The yield curve followed suit of the Fed and also inverted. Inverted yield curve is a sign of an incoming recession, they say. However, what is the background of this yield inversion and how will gold react to its emerging story?

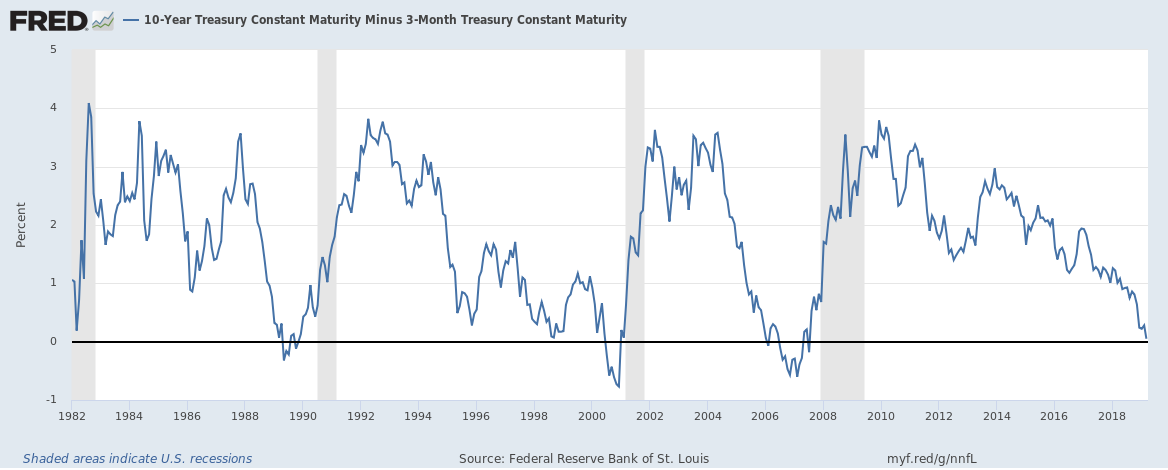

Red alert! Or, actually, a yield alert! After months of worries, the yield curve has finally inverted. Well, maybe not the whole yield curve, but one of its segment. As one can see in the chart below, the spread between US 10-year Treasury and 3-Month Treasury dived on Friday to its lowest since 2007.

Chart 1: Spread between US 10-year Treasury and 3-Month Treasury from March 2018 to March 2019

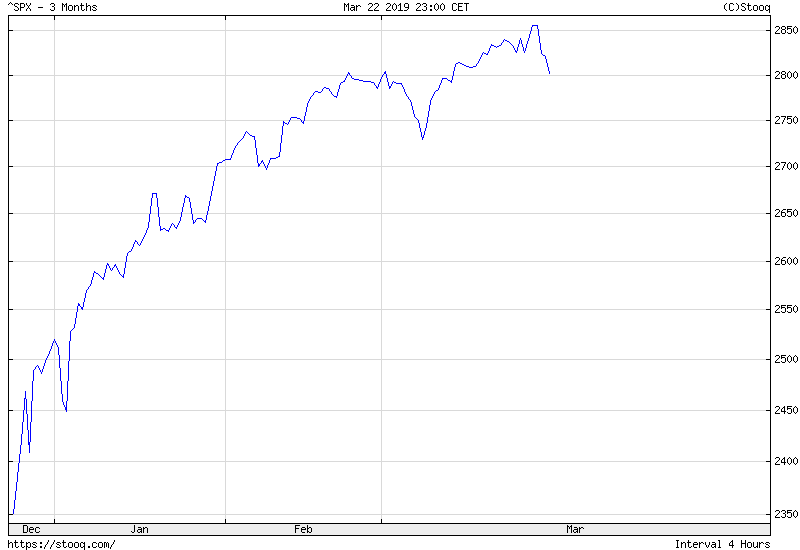

The fact that long-term bond yields fell below the short-term interest rates rattled investors. The S&P 500 dropped 0.8 percent to 2,801 on Friday, the biggest plunge since January, as the chart below shows. The reason is that, as we explained in the March edition of the Market Overview, the inversion of the yield curve is considered to be one of the most reliable recession indicators.

Chart 2: S&P 500 Index from December 2018 to March 2019

Indeed, the yield curve inversions have preceded each of the last seven recessions, including the Great Recession. Therefore, it is not surprising that investors panicked and that the VIX surged.

But are these fears really justified? Is a recession coming? Well, not necessarily. Although the yield curve inversion is relatively reliable, it still produced a few false positives (for example, an inversion in late 1966).

Moreover, because of the international capital flows and quantitative easing, the underlying determinants of the yield spread today are materially different from the determinants that generated yield spreads during prior decades. We mean here that without the central banks’ purchases of assets (the BoJ and the ECB still buy or reinvest maturing securities into new bonds), the yield curve would be steeper and it would not signal a recession.

However, the most important is the reason behind the recent inversion. Investors should always be careful when interpreting economic indicators and dig into their underlying drivers. You see, the yield curve may invert either because the short-term rates are running high or because the long-term rates are running low. Historically speaking, the yield curve inverted when the Fed tightened its monetary policy by raising the short-term interest rates which triggered recessions at some point.

But the yield curve inverted on Friday after the dovish FOMC meeting on Wednesday, when the US central bank signaled longer pause in further tightening (no hikes this year) and announced the end of shrinking its balance sheet as early as in September. The Fed’s volte-face scared investors who followed suit and cut their outlook for future economic growth. Consequently, the long-term rates declined. After all, if the Fed can really see around corners, and it doubled down on its dovish stance, it is better to move from risky assets and allocate funds into Treasuries (or other safe havens, such as gold).

In others words, the latest yield curve inversion did not fit the classical story when the Fed raises the short-term interest rates to combat inflation. This is why we believe that the yield curve has lost some of its prediction power. Precious metals investor should take this into account in their investment decisions.

Implications for Gold

The bottom line is that the yield curve has inverted. It should add to the fears of recession, which should help the yellow metal in the near future. However, the effect might be temporary. In the March edition of the Market Overview, we have analyzed several other recession indicators (such as the unemployment rate) and they do not blink red. And in the April report we will present important arguments in favor of the view that the current global slowdown will be only temporary. So, we believe that it’s probably premature to press the panic button.

For us, one of the two scenarios is true. The first one is that Mr. Powell just made an error. He wanted to please the Wall Street, but he over-delivered on a dovish side, raising unnecessary fears. When the US central bank realizes its mistake, it will adjust its stance and calm the markets. The positive effects on gold will vanish, then.

Second, the Fed knows something we are not aware of. We signaled this possibility on Thursday edition of the Gold News Monitor. If it sees recession around the corner, gold could shine for longer. However, given the solid state of the US economy, it’s more probable that Mr. Powell and his colleagues noticed something scary – but unfolding outside America, for example, in the Eurozone or China. In such a scenario, gold may still benefit from safe-haven demand, but gains will be limited by the US dollar’s appreciation.

Hence, gold is likely to go up in the short-term and end the year with better results than in 2018. But it should not rally until we see a US recession. It is still premature to herald it, so medium-term gold bulls should hold their horses. We will monitor carefully the situation and we are ready to change our stance as soon as we will see a sustained yield curve inversion and other recession indicators also blinking red. Stay tuned!

If you enjoyed the above analysis, we invite you to check out our other services. We provide detailed fundamental analyses of the gold market in our monthly Market Overview reports and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron, Ph.D.

Sunshine Profits‘ Gold News Monitor and Market Overview Editor