Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

The technical part of today’s analysis is going to be relatively short, as the PMs declined yesterday, and what I wrote in yesterday’s extensive Gold & Silver Trading Alert simply remains up-to-date.

Immediately after junior miners soared on Thursday, I wrote the following:

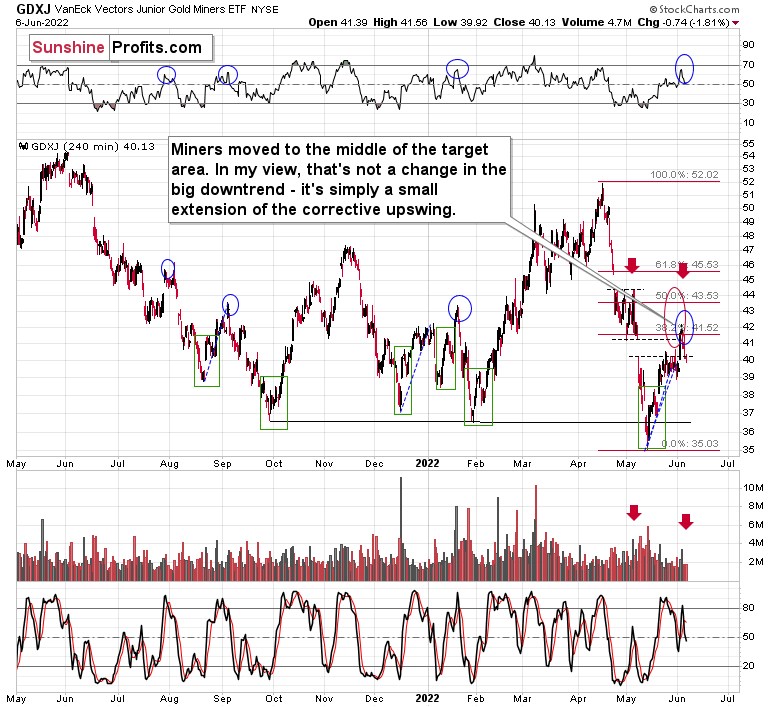

The GDXJ moved sharply higher after the session started, and at the moment of writing these words, it moved to the upper border of the previous, early-May price gap. Please note that it was my original target for the previous long positions, and it was just reached.

It doesn’t change the outlook here. When we took profits from the long positions and re-entered short ones, I wrote that we were doing so, not because it was clear that the top was in, but because the risk to reward ratio changed dramatically. And that was indeed the case. The fact that juniors rallied today doesn’t change it. In my view, it was a good decision to switch the positions then based on the data that we had at that time.

Anyway, the medium-term trend remains down, and it seems that we’ll see another – very powerful – downswing shortly.

We didn’t have to wait long for the market to agree with me. Let’s see what happened.

The GDXJ moved slightly above the lower and upper borders of the price gap and above the 38.2% Fibonacci retracement level. Then, we saw an invalidation of all the above-mentioned breakouts. Invalidations of breakouts are immediate sell signals, so the implications are, of course, bearish.

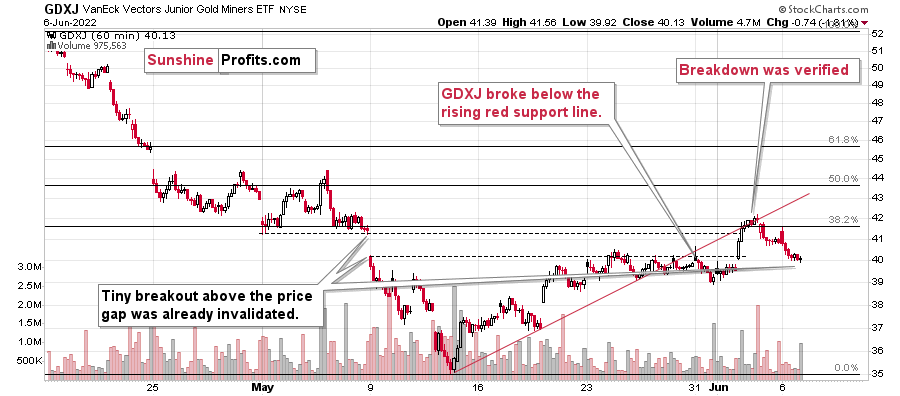

It’s even clearer on the 1-hour candlestick chart.

The above chart allows us to see that, in addition to the above, the GDXJ first broke below its rising red support line, and then it verified this breakdown – twice. The first verification was an immediate one at the end of May, and we just saw the second one a few days ago.

Yesterday’s close back below the lower border of the price gap confirms the bearish nature of the recent patterns.

Even though the price is slightly higher than it was at the end of May, based on what happened (the failed breakouts), the short-term outlook is even more bearish now than it was back then.

I’ve written this many times in the previous weeks, but it won’t hurt to clarify it once again. In my opinion (just an opinion, of course, I can’t guarantee any kind of performance), this is an epic shorting opportunity that will seem obvious to everyone several months from now. There are myriads of signs, but let’s state the obvious: gold was unable to rally despite the – literally – war in Europe. If that isn’t a screaming sell indication for the precious metals market, I don’t know what is. Still, at this time, very few people realize this. You do, though :)

Having said that, let’s take a look at the markets from a more fundamental angle.

Stuck in Quicksand

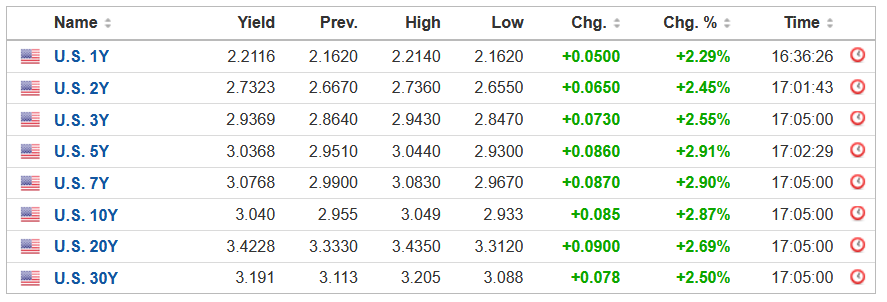

With anxious bulls unable to muster long-lasting rallies, the harsh realities of unanchored inflation and a hawkish Fed have kept sentiment in check. Moreover, with the U.S. 10-Year Treasury yield recapturing 3% on Jun. 6, the bond market isn’t helping the situation.

Please see below:

Source: Investing.com

Source: Investing.com

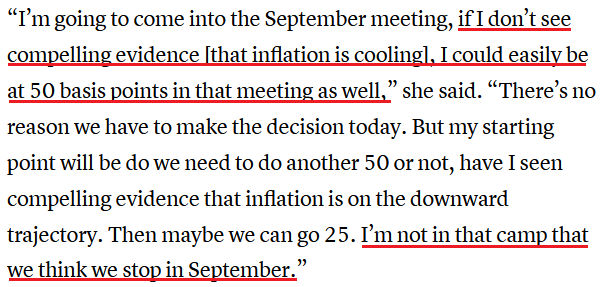

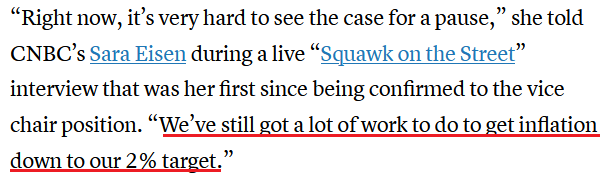

Likewise, with Fed officials warning of further interest rate hikes in the coming months, the economic strain should weigh heavily on the S&P 500 and the PMs. For example, Cleveland Fed President Loretta Mester said on Jun. 3: “It’s too soon to say that that’s going to change our outlook or my outlook on policy. The No. 1 problem in the economy remains very, very high inflation, well above acceptable levels, and that’s got to be our focus going forward (…).”

“I think the Fed has shown that we’re in the process of recalibrating our policy to get inflation back down to our 2% goal. That’s the job before us.”

As a result, while 50 basis point rate increases in June and July are likely done deals, Mester expects the hiking spree to continue in September.

Please see below:

Source: CNBC

Source: CNBC

In addition, Fed Vice Chair Lael Brainard mirrored that sentiment on Jun. 2. Speaking with CNBC, she said:

“We’re certainly going to do what is necessary to bring inflation back down. That’s our No. 1 challenge right now. We are starting from a position of strength. The economy has a lot of momentum.”

Therefore, as long as inflation remains uplifted, the Fed has no cause for pause:

Source: CNBC

Source: CNBC

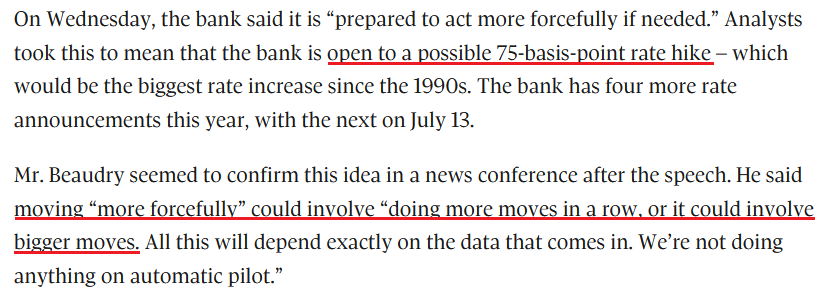

Furthermore, I’ve warned on numerous occasions that the Bank of Canada (BoC) is the hawkish canary in the coal mine. In a nutshell: due to the geographical proximity and the fact that 75% or more of Canadian exports are sent to the U.S., the two regions often have similar economic and monetary policy outcomes. Moreover, with the BoC hiking interest rates by another 50 basis points on Jun. 1, the feedback loop should continue.

For example, BoC Deputy Governor Paul Beaudry said on Jun. 2 that the central bank may need to raise its overnight lending rate above 3% to curb inflation.

“Price pressures are broadening and inflation is much higher than we expected and likely to go higher still before easing,” he said. “This raises the likelihood that we may need to raise the policy rate to the top end or above the neutral range to bring demand and supply into balance and keep inflation expectations well anchored.”

As a result, investors are unprepared for the policy measures needed to calm unanchored inflation.

Please see below:

Source: The Globe and Mail

Source: The Globe and Mail

Also noteworthy, Beaudry added:

“The longer inflation remains well above our target, the more likely it is to feed into inflation expectations, and the greater the risk that inflation becomes self-fulfilling. History shows that once high inflation is entrenched, bringing it back down without severely hampering the economy is hard. Preventing high inflation from becoming entrenched is much more desirable than trying to quash it once it has.”

For context, I’ve long warned that ignoring inflation would have dire long-term consequences for the U.S. economy and any region. Therefore, while the consensus wants central banks to turn dovish, Beaudry realizes that doing so is worse than pushing interest rates “above the neutral range.” I wrote on May 25:

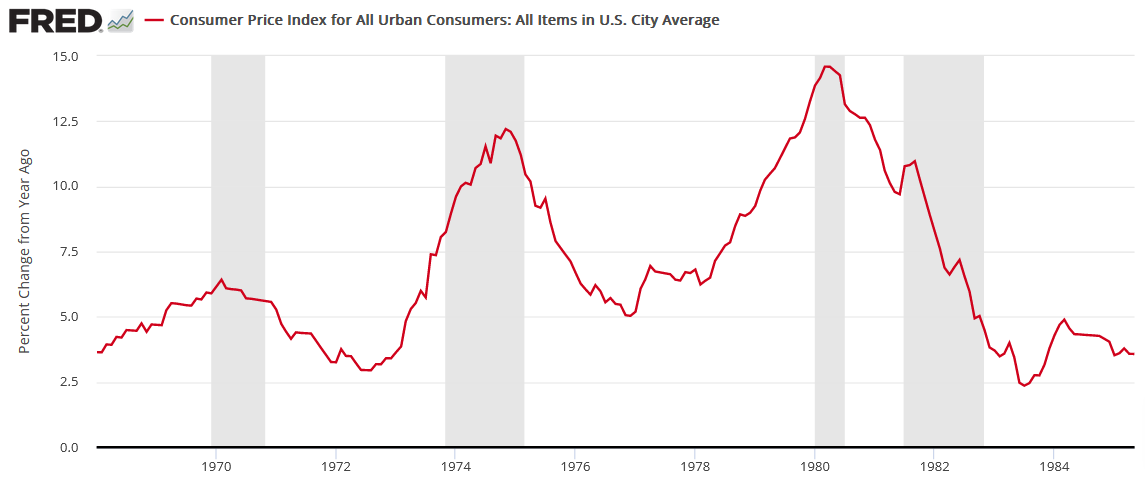

We’ve officially entered the monetary version of The Boy Who Cried Wolf. With Fed officials running to the rescue each time the financial markets show signs of stress, investors are programmed to ignore their hawkish threats. However, while these post-GFC pivots occurred with inflation perched near 2%, investors are so steadfast in their belief that they ignore the climactic consequences of unanchored inflation.

In a nutshell: consumers will eventually run out of money; and if the Fed lets inflation rage, a re-enactment of the 1970s is the worst-possible long-term outcome for Americans. Again, while the post-GFC crowd doesn’t care or doesn’t know history, unanchored inflation in the 1970s/1980s pushed the U.S. into recession four times over ~12 years (the vertical gray bars below). As a result, be careful what you wish for.

Thus, the Fed finds itself in a catch-22. Curbing inflation should lead to a recession, as nearly all bouts of unanchored inflation have ended in an economic downturn over the last ~70 years. Likewise, waiting for inflation to subside on its own would result in even more suffering.

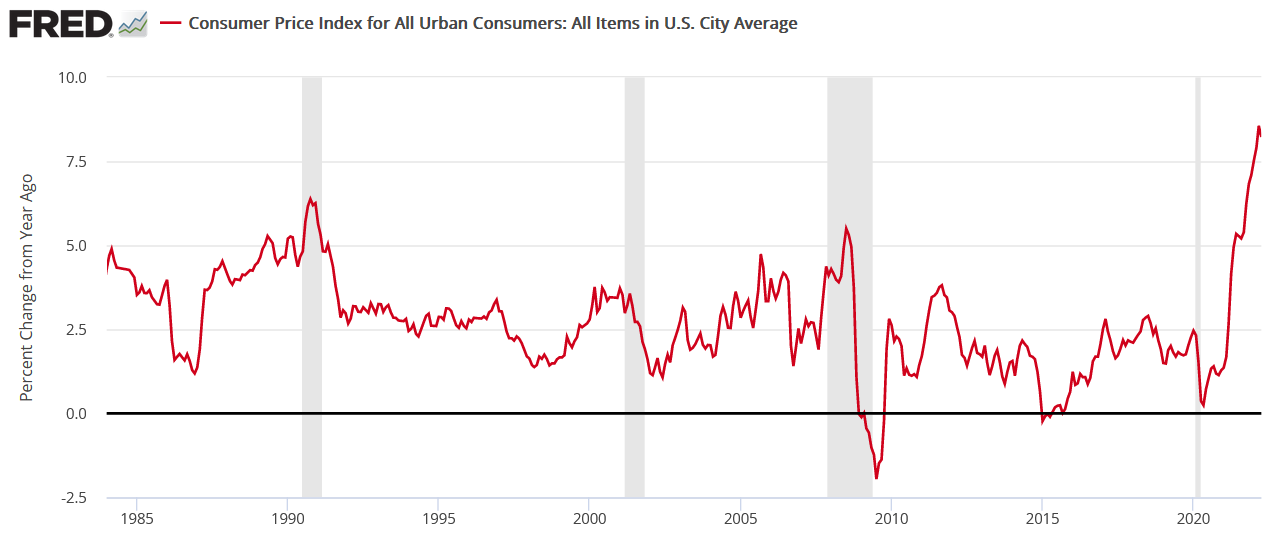

To explain, I noted above that unanchored inflation in the 1970s/1980s pushed the U.S. into recession four times over ~12 years. As such, that’s roughly one recession every three years. Conversely, stable inflation often coincides with a recession roughly every eight to 10 years.

Moreover, the chart below highlights how all of the post-1970/1980 recessions coincided with rising inflation (except for COVID-19). Thus, with the current inflation rate much higher than any of those periods and more similar to the 1970/1980s, the Fed and the BoC should know that the smaller and less frequent recessions below are preferable to the larger and more frequent recessions above. As a result, the post-GFC crowd suffers from recency bias and fails to understand these economic challenges.

To that point, I’ve been bullish on the U.S. economy for some time, and the region remains in a relatively healthy position, all things considered. However, I noted on May 5 that the present situation holds no bearing on the future and that the recession roadmap is always drawn from economic optimism. I wrote:

It’s important to distinguish between where we are now and where we are likely headed. Regarding the latter, the “soft landing” crowd will likely be the 2023 version of the “transitory” crowd from 2021/2022. Regarding the former, the U.S. economy remains on solid footing RIGHT NOW. However, the dynamic only adds further fuel to the hawkish fire.

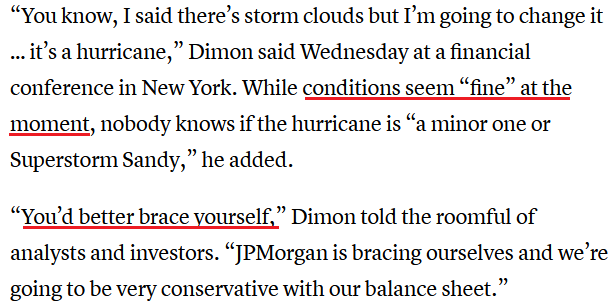

Furthermore, JPMorgan CEO Jamie Dimon summed it up perfectly on Jun. 1. He said:

“Right now, it’s kind of sunny, things are doing fine, everyone thinks the Fed can handle this. [But] that hurricane is right out there, down the road, coming our way (…).”

“We’ve never had QT like this, so you’re looking at something you could be writing history books on for 50 years.”

As a result, the CEO of the largest U.S. bank understands the economic damage that higher interest rates produce.

Please see below:

Source: CNBC

Source: CNBC

In addition, the “soft landing” crowd doesn’t realize that their bullishness is sealing the Fed’s fate. For example, the S&P 500 has rallied in recent weeks. However, the optimism only exacerbates the central bank’s inflation problem. To explain, I wrote on May 31:

The only bullish outcome is if economically-sensitive commodities collapse on their own. Then, input inflation would subside and eventually cool output inflation, and the Fed could turn dovish.

However, the central bank has been awaiting this outcome for two years. Thus, my comments from Apr. 6 remain critical. If investors continue to bid up stock prices, the follow-through from commodities will only intensify the pricing pressures in the coming months. Therefore, investors are flying blind once again.

To that point, the S&P Goldman Sachs Commodity Index (S&P GSCI) also participated in the recent run-up. For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products and two precious metals. However, energy accounts for roughly 54% of the index’s movement.

Moreover, with the index gunning for its 2022 Russia-Ukraine war highs, the merry-go-round of input/output inflation is easy to see by those paying attention.

Finally, the Dallas Fed released its Texas Service Sector Outlook Survey on Jun. 1. The report stated:

“Price pressures remained near record highs in May, while wage growth accelerated slightly. The selling prices index softened one point to 32.6, with 36 percent of respondents noting monthly price increases, while the input prices index was unchanged at 53.5. The wages and benefits index added two points to rise to 35.0, only slightly off a record 37.4 reading in January 2022.”

The bottom line? The bulls are stuck in quicksand, and the more they struggle, the deeper they sink. However, they still don’t realize it. When economic optimism buoys stocks, it supports higher prices for cyclical commodities. Then, month-over-month (MoM) inflation rises, and the Fed needs to up the hawkish ante. As a result, the gambit should end in a hard landing; it’s simply a matter of when.

In conclusion, the PMs were mixed on Jun. 6, as silver ended the day in the green. However, the medium-term outlook is extremely treacherous, as investors underestimate the ferocity of inflation. As such, more downside should confront the S&P 500 and the PMs as the Fed’s liquidity drain unfolds.

Overview of the Upcoming Part of the Decline

- It seems to me that the short-term rally in the precious metals market is either over or very close to being over. It’s so close to being over that I think it’s already a good idea to be shorting junior mining stocks.

- We’re likely to (if not immediately, then soon) see another big slide, perhaps close to the 2021 lows ($1,650 - $1,700).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

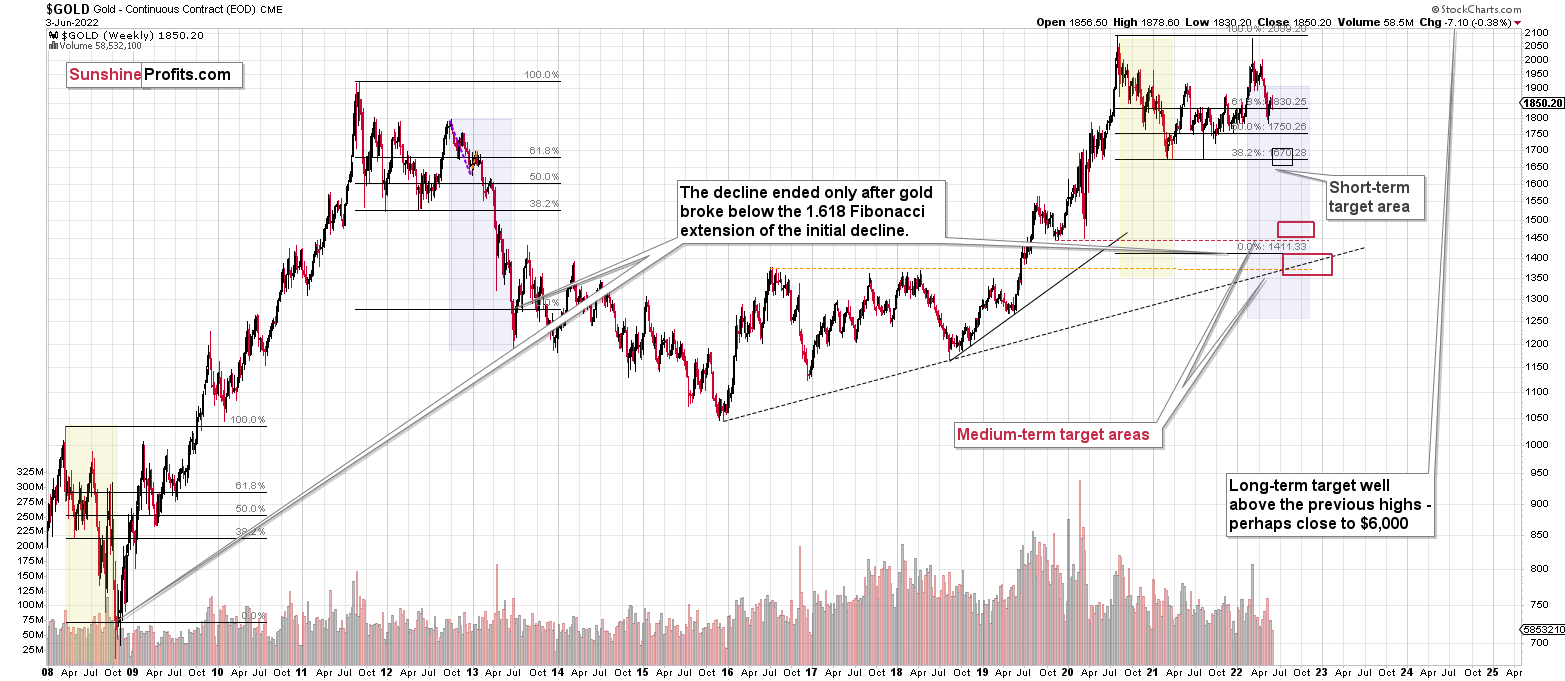

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, it seems to me that the short-term rally in the precious metals market is either over or close to being over. In fact, it’s so close to being over that I think it’s already a good idea to be shorting junior mining stocks.

I previously wrote that the profits from the previous long position (congratulations once again) were likely to further enhance the profits on this huge decline, and that’s exactly what happened. The profit potential with regard to the upcoming gargantuan decline remains huge.

As investors are starting to wake up to reality, the precious metals sector (particularly junior mining stocks) is declining sharply. Here are the key aspects of the reality that market participants have ignored:

- rising real interest rates,

- rising USD Index values.

Both of the aforementioned are the two most important fundamental drivers of the gold price. Since neither the USD Index nor real interest rates are likely to stop rising anytime soon (especially now that inflation has become highly political), the gold price is likely to fall sooner or later. Given the analogy to 2012 in gold, silver, and mining stocks, “sooner” is the more likely outcome.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

As always, we'll keep you – our subscribers – informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $27.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $19.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $17.22

SLV profit-take exit price: $16.22

ZSL profit-take exit price: $41.87

Gold futures downside profit-take exit price: $1,706

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $11.87

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $31.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief