tools spotlight

-

What Will the Fed Choose: Recession or an Economic Crisis?

April 29, 2022, 6:33 AMThis week was all about earnings, as some of Wall Street’s heavyweights released their quarterly reports. Moreover, while mixed results caused sentiment to swing from one extreme to the other, inflation remains front and center, and the outlook for Fed policy is bullish.

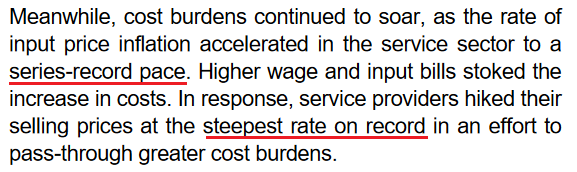

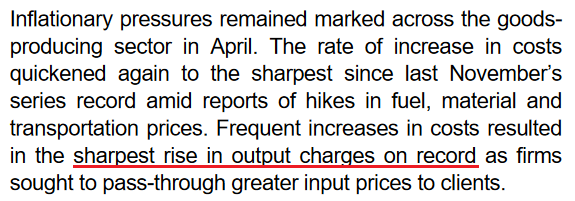

For example, whether it’s PepsiCo, Mondelez, or Whirlpool, companies have warned that inflation remains extremely problematic. Moreover, with American Express and Visa highlighting consumers’ eagerness to spend, the pricing pressures show no signs of slowing down. Likewise, S&P Global released its U.S. Composite PMI on Apr. 22, and I wrote on Apr. 25 that it was another all-time high for inflation.

Isolating services:

Source: S&P Global

Source: S&P GlobalIsolating manufacturing:

Source: S&P Global

Source: S&P GlobalWith growth, employment and inflation supporting several rate hikes over the next several months, there is little in the release that implies a dovish U-turn. To that point, please remember that the survey was conducted from Apr. 11 to Apr. 21. Therefore, while investors hope that decelerating growth and inflation will allow the Fed to back off, the PMI data suggests otherwise. As such, the Fed’s conundrum continues to intensify.

Furthermore, with more appetizing earnings reports released on Apr. 28, the results were even more bullish for Fed policy. Likewise, with the PMs’ force fields wearing off, they should suffer profoundly as rate hike volatility increases. For example, McDonald’s released its first-quarter earnings on Apr. 28. CFO Kevin Ozan said during the Q1 earnings call:

“In the U.S., I think last quarter, I mentioned that we thought commodities were going to be up roughly 8% or so for the U.S. That number is now more like 12% to 14% for the year. So U.S. commodities clearly have risen (…).”

“On the labor side, in the U.S., it's probably over 10% right now. Part of that is because you'll recall that we made adjustments to our wages in our company-owned restaurants mid-year last year, so we haven't lapped that. So part of it is due to that and part of it is due to just continued wage inflation.”

As a result, the Fed is losing control of the inflation situation, and the largest restaurant chain in the world is still sounding the alarm. Therefore, with the pricing pressures unwilling to abate on their own (which I’ve warned about for some time), killing demand is the only way to reduce the wage-price spiral.

Please see below:

Source: McDonald’s/Seeking Alpha

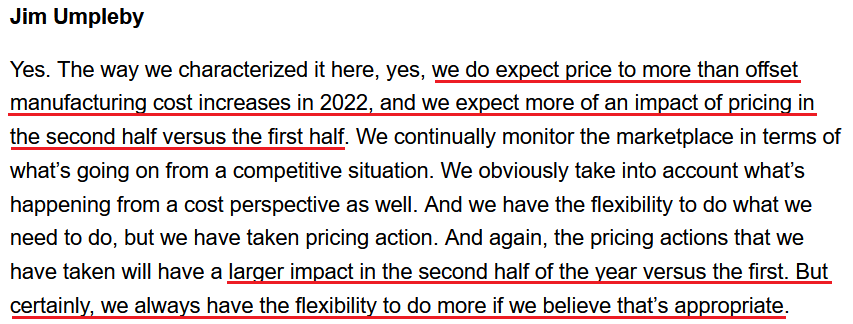

Source: McDonald’s/Seeking AlphaOn top of that, Caterpillar released its first-quarter earnings on Apr. 28. For context, the company is the world's largest construction equipment manufacturer. CFO Andrew Bonfield said during the Q1 earnings call:

“We remain encouraged by the strong demand for our products and services. The first quarter of 2022 marked the fifth consecutive quarter of higher end user demand compared to the prior year. Services remained strong in the quarter. We continue to make progress on our service initiatives, including customer value agreements, e-commerce, connected assets and prioritized service events.”

CEO Jim Umpleby added:

“Absent the supply chain constraints, our top line would have been even stronger. When the supply chain conditions ease, we expect to be well positioned to fully meet demand and gain operating leverage from higher volumes.”

Thus, with each new earnings season, companies note that demand remains resilient. As a result, why not raise prices and capitalize on too much stimulus?

Source: Caterpillar/Seeking Alpha

Source: Caterpillar/Seeking AlphaAs expected, the “transitory” camp waved the white flag in 2022. However, the merry-go-round of input/output inflation was visible from a mile away. For example, remember what I wrote on Mar. 30, 2021?

Didn’t Powell insist that near-term inflation was only “one-time” and “transient”? Well, despite government-issued CPI data failing to capture the effect of the Fed’s liquidity circus, pricing pressures are popping up everywhere. And with corporations’ decision tree left to raising prices or accepting lower margins, which one do you think they’ll choose?

Continuing the theme, Domino's Pizza reported its first-quarter earnings on Apr. 28. For context, the company is the largest pizza chain in the U.S. Moreover, when contrasting the quarterly results of Microsoft and Alphabet on Apr. 28, I wrote that investors fail to realize that some companies have succumbed to the medium-term realities sooner than others. Therefore, Domino's Pizza is another example. CEO Ritch Allison said during the Q1 earnings call:

“Consistent with our communications during our prior earnings call, we faced significant inflationary cost increases across the business in Q1. Those cost pressures combined with the deleveraging from the decline in U.S. same-store sales resulted in earnings falling short of our high expectations for the business (…).”

“We believe that we will continue to face pressure both on the top line for our U.S. business and on our bottom line earnings over the next few quarters. While we remain very optimistic about our ability to drive long-term profitable growth in the near-term 2022 is shaping up to be a challenging year.”

CFO Sandeep Reddy added:

“In addition, we would like to update the guidance we provided in March for 2022. Based on the continuously evolving inflationary environment, we now expect the increase in the store food basket within our U.S. system to range from 10% to 12% as compared to 2021 levels.”

If that wasn’t enough, with unprecedented handouts reducing U.S. citizens’ incentive to work, staffing shortages materially impacted Domino’s Q1 results. Moreover, the development is extremely inflationary and only increases the chances of future interest rate hikes.

Please see below:

Source: Domino’s Pizza/Seeking Alpha

Source: Domino’s Pizza/Seeking AlphaTherefore, while I've warned on numerous occasions that the Fed is in a lose-lose situation, investors still hold out hope for a dovish pivot. However, they fail to understand the consequences. For example, a dovish 180 is extremely unlikely in this environment; but even if officials completely reversed course, the long-term economic damage would be even more paramount.

When companies are saddled with input pressures, even value-oriented chains like Domino's Pizza can only endure margin erosion for so long. Thus, with management searching for new ways to appease investors, Fed officials' patience will only cause an even bigger long-term collapse once inflationary demand destruction unfolds.

Please see below:

Source: Domino’s Pizza/Seeking Alpha

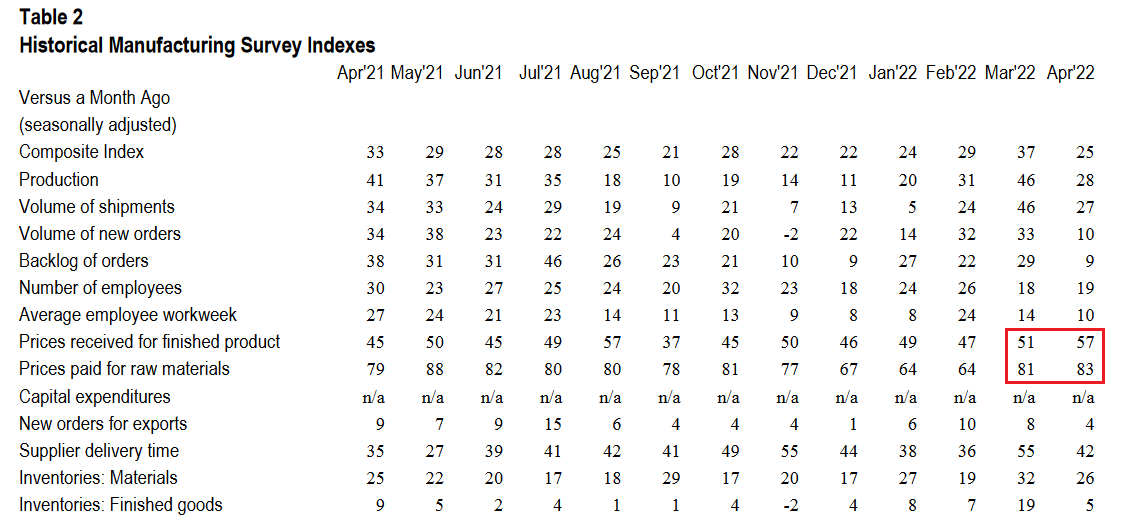

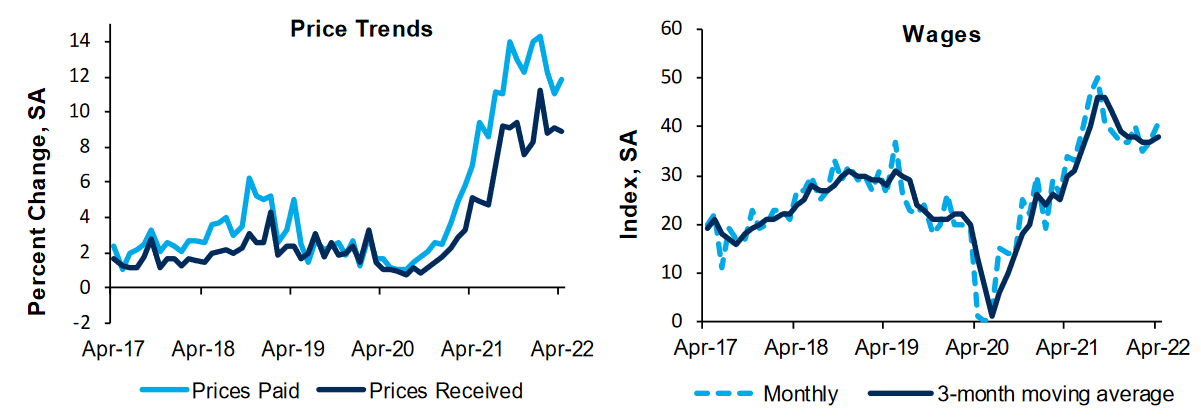

Source: Domino’s Pizza/Seeking AlphaTurning to the macroeconomic front, some interesting data also hit the wire on Apr. 28. For example, the Kansas City Fed released its Tenth District Manufacturing Survey. The headline index declined from 37 in March to 25 in April. Chad Wilkerson, Vice President and Economist at the KC Fed, said:

“The pace of regional factory growth eased somewhat but remained strong. Firms continued to report issues with higher input prices, increased supply chain disruptions, and labor shortages. However, firms were optimistic about future activity and reported little impact from higher interest rates.”

To that point, both the prices paid and received indexes increased month-over-month (MoM).

Please see below:

Source: KC Fed

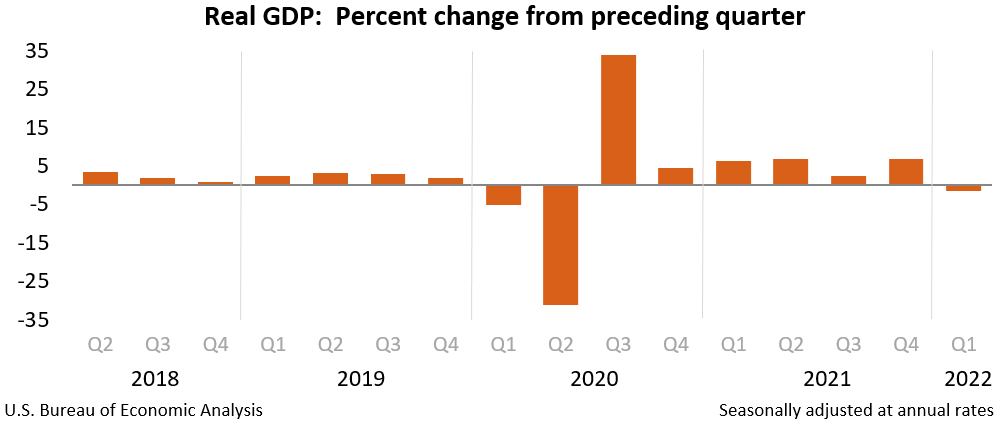

Source: KC FedFinally, the major surprise on Apr. 28 was that U.S. real GDP contracted by 1.4% (advance estimate) in Q1. The report stated: “The decrease in real GDP reflected decreases in private inventory investment, exports, federal government spending, and state and local government spending, while imports, which are a subtraction in the calculation of GDP, increased.”

However: “Personal consumption expenditures (PCE), nonresidential fixed investment, and residential fixed investment increased.”

Therefore, with supply chain disruptions leading to import stockpiling (which hurts GDP), net trade was the weak link. However, the dynamic should reverse in Q2 and Q3, and if so, shouldn’t impact the Fed’s rate hike cycle.

The bottom line? The Fed is stuck between a rock and a hard place: deal with inflation now and (likely) push the U.S. into a recession later or ignore inflation and watch an even bigger crisis unfold down the road. As such, the first option is the most likely outcome. Remember, while Fed officials may seem out of touch, they’re not stupid, and history shows the devastating consequences of letting unabated inflation fester. Therefore, interest rate hikes should dominate the headlines over the next several months, and the PMs and the S&P 500 should suffer mightily along the way.

In conclusion, the PMs were mixed on Apr. 28, as silver was the daily underperformer. Moreover, while mining stocks were boosted by the S&P 500, the ‘buy the dip’ crowd is fighting a losing battle. With Amazon and Apple down after the bell on Apr. 28, weak earnings guidance should also dominate the headlines in the months to come. As a result, with the USD Index on fire and real yields poised to continue their ascent, the PMs’ medium-term outlooks are extremely treacherous.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- May 2: ISM Manufacturing PMI

Like this week’s S&P Global Report, ISM’s report is one of the most important data points because it covers growth, inflation, and employment across the entire U.S. Therefore, the results are more relevant than regional surveys.

- May 3: JOLTS job openings

Since the lagged data covers March’s figures, it’s less relevant than leading data like the PMIs. However, it’s still important to monitor how government-tallied results are shaping up.

- May 4: ADP private payrolls, ISM Services PMI, FOMC statement and press conference

With the FOMC poised to hike interest rates by 50 basis points on May 4, the results and Powell’s comments are the most important fundamental developments of the week. However, ADP’s private payrolls will also provide insight into the health of the U.S. labor market, while the ISM’s Services PMI will have similar implications as the manufacturing PMI. Moreover, both will provide clues about future Fed policy.

- May 5: Challenger jobs cuts

With the data showcasing how many employees were fired in April, it’s another indicator of the health of the U.S. labor market.

- May 6: Nonfarm payrolls, unemployment rate, average hourly earnings

Half of the Fed’s dual mandate is maximum employment, so continued strength in nonfarm payrolls is bullish for Fed policy. In addition, a low unemployment rate is also helpful, while average hourly earnings will showcase the current state of wage inflation.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Are Gold Miners in a Stalemate on the Market Chessboard?

April 28, 2022, 8:20 AMWith the GDXJ ETF suffering a mild drawdown on Apr. 27, the recent rout has calmed for the time being. However, with the medium-term fundamental outlook remaining profoundly bearish, the junior miners and the S&P 500 are fighting a losing battle.

To explain, the Fed needs to lower asset prices to help calm inflation. Moreover, with the earnings season delivering some hit-and-miss results, market participants are dumping the losers and holding on to the winners for dear life. However, while investors rotate from one scarred corner of the stock market to another, the hiding places are shrinking. Therefore, when the walls close in, the only place left to go is down.

For example, Microsoft hit, Alphabet missed, and RBC Capital Markets analysts said that Microsoft’s “solid” fourth-quarter guidance “should allay investor fears of a macro slowdown.” As a result, the bull is alive and well.

Please see below:

Source: Barrons

Source: BarronsMissing the forest through the trees, investors fail to realize that some companies have succumbed to the medium-term realities sooner than others. For context, I’ve been bullish on the U.S. economy for some time, and I still am RIGHT NOW. However, with each Fed rate hike and each passing quarter, that will change materially, and so should investors’ optimism.

Please see below:

Source: Google Finance

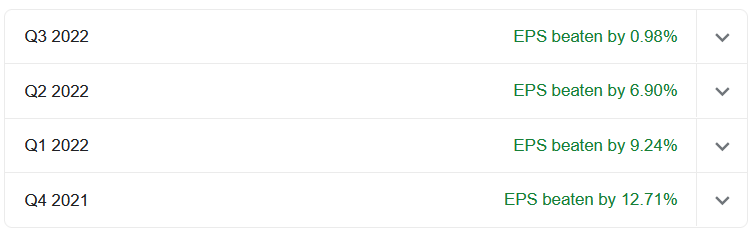

Source: Google FinanceWhen You Gain, the Fed Inflicts Pain

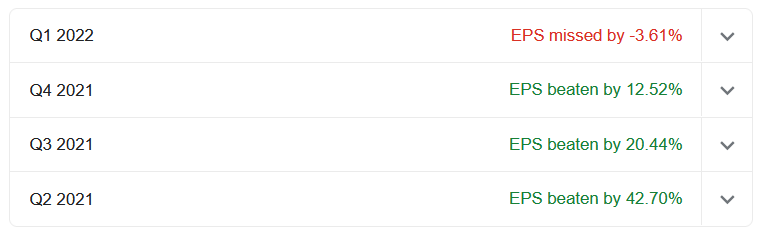

To explain, the figures above represent Google Finance’s tally of how much Microsoft outperformed analysts’ earnings per share (EPS) estimates over the last four quarters. Notice the trend? After beating estimates by 12.71% in Q4 2021, Microsoft’s EPS outperformance declined sequentially to a slight 0.98% in Q3 2022. Moreover, its revenue outperformance showcased a similar pattern.

Furthermore, the decelerating trend is also present with Alphabet, only ahead of schedule. As a result, with the Fed poised to slow the U.S. economy to calm inflation, it’s only a matter of time before the stock market’s winners (Microsoft) turn into losers (Alphabet).

Source: Google Finance

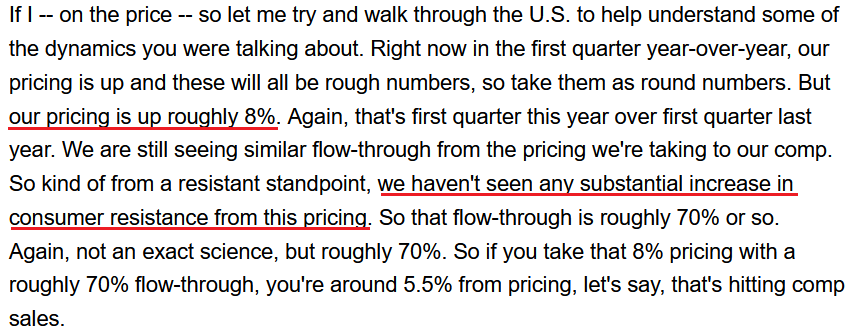

Source: Google FinanceSpeaking of winners, Visa reported its second-quarter earnings on Apr. 26. CEO Al Kelly said during the Q2 earnings call:

“After the short four to five-week impact of Omicron in December and January in the United States and many other parts of the world, the recovery continues to be robust…. In the U.S., payments volume index to 2019 was 144 in the quarter. Volume growth relative to three years ago has been stable and strong now for four quarters in a row.”

“When looking at specific spend categories for credit cards, we saw greater than a 10-percentage point improvement in the three-year index from Q1 to Q2 in travel, retail goods, food and drug, restaurant, QSR and fuel.”

As a result, while investors hope that a slowing U.S. economy will allow a dovish 180 by the Fed, Visa hasn’t seen any demand description.

Please see below:

Source: Visa/The Motley Fool

Source: Visa/The Motley Fool Furthermore, with consumers eager to spend, companies are eager to raise prices. For example, Mondelez released its first-quarter earnings on Apr. 26. The company is home to confectionary brands like Oreo, Cadbury, Ritz and Toblerone. CFO Luca Zaramella said during the Q1 earnings call:

“We now expect input cost inflation in the low double-digit range for 2022 versus our prior view of approximately 8%, despite our coverage is approaching 90% for the year. The revise view of inflation reflects the war in the Ukraine and the related step-up in cost pressure to our commodity basket, including energy, wheat, oil and packaging.”

He added:

“We continue to expect pricing to be a larger driver of top line growth, given its impact in Q1 and we are also announcing price increases across a number of markets for the rest of the year tied to inflation.”

As a result, the Fed can’t wish its problems away, and these hawkish realities should spook investors over the next few months.

Please see below:

Source: Mondelez/Seeking Alpha

Source: Mondelez/Seeking AlphaSinging a similar tune, PepsiCo released its first-quarter earnings on Apr. 26. CFO Hugh Johnston said during the Q1 earnings call:

“Inflation has clearly gotten a bit more challenging for the year. No question about that. We had previously indicated it was low teens. It’s several points higher than that now (…).”

“We think the consumer is very early in this process of adjusting to the new inflationary environment. I think there’s going to be new behaviors adapting to the new realities.”

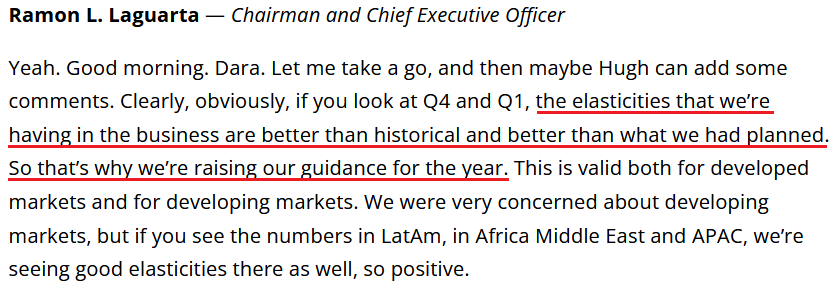

As such, while Johnston didn’t mention any specifics on pricing, “new realities” are not what the Fed had in mind. Moreover, CEO Ramon Laguarta raised PepsiCo’s full-year guidance and added that elasticities are still outperforming. Therefore, with inflation “several points higher” than previously expected, would you bet that PepsiCo isn’t riding the inflationary merry-go-round?

For context, positive elasticities mean that when PepsiCo increases prices, it’s not seeing a drop-off in demand.

Please see below:

Source: PepsiCo/Alpha Street

Source: PepsiCo/Alpha StreetThus, while the U.S. economy remains on solid footing RIGHT NOW, the reality is that all of this data is bullish for Fed policy. With companies still raising prices and receiving little pushback from consumers, we're nowhere near the demand destruction needed to reduce annualized inflation from 8.6% to 2%. As such, the Fed will have to do the heavy lifting.

Moreover, while investors breathe a sigh of relief that corporate profits haven't collapsed, the optimism is short-sighted. Of course, a recession isn't upon us; the Fed has only hiked interest rates once. The damage occurs after the fourth, fifth, sixth, etc., rate hike, as higher interest rates eat away at consumers' disposable income and depress corporate profits. Therefore, the current environment is full of clear skies. However, if you want to get 8.6% annualized inflation down, everything else likely goes down with it.

Also noteworthy, the Richmond Fed released its Fifth District Survey of Manufacturing Activity on Apr. 26. The data was largely bullish for Fed policy. The report revealed:

“Our wage index increased to 41 in April from 37, and firms don’t expect the increase in wages to let up. The average growth rate of prices paid increased slightly in April while the growth rate of prices received from customers edged down slightly. Firms expect growth rates for both prices paid and prices received to decrease somewhat in the next 12 months.”

Please see below:

Source: Richmond Fed

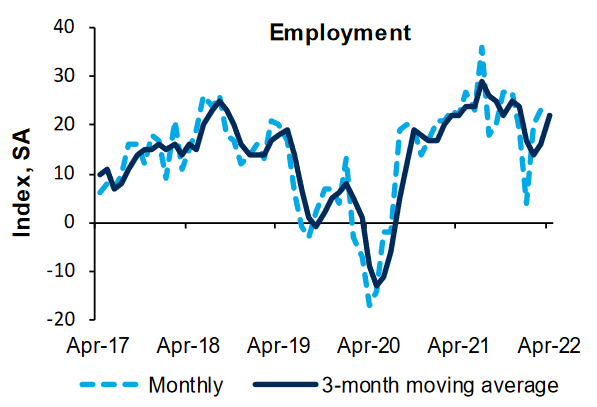

Source: Richmond FedLikewise, with employment also moving higher, continued strength in the U.S. labor market is also bullish for Fed policy.

Source: Richmond Fed

Source: Richmond FedIn addition, the Dallas Fed released its Texas Manufacturing Outlook Survey on Apr. 25. Showcasing similar results, the data is also supportive of Fed policy. An excerpt from the report read:

“Prices and wages continued to increase strongly in April, though the indexes eased off their historical highs. The raw materials prices index fell 13 points to 61.5, its lowest reading in more than a year, though still well above its average of 27.7. The finished goods prices index moved down from 47.8 to 43.5. The wages and benefits index came in at 50.9, down slightly from its high last month of 55.2 but still markedly elevated from its average reading of 20.1.”

Finally, the Dallas Fed released its Texas Service Sector Outlook Survey on Apr. 26. Similar to the other reports above, inflation increased, though at a slower pace in April. The report stated:

“April saw continued upward pressure on wages and prices, though growth in wages and input prices eased slightly. The wages and benefits index fell from 36.5 to 33.0, still near a record high. The selling prices index was unchanged at 33.7, with 37 percent of respondents noting monthly price increases, while the input prices index declined five points to 54.2.”

The bottom line? While investors are supposed to be forward-looking, they fail to realize that current earnings and guidance don’t reflect the impact of future rate hikes. Moreover, with the Fed on a mission to curb inflation, quarterly price increases and robust elasticities are not helping the situation. As a result, once this reality hits home, the PMs will suffer mightily as the negativity cascades across Wall Street.

In conclusion, the PMs declined on Apr. 27, as commodities have lost some of their mojo. Moreover, while technical conditions may present an opportunity for a short-term rally, both technicals and fundamentals signal lower lows over a medium-term time horizon. As such, long-term buying opportunities will likely present themselves later in 2022.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Inflation, the USDX, Real Yields: The Doom Trio Hangs Over Gold

April 27, 2022, 10:10 AMDespite the reality check, investors keep up their buying spree. Meanwhile, problematic events are starting to gain on gold, silver, and mining stocks.

With reality rearing its ugly head recently, the S&P 500 and the GDXJ ETF have suffered mightily. Moreover, while I’ve been warning for months that investors underestimated the implications of rampant inflation, the chickens have come home to roost. To explain, I wrote on Oct. 26:

Originally, the Fed forecasted that it wouldn’t have to taper its asset purchases until well into 2022. However, surging inflation pulled that forecast forward. Now, the Fed forecasts that it won’t have to raise interest rates until well into 2023. However, surging inflation will likely pull that forecast forward as well.

Moreover, I added on Nov. 4, following the FOMC meeting:

With Fed Chairman Jerome Powell still searching for his inflationary shooting star, the FOMC chief isn’t ready to label inflation as problematic. “I don’t think that we’re behind the curve,” he said. “I actually believe that policy is well-positioned to address the range of plausible outcomes, and that’s what we need to do.”

The reality is: while Powell has taken the path of least resistance to help calm inflation (the taper), his inability to understand the realities on the ground leaves plenty of room for hawkish shifts in the coming months (interest rate hikes).

Thus, while Powell has shifted his stance materially and Fed officials now expect seven to 12 rate hikes in 2022, the financial markets initially ignored the repercussions. However, always late to the party, the consensus now fears that the medium-term outlook has lost its luster.

Please see below:

Source: CNBC

Source: CNBCLikewise, while the fundamental implications have been loud and clear for months, sentiment doesn’t die easily. However, since reality is undefeated, the impact of evaporating liquidity is becoming too much to bear. To explain, I wrote on Feb. 2:

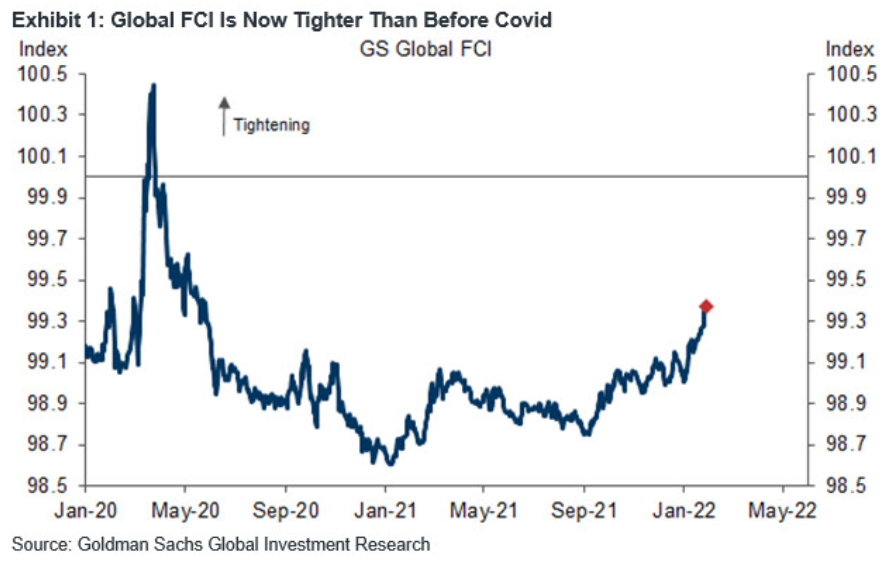

If you analyze the right side of the chart, you can see that the FCI has surpassed its pre-COVID-19 high (January 2020). Moreover, the FCI bottomed in January 2021 and has been seeking higher ground ever since. In the process, it's no coincidence that the PMs have suffered mightily since January 2021. Furthermore, with the Fed poised to raise interest rates at its March monetary policy meeting, the FCI should continue its ascent. As a result, the PMs' relief rallies should fall flat, like in 2021.

Likewise, while the USD Index has come down from its recent high, it's no coincidence that the dollar basket bottomed with the FCI in January 2021 and hit a new high with the FCI in January 2022. Thus, while the recent consolidation may seem troubling, the medium-term fundamentals supporting the greenback remain robust.

I provided an update on Apr. 13:

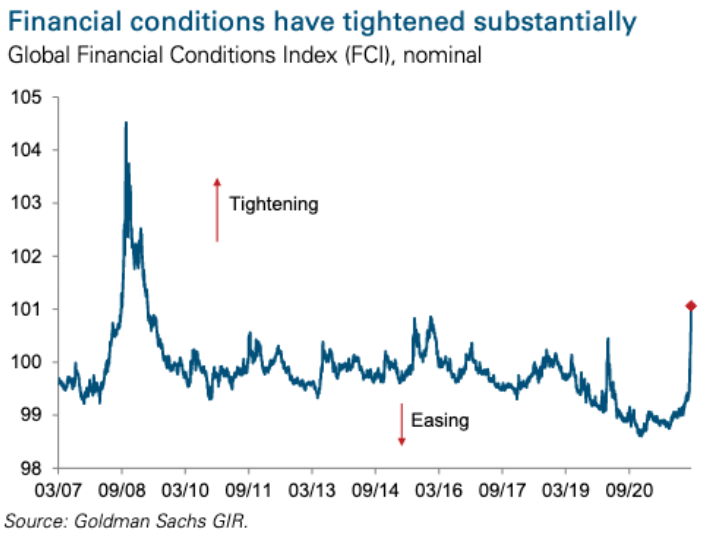

While the USD Index has surpassed 100 and reflects the fundamental reality of a higher FCI and higher real yields, the PMs do not. However, the PMs are in la la land since the FCI is now at its highest level since the global financial crisis (GFC).

Please see below:

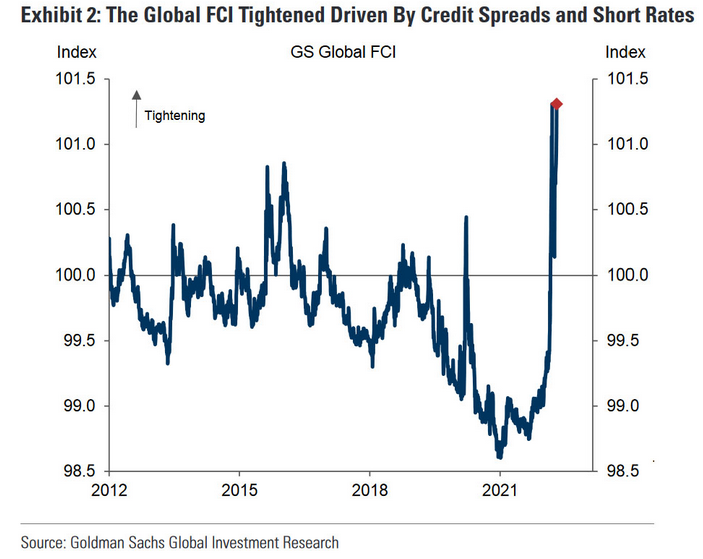

Also noteworthy, the FCI made quick work of the March 2020 high from the first chart above. Again, Fed officials know that higher real yields and tighter financial conditions are needed to curb inflation. That’s why they keep amplifying their hawkish message and warning investors of what lies ahead. However, with commodities refusing to accept this reality, they’ll likely be the hardest-hit once the Fed’s rate hike cycle truly unfolds.

Surprise, surprise: after surpassing its March 2020 highs, the FCI has continued its ascent.

Please see below:

Who Could’ve Seen This Coming?

As a result, while the Russia-Ukraine conflict and misguided optimism disrupted our bearish timeline, the important point is that investors can only ignore technical and fundamental realities for so long. With a resurgent USD Index and rising real yields, which are profoundly bearish for the PMs, the latter have come down from their recent highs.

Moreover, with the general stock market's suffering adding to the GDXJ ETF's ills, the junior miners have underperformed their precious metals counterparts, which has been very beneficial for our short position.

However, the bearish medium-term thesis remains unchanged: inflation is problematic, the Fed is hawked up, and a higher USD Index and higher real yields should materialize in the coming months.

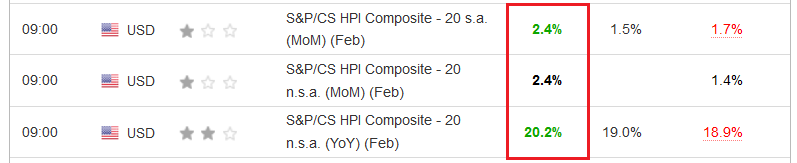

Case in point: while February's lagging data may not reflect the impact of rising mortgage rates, the S&P/Case-Shiller U.S. National Home Price Index surged by more than 20% year-over-year (YoY) on Apr. 26 and outperformed expectations (19%). As a result, the data is profoundly bullish for shelter inflation, which accounts for more than 30% of the headline Consumer Price Index's (CPI) movement.

Please see below:

Source: Investing.com

Source: Investing.comAlso noteworthy, Whirlpool released its first-quarter earnings on Apr. 25. For context, the company manufacturers home and kitchen appliances like washing machines, dryers, refrigerators, and stand mixers. CEO Marc Bitzer said during the Q1 earnings call:

“As our industry and most other industries face historical levels of cost inflation, we observed over $400 million in the fourth quarter, or approximately a 10% increase on cost of goods sold. Despite this, we delivered over 9% ongoing EBIT margins and over 16% EBIT margins in our North America business, again demonstrating the earnings strength of the region and the actions we took, transforming margins over the years.”

“We now expect higher levels of inflation to persist throughout the year and have increased our full year cost inflation expectations by $600 million to $1.8 billion.”

However, is Whirlpool waiting for the Fed to solve the problem?

“Our first quarter results demonstrate that we are a different Whirlpool, delivering structurally improved EBIT margins no matter the operating environment. We have the right actions in place to deliver a solid 2022, including our previously announced cost-based price increases of 5% to 18%, addressing inflation across the globe.”

To that point, due to the time lag between incurring costs and implementing price hikes, Bitzer said that more increases are scheduled for the back half of 2022.

Please see below:

Source: Whirlpool/Seeking Alpha

Source: Whirlpool/Seeking AlphaOn top of that, Indeed released its latest State of the Labor Market report on Apr. 21. An excerpt read:

“Employer demand for seasonal work is growing in line with pre-pandemic trends, with summer job postings on Indeed soaring 40.1% above their February 1, 2022 baseline as of April 10 (…).”

“Seasonal postings on Indeed for spring and summer jobs comprise a variety of positions. Some of these jobs, like camp counselor and lifeguard, fit the traditional summer mold. But more general roles, like retail sales associate and cashier, make strong showings too.”

However:

“Domestic job seeker interest in seasonal jobs lags prior year trends. As of April 10, the 2022 share of domestic job seeker searches for seasonal work was respectively 27.6% and 16.9% below the comparable periods in 2019 and 2021.”

Please see below:

To explain, the blue and green lines above track U.S. citizens’ interest in seasonal work in 2019 and 2021 (before/after the height of the pandemic), while the pink line above tracks their current interest. As you can see, there is a clear underperformance.

More importantly, the combination of normalized demand and insufficient supply is extremely inflationary. With demand “growing in line with pre-pandemic trends,” while supply is roughly 17% to 28% below comparable periods, it should put upward pressure on wage inflation. Moreover, remember what I wrote on Apr. 22?

Powell said on Apr. 21 that the U.S. labor market is "too hot" and that the Fed needs to cool it down. "It is a very, very good labor market for workers," he said. "It is our job to get it into a better place where supply and demand are closer together."

As a result, he understands the problem. However, reducing 8.6% annualized inflation without impairing the U.S. labor market is like trying to hit a hole in one on the golf course.

Please see below:

Source: CNBC

Source: CNBCFinally, The Conference Board released its Consumer Confidence Index on Apr. 26. The headline index decreased from 107.6 in March to 107.3 in April, and Lynn Franco, Senior Director of Economic Indicators at The Conference Board, said:

“The Present Situation Index declined, but remains quite high, suggesting the economy continued to expand in early Q2. Expectations, while still weak, did not deteriorate further amid high prices, especially at the gas pump, and the war in Ukraine. Vacation intentions cooled but intentions to buy big-ticket items like automobiles and many appliances rose somewhat.”

All in all, the data is largely inconclusive, as there are some good and some bad results. However, since “concerns about inflation retreated from an all-time high in March but remained elevated,” more QE is far from the right medicine.

The bottom line? While I warned on Apr. 8 that when sentiment shifts, the PMs will confront one of the worst domestic fundamental environments since late 2018, the troublesome developments are catching up to gold, silver, and mining stocks. However, despite their recent drawdowns, the PMs are still trading well above their medium-term-trend-based fair values. Therefore, more pain should materialize over the medium term. It seems that we might see a sharp rebound in the near future, though (after PMs decline some more).

In conclusion, the PMs were mixed on Apr. 26, as mining stocks continued their material underperformance. Moreover, while investors will likely remain in ‘buy the dip’ mode until the very end, lower highs and lower lows should confront the S&P 500 and the PMs over the next few months. As a result, the medium-term outlook for the GDXJ ETF is profoundly bearish.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Shop Til You Drop – Investors Continue Their Buying Frenzy

April 26, 2022, 9:16 AMWhile investors’ optimism suffers a death by a thousand cuts, I’ve warned on numerous occasions that old habits die hard. As a result, while the financial markets teetered near a breaking point on Apr. 25, the ‘buy the dip’ crowd swooped in and pushed the S&P 500 higher. In the process, the GDXJ ETF also closed off its lows.

However, the lessons investors learned after the global financial crisis (GFC) should be their undoing this time around. To explain, investors buy the dip in hopes that the Fed will come to their rescue. With the strategy making money more often than not since the GFC, why not continue the charade?

Well, the reality is that optimism is contagious. Therefore, when the S&P 500 refuses to die, other areas of the financial markets showcase similar resiliency. However, with higher asset prices antithetical to the Fed’s goal of taming inflation, buying dips should result in even more pain over the medium term. For context, I wrote on Apr. 6:

Please remember that the Fed needs to slow the U.S. economy to calm inflation, and rising asset prices are mutually exclusive to this goal. Therefore, officials should keep hammering the financial markets until investors finally get the message.

Moreover, with the Fed in inflation-fighting mode and reformed doves warning that the U.S. economy “could teeter” as the drama unfolds, the reality is that there is no easy solution to the Fed’s problem. To calm inflation, it has to kill demand. As that occurs, investors should suffer a severe crisis of confidence.

Thus, with the optimistic close on Apr. 25 only reinforcing the thesis, investors don’t realize that they’re digging their own graves.

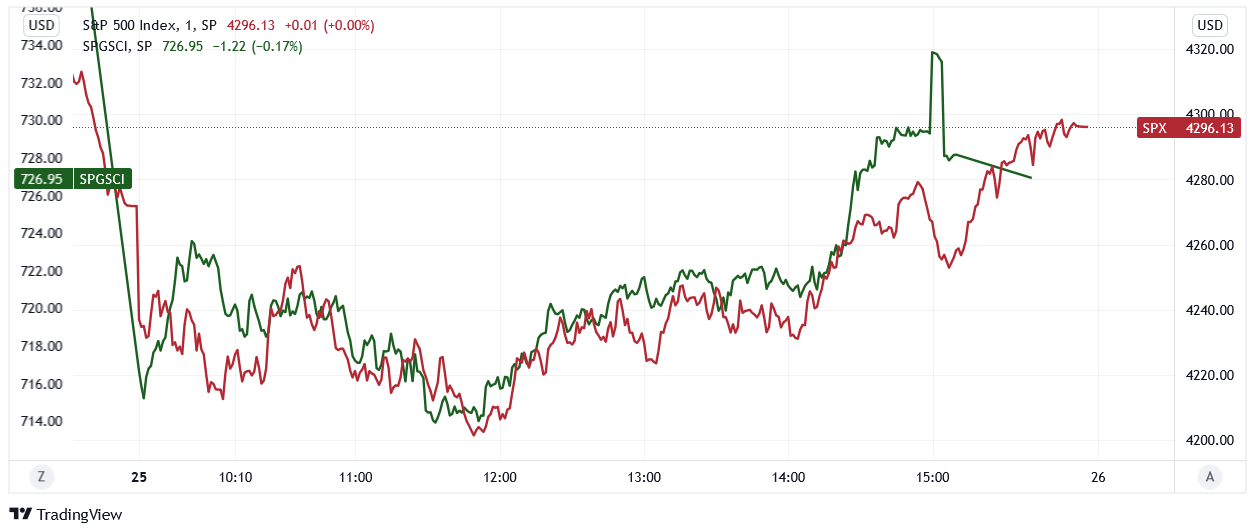

Please see below:

To explain, the red line above tracks the one-minute movement of the S&P 500, while the green line above tracks the one-minute movement of the S&P Goldman Sachs Commodity Index (S&P GSCI). If you analyze the relationship, you can see that both sank at the open, bottomed mid-day, then rallied off of the lows.

However, the important point is that the Fed needs the S&P GSCI to decline to curb inflation. Therefore, when the index says to the S&P 500, “I go where you go,” buying the dip only encourages more hawkish actions from the Fed.

Remember, post-GFC was a period of relatively low inflation and outperformance by technology stocks. As a result, the Fed would be happy to replicate that environment once again. However, with commodities unwilling to decline materially unless the S&P 500 and the NASDAQ Composite follow suit, the more the latter rally, the more inflation remains. As such, investors’ inability to see the forest through the trees should cause them plenty of pain over the next few months.

To that point, I warned previously that Canada is the hawkish canary in the coal mine. With more than 76% of Canadian exports sent to the U.S. in February, the two economies are increasingly intertwined. Moreover, I noted on Apr. 14 and updated on Apr. 22 how the Bank of Canada (BoC) announced a jumbo rate hike and that Canadian inflation is still raging. I wrote:

The BoC announced a 50 basis point rate hike on Apr. 13, and with the Fed likely to follow suit in May, the domestic fundamental environment confronting the PMs couldn’t be more bearish.

Please see below:

Source: BoC

Source: BoCMoreover, BoC Governor Tiff Macklem (Canada's Jerome Powell) said: "We are committed to using our policy interest rate to return inflation to target and will do so forcefully if needed."

Furthermore, while he added that the BoC could "pause our tightening" if inflation subsides, he cautioned that "we may need to take rates modestly above neutral for a period to bring demand and supply back into balance and inflation back to target."

However, with the latter much more likely than the former, the BoC's decision is likely a preview of what the Fed should deliver in the months ahead.

To that point, Canadian inflation data was released on Apr. 20, and, surprise, surprise, the scorching results came in hotter than expected. For context, the figures in the middle column represent economists’ consensus estimates.

Please see below:

Source: Investing.com

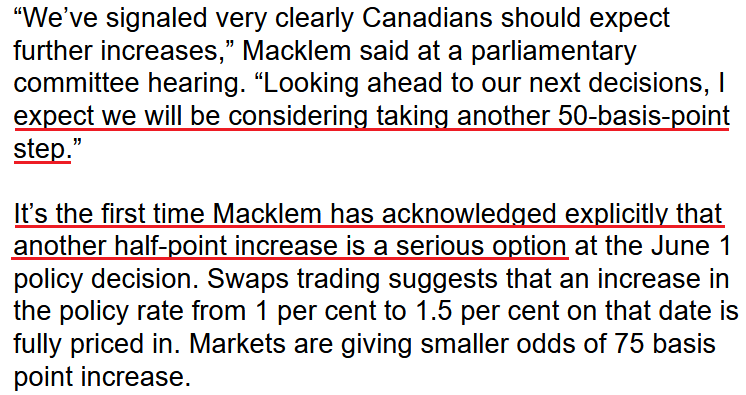

Source: Investing.comFurthermore, after admitting that the first 50 basis point rate hike in 20 years was an “unusual step,” Macklem said on Apr. 25 that investors should expect more of the same in the coming months.

Please see below:

Source: Bloomberg

Source: BloombergAgain, the Canadian economy is highly leveraged to U.S. economic growth. Therefore, with Macklem increasingly willing to fire a second 50 basis point bullet, the Fed shouldn’t be far behind.

Likewise, Canadian headline inflation hit 6.7% year-over-year (YoY) in March, while the U.S. stands at 8.6%. Thus, with the buy the dippers making Macklem and Fed Chairman Jerome Powel’s jobs even more difficult, don’t be surprised if they drop the hawkish hammer over the medium term.

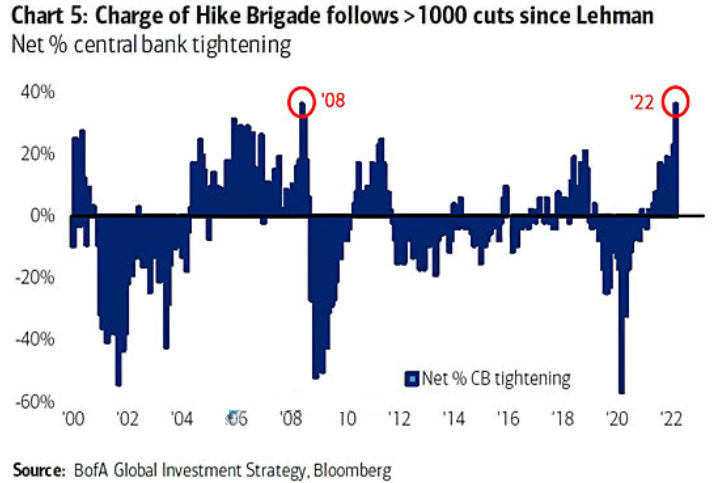

In addition, while Bank of America notes that the “Hike Brigade” has already staged an offensive, the ramifications of evaporating liquidity are far from priced in.

Please see below:

You Can’t Run From Reality

To explain, the blue bars above track the net percentage of global central banks tightening monetary policy. If you analyze the two red circles above, you can see that the current state of play rivals the lead-up to the GFC. Moreover, the Fed has barely even started its hiking cycle, and if investors keep buying the dip, the BoC may be talking about a third 50 basis point rate hike. As a result, the domestic fundamental environment is profoundly bearish for the PMs.

Furthermore, while Fed officials have warned about the potential “collateral damage” from their war with inflation, I warned on Apr. 6 that recessionary winds should gain steam in the coming months. I wrote:

Does a U.S. economy that “could teeter” sound bullish for the S&P 500 or the PMs? Moreover, while [Daly’s] relatively optimistic assessment assumes that a recession is unlikely, the data suggests otherwise. With annualized inflation at ~8% and the latest PMI and rental market data signaling even more price increases in March, plenty of demand destruction needs to unfold to reduce inflation to normalized levels.

Expecting just that, the Federal National Mortgage Association (Fannie Mae) – a U.S. government-sponsored enterprise – released its Economic and Housing Outlook report on Apr. 19. An excerpt reads:

“Our updated forecast includes an expectation of a modest recession in the latter half of 2023 (…).”

“While a ‘soft landing’ for the economy is possible, which is where inflation subsides without economic contraction, historically such an outcome is an exception, not the norm. With the most recent inflation readings at levels not seen since the early 1980s and wage growth exceeding that which is consistent with a 2-percent inflation objective, we believe the odds of a soft landing are even lower.”

Please see below:

Source: Fannie Mae

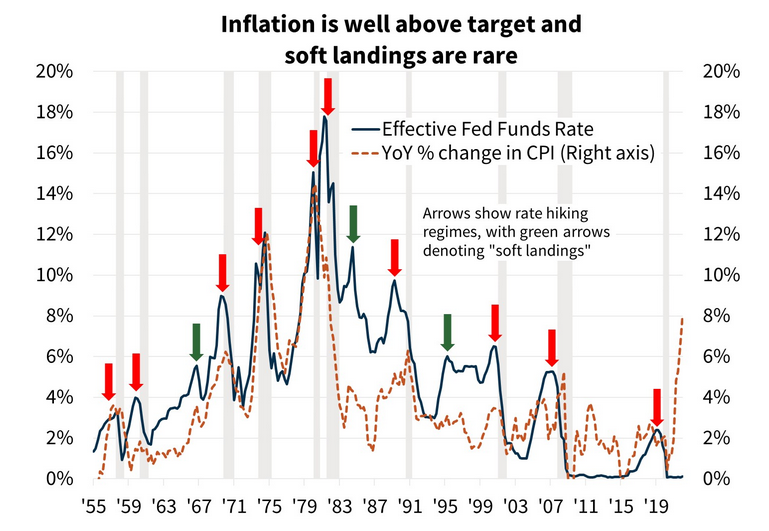

Source: Fannie MaeTo explain, the green line above tracks the U.S. federal funds rate, while the dashed brown line above tracks the YoY percentage change in the headline Consumer Price Index (CPI). More importantly, the red arrows above depict hard landings, while the green arrows above depict soft landings. As such, the odds are not in the Fed’s favor.

Even more revealing, if you analyze the green arrows near 67, 83, and 95, you can see that the YoY inflation (the dotted brown line) was no more than ~4.5%. As a result, all of the soft landings occurred alongside manageable inflation, not a headline CPI of 8.6%.

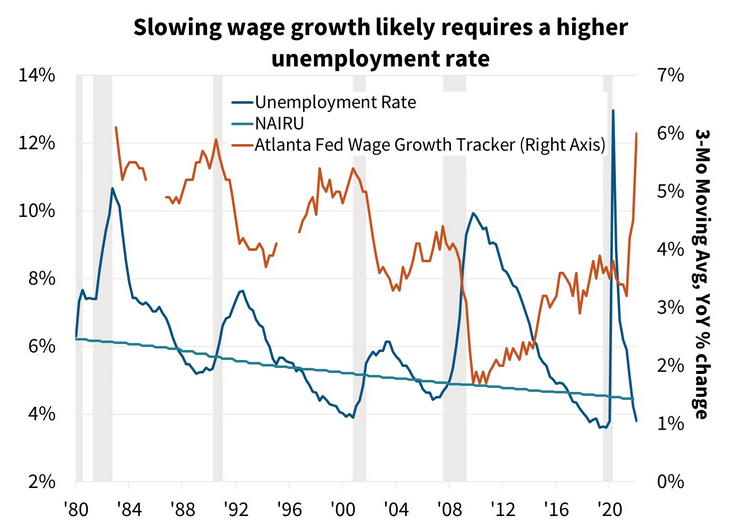

On top of that, with the Fed letting the U.S. labor market run too hot for too long – as evidenced by the nearly five million more job openings than unemployed – the Fed needs to increase the unemployment rate to curb wage inflation. Moreover, with the blue line below (unemployment) near an all-time low and the brown line below (wage inflation) at/near an all-time high, does a reversal of fortunes sound like fun for the U.S. economy?

Fannie Mae analysts stated:

“The unemployment rate is below the ‘full employment’ level, inflation is accelerating as growth slows, and the Federal Reserve is beginning to tighten policy. These conditions typically mark the beginning of the end of an economic expansion.”

Source: Fannie Mae

Source: Fannie MaeThe bottom line? While investors remain all-in on the post-GFC playbook, the reality is that this time is different. Before, the Fed could bow down to the financial markets without impacting the real economy. Now, inflation is raging, and the Fed can’t run from this reality. Not only will the economic consequences worsen the longer the Fed waits, but I’ve noted the political ramifications on numerous occasions. As a result, plenty of hawkish fireworks should erupt over the medium term.

In conclusion, the PMs declined on Apr. 25, as fundamental realities stifled sentiment. Unless the Fed performs the most reckless dovish pivot of all-time (highly unlikely), the PMs should suffer profound drawdowns over the next few months.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Gold Stocks: Are We Witnessing the Onset of a Major Collapse?

April 25, 2022, 6:53 AMAfter gold ran out of steam, the market was flooded by a wave of invalidated breakouts. Can anything keep the precious metals from nosediving?

Remember when gold tried to rally above $2,000? It was just a week ago. Now, it’s likely about to drop below $1,900, silver and mining stocks are sliding too. While the white metal has been weak for a while now, mining stocks finally woke up to the reality and appear to be catching up with gold’s and stocks’ declines.

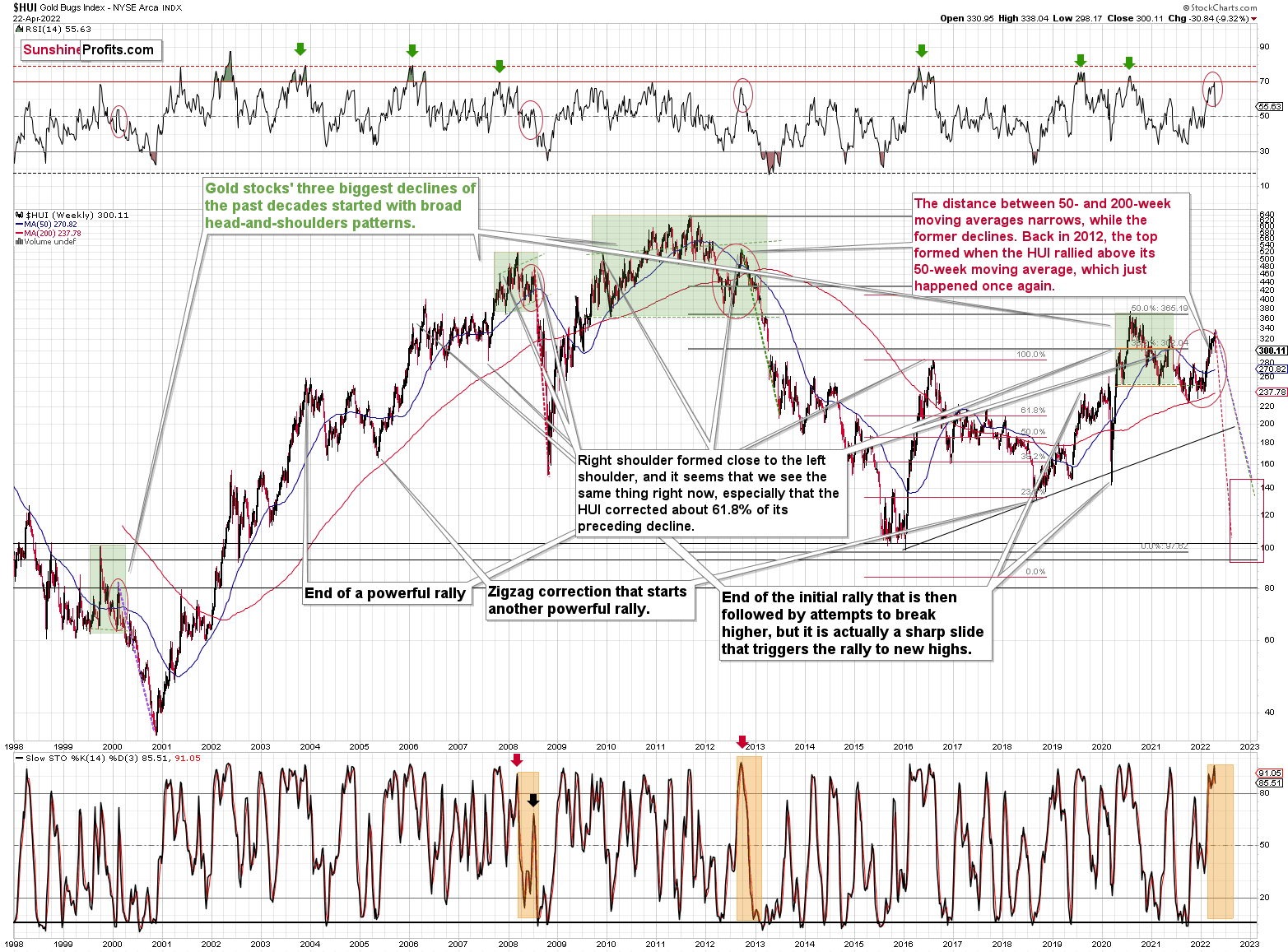

Boy, they sure have some catching up to do! Even though last week’s ~10% decline might appear terrific, let’s keep in mind that this is most likely just the beginning of a huge slide, probably quite similar to what we saw in 2012, 2013, and in 2008.

Let’s start today’s analysis with a quick look at changes in the long-term HUI Index chart – the flagship proxy for gold stocks.

We saw a powerful weekly reversal, a decline in the RSI indicator from about 70, which confirmed the previous sell signal, and a fresh medium-term sell signal from the stochastic indicator.

In particular, the weekly reversal and the sell signal from stochastic are important, as they closely link last week with what we saw right after the final top in 2008 and 2012.

History is likely about to rhyme, and the implications are extremely bearish for mining stocks for the next few months.

Let’s zoom in.

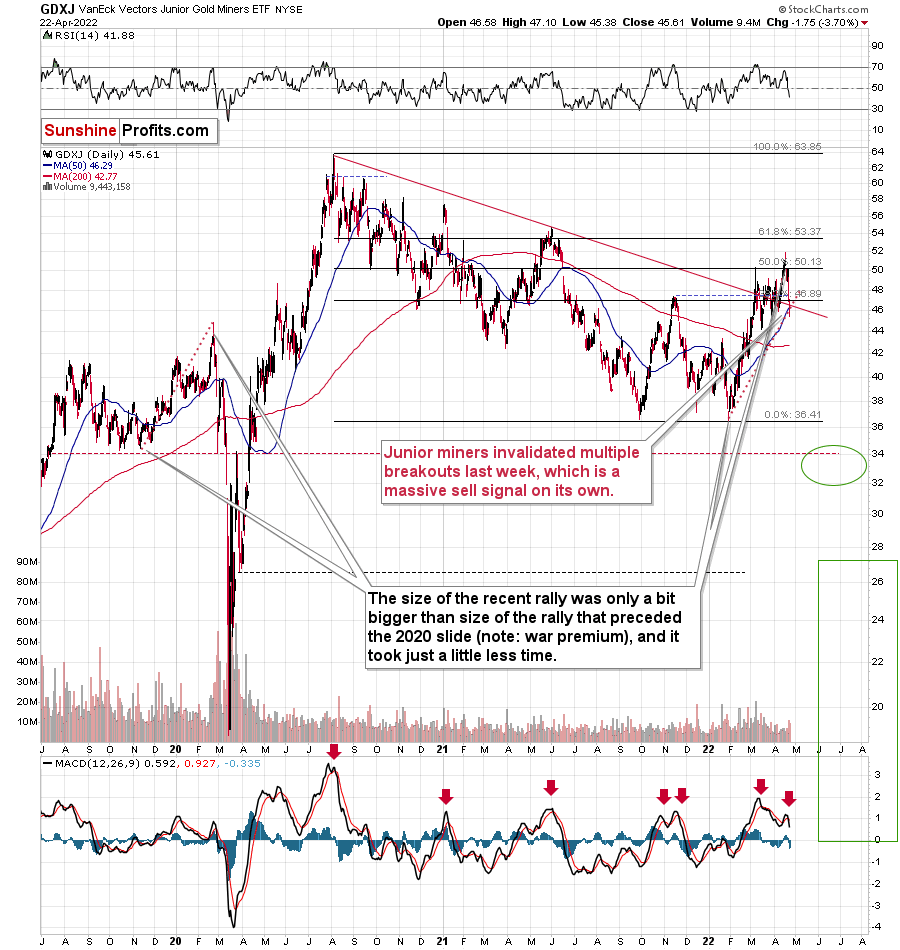

While senior gold stocks declined by a bit less than 10%, junior miners fell by a bit more than 10% last week.

However, that’s the least important fact about this sector.

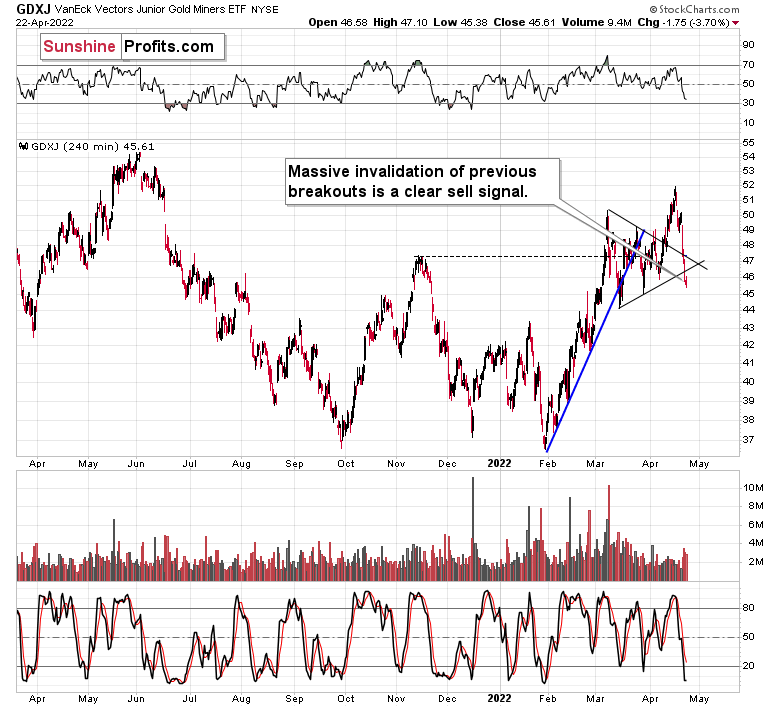

The key thing is that practically all the seemingly bullish breakouts that we saw recently were just invalidated.

The breakout above the declining red resistance line was invalidated.

The breakout above the late-2021 high was invalidated.

The breakout above the 50% Fibonacci retracement level based on the 2020-2022 decline had been (earlier) invalidated.

The breakout above the upper border of the previous triangle pattern was invalidated.

The breakout above the lower border of the previous triangle pattern was invalidated.

That’s a sell signal on top of a sell signal, on top of a sell signal, on top of a sell signal, on top of a sell signal.

We saw sell signals from the GDXJ-based MACD indicator too.

Speaking of the triangle on the above chart, its vertex is at the end of April, so we might see some kind of turnaround then – perhaps a volatile comeback, which is then followed by another – even bigger – slide.

This would fit the gold chart too.

Gold has a triangle-vertex-based reversal point nearby, so they both confirm each other.

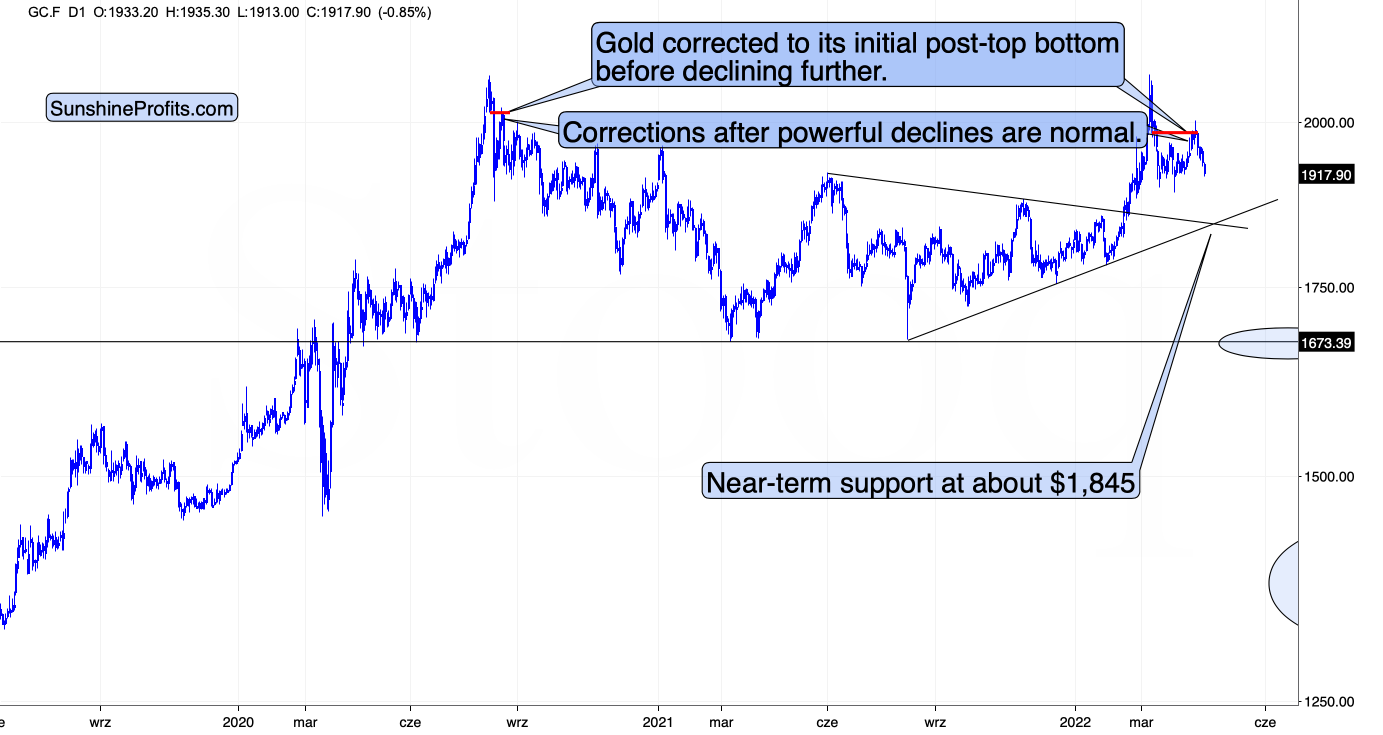

In the case of gold, please note how it followed its self-similarity to the post-2020 top trading patterns. The yellow metal moved slightly above its initial post-top bottom, and then it immediately turned south.

The support lines cross at about $1,845, so that’s where we might see the next short-term rebound, but let’s keep in mind that it’s not likely to be anything more than that – a corrective rebound that is then followed by another move lower.

Silver declined profoundly recently, and just like miners, it invalidated multiple previous breakouts. Most interestingly, though, it now clearly invalidates the breakout above its January 2022 high.

The next strong support is based on the previous lows, close to the $22 level. That’s where silver might correct before moving much lower.

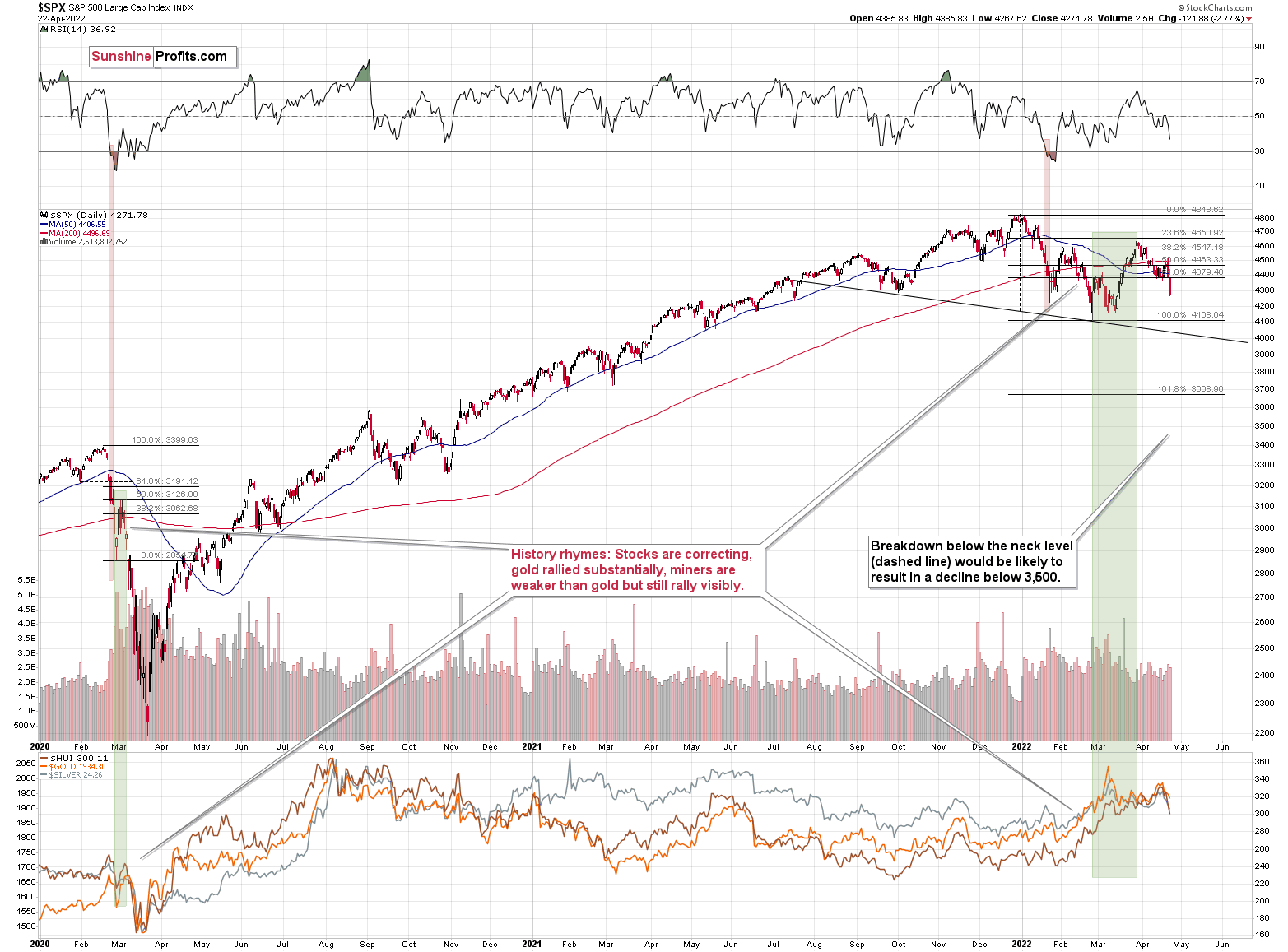

Why are mining stocks and silver declining so much nowadays?

It is quite likely due to their connection with the general stock market.

I’ve been writing about the stock market’s incoming demise for quite some time, and that’s what we’re finally seeing. Both silver and miners (especially junior miners) are responding accordingly.

Provided that stocks continue to decline, silver and miners are likely to fall even more than gold.

Let’s keep in mind what happened in the previous cases when stocks declined profoundly – in early 2020 and in 2008. Miners and silver declined in a truly epic manner, and yes, the same is likely to take place in the following months, as markets wake up to the reality, which is that the USD Index and real interest rates are going up.

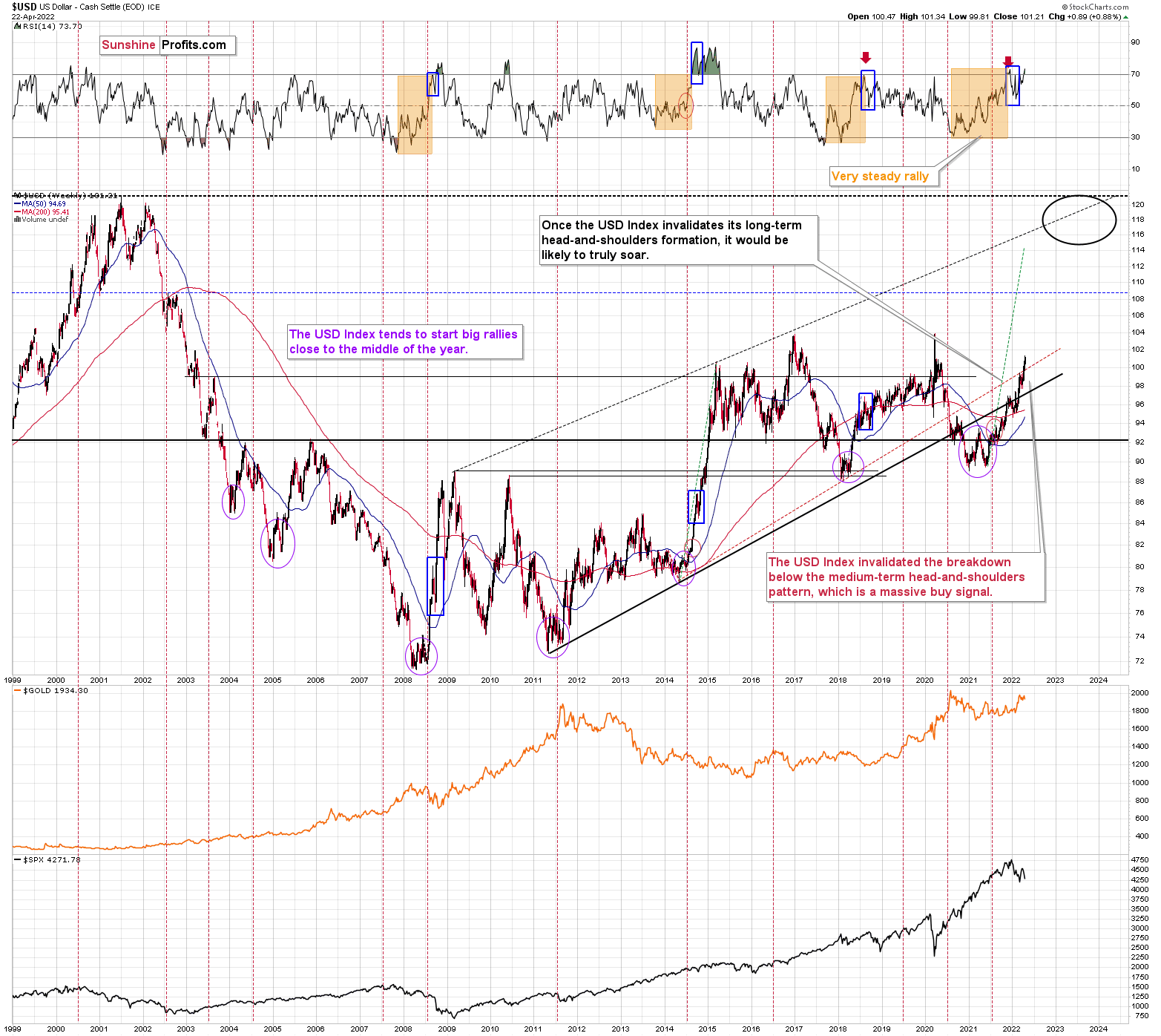

Speaking of the USD Index, after invalidating the breakout below the multi-year head-and-shoulders pattern, the USDX is poised to soar, just like I’ve been expecting it to do for more than a year ago.

The RSI is above 70, but since the USDX is in a medium-term rally and is already after a visible correction, it can rally further. Please note that we saw the same thing in 2008 and in 2014. I marked the corrections with blue rectangles.

The next strong resistance is at the previous highs – close to the 104 level.

It doesn’t mean that the USD Index’s rally is likely to end there. It’s not – but the USDX could take a breather when it reaches 104. Then, after many investors think that the top has been reached as the USDX corrects, the big rally is likely to continue.

All in all, the technical picture for mining stocks is extremely bearish for the following months, even though we might see a short-term correction close to the end of April.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM