In this essay I would like to make an update on silver’s performance relative to gold and at the same time address a letter that one of my Readers have sent me. Before proceeding, I will provide you with a few charts (courtesy of stockcharts.com) to make it easier to visualize what I will be writing about. The first chart features gold and its performance in the last 3 years.

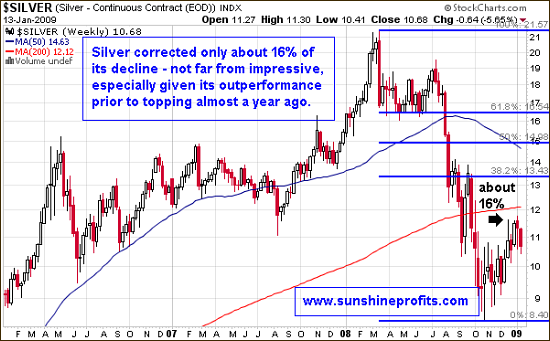

Gold plunged, but managed to recover rather quickly a large part of the decline. It is very difficult to say the same about the silver market at the moment:

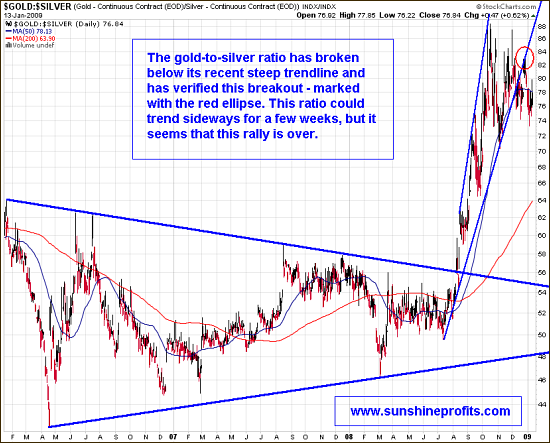

Only 16% compared to gold’s 60% seems very small. Should this number concern those (I fall into this category), who have invested in physical silver and are on the long side of this market? Taking a closer look on the gold-to-silver ratio should provide us with more details:

The gold-to-silver ratio has performed quite ‘normally’ in the first half of 2008, which was followed by a massive rally, that sent silver prices so low. Remembering silver’s overall outperformance relative to gold and looking at the above charts it is natural to ask why has the situation changed so much in the last several months.

In the abovementioned letter, Reader comments on the popular gold-to-silver ratio, and asks why it is now at 80+ level, while the long term average for this bull market is below 50. Those of you, who are not familiar with my past essays on this matter, may want to read this essay for additional information. In short – the trend line best describing the relation of gold to silver is linear and the slope coefficient equals 43 (as of June 2008). It is a little higher right now, but that is not the point. The important thing here is that this is just an average number that this ratio achieved throughout many phases of the bull market.

The major point made in this essay is that silver, just like junior mining companies, tends to ‘take its time’ before finally starting to rise really significantly. However, when it finally does move, then it’s ‘up, up and away’ for silver and its relative performance to gold.

In other words: the average ratio of 43 is based on a long-term trend line and therefore represents the average value of the gold / silver ratio - on a multi-year basis. As we have the ratio of about 80 today, we will probably see it well below 40 in a few years, so that it averages out around 43. Silver underperforms gold at the beginning of an upleg and outperforms, when the rally is ending. This is what we see today - a new upleg has already started or is about to start and silver's performance relative to gold is rather weak.

Technically speaking, the gold-to-silver ratio has already broken down from its uptrend, which suggests that silver should ‘outshine’ gold from now on. This is a long-term signal and I would not advise using it for short term trades (in fact, I expect prices to correct a little more before rising again). We may have another bottom, but I believe that there may be weeks of perhaps months (though I doubt that) of low prices, definitely not years.

Another thing is that the industrial demand accounts for a larger share of the demand for silver, than it is the case with gold. According to Gold Fields Mineral Services in 2006 silver’s industrial demand amounted to 430 mln oz which is over 47% of the total demand. The analogical figure for gold is 12%. Silver, is therefore much more of an ‘industrial metal’, than gold is.

Silver has been used as money throughout the history and Milton Friedman called it the most important monetary metal. Historically speaking, fiat monetary systems have always collapsed and nobody can say for sure that it will not happen again. In that case, the monetary value of silver will dwarf any other type of demand and will cause the price of the white metal to rise tremendously. However, we are not there at the moment, and we need to take into account what influences the price of silver today.

The fact is that today silver is mostly bought as a commodity that is widely used in the industry. As such it is dependent on companies producing goods that include silver such as computers or cell phones. Companies purchase silver to produce these goods, if they can sell them profitably. Companies have their own problems, caused mainly by declining global demand and are reluctant to purchase increasing amounts of silver. As market discounts these problems, the value of silver and world stock indices decline together. This is naturally a very simplified version of the mechanism, but it provides the logic behind the negative correlation between gold-to-silver ratio and the general stock market.

Silver’s poor performance relative to gold can be explained by its correlation with the general stock market, as well as its cyclical nature. Stocks’ valuation and the amount of money pumped into the system lately suggest that we are in the ‘oversold’ territory. Since we are not ending an upleg in the precious metals, but are rather beginning one, we should expect silver to outperform in the future.

Summing up, we may not have higher prices tomorrow or in one week, but buying here should be very profitable in the long run.

Of course the market might prove me wrong, as nobody can be right 100% of the time. Should my view on the market situation change substantially, I will send an update to the registered Users along with suggestions on how to take advantage of it. Register today to make sure you won’t miss this free, but valuable information. You’ll also gain access to the Tools section on my website. Registration is free and you may unregister anytime.

P. Radomski

Back