Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Last week was quite rich in volatile price moves, and I commented on most of them in Thursday’s extensive analysis.

What happened on Friday (the USD Index’s decline) didn’t really change anything regarding the outlook. In fact, it actually confirmed it.

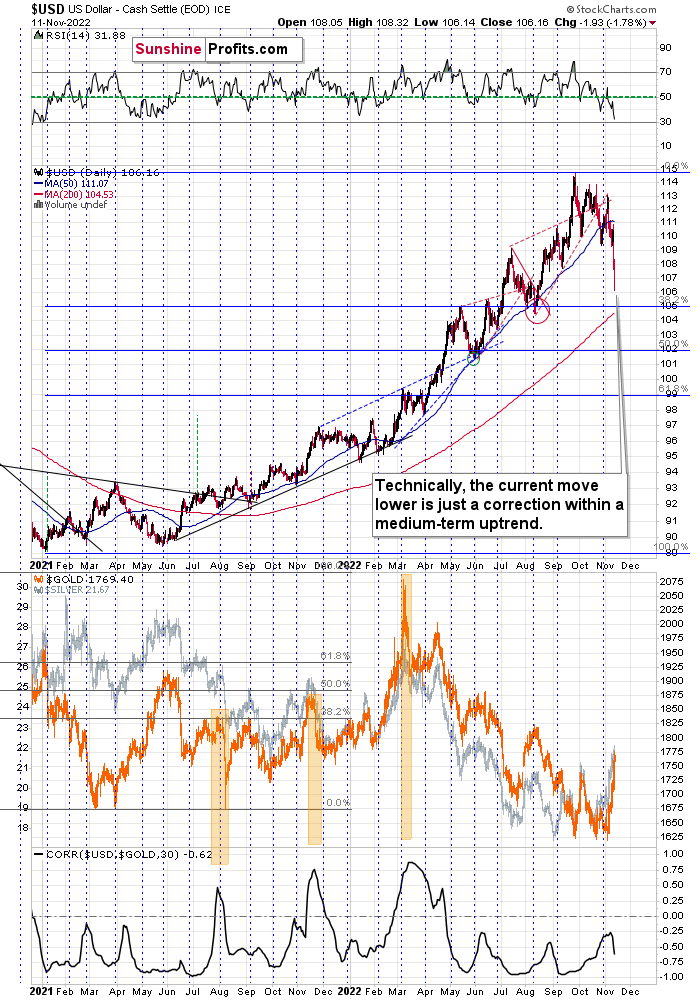

I received quite a few questions about the USDX, so let’s start today’s analysis with it.

From a short-term point of view, the decline was very sharp. It was near-vertical. The USD Index almost touched its August lows. What does it tell us about the USDX, and about gold?

As far as the USD Index itself is concerned, it actually tells us very little. This is because the correction was smaller than 38.2% of the preceding big upswing. As such, from the technical point of view, this correction is simply “normal.”

I realize that moves over 1+ index point per day seem to be far from normal, but please consider the context – “context is king” after all. The preceding rally was huge, and the USDX hasn’t corrected in a truly meaningful manner for many months.

The previous moves lower were really small compared to the size of the rally.

Now, does the size of the current corrective decline indicate that this short-term decline is something more than just a correction? Maybe the start of a new, powerful downtrend?

No.

The Fibonacci retracement levels help put the price moves into proper perspective. Generally, anything less than 38.2% or exactly 38.2% as the size of the correction means that it’s… Well, just a correction, and there’s little reason to think otherwise.

If the previous trend resumes after a correction that’s equal to or smaller than the 38.2% of the previous move, it suggests that the main trend is very strong.

At this moment, we don’t have a good reason to think that the medium-term uptrend in the USDX has been invalidated.

Yes, the current correction is bigger than the previous ones, but it doesn’t have particularly bearish implications.

Before we move to the analysis of the general stock market, I’d like to point out where the RSI is right now.

It’s slightly above 30. The last time it was this low was in mid-2021 – right at the major bottom (and at a major top in gold).

Speaking of gold, the above means that the bullish impact that the recent decline in the USD Index had on gold, is about to reverse, either right away or shortly. And as the medium-term trend in the USD Index remains up, the medium-term trend in the precious metals sector remains down. Consequently, the next big move in gold is likely to be to the downside, not to the upside.

This, in turn, means that now is a great time to enter short positions in the precious metals market (I prefer junior mining stocks as a proxy for this), not to exit them or to enter long positions. Of course, that’s just my opinion, but please consider the obvious fact that tops are formed when bullishness and emotionality reach zenith.

The number of not only emails that I just received but also messages about gold that I received from my non-work-related friends and colleagues is huge. This is usually a good indication that a top is in or at hand.

Additionally, there was one great “enough is enough” signal from the USD Index on Friday. Namely, while the USD Index declined once again, the precious metals market didn’t really move to new highs. I mean, from a practical point of view - a $0.09 rally in the GDXJ is not much different than nothing. The implications are bearish for the precious metals market, as the above indicates that the buying power is drying up or has already dried up.

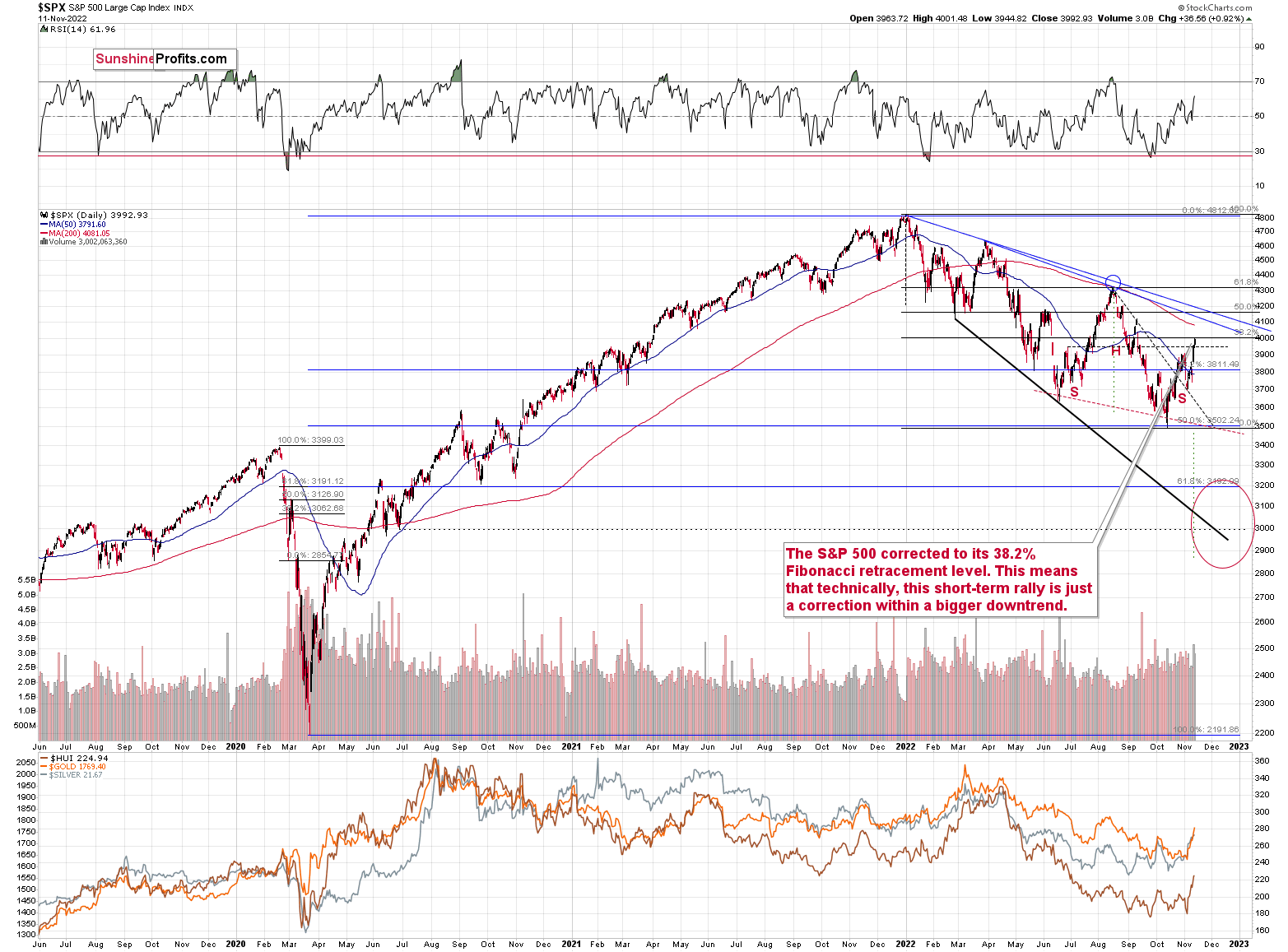

As the USD Index’s corrective downswing appears to be over or about to be over, the corrective upswing in stocks seems to be ending as well.

As you can see on the above chart, the S&P 500 moved to its 38.2% Fibonacci retracement and the psychologically important 4,000 level, and then it closed the week below it.

While it doesn’t guarantee it (there are no guarantees on any market), the above indicates that the corrective upswing might already be over.

This also makes sense from a fundamental point of view. The market rallied, hoping that the Fed would make a dovish U-turn as the job appeared to be done since the CPI declined a little. But those expectations actually mean that the Fed will have to raise rates higher and for longer! If people believe that interest rates will not rise but that inflation will fall, they will continue to spend, and businesses will increase hiring, etc. That’s inflationary. If the Fed is serious about fighting inflation, it must persuade people that it will not back down.. And they want to fight it, because that’s what the voters are concerned about the most.

As a result, we can expect various clarifications from Fed members that they will fight inflation in order to shift expectations in the opposite direction. That’s likely to push stocks and the precious metals market lower. Probably much lower.

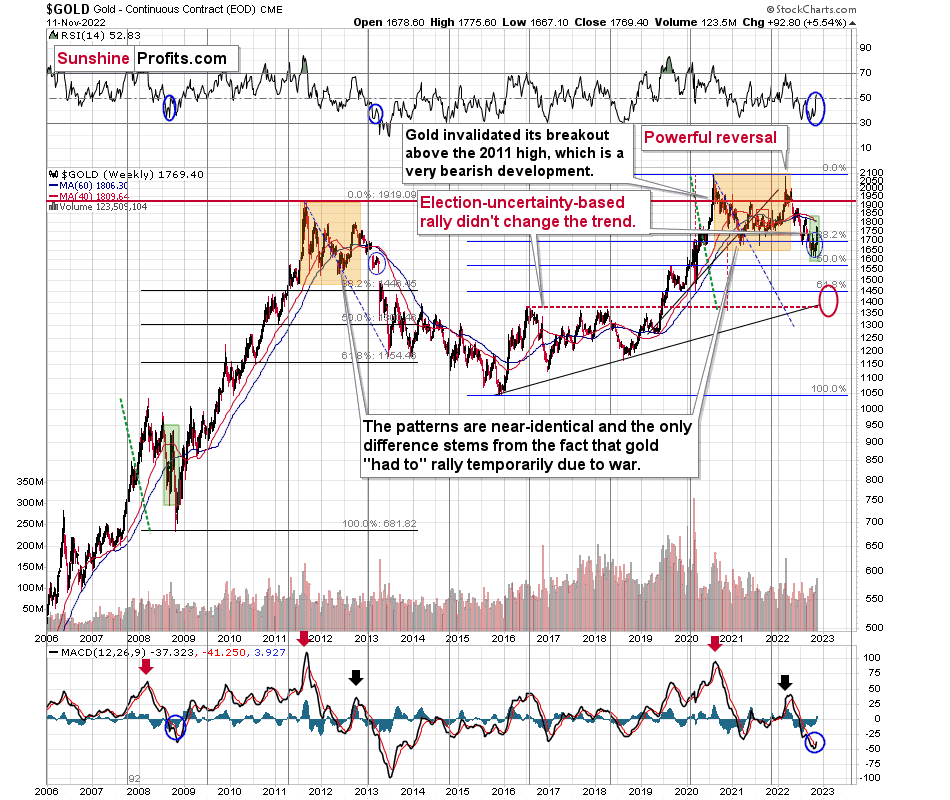

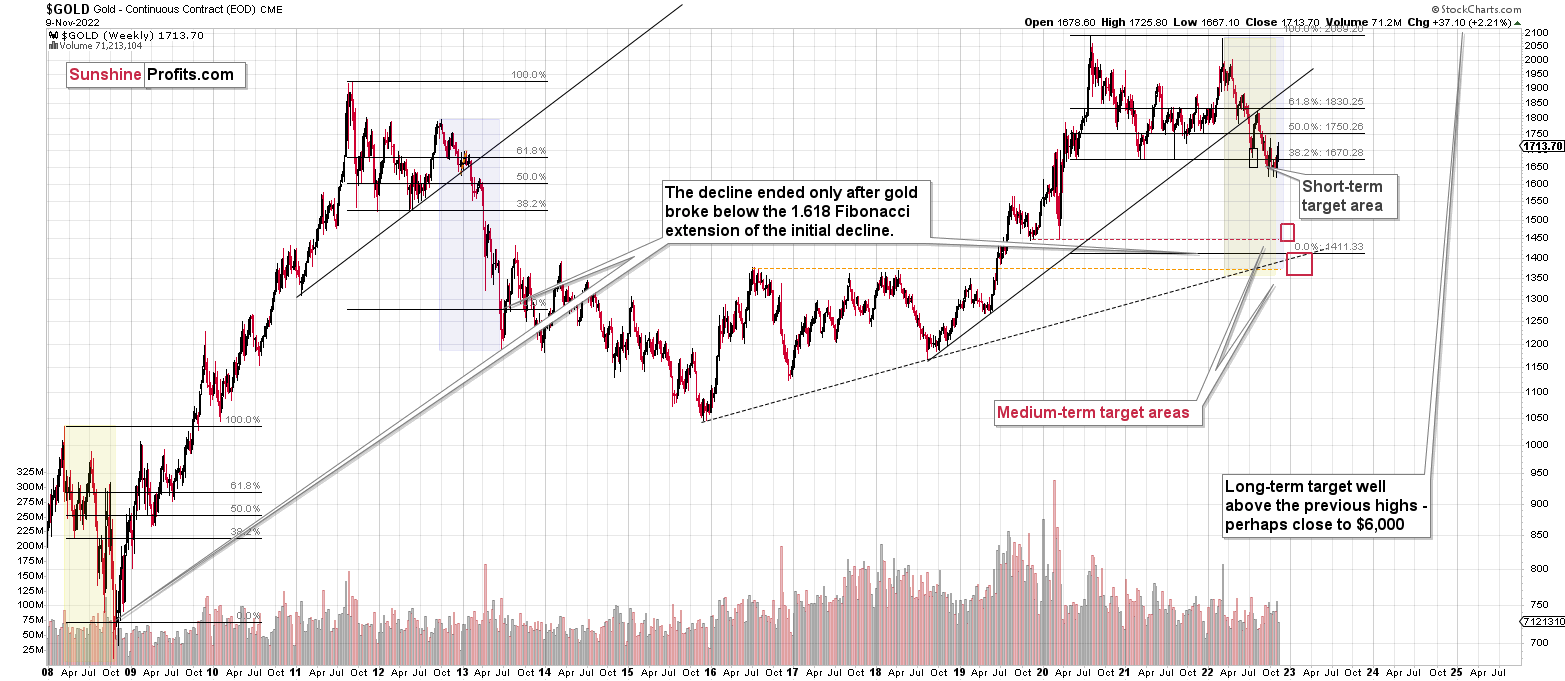

Looking at the gold market from a broader point of view reveals that what we saw recently is something between what we saw in 2013 and what we saw in 2008.

For many months, I've been writing that the situation is analogous to both of the preceding periods, and that the recent sharp corrective upswing fits this narrative rather than breaking it.

Yesterday’s weekly volume reading was the second biggest reading that we have seen this year. The record was formed in early March – at the yearly top. Does this sound bullish? No, it’s a bearish indication, as history tends to rhyme.

Returning to the 2008 comparison, please keep in mind that the sharp rally seen back then was much larger than what we saw this time. The moves higher in the RSI are similar, and I marked them with blue.

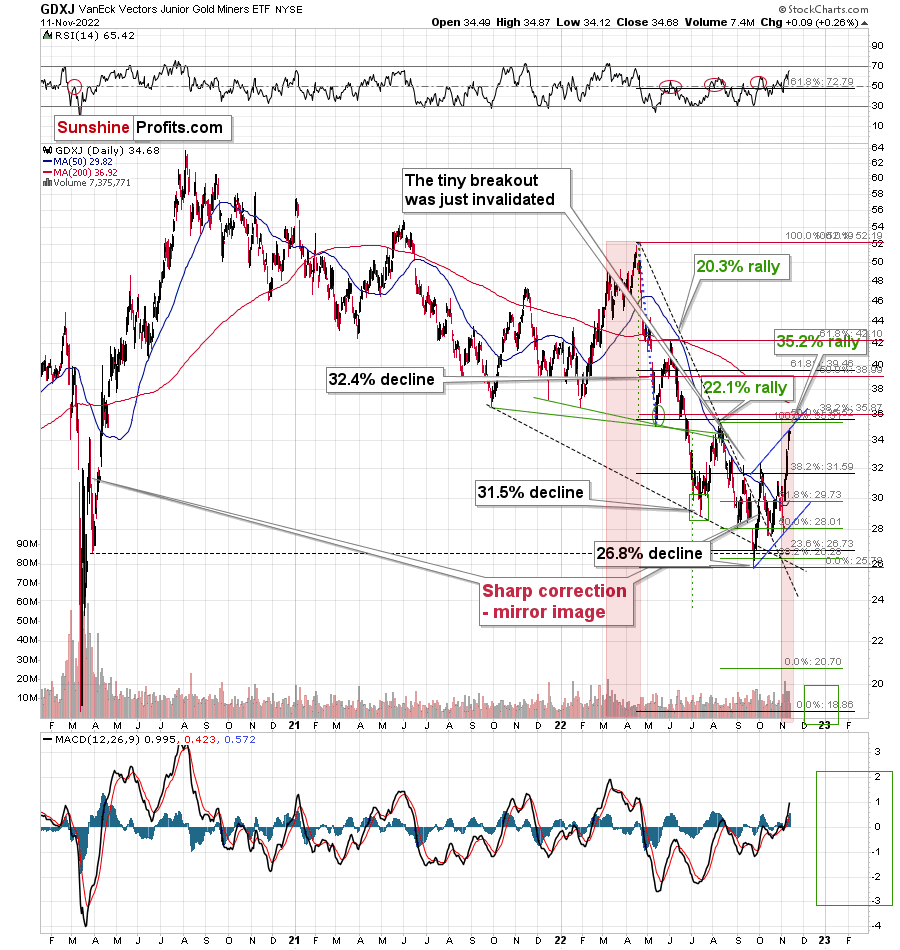

As far as the GDXJ is concerned, it has reached or almost reached its strong resistance levels.

The junior miners’ proxy moved to the upper border of the corrective trend channel (marked with blue), which serves as resistance.

The GDXJ is close to its August 2022 high.

The GDXJ is close to its 38.2% Fibonacci retracement based on this year’s decline. Consequently, everything that I wrote earlier about this retracement and the medium-term trend being intact, applies also to the GDXJ.

Moreover, my Thursday analysis remains up-to-date:

The junior mining stocks moved sharply higher recently, and this move took place on huge volume. The only similarly big volume that we saw recently was at the early-March top and the January top. As history tends to rhyme, this kind of massive attention that junior miners got serves as a bearish indication.

Interestingly, back in early 2022, the huge volume didn’t mark the final top, but we saw it a bit before the top. Then the GDXJ rallied some more, and that was when the true top materialized.

Also, I already wrote about the relative size of the recent upswing in gold and how it’s similar to what we saw in 2008, but we can say something similar about this analogy in mining stocks.

Back in 2008, the biggest corrective upswing (the 41.6% rally) was the thing that preceded the biggest part of the medium-term decline.

This time, the volatility is not as big, but the size of the corrective upswing (assuming that it started in September) that we just saw is also greater than what we’ve seen before. Consequently, it could be the case that what happened recently is what “had to” happen given the way history decided to rhyme. Please note that we can estimate what is likely to happen based on historical analogies, but we can never be 100% certain that a given analogy will work and some others won’t.

In this case, it seems that the correction happened, even though it didn’t “have to” happen based on many other techniques. Either way, the medium-term trend remains down, so the current corrective upswing is likely to be a “thing of the past of little meaning” sooner rather than later.

Speaking of analogies, I previously wrote that the current rally is a mirror image (it’s not a crystal-clear mirror, though) of the corrective decline that we saw in late-March 2020. As it turned out, due to the most recent part of the upswing, the size of both moves became even more aligned.

And yes, this means that another decline could take the GDXJ all the way down to its 2020 low, or very close to it.

Having said that, let’s take a look at the market from a more fundamental point of view.

A Matter of Time

With risk assets squeezing higher after the Consumer Price Index (CPI) release on Nov. 10, gold, silver and mining stocks benefited from the lower-than-expected print. Moreover, with the USD Index suffering and real yields declining, the crowd has flipped from depressed to euphoric in just over a month.

However, while the recent price action hasn’t really benefitted our short positions in the GDXJ, the medium-term technicals and fundamentals have not changed, and the bear market rally should culminate with new lows in the months ahead.

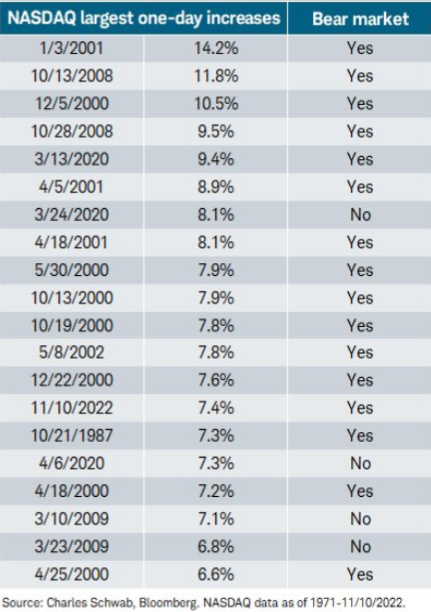

For example, the NASDAQ Composite squeezed 7.4% higher on Nov. 10, which was one of the 20 largest daily gains since 1971. Yet, 16 of those 20 rallies occurred in bear markets, and this iteration should be no different.

Please see below:

To explain, the table above depicts how large one-day moves are often commonplace during bear markets; and they often happen because short squeezes amplify the rallies as investors frantically unwind their bearish bets.

In addition, one of the tallies not labeled a bear market occurred on Apr. 6, 2020 (7.3% gain). This rally came when the Fed fired its liquidity bazooka to help offset the COVID-19 crisis, which is much different than the current fundamental environment.

Therefore, the data highlights how frenzied short-covering rallies are bearish, not bullish, and double-digit jumps occurred in 2000, 2001 and 2008, and were far from the index’s medium-term bottoms. As a result, risk assets should endure more downside once reality returns.

To that point, investors’ manic mood swings leave plenty of room for reversals in the near term.

Please see below:

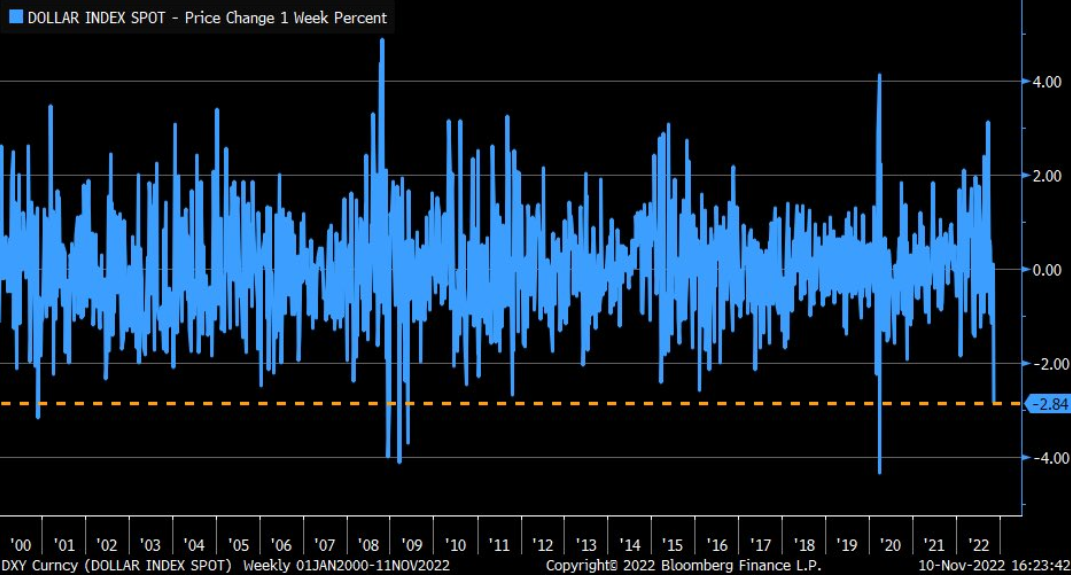

To explain, the blue line above tracks the one-week percentage change in the USD Index. If you analyze the right side of the chart, you can see that last week’s decline was the worst since March 2020, and preceding that, 2009.

Furthermore, if you focus your attention on the large drop in 2000/2001 and the cluster of drops in 2008/2009, you can see that when short squeezes occur during bear markets, risk assets soar and the USD Index heads in the opposite direction.

Yet, the sizeable one-week drop in 2000/2001 did not stop the USD Index from surging to a new high months later, and the cluster in 2008 culminated with the dollar basket making a new high before the S&P 500 bottomed in 2009 and a reversal of fortunes followed.

So, while the dollar dump and the risk rally may seem material, investors’ misguided optimism is nothing new. Also, they have a long history of buying hope and selling reality, and regret should confront the bulls when the fundamental problems prove more poignant over the medium term.

Likewise, we may not have to wait long for the sentiment to shift.

Please see below:

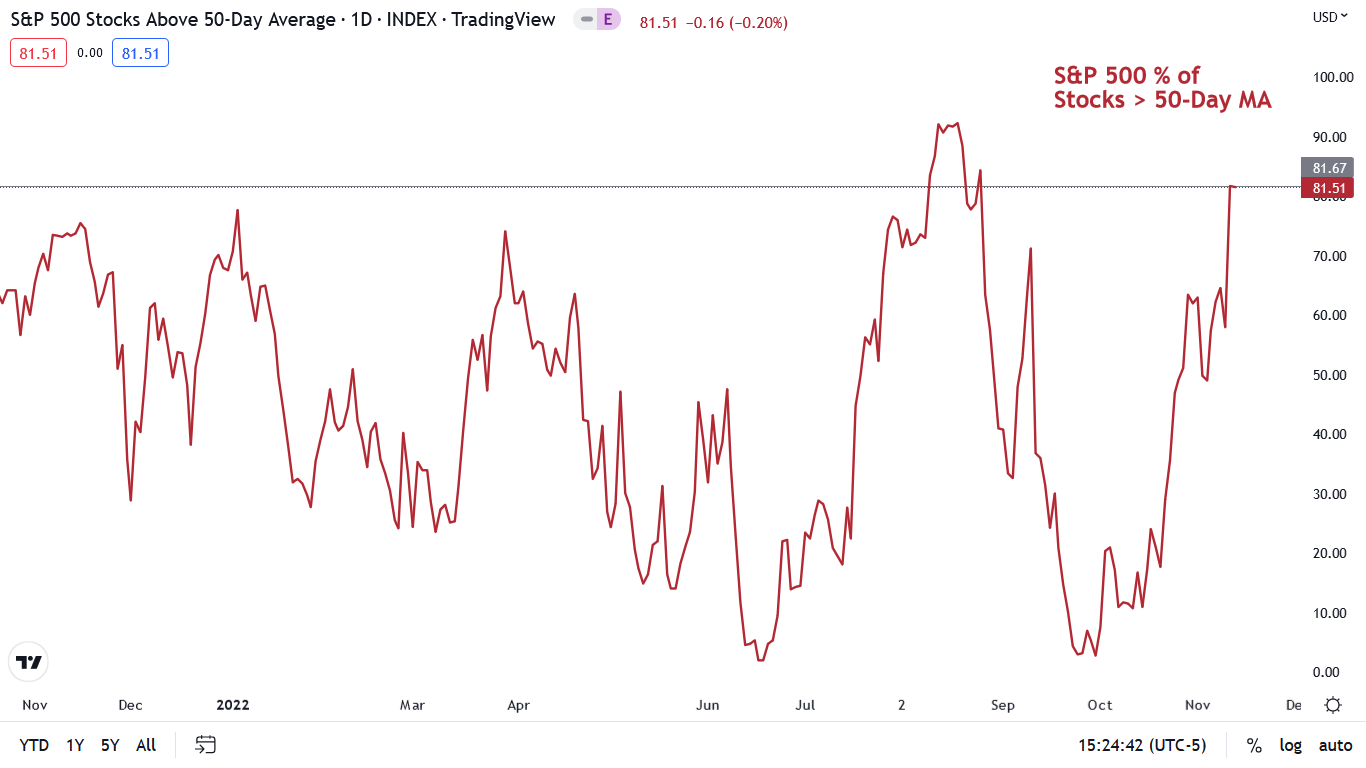

To explain, the red line above tracks the percentage of S&P 500 stocks trading above their 50-day moving average. For context, the metric is a contrarian indicator, as abnormally low readings often help spur bear market rallies (and vice versa).

However, if you analyze the right side of the chart, you can see that nearly 82% of S&P 500 constituents have risen above their 50-day MA, one of the highest readings in 2022. Moreover, the metric peaked near 92% during the August bear market rally, and it’s a long way down once sentiment turns.

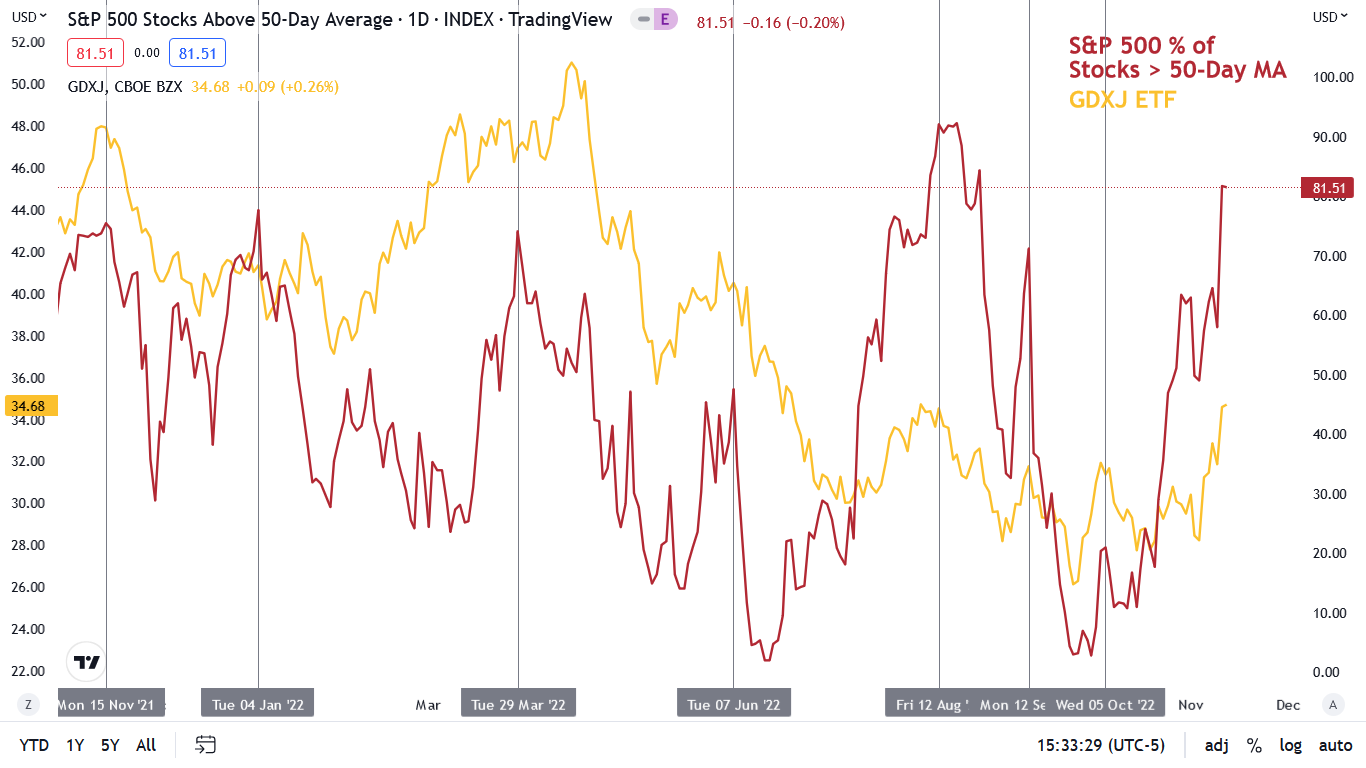

More importantly, the GDXJ ETF often suffers mightily after the S&P 500 metric peaks.

Please see below:

To explain, the red line above tracks the percentage of S&P 500 stocks trading above their 50-day moving average, while the gold line above tracks the GDXJ ETF. Outside of the short-term divergence in March/April 2022 – which occurred due to the Russia-Ukraine war – the GDXJ ETF often sinks when the percentage of S&P 500 constituents trading above their 50-day MA falls.

As such, with the S&P 500 metric poised to run out of gas sooner rather than later, a material reversal should confront the GDXJ ETF shortly.

Pervasive Inflation

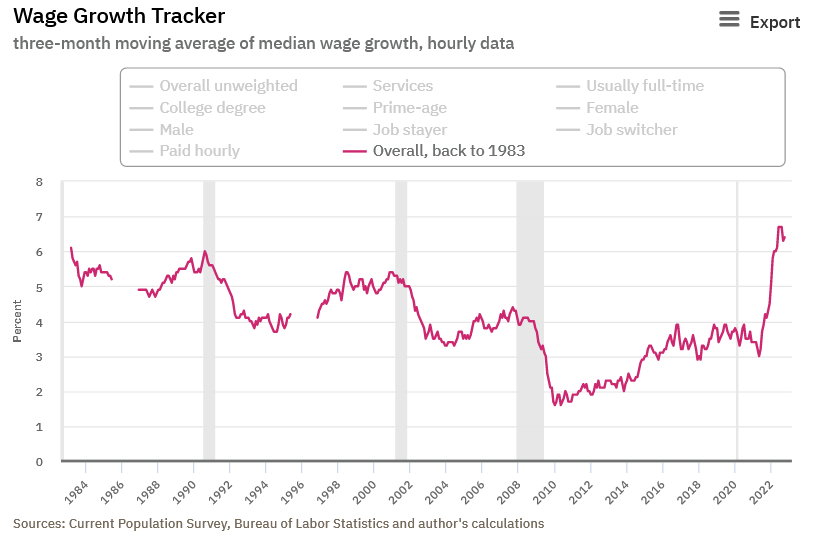

While the crowd buys into the false narrative that inflation will go quietly into the night, the fundamental realities are much different. For example, the Atlanta Fed updated its Wage Growth Tracker on Nov. 11; and after the metric declined from 6.7% (an all-time high) to 6.3% in September, mild progress was realized. However, with the metric increasing from 6.3% to 6.4% in October, I warned on numerous occasions that the Fed’s inflation fight will be one of attrition.

Therefore, while the consensus assumes a 2% CPI is on the horizon, disappointment should reign supreme when investors realize that major challenges lie ahead.

Please see below:

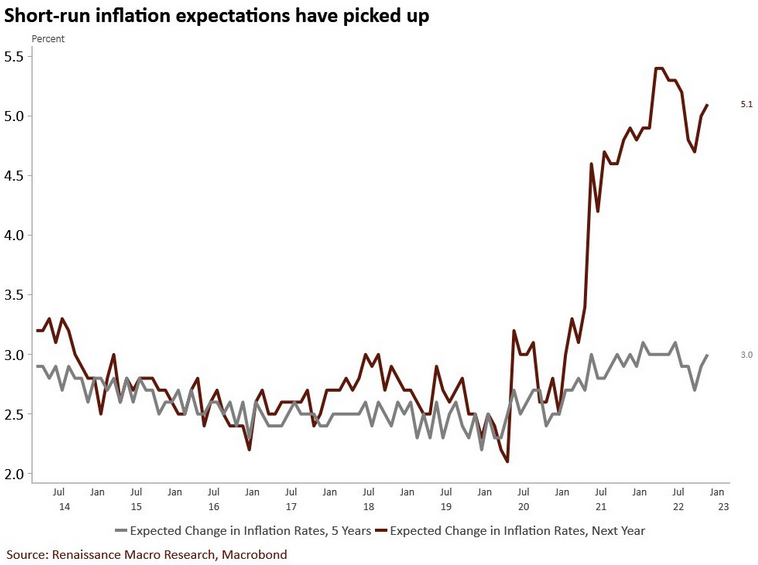

Likewise, the University of Michigan released its Consumer Sentiment Index (CSI) on Nov. 11; and with inflation expectations rising once again, the realities felt by Americans are much different than the narrative on Wall Street.

Please see below:

To explain, the brown line above tracks Americans’ 12-month inflation expectation, while the gray line above tracks their five-year forecast. If you analyze the right side of the chart, you can see that both metrics have risen recently, which highlights the stickiness of inflation psychology. So, while the crowd assumes the war is over, the reality is that the Fed has made little progress in solving the problem.

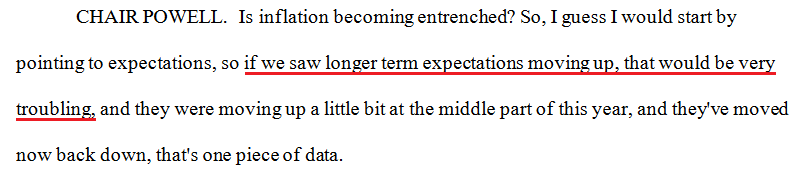

Furthermore, Fed Chairman Jerome Powell said during his press conference on Nov. 2:

“Shorter-term inflation expectations moved up between the last meeting and this meeting, and we don't think those are as indicative, but they may be important in the wage setting process. There's a school of thought that believes that. So that's very concerning….

“The thing we need to do from a risk management standpoint is to use our tools forcefully but thoughtfully, and get inflation under control, get it down to 2%, get it behind us. That's what we really need to do and what we're strongly committed to doing.”

Thus, while Powell said on Nov. 2 that the U.S. federal funds rate (FFR) would need to rise more than previously expected, ignoring the recent ascent of the gray line above (Americans’ five-year inflation expectation) should haunt the bulls in the months ahead.

Please see below:

Source: U.S. Fed

Source: U.S. Fed

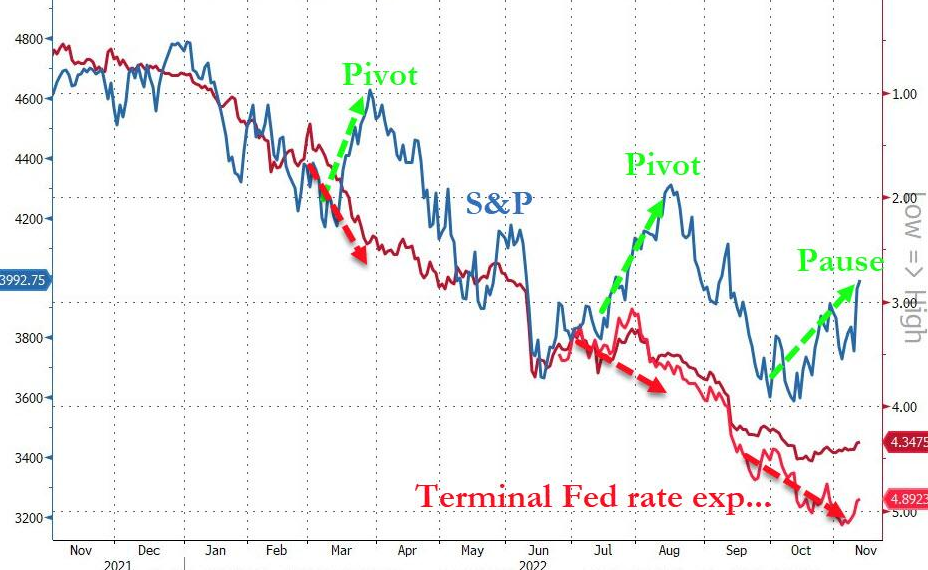

Finally, while the bulls pump the S&P 500 higher in an attempt to create their own reality, their prior failures are likely a warning sign of what’s to come.

Please see below:

Source: Bloomberg/ZeroHedge

Source: Bloomberg/ZeroHedge

To explain, the blue line above tracks the S&P 500, while the red line above tracks the inverted (down means up) peak FFR priced in by the futures market. As you can see, each time the S&P 500 runs away from the red line, reality re-emerges and the S&P 500 plunges.

As a result, the gap on the right side of the chart shows how despite the S&P 500’s optimism, rate hike expectations have only declined slightly. Therefore, don’t be surprised if a third bearish rendition occurs in the weeks ahead. And perhaps much, much sooner. In fact, we could see lower prices as soon as this week.

The Bottom Line

Risk assets are behaving the way they often do during bear market squeezes, and the USD Index’s plight follows the same playbook. However, with the countertrend moves often reversing sharply, the dot-com bubble and the global financial crisis (GFC) showed that sentiment can only uplift risk assets for so long. As such, while gold, silver and mining stocks’ recent rallies have been far from fun, they’re commonplace on the path to lower lows.

In conclusion, the PMs were mixed on Nov. 11, as silver ended the day in the red. Moreover, while the USD Index declined, the bond market was closed, so the U.S. 10-Year real yield was out of the equation. However, with both metrics poised to resume their bull markets in due time, the PMs should head in the opposite direction.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, while the precious metals sector moved higher last week, it seems that it’s just a part of a bigger – bearish – analogy to what we saw in 2008. I realize that volatile upswings generate a lot of emotions, but taking a calm, broad look at the markets shows that nothing really changed.

In fact, I would like to take this opportunity to congratulate you on your patience with this trade (and I’m grateful for your understanding that not every corrective upswing can be “caught” in trading terms). Many investors and traders panic, and get out of the market exactly at the wrong time, and your patience and self-discipline mean that you’re poised to make the most of what the market brings us this and next year.

Moving back to the market, it appears to be yet another time when the markets are incorrectly expecting the Fed to make a dovish U-turn, and based on this, the part of the 2008 decline where we saw the biggest corrective upswing materialized.

In my opinion, the current trading position is going to become profitable in the following weeks, and quite possibly in the following days. And while I can’t promise any kind of performance, I fully expect it to become very profitable before it’s over and it to prolong our 2022 winning streak.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $20.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $27.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $12.32

SLV profit-take exit price: $11.32

ZSL profit-take exit price: $74.87

Gold futures downside profit-take exit price: $1,504

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $18.47

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $46.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief