tools spotlight

-

After Recent Highs, What’s Next for the Junior Miners?

May 24, 2022, 8:04 AMSigns are pointing to gold’s May rally running out of steam as the USDX reaches its short-term bottom. But how much stamina does the yellow metal still have?

Another day, another higher close in the junior miners. And another day where profits on our long positions in the latter increased. There is a sign that the rally in the precious metals sector is close to being over.

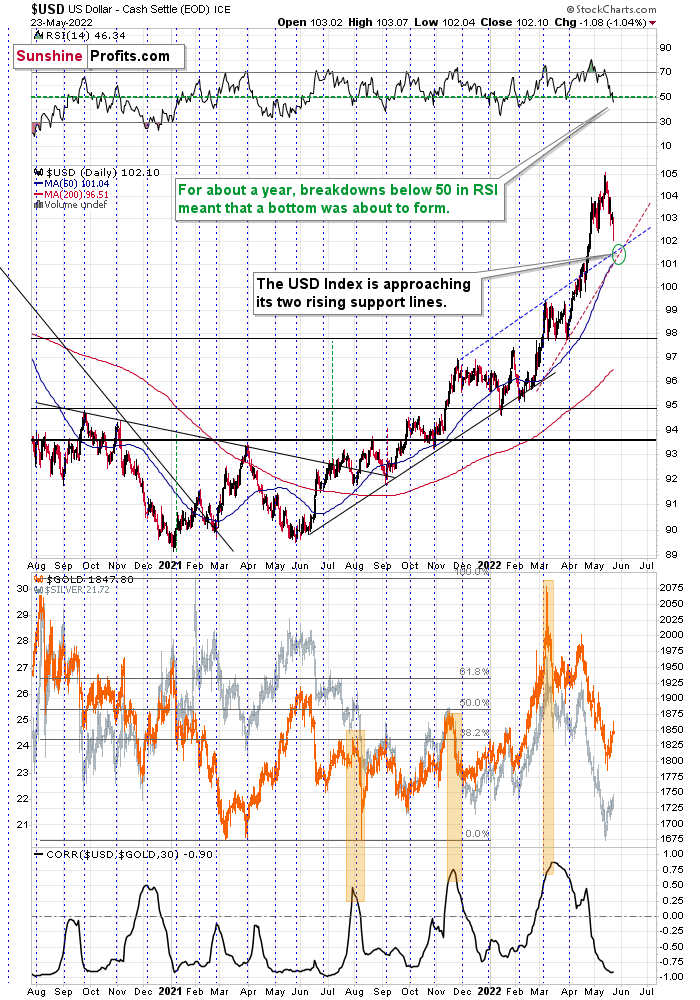

That sign is the situation in the USD Index, and the shape of the gold-USD link.

Starting with the gold-USD link, please note that while gold ended yesterday’s session higher, it was only ~$6 higher. Given that the USD Index declined by over one index point, it would be “normal” for gold to rally much more.

That’s a sign that gold is getting “exhausted”, which is another way of saying that the buying power for this particular rally appears to be drying up. Of course, one swallow doesn’t make a summer, but given the size of USD’s decline, it’s quite notable.

USD’s decline took it below its recent lows, and since it’s slightly down also in today’s pre-market trading, it seems that it can now decline further in the very near term. “Further” here shouldn’t be viewed as “by a lot”. In fact, there is a combination of rising support lines just above where the USD Index is trading right now.

The dashed lines: blue and red one are likely to stop this correction. Of course, it’s not 100% certain, but the fundamental situation continues to favor higher USD values (rising real interest rates), so significant changes don’t appear likely. The possibility is there, especially if the geopolitical situation changes, but it’s simply not likely.

Besides, the RSI just moved below 50, and while this doesn’t mean anything based on “classic” interpretation of this indicator’s signals, I would like to emphasize that practically each time when we saw something like that in the past year or so, it meant that the USD Index was about to bottom.

So, on one hand, gold no longer “wants” to react to the USD’s weakness, and on the other hand, the short-term bottom in the USD Index appears to be at hand.

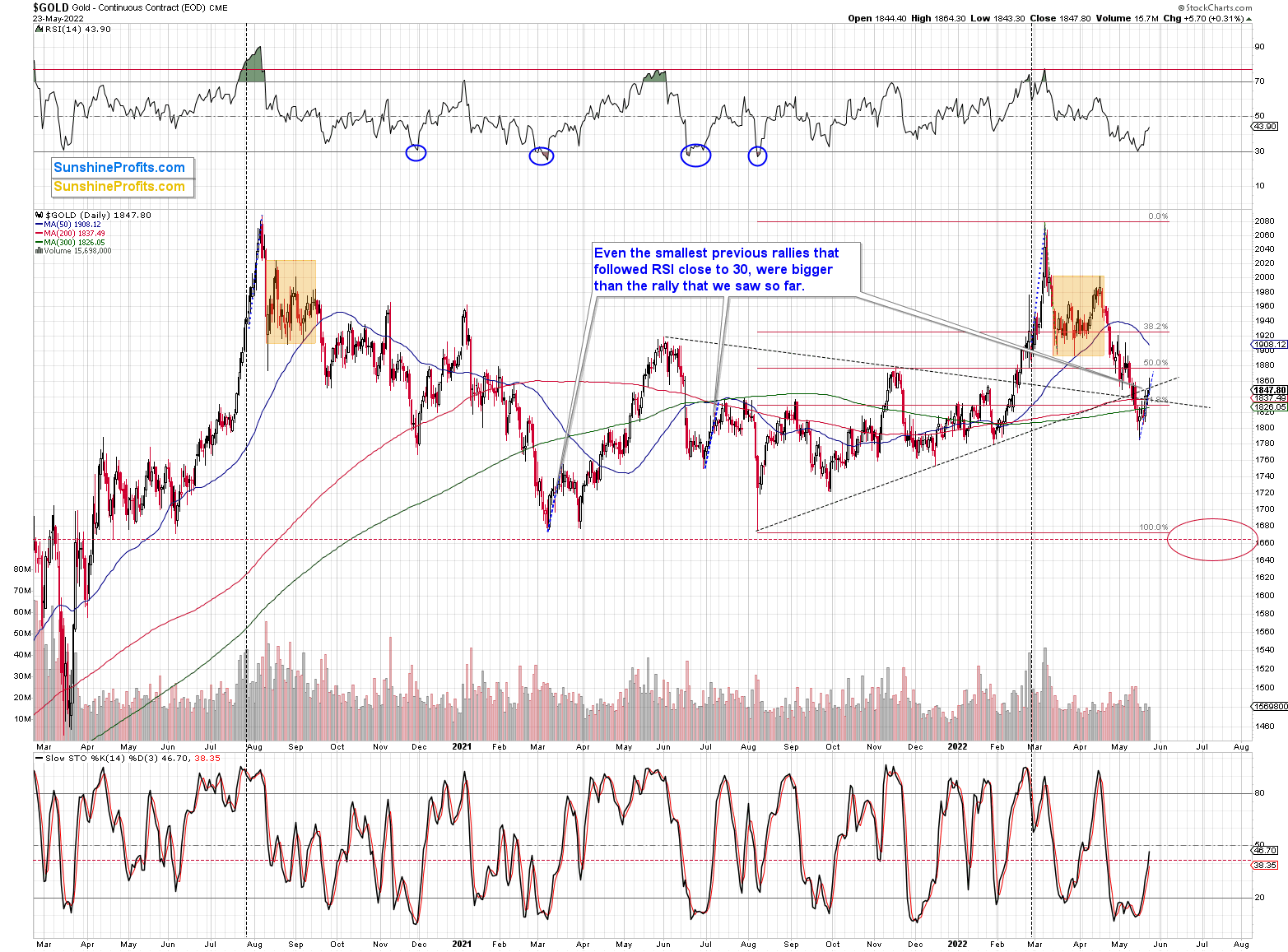

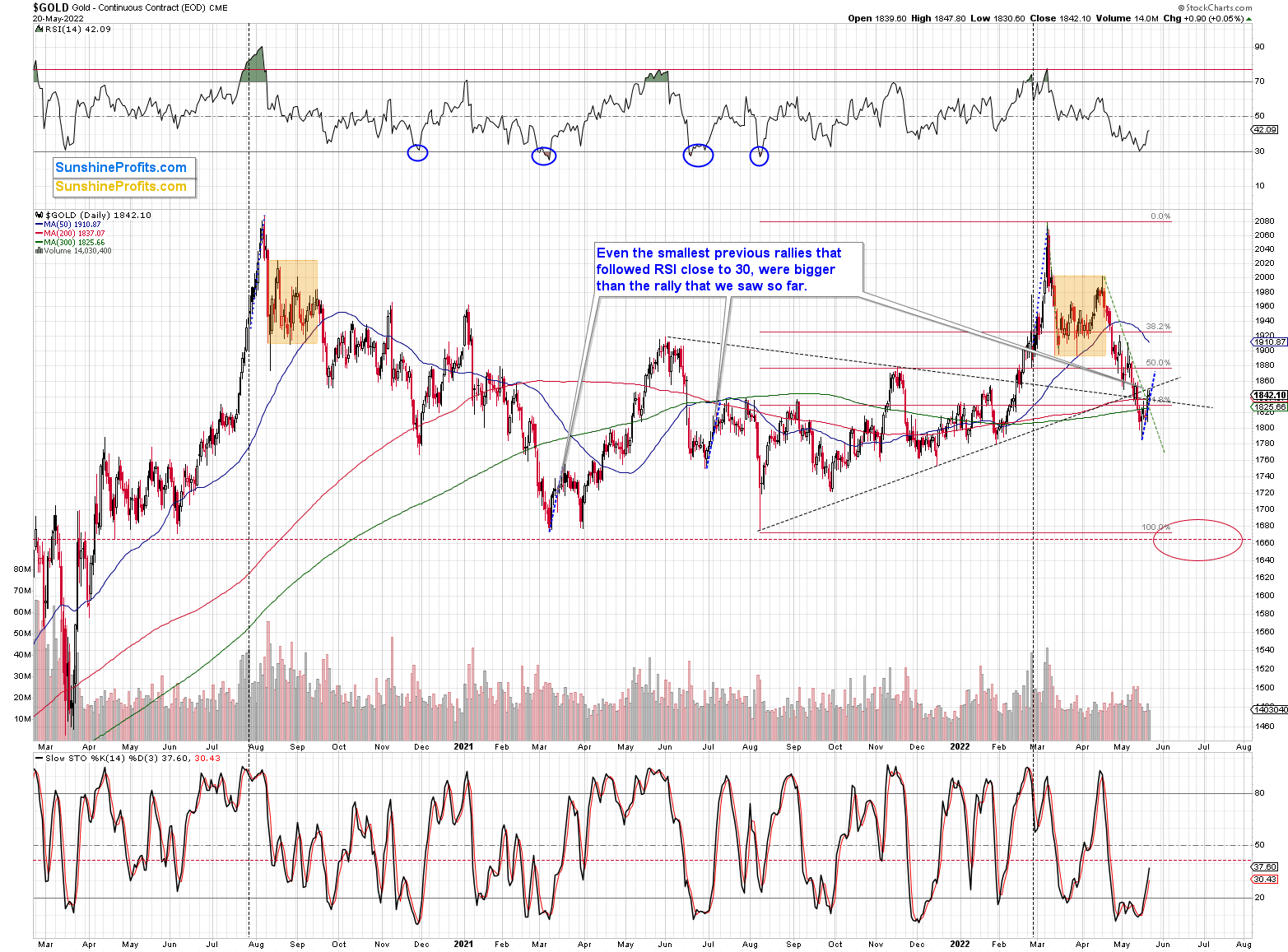

Gold itself still didn’t correct as much as it did after previous cases when the RSI touched the 30 level. I marked the smallest rallies that followed this signal in the recent past with blue, dashed lines.

If history is about to rhyme, then gold’s rally might be nearing its end, but it’s not yet there.

And what about the junior mining stocks?

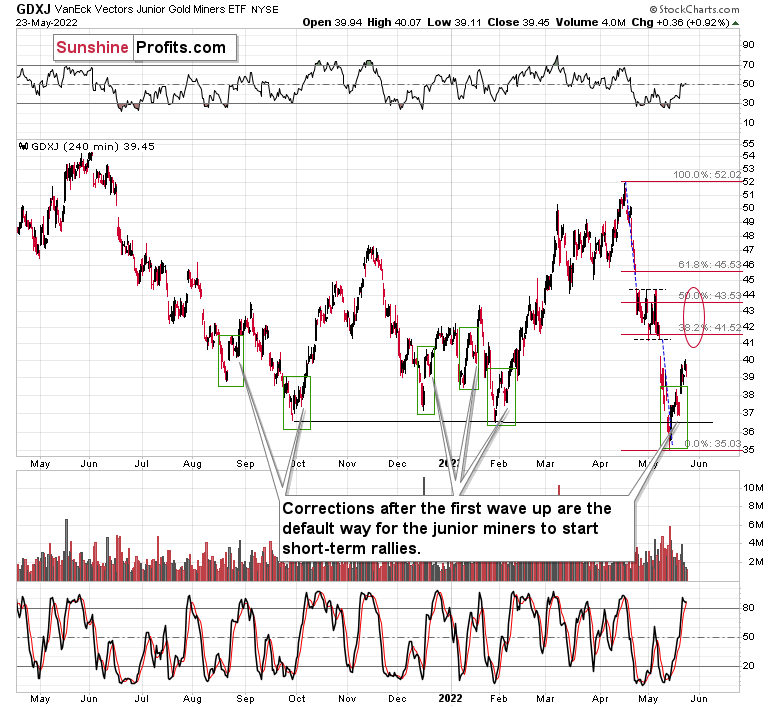

Well, their rebound simply continues. The GDXJ ETF ended yesterday’s session 0.92% higher (GDX was up by 0.59%, silver was up by 0.23% and gold by 0.31%). They are up by almost $4 (about 10%) from May 12, when we switched from short to long positions in the USDX – more than any of the above-mentioned markets.

The USD’s decline appears to be close to its end, and the same goes for the end of the short-term rally in gold, which means that the same fate likely awaits the junior miners – their rally too is about to end, in my view.

The target area that I placed on the above chart remains up-to-date. Yesterday’s weakness in gold relative to the USD Index tells me that it’s more likely that the rally will end in the lower part of the target area – probably close to its early-May low.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few days. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Don’t Panic Over the Recession Rumor Mill

May 23, 2022, 9:28 AMThe cherry-picked narrative that a recession is just around the corner is a little off the mark. Don’t forget the demand side of the inflation equation.

As you’ve read in my (extra) Saturday analysis, the technical outlook for the precious metals market remains bullish in the near term. And the market already agrees - gold is already up in today’s pre-market trading, and the odds are that our profitable long positions will be even more profitable shortly. As I indicated on Saturday, today’s analysis will focus on fundamentals.

Take the Ball and Run with It

With the new narrative on Wall Street proclaiming that a destitute U.S. consumer is all tapped out and a recession looms, investors have succumbed to the same pitfalls that led them astray in 2021. To explain, when market participants were blindly following the Fed’s “transitory” narrative, I wrote on Dec. 23:

Please note that when the Fed called inflation “transitory,” I wrote for months that officials were misreading the data. As a result, I don’t have a horse in this race. However, now they likely have it right. Thus, if investors assume that the Fed won’t tighten, their bets will likely go bust in 2022.

To that point, with the same merry-go-round on full display now, the permabears and the media are running in circles once again.

Please see below:

Likewise, Bloomberg published an article on May 21 that stated:

“The retailers now find themselves flush with clothes, televisions and other discretionary items that customers aren’t buying as they channel more spending into basic needs and services. As a result, the companies took markdowns that eroded profits.”

Please see below:

Source: Bloomberg

Source: BloombergAgain, please remember that I don’t have a horse in this race. I expect the U.S. to fall into a recession as the prospect of a “soft landing” is highly unrealistic. However, the recession should come as the Fed’s rate hike cycle intensifies, not now.

Moreover, those that cry wolf until one finally arises lack objectivity, and therefore lead investors astray. Thus, the bond bulls that saluted “transitory” died a slow death in 2021/2022, and the investors that cried wolf about a recession for the last two years are louder than ever. However, objective analysis suggests otherwise.

For example, the narrative crowd focuses all their attention on Walmart and Target while turning a blind eye to Home Depot’s outperformance. For context, I wrote on May 20:

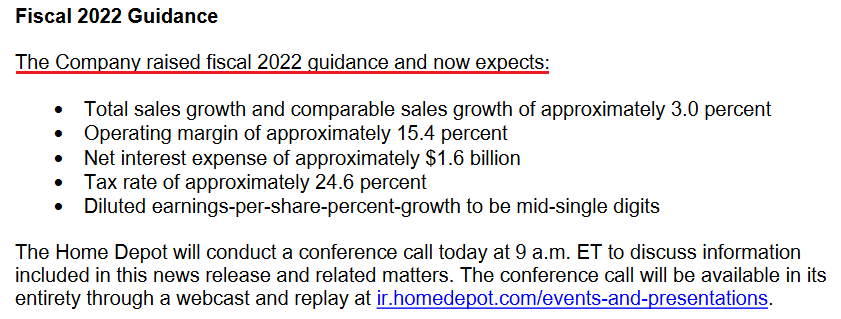

Home Depot – the fourth-largest retailer in the U.S. – had a phenomenal quarter. Moreover, the company primarily sells discretionary items (products purchased with disposable income), and management raised their 2022 guidance. As a result, with the U.S. housing market more affected by higher interest rates than any other sector, Home Depot hasn't seen any demand destruction.

Please see below:

Source: Home Depot

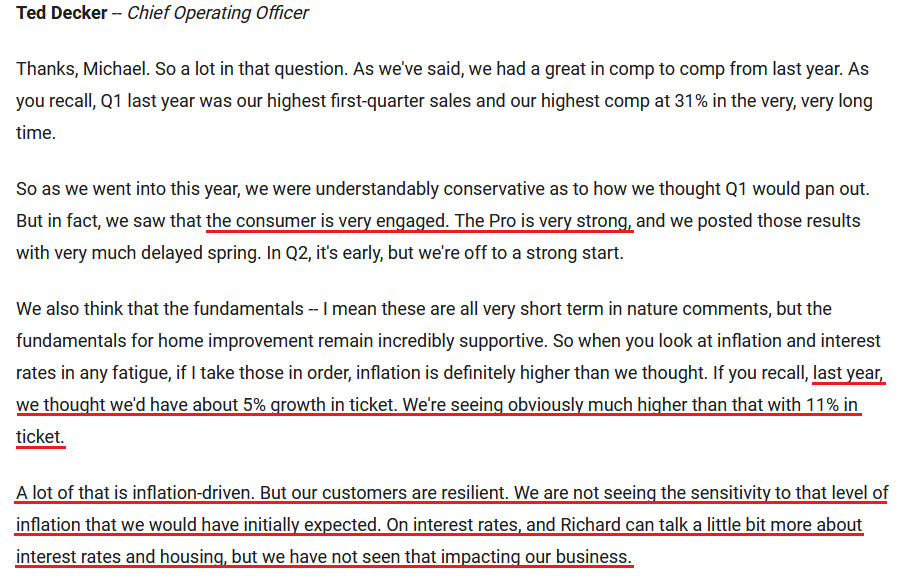

Source: Home DepotMoreover, I noted the optimistic comments from now CEO Ted Decker previously:

Source: Home Depot/The Motley Fool

Source: Home Depot/The Motley FoolLikewise, Foot Locker released its earnings on May 20. For context, the retailer sells apparel and footwear from brands like Nike, Adidas, and New Balance. CFO Andrew Page said:

“Based on our current visibility, we now expect to achieve the upper end of our revenue and earnings guidance for the full year. While supply chain volatility continues, we are pleased with our receipt flow so far this year, which gives us incremental confidence in our ability to fill demand for the balance of the year.”

As a result, while the demand destruction narrative percolates, Foot Locker isn’t sounding the alarm.

Please see below:

Source: Foot Locker/Seeking Alpha

Source: Foot Locker/Seeking AlphaFurthermore, Canada Goose released its earnings on May 19. For context, the luxury retailer sells parkas at price points of more than $1,000; and after increasing its guidance, CEO Dani Reiss said:

Source: Canada Goose/Seeking Alpha

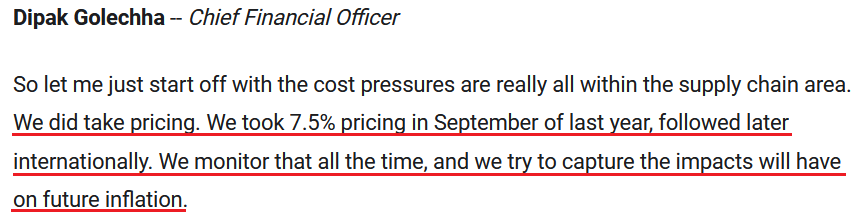

Source: Canada Goose/Seeking AlphaContinuing the theme, Deere & Company – which manufactures agricultural machinery, heavy equipment, forestry machinery, and lawn care equipment – released its earnings on May 20. In-house economist Kanlaya Barr said:

“We expect U.S. and Canada industry sales of large [agriculture] equipment to be up approximately 20%. Order books for the remaining of the current fiscal year are mostly full, and we already see signs of strong demand for model year '23 equipment, with some order books opening in June.”

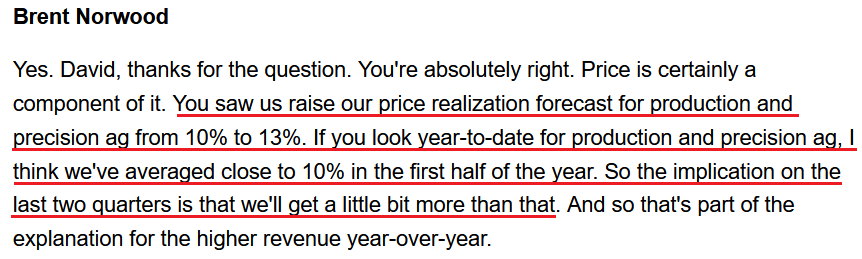

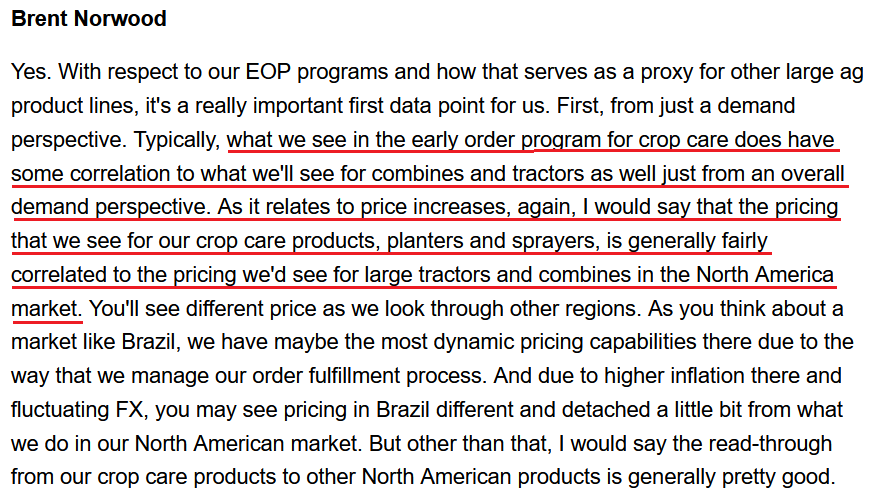

Moreover, Brent Norwood, head of investor relations, said:

“We expect our price for the full year will more than offset increases in material and freight…. With respect to price, so far what we've seen in 2022 is it hasn't had much of effect on demand. And as we noted, we're already seeing indication of interest for '23, even though some products may be above trend line price realization already for '23.”

As a result, not only has demand remained resilient, but management expects more price increases in the second half of 2022.

Please see below:

Source: Deere & Company/Seeking Alpha

Source: Deere & Company/Seeking AlphaNorwood added:

“With respect to our crop care or the order program, where we do have prices set, we are seeing pricing for crop care products in the high single digits for next year. So, we would expect pricing to be above trend line for those products going into next year.”

Moreover, with crop care pricing “fairly correlated” with the rest of Deere & Company’s products, the overlooked results are highly inflationary.

Please see below:

Source: Deere & Company/Seeking Alpha

Source: Deere & Company/Seeking AlphaAlso noteworthy, Palo Alto Networks – the largest cybersecurity company in the U.S. – released its earnings on May 19. CEO Nikesh Arora said:

“If you compare and contrast what we're seeing today with what we saw about two and a half years ago, two years ago when the pandemic hit, believe it or not, there were more industries impacted by the pandemic than are impacted right now by inflation concerns….

“And even when it is felt, you'll see it in some constrained industries because the service is boom right now. There are more jobs than people being hired. So, we're not seeing the pressure from an inflation or reduced economic activity perspective.”

Thus, resilient demand and higher prices remains the story at Palo Alto Networks.

Please see below:

Source: Palo Alto Networks/The Motley Fool

Source: Palo Alto Networks/The Motley FoolTherefore, while a recession remains the most likely outcome over the medium term, cheering it on won’t make it come to fruition. Moreover, cherry-picking data that supports one’s narrative is neither objective nor profitable. As such, while commentators issue dire warnings about Walmart and Target’s performances, other retailers are still flourishing.

In addition, it’s important to remember that Walmart and Target sell a lot of generic clothing items that don’t have brand power. Therefore, it’s easy to see the dichotomy between Walmart – where management said that “we started being aggressive with rollbacks in apparel” – and the strong results from companies like Foot Locker and Canada Goose.

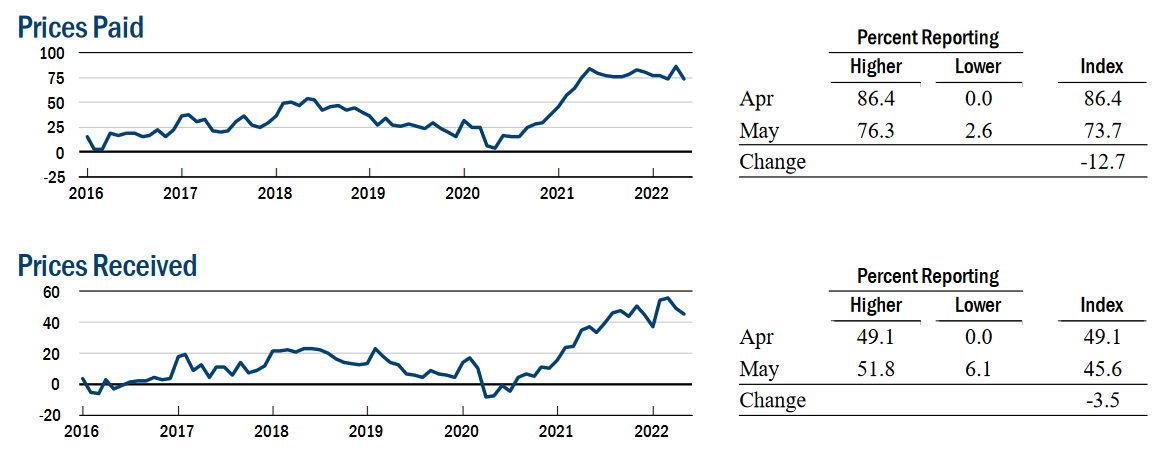

Finally, the New York Fed released its Empire Manufacturing Survey on May 16. The data is largely neutral for Fed policy since “the headline general business conditions index dropped thirty-six points to -11.6.”

However:

“The index for number of employees increased seven points to 14.0, and the average workweek index held steady at 11.9, indicating a modest increase in employment levels and the average workweek.”

In addition:

“After reaching a record high last month, the prices paid index fell thirteen points to a still elevated 73.7, and the prices received index edged down to 45.6, signaling ongoing substantial increases in both input prices and selling prices, though at a slower pace than last month.”

Thus, the mixed results show employment and inflation increasing while output decelerated sharply. However, the data compiled from May 2-9 highlights how inflationary pressures remain problematic.

Please see below:

Source: New York Fed

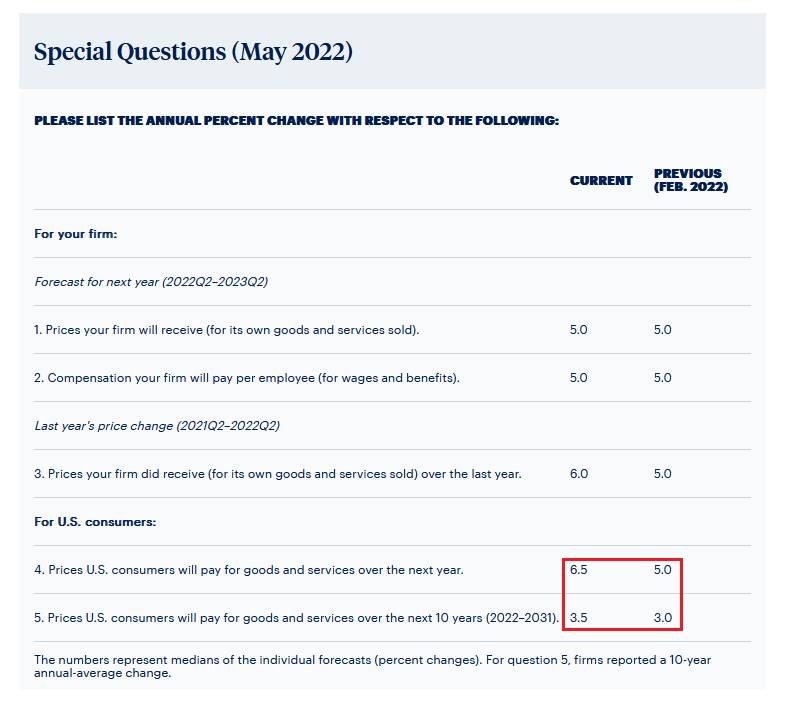

Source: New York FedSinging a similar tune, the Philadelphia Fed released its Manufacturing Business Outlook Survey on May 20. For context, the data was compiled from May 9-16. The report stated:

“The survey’s current general activity index declined, while the indicators for new orders and shipments rose. The employment index decreased, and the price indexes remained elevated but edged down…. The firms continued to report increases in prices for inputs and their own goods.”

However, the release added that “the firms’ median forecast for the rate of inflation for U.S. consumers over the next year was 6.5 percent, up from 5.0 percent from when the question was last asked in February,” and that “the firms’ median forecast for the long-run (10-year average) inflation rate was 3.5 percent, up from 3.0 percent in February.”

As a result, the Fed still has plenty of work to do to keep inflation expectations in check.

Source: Philadelphia Fed

Source: Philadelphia FedThe bottom line? While narratives move markets, the doom-and-gloom crowd is cherry-picking data to support their conclusion. Moreover, I don’t care if/when the U.S. falls into recession. I’m simply presenting an objective analysis. Also, I’ve noted on numerous occasions that investors underestimated the demand side of the inflation equation.

In addition, the recession crowd doesn’t realize that a penniless consumer is actually bullish for the S&P 500 because demand destruction reduces inflation and allows the Fed to resume QE. In contrast, resilient consumer spending keeps the Fed’s foot on the hawkish accelerator. As a result, with the latter stronger than many believe, inflation should remain uplifted, and the Fed’s liquidity drain should result in more medium-term pain for the PMs and the general stock market.

In conclusion, the PMs were mixed on May 20, as gold managed to close in positive territory. However, with our long position in the GDXJ ETF still in the green, and more short-term upside poised to materialize, relief rallies should reign before pessimism dominates in the months ahead.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few days. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

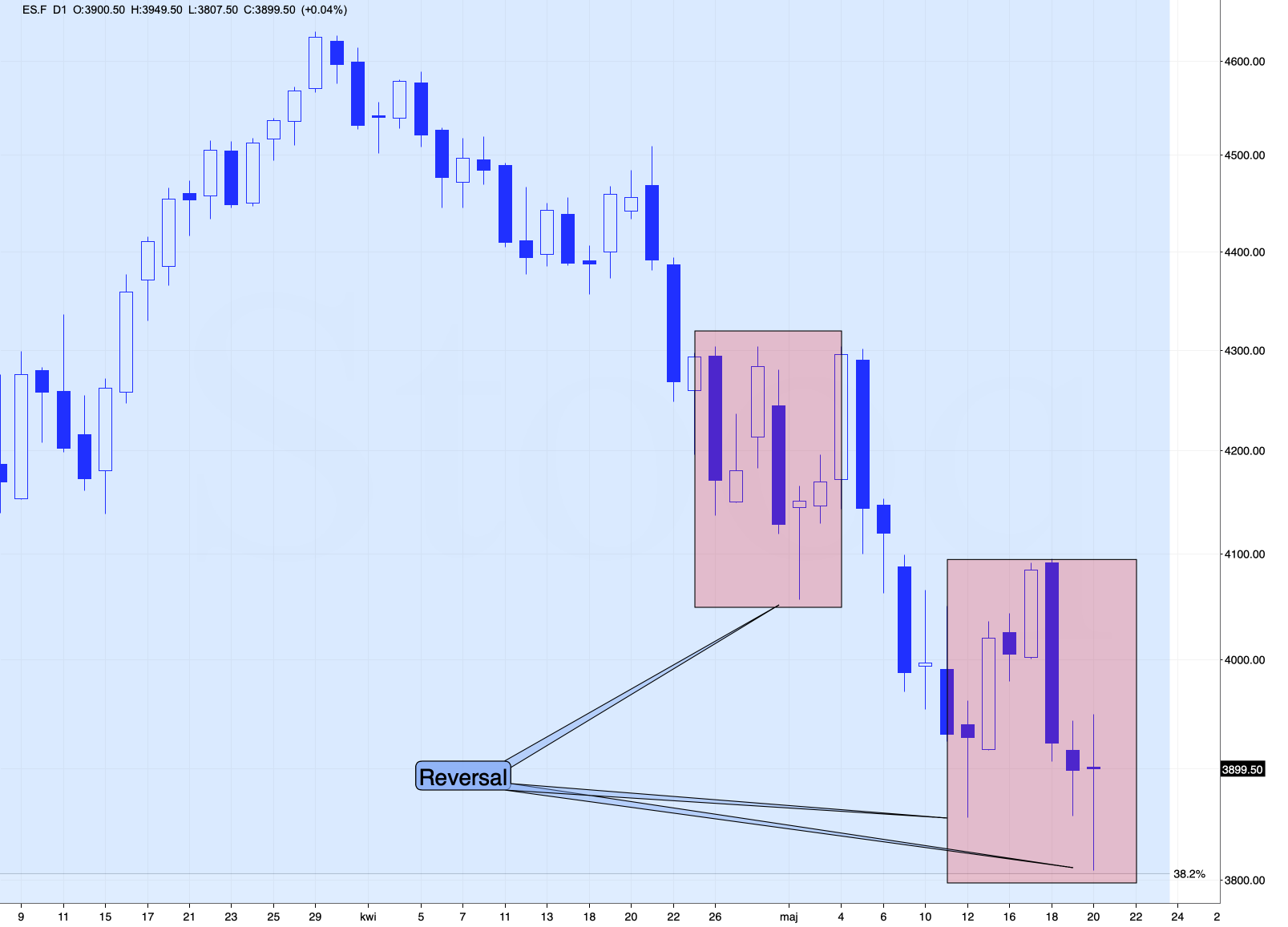

Meaningful Juniors’ and Stocks’ Reversals – Extra Update

May 21, 2022, 7:49 AMI’m usually not posting/sending anything over the weekend, but this time I decided to make an exception, as we’re so close to taking profits from the current long positions and re-entering the short ones. And because I have some good news to share.

Getting to the point, Friday’s session, where we saw reversals in gold, miners, and stocks, suggests that what I wrote previously remains up-to-date. The odds are that the short-term rally will continue, at least for a short while.

You see, both: stocks and juniors have reached important support levels yesterday. The support that the S&P 500 reached was more important, so let’s start with it.

On Friday’s I wrote the following:

On a very short-term basis, junior miners could be driven by stock market moves. Meanwhile, the stock market appears to be repeating its very recent consolidation pattern.

After stocks’ initial rebound (late April), they declined once again, and then they rallied back up to their previous high before sliding to new lows.

So far, we’re seeing something similar. The initial rebound was indeed followed by a sharp decline. In fact, even the intraday performance is similar. The daily decline was big and sharp, and it was followed by a daily reversal. What followed then was a small daily rally and then a huge daily rally, which was the final top.

If history rhymes, then perhaps today’s or Monday’s (or Tuesday’s) rallies will be significant and take stocks to the final short-term top. This could correspond to a short-term top in junior miners as well.

The above would fit the scenario in which the miners continue to rally for the next 1-3 days.

What happened yesterday made the two situations even more alike. Stocks declined below the initial lows and then reversed profoundly before the end of the day, closing slightly (but still) higher.

If history rhymes – as it usually tends to – we’re likely to see higher stock market values in the next 1-3 days. That’s likely to support higher junior mining stock prices.

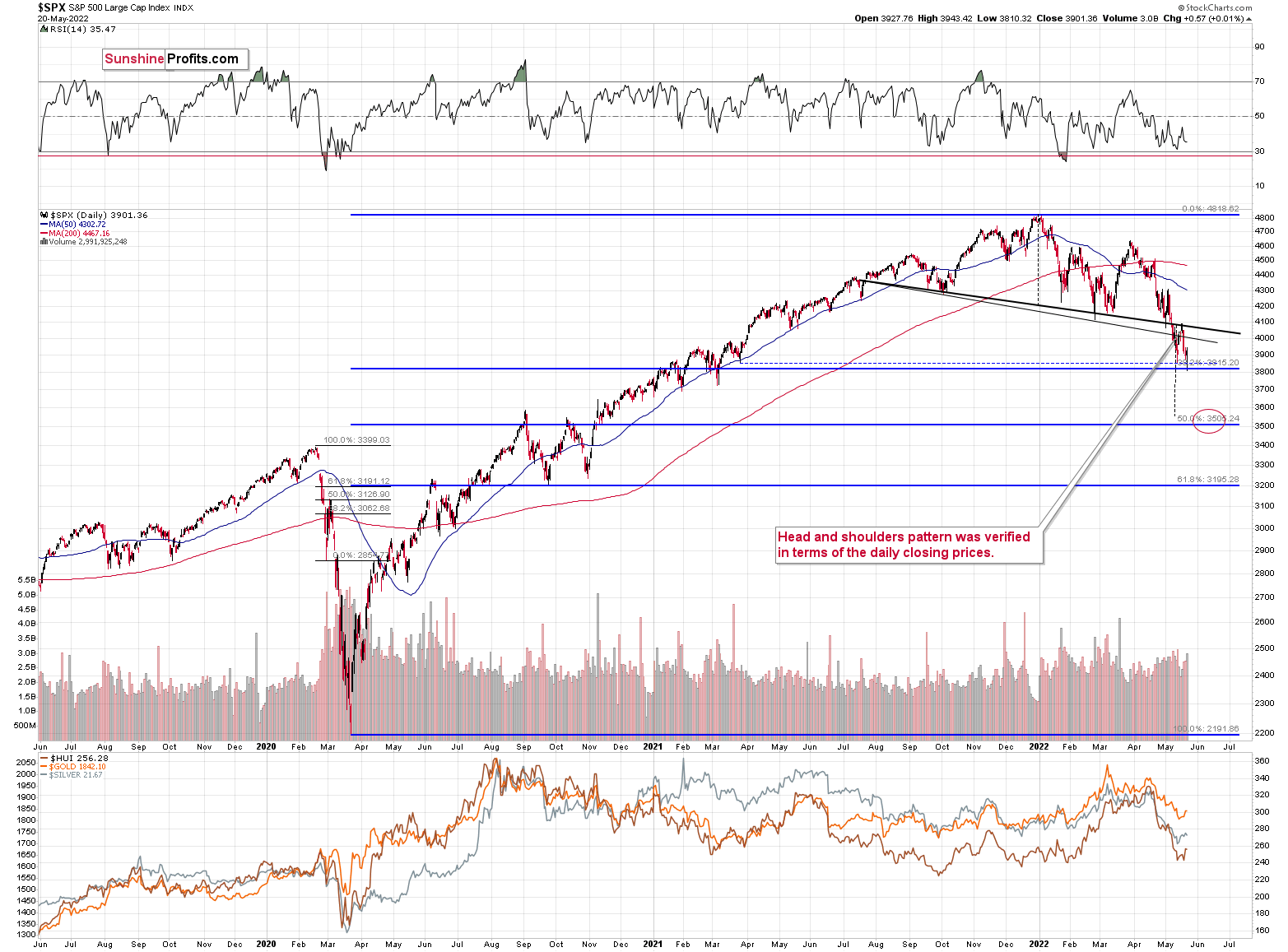

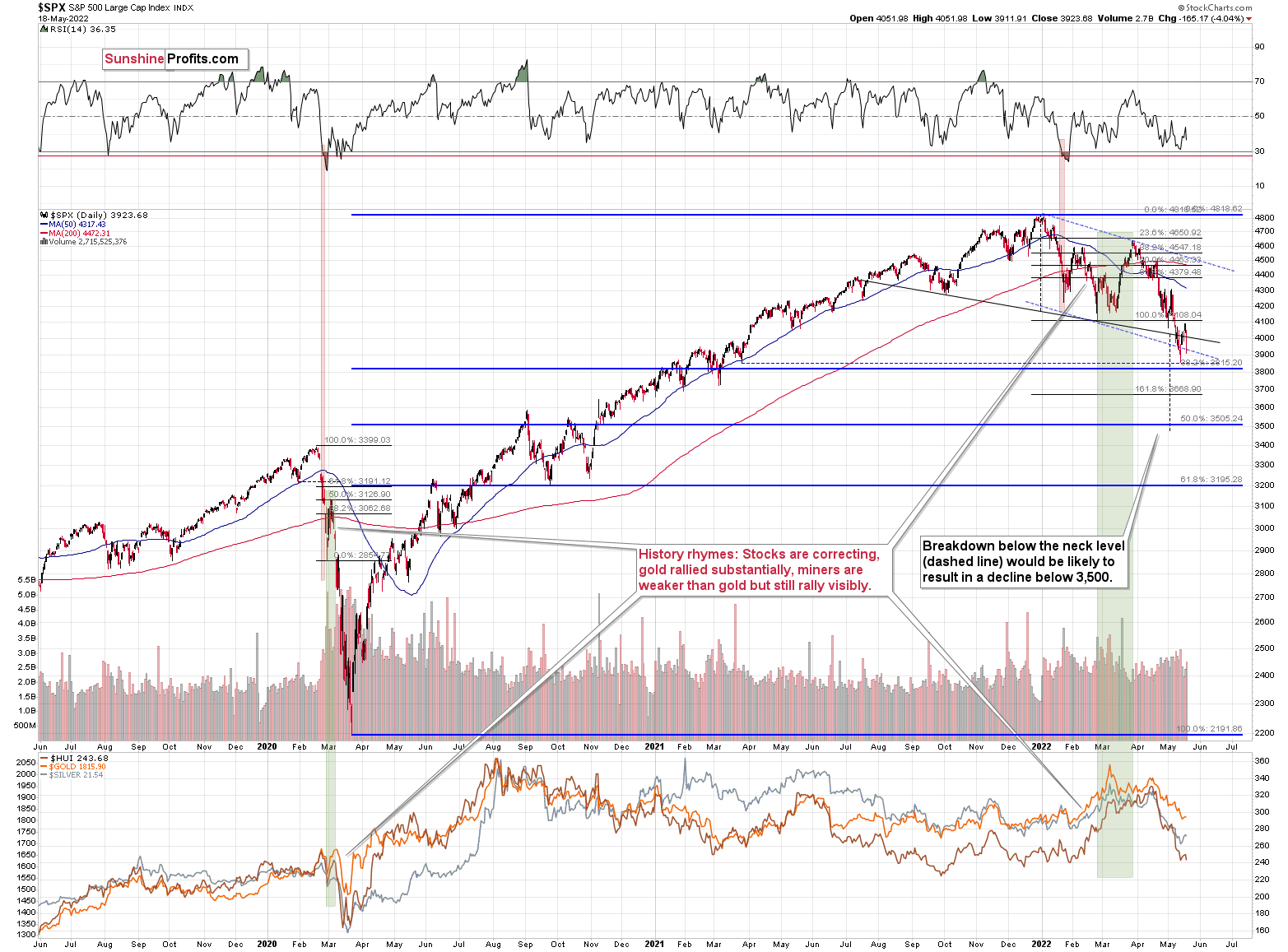

Also, let’s not forget about the forest while looking at the trees. Yesterday’s intraday low in the S&P 500 was 3810.32, which was just about 5 index points below my initial target for this short-term decline at the 38.2% Fibonacci retracement based on the entire 2020 – 2022 rally.

This means that the odds for a short-term rally in stocks have greatly increased.

Gold moved slightly higher as well.

That’s important to note, because the USD Index moved higher by 0.42 yesterday, which “should have” caused gold to decline. It didn’t – gold showed immediate-term strength. This means that the odds are that its rally isn’t over yet.

Also, silver declined by $0.23 yesterday, which means that it’s definitely not outperforming gold. Therefore, the usual confirmation of a top (silver’s immediate-term strength) is absent.

Looking at GDXJ’s 4-hour chart doesn’t provide us with any interesting clues – at least nothing that I haven’t covered previously.

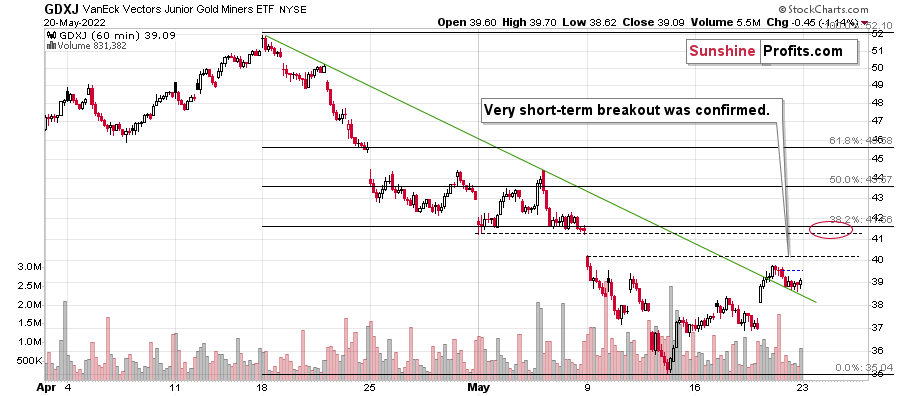

The 1-hour chart, however, tells us something very important.

What we saw yesterday, was actually a verification of a very short-term breakout. The breakout was indeed verified, which means that junior miners can (and are likely to) now rally once again.

In other words, our profits from the long positions are likely to be taken off the table relatively soon, once they are even bigger than they are right now.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few days. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Gold Miners Still on a Rise – Where Will the Top Be?

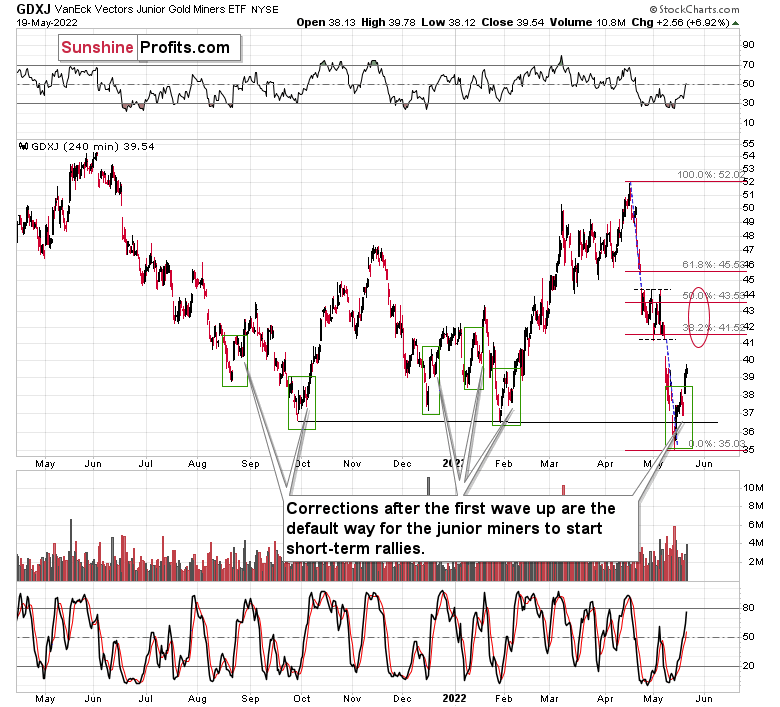

May 20, 2022, 9:04 AMTo answer this question, let’s take a look at what happened in junior mining stocks over the last few days. In yesterday’s analysis, I wrote the following:

Of course, there will be some back-and-forth movement on an intraday basis, but it doesn’t change anything. Junior miners are likely to rally this week nonetheless. And perhaps not longer than that, as the next triangle-vertex-based reversal is just around the corner – on Friday/Monday.

The previous few days were the “forth” and yesterday [May 18] was the “back” movement – so far, my comments remain up-to-date. However, comparing the market action with what I wrote previously isn’t what I meant by analogies to past situations. I meant this:

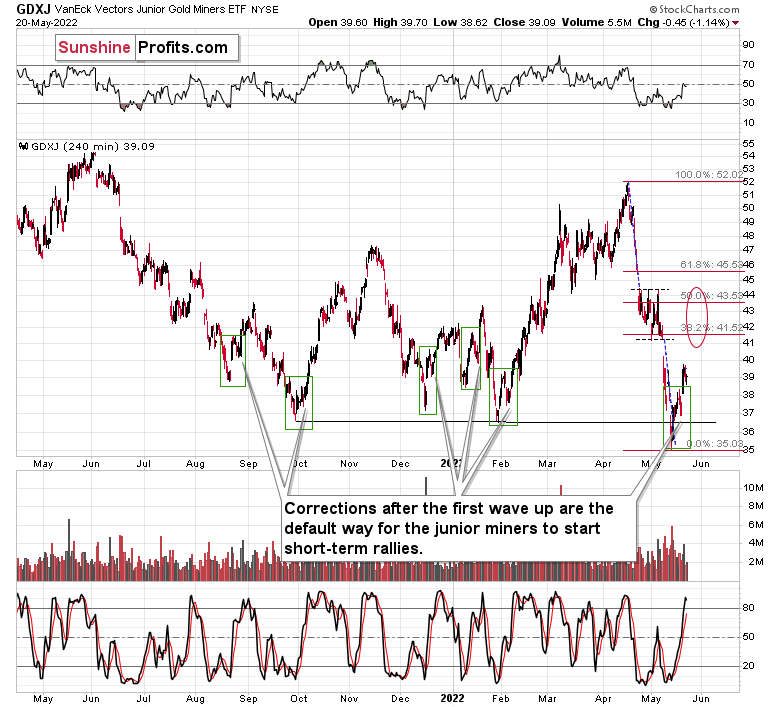

The areas marked with green rectangles are the starting moments of the previous short-term rallies. Some were bigger than others, and yet they all had one thing in common. They all included a corrective downswing after the initial post-bottom rally.

Consequently, what we saw yesterday [May 18] couldn’t be more normal during a short-term rally. This means that yesterday’s decline is not bearish at all and the profits from our long positions are likely to increase in the following days.

Besides, the general stock market declined by over 4%, while the GDXJ (normally moving more than stocks) ETF – a proxy for junior mining stocks – declined by only about 2%.

Well, that’s exactly what happened. Juniors soared yesterday, and so did profits from our long positions (which we managed to open practically right at the bottom).

I would like to clarify one of the points that I made previously with regard to timing the top. I previously wrote that based on the next triangle-vertex-based reversal, it’s likely that the top will take place today (Friday) or on Monday. However, I re-visited the charts to make sure that I got the date right, and when I applied the same methodology on a bigger chart, it turned out that the vertex that I described was already behind us, and that it simply confirmed the bottom when we switched from short to long positions.

Consequently, it’s not very likely that the final top for the rally will take place today or on Monday. It could be the case based on other reasons, but not based on the triangle-vertex-based reversal.

Since gold and silver are likely to move higher, so are junior miners.

I previously wrote that the target for junior miners is at the 38.2% Fibonacci retracement and the recent short-term low, a bit above $41. However, it could be the case that the next resistance is a bit higher, closer to the upper border of the previous consolidation. This could correspond to the 50% Fibonacci retracement close to the $44 level.

Still, remaining conservative and keeping our chances of exiting the current trade and cashing profits at all, I’m keeping the profit-take level intact.

On a very short-term basis, junior miners could be driven by stock market moves. Meanwhile, the stock market appears to be repeating its very recent consolidation pattern.

After stocks’ initial rebound (late April), they declined once again, and then they rallied back up to their previous high before sliding to new lows.

So far, we’re seeing something similar. The initial rebound was indeed followed by a sharp decline. In fact, even the intraday performance is similar. The daily decline was big and sharp, and it was followed by a daily reversal. What followed then was a small daily rally and then a huge daily rally, which was the final top.

If history rhymes, then perhaps today’s or Monday’s (or Tuesday’s) rallies will be significant and take stocks to the final short-term top. This could correspond to a short-term top in junior miners as well.

The above would fit the scenario in which the miners continue to rally for the next 1-3 days.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Here is Why I’m Still Bullish on Gold Miners

May 19, 2022, 7:53 AMThe medium-term outlook for the precious metals remains bearish, but does this mean we can’t profit on shorter-term moves? Quite the opposite!

Precious metals declined yesterday, and so did the general stock market. Is the rally already over?

When I wrote about this rally on May 12, which took place at the same time when I took profits from the short positions and entered the long ones, I mentioned that I planned to hold these long positions for a week or two. Since that was exactly a week ago, the question is: is the top already in?

In short, it probably isn’t. As always, it’s useful to check what happened in the past in similar situations to verify whether what we see is normal or some kind of an outlier that cannot be explained by something that has already happened.

Let’s start with a quote from yesterday’s analysis:

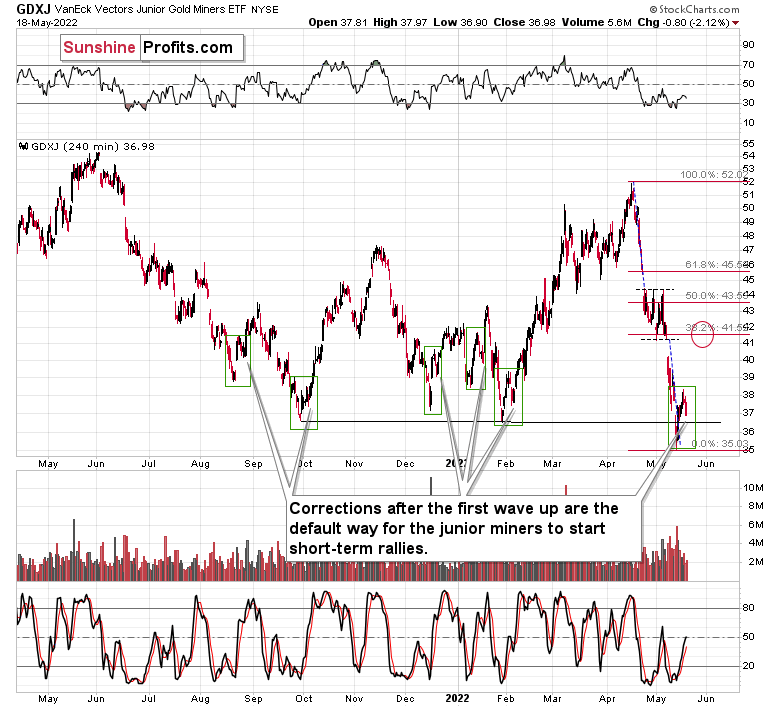

Of course, there will be some back-and-forth movement on an intraday basis, but it doesn’t change anything. Junior miners are likely to rally this week nonetheless. And perhaps not longer than that, as the next triangle-vertex-based reversal is just around the corner – on Friday/Monday.

The previous few days were the “forth” and yesterday was the “back” movement – so far, my comments remain up-to-date. However, comparing the market action with what I wrote previously isn’t what I meant by analogies to past situations. I meant this:

The areas marked with green rectangles are the starting moments of the previous short-term rallies. Some were bigger than others, and yet they all had one thing in common. They all included a corrective downswing after the initial post-bottom rally.

Consequently, what we saw yesterday couldn’t be more normal during a short-term rally. This means that yesterday’s decline is not bearish at all and the profits from our long positions are likely to increase in the following days.

Besides, the general stock market declined by over 4%, while the GDXJ (normally moving more than stocks) ETF – a proxy for junior mining stocks – declined by only about 2%.

If the general stock market continues to decline, junior miners could get a bearish push even if gold prices don’t decline.

However, let’s keep in mind the fact that miners tend to bottom before stocks do – in fact, we saw that in early 2020. This means that even if the S&P 500 moves to new yearly lows shortly and then bounces back up, the downside for miners could be limited, and the stocks’ rebound could trigger a profound immediate-term rally.

If stocks decline, then they have quite strong support at about 3815 – at their 38.2% Fibonacci retracement level.

Let’s keep in mind that junior miners have triangle-vertex-based reversal over the weekend, so they might form some kind of reversal on Friday or Monday.

Ideally, miners would be after a quick rally that is accompanied by huge volume on Friday. This would serve as a perfect confirmation that the top is in or at hand.

However, we can’t tell the market what it should do – we can only respond to what it does and position ourselves accordingly. Consequently, if stocks take miners lower, it could be the case that Friday or Monday will be the time when they bottom. This seems less likely to me than the previous (short-term bullish) scenario, but I’m prepared for it as well. In this case, we’ll simply… wait. Unless we see some major bearish indications, we will wait for the rally to end, perhaps sometime next week.

Again, a nearby top appears more likely than another bottom, in particular in light of what I wrote about the common post-bottom patterns in the GDXJ.

Naturally, as always, I’ll keep my subscribers informed.

Having said that, let’s take a look at the markets from a fundamental point of view.

The Chorus Continues

While investors still struggle with the notion that the Fed can’t bail them out amid soaring inflation, the S&P 500 and the NASDAQ Composite suffered another reality check on May 18. Moreover, with Fed officials continuing to spread their hawkish gospel, I warned on Apr. 6 that demand destruction does not support higher asset prices. I wrote:

Please remember that the Fed needs to slow the U.S. economy to calm inflation, and rising asset prices are mutually exclusive to this goal. Therefore, officials should keep hammering the financial markets until investors finally get the message.

Moreover, with the Fed in inflation-fighting mode and reformed doves warning that the U.S. economy “could teeter” as the drama unfolds, the reality is that there is no easy solution to the Fed’s problem. To calm inflation, it has to kill demand. And as that occurs, investors should suffer a severe crisis of confidence.

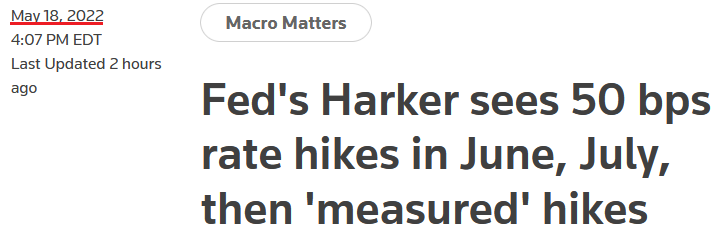

To that point, while the S&P 500 and the NASDAQ Composite plunged on May 18, Fed officials didn't soften their tones. For example, Philadelphia Fed President Patrick Harker said:

"Going forward, if there are no significant changes in the data in the coming weeks, I expect two additional 50 basis point rate hikes in June and July. After that, I anticipate a sequence of increases in the funds rate at a measured pace until we are confident that inflation is moving toward the Committee’s inflation target."

For context, "measured" rate hikes imply quarter-point increments thereafter.

Please see below:

Source: Reuters

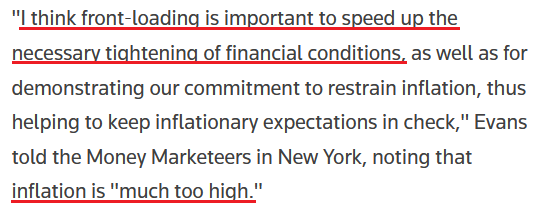

Source: ReutersLikewise, Chicago Fed President Charles Evans delivered a similar message on May 17. He said that by December, "we will have completed any 50 [basis point rate hikes] and have put in place at least a few 25 [basis point rate hikes]."

Moreover, "given the current strength in aggregate demand, strong demand for workers, and the supply-side improvements that I expect to be coming,” he added that “I believe a modestly restrictive stance will still be consistent with a growing economy."

Therefore, while their recent rhetoric had Fed officials “expeditiously” marching toward neutral, now the prospect of a “restrictive stance” has entered the equation. For context, a neutral rate neither stimulates nor suffocates the U.S. economy. However, when the federal funds rate rises above neutral (restrictive), the goal is to materially slow economic activity and consumer spending. As such, the medium-term liquidity drain is profoundly bearish for the S&P 500 and the PMs.

Please see below:

Source: Reuters

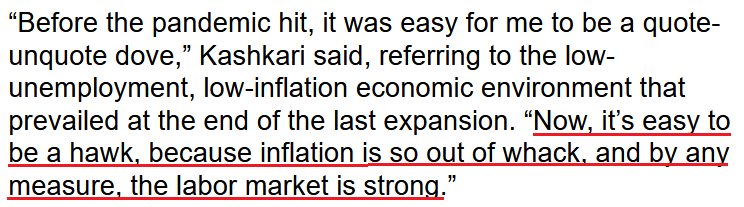

Source: ReutersMaking three of a kind, Minneapolis Fed President Neel Kashkari (a reformed dove) said on May 17 that “My colleagues and I are going to do what we need to do to bring the economy back into balance…”

“What a lot of economists are scratching their heads and wondering about is: if we really have to bring demand down to get inflation in check, is that going to put the economy into recession? And we don’t know.”

For context, Fed officials initially thought inflation was “transitory,” so don’t hold your breath waiting for that “soft landing.” However, while Kashkari is ~16 months too late to the inflation party, he acknowledged the reality on May 17:

Source: Bloomberg

Source: BloombergAs a result, while the S&P 500 and the NASDAQ Composite sell-off in their search for medium-term support, Fed officials haven’t flinched in their hawkish crusade. As such, I’ve long warned that Americans’ living standards take precedence over market multiples.

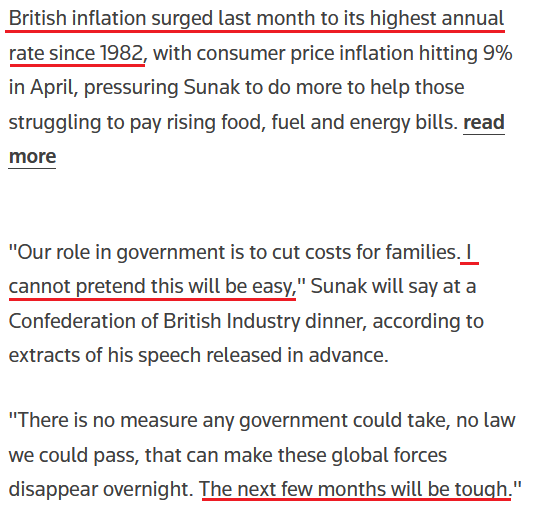

To that point, the U.K. headline Consumer Price Index (CPI) hit 9% year-over-year (YoY) on May 18. For the sake of objectivity, the results underperformed economists’ consensus estimates (the middle column below).

Source: Investing.com

Source: Investing.comHowever, while investors may take solace in the miss, they should focus on the fact that the U.K. output Producer Price Index (PPI) materially outperformed expectations and often leads the headline CPI. As a result, the inflation story is much more troublesome than it seems on the surface.

Please see below:

Source: Investing.com

Source: Investing.comIn addition, British Finance Minister Rishi Sunak warned of a cost of living crisis on May 18, saying that “as the situation evolves our response will evolve” and “we stand ready to do more.”

Please see below:

Source: Reuters

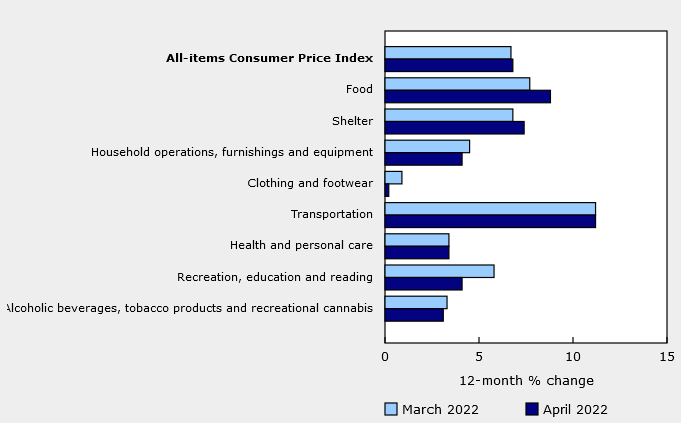

Source: ReutersEven more revealing, I’ve noted on numerous occasions that Canada is the best comparison to the U.S. due to its geographical proximity and its reliance on the U.S. to purchase Canadian exports. Therefore, with Canadian inflation outperforming across the board on May 18, the data paints an ominous portrait of the challenges confronting North American central banks.

Please see below:

Source: Investing.com

Source: Investing.comTo that point, the official report stated:

“Canadians paid 9.7% more in April for food purchased from stores compared with April 2021. This increase, which exceeded 5% for the fifth month in a row, was the largest increase since September 1981. For comparison, from 2010 to 2020, there were five months when prices for food purchased from stores increased at a rate of 5% or higher….

“Basics, such as fresh fruit (+10.0%), fresh vegetables (+8.2%) and meat (+10.1%), were all more expensive in April compared with a year earlier. Prices for starchy foods such as bread (+12.2%), pasta (+19.6%), rice (+7.4%) and cereal products (+13.9%) also increased. Additionally, a cup of coffee (+13.7%) cost more in April 2022 than in April 2021.”

Moreover, “in April, shelter costs rose 7.4% year over year, the fastest pace since June 1983, following a 6.8% increase in March.” Therefore, the data is nearly synonymous with the U.S., and I’ve been warning for months that rent inflation would prove much stickier than investors expected.

Please see below:

Source: Statistics Canada

Source: Statistics CanadaFinally, the investors awaiting a dovish pivot from the Fed assume that growth will overpower inflation. In a nutshell: the U.S. economy will sink into a deep recession in the next couple of months (some believe that we are already in one), and the Fed will resume QE. Moreover, they assume that the inflationary backdrop has left consumers destitute and that we’re a quarter away from famine.

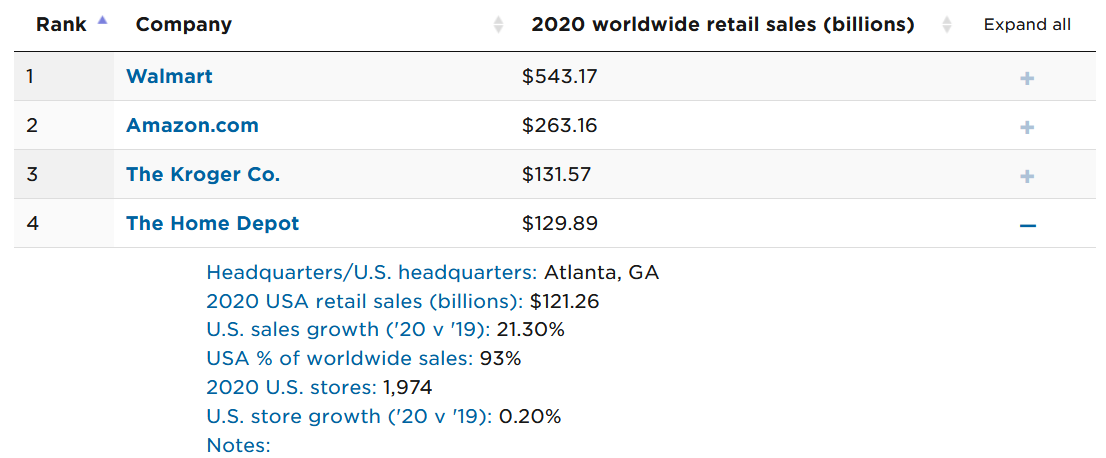

However, I couldn’t disagree more. With Home Depot – which primarily sells discretionary items – noting that consumers are showing no signs of slowing down, I warned on May 18 that investors don’t realize that the Fed’s war with inflation would be one of attrition.

Please see below:

Source: Home Depot/The Motley FoolFor context, the National Retail Federation (NRF) listed Home Depot as the fourth-largest retailer in the U.S. in its 2021 report. As a result, the company's performance is a reliable indicator of U.S. consumer spending.

Source: NRF

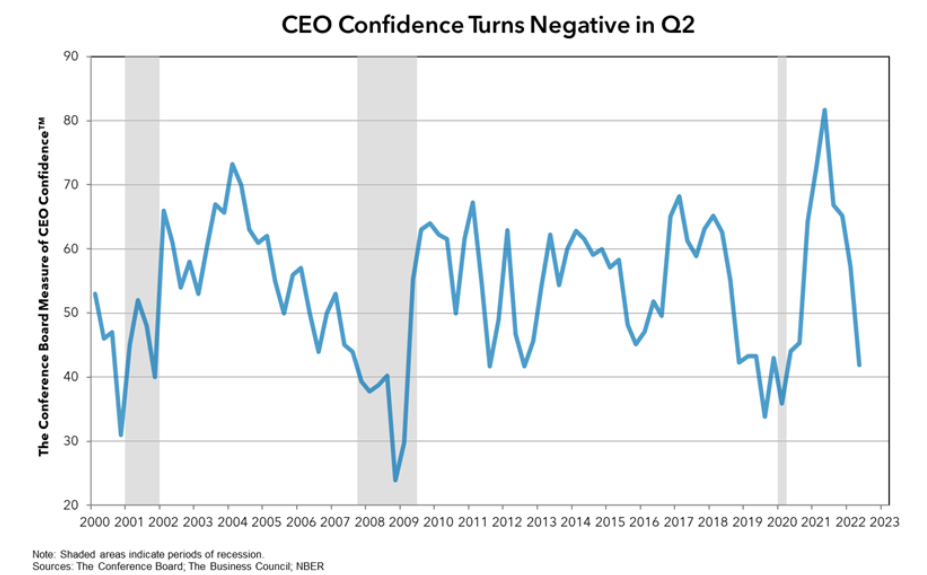

Source: NRFTo that point, The Confidence Board released its U.S. CEO Confidence survey on May 18. The report revealed:

CEO confidence “declined for the fourth consecutive quarter in Q2 2022. The measure now stands at 42, down from 57 in Q1. The measure has fallen into negative territory and is at levels not seen since the onset of the pandemic. (A reading below 50 points reflects more negative than positive responses.)”

Please see below:

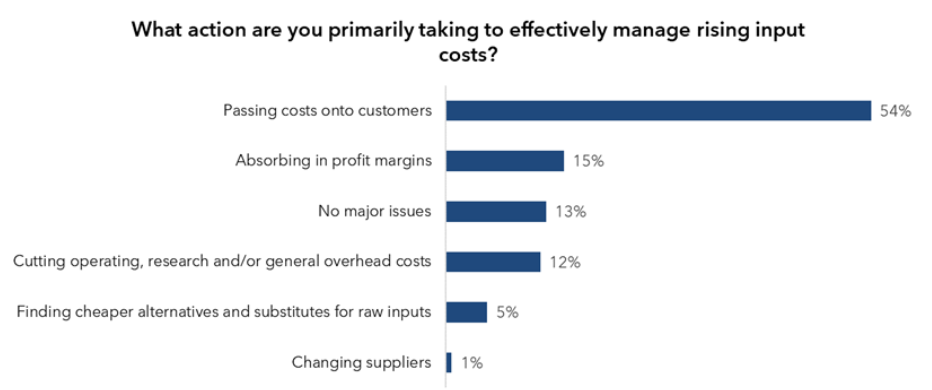

However, the devil is in the details and the details are what matter to the Fed. For example:

“More than half (54%) of CEOs said they were effectively managing rising input costs by passing along costs to customers, while 13% said they had no major issues with input costs.”

Source: The Confidence Board

Source: The Confidence BoardSecond:

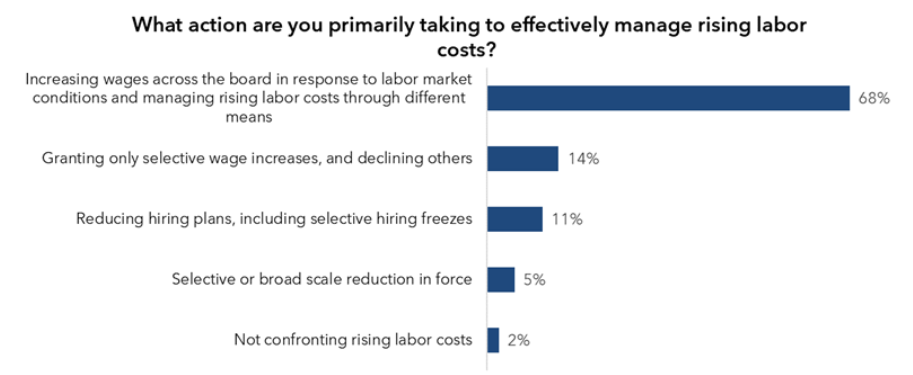

“More than two-thirds of CEOs said they are increasing wages across the board in response to labor market conditions and managing rising labor costs through different means.”

Source: The Confidence Board

Source: The Confidence BoardMore importantly, though:

Source: The Confidence Board

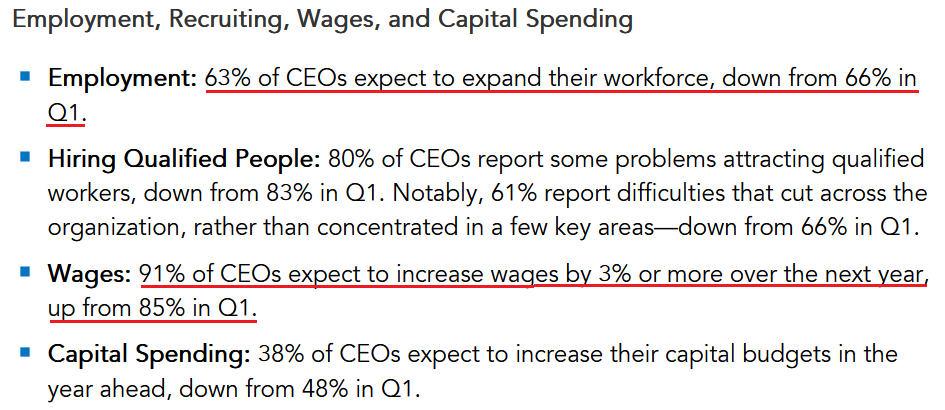

Source: The Confidence BoardTherefore, while consolidated CEO confidence has crashed to “levels not seen since the onset of the pandemic,” nearly two-thirds of CEOs plan to increase their workforce and more than nine out of 10 plan to increase wages. As a result, would major U.S. corporations be adding employees and paying them more if demand has fallen off a cliff? Of course not. Moreover, when considering the 15-point drop in consolidated CEO confidence, the three-point decline in employment expectations is largely immaterial.

The bottom line? While investors keep using the post-GFC script as their roadmap for when the Fed turns dovish, they don’t realize that 1970s/1980s-like inflation is a completely different animal. Thus, what I wrote on May 18 should prove prescient in the coming months:

While Powell keeps warning investors of what’s to come, a decade of dovish pivots has a generation of investors believing that the central bank is all talk and no action. However, with inflation at levels unseen in 40+ years, Powell is not out of ammunition, and the Fed followers should suffer profound disappointment as the drama unfolds.

In conclusion, the PMs declined on May 18, as risk-off sentiment returned to the financial markets. However, since fits and starts are always expected along the way, the GDXJ ETF should have more upside in the coming days, and profits from our long position should increase. The medium-term outlook for the mining stocks remains bearish, though.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM