Gold performed relatively weak last month, confirming the last Market Overview’s thesis that the role of geopolitical concerns on the gold price is often overstated. The recent ceasefire in the Ukrainian-Russian conflict might have contributed to the decline in the price of gold, but the expectations that the Federal Reserve will raise interest rates seemed to play much bigger role. Gold reached its lowest since January (around $1220 an ounce), just after the release of the Federal Reserve Bank of San Francisco report. The report – interpreted as a signal that investors’ interest rates expectations are lower than those of the Fed – indicated that investors may underestimate the speed at which the Fed might raise rates, evidenced by low volatility.

The relationship between interest rates and the gold price has been discussed in one of the Market Overviews, however its significance definitely needs much more attention. Interest rates are extremely important and have far-reaching effects for virtually all markets, including precious metals markets. To some extent their impact on gold may be even greater because, unlike other commodities, this metal is stored and not consumed in the traditional sense. Hence the impact of some basic demand and supply factors (like new flows of mined metal) is less relevant compared to other commodities, e.g. copper. Gold is more like a store of real wealth and a competitor for printed currencies. Thus, a thorough analysis of the relationship between interest rates and gold is necessary for understanding lat movements in the price of the yellow metal.

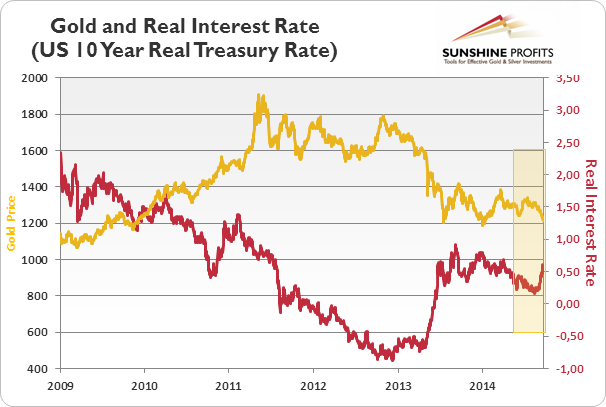

Indeed, it seems that recent declines in gold prices in August and September were caused by the changes in the real interest rates, and not by a stronger US dollar or the belief in interest rates hikes soon. For example, the 5-Year Real Interest Rate rose from -0.21% in August 1 to 0.08% by September 12, while the 10-Year Real Interest Rate rose from 0.22% to 0.49% in that period.

Graph: Gold (yellow line, left scale) and Real Interest Rate (US 10 Year Real Treasury Rate, red line, right scale) from 2009 to 2014

However, positive signals from the US economy (high level of manufacturing PMI) and expectations that the Fed will raise the nominal interest rates (especially compared to the lowering interest rates by the European Central Bank) could cause a rise in the medium and long-term real interest rates and appreciation of the US dollar.

All this is not good news for the gold market. If real interest rates stay positive and rise, and investors believe that those changes will be reasonably stable, the price of gold is at stake, at least for a while. However, a new dollar bull and gold bear is less certain until we see sustained, really healthy real rates.

What are ‘healthy” real rates after all? There is no clear-cut answer; nevertheless history can provide some guidance. Gold bull in the 1970s ended when real interest rates were radically raised to 6%. Given the CPI at 2%, the nominal interest rates should be raised to around 8%, i.e. levels unthinkable in the modern debt-based inflationary and low interest rates world. Real estate and equity investors as well as bondholders could not survive even half so radical a move. This is because the bond prices and interest rates are inversely related to each other. Therefore, although higher real interest rates encourage new investments, they would be devastating for the current bond-holders (this is called a principal risk). This means that Fed faces a choice: keep extremely low interest rates, risking the rise of inflationary expectations, negative real interest rates and a declining US dollar or hike the federal funds rate and risk a collapse of the US equity, real estate and bond markets. You would not have believed it, but since a courageous Paul Volcker’s presidency Fed always chose lowering the interest rate to support the equity or real estate markets. Bernanke chose to reinflate the real estate bubble, just like Greenspan did after the stock bubble.

Given that Yellen is considered as the most dovish Fed’s chief of the three, investors should not expect a sudden hike of the interest rates. We do not claim that the USA will necessarily follow the Japanese scenario of 19 years of extremely low interest rates; however it seems very likely that gold will still stay in the game for quite a long time. If you’re interested in learning more about the gold story - we focus on the macroeconomics and fundamental side in our monthly Market Overview reports and we provide Gold & Silver Trading Alerts for traders interested more in the short-term prospects. In order to start receiving free articles based on both publications, please sign up today for our gold mailing list. It's free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Market Overview Editor