Visit our archives for more gold & silver articles.

The Wall Street Journal had an especially colorful metaphor to describe what has happened to the price of gold that fateful week when gold tumbled 13% in the two sessions through April 15, the biggest drop in 33 years.

“Slick with the viscera of crushed gold bugs, the world’s trading floors look even more treacherous than usual.”

Do we feel like crushed bugs? Not at all.

Do we think that the bull market in gold is over? Not yet.

Do we know that markets can be cruel? Hell, yes.

Needless to say the gold bears have been feeling lately like they have landed in a huge vat of honey. They are smug, to say the least. But we see this as an opportunity to get back into gold at a lower price and in the meantime, we made money shorting some of the downside (and on the pullback). We are not alone. Jim Rogers, who foresaw the start of a commodity secular bull market in 1999, said this may be the correction that gold needs. “If it goes down enough, I will start buying it,” he told reporters.

Marc Faber, publisher of the Gloom, Boom & Doom report, could hardly contain his glee at the opportunity offered by the steep drop.

“I love the fact that gold is breaking down because it will give a good entry point. The fundamentals for gold are intact.”

He pointed out that while gold may be down 21 per cent from its September 2011 high, Apple is 39 per cent lower than last year’s high. The S&P is almost 1 per cent higher than its peak in October 2007, but over the same period gold is up 100 per cent.

Pundits have given a garden variety of reasons for the decline. We have already covered some of them in our last essay. But there’s more - Goldman Sachs in an April 10 report reduced its gold futures forecast and made a self-fulfilling prophecy to short gold, hurting gold sentiment and likely triggering stop-loss orders. (They must be laughing all the way to the bank. Wait, they are the bank.) Cyprus said it might unload 10 tons of reserves to help fund its bank bailout - the biggest sovereign sale for several years. It stoked fears that similar gold sales may be forced on other troubled Eurozone countries. Italy has the fourth largest gold holdings in the world of 2,452 tons.

Gold prices have been slowly gaining back some of the lost ground as traders and investors step in to buy bargains. Since making the call that started the downward spiral Goldman Sachs has covered its gold short this week.

There has been strong demand for physical gold, especially from Asia, which continues to underpin the gold market. Asia is witnessing one of the strongest waves of physical gold buying in 30 years. Retail sales of gold tripled across China April 15 to April 16, the China Gold Association said. The feverish buying has left many of Hong Kong’s banks, jewelers and even its gold exchange without enough gold to meet demand.

Is it time to be already back in the market? Let’s take a look at gold charts to find out (charts courtesy of http://stockcharts.com).

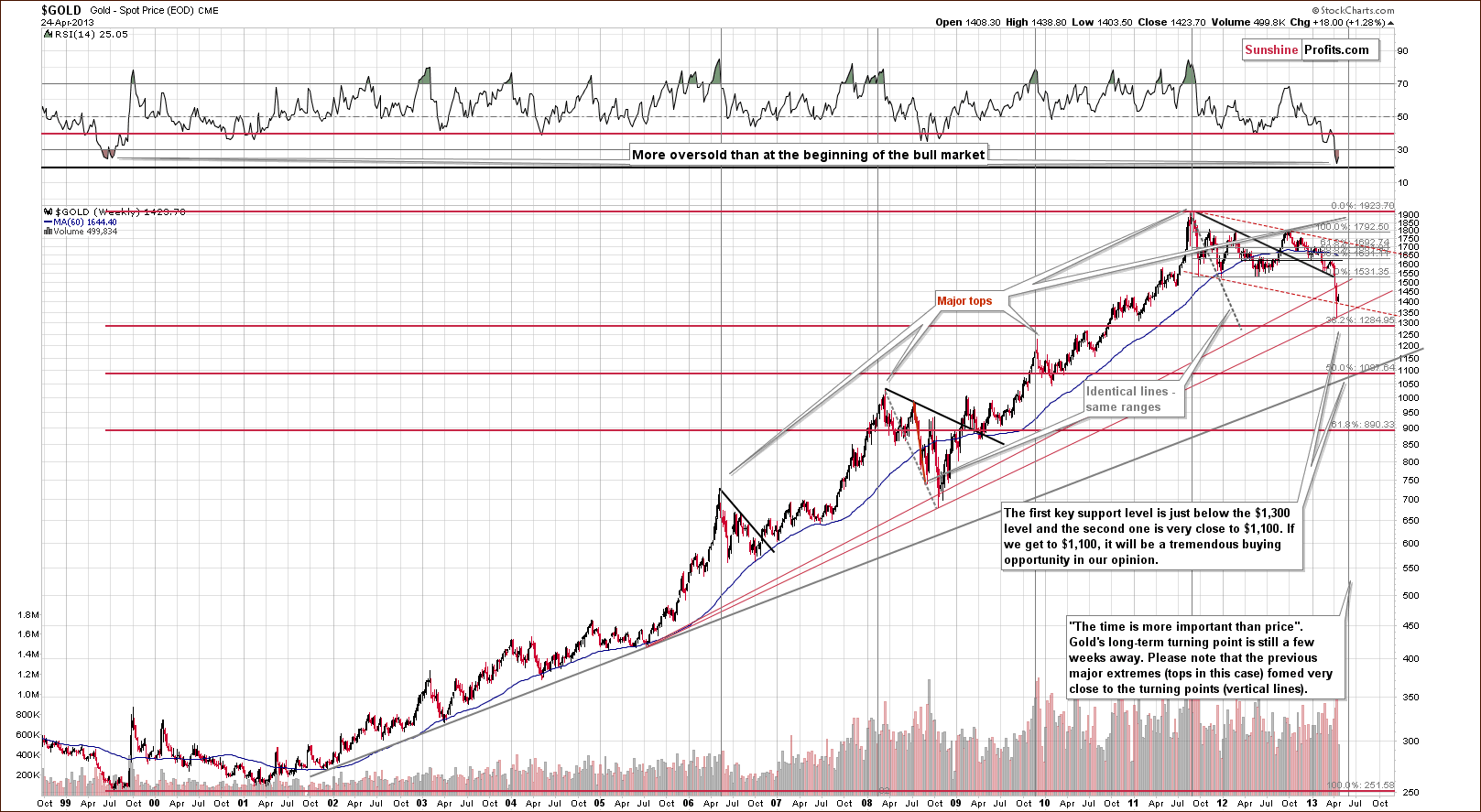

On the above long-term gold chart, we see a pullback, which will be more visible when we zoom closer in our next chart. A local bottom may have been reached, though it seems that further declines are likely.

At this point, this major long-term cycle is still several weeks away, and with the precision of this cycle in the past, we expect that the final bottom will be seen much closer to it than what we’ve seen recently.

Please note that gold could decline to as low as $1,100 and still be in a long-term uptrend. In fact, technically, it could decline all the way to the 61.8% Fibonacci retracement level close to $900 and still remain in a bull market.

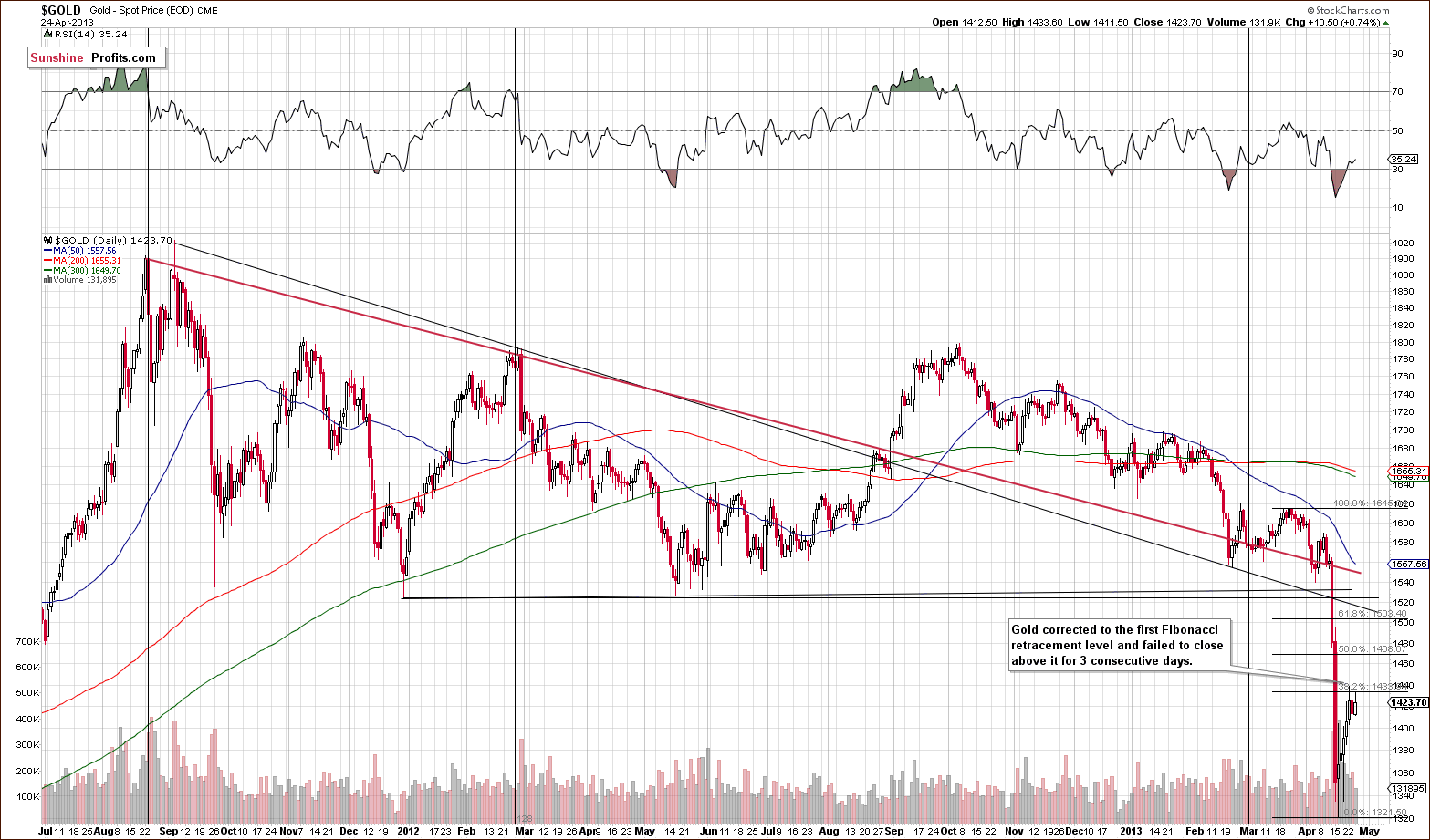

Let us now zoom in a bit and see how the situation looks like from the medium-term perspective.

In the chart, we saw a correction last week as gold’s price rallied first to the 38.2% Fibonacci retracement level and after a brief pause, moved to the second one (50%) – on Friday it closed slightly below it. Prices are currently consolidating around this level and the correction could actually be over. We have a situation where a moderate pullback was already seen – the bound is no longer likely because it was already seen. The RSI indicator reflects that – the market was extremely oversold on a short-term basis, but it’s no longer the case.

We see that volume levels were low on Wednesday when prices rallied, the same happened on Thursday and volume peaked on Friday where the price actually declined, which is not a good sign and suggests that further declines are likely.

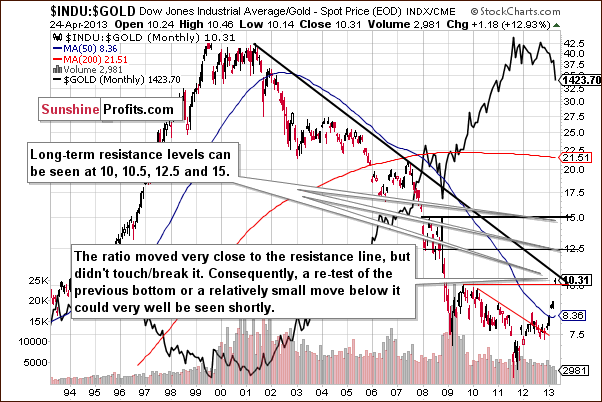

Now, we’ll have a look at Dow:gold ratio to see whether it indicates any important moves for gold.

Here, we see that the ratio moved close to the declining resistance line but didn’t really reach it. There is still some room for the ratio to move higher. If gold declines to its previous low or slightly lower, this declining resistance line will be reached, so basically further weakness could be seen here. The important point here is: the Dow to gold ratio chart does not imply a move higher for gold prices just yet.

Summing up, generally this week’s gold charts indicate that the yellow metal’s decline is not over yet. To the contrary, it could take a few more weeks before the rally really starts. There are also some indications that the correction (within the decline) is already over or close to being over.

Thank you for reading.

Sincerely,

Przemyslaw Radomski, CFA

PS. Our subscribers have been profiting during these turbulent times and are profiting on today's decline as well. We encourage you to join them and get to know our detailed downside targets and trading plan.

Back