A lot has changed in American policy since the last edition of the Market Overview. Generally speaking, Donald Trump ceased to be Donald Trump. What do we mean and how can this affect the gold market?

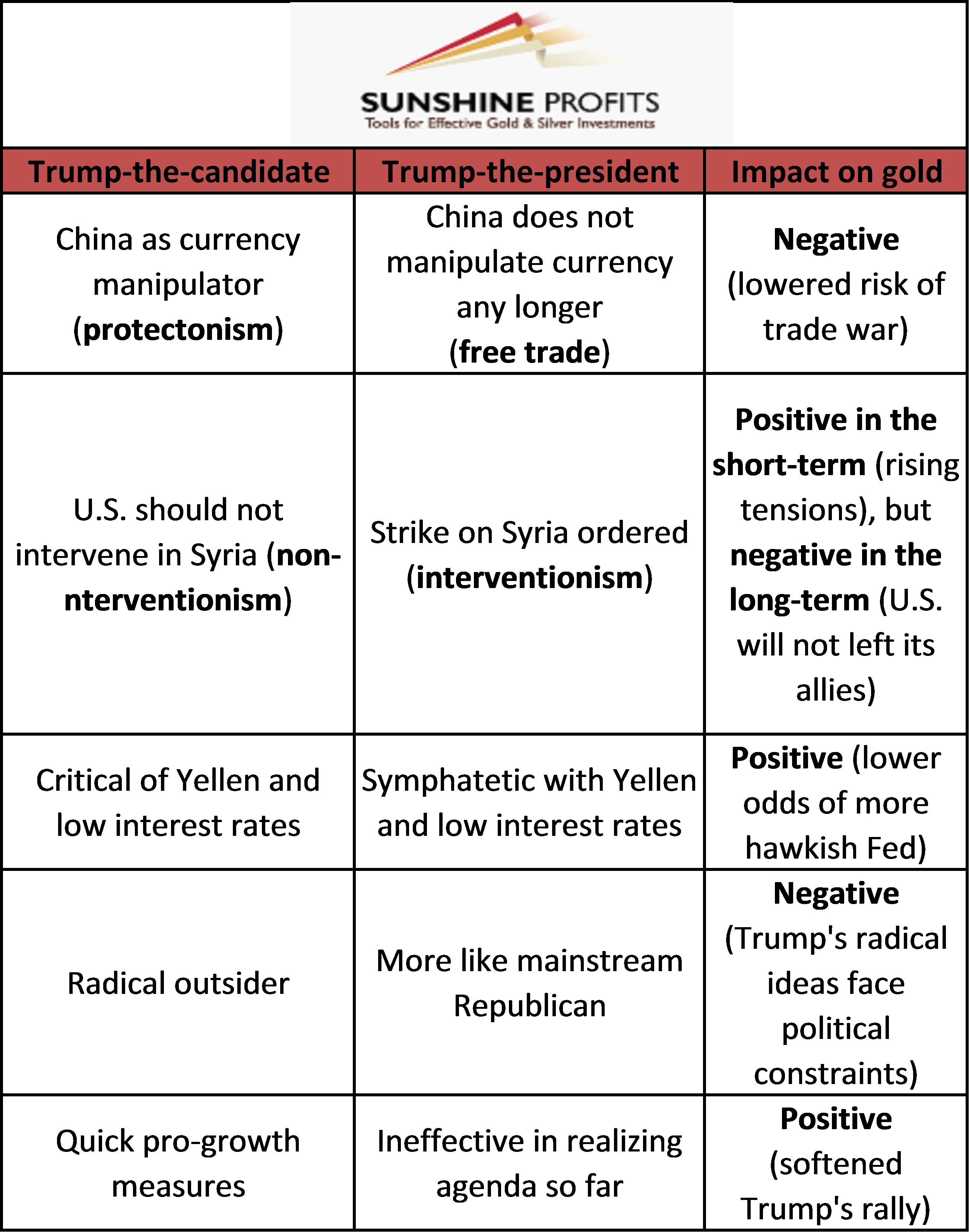

First of all, on April 7, POTUS ordered to bombard Syria. As a reminder, during the campaign Donald Trump argued that the U.S. should not get involved in the conflict. The recent strike signals a retreat from his isolationist tendencies (importantly, Trump has declared recently that NATO was no longer obsolete). It should be welcomed by America’s allies, but the impact on gold is harder to determine. On the one hand, a less isolationist stance means higher odds that the USA will intervene if necessary. When the USA is on guard, other countries could sleep more calmly, which reduces global uncertainty. On the other hand, a more aggressive approach in foreign conflicts may imply more conflicts and geopolitical incidents. If such occur, they should increase the safe-haven demand for gold, but their positive impact should be limited to the short-term.

Second, in an April's interview with the Wall Street Journal, Trump changed his view on China. Before the election, he promised to label that country a ‘currency manipulator’ on the first day of presidency. But he told reporters that his administration will not do it, as China has stopped manipulating its currency recently. This change lowers odds of imposing tariffs on Chinese imports and diminishes the likelihood of a trade war. From an economic point of view, it’s a positive shift, but it’s bad for the gold market, as Trump’s flip-flop reduced the biggest uncertainty related to his presidency.

Third, in the same interview, the new president reversed his position on the Fed. During the election campaign, Trump used to criticize the unconventional measures of the U.S. central bank, but now he seems to like Yellen and her dovish stance. He said: “I do like a low-interest rate policy, I must be honest with you.” This is exactly what we predicted in the December edition of the Market Overview, writing that “although Trump-the-candidate was highly critical of Yellen, we believe that Trump-the-president may soften his positions.” Indeed, this is precisely what happened: Trump became more supportive of the Fed, which may be bad for gold, as it reduces the risk of conflicts and radical changes in the U.S. monetary policy. However, Trump’s preference for low interest rates implies lower odds of a more hawkish Fed in the future – as a reminder, Yellen’s term expires in 2018 – which is positive for the yellow metal.

Given Trump’s unpredictability and erratic decisions, some would say that the recent shifts are not relevant, because POTUS can reverse his position again, faster than anyone would realize. We totally agree that the capricious nature of Donald Trump remains an important risk, which should provide some support for the price of gold. And there is still the danger that Republicans and Trump will introduce the border tax.

However, the change is clear, as one can see in the table below. Trump-the-president is less radical than Trump-the-candidate. Actually, given the nature of democratic elections and Trump’s low approval rating, the turn towards more mainstream positions should not be surprising. The recent reversals signal that Trump is going away from his nationalistic and protectionist stance, while adopting a more mainstream approach towards military interventions, free trade and even the Fed’s policies.

Table 1: Trump-the-president vs. Trump-the-candidate.

In a way, Trump transformed himself into typical Republican (well, almost). As a reminder, gold performed better under Democrats, but these statistics are the result of gold’s unprecedented rally under Carter’s presidency. Anyway, the recent Trump shifts imply that protectionist risks have eased recently on the margin. This is good for risky assets, while negative for gold.

Having said that, investors should remember that not only risks associated with Trump have been vanishing, but so also hopes related to his pro-growth policies. Surprisingly, it turned out that Trump is neither a monster, nor a miracle worker. He is just a president who lacks a support in Congress. Therefore, as we have repeatedly argued, both positive and negative expectations were overestimated, so they should scale back, partially neutralizing their impact on the gold market. We will say more about the reflation trade and Trump’s rally in the next part of this report.

If you enjoyed the above analysis and would you like to know more about the impact of the current macroeconomic trends and geopolitical uncertainty on the gold market, we invite you to read the May Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It's free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview