The yield curve has inverted. If its strong predictive power of the recession remains intact - in the previous part of this report, we presented strong arguments that this is really the case (or, that there are no strong evidence for a weakened predictive power) - it means that we should expect an economic slump around May 2020.

But what about gold? How should the yellow metal behave in a pre-recession world? To answer this trillion question, we analyzed the historical yield curve inversions and examined their impact on gold prices. We put the results in the table below.

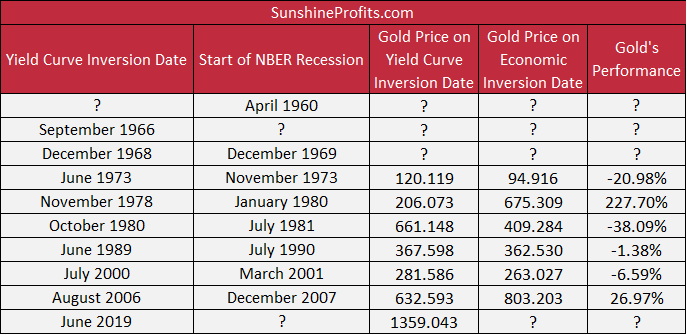

Table 1: Gold prices between the yield curve inversion and the following economic recessions.

Our research sample is terribly small, as Treasury spread series goes back just to 1959, while the gold prices were not freed until the gold standard was dismantled in early 1970s. So we could investigate the impact of only six yield curve inversions on the price of the yellow metal. Nevertheless, the results are interesting, if not surprising, at least for some investors. Gold gained only in two in two cases: after the yield curve inversion in November 1978 and in August 2006. Surely, the geometric average is positive - 11 percent up - but this is because of the astronomical surge of 228 percent in the late 1970s.

What does it imply for the precious metals investors? First, the yield curve inversion has not been necessarily bullish for the gold prices. They responded positively in the medium term only in one third of cases. Second, gold is not the best recessionary indicator. More often than not its price declines between the yield curve inversion and the following recession. Third, it seems that the secular trends were much more important for the gold's behavior. The prices went up in the aftermath of the yield curve inversion only in the late 1970s and mid-2000, when the yellow metal enjoyed its great bull markets.

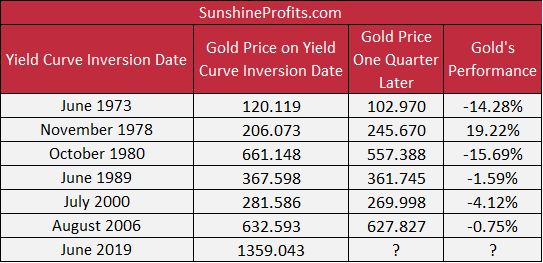

But what about the short run? Maybe the gold prices reacted positively to the yield curve inversion, but the effect was seen only in the short term? Well, the table below shows the gold's performance within one quarter after the yield curve inversion.

Table 2: Gold prices on the yield curve inversion date and one quarter later.

As one can see, the results are even worse. Gold reacted positively only once, in the late 1970s, but the gain shrunk to 19 percent. Consequently, the geometric average plunged to negative 3.5 percent.

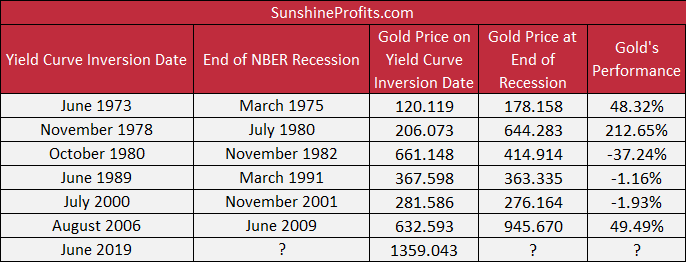

But maybe gold shined in the long-run? Let's investigate this possibility as well. This time, we lengthened the period up to the end of the recession following the yield curve inversion. The table below provides the results.

Table 3: Gold prices between the yield curve inversion and the end of the following economic recessions.

As one can see, the results are better than in both previous views. Gold gained in three cases now, and the geometric average jumped to 27 percent. Although the yellow metal did not shine in each case, the better results over the longer horizons, which included recessions, confirm to some extent the notion that gold may serve as a safe-haven asset.

What are the implications of our analysis for gold in the context of the recent yield curve inversion? Contrary to popular opinion, neither the inversion nor even the following recession have to be necessarily bullish for the gold prices. This is at least what history teaches us: there were both cases when the price of the yellow metal reacted positively but there were also instances of bearish response.

Who wins this time: the bears or the bulls? We believe that the latter will be victorious in the end, while gold might suffer in the short run. Why? Fundamental axiom about gold is that it tends to perform relatively well during periods when confidence in the financial system is declining. The key is that the yield curve inversion will add to recessionary fears. Actually, this is what the inversion means - that investors expect risks to increase substantially very soon. And they might be right. After all, the Fed's 'insurance' cut is a clear signal that the U.S. central bank panics in a desperate effort to steepen the yield curve. But this may be not enough to avert the recession - and investors know it. They will be afraid that - with the current level of the federal funds rate - the Fed will lack of ammunition when the recession hits. They will fear the negative interest rate policy and other unconventional monetary policy, looking for a shelter in gold. Unless policymakers propose some reasonable escaping the debt trap - hint: lower interest rates and more debt are not the real solution - the confidence in the financial system will remain low, supporting the gold prices.

If you enjoyed the above analysis and would you like to know more about gold in the pre-recession world, we invite you to read the August Gold Market Overview report. If you're interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you're not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It's free and if you don't like it, you can easily unsubscribe. Sign up today!

Thank you.

Arkadiusz Sieron

Sunshine Profits' Gold News and Gold Market Overview Editor