Last week was rich in economic data. What do recent pieces of data on the U.S. economy imply for the gold market?

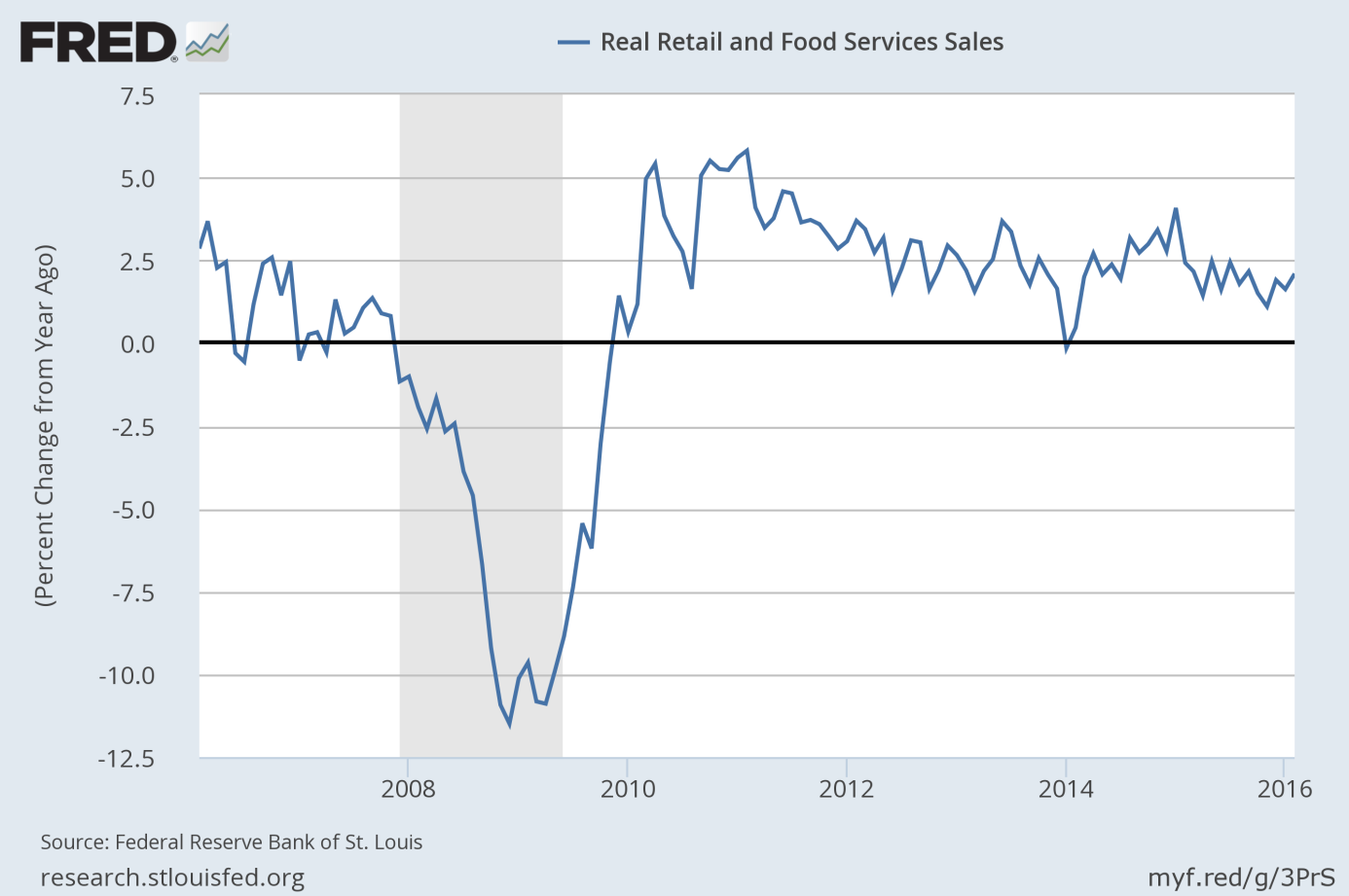

Retail Sales Fall in February

Due to the hype surrounding the FOMC meeting, we did not cover the latest economic news. Let’s try to make up for lost time. First, U.S. retail sales fell 0.1 percent in February, following a 0.4 percent decline in January (revised from a 0.2 percent gain). Importantly, sales of vehicles decreased 0.2 percent, confirming that the boom in automotive industry had ended. In consequence of weak retail sales, the GDP growth projected for first quarter of 2016 by the Atlanta Fed GDPNow model dropped from 2.2 percent to 1.9 percent. The long-term trend in retail sales does not look encouraging, as one can see in the chart below. It is good news for the yellow metal, given the fact that retail sales are a relatively influential indicator for the gold market.

Chart 1: Retail sales (as percent change from year ago) from 2006 to 2016.

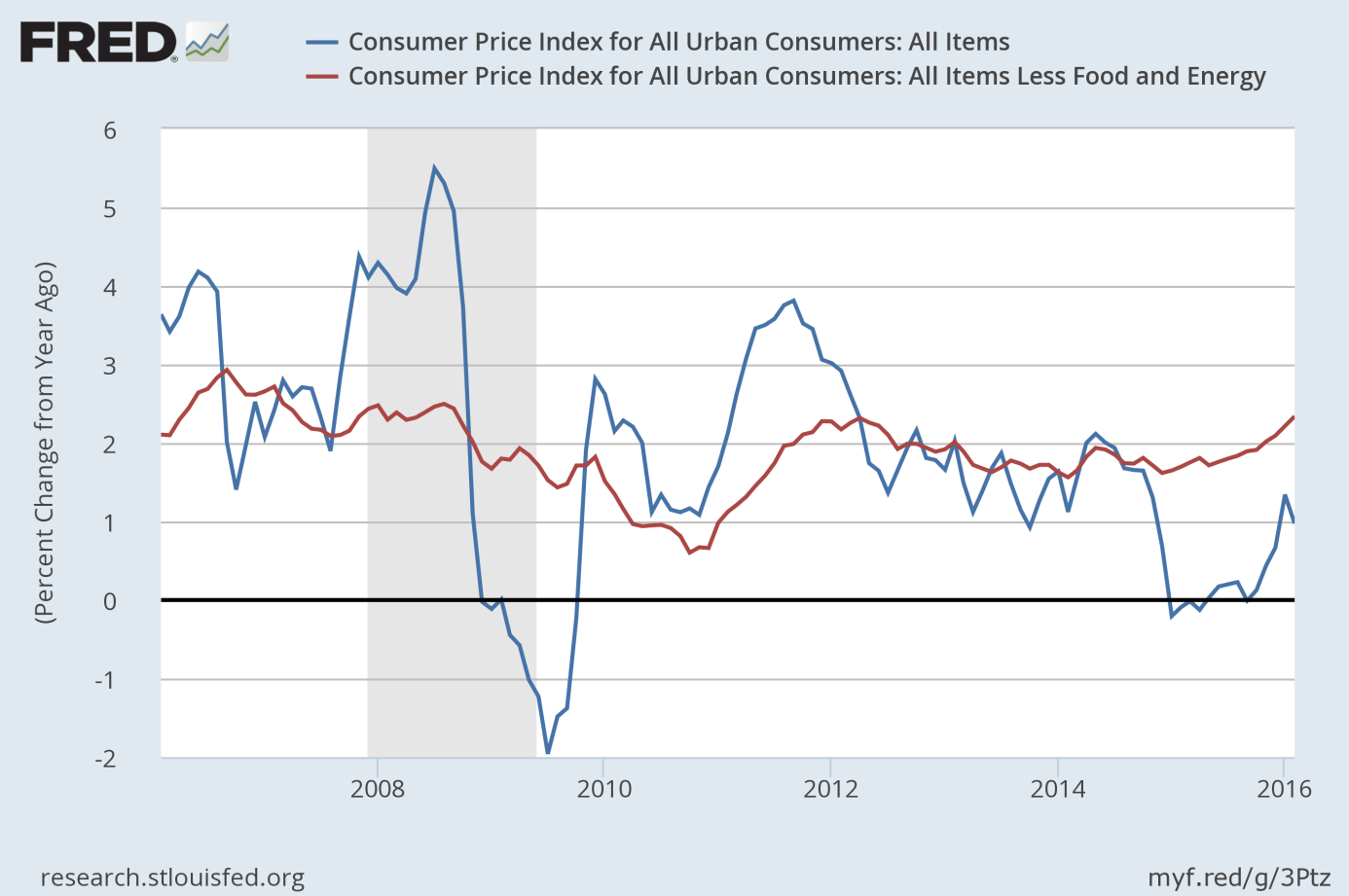

CPI Drops, but Core CPI Surges

Second, the consumer price index declined 0.2 percent last month, while the core CPI rose 0.3 percent, according to the Bureau of Labor Statistics. On an annual basis, the CPI increased at a 1-percent rate, down from 1.4 percent in January, while the core CPI surged 2.3 percent, the largest 12-month increase since May 2012. As one can see, both indices have been in an uptrend for several months. Actually, as one can see in the chart below, inflation is higher than in December, when the Fed was “reasonably confident that inflation will rise, over the medium term, to its 2 percent objective” and hiked interest rates.

Chart 2: CPI (blue line) and Core CPI (red line) as percent change from year ago from 2006 to 2016.

Interestingly, wholesale prices showed a similar dynamics: the producer price index fell 0.2 percent in February, while the core PPI inched up 0.1 percent. On an annual basis, wholesale prices were flat, while the core PPI rose 0.9 percent, the largest 12-month advance since July 2015.

However, although inflation has recently gone up, the FOMC members reduced their median projection. Therefore, the very recent report on consumer inflation is rather irrelevant for the Fed’s monetary policy and, thus, for the gold market.

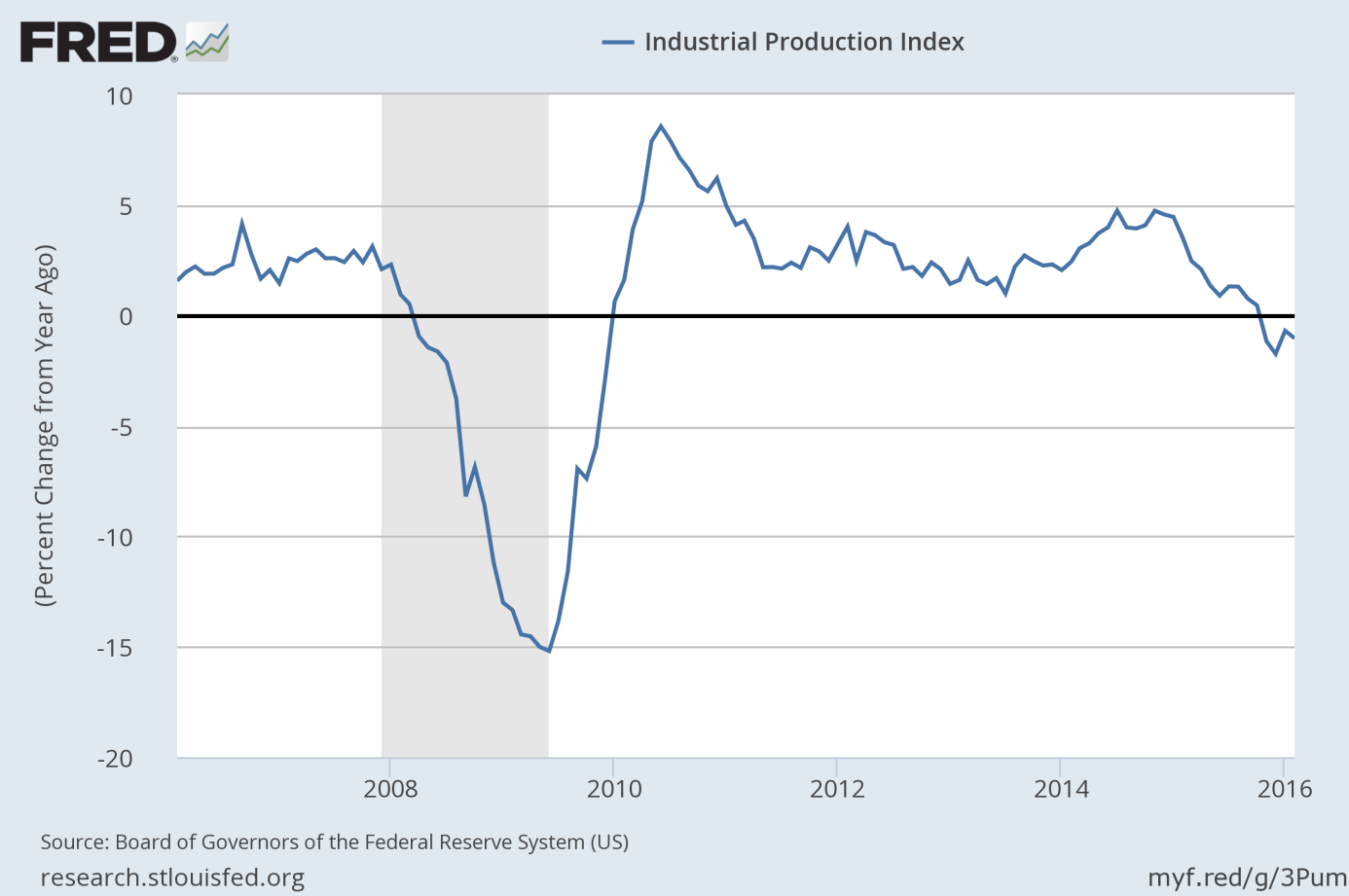

Industrial Production Declines, but Regional Indexes Improve

U.S. industrial production dropped 0.5 percent in February, according to the Fed. It was the fourth decline in total output over the past five months. Capacity utilization also decreased by 0.4 percentage point to 76.7.

On the other hand, some analysts say that the decline was caused by mining and utilities, while manufacturing was actually up for the second straight month. They also point out that the the Empire State general business conditions index jumped to a reading of positive 0.6 in March from a negative 16.6 in February, while the Philadelphia Fed manufacturing index rose to 12.4 in March from a negative 2.8 in February. We will see whether these increases are real improvements or only breathers. Anyway, the annual dynamics of industrial production looks recessionary, as one can see in the chart below.

Chart 3: Industrial Production (as percent change from year ago) from 2006 to 2016

Surely, this indicator does sometimes send false signals, but it has happened only three times since 1920 that industrial production declined for four straight months on an annual basis without the U.S. economy being in recession. If the weakness in the U.S. output persists, the yellow metal should gain.

The key takeaway is that last week was rich in economic data. Although the U.S. economy has been recently expanding at a moderate pace, some indicators, such as retail sales and, especially, industrial production, look discouraging. This is good news for the gold market, since bad data are likely to reduce the confidence in the strength of the U.S. economy, which should spur some safe-haven demand for the yellow metal.

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview