-to-date.

The same goes for my previous comments, with the addition that the same goes for the initial jobless claims.

That’s all, folks. Whatever “bullish news” for gold was likely to happen has likely already happened. And you know what happens next? Declines.

The nonfarm payrolls were lower than expected, and miners rallied. Temporarily only, but still.

The CPI numbers were also lower than expected, and the precious metals sector moved higher. Once again, most likely temporarily, based on the analogy to the previous similar situations.

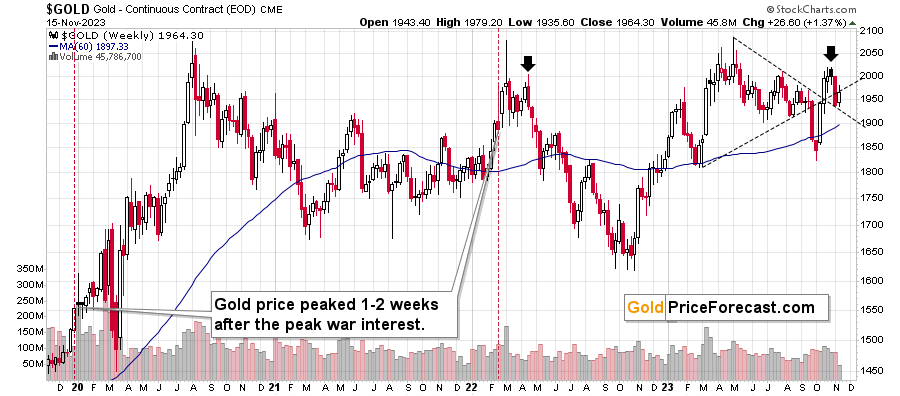

And the situation in the Middle East? It continues to be very tense. And yet, the concern with “war” in general is already after its peak and is now declining.

All three above factors should have made the precious metals sector move much lower. And did they? The situation in the Middle East did cause gold to move higher, as it’s a safe-haven asset, but gold didn’t move above its 2022 high when the analogous concerns regarding Ukraine arose.

And… both wars are still taking place, and gold still failed to hold above $2,000. It’s trading pretty much where it topped 12 years ago, while silver and gold stocks are not even close to their 2011 highs.

Massive bull market in the precious metals sector?

No.

It was a local response to military conflicts in the case of gold. Silver and mining stocks continue their downward trends in a clear manner. The same goes for platinum and palladium. Gold is the exception.

Now, since the bullish news already happened, what kind of surprises await the precious metals market in the following days? Bearish ones. People already extrapolated the bullishness to the following days, and the precious metals sector likely moved too high too fast. Especially that… the real rates moved higher based on the recent move lower in CPI and core CPI.

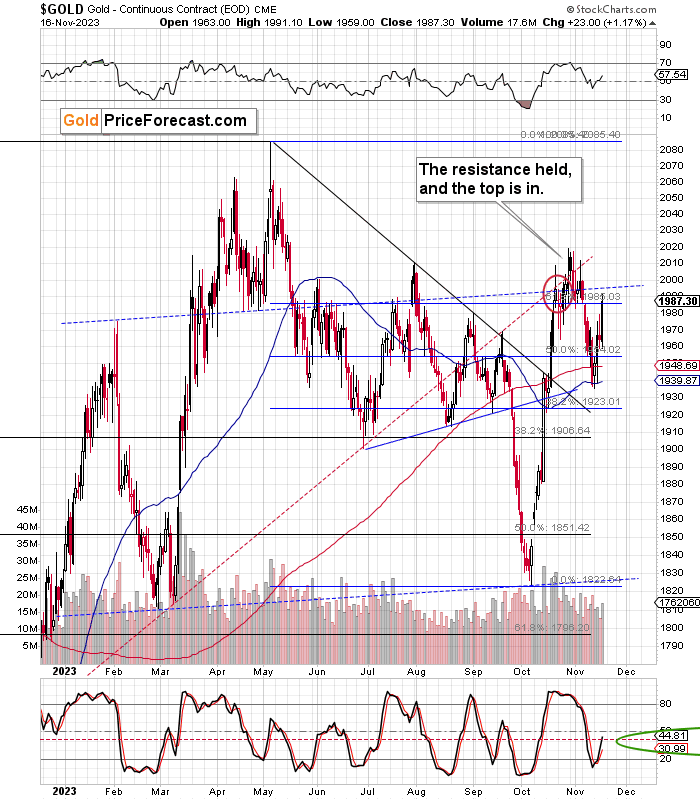

From the weekly point of view (after three sessions in the case of this week), we see that gold simply corrected after moving to its declining support line, but it failed to hold above its rising resistance line – at least based on Wednesday’s data. Gold then moved higher on Thursday, but since the week is not over yet, it’s still quite likely that gold will close back below the rising dashed line.

This means that the recent move higher is likely a regular breather.

Please note the moments marked with arrows. That’s when gold topped after the concern with “war” (based on Google Trends’ data) peaked. Any back-and-forth movement here should be viewed as smoke and mirrors before the big move happens. And the big move is likely to be to the downside – just like what we saw in 2022.

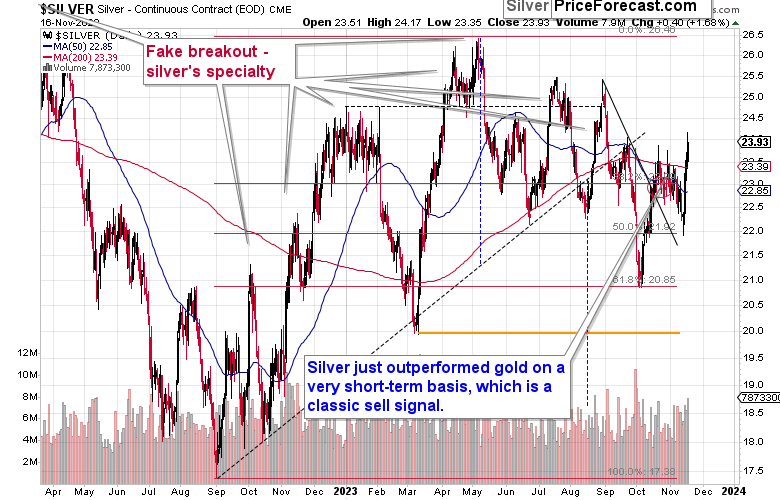

From the short-term point of view, we see that gold moved higher but it did not reach its October highs.

The interesting thing about this recent upswing is how much silver rallied compared to the rally in gold.

The white metal soared and moved above its October highs! Gold was nowhere close to those levels. In other words, silver just outperformed gold on a very short-term basis. If you’ve been following my analyses for some time, you know that this is something that we often see right before bigger declines.

Mining stocks, however, did not move above their October high this week. This makes silver’s strong performance stand out even more – making it even more bearish.

Plus, the fact that the GDXJ tried to move above the declining resistance line – and failed – once again is also telling. It seems that after the triple top, junior miners are finally ready to slide.

The vertical, dashed lines on the above chart mark the situation when CPI statistics were below expectations.

- Back in August 2022, it was practically right at the top, which was followed by a sizable decline.

- In November 2022, it was right before a local top.

- In December 2022, it was practically right at the local top.

- In July 2023, it was right before a local top, which was followed by a sizable decline.

What are the implications? They are unclear for the immediate term (1-3 days), bearish for the short-term (1-2 weeks), and likely bearish also for the medium-term (several weeks).

The reason for the latter is that the medium-term trend in the mining stocks is clearly down, and the fact that junior miners clearly underperformed both gold and the general stock market in recent weeks, confirms this bearish gold forecast.

Besides, the reaction of the precious metals market was weak in general – at least when compared to what happened in stocks and in the USD Index.

Remember when, on Nov. 6, I told you that negative surprises in nonfarm payrolls are not necessarily a bullish thing despite the market’s initial reaction? The GDXJ plunged shortly thereafter. It seems that we are in a similar situation with regard to the CPI numbers.

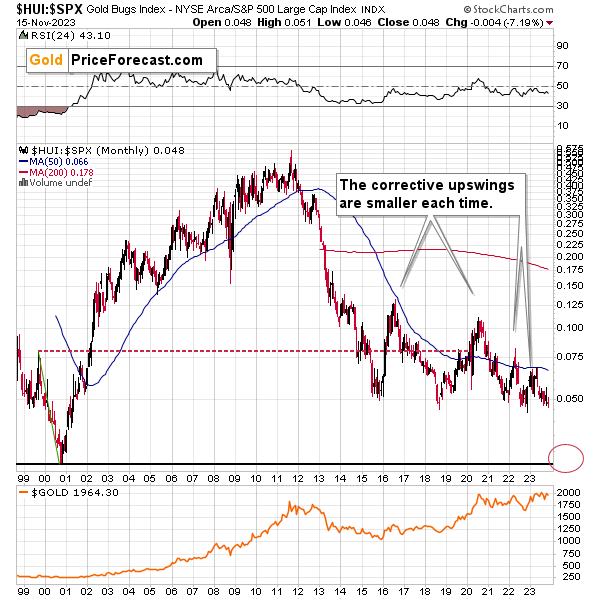

Moreover, comparing prices of gold stocks to the general stock market reveals a medium-term downtrend.

The chart above features the HUI Index to S&P 500 Index ratio. It’s been in a long-term decline for over a decade, and it’s been declining in recent years and months as well.

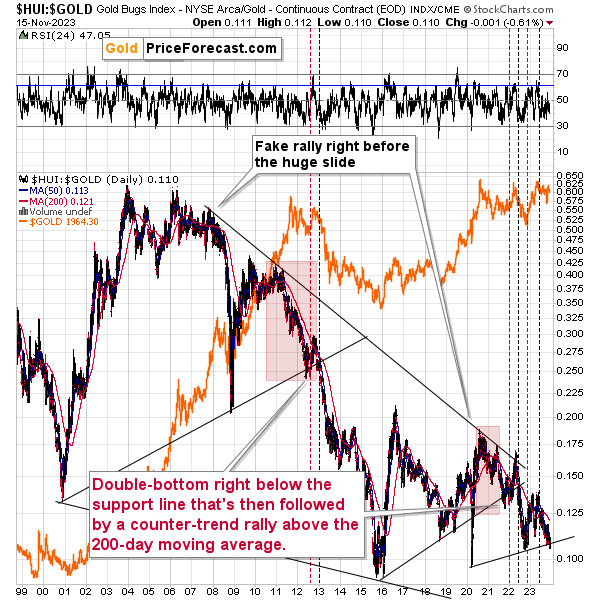

The chart below shows that gold stocks have been weak relative to gold, too.

The interesting thing about the HUI Index to gold ratio is that it just broke below it is rising, medium-term support line. This indicates weakness and suggests that lower values of gold, silver, and mining stocks are in store for the following weeks and months.

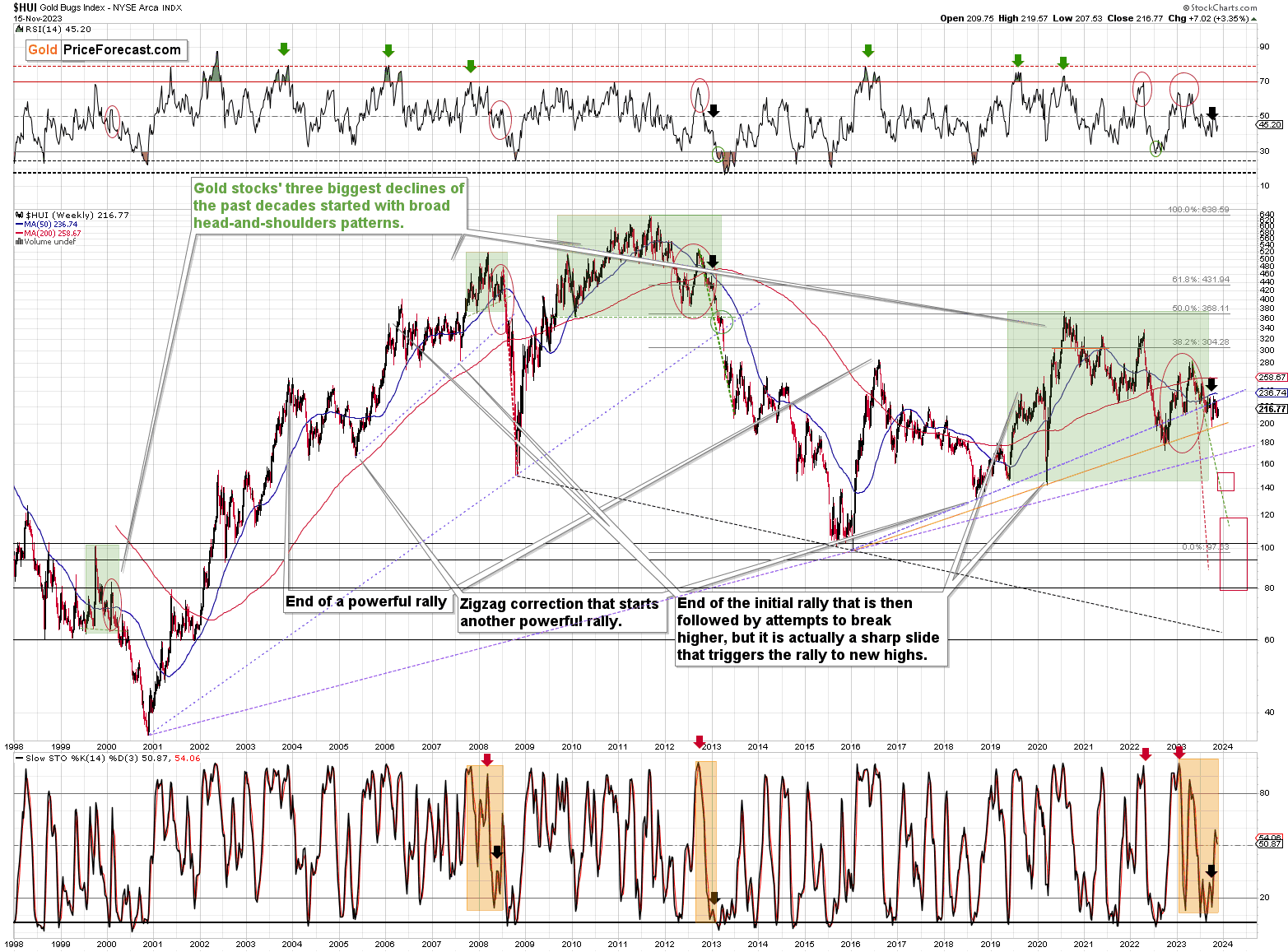

Let’s check the chart of the HUI Index – a classic proxy for gold stocks.

The recent move higher is barely visible from the long-term point of view. In reality, it’s just a consolidation that followed a breakdown below the rising, long-term support line.

The fact that this breakdown was not invalidated is bearish on its own. It looks like we’re about to see a much bigger decline than what we saw so far this year. The current breakdown can be compared to the breakdowns that we saw in 2013 and in 2008. Enormous declines followed in both cases.

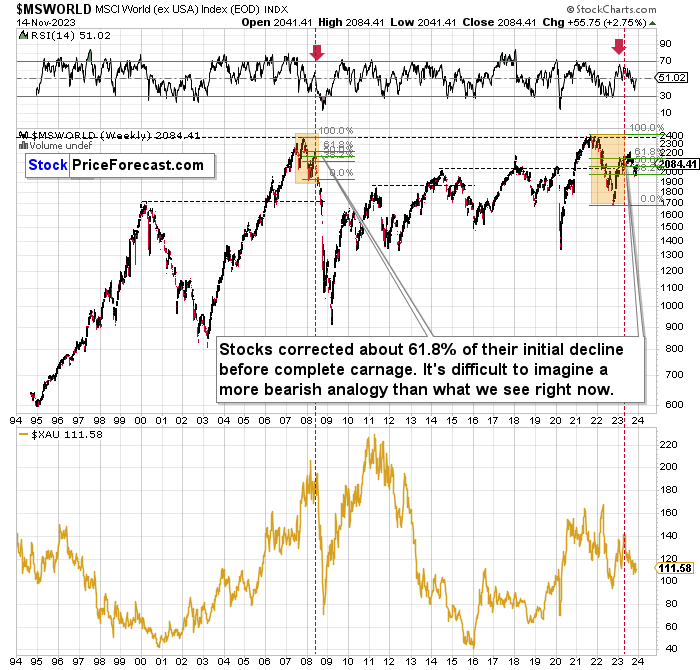

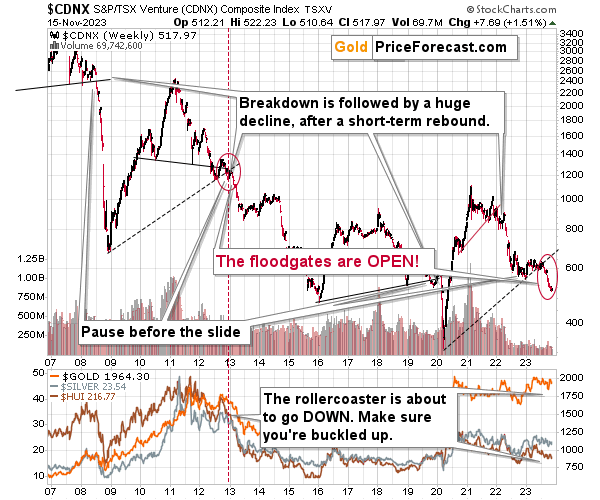

Speaking of analogies to 2008, let’s not forget that we also have them in the case of world stocks and junior mining stocks’ proxy – the Toronto Stock Exchange Venture Index.

The current situation in world stocks is very similar to what we saw in 2008, right before the biggest part of the decline. Stocks started their decline from pretty much the same price levels, then they declined, then they corrected about 61.8% of the initial decline, and now they are moving lower once again.

The lower part of the chart shows how extremely bearish the implications were for the mining stocks – the same is the case right now.

The TSXV continues to point to much lower prices in the following weeks. The current situation is very similar to what we saw in 2008 and 2013, right before the enormous declines in the precious metals sector – and especially in mining stocks.

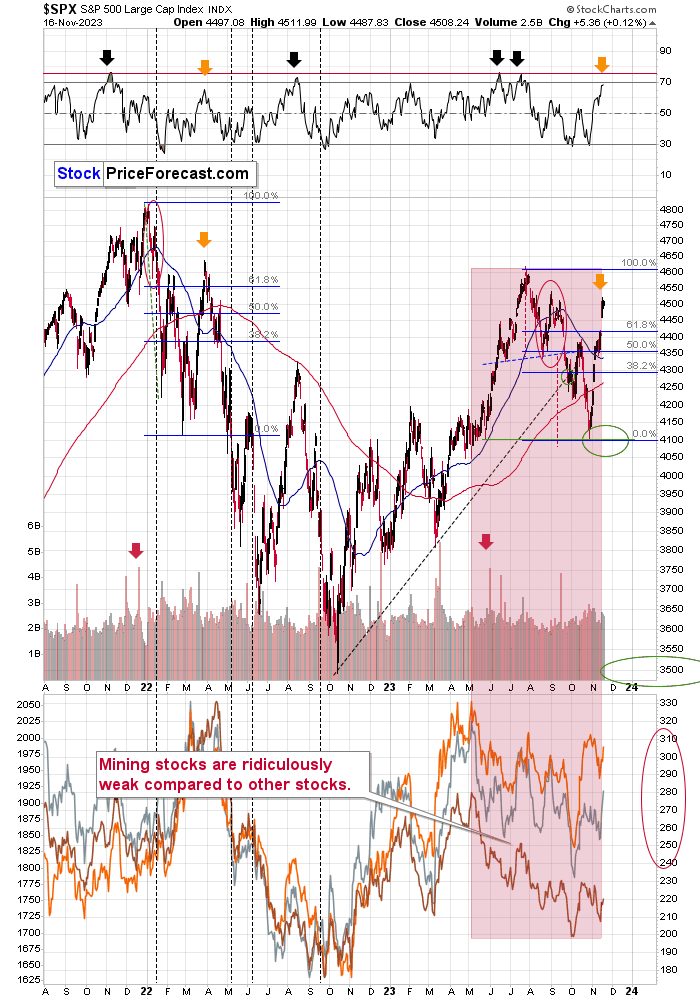

From the short-term point of view and looking at the general stock market, the situation is similar to what we saw in early 2022, which is remarkable, as it similarly extends beyond the chart. After all, it was also then when the “war concern” peaked.

Technically speaking, stocks moved above their 61.8% Fibonacci retracement level, while the RSI level based on the S&P 500 moved close to 70. This situation is very similar to what we saw in March 2022. The rally was sharp, and it was just as fake as it was sharp. Stocks plunged shortly thereafter then and the same thing is likely right now (or soon).

What does it mean for the precious metals sector? Stocks moved in tune with the precious metals sector recently, but in particular, they are strongly linked to the performance of junior mining stocks. And the latter ignored a large part of the stocks’ rally, anyway. The point is, once stocks decline, junior mining stocks are likely to truly slide, increasing our profits in a really substantial manner.

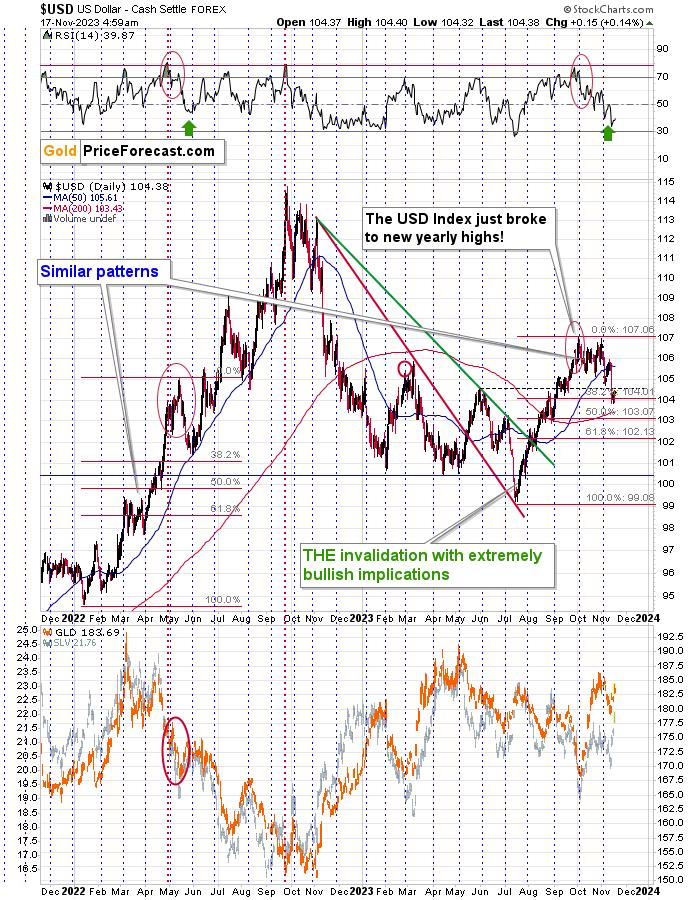

Meanwhile, the situation in the USD Index has the “ok, that was it” written all over it. The corrective downswing appears to be over.

The USD Index declined significantly this week, but did it change the outlook? Not at all. In fact, the USDX is already moving back up.

The USDX moved to its 38.2% Fibonacci retracement based on the recent big rally, and that’s a normal thing for a market to do in order to cool down some of the more emotional investors.

The mid-2022 correction also ended when the USD Index moved close to its 38.2% Fibonacci retracement, so I’d say that this kind of decline is not bearish but rather in tune with the previous bullish pattern.

Also, while the USD Index moved to a new monthly low, gold and miners are far from their monthly highs. So, yes, the precious metals market is weak here, even though it might not be apparent based on the size of yesterday’s rally.

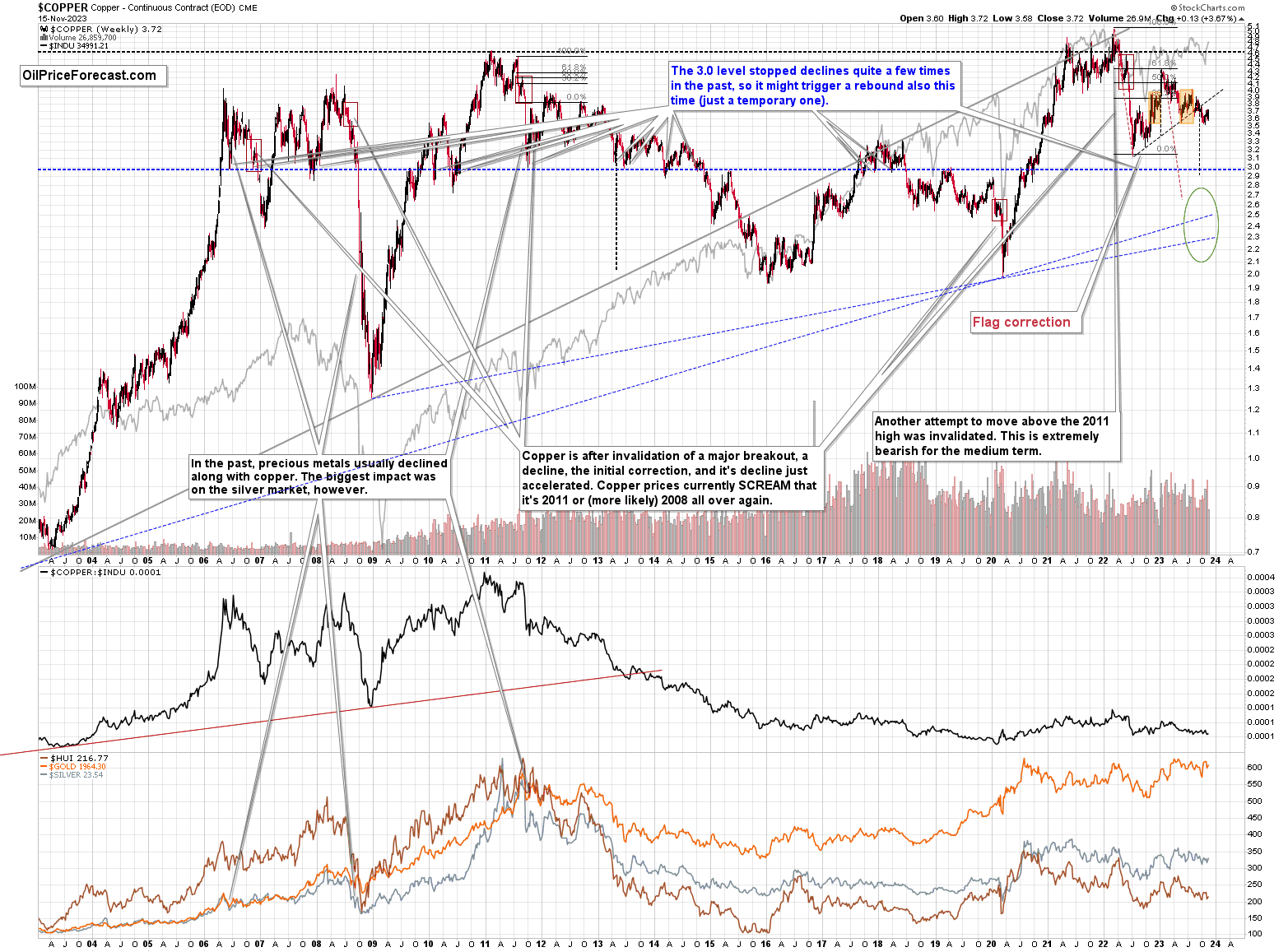

Finally, let’s consider what the commodities markets are telling us. We’ll use copper as a proxy for the commodity sector.

In short, copper already verified its breakdown below the rising resistance line, and the recent small upswing didn’t change anything regarding the validity of the breakdown. The next big move in the price of copper is likely to be to the downside. The initial medium-term target is just at / slightly below $3. And then – after a pause – even lower, in the $2.3 - $2.6 range.

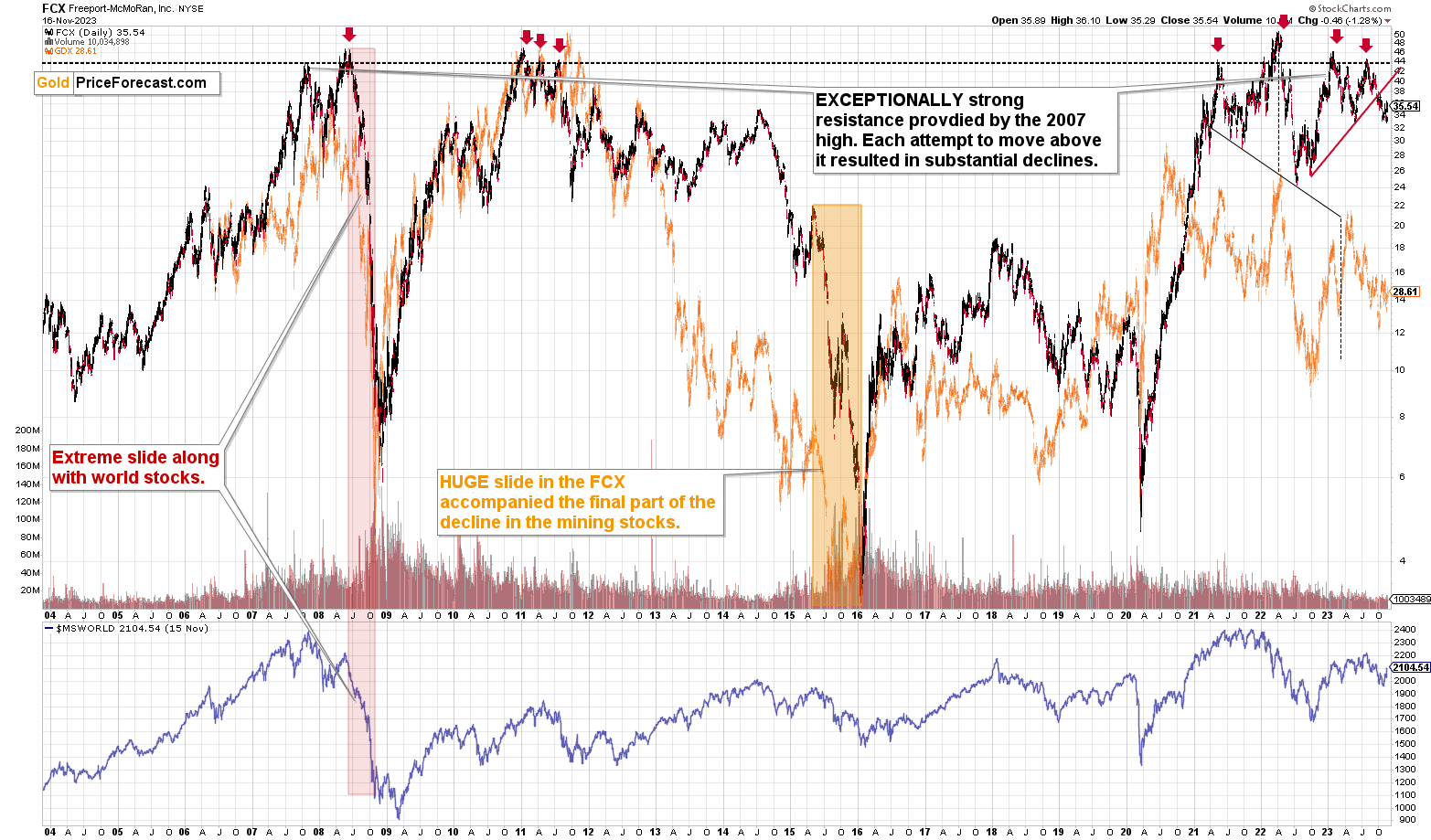

The FCX – one of the key gold and copper producers – moved higher this week, but it’s likely just a breather based on the fact that FCX already declined to its previous yearly lows. The trend remains down, and it seems that we’ll see a breakdown to new lows any day or week now.

Please keep in mind that FCX has been one of the weakest stocks in recent weeks, and the final parts of the rallies on the stock market are often characterized by laggards’ catch-up. This is what we are probably seeing in FCX right now. I don’t view it as bullish.

All in all, it seems that our profits from the short positions in the GDXJ are likely to increase soon. And FCX is likely to slide as well.

= = =

If you’d like to become a partner/investor in Golden Meadow, you’ll find more details in the above link.

Overview of the Upcoming Part of the Decline

- It seems that the recent – and probably final – corrective upswing in the precious metals sector is over.

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

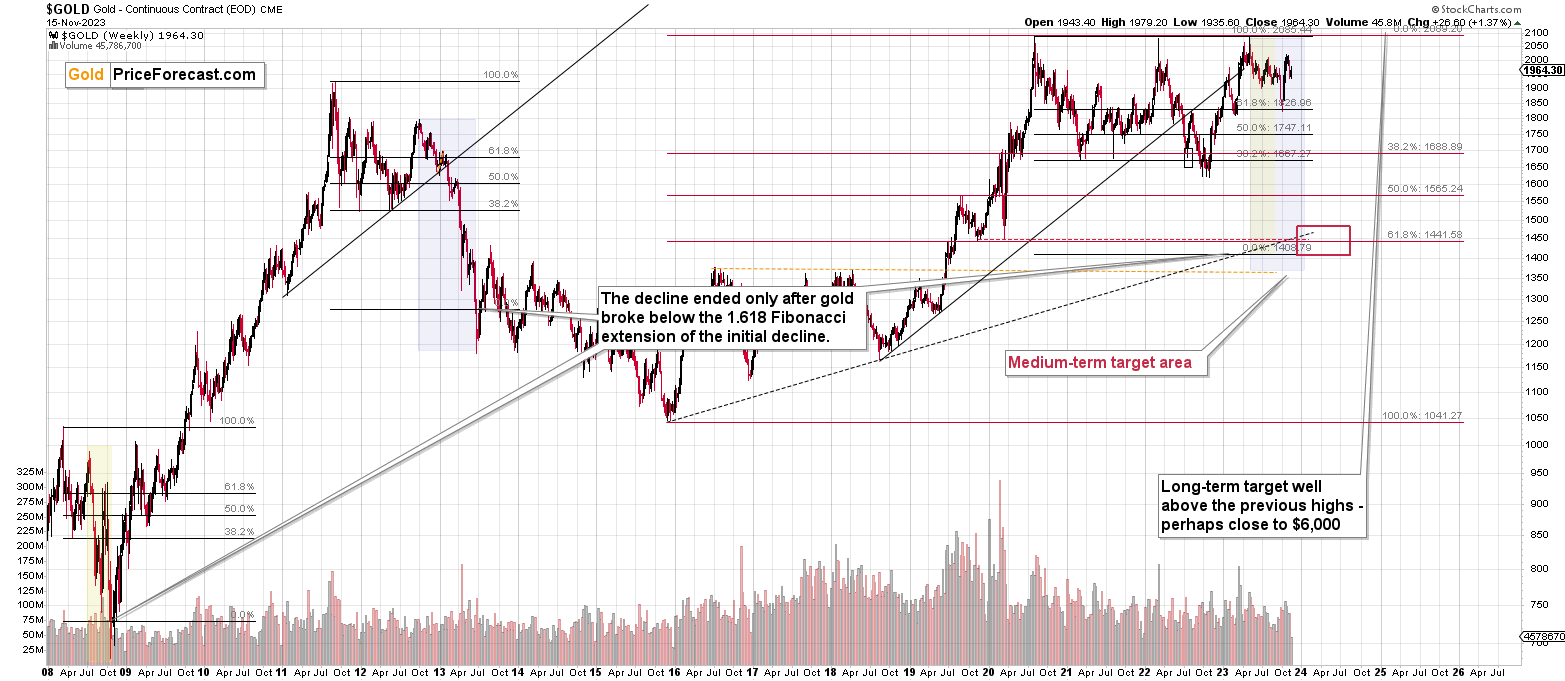

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Letters to the Editor

Please post your questions in the comments feed below the articles if they are about issues raised within the article (or in the recent issues). If they are about other, more universal matters, I encourage you to use the Ask the Community space (I’m also part of the community) so that more people can contribute to the reply and enjoy the answers. Of course, let’s keep the target-related discussions in the premium space (where you’re reading this).

Summary

To summarize, the medium-term trend in the precious metals sector remains clearly down, and it seems that the corrective upswing is already over and the profits on our current short position are going to increase. We just caught the 11th profitable trade in a row – congratulations. The outlook for the short positions in junior miners and in the FCX remains very favorable.

===

Finally, since 11th profitable trade in a row is such a great piece of news (and the same goes for the fact that the current short position is already profitable), here’s… Even more great news! The possibility to extend your subscription for up to three years (at least by one year) with a 20% discount from the current prices is still open.

Locking in those is a great idea not only because it’s perfect time to be ready for what’s next in the precious metals market, but also because the inflation might persist longer than expected and prices of everything (including our subscriptions) are going to go up in the future as well. Please reach out to our support – they will be happy to assist you and make sure that your subscription days are properly extended at those promotional terms. So, for how many years would you like to lock-in your subscription?

To summarize:

Short-term outlook for the precious metals sector (our opinion on the next 1-6 weeks): Bearish

Medium-term outlook for the precious metals sector (our opinion for the period between 1.5 and 6 months): Bearish initially, then possibly Bullish

Long-term outlook for the precious metals sector (our opinion for the period between 6 and 24 months from now): Bullish

Very long-term outlook for the precious metals sector (our opinion for the period starting 2 years from now): Bullish

As a reminder, Gold Investment Updates are posted approximately once per week. We are usually posting them on Monday, but we can’t promise that it will be the case each week.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

Moreover, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don’t promise doing that each day). If there’s anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief