Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Welcome to this week's flagship Gold & Silver Trading Alert. Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

The key thing is that while the medium-term outlook remains profoundly bearish, the short-term outlook changed from bullish to bearish once again.

Let’s start today’s analysis with a recap of what recently happened on the fundamental front.

The Weekly Fundamental Roundup

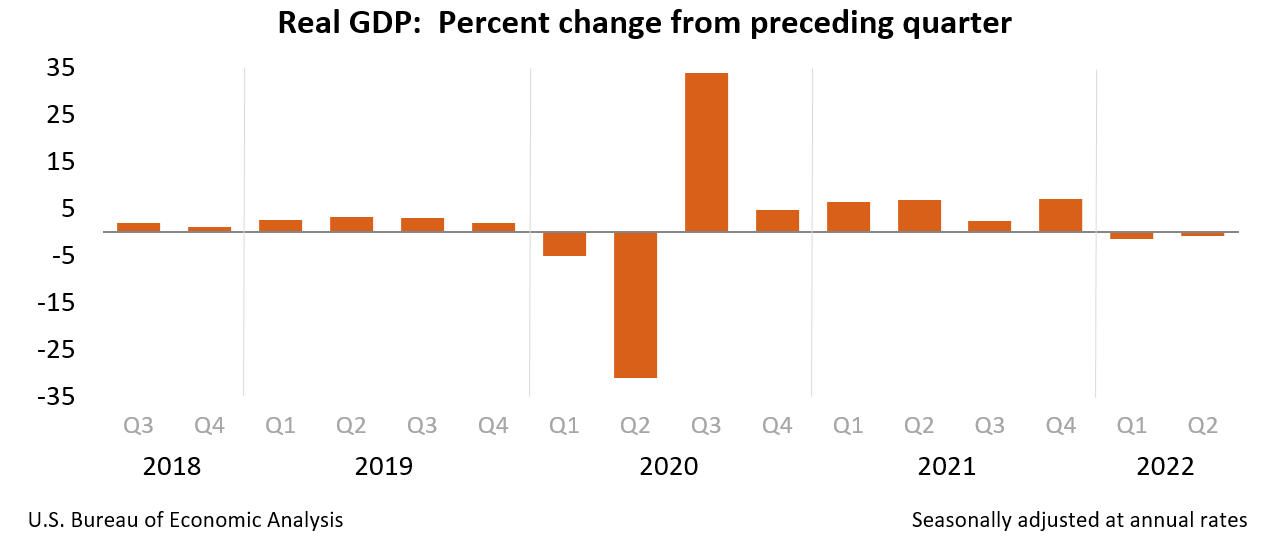

It was a busy week on the fundamental front, with major corporate earnings, an FOMC meeting, and a real GDP release vying for investors’ attention. Moreover, with the latter declining “at an annual rate of 0.9% in the second quarter of 2022,” the U.S. has recorded two consecutive quarters of negative real GDP growth, which marks a technical recession.

Please see below:

However, if you’re confused about why real GDP growth has slumped while consumer spending and corporate earnings remain resilient, it all boils down to inflation. For example, real metrics are calculated as nominal data minus the inflation rate. Therefore, ~9% inflation was higher than nominal GDP growth and pushed the real reading into negative territory.

But with metrics like retail sales and corporate earnings measured nominally, flat volume coupled with price increases can result in ~9% nominal growth. As a result, the dark real GDP clouds are overshadowed by sunny nominal spending and corporate earnings.

To that point, with investors more concerned about nominal corporate earnings than real GDP growth, price increases make quarterly reports look appetizing. Thus, the bulls continue to celebrate on Wall Street.

Furthermore, with the junior miners jumping by more than 3% on Jul. 28, our technical, sentiment, and positioning indicators proved prescient in recent days. For example, I wrote on Jul. 21:

I’ve noted how oversold conditions support a short-term rally for the GDXJ ETF. Moreover, with fund flows emphasizing the technical conclusions, it’s important to remember that too much bearishness is often bullish.

Please see below:

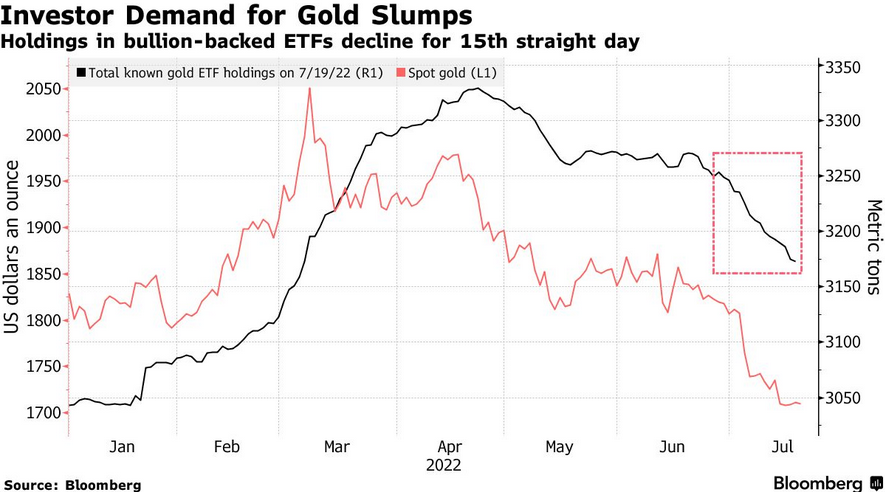

To explain, the red line above tracks the spot gold price, while the black line above tracks gold-backed ETF holdings as of Jul. 19. If you analyze the right side of the chart, you can see that gold-backed ETFs have suffered 15 straight days of outflows. Moreover, with the PMs declining on Jul. 20, the tally is likely at 16 days.

Thus, with the bullion bulls back in control, gold outperformed most risk assets on Jul. 28, and silver had its best day in months. However, the short-term optimism has likely run its course, and we believe that short positions now offer a better risk-reward proposition.

Watch Out Powell

With Fed Chairman Jerome Powell’s dovish press conference on Jul. 27 encouraging speculators to flood into risk assets, the consensus assumes the post-GFC script still applies. In a nutshell: buy everything, so you won’t be left behind when the Fed pivots.

However, while that playbook worked when inflation was hovering near 2%, the reality is that 9%+ inflation will only worsen the more the Fed backtracks. To explain, I wrote on May 31:

When economic optimism elicits rallies on Wall Street, that same optimism uplifts commodities. Therefore, if the Fed tries to appease investors and passively attack inflation, it will only spur more inflation.

As such, the idea of a “positive feedback loop” where ‘stocks rally, inflation cools [and] Fed tightening expectations abate” is extremely unrealistic. In fact, it’s the exact opposite. The only bullish outcome is if economically-sensitive commodities collapse on their own. Then, input inflation would subside and eventually cool output inflation, and the Fed could turn dovish.

However, the central bank has been awaiting this outcome for two years. Thus, my comments from Apr. 6 remain critical. If investors continue to bid up stock prices, the follow-through from commodities will only intensify the pricing pressures in the coming months. Therefore, investors are flying blind once again.

To that point, while the recent cheer has uplifted the S&P 500 and the NASDAQ Composite, commodities have also rallied.

Please see below:

Source: Investing.com

Source: Investing.com

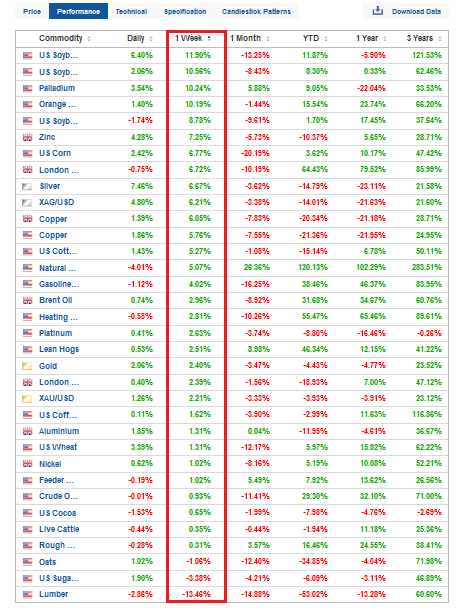

To explain, the table above tracks the performance of several commodities over different timeframes. If you analyze the column next to the red rectangle (“1 Month”), you can see that most commodities have declined significantly. As a result, the consensus viewed the drawdowns as evidence that inflation would subside, allow the Fed to turn dovish, and support higher stock prices.

However, while the short-term ramifications were true – which we took advantage of by going long (and making money on) the GDXJ ETF – they don’t understand the medium-term consequences. For example, commodities crashed due to fears that the Fed would hike the U.S. into a recession. However, if the Fed slows its roll to support growth, money will flow back into commodities. As such, inflation will reign the longer Powell drags his feet.

Furthermore, the vertical red rectangle highlights how most commodities have rallied over the last week, and the inflation progress that Powell achieved is being eroded. Thus, he should learn a hard medium-term lesson that trying to support economic growth and tame inflation simultaneously will result in him failing at both.

Demand, Not Supply

With second-quarter earnings calls continuing to sound the alarm on inflation, I’ve warned for months that demand is much stronger than the consensus understands. Remember, resilient corporate earnings are bullish for the Consumer Price Index (CPI) because companies are passing through higher input costs. As such, while investors celebrate the optimistic earnings prints, they don’t realize the results make the Fed’s job more difficult.

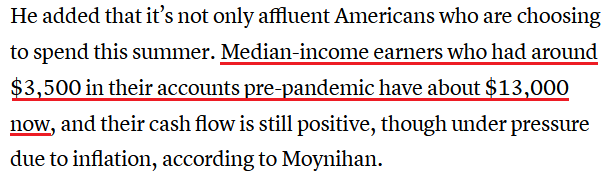

For example, Bank of America CEO Brian Moynihan – who runs the second-largest bank in the U.S. – told CNBC on Jul. 27: “the consumer is the greatest benefit and the greatest trouble to the Fed. One of the toughest jobs they have is the American consumer is still in pretty good shape.”

He added:

“Data through last Friday basically says that for the month of July (…) [spending] is up about 10 percentage points from last year’s July first three weeks. And the transaction growth is 6% to 7%, so that means it’s growing (…).”

“People are spending on vacations. European transactions are through the roof right now. Spending on vacations, theme parks; home improvement [is] a little bit more mitigated, but still holding on bigger than 2019.”

More importantly:

Source: CNBC

Source: CNBC

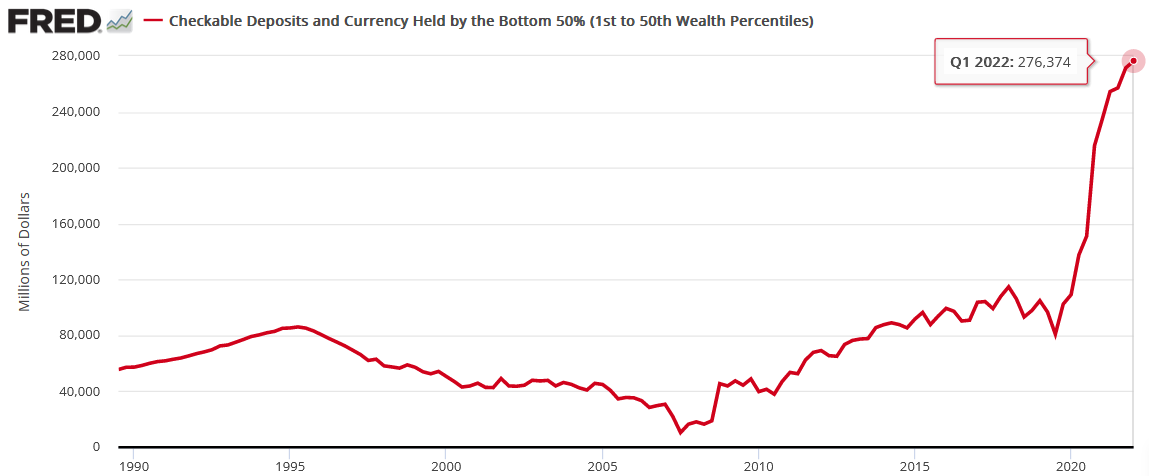

However, I warned on Dec. 23, 2021 that U.S. consumers had a war chest of cash. I wrote:

While the fiscal spending spree may end, U.S. households are flush with cash. U.S. households have nearly $3.54 trillion in their checking accounts. For context, this is 253% more than Q4 2019 (pre-COVID-19) (…).

While some investors expect a dovish 180 from the Fed, they shouldn’t hold their breath. With U.S. economic growth still resilient and the U.S. consumer in much better shape than some portray, the Fed can raise interest rates without crashing the U.S. economy. As a result, Powell will likely stick to his hawkish script and forge ahead with rate hikes in 2022.

Likewise, I noted on Jul. 19 that even low-to-middle-income Americans still have plenty of spending firepower. I wrote:

The Fed updated the data by wealth percentile on Jun. 29. Moreover, with the bottom 50% (the poorest Americans) seeing their checking account balances also hit an all-time high in Q1, the inflation bears should learn hard lessons over the medium term.

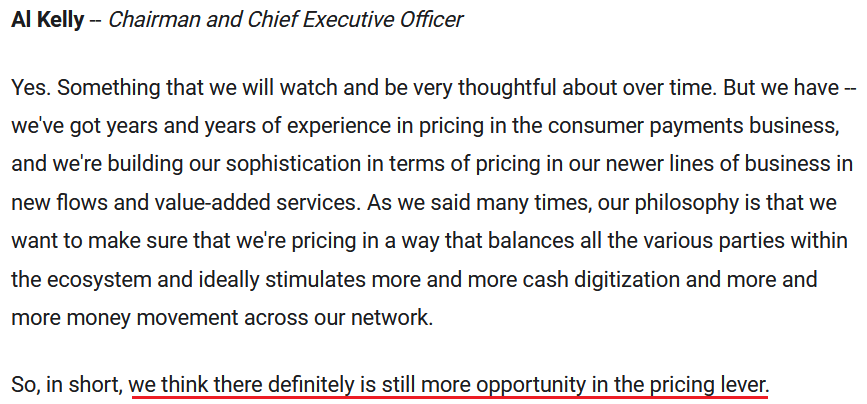

As further evidence, Visa – which is home to the world’s largest credit card payments network – released its third-quarter earnings on Jul. 27. CEO Al Kelly said during the Q3 earnings call.

“I wanted to take a moment to discuss two topics: recession and inflation. On the first, we're not economic forecasters, so I'm not going to predict the future or a potential likelihood of a recession. Instead, let's focus on the facts. From the numbers I just reviewed relative to 2019 levels, growth has been stable or improving in overall domestic payment volume, credit, debit, card present and card backwards, and volume. And this indicates the most of 2022 with no indication of any slowdown, including in more recent weeks (…).”

“Early in the pandemic, goods surpassed services. We were seeing the historic trend. Even as services have rebounded in the last six months, the percentage spending on goods in our payments volumes still remained high, higher than the pre-pandemic levels. For example, while U.S. home improvement and retail goods spending during the third quarter grew only low single digit year-over-year, it remains well ahead of pre-pandemic trend line. Second, many discretionary segments have further strengthened. If you look at U.S. travel spend, it is not back to the pre-COVID trend line but grew more than 40% versus last year.”

“Third, the affluent spend continue to recover, particularly in the areas of restaurants, travel, and entertainment. At the same time, non-affluent spend remained relatively resilient. We mentioned the affluent spend returning to restaurants last quarter. That trend continued this quarter with affluent restaurant spend indexing in the 160% to 180% range versus 2019.”

As a result, robust consumer spending is present throughout Visa’s card network, giving the company more leeway to raise prices.

Please see below:

Source: Visa/The Motley Fool

Source: Visa/The Motley Fool

The Bottom Line

With the consensus missing the fundamental forest through the trees, the medium-term implications of rampant inflation are dire. Moreover, with Powell’s dovish press conference making a bad situation worse, this week has pushed the Fed even further behind the inflation curve. As a result, while the bulls celebrate the short-term strength of corporate earnings, don’t be surprised if the U.S. federal funds rate hits ~4.5% or higher when it’s all said and done.

In conclusion, the PMs rallied on Jul. 28, as the bulls gored everything in sight. Moreover, while the developments were bullish for our long position (and helped us reap profits once again), we think the easy gains are behind us. Therefore, with the downside risk greater than the upside, a short position is prudent, and the GDXJ ETF should break below its 2022 lows sooner rather than later.

What to Watch for Next Week

With more U.S. economic data releases next week, the most important are as follows:

- Aug. 1: ISM Manufacturing PMI

Like S&P Global, the ISM surveys manufacturers across the U.S. Moreover, their responses are leading indicators of future government inflation, employment, and growth data.

- Aug. 2: JOLTS job openings

While the JOLTS data is lagged, it still provides insight into the strength of the U.S. labor market. However, the weekly data from Indeed is timelier.

- Aug. 3: ISM Services PMI, S&P Global U.S. Composite PMI

Like the ISM's Manufacturing PMI released on Aug. 1, the services PMI will cover the inflation, employment and growth outlook across the U.S. service sector. In addition, S&P Global will combine two similar surveys into one.

- Aug. 4: Challenger job cuts

With the U.S. labor market accounting for one-half of the Fed’s dual mandate, monitoring job gains and losses is paramount.

- Aug. 5: U.S. nonfarm payrolls, average hourly earnings

While payrolls are a lagging indicator, they often move markets. Moreover, a decent print and resilient wage inflation will put even more pressure on the Fed.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. If that occurs, the outcome is profoundly bearish for the PMs.

Technically Speaking

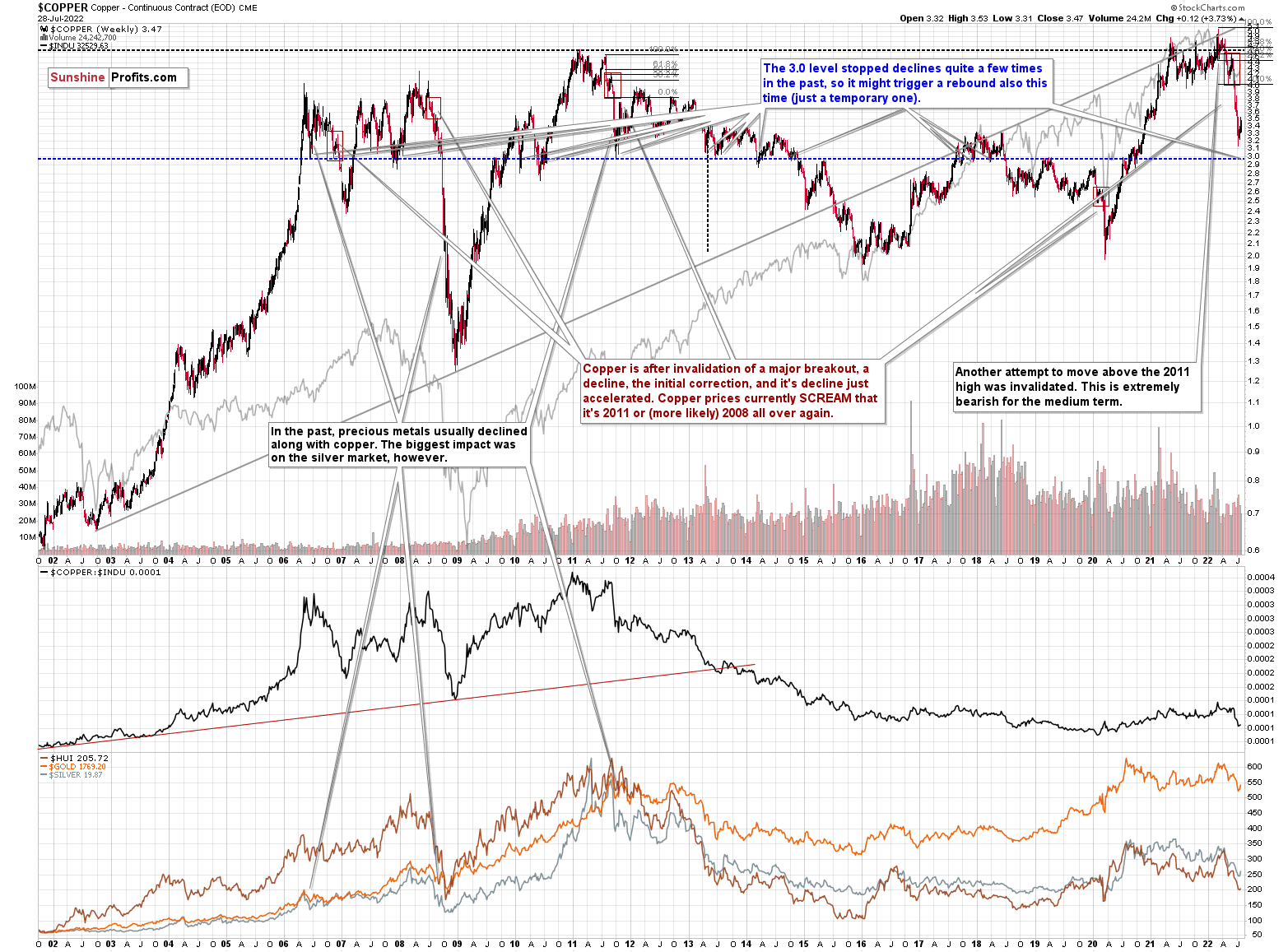

Let’s start today’s technical discussion with a quick check on copper prices.

Practically, everything that I wrote about it last week (and in the previous weeks/months) remains up-to-date:

Copper recently CLEARLY invalidated another attempt to move above its 2011 high. This is a very strong technical sign that copper (one of the most popular commodities) is heading lower in the medium term.

Interest rates are going up, just like they did before the 2008 slide. What did copper do before the 2008 slide? It failed to break above the previous (2006) high, and it was the failure of the second attempt to break higher that triggered the powerful decline. What happened then? Gold declined, but silver and mining stocks truly plunged.

Again, copper is after invalidation of a major breakout, a decline, the initial correction, and its decline just accelerated. Copper prices currently SCREAM that it’s 2011 or (more likely) 2008 all over again. This is extremely bearish for mining stocks (especially juniors) and silver.

No market moves in a straight line, up or down, but since we just saw a corrective upswing, the downtrend might now resume (or it might resume after additional very short-term upswing).

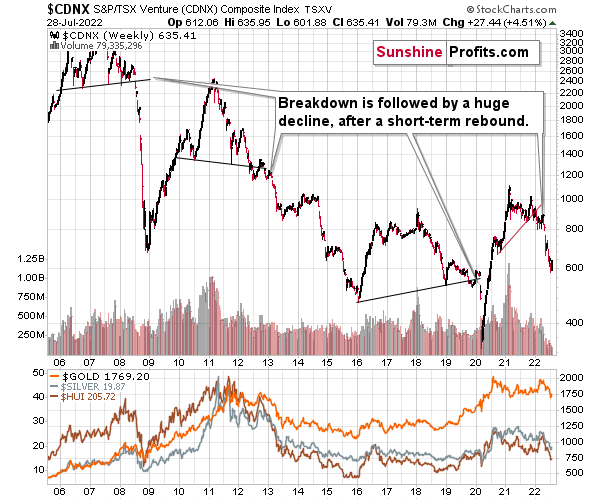

Having said that, let’s check junior miners’ really big picture.

I previously commented on the above chart in the following way:

The Toronto Stock Exchange Venture Index includes multiple junior mining stocks. It also includes other companies, but juniors are a large part of it, and they truly plunged in 2008.

In fact, they plunged in a major way after breaking below their medium-term support lines and after an initial corrective upswing. Guess what – this index is after a major medium-term breakdown and a short-term corrective upswing. It’s likely ready to fall – and to fall hard.

So, what’s likely to happen? We’re about to see a huge slide, even if we don’t see it within the next few days.

What has happened recently?

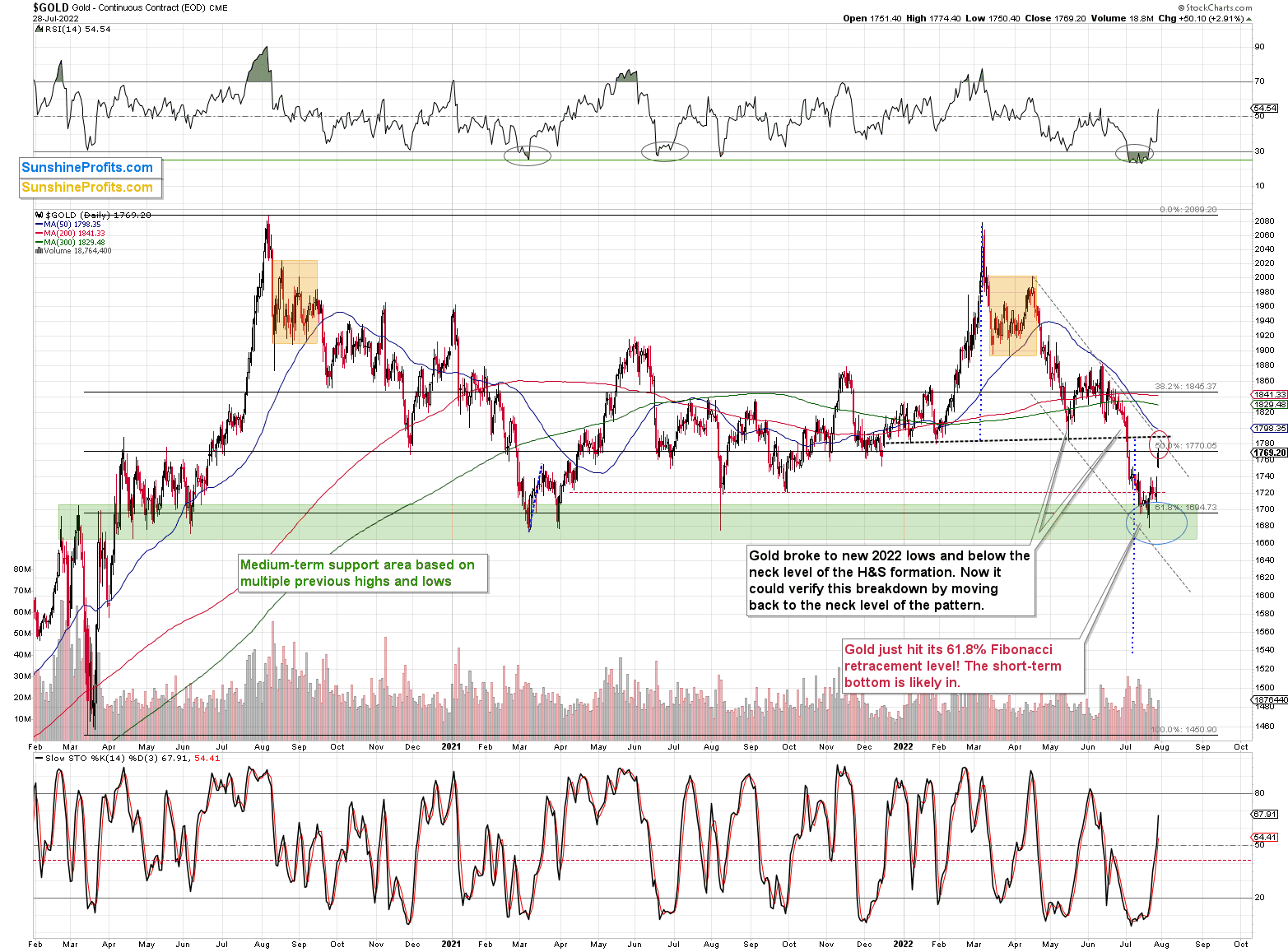

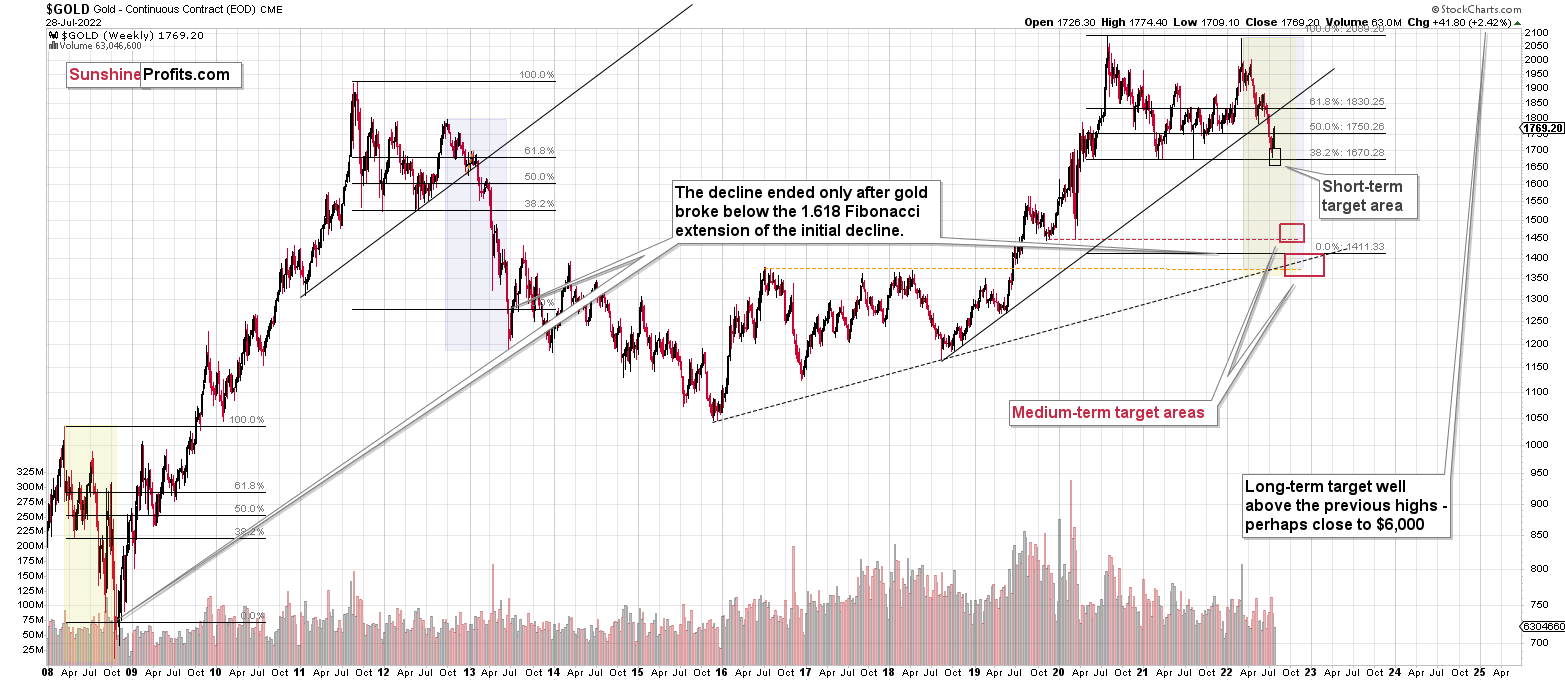

Gold just moved to the middle of my previous target area, and it seems that it might have topped.

The resistance levels that were reached are provided by the 50% Fibonacci retracement from the 2020 rally and the previous lows – the late-2021 lows, the June 2021 low, and the late-2020 low.

Additionally, the move (and a tiny reversal before the end of the day) materialized at the same time when the two resistance lines crossed – the neck level of the previously broken head and shoulders pattern (thick, black, dashed line) and the upper border of the declining trend channel. Those intersections – vertexes often mark reversal points, so we might have indeed just seen one.

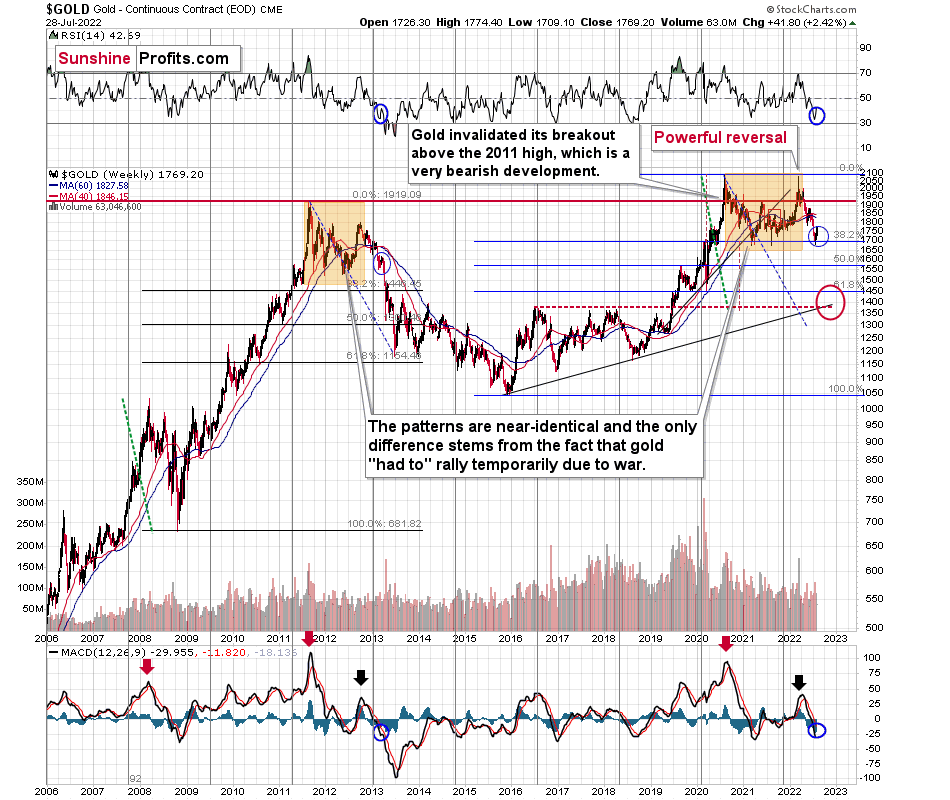

I admit that the above on its own might not be enough to determine gold’s outlook, but the thing is that it’s just a cherry on top comprised of multiple other – more important – factors. One of the most important of those factors is the analogy between what happened in 2008 and 2013. You can see this analogy on the long-term gold chart below.

Let’s keep in mind that between 2020 and now, quite a lot happened, quite a lot of money was printed, and we saw a war breaking out in Europe. Yet, gold failed to rally to new highs.

In fact, it’s trading very close to its 2011 high, which tells you something about the strength of this market. It’s almost absent.

Truth be told, what we see in gold is quite in tune with what we saw after the 2011 top, and in particular, shortly after the 2012 top. The long-term gold price chart below provides details.

Please note that the 38.2% Fibonacci retracement based on the entire 2015-2020 rally is very close to $1,700, which makes the above-mentioned support area even stronger. Indeed, that’s when gold bottomed recently.

It seems that if it weren’t for the war in Europe, gold wouldn’t have been able to move above $2,000 and instead it would have topped close to its previous highs, which provided strong resistance.

The extraordinary thing about that is that that’s exactly what happened in 2012. Gold moved higher but only until it reached its previous highs, which happened in the second half of 2012.

This time the RSI was a bit higher, but it was close to 70, just like in 2012.

Yes, this time gold moved back to the previous high, but:

- This happened as a result of a geopolitical event (the war in Europe), and geopolitically-driven rallies are generally unsustainable;

- When gold reached its previous highs, it also formed a profound weekly reversal, which formed on huge volume, and that’s very bearish.

So, the current medium-term outlook for gold is very bearish.

There are also very interesting short-term takeaways from the above chart.

If the 2012-2013 is currently being replayed (at least to a significant extent), then let’s not forget that this decline initially took the shape of a back-and-forth decline with lower lows and lower highs (but there were notable short-term rallies within the decline).

The final of the corrections that still took place within the back-and-forth decline started in early 2013 - when gold moved close to its previous medium-term lows, when RSI was a bit above 30, and when the MACD was close to -20, which was also slightly below its previous medium-term low.

We can see all three above-mentioned similarities on the above chart. I marked them with blue ellipses. They are not “somewhat similar” – they are remarkably similar in both cases!

Indeed – gold rallied recently just like it had rallied in 2013, right before the most volatile part of the slide.

What does it imply going forward?

Please note that, based on the above-mentioned similarity, the corrective upswing in gold has probably already been completed. Even at first sight, the rallies within blue ellipses appear practically identical. The RSI moved similarly higher as well.

Since the short-term rally appears complete, the big, medium-term decline is now about to resume.

How low is gold likely to go during this upcoming decline? Perhaps as low as its 2020 low – to the $1,450-1,500 area.

I realize this is far from the current price, but nonetheless, this target area appears justified in my opinion. There are two important Fibonacci retracements based on the 2015-2020 rally that gold can bounce from (it recently bounced from the 38.2% retracement). These are: 50% and 61.8% retracements.

The support provided by the 61.8% retracement is strengthened by the 2020 low and the support provided by the 50% retracement is strengthened by the 2019 high.

However, based on gold’s self-similarity to 2013, it seems that we’re about to see a slide that’s bigger than what we’ve been seeing so far this year. This time – based on the similarity – gold is likely to decline profoundly, but no longer in the back-and-forth mode. If gold formed its next local low at the 50% retracement (so at about $1,560), then it might do so still within the declining, short-term trend channel (sometime in September).

However, if gold is to stick to the link to 2013, then it should decline more rapidly. In this case, the technique that can help us estimate the short-term target is the one that says that after a breakdown from a trend channel, price is likely to move approximately by as much as the height of the previous trend channel. In this case, gold could break below the trend channel soon and then decline even more. Based on the height of the trend channel, the above means that a move to the 61.8% retracement as the next downside target is more likely than a move to the 50% retracement.

Besides, the decline in gold would likely be linked to a breakdown in the EUR/USD below 1, which – if confirmed – would likely trigger significant selling.

On the fundamental news front, this fits the current situation as well. The likelihood of real interest rates moving higher in the future didn’t decrease at all, but at the same time, the market focused on something insignificant – Powell’s speech. Yes, it was insignificant because of all the times Powell’s suggestions didn’t result in actual action. Also, wasn’t it Powell who spoke many times about the benefits of higher interest rates, but then cut them (probably as he was pressured to do so by Trump)?

This time, the pressure is different – people are most concerned with inflation, and the latter has become political. So, while it remains clear that real interest rates are going up, the market’s perception triggered this artificial short-term rally, which means that now the gold price has more room to fall.

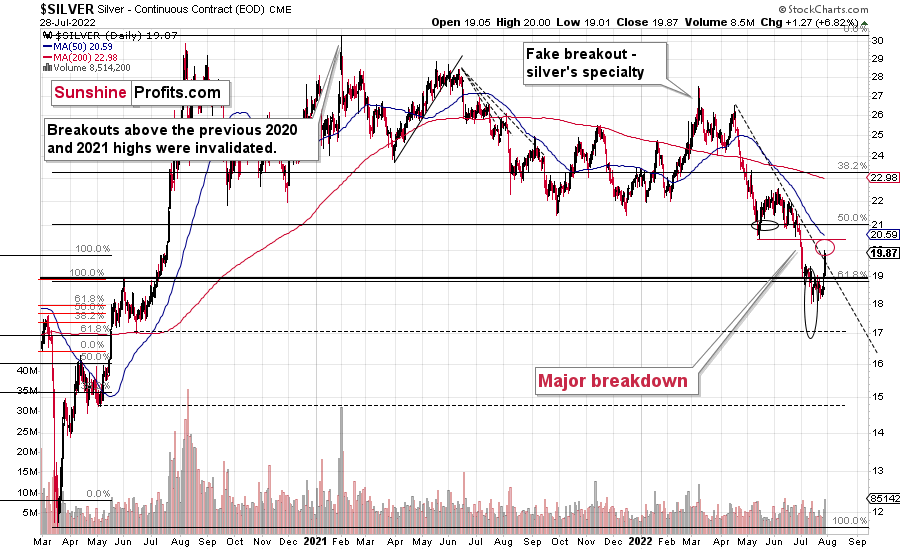

Silver and mining stocks are likely to be affected even more than gold, though.

Let’s take a look at the silver market.

Like gold, silver just hit my previous target area. Yesterday’s intraday high was exactly $20.00, and it doesn’t get much more important from a psychological point of view when it comes to the importance of round numbers.

This, plus the fact that silver moved to its declining resistance line, suggests that the top might be in. Of course, since silver is known for its fake breakouts, it wouldn’t be that surprising to see silver return to its May lows or even slightly above them before moving much lower. But it’s not that likely given what we saw in gold (and in the general stock market).

Furthermore, silver outperformed gold on high volume, which we frequently see as confirmation of a short-term top being in or near. How low will silver now move? This is rather unclear, because things can now get very volatile (like in 2008, 2013 or 2020), and it seems to be a better idea to be looking at gold than at silver when determining the exit moment for the white metal.

However, to provide you with some numbers, I’d say that silver is likely to decline at least to $15 before the next important correction. I wouldn’t be surprised to see it fall all the way down to its 2020 lows of $12 before moving up in a more visible way.

As you see, the silver outlook is not as precise as it is for gold, as the support levels and targets based on multiple techniques don’t necessarily align. In the case of gold, they do.

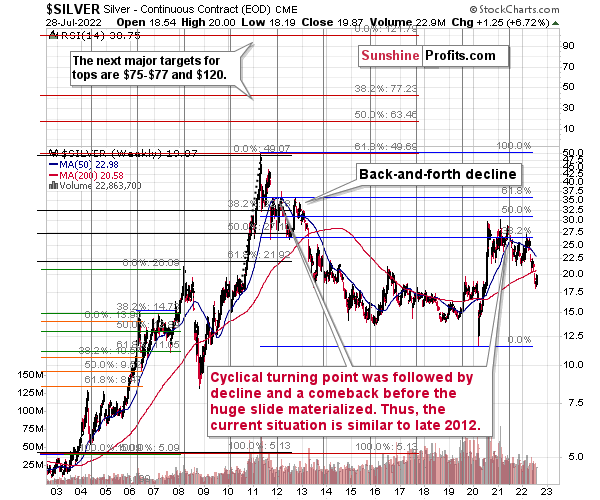

Let’s not forget that gold is not the only precious metal that is repeating its 2012 performance right now, and you can see more details on silver’s long-term chart.

As you can see on the above chart, silver corrected about 50% of the previous downswing, and this correction ended at about $30, a long time ago. Ever since, silver has been declining, and even the outbreak of war in Europe didn’t make silver rally above that level.

On the above chart, you can see how silver first topped in 2011, then declined and formed another top at the cyclical turning point. Next, it declined once again – to the previous lows. After that, silver rallied (in 2012 and 2022), and it topped between its 50-week moving average (marked in blue) and the previous top. Now silver is declining in a back-and-forth manner (you can see it more clearly on the previous short-term silver chart).

Back in 2012, these were just the early days of a gargantuan decline, and the same appears likely to be the case this time. Interest rates are going up after all, and the Fed is determined to quench inflation.

Let’s not forget that rising interest rates are likely to negatively impact not just commodities, but practically all industries. This will likely cause silver’s price to decline profoundly, as silver’s industrial demand could be negatively impacted by lower economic growth (or a decline in economic activity).

Besides, please note that silver didn’t even manage to rally as much as copper (which tried to move to new highs recently) or most other commodities, thus being rather weak.

Consequently, it seems that silver will need to decline profoundly before it rallies (to new all-time highs) once again.

Having said that, let’s take a look at what happened in mining stocks.

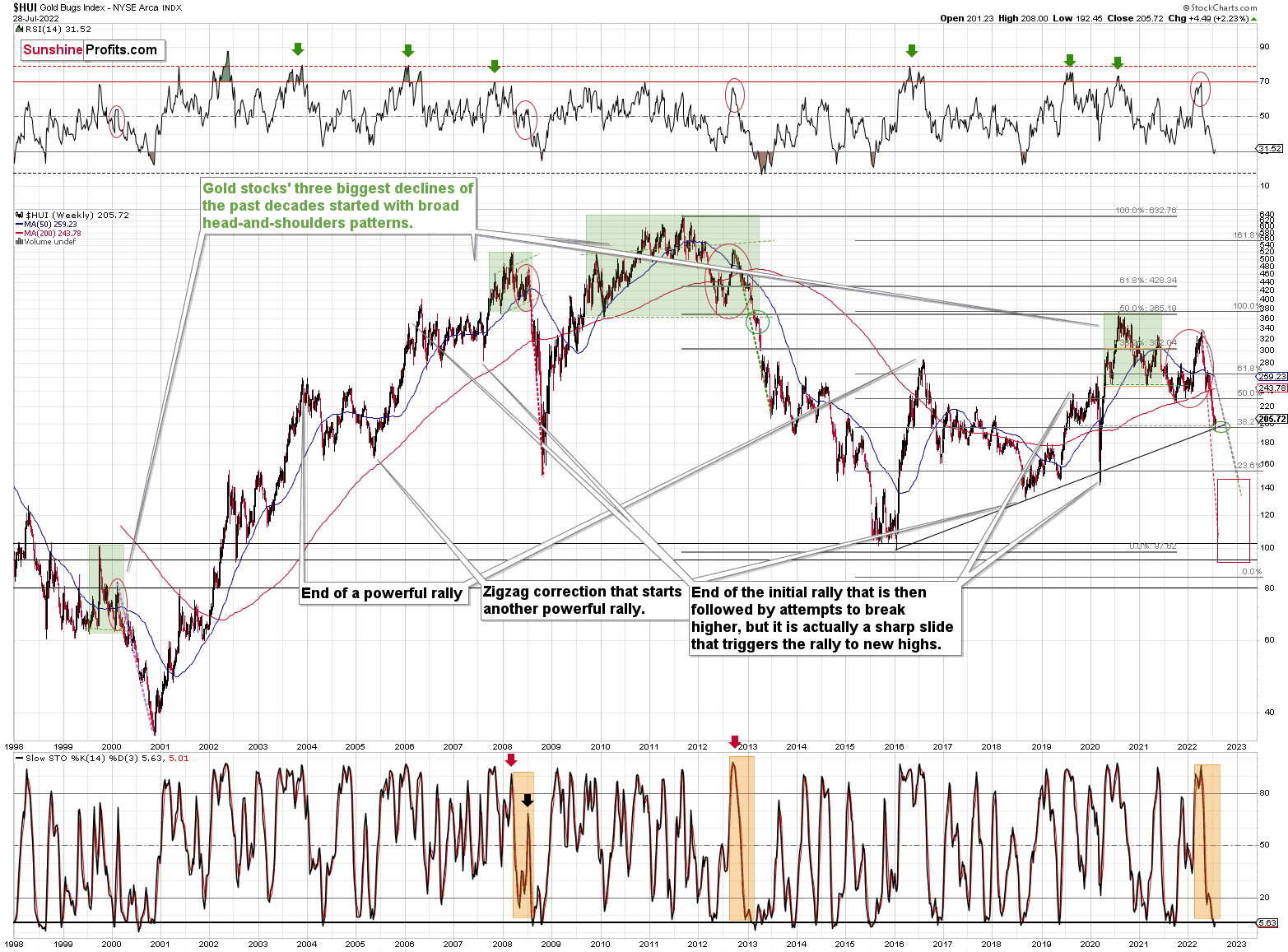

History tends to repeat itself. Not to the letter, but in general. The reason is that while economic circumstances change and technology advances, the decisions to buy and sell are still mostly based on two key emotions: fear and greed. They don’t change, and once similar things happen, people’s emotions emerge in similar ways, thus making specific historical events repeat themselves to a certain extent.

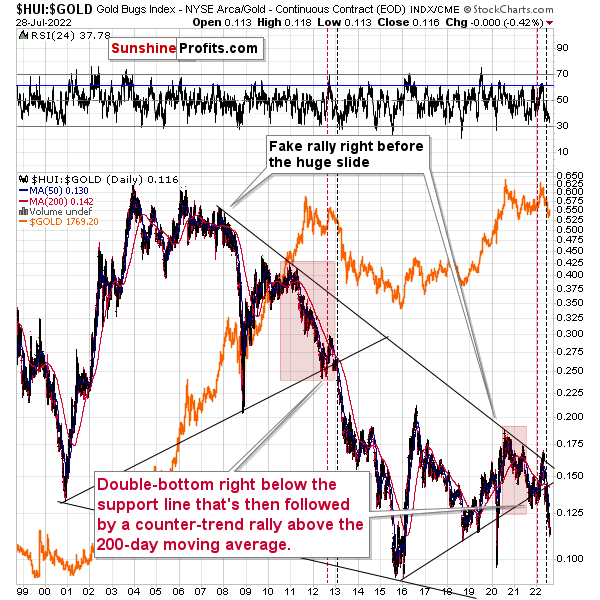

For example, right now, gold stocks are declining similarly to how they did in 2008 and in 2012-2013.

The Russian invasion triggered a rally, which was already more than erased, and if it wasn’t for it, the self-similarity would be very clear (note the head-and-shoulders patterns marked with green). Since the latter happened, it’s not as clear, but it seems that it’s still present. At least that’s what the pace of the current decline suggests.

I used a red dashed line to represent the 2008 decline, and I copied it to the current situation. They are very similar. We even saw a corrective upswing from more or less the 200-week moving average (red line), just like what happened in 2008.

We saw a breakdown to new short-term lows, which means that the volatile part of the slide is likely already underway.

Moreover, two weeks ago, I commented on the above chart in the following way:

On a short-term basis, we see a short-term (only) downside target of around 200. That’s about 10% below yesterday’s (Thursday’s) closing price. There are several reasons for it:

- It’s a round number, and those tend to be more important psychologically than other numbers.

- That’s where we have the rising medium-term support line based on the 2016 and 2018 lows. The temporary move below this line triggered a massive rally in 2020.

- That’s where we have the 61.8% Fibonacci retracement level based on the entire 2016-2020 rally.

The 200 target was then reached, briefly breached, and it was followed by a rally.

Analogy-wise, it’s what we previously saw in 2013. It might not be obvious which part of the chart to look at, as the upswings are not that visible from the long-term point of view, so I marked them with green ellipses.

There was no major rally in the RSI recently, which might seem concerning (after all, an RSI close to 30 is bullish in theory), but that’s also what we saw (what we didn’t see) in 2013 right before the biggest part of the slide.

How low can the HUI Index fall during the next big downswing?

As it’s the case with gold and silver, a move back to the 2020 lows is definitely in the cards. Please note that this level is also strengthened (as support) by other major lows: the 2019, 2014, and 2008 ones.

However, I wouldn’t rule out a move even lower on a temporary basis. If gold were to decline to about $1,450-1,500, it would mean that it would double its current 2022 decline. If the HUI Index does that, it will move below 150.

So, all in all, 120-150 is my current target area for the upcoming slide in the HUI Index.

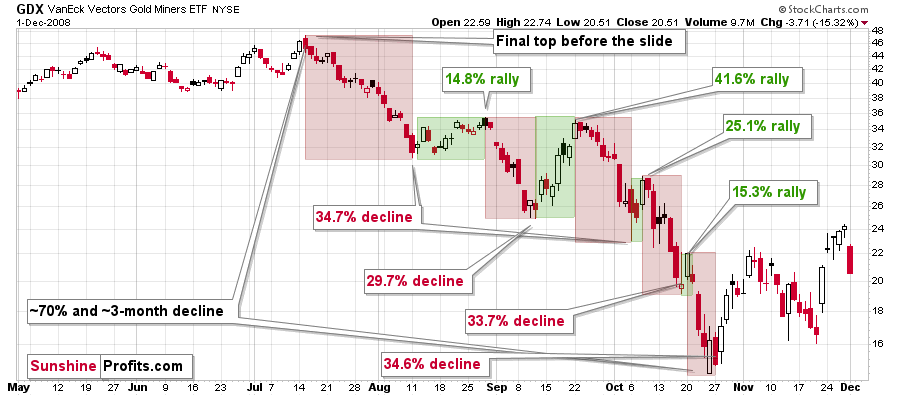

All right, let’s zoom in and see how mining stocks declined in 2008.

Back then, the GDXJ ETF was not yet trading, so I’m using the GDX ETF as a short-term proxy here.

The decline took about 3 months, and it erased about 70% of the miners’ value. The biggest part of the decline happened in the final month, though.

However, the really interesting thing about that decline – that might also be very useful this time – is that there were five very short-term declines that took the GDX about 30% lower.

I marked those declines with red rectangles. After that, a corrective upswing started. During those corrective upswings, the GDX rallied by 14.8-41.6%. The biggest corrective upswing (where GDX rallied by 41.6%) was triggered by a huge rally in gold, and since I don’t expect to see anything similar this year, it could be the case that this correction size is an outlier. Not paying attention to the outlier, we get corrections of between 14.8% and 25.1%.

The interesting thing was that each corrective upswing was shorter (faster) than the preceding one.

The first one took 12 trading days. The second one took seven trading days. The third one took 2 trading days, and the fourth and final one took just 1 trading day.

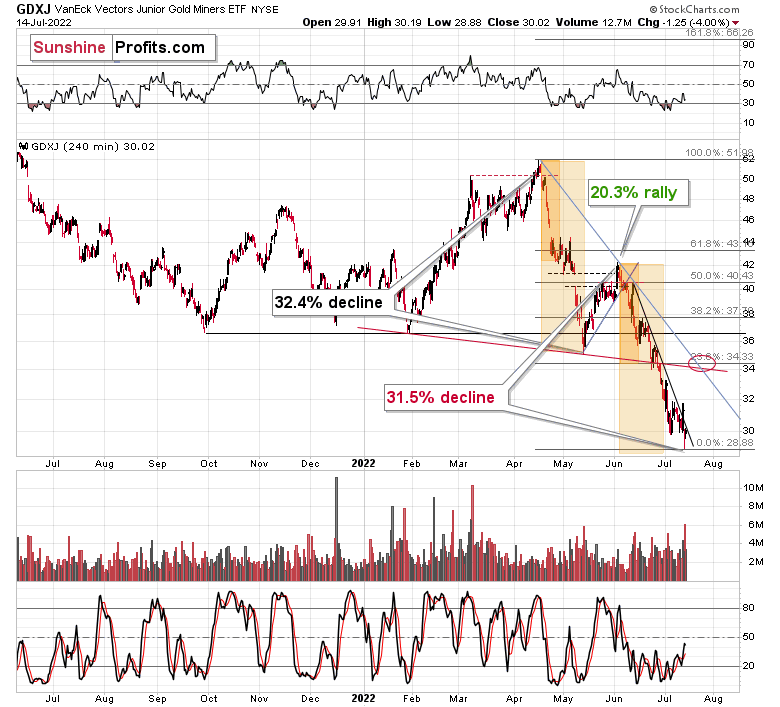

Fast forward to the current situation. Let’s take a look at the GDXJ ETF.

The GDXJ ETF declined by 32.4% and then corrected – it rallied by about 20.3%. The corrective upswing took 14 trading days.

Now, it had declined by about 31.5% and then rallied by about 16.1%. The corrective upswing took less time than the previous one.

The above is in perfect tune with the previous patterns seen in the GDX during the 2008 slide.

I previously wrote the following:

What does it tell us? It indicates that history can be rhymed, and while it will not be identical, we should pay attention to the indicators that worked in 2008. The next corrective upswing (a notable one, that is) might start when the GDXJ ETF declines by about 29-35% from its recent top. To clarify, I don’t claim that the above technique would be able to detect all corrective upswings, or that I aim to trade all of them. For instance, in my view, it was a good idea to enter a long position on May 12 and switch to a short position on May 26, but I wasn’t aiming to catch the intraday moves.

Based on how long the corrective upswings took in 2008 and how long the recent one took, the upcoming corrective upswing is likely to take between 5 and 10 trading days. If the bottom formed yesterday, which seems likely as the GDXJ ETF is already up by over 1% in today’s London trading, then we can expect the next local top to form within 1-2 weeks. In other words, it seems that the corrective upswing is likely to end in the next part of July – probably in its final week.

Back in 2008, the counter-trend rallies varied greatly in their magnitude, but please keep in mind that back then, the decline was very much news-based – Lehman Brothers’ collapse, etc. This time, the decline is more measured, so declines and corrections are more measured as well.

While back in 2008, during the first correction, the GDX gained only 14.8% and during the second one it gained a sizable 41.6%, this time the first rally provided a measured 20.3% increase. If the upcoming correction is also measured, then the GDXJ might also rally by about 20%.

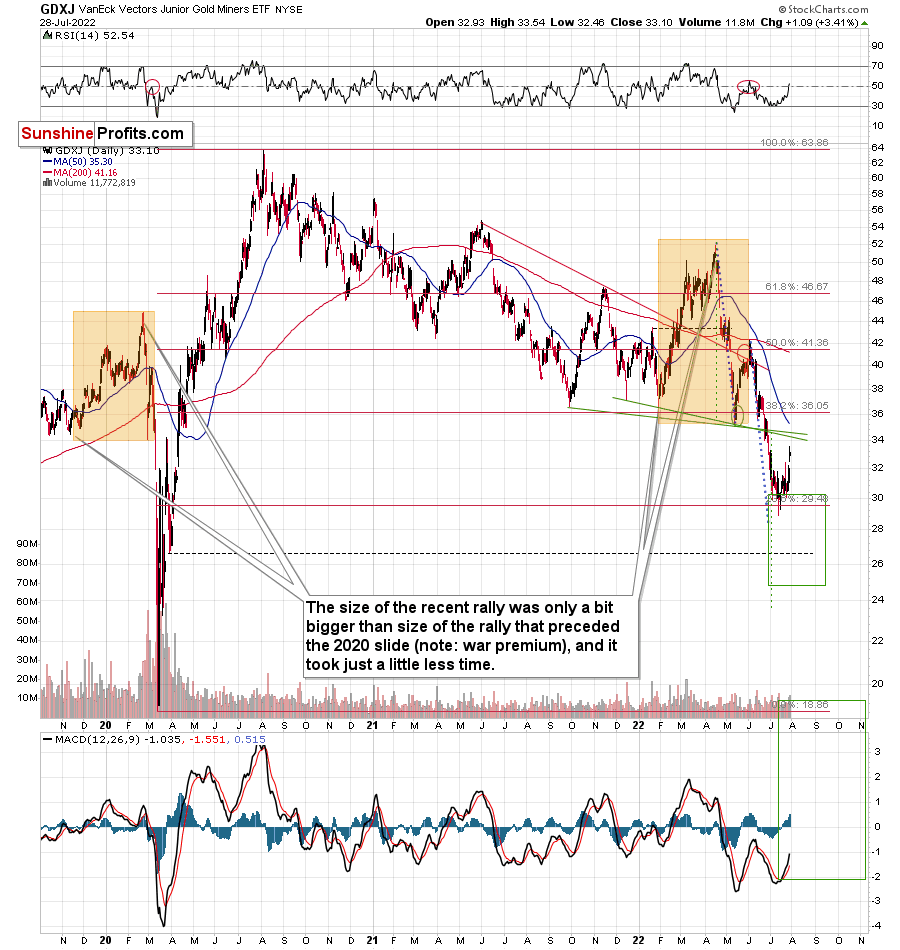

It appears that it’s exactly what we saw. The medium-term downtrend can now continue (or if it hasn’t started yet, it might start soon).

How low can the GDXJ ETF move during the (this?) next big move lower? A move to its 2020 lows (~$20) seems quite likely.

And yes, it is possible that the GDXJ ETF would fall below its 2020 lows, but it might need to correct first.

Please note that a move to the 2020 lows (~$20) is something that fits what I wrote about gold and the HUI Index - that they could repeat their so-far 2022 decline (approximately).

Moreover, please note that due to their recent outperformance, juniors can now reverse their trend and decline more than senior miners – this would fit a situation in which the general stock market declines.

Also, let’s not forget about the forest while looking at individual trees. By that, I mean looking at how gold stocks perform relative to gold. That’s one of the major indications that the current situation is just like what we saw at the 2012 top.

The situation in the gold stock to gold ratio is similar to what we saw in late 2012 and early 2013. The HUI to gold ratio invalidated its first attempt to break lower (marked with red, dashed lines), but after a corrective upswing, it then broke lower more decisively. That’s what I marked using black, dashed lines.

If history is to rhyme, we’re about to see a profound decline. In fact, we’re likely already past its beginning.

Also, please note that the pattern that we currently see, which started in early 2016, is somewhat similar to what happened between 2003 and 2008.

Back in 2008, the breakdown from the consolidation resulted in sharply lower ratio values and much lower prices of gold stocks.

So, if the situation is analogous to 2012-2013, we’re likely to see a big decline in the following weeks/months, and if it’s analogous to 2008, we’re likely to see an enormous decline in the following weeks/months.

Declining stock prices would only add fuel to the bearish fire (after all, gold stocks are… just stocks) and that’s exactly what’s likely to happen.

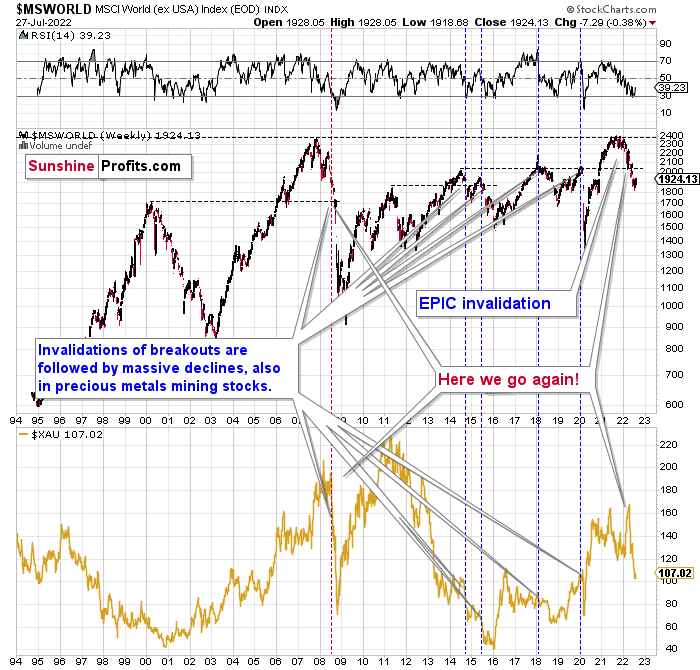

The technical picture in the case of world stocks remains extremely bearish, and my previous comments on it were just confirmed. Here’s what I’ve been writing about the above chart for quite a few weeks now:

World stocks have already begun their decline, and based on the analogy to the previous invalidations, the decline is not likely to be small. In fact, it’s likely to be huge.

For context, I explained the ominous implications on Nov. 30. I wrote:

Something truly epic is happening in this chart. Namely, world stocks tried to soar above their 2007 high, they managed to do so, and… failed to hold the ground. Despite a few attempts, the breakout was invalidated. Given that there were a few attempts and that the previous high was the all-time high (so it doesn’t get more important than that), the invalidation is a truly critical development.

It's a strong sell signal for the medium - and quite possibly for the long term.

From our – precious metals investors’ and traders’ – point of view, this is also of critical importance. All previous important invalidations of breakouts in world stocks were followed by massive declines in mining stocks (represented by the XAU Index).

Two of the four similar cases are the 2008 and 2020 declines. In all cases, the declines were huge, and the only reason why they appear “moderate” in the lower part of the above chart is that it has a “linear” and not a “logarithmic” scale. You probably still remember how significant and painful (if you were long, that is) the decline at the beginning of 2020 was.

All those invalidations triggered big declines in the mining stocks, and we have “the mother of all stock market invalidations” at the moment, so the implications are not only bearish, but extremely bearish.

World stocks have declined below their recent highs, and when something similar happened in 2008, it meant that both stocks and gold and silver mining stocks (lower part of the chart) were about to slide much further.

The medium-term implications for mining stocks are extremely bearish.

However, let’s get back to the short- and medium-term point of view.

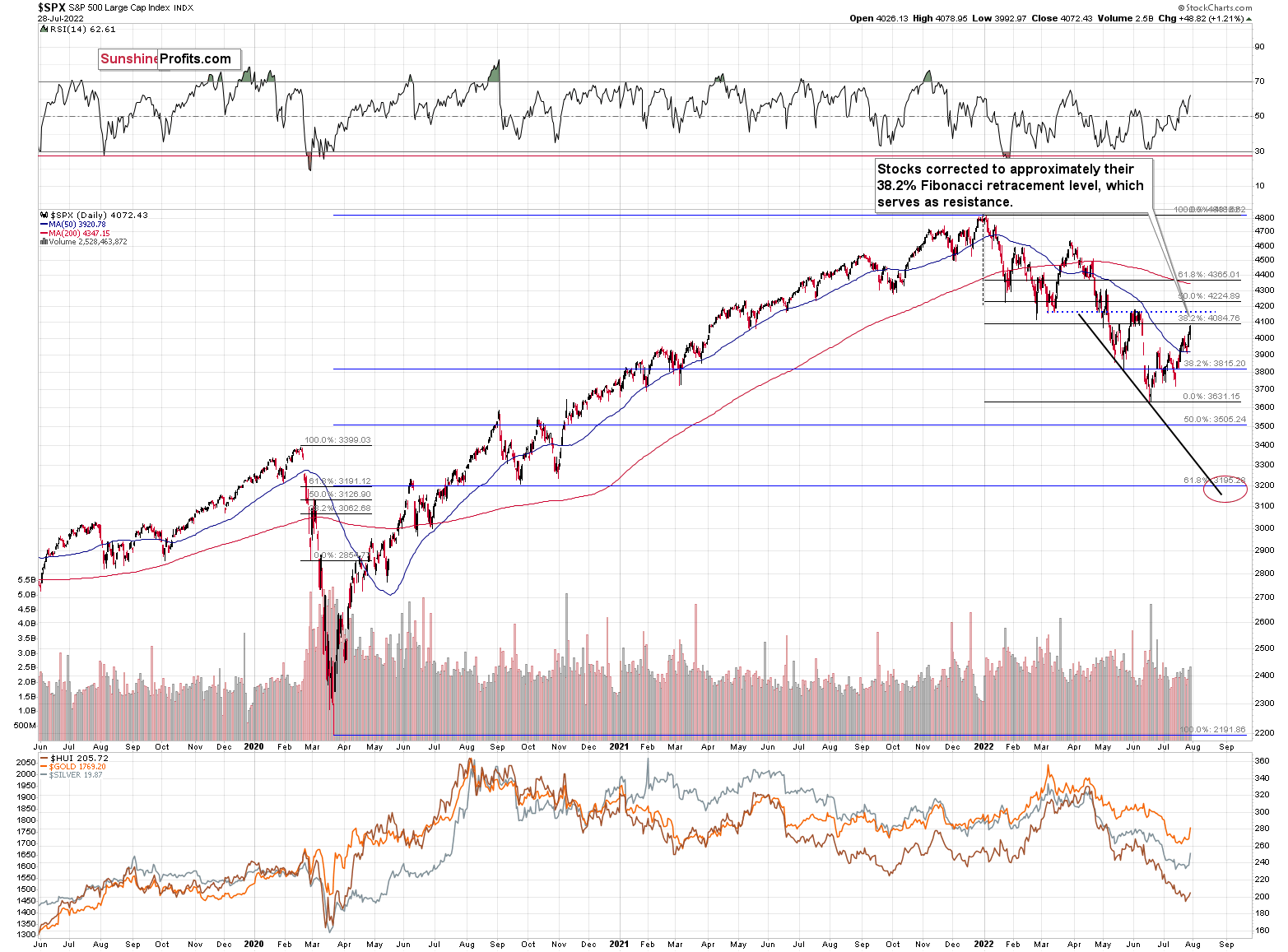

Stocks rallied recently, but since they corrected approximately 38.2% of their 2022 decline, they might now decline once again.

As I had indicated previously, interest rates are likely going up, which is a bearish factor for the stock market, and the recent rally was likely due to the market’s misinterpretation of the importance of Powell’s speech. The S&P 500 wanted to correct (based on emotional = technical reasons) and it used Powell’s seemingly dovish comments as an excuse to do so. However, what materially changed? Nothing. Interest rates are likely to be raised, as inflation remains the key political issue right now, and the markets are likely to respond by declining.

Most interestingly, though, such a decline would likely have a devastating effect on the prices of mining stocks (especially junior mining stocks) and silver. There might be some impact on gold, too.

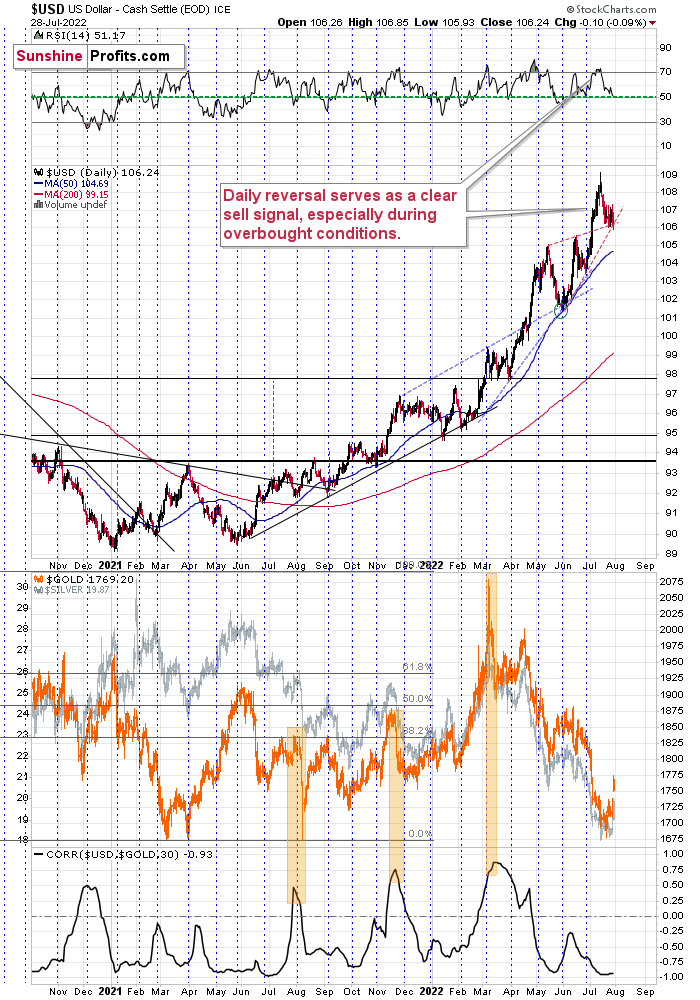

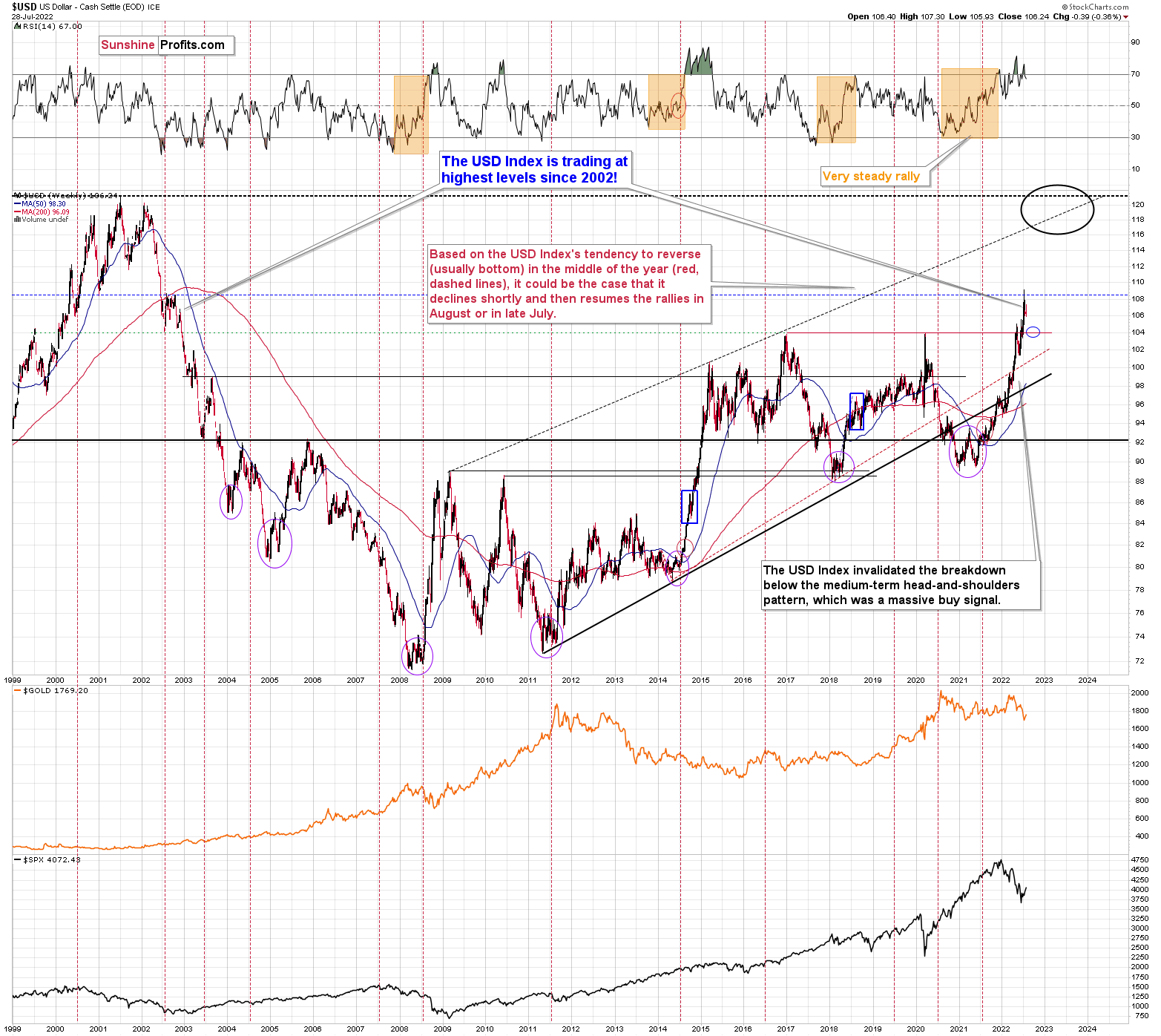

The above would also be in tune with an extra rally in the USD Index. After all, less competitive exports are not that favorable for the U.S. economy.

In the case of the USD Index, we saw a decline, but not yet a move below the nearby support lines.

Did we just see the bottom? Perhaps, but there’s much stronger support at about 105 and 104 – the previous long-term price extreme and the 50-day moving average, so it could be the case that the USD Index has either bottomed or that it will bottom after an additional brief decline.

A rally from here would be more in tune with the previous (May/June) bottom, when the USDX bottomed at the intersection of two previous support/resistance lines.

Also, let’s not forget that the turn of the month is just around the corner, and the USD Index tends to reverse its course at those times. Since the previous short-term move was to the downside, the implications are bullish.

It’s also the case that the USD Index tends to reverse (usually bottom) close to the middle of the year. This tendency also supports a scenario in which the USD Index starts another move higher shortly.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is either over or about to be over, and that the next big move lower is about to start.

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, it seems that the corrective upswing is over (or close to being over), which means that the powerful medium-term downtrend can now resume.

Yesterday, we closed yet another profitable trade in a row. This year’s profits are already enormous, but it seems likely to me that they will grow even more in the following weeks and months. Making money on corrections during powerful trends is a difficult feat, but you managed to do just that – congratulations!

Moreover, please note that it’s not only the profits on the long positions that are so great about this success – it’s also the ability to get back on the short side of the market at more favorable (higher) prices, thus increasing the likely profits from the current trade. Congratulations, once again!

Also, please note that I will be updating the targets for the leveraged ETFs as we move closer to them, as their prices will depend on the path prices take to reach their targets.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $20.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $29.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $12.32

SLV profit-take exit price: $11.32

ZSL profit-take exit price: $79.87

Gold futures downside profit-take exit price: $1,504

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $19.87

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $49.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief